The Exchange

Auto Added by WPeMatico

Auto Added by WPeMatico

Last year, a number of startups building OKR-focused software raised lots of venture capital, drawing TechCrunch’s attention.

Why is everyone making software that measures objectives and key results? we wondered with tongue in cheek. After all, how big could the OKR software market really be?

It’s a subniche of corporate planning tools! In a world where every company already pays for Google or Microsoft’s productivity suite, and some big software companies offer similar planning support, how substantial could demand prove for pure-play OKR startups?

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Pretty substantial, we’re finding out. After OKR-focused Gtmhub announced its $30 million Series B the other day, The Exchange reached out to a number of OKR-focused startups we’ve previously covered and asked about their 2020 growth.

Gtmhub had released new growth metrics along with its funding news, plus we had historical growth data from some other players in the space. So let’s peek at new and historical numbers from Gthmhub, Perdoo, WorkBoard, Ally.io, Koan and WeekDone.

Gtmhub had released new growth metrics along with its funding news, plus we had historical growth data from some other players in the space. So let’s peek at new and historical numbers from Gthmhub, Perdoo, WorkBoard, Ally.io, Koan and WeekDone.

A startup growing 400% in a year from a $50,000 ARR base is not impressive. It would be much more impressive to grow 200% from $1 million ARR, or 150% from $5 million.

So, percentage growth is only so good, as metrics go. But it’s also one that private companies are more likely to share than hard numbers, as the market has taught startups that sharing real data is akin to drowning themselves. Alas.

As we view the following, bear in mind that a simply higher percentage growth number does not indicate that a company added more net ARR than another; it could be growing faster from a smaller base. And some companies in the mix did not share ARR growth, but instead disclosed other bits of data. We got what we could.

Powered by WPeMatico

And we’re off to the races!

Last night, Affirm priced its IPO above its raised range at $49 per share, a sign that the public markets remain hungry for new listings. Provided that Affirm today trades similarly to how it priced, we could be looking at a 2021 IPO market that resembles last year’s heated results.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

That’s good news for a host of companies looking to follow in the financial technology unicorn’s footsteps.

Poshmark prices tonight and trades tomorrow. With Qualtrics in the wings along with Coinbase, Roblox set to direct list, and Bumble said to file as well, we’re heading into another busy IPO quarter. Affirm’s first-day trading results will therefore hold extra importance, even if its pricing augurs well for IPOs more generally.

Affirm first targeted $33 to $38 per share before raising its range to $41 to $44 per share. Pricing at $49 is a victory. Briefly, why, and then a thought about what’s next for the IPO market.

Affirm first targeted $33 to $38 per share before raising its range to $41 to $44 per share. Pricing at $49 is a victory. Briefly, why, and then a thought about what’s next for the IPO market.

What does Affirm sell? First, per its S-1 filings, it charges merchants a fee to “convert a sale and power a payment.” That sounds like software revenues, albeit not in the recurring manner of a SaaS company.

Second, Affirm earns from “interest income [from] the simple interest loans that we purchase from our originating bank partners.” And, it offers virtual cards to consumers via its app, allowing it to generate interchange revenues.

We care about all of that as it’s important to realize that Affirm is not a software company in the context that we usually think about them, namely software as a service, or SaaS.

This matters when we consider how the market values Affirm; the more richly Affirm is valued in revenue-multiple terms by its new, $49 per-share IPO price, the more bullish we can presume the IPO market is.

What are Affirm’s gross margins? A great question, and one that is surprisingly hard to answer. If you read its final S-1 filing, you’ll find that all its chatter concerning “contribution profit” has been removed. This is a shame to some degree as contribution profit — and margin — were Affirm’s closest shared cognate to gross margin.

Powered by WPeMatico

The new year is off to a busy IPO start. As The Exchange reported a few weeks ago, investors anticipate a busy Q1 IPO cycle, followed by a slower Q2 and a busy Q3 and Q4.

