The Exchange

Auto Added by WPeMatico

Auto Added by WPeMatico

Mere days after we discussed Coinbase at $77 billion and Stripe at $115 billion in the private markets, those same semi-liquid exchanges have provided a new valuation for the cryptocurrency company. It’s now $100 billion, per Axios’ reporting.

Good thing we argued last week that there could be some merit to Coinbase’s $77 billion secondary market valuation from a particular perspective. We’d look silly today if we’d mocked the $77 billion figure only for it to go up by about a third in just a few days.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Luckily for us, Axios also got its hands on a few numbers regarding Coinbase’s 2019 and 2020 financial performance, so we can get into all sorts of trouble this morning. We’ll look at the data, which stretches to the end of Q3 2020, and then do some creative extrapolating into Q1 2021 to decide whether Coinbase at $100 billion makes no sense, a little sense or perfect sense.

As always, we’re riffing, not giving investment advice. So read on if you want to noodle on Coinbase with me; its impending direct listing will be one of the year’s most watched financial events.

We’ll drag Stripe back in at the end. Given that the companies now nearly share private-market valuations, we’d be remiss to not unfairly stack them against one another. Into the breach!

Axios’ Dan Primack, a good egg in my experience, got the goods on Coinbase’s historical performance. Summarizing the bits we need, here’s what the crypto exchange got up to recently:

It’s simple to take the 2020 data that we have and extrapolate it into full-year data. Indeed, you get revenues of $921.33 million and net income of $188 million. Compared to its 2019 data, Coinbase would have managed around 74% growth while swinging steeply into the profitable domain.

That’s a killer year. But it’s actually a bit better than we are giving Coinbase credit for. Poking around volume data compiled by Bitcoinity.org, Coinbase had its biggest period of 2020 in terms of bitcoin trading volume in the fourth quarter. Thinking about Coinbase’s 2020 from a trading perspective using the same dataset, it had a great Q1, more staid Q2 and Q3, and a blockbuster Q4 that ramped to record highs at the end.

Powered by WPeMatico

If we are not careful, every entry of this column could consist of SPAC news.

Special purpose acquisition companies, or blank-check companies, whatever you prefer to call them, are enormous business today. But they aren’t the only thing going on, and we’ll get to other things shortly. Consider this an apology for having written about SPACs twice in two days.

Yesterday, we considered the rise of the VC-led SPAC and whether venture capital groups that offer seed-through-SPAC money will wind up with advantage in the market over firms that specialize on any particular startup stage. Sticking to the blank-check theme, this morning we’re looking into two SPAC-led deals, namely those involving Rover and MoneyLion.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

We’re doubling up to prevent more SPAC-related posts. And we’ve selected Rover because Chewy, another pet-themed entity, is an already-public company. As both were venture-backed, we may be able to contrast their trading performance post-debut. Sadly, Chewy is focused on pet e-commerce while Rover is more centered around pet services, but they may prove close enough for some loose comparisons.

And why chat about MoneyLion? Because it’s a heavily venture-backed fintech startup, one that TechCrunch has covered extensively. If its SPAC-assisted vault into the public markets goes well, it could smooth the same path forward for myriad other yet-private fintechs sitting atop a mountain of raised capital.

And why chat about MoneyLion? Because it’s a heavily venture-backed fintech startup, one that TechCrunch has covered extensively. If its SPAC-assisted vault into the public markets goes well, it could smooth the same path forward for myriad other yet-private fintechs sitting atop a mountain of raised capital.

So this is a SPAC post, but as we’ll largely be looking at the financial health of two companies that we’ve heard about for ages and never got to see inside of, I hope you join me all the same.

We’re starting with the Rover investor presentation, before zipping over to MoneyLion’s own.

Rover is merging with Nebula Caravel Acquisition Corp., which is affiliated with True Wind Capital. The deal gives Rover an anticipated market cap of around $1.6 billion, with around $300 million in cash on its books.

So, how attractive is this new unicorn? You can find its investor deck here, if you want to read along as we peek.

First up, the company stresses rising use of digital services in the last year thanks to the pandemic and the fact that pet ownership is growing. Both of which are true. We’ve seen the accelerating digital transformation for both companies and consumers. And if you’ve tried to adopt a pet lately, you’ve seen how few are left waiting for forever homes.

With those things behind it, you might be wondering why Rover is pursuing a SPAC-led debut as well. If its market is hot and it has previously raised venture capital, why not just go public via an IPO? Because 2020 was tough on the company.

