The Exchange

Auto Added by WPeMatico

Auto Added by WPeMatico

This is The TechCrunch Exchange, a newsletter that goes out on Saturdays, based on the column of the same name. You can sign up for the email here.

Welcome to a special Thanksgiving edition of The Exchange. Today we will be brief. But not silent, as there is much to talk about.

Up top, The Exchange noodled on the Slack-Salesforce deal here, so please catch up if you missed that while eating pie for breakfast yesterday. And, sadly, I have no idea why Palantir is seeing its value skyrocket. Normally we’d discuss it, asking ourselves what its gains could mean for the lower tiers of private SaaS companies. But as its public market movement appears to be an artificial bump in value, we’ll just wait.

Here’s what I want to talk about this fine Saturday: Bloomberg reporting that Stripe is in the market for more money, at a price that could value the company at “more than $70 billion or significantly higher, at as much as $100 billion.”

Hot damn. Stripe would become the first or second most valuable startup in the world at those prices, depending on how you count. Startup is a weird word to use for a company worth that much, but as Stripe is still clinging to the private markets like some sort of liferaft, keeps raising external funds, and is presumably more focused on growth than profitability, it retains the hallmark qualities of a tech startup, so, sure, we can call it one.

Which is odd, because Stripe is a huge concern that could be worth twelve-figures, provided that gets that $100 billion price tag. It’s hard to come up with a good reason for why it’s still private, other than the fact that it can get away with it.

Anyhoo, are those reported, possible prices bonkers? Maybe. But there is some logic to them. Recall that Square and PayPal earnings pointed to strong payments volume in recent quarters, which bodes well for Stripe’s own recent growth. Also note that 14 months ago or so, Stripe was already processing “hundreds of billions of dollars of transactions a year.”

You can do fun math at this juncture. Let’s say Stripe’s processing volume was $200 billion last September, and $400 billion today, thinking of the number as an annualized metric. Stripe charges 2.9% plus $0.30 for a transaction, so let’s call it 3% for the sake of simplicity and being conservative. That math shakes out to a run rate of $12 billion.

Now, the company’s actual numbers could be closer to $100 billion, $150 billion and $4.5 billion, right? And Stripe won’t have the same gross margins as Slack .

But you can start to see why Stripe’s new rumored prices aren’t 100% wild. You can make the multiples work if you are a believer in the company’s growth story. And helping the argument are its public comps. Square’s stock has more than tripled this year. PayPal’s value has more than doubled. Adyen’s shares have almost doubled. That’s the sort of public market pull that can really help a super-late-stage startup looking to raise new capital and secure an aggressive price.

To wrap, Stripe’s possible new valuation could make some sense. The fact that it is still a private company does not.

And speaking of edtech, Equity’s Natasha Mascarenhas and our intrepid producer Chris Gates put together a special ep on the education technology market. You can listen to it here. It’s good.

Hugs and let’s both go do some cardio,

Powered by WPeMatico

In the wake of insurtech unicorn Root’s IPO, it felt safe to say that the big transactions for the insurance technology startup space were done for the year.

After all, 2020 had been a big one for the broad category, with insurtech marketplaces raising lots, rental insurance startup Lemonade going public, Root itself debuting even more recently on the back of its automotive insurance business, a big round to help Hippo keep building its homeowners company and more.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But yesterday brought with it even more news: Metromile, a startup competing in the auto insurance market, is going public via a blank-check company (SPAC), and Hippo raised a huge, unpriced round.

So let’s talk about why Metromile might be plying the public markets, and why Hippo may have have decided to pick up more cash. Hint: The reasons are related.

So let’s talk about why Metromile might be plying the public markets, and why Hippo may have have decided to pick up more cash. Hint: The reasons are related.

The Lemonade IPO was a key moment for neoinsurance startups, a key part of the broader insurtech space. When the rental insurance provider went public, it helped set the tone for public exit valuations for companies of its type: fast-growing insurance companies with slick consumer brands, improving economics, a tech twist and stiff losses.

For the Roots and Metromiles and Hippos, it was an important moment.

So, when Lemonade raised its IPO range, and then traded sharply higher after its debut, it boded well for its private comps. Not that rental insurance and auto insurance or homeowners insurance are the same thing. They very most decidedly are not, but Lemonade’s IPO demonstrated that private investors were correct to bet generally on the collection of startups, because when they reached IPO-scale, they had something that public investors wanted.