With Affirm releasing an initial IPO price range last night and Poshmark repeating the feat this morning, private-market investor expectations are holding up thus far.

Secondhand fashion marketplace Poshmark anticipates its IPO could price between $35 and $39 per share. Using its simple share count, the former startup could be worth nearly $3 billion. So, we’ve seen two multiunicorns set early pricing terms this week. That’s comfortably busy.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

As we did with Affirm, we’ll dig into Poshmark’s new pricing interval, calculate valuations for the company using both simple and fully diluted share counts, and figure out how they compare to its most-recent financial results and final private valuation. For the last bit, we’ll pull from PitchBook data and the S-1/A filing itself.

But for those of you in a hurry, the short gist is that for Mayfield, GGV, Menlo Ventures, Inventus Capital and Temasek, the company’s first pricing estimate looks like a win.

If you want to read our first dig into the company’s IPO filing that is more focused on performance than pricing, head here. Let’s go!

Poshmark’s $35 to $39 per-share IPO price interval could change, but even if it fails to rise, the company’s implied valuation is a dramatic step up from prior rounds.

For example, the company’s S-1 filings note that during its 2017 venture round — the last that it raised per the IPO filing and PitchBook data — Poshmark sold shares at $8.37 per share. That’s a fraction of the price that the company now expects public-market investors to pay.

As with Affirm, let’s calculate Poshmark’s valuation using both simple and fully diluted share counts. The latter takes into account shares that have been earned, but not yet exercised or converted.

Here’s the company’s valuation range using a simple share count, inclusive of its underwriters’ option to purchase 990,000 shares at its IPO price:

If we expand the company’s share count to include vested options and RSUs, the numbers go up. Again, the following math is inclusive of the underwriters’ option:1

So, are those good numbers? Yes.

Powered by WPeMatico

Welcome to 2021, a year that could extend 2020’s startup market disruptions and excesses — or change patterns that previously performed well for early-stage tech companies and their investors.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

As we turn the page, I have a number of questions worth raising as we muck into 2021.

Each relates to a 2020 change that is expected to persist, by either the general market or those bullish on startups. I want to know what would need to change to shake up what became the new normal last year. After all, it’s precisely when it feels like nothing could shake up a downturn (or a boom) that things often do.

Today, let’s discuss seed deals, venture investing cadence, the resulting valuation pressures from rapid-fire bets, current IPO expectations and what happens to software sales when remote work begins to fade.

Today, let’s discuss seed deals, venture investing cadence, the resulting valuation pressures from rapid-fire bets, current IPO expectations and what happens to software sales when remote work begins to fade.

As 2020 came to a close, Natasha Mascarenhas and I reported on seed investing’s strong year and its especially strong second half. How long can that pace keep up?

Nearly all our questions today deal with the endurance of certain conditions, namely: how long the market can keep parts of startup land red-hot.

When it comes to seed deal-making, Q1 and Q2 2020 saw similar levels of investment in the United States. But Q3 proved explosive, with money invested into domestic seed deals rising from around $1.5 to $1.6 billion during the first two quarters to $2.2 billion in the July-September period.

Q4 numbers are yet to fully come in, but it’s clear that private investors were incredibly bullish on early-stage startups in the second half of 2020. How long can that keep up? I think the answer is for a while yet, as investors have shown scant enthusiasm for slowing down their dealmaking cadence.

While cadence remains hot generally, seed deals should stay heated as the number of investors who are willing to invest early has increased.

Which brings us to our second question:

A theme that cropped up in the second half of 2020 was the pace at which investors were conducting venture capital deals. This was for a few reasons. To start, venture capitalists have raised larger funds in recent years, meaning that they need larger returns to make the math work out. This led to many investors putting money to work in younger and younger companies, hoping to get in early on a big win. That setup led to more deal competition and faster deal-making.