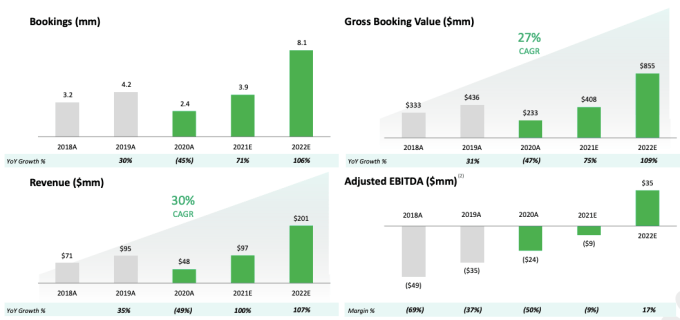

Image Credits: Rover

Revenue dipped from $95 million in 2019 to just $48 million last year. Bookings fell from 4.2 million to 2.4 million over the same time frame, leading to gross booking value falling from $436 million in 2019 to $233 million in 2020. Why? Because everyone was stuck at home. With their pets. A situation that limited demand for Rover-delivered pet services.

Powered by WPeMatico

Since last year, we’ve been tracking the growing list of capitalists who got into the SPAC game. You can read an interview we conducted with Amish Jani, the co-founder of FirstMark Capital, about his SPAC here. And if you need a refresher on all things SPAC, we have that for you as well.

This morning, I want to better understand the trend by parsing a few new venture capitalist SPACs. We’ll examine Lerer Hippeau Acquisition Corp. and Khosla Ventures Acquisition Co. I, II and III. The SPACs are, somewhat obviously, associated with New York-based Lerer Hippeau and Menlo Park’s Khosla Ventures. And all four dropped formal S-1 filings last week.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Today’s topic may sound dry, but it really does matter. As we’ve reported, Lux Capital is in on the SPAC wager, along with Ribbit and, of course, SoftBank. Adding our latest names to the mix and you have to wonder if every VC worth a damn in the future will have their own raft of SPAC offerings.

In that way, as some late-stage venture capital funds invest earlier — and now later — full-service VC outfits will offer first check to final liquidity, will such a full-stack venture outfit be able to win more deals than a group offering a limited set of financing options? If so, the recent venture capital SPAC wave could become more of a rising tide in time, to torture a metaphor.

In that way, as some late-stage venture capital funds invest earlier — and now later — full-service VC outfits will offer first check to final liquidity, will such a full-stack venture outfit be able to win more deals than a group offering a limited set of financing options? If so, the recent venture capital SPAC wave could become more of a rising tide in time, to torture a metaphor.

Regardless, let’s quickly parse what Khosla and Lerer Hippeau are telling public investors about why they will be great SPACers before working our way backward to what the resulting pitch must be to startups themselves.

The Lerer Hippeau SPAC is the most interesting of the two firms’ combined four offerings, so we’ll start there. That isn’t to diss Khosla, but the Lerer Hippeau blank check has some explicit wording I want to highlight.

From the Lerer Hippeau Acquisition Corp. S-1 filing, read the following (bolding: TechCrunch):

As our seed portfolio matured over the last decade, we added a growth strategy to our platform through our select funds. This capital enables us to continue providing financial support to our top performing early-stage companies as they scale, and to selectively make new investments in later-stage companies in the Lerer Hippeau network. With our portfolio now maturing to the stage at which many are considering the public markets, we view SPACs as a natural next step in the evolution of our platform.

After writing that it has had four portfolio companies “publicly announced business combination agreements with SPACs” and noting that it expects more of the same, Lerer Hippeau added that it considers its “expansion into the SPAC market as a highly complementary element of our strategy to support founders throughout their entrepreneurial journeys.”

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Ready? Let’s talk money, startups and spicy IPO rumors.

Earlier this week TechCrunch broke the news that Public, a consumer stock trading service, was in the process of raising more money. Business Insider quickly filled in details surrounding the round, that it could be around $200 million at a valuation of $1.2 billion. Tiger could lead.

Public wants to be the anti-Robinhood. With a focus on social, and a recent move away from generating payment for order flow (PFOF) revenues that have driven Robinhood’s business model, and attracted criticism, Public has laid its bets. And investors, in the wake of its rival’s troubles, are ready to make it a unicorn.

Of course, the Public round comes on the heels of Robinhood’s epic $3.4 billion raise, a deal that was shocking for both its scale and speed. The trading service’s investors came in force to ensure it had the capital it needed to continue supporting consumer trades. Thanks to Robinhood’s strong Q4 2020 results, and implied growth in Q1 2021, the boosted investment made sense.

As does the Public money, provided that 1) The company is seeing lots of user growth, and 2) That it figures out its forever business model in time. We cannot comment on the second, but we can say a bit about the first point.

Thanks not to Public, really, but M1 Finance, a Midwest-based consumer fintech that has a stock-buying function amongst its other services (more on it here). It told TechCrunch that it saw a quadrupling of signups in January as compared to December. And in the last two weeks, it saw six times as many signups as the preceding two weeks.