Powered by WPeMatico

Time flies.

It was nearly a year ago that The Exchange started keeping tabs on startups that managed to reach $100 million in annual recurring revenue, or ARR. Our goal was to determine which unicorns were more than paper horses so we could keep tabs on upcoming IPO targets.

We found that Bill.com, Asana, WalkMe and Druva were impressively large and growing nicely. Since then two of the four companies from that post have gone public.

GitLab, Egnyte, Braze and O’Reilly Media joined the club before 2019 was even closed, with two of those companies taking part in the recent Disrupt conference, talking about how they managed their historical growth.

In early 2020 we added Sisense, Siteminder, Monday.com and Lemonade to the club, wrote about ExtraHop’s path to $100 million ARR, Cloudinary’s epic growth sans external capital, Siteminder’s own records and BounceX reaching $100 million ARR while it rebranded to Wunderkind.

In early 2020 we added Sisense, Siteminder, Monday.com and Lemonade to the club, wrote about ExtraHop’s path to $100 million ARR, Cloudinary’s epic growth sans external capital, Siteminder’s own records and BounceX reaching $100 million ARR while it rebranded to Wunderkind.

As the year rolled along, MetroMile, Tricentis, Kaltura and Diligent joined the club. As did Recorded Future, ON24 and ActiveCampaign. There were even more names: Movable Ink, Noom, Riskified, Seismic, ThoughtSpot, along with Snow Software, A Cloud Guru, Zeta Global and Upgrade.

Today we have three more names to add to the group: UserTesting, Udemy’s business arm and Expensify. But, more than merely adding those companies to the mix — more after the jump — I wanted to shake up our radar a bit as we head into 2021.

Yes, The Exchange will keep tabs on startups and other private companies that reach $100 million in ARR, or annual run rate, as the case may be. But next year we also want to find the startups around $50 million ARR that are growing like hell. We want to go a year or two earlier in growth histories to better watch how startups scale into nine-figure revenues, instead of hearing about it after the fact.

So, if you are a startup that is expanding aggressively and will reach the $50 million revenue mark inside the next quarter or two, please say hello. I suspect a good cut of the global unicorn market could fit this bill, and therefore might provide a window into which highly valued startups are growing into their valuations.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

It’s going to be fun. Now, let’s quickly chat about the latest members of the $100 million ARR club.

You’ve heard of each of our $100 million ARR companies this morning, so there’s less need for prelude and introduction. Here’s the group:

Expensify is an expense-tracking company well-known around the technology world, so it’s no real surprise that it has reached the $100 million ARR threshold, a feat it announced yesterday.

But the company did us one better than merely dropping a single data point and racing back into the shadows. Instead, Expensify also disclosed that it has “maintained profitability for years [and] recorded its highest monthly revenue ever in October.”

Powered by WPeMatico

A spate of startups focused on mental health recently made enough noise as a group that they caught the eye of the Equity podcast crew. Sadly, the segment we’d planned to discuss this topic was swept away by a blizzard of IPO filings that piled up like fresh snow.

But in preparation, I reached out to CB Insights for new data on the mental health startup space that they were kind enough to supply. So this morning we’re going to dig into it.

Regular readers of The Exchange will recall that we last dug into overall wellness venture capital investment in August, noting that it was mental health startups inside the vertical that were seeing the most impressive results.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

I wanted to know what had happened even more recently.

After all, Spring Health recently raised $76 million for its service that helps companies offer their workers mental health benefits, Mantra Health disclosed that it has raised $3.2 million to help with college-age mental health issues and Joon Care announced $3.5 million in new capital to “grow its remote therapy service for teens and young adults,” per GeekWire.

Sticking to theme, Headway just raised $32 million to build a platform that “helps people search for and engage therapists who accept insurance for payments,” according to our own reporting, and online therapy provider Talkspace is pursuing a sale — it looks like an active time in the mental health startup realm.

So, let’s shovel into the latest data and see if the signals that we are seeing really do reflect more total investment into mental health startups, or if we’re overindexing off a few news items.

So, let’s shovel into the latest data and see if the signals that we are seeing really do reflect more total investment into mental health startups, or if we’re overindexing off a few news items.

To prepare the ground, let’s talk about the general state of healthcare investing in the venture capital world. Per CB Insights’ Q3 healthcare VC report, venture capital deal volume and venture capital dollar volume reached new record highs in the sector during Q3 2020.