How? Two things. Investors who were already on a startup’s cap table — already part-owners, in other words — led preemptive rounds, in part to get ahead of other investors who might want to poach the succeeding deal. Other investors, knowing this, seemed to do the same math and move even faster, and earlier, to get around the defense.

So how long can the trend keep up? Given that many big VC firms raised in 2020, many startups picked up some tailwinds from the COVID-19 economy and exits have been strong, forever? Until something stops things? Think of it as Newton’s First Law of startup investing.

What could be the sudden impact to shake up the current set of conditions boosting the pace at which seed and later deals occur? An asteroid strike is probably too extreme, but inertia is one hell of a drug and markets love to stay happy.

Moving along, all the competition to get money to work in hot startups now has had another effect than the mere speed of deal-making; it has also pushed prices higher.

Powered by WPeMatico

The Exchange is taking a break from vacation to dig into the new Qualtrics S-1 filing. Then the column and newsletter are back on hold until January 4.

This afternoon, Qualtrics, a software company that helps companies poll their employee base, customers and others, filed to go public. It’s the second time that the Utah-based unicorn has done so, failing the first time to complete its offering after SAP swooped in and bought it for around $8 billion in cash.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

SAP announced in late July of this year that Qualtrics would be spun out via an IPO, bringing the smaller company’s saga full-circle.

The new S-1 filing — you can view the 2018 original here — is a different animal from the first. First, Qualtrics is larger than it was, and older. And its financials are more complex as it extricates itself from its soon-to-be-erstwhile corporate parent.

Qualtrics intends to list on the Nasdaq under the ticker symbol “XM.”

Looking back at my chat with Ryan Smith, then Qualtrics CEO and today its chairman, and Bill McDermott, then SAP’s CEO and today the CEO of ServiceNow, it’s hard to believe that the acquisition deal was only two years ago.

Much has changed since late 2018. Let’s see what happened to Qualtrics in the meantime. We’ll dig into the financials, the company’s implied valuation range (spoiler: It has gone up) and whatever else we can shake loose.

A few things up top. First, SAP will be the company’s controlling shareholder after the Qualtrics’ IPO. That’s early in the S-1 filing. And, Smith and Silver Lake are investing in the company as part of its new debut.

Powered by WPeMatico

The last 12 months have provided us with shocking lows and surprising highs. In startup land, great expectations in January and February were followed by dashed hopes in March.

Those woes were followed by April despair, surprised optimism from May through June, and, finally, a straight shot all the way to the moon through December.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

It’s been a lot. But it’s all behind us. We don’t need to spend more time thinking about 2020 for now. We need to look ahead.

This morning, I’ve compiled notes on what’s coming. We have notes from GGV’s Hans Tung on the 2021 IPO market, Sapphires’s Beezer Clarkson on what fundraising will look like for VCs next year, and a prediction from the PitchBook analyst crew that caught my eye.

This is the last Exchange column for 2020. Thanks for reading so I could keep having fun every day at my job. Now, to work!

We’ll start with the 2021 IPO market, only because so many of you cared so very much about it this year.

Hans Tung, an investor at GGV and recent Extra Crunch Live guest, is an investor with an international perspective and a good read on global startup liquidity. So, when I got on the phone with him last week to catch up, I wanted to know his read on the 2021 IPO market.

Given that we’ve seen a number of blockbuster IPOs this year, I was expecting him to forecast an active start to the year. Correct.

But Tung added that while Q1 could be very busy, Q2 could present a lull. Why? Tung expects IPOs that failed to finish the job in Q4 2020 to slip into the first quarter of next year. That explains why the first quarter is busy. But why the slowdown in the following three months?

Powered by WPeMatico

As we head toward the exits of 2020, we have one more name to add to our roll call of private companies that have reached the $100 million annual recurring revenue (ARR) milestone. Well, one and a half.

But before we get into Nexthink and give Coalition a honorable mention, let’s talk about the startups we’re looking for in 2021.