Given that M1 doesn’t allow for trading — something that its team repeatedly stressed in notes to TechCrunch — we can’t draw a perfect line between M1 and Public and Robinhood, but we can infer that there is huge consumer interest in investing of late. Which helps explain why Public, which is hunting up a way to generate long-term incomes, can raise another round just months after it closed a different investment.

Our notes last year on how savings and investing were the new thing last year are accidentally becoming even more true than we expected.

As the week came to a close, Coupang filed to go public. You can read our first look here, but it’s going to be big news. Also on the IPO beat, Matterport is going out via a SPAC, I chatted with Metromile CEO Dan Preston about his insurtech public offering this week that also came via a SPAC, and so on.

Oscar Health filed, and it doesn’t look super strong. So its impending valuation is going to test public traders. That’s not a problem that Bumble had when it priced above-range this week and then skyrocketed after it started to trade. Natasha and I (she’s on Equity, as well) have some notes from Bumble CEO Whitney Wolfe Herd that we’ll get to you early next week. (Also I chatted about the IPO with the BBC a few times, which was neat, the first of which you can check out here if you’d like.)

Roblox’s impending public debut was also back in the news this week. The company was a bit bigger than it thought last year (cool), but may delay its direct listing to March (not cool).

Near to the IPO beat, Carta started to allow its own shares to trade recently, on the back of news that its revenues have scaled to around $150 million. Not bad Carta, but how about a real IPO instead of staying private? The company’s valuation more than doubled during the secondary transitions.

And then there were so very many cool venture capital rounds that I couldn’t get to this week. This Koa Health round, for example. And whatever this Slync.io news is. (If you want some earlier-stage stuff, check out recent rounds from Treinta, Level, Ramp and Monte Carlo.

And to close, a small callout to Ontic, which provides “protective intelligence software” and said that its revenue grew 177% last year. I appreciate the sharing of the numbers, so wanted to highlight the figure.

Wrapping this week, I have a final bit for you to chew on from Mark Mader, the CEO of Smartsheet, a public company — former startup, it’s worth noting — that plays in the no-code, automation and collaboration markets. That’s a rough summary. Anyhoo, I asked Mader about no-code trends in 2021, as I have my eyes on the space. Here’s what he wrote for us:

If you thought the sudden shift to remote work sped up corporate America’s shift to digital, you haven’t seen anything yet. Digital transformation is going to accelerate even more rapidly in 2021. Last year, the workforce was exposed to many different types of technology all at once. For example, a company may have deployed Zoom or DocuSign for the first time. But much of this shift involved taking analog processes like meetings or document signing and approval and bringing them online. Things like this are merely a first step. 2021 is the year the companies will begin to connect large-scale digital events to infrastructure that can make them automated and repeatable. It’s the difference between one person signing a document and hundreds of people signing hundreds of documents, with different rules for each one. And that’s just one example. Another use case could involve linking HR software to project management software for automated, real-time resource allocation that allows a company to get more out of both platforms, as well as its people. The businesses that can automate and simplify complex workflows like these will see dramatically improved efficiency and return on their technology investments, putting them on the path to true transformation and improved profitability.

We shall see!

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Ready? Let’s talk money, startups and spicy IPO rumors.

It’s been a bizarre few weeks, with Robinhood raising a torrent of new funds to keep its zero-cost trading model afloat during turbulent market conditions, other neo-trading houses changing up their business model and more. But amidst all the moves in startup-land, something has been itching in the back of my head: Why are several rich people pumping crappy assets?

It’s fine for a retail investor to share trading ideas amongst themselves; it has happened, will happen, and will always happen. But we’ve seen folks like Elon Musk and Chamath Palihapitiya use their broad market imprint to encourage regular folks — directly and indirectly — to buy into some pretty silly trades that could lose the retail crowd lots of money that they may not be able to afford.

Think of Elon coming back to Twitter to pump Doge, a joke of a cryptocurrency that is highly volatile and mostly useless. Or Chamath putting money into GameStop publicly, a move that he is better equipped than most to get into and out of. Which he did. And made money. Most folks that played the GameStop casino have not been as lucky, and many have lost more than they can afford.

Caveat emptor and all that, but I do not love folks with savvy and capital leading regular people into risky trades or into assets that are not backed by long-term fundamentals, but instead a small shot at near-term returns. Yoof.

Finally, keeping up the theme of general annoyance, Senator Hawley is back in the news this week with an attention-focused announcement of an idea to block big tech companies from buying smaller companies. As you would expect from the insurrection-friendly Senator, it’s not an incredibly serious proposal, and it’s written so vaguely as to be nearly humorous.