The quarter’s 1,539 rounds and $21.8 billion in invested capital were each comfortably ahead of prior records set in Q2 2018 for round volume (1,431) and Q2 2020 for dollar volume ($18.4 billion) for healthcare startups.

Powered by WPeMatico

This is The TechCrunch Exchange, a newsletter that goes out on Saturdays, based on the column of the same name. You can sign up for the email here.

I had a neat look into the world of mental health startup fundraising planned for this week, but after being slow-motion carpet-bombed by S-1s, that is now shoved off to Monday and we have to pause and talk about COVID-19.

The pandemic has been the most animating force for startups and venture capital in 2020, discounting the slow movement of global business into the digital realm. But COVID did more than that, as we all know. It crashed some companies as assuredly as it gave others a boost. For every Peloton there is probably a Toast, in other words.

Such is the case with this week’s crop of unicorn IPO candidates, though they are unsurprisingly weighted far more toward the COVID-accelerated cohort of startups instead of the group of startups that the pandemic cut off at the knees.

More simply, COVID-19 gave most of our recent IPOs a polite shove in the back, helping them jog a bit faster toward the public-offering finish line. Let’s talk about it.

Roblox, the gaming company that targets kids, has been a beneficiary during the COVID-19 pandemic, as folks stayed home and, it appears, gave their kids money to buy in-game currency so that their parents could have some peace. Great business, even if Roblox warned that growth could slow sharply next year, when compared to its epic 2020 gains.

But Roblox is hardly the only company taking advantage of COVID-19’s impacts on the market to get public while their numbers are stellar. We saw DoorDash file last week, crowing from atop a mountain of revenue growth that came in part from you and I trying to stay home since March. As it turns out you order more delivery when you can’t leave your house.

Affirm got a COVID-19 boost as well, with not only e-commerce spend growing — Affirm provides point-of-sale loans to consumers during online shopping — but also because Peloton took off, and lots of folks chose to finance their new exercise bike with the payment service. Call it a double-boost.

The IPO is well-timed. Wish falls into the same bucket, though it did hit some supply-chain and delivery issues due to the pandemic, so you could argue it either way.

Regardless, as we have seen from global numbers, COVID-19 is very much not done wreaking havoc on our health, happiness, and ability to go about normal life. So the trends that this week’s S-1s have shown us still have some room to run.

Which is irksome for Airbnb, a unicorn that was supposed to have debuted already via a direct listing, but instead had to hit pause, borrow money, lay off staff, and now jog to the startup finish line with less revenue in this Q3 than the last. In time, Airbnb will get back to full-speed, but among our new IPO candidates it’s the only company net-harmed by COVID-19. That makes it special.

There are other trends to keep tabs on, regarding the pandemic. Not every software company that you might expect to be thriving at the moment actually is; Workday shares are off 8% today as I write to you, because the company said that COVID-19 is harming its ability to land new customers. Here’s its CFO Robynne Sisco from its earnings call

Keep in mind, however, that while we have seen some recent stability in the underlying environment, headwinds due to COVID remains particularly to net new bookings. And given our subscription model, these headwinds that have impacted us all year will be more fully evident in next year’s subscription revenue weighing on our growth in the near-term.

Yeesh. So don’t look at recent IPOs and think that all things are good for all companies, or even all software companies. (To be clear, the pandemic is a human crisis, but my job is to talk about its business impacts so here we are. Hugs, and please stay as safe as you can.)

There was so much news this week that we have to be annoyingly summary.

I caught up with Brex CEO Henrique Dubugras the other day, giving The Exchange a chance to parse what happened to the company during the early COVID days when the company decided to cut staff. The short answer from the CEO is that the company went from growing 10% to 15% each month, to seeing negative growth — not a sin, Airbnb saw negative gross bookings for a few months earlier this year — and as the company had hired for a big year, it had to make cuts. Dubugras talked about how hard of a choice that was to make.

Brex’s business rebounded faster than the company expected, however, driven in part by strong new business formation — some data here — and companies rapidly moving into the digital realm and moving to finance systems like Brex’s.

Looking forward, Dubugras wants to expand the pool of companies that Brex can underwrite, which makes sense as that would open up its market size quite a lot. And the company is as remote as companies are now, with its CEO opening up during our chat about the pros and cons of the move. Happily for the business fintech unicorn, Dubugras said that some of the negatives of companies working more remotely haven’t been as tough as expected.