The $100 million ARR list came together by accident, a quirk of a news cycle that happened to have a few companies reach the threshold when I was in transition back to working at TechCrunch. So, when I got back into our WordPress install, the group of companies that had each recently reached nine-figure revenues was top of mind.

The $100 million ARR list came together by accident, a quirk of a news cycle that happened to have a few companies reach the threshold when I was in transition back to working at TechCrunch. So, when I got back into our WordPress install, the group of companies that had each recently reached nine-figure revenues was top of mind.

But looking at $100 million ARR companies proved less useful than we might have hoped. Mostly what we managed was to collect a bucket of companies that were about to go public.

That was always a risk. As we wrote at the time:

Perhaps the startup market would do well to celebrate the $50 million ARR mark even more loudly. At $50 million ARR, a startup is scaling to IPO size. That’s the goal, after all.

This is our aim for 2021.

If your startup is approaching the $50 million ARR mark, or the $50 million annual run rate threshold, I want to hear from you. Drop a line if your startup has an annualized run rate between $35 million and $60 million, is privately held, and you are willing to chat about how quickly it is growing. (The Exchange first raised this idea in November.)

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But that’s next year. Today, let’s chat about Nexthink, what the hell “digital employee experience” is and what’s good with cyber insurance and why it’s helping Coalition grow rapidly.

Nexthink is a venture-backed software company with headquarters in Lausanne, Switzerland and Boston. According to PitchBook, Nexthink raised external capital in modest amounts from 2006 until 2014, when the startup picked up a $14.5 million Series D. That round was its first worth more than $10 million.

From there, Nexthink was a venture capital success story, presumably scaling quickly as it raised two larger rounds in 2016 and 2018 worth an estimated $40 million and $85 million, respectively. Nexthink was valued at a little over $558 million (post-money) following its 2018 round.

How did it attract so much external funding? By building digital experience monitoring software. Which, after doing a bit of research this morning, appears to be software aimed at tracking what corporate end users are doing with devices and how well software running on those devices perform.

Powered by WPeMatico

As 2020 comes to a close, some parts of the startup world are completing a loop, ending the year where they began.

Startup valuations, for example, as seen in the Silicon Valley area are effectively back to where they were at the start of the year. According to a report from Fenwick & West examining data through October in the San Francisco Bay area, the percentage of startups that raised up rounds (rounds priced higher than preceding investments) came within spitting distance of its pre-COVID levels.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

There are other positive signs in the data for startup bulls.

Median and average price increases for startup valuations in the Valley have both crested their 2019 averages. The gains have proven especially sharp amongst software startups, which managed somewhat epic valuation gains in October; Fenwick’s data, something we’ve covered before on The Exchange, lags the calendar month somewhat.

This morning, let’s take a break from IPOs to look at startup health in the region still generally heralded as its promised land.

As optimism for business conditions — tech-focused startups in particular — improved in Q3, startup valuations kicked off Q4 on a strong note.

In October, Silicon Valley startup investments that were priced up from their preceding deal rose to 79%. That’s down from what Fenwick reports as 2019’s average, but a dip from 83% to 79% is not much. Notably, startups in the region managed to reach an up-round percentage of rounds in the mid-to-high-seventies over the summer, but during those months down rounds were 11% to 17% of the total.

Powered by WPeMatico

This quarter, strong earnings results from public cloud companies were overshadowed by a seemingly endless IPO cycle. Another moment we somewhat missed over the last few weeks was the stock market pushing the value of public cloud companies to all-time highs.

These events are connected. And they bode well for startups working on SaaS and API-delivered software, which are keeping the climate for cloud venture investment warm and valuations stretched by historical norms.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The earnings results that have made Wall Street content include a growing number of cloud companies that are seeing revenue growth accelerate from Q2 2020 to Q3 2020, according to a recent analysis by Redpoint’s Jamin Ball.