But as I wrote here on my personal blog about all of this, what does matter out of the generally irksome pol is that there is bipartisan interest in limiting the ability of big tech companies to buy smaller companies. For startups, that is not good news; M&A exits are critical liquidity events for startups, and big companies have the most money.

It’s no sauté of my onions if startup valuations fall, but I think there’s been plenty of attention noting that some Democrats and some Republicans in the U.S want to undercut top-down tech M&A, and not nearly enough notice concerning what the effort might do to startup valuations and funding. And if those metrics dip, there could be fewer upstarts in the market actually working to take on the giants.

Food for thought.

The Exchange caught up once again with Unity CFO Kim Jabal. We did so not merely to make jokes with her about games that we like or don’t like, but to keep tabs on how Jabal thinks as the financial head of a company that was private when she joined, and public now. A few observations:

And speaking of startups, let’s talk about a company that I’ve had my eye on that recently raised more capital: Deepgram. I covered the company’s Series A, a $12 million round in March 2020. Now it has raised $25 million more, led by Tiger, so this is a fun case of big money investing early-stage, I think. Regardless, Deepgram was a bet on a particular model for speech recognition, and, then, its market. its new investment implies that both wagers came out the right way up.

And I was chatting with the CEO of Databricks recently (more here on its latest megaround), who mentioned the huge gains made in AI, and more specifically around generative adversarial networks (GANs) NLP, and more. Our read is that we should expect to see more Deepgram-ish rounds in the future as AI and similar methods of approaching data make their way into workflows.

And fintech player Payoneer is going public. Via a SPAC. You can read the investor presentation here. Payoneer is not a pre-revenue firm going out via a blank check; it did an expected $346 million in 2020 rev. I’m bringing it to you for two reasons. One, read the deck, and then ask yourself why all SPAC decks are so ugly. I don’t get it. And then ask yourself why isn’t it pursuing a traditional IPO? Numbers are on pages 32 and 40. I can’t figure it out. Let me know if you have a take. Best response gets Elon’s dogecoin.

Wrapping up this week, TechCrunch has a new newsletter coming out on apps that is going to rule. Sarah Perez is writing it. You can sign up here, it’s free!

And if you need a new tune, you could do worse than this one. Have a great weekend!

Powered by WPeMatico

The recent Databricks funding round, a $1 billion investment at a $28 billion valuation, was one of the year’s most notable private investments so far.

For Databricks signaled its IPO readiness by disclosing to TechCrunch last year that it had scaled its revenue run rate from $200 million to $350 million in a year, so the new capital looked like the capstone on its private fundraising before an eventual public debut.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But I did have a few questions, starting with the price of the round.

At a $28 billion valuation and ARR of $425 million, Databricks is valued at around 66x top line. That’s steep, if not the highest number we can dredge up on the public markets. Of course, for Databricks shareholders, seeing the value of their stock rise so quickly is hardly a bad thing. They are hardly going to complain about having more paper wealth.

But what about the investor perspective? Does the price really make sense? The Exchange caught up with Battery Ventures’ Dharmesh Thakker earlier this week to discuss a number of things, one of which was Databricks’ round and pricing. Thakker is named in the Databricks Series D funding announcement, which brought Battery into the company.

What was surprising about our conversation was not that Thakker was bullish on Databricks — a company that he and his firm have backed since its $140 million, 2017 round when the company was worth just under $1 billion. What surprised me was that he thinks its new $28 billion valuation might be a little low.

What was surprising about our conversation was not that Thakker was bullish on Databricks — a company that he and his firm have backed since its $140 million, 2017 round when the company was worth just under $1 billion. What surprised me was that he thinks its new $28 billion valuation might be a little low.

Intriguing, yeah? So this morning for both of us, I’ve pulled out quotes from our chat to help explain how Thakker views the market for Databricks, unicorns at scale more broadly through the lens of risk-adjusted investing, and the scale of the market some unicorns are playing in.

At the close, we’ll remind ourselves what Databricks CEO Ali Ghodsi told TechCrunch when we asked him the same question. Let’s go!

Here’s how the valuation part of my chat with the Battery Ventures’ investor went down:

The Exchange: I want to talk about Databricks, because I spoke to [CEO] Ali [Ghodsi] yesterday about this round, and hot damn, it’s a lot of money at a valuation that is roughly 64x ARR, give or take. I don’t understand the price, and I know it’s a boring thing to talk about. [It’s a] great company, I get their market, I’ve talked to them a bunch, I know their revenue numbers. [But] I don’t understand the price, and I was hoping you could tell me why I’m being too conservative.

Dharmesh Thakker: I, for what it’s worth, think [the price] fair. If anything, I think it is on the lower end — he could have done better, frankly. But I think it comes down to three major things, right?