Next up: Growth metric. Verbit, a startup that uses AI to transcribe and caption videos, raised a $60 million Series C this week led by Sapphire Ventures. I couldn’t get to the round, but the company did note in its release that it has seen 400% year-over-year revenue growth, and that its “revenue run-rate [has] grown five-fold since 2019.” Nice.

Jai Das led the round for Verbit, and, in a quirk of good timing, I’m hosting an Extra Crunch Live with him in a few weeks. (Extra Crunch sub required for that, head here if you need one. The discount code ‘EQUITY’ should still be working if it helps.)

Telos, a Virginia-based cybersecurity and identity company went public this week. It fell under our radar because there is more news than we have hands to type it up. Such is the rapid-fire news cycle of late 2020. But, to catch us both up, Telos priced midrange but with an upsized offering, valuing it around $1 billion, according to MarketWatch.

After going public, Telos shares have performed well. Cybersecurity is having one hell of a year.

Turning back to our favorite topic in the world, SaaS, ProfitWell’s Patrick Campbell dropped a grip of data on the impact of COVID-19 on the B2B SaaS market. Mostly it’s positive. There was a hit early on, but then growth seems to have accelerated. Just keep in mind the Workday example from earlier; not everyone is in software growth paradise as 2020 comes to a close.

And, finally, after Affirm released its S-1 filing, competing service Klarna decided it was a good time to drop some performance data of its own. First of all, Klarna — thanks. We like data. Second of all, just go public. Klarna said that it grew from 10 million customers in the United States to 11 million in three weeks, and that the second statistic was up 106% compared to its year-ago tally.

Affirm, you are now required by honor to update your S-1 with even more data as an arch-nerd clapback. Sorry, I don’t make the rules.

Alright, that’s enough of all that. Chat to you soon, and I hope that you are safe and well and good.

Powered by WPeMatico

With Roblox joining the end-of-year unicorn stampede toward the public markets, we’re set for a contentedly busy second half of November and early December. I hope you didn’t have vacation planned in the next few weeks.

This morning we need to get deeper into the Roblox S-1 so we can better understand the nature of its revenue generation. Why? Because we want to start working on what the gaming company is worth; some comparisons are being made to Unity, another unicorn that went public earlier this year with a gaming focus.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Should we apply Unity’s revenue multiple to Roblox? Or does the company deserve a slimmer multiple based on the substance of its revenue?

We’ll also have to remind ourselves how much capital Roblox last raised while private, and at what price. Given our historical knowledge of its financial results, we might be able to nail some valuations to revenue figures, helping us understand, roughly, how the venture capital community was valuing Roblox while it was private.

We’ll also have to remind ourselves how much capital Roblox last raised while private, and at what price. Given our historical knowledge of its financial results, we might be able to nail some valuations to revenue figures, helping us understand, roughly, how the venture capital community was valuing Roblox while it was private.

If you want an overview of just the numbers, Natasha and I wrote a digest here.

Now, let’s get to work.

To get a foundation, let’s recall how Roblox was valued during its last private round. According to Crunchbase data, Roblox’s $150 million Series G was raised at a $3.9 billion pre-money valuation. So, Roblox was worth $4.05 billion after the February 2020 funding event.

Naturally there is a lag between when a deal is struck and when it is announced. So, let’s rewind the clock to Q4 2019 and ask ourselves what Roblox looked like at the time. From its S-1, here are the Q4 2019 numbers:

Annualizing that revenue figure, Roblox was on a $553.3 million run rate at around the time it raised that Series G. In revenue-multiple terms, Roblox was valued at 7.3x its top line on an annualized basis.

If you are a SaaS fan you are probably pretty shocked right now. Why the hell was Roblox, a software company, worth so little? Well let’s remind ourselves how it makes money:

We generate substantially all of our revenue through the sales of Robux to users. Users can spend Robux to purchase access to experiences, enhancements in experiences, and items in the Avatar Marketplace. Robux are available as one-time purchases or monthly subscriptions. We recognize revenue ratably over the estimated average lifetime of a paying user. […]

Other revenue streams include a minimal amount of revenue from advertising, licenses, and royalties.

Powered by WPeMatico

This is The TechCrunch Exchange, a newsletter that goes out on Saturdays, based on the column of the same name. You can sign up for the email here.