Astute readers will recall that The Exchange chatted with Ball after the Q2 earnings cycle, a conversation that included puzzling over how to square a nearly uniform deceleration in revenue growth from Q1 to Q2 in the software sector, which, at the very same time, was supposedly undergoing a boom in demand thanks to the pandemic and a suddenly remote workforce.

One hypothesis Ball offered was that deals signed in Q2 by SaaS companies would not show up much until Q3 if they were signed in the back-half of the quarter. Regardless of the reason, Q3 featured a far-stronger crop of cloud results that imply a strengthening sector.

For us startup watchers on the hunt for a hint of what is going on in opaque private markets, this is a useful data point. If you’ve been slightly befuddled as to why the venture capital space has seen deals accelerate with time-to-conviction falling from weeks to minutes — and pre-emption the new normal — this is part of the why.

As the future has been pulled forward when it comes to digitizing the American and global economies, it’s a good time to be a software company. This was visible in SaaS company Smartsheet’s earnings this quarter. The Exchange chatted with CEO Mark Mader about his company’s recent earnings results that beat expectations and led to the company’s shares rising. Analyst upgrades have followed.

This morning, let’s examine the data regarding how many cloud companies are seeing revenue growth accelerate, dig into Smartsheet’s results to see what we can learn (hint: SMBs matter), and then apply all our findings to the startup market itself so that we can go into the weekend as informed as possible.

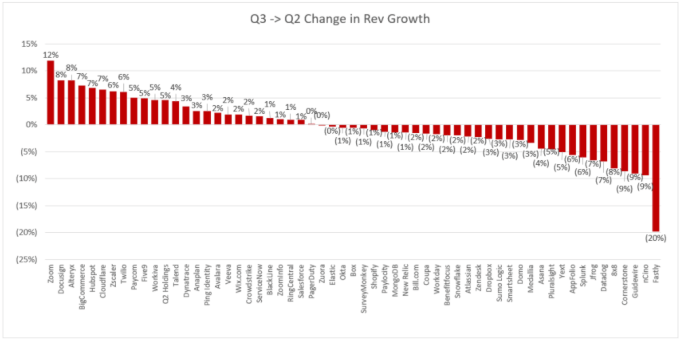

At the risk of being cheeky, I’ve embedded Ball’s chart concerning Q3 revenue acceleration from cloud companies below. (If you are into similar data sets, he’s worth following on Twitter.) Here’s the data:

Image: Jamin Ball

This chart shows Q2’s cloud year-over-year growth rates subtracted from Q3’s own; a result greater than one shows that a company’s year-over-year growth accelerated from the second quarter to the third. The higher the number of cloud companies that wind up with a result of 1% or greater in the above chart, the faster the cloud market as a whole is accelerating.

Powered by WPeMatico

Venture capital activity is high at the moment, making it difficult to keep up with the influx of new rounds that are being announced.

Our cup runneth over, and I would much rather be busy than bored, but not all sectors are as busy as others. We’re not drowning in consumer social rounds, for example. We are, however, seemingly suffering from a deluge of edtech investments.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Happily for the TechCrunch crew, Natasha Mascarenhas has become our resident expert on the sector, covering it week in and week out. But even though it’s her beat, I couldn’t help but wonder this morning upon yet another large edtech round coming across the wires, just what is going on in the sector in aggregate?

I had to know. So, I’ve done a little digging into Crunchbase data, parsed through some other information and have something approaching an idea. My goal is to help us both understand if there are more edtech rounds than ever being announced, or if it simply seems that way.

Into the breach!

The best way to start examining at a sector is to take its aggregate performance data and cut it into smaller bits. Companies do this with quarterly results, for example, an utterly arbitrary period of time to report on that is also very useful.

To get a handle on edtech in 2020, I went a bit more caveman and decided to look at the sector’s funding totals in 2020 by merely comparing the first and second half of the year.

Per Crunchbase’s “edtech” category, here’s what that data looks like:

Powered by WPeMatico