One is the addressable market. Just think about the addressable market of data. If there’s a trillion dollars spent in software or technology, I think you and I would be both hard pressed to say, almost all of that [isn’t] influenced by some data-oriented decisioning. Whether it’s digital transformation, whether it’s analytics, data is everywhere. So the TAM is massive … I think you and I both agree on that, whether it is $20 billion or $80 billion — it’s massive.

Powered by WPeMatico

This morning, investor and SPAC raconteur Chamath Palihapitiya announced two new blank-check deals involving Latch and Sunlight Financial.

Latch, an enterprise SaaS company that makes keyless-entry systems, has raised $152 million in private capital, according to Crunchbase. Sunlight Financial, which offers point-of-sale financing for residential solar systems, has raised north of $700 million in venture capital, private equity and debt.

We’re going to chat about the two transactions.

There’s no escaping SPACs for a bit, so if you are tired of watching blind pools rip private companies into the public markets, you are not going to have a very good next few months. Why? There are nearly 300 SPACs in the market today looking for deals, and many will find one.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Think of SPACs are increasingly hungry sharks. As a shark get hungrier while the clock winds down on its deal-making window, it may get less choosy about what it eats (take public). There are enough SPACs on the hunt today that they would be noisy even if they were not time-constrained investment vehicles. But as their timers tick, expect their deal-making to get all the more creative.

This brings us back to Chamath’s two deals. Are they more like the Bakkt SPAC, which led us to raise a few questions? Or more akin to the Talkspace SPAC, which we found pretty reasonable? Let’s find out.

Let’s start with the Latch deal.

New York-based Latch sells “LatchOS,” a hardware and software system that works in buildings where access and amenities matter. Latch’s hardware works with doors, sensors and internet connectivity.

The company has raised a number of private rounds, including a $126 million deal in August of 2019 that valued the company at $454.3 million on a post-money basis, according to PitchBook data. The company raised another $30 million in October of 2020, though its final private valuation is not known.

As Chamath tweeted this morning, Latch is merging with TS Innovation Acquisitions Corp, or $TSIA. The SPAC is associated with Tishman Speyer, a commercial real estate investor. You can see the synergies, as Latch’s products fit into the commercial real estate space.

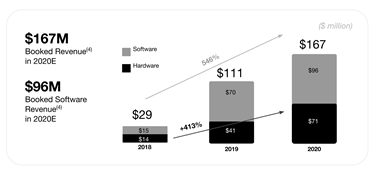

Up front, Latch is not a company that is only reporting future revenues. It has a history as an operating entity. Indeed, here’s its financial data per its investor presentation:

Image Credits: Latch

Doing some quick match, Latch grew booked revenues 50.5% from 2019 to 2020. Its booked software revenues grew 37.1%, while its booked hardware top line expanded over 70% during the same period.

That could be due to strong hardware installation fees, which could later result in software revenues; the company claims an average of a six-year software deal, so hardware revenues that are attached to new software incomes could low key declaim long-term SaaS revenues.

Update: Adding some clarity here, the above are “booked” revenues, which I’ve made more clear, not actual revenues. Its net revenues, better known as actual revenues, were $18 million, with $14 million of that coming from hardware. So, today, the company is certainly more hardware-heavy than I first thought. Damn non-S-1 filings!

While some were quick to note that the company is far from pure-SaaS — correct — I suspect that the model that could get some traction amongst investors is that this feels a bit like Peloton for real estate. How so? Peloton has large hardware incomes up front from new users, which convert to long-term subscription revenues. Latch may prove similar, albeit for a different customer base and market.

Per the deal’s reported terms, Latch will be worth $1.56 billion after the transaction. The combined entity will have $510 million in cash, including $190 million from a PIPE — a method of putting private money into a public entity — from “BlackRock, D1 Capital Partners, Durable Capital Partners LP, Fidelity Management & Research Company LLC, Chamath Palihapitiya, The Spruce House Partnership, Wellington Management, ArrowMark Partners, Avenir and Lux Capital.”

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Click here if you want it in your inbox every Saturday morning.

Ready? Let’s talk money, startups and spicy IPO rumors.

We’re shaking things up this weekend in the newsletter, focusing on a series of larger themes and news items instead of having a few discrete sections. Why? Because there was too much to fit into our usual format. If you were a fan of the original layout, we’ll be back to it next week.

Today we’re talking Coinbase’s growth, how Juked.gg tapped the equity crowdfunding market, a noodle or two on the a16z media game, Talkspace’s SPAC, VC and founder predictions for 2021, and where’s the right place to found a company.

Sound good? Let’s get into it!