DoorDash filed to go public on Friday, meaning we’ll have at least one more unicorn IPO before 2020 comes to a close. For a high-level look at its numbers, I wrote this, Danny covered who will profit from the deal, and I noodled on the impact of COVID-19 on its business.

I bring all that up because there is another COVID-19 impacted unicorn that we are expecting to see go public in very short order: Airbnb.

When Airbnb filed to go public in August, it seemed like a solid plan. The company was widely reported to be on an upswing from its COVID-doldrums, the public markets were hot for growth and tech shares, and the pandemic’s caseload in the United States was coming down from its summer highs. It looked great for Airbnb to wrap its Q3, drop its public S-1 with the new numbers, and laugh all the way to the bank after showing investors that even a global pandemic and travel industry depression couldn’t stop it.

And yet. The United States and world at large are now in the midst of the worst COVID-19 spike yet, and consumer spend is going down right before we get the company’s S-1. November feels less winsome for an Airbnb recovery than August or September did. Still, when Airbnb files — next week, the scuttlebutt indicates, so get ready — we’ll only have a look at its numbers through the third quarter.

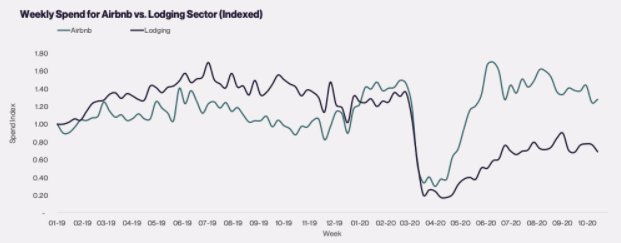

That’s effectively the same timeframe for a dataset that the folks at Cardify sent over and I dug through. Per the company, which tracks real-time consumer spend data, here’s a look at how well Airbnb recovered ahead of its larger industry after the initial recession in pandemic lodging spend:

Impressive, right? Sadly for Airbnb, the initial boom of demand through late June into July tapered as time continued.

Zooming in somewhat, here’s Airbnb spend data from July 2020 through the end of October, the first month of Q4, compared to the same period of 2019:

Declines, then, but still an encouraging set of data for the company regardless. I would not have expected Airbnb spend — via third-party, admittedly — to be this strong.

The trend of folks renting a house for a month seems to have diminished somewhat, in case you are factoring that into your mental math concerning Airbnb revenues from the above charts. Cardify told TechCrunch that after peaking at around +70% in the March-April timeframe, “average booking sizes have now normalized and are approximately 30% higher on a YTD basis.”

There is weakness in October, the charts show, but that appears to be at least partially seasonal given the 2019 line, so I don’t want to over-ascribe rising COVID cases as the cause. The drooping line, however, was echoed in similar SimilarWeb data that was also shared with The Exchange. The dataset concerned accommodation booking volume around the world for a number of travel services, including Airbnb. Its data tracking the US market showed that a bookings recovery through September that made up some ground on March lows was undercut by October declines. Europe’s bookings’ recovery peaked in July and has been falling ever since. Asian volume is creeping higher, but down sharply from prior levels.

It was a mixed picture, but as Airbnb is doing better than its broader industry per Cardify, the aggregated data could be leading us to be more pessimistic than we otherwise need to be. We’ll see shortly what the real numbers are, but I couldn’t help but share what I was reading with you. On to the S-1!

Before DoorDash filed, we were going to talk about Brex today in this space after Airbnb. But, since we got extra busy, expect those notes early next week on The Exchange.

The week was super busy with earnings, so I’ve collected a few notes from calls with select companies after they reported. Apologies to everyone’s’ favorite reporting firm, but we’re space-limited.

Appian crushed earnings expectations. What drove the low-code application development services’ growth forward? According to CEO Matt Calkins, it wasn’t a single thing. Instead, the company’s performance was driven by a long ramp he said, though he did also state that the concept of low-code has reached the public consciousness in new, higher levels during the last few quarters.

Why? The year’s chaos pushed companies into new patterns faster than they had anticipated. Chalk this result up to the accelerating digital transformation being real, which is good news for startups. (For more on Appian and the low-code space, head here.)

Alteryx gave The Exchange an earnings first, providing both its newly former CEO Dean Stoecker and its new CEO Mark Anderson to chat results. The company crushed Q3 expectations, but its Q4 projections did not excite investors. What was up? Anderson argued that ARR growth, not forward GAAP revenue projections, is the most transparent and clear view of an expanding software company, to paraphrase his thinking. You can’t ignore revenue, he said, but given the nuances in how revenue is counted, pay attention to ARR.