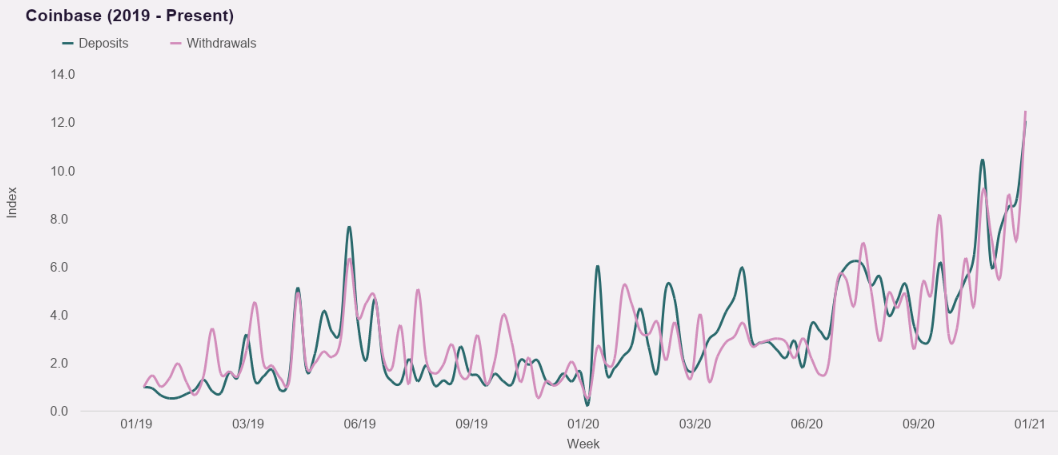

Thanks to Kazim Rizvi of Drop, parent company to Cardify which provides data on consumer spending, we have a look into how quickly deposits have scaled at American cryptocurrency platform Coinbase. As Coinbase has filed to go public, and we’re eagerly anticipating its eventual S-1 filing, we were stoked to get a directional look at how quickly consumer interest was growing for the assets it helps folks buy.

They are scaling rapidly. Using the first week of January 2019 as a baseline, by the last week of December 2020 deposits and withdrawals from Coinbase had grown by more than 12x apiece. That’s staggering growth, and while the data is somewhat volatile — and we’d treat it as directional instead of exact — on a week-to-week basis, it underscores how well companies like Coinbase may be performing as Bitcoin booms once again, bringing in more trading interest and consumer demand.

Via Cardify, Cardify data.

The Cardify data also indicates a multiplying of new customer acquisition at Coinbase over the same time period, and deposits scaling alongside the price of Bitcoin. As Bitcoin has topped the $30,000 mark recently, sharply higher than in recent quarters, the price gains may have helped Coinbase not only a solid Q4 2020, but perhaps put it on a path for a bonkers Q1 2021 as well.

If we were 10/10 excited about the Coinbase S-1 before this dataset, we’re now a heckin’ 12/10.

Esports is super cool and if you don’t agree, you are incorrect. But it doesn’t matter if you or I are right or not on the question, as the market has largely decided that competitive gaming is worth time, attention and investors’ money.

The proliferation of esports leagues and games and the like has led to a decidedly fragmented universe, however, lacking a central hub akin to what ESPN provides the world of traditional sports.

But not to worry, Juked.gg just raised capital to build a content hub for esports. This means that old folks like myself can still find out when tournaments are happening, and enjoy a dabble of League of Legends or Starcraft 2 pro play when we can, sans hunting around the internet for dates and times.

Juked.gg went through 500 Startups (more on its class here), catching our eye at the time as a neat nexus for esports-related content. Now flush with a little over $1 million that it raised on the Republic platform, it has big plans.

The Exchange spoke with Juked.gg’s co-founder and CEO Ben Goldhaber about his company’s performance to date. Per Goldhaber, Juked has scaled from 500 users when it launched in late 2019, to 50,000 in December of 2020. Ahead, Juked may invest more in journalism, more into social features, and more into user-generated content. We’ll have more on Juked as it gets its vision built, now powered by over a million dollars from 2,524 investors, each betting that the startup is building the right product to help unify a growing, if distributed, entertainment category.

To preserve our collective sanity, I’m not going to bang on at length here, but building out content at a VC firm is not new. Hell, how long ago did the First Round Review launch? What a16z appears to have in mind is different in scale, not substance. We chatted about it on Equity this week, in case you need more on the matter.