Alteryx has a solid ARR target for 2021. We’ll see how investors view its Q4 results and if they align their thinking to that of the new CEO. Alteryx’s former CEO is bullish, saying that in time the market will realize that analytics is at the epicenter of digital transformation. And his company will be there with code to sell.

Moving along, earlier this week I asked a number of VCs about the software venture capital market in the wake of Monday’s sharp selloff and my question about what might happen to public and private software companies if other stocks suddenly became more attractive — strong vaccine news on Monday was later overwhelmed by surging cases as the week went along, but on Monday Zoom lost billions in value as investors fled.

One set of responses came in late, but I wanted to share them all the same as they were more bullish than I anticipated. In the view of Laela Sturdy, a general partner at Alphabet Capital G, “private software investors are unlikely to change their investing patterns much as a result of fluctuations in the public market,” adding later that “public market changes would have to be very extreme — as in 30 percent or more — in order to impact growth stage valuations.”

The connection between public valuations and trading patterns and private capital deployment exists, but how closely the two are linked depends on what’s happening at any given moment, and it appears that at the moment private investor excitement about software is durable.

Sturdy explained why that may be: “Long-term secular trends around cloud adoption, automation and AI, data, security, fintech infrastructure, and the ongoing rapid acceleration of digital transformation will help tech companies maintain their status as the darlings of growth investors in both the private and public markets.”

And finally, the rest of the stuff that I couldn’t get to this week. Here we go:

Closing with something fun, remember that look we did of the performance of various startups in Q3? That was fun. Anyhoo, no-code “online form builder” JotForm told The Exchange that its revenue is up 50% from its 2019 results, that its enterprise customer base is up 620%, and that it expects to reach “100,000 total paid users by end of year.” Neat!

Powered by WPeMatico

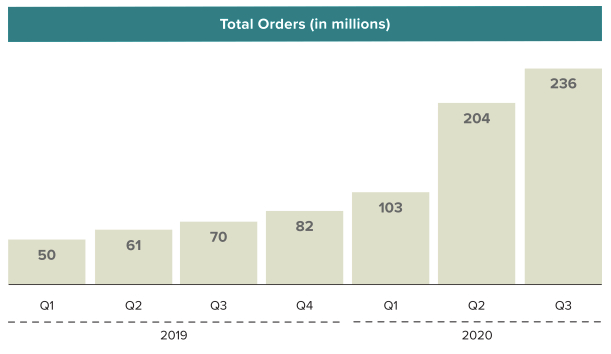

DoorDash filed to go public today, publishing numbers that showed rapid growth, enhanced profitability and an improving cash flow record which helped explain how the company had grown to a $16 billion valuation while private. The unicorn’s impending liquidity event will enrich a host of venture capital firms that bet on its eventual maturity.

Instead of posting this entry of The Exchange on Monday, we’ve put it out today for your Friday and weekend reading. Enjoy! — Alex and Walter.

But notable in DoorDash’s impressive results is the impact of COVID-19, accelerating secular trends already in place, and boosting the unicorn’s growth. Before we get into pricing this IPO and guessing what the company might be worth, let’s strive to understand what portion of its 2020 business gains could stem from the pandemic — and might not persist into the future.

We’re not being pessimistic; we merely want to better understand the company. And DoorDash agrees with our general thrust, writing in its S-1 filing that “58% of all adults and 70% of millennials say that they are more likely to have restaurant food delivered than they were two years ago,” adding that it believes “the COVID-19 pandemic has further accelerated these trends.”

Even more, elsewhere in its filings DoorDash states plainly that COVD-19 led it to experience “a significant increase in revenue, Total Orders, and Marketplace [gross order volume] due to increased consumer demand for delivery, more merchants using our platform to facilitate both delivery and take-out, and improved efficiency of our local logistics platform.” The company then went on to warn investors that the “circumstances that have accelerated the growth of our business stemming from the effects of the COVID-19 pandemic may not continue in the future, and we expect the growth rates in revenue, Total Orders, and Marketplace [gross order volume] to decline in future periods.”

We’re not idly speculating.

Let’s observe how DoorDash’s growth accelerated from 2019 through 2020 and then peek at how the company’s economics improved during the same period, giving the company a shot at adjusted profitability for the full year, a nearly unheard of result in the on-demand market.