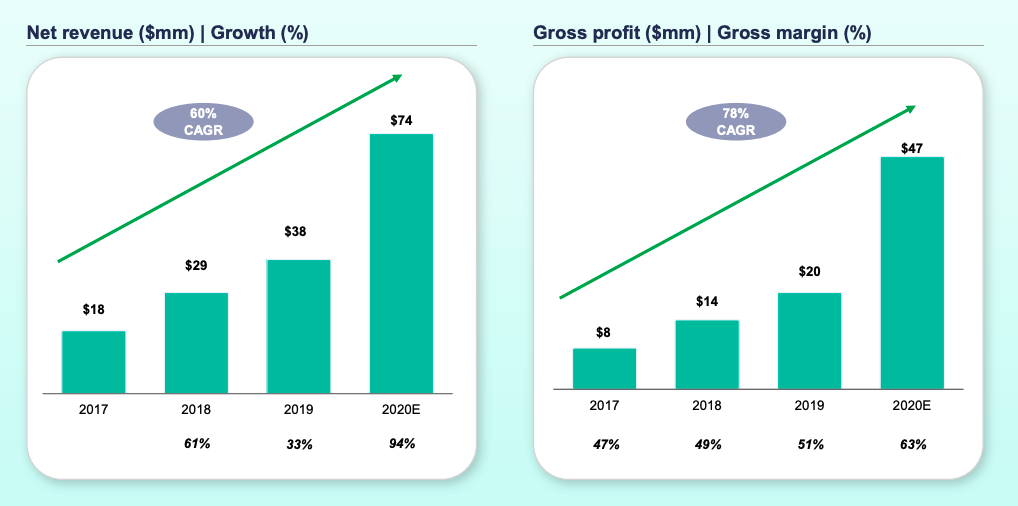

While it is enjoyable to mock SPACs, featuring as many do companies that are nascent to say the least, not all SPAC-led debuts are as silly as the rest. This is the case with the impending Talkspace deal, the deck for which you can read here.

What matters is this set of charts:

Look at that! Historical revenue growth! Improving gross margins! Rising gross profit!

You may argue that the company is not really worth an enterprise value of $1.4 billion that it will sport after its combination with Hudson Executive Investment Corp., but, hey, at least it’s a real business.

Seed VC NFX dropped a VC and founder survey the other day that I’ve been meaning to share with you. You can read the whole thing here, if you’d like.

I have two pull-outs for you this morning:

Initialized Capital put together some data on where founders think it is best to found a company. In 2020, nearly 42% of surveyed founders said the Bay Area. By 2021 that number had slipped to a little over 28%, with a plurality of 42% indicating that a distributed company is the best way to go.

I hear about this a lot from early-stage founders. They are often building what I call micro-multinationals, small companies that have a few employees in one country, and then a handful in others. Making that setup work is going to be a hotspot for HR software I reckon.

Regardless, the requirement of founding companies in the Bay Area is kaput. The advantages of founding there will linger much longer.

Coming up on The Exchange next week: The first entries of our new $50 million ARR series, featuring interviews with Assembly, SimpleNexus, Picsart, OwnBackup and others. And we have some $100 million ARR interviews in the can, as well.

Finally, to keep the The Powers That Be happy, The Exchange covered some neat stuff this week, including American VC results, fintech and unicorn venture capital, European and Asian venture capital results, how the IPO market is even more bonkers than you thought, and notes on what Qualtrics may be worth when it goes public.

Hugs, and let’s all get a nap in,

Powered by WPeMatico

The fourth quarter of 2020 was as busy as you imagined, with super-late-stage startups reaching new valuation thresholds at a record pace, and total venture capital funding in the United States recording its second-best result of all time.

That’s according to data released recently by CB Insights, which complements our look back at 2020’s venture capital year in America from yesterday.

At the time, we noted that American startups raised an average of $428 million each day last year, a sum that helps illustrate how rapid the private markets moved during the odd period.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But a peek at aggregate results for the world’s largest VC market provides only part of the picture. We need to narrow our lens and peer more deeply into standout categories to understand how the U.S. venture capital market managed to post its biggest year ever in terms of dollars invested, despite seeing deal volume slip for a second consecutive year.

This morning, we’re scraping data together to better understand.

This morning, we’re scraping data together to better understand.

First, we want to see how unicorns performed in Q4 2020. This column noted in late December that it felt like unicorn creation was rapid in the quarter; how did that hold up?

Then we’ll dig into PitchBook data concerning the fintech sector, a huge recipient of venture capital time, attention and money.

Fintech’s 2020 is a good perspective to view both the year and its wild final quarter. So this morning, as America itself resets, let’s take a moment to understand last year just a little bit better as we get into this new one.

One of the most curious things about the unicorn era is the rising bet it represents. I’ve written about this before so I will be brief: Nearly every quarter, the number of unicorns — private companies worth $1 billion or more — goes up.

The private market is able to create more unicorns than it has been historically able to exit them.

Some of these companies exit, sometimes in group fashion. But, quarter after quarter, the number of unexited unicorns rises. This means that the bet on expected future liquidity from venture capitalists and other private investors keeps ratcheting higher.

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Click here if you want it in your inbox every Saturday morning.

Ready? Let’s talk money, startups and spicy IPO rumors.

It was yet another week of startups that became unicorns going public, only to see their valuation soar. Already marked up by their IPO pricing, seeing so many unicorns achieve such rich public-market valuations made us wonder who was mispricing whom.

It’s a matter of taste, a semantic argument, a tempest in a teacup. What matters more is that precisely no one knows what anything is worth, and that’s making a lot of people rich and/or mad.

This is not a new theme. I’ve touched on it for years, but what matters for us today is that there appear to be three distinct valuation bands for companies, and the gaps between them do not appear ready to shrink. You could even argue that they have widened.

Band 1 is the private capital cohort. These are the folks who valued Affirm at $19.93 per share in its September 2020 round and Roblox at $4 billion in February of 2020. Now Affirm is worth $116.58 per share, and Roblox is worth $29.5 billion. Whoops?

Band 2 is the long-term public investing cohort. These are folks critical in the IPO pricing context. They are willing to pay more for startups than the private capital crew. Affirm was not worth under $20 per share to this group, instead it was worth $49 per share just a few months later. Whoops?

Band 3 is the retail cohort, the /r/WallStreetBets, meme-stock, fintech Twitter rabble that are both incredibly fun to watch and also the sort of person you wouldn’t loan $500 to while in Las Vegas. They are willing to pay nearly infinite money for certain stocks — like Tesla — and often far more than the more conservative public money. Demand from the retail squad can greatly amplify the value of a newly listed company by making the supply/demand curve utterly wonky. This is how you get Poshmark more than doubling a strong IPO valuation on its first day.

Most investors do well in today’s world. Though Band 1 likes to blame Band 2 for not being willing to pay Band 3 prices, it always sounds like the private capital folks are merely complaining about sharing some of the winnings with another party.

Regardless, who really knows what anything is worth? I was recently chatting with an early-stage founder who has a history of investing — narrowing it down to 17,823 people, I know — about the price of software companies both private and public and why they may or may not make sense. He said that old valuation models at banks presumed that software companies’ growth would go to zero over time, and that profits would be rare among SaaS concerns. Both concepts were wrong, so prices went up.

But I have yet to have anyone explain to me why companies that would have been valued at 10x next year’s revenues can now get, at median, 18.1x. I have a working theory of what’s going on, but none of it points to sanity, or pricing that is grokkable through a lens that isn’t hype.

(You can hit reply to this email and tell me why I am dumb if you’d like. I will buy the person with the best valuation explanation coffee when the world works again.)

On the milestone front, it was a huge week for leaving the private markets and joining the Big Kid Club. Namely for Affirm and Poshmark, which priced well and started to trade. And for Bumble, which filed to go public. They are targeting a good IPO window.

But there was lots more going on, including a milestone that caught my eye. M1 Finance, a fintech startup that brings together lots of pieces of the fintech playbook into a single service, reached $3 billion in assets under management (AUM) this week. The company had reached $2 billion in AUM last September, after reaching $1 billion in February of 2020.

Why do we care? The company previously told TechCrunch that it works to generate revenues worth around 1% of AUM. If that percentage has held past its October, 2020 Series C, the company just added around $10 million in ARR in under half a year. That’s a pace of revenue creation that made me sit up and take notice. (Shoutout Josh for never shutting up about the Midwest.)

But I really bring up the M1 Finance milestone for a different reason. Namely that I am consistently surprised at how deep certain markets are. Neobanks that are still growing; the OKR software market’s surprising depth; the ability of M1 to accrete deposits in a market with so many incumbents and well-funded startups.

Perhaps this is why prices make no sense; if you can’t see the edge limits of TAM, can anything be overpriced?

Moving on, some quick notes on things from the week that mattered:

Aziz Gilani, a managing director at Mercury Fund and an advocate of Texas (observe his Twitter handle), wrote in late regarding our query for investor notes on the Visa-Plaid breakup. You can read the rest here.

But who are we to deprive you of useful notes. And Gilani is a nice person. So, here are his $0.02:

My big take-away on the Plaid/Visa deal falling apart is about how fast everything in 2021 is moving. Arguably the biggest advantage of SPACs over direct listings and IPOs is how fast those liquidity events can get done. In a world in which valuation[s] change week to week, the delays created by the DOJ can kill a deal – even if the DOJ would eventually lose in court.

I’m philosophically super negative about the government imposing their will, but I’m also personally excited about the current wave of insurgent startups not getting gobbled up by the FAANGs of the world. For the last several years too many startups fell victim to the “quick exit” mentality personified by Mint selling so fast to Intuit. With fast/cheap capital freely available, today’s crop of startups are going big.

Worth chewing on.

What a week. I have only a few things left for you, including some early-stage rounds that I could not get thanks to waves arms around generally but wanted to flag all the same.

Hugs,

Powered by WPeMatico