DoorDash generates revenue when a customer orders food via its service, splitting the total bill of food costs, taxes, fees and tips, distributing them to itself, the merchant creating the goods and the delivery person.

In an “illustrative” example that DoorDash notes its 2019 “approximate average per-order information,” the split works out as follows:

Given that the company is giving us old data and DoorDash’s performance has been stellar this year in terms of generating more gross profit, I wonder what has happened amidst 2020’s upheaval. But, the old numbers do for what we need, which is to understand the link between gross order volume (GOV) and DoorDash revenue. When the former goes up, the latter goes up.

So, as orders rise:

Powered by WPeMatico

Earnings season is racing past us, with the big ride-hailing companies’ numbers in, all of the Big Five having wrapped their reporting and lots of SaaS numbers in the market. But amidst all the noise, The Exchange has kept an eye on two companies in particular: PayPal and Square.

We’re not really concerned with their overall revenue and profit metrics. Instead, we’ve been hunting around in their numbers for hints and notes about what is going on inside of fintech itself. Why? There are a host of hugely valuable fintech unicorns that have to go public in the future that also share some market space with one or both of our public charges.

What can we learn from looking at what PayPal and Square reported to their own investors?

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Lots, it turns out.

As TechCrunch reported when PayPal dropped its Q3 numbers, the public company had bullish results from its Venmo service, payment processing and consumer activity metrics. The numbers pointed to strong consumer adoption of fintech services during the pandemic, something that we presumed was not unique to PayPal itself, but was likely indicative of a generally warm environment for consumer fintech services.

Square continued the trend, posting a set of results that contains nearly all positive data for consumer fintech activity — with one critical caveat for Q4 that we’ll get to at the end.

Still, what the majors tell us about the fintech space indicates a warmth in activity that explains why Chime, Robinhood and others have had such fun in 2020, accreting tectonic capital to keep their growth hot.

Digging through Square’s earnings gives us a window into consumer payment activity, card usage, stock purchases and more. Let’s see what we can learn, and to which unicorns it might apply.

Let’s start by talking about the broader fintech market before niching down.

Powered by WPeMatico

Monday’s news that a COVID-19 vaccine candidate looks to be incredibly effective gave investors reasons to believe in a better future. Perhaps COVID-19 won’t be with us for years, investors appeared to think, but will instead become something that we can bend the curve on sooner than we thought.

A strong vaccine would be key toward moving back to life as it was. And for many companies battered by the pandemic, news that one was coming was more than a shot in the arm — it was stock market salvation. Airline shares soared. Cruise companies jumped. Even long-suffering Boeing shares took flight.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But amidst the cheering, one sector of the stock market, a key comp for a host of startups, took hits. Yes, the high-flying SaaS and cloud stocks that have been such a key narrative in 2020 thanks to the pandemic and low interest rates, fell sharply while other sectors rallied off the vaccine tidings.

SaaS and cloud stocks are off more this morning, though their declines are shallower than Monday’s losses.

We asked yesterday what signal public investors were trying to send with their trades. But that’s just one angle of the picture. So, to better understand how private investors are viewing the same signals, I reached out to a few VCs who invest in SaaS and, in my experience, are worth listening to.

Below I’ve compiled notes from Bessemer’s Mary D’Onofrio, Work Life Ventures’ Brianne Kimmel, Day One Ventures’ Masha Drokova, Floodgate’s Iris Choi and Shasta’s Jacob Mullins on our question.

Are the bulls still bullish? Let’s find out.

D’Onofrio wrote that her firm was still digesting the vaccine news and that it was “too early to say decisively whether or not people will be back to a pre-COVID life in the next few quarters.” That’s fair. Some good vaccine news does not mean that I’ll be back to speed-running United Economy Plus across the country every two weeks come April.

That said, D’Onofrio doesn’t appear too worried about the early-week selloff, noting that SaaS and cloud stocks — as measured via her firm’s cloud index — are still far ahead of other, broader indices this year. Why does that matter? “Stocks are forward-looking,” she said, which tells her “that even with more visibility into returning to ‘normal,’ the market anticipates that cloud companies will still be able to capitalize on the [market expansion] and growth opportunities that COVID helped to propel.”

“The pie,” she concluded, “has expanded.” That’s bullish and fair, I reckon.

Powered by WPeMatico