The Exchange

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading.

Ready? Let’s talk money, startups and spicy IPO rumors.

The startup world could be in for a busy summer.

Today the economy is improving. Unemployment is falling, while interest rates are staying low. There’s lots of new capital on offer, and some expectation that we’ll get back to Q1’s IPO wave in Q3. Throw in widespread vaccinations and a return to something akin to our old lives, and the world of business could be ready to accelerate further in short order.

There are caveats, of course. Lots of folks are being left behind in the recovery. And vaccine hesitancy is as lethally stupid as it is surprisingly common. But anticipated summer economic conditions, strong markets and a general belief that the digital transformation’s acceleration will continue point to a coming hot(ter) period for tech.

That is good news for startups.

We’re already starting to see anticipatory reporting on the matter. Wired’s recent piece on venture capitalists telling startups to invest rapidly is worth reading. I’ll back it up by saying that it seems that most startups that I am chatting with every week had a solid-as-heck first quarter and aren’t worried about the second. If I am not accidentally speaking with only founders who are doing well and somehow missing legion startups that are struggling, it seems to be a pretty darn good time to build a tech company.

Plaid’s round from earlier this week underscores what I’m talking about. The API-powered consumer fintech company’s CEO Zach Perret told TechCrunch how much the digitization of the world of financial services had accelerated in the last year. Yep. Startups that would have done well in more normal times are often seeing their market move in their direction. Often rapidly. That’s why Plaid is worth north of $13 billion today, nearly triple what it was worth in early 2020.

For the startups doing well, there’s ample cash on offer. Ramp’s latest round, a two-in-one, makes that point plain. So, if the broader economy and its technological sector do accelerate, expect wallets to open even further. As the temperature heats up, so too could the business climate.

I mean, how else can you explain the Clubhouse news? Or the Topps news? TechCrunch had to cover the middle ground between baseball cards, NFTs and candy, for the love of all that is holy.

Next week The Exchange is digging into Q1 2021 venture capital numbers from around the world. We’ll see soon enough how big the start to the year was, but we have a guess.

Sticking to our theme of growth and a hot and warming climate for tech startups, a few more data points from the last week.

I caught up with the CEO of Kudo this week, a few days after his company announced a $21 million Series A round of funding. I covered the translation-as-a-service company last year when it raised a seed round. Per its chief executive Fardad Zabetian, the company had 14 employees last March. It now has 150 and has more than 50 open positions. That’s not the sort of growth you see off of merely a few capital raises. That’s growth.

Coinbase’s monster quarter highlights how some technology work from the past decade is maturing in a lucrative manner. The company’s epic revenue growth and nearly hilarious profitability are going to make its impending direct listing an even bigger event than I had expected. Get ready for that on the 14th. (More from the original Coinbase listing here.)

And then there’s Canva, which just repriced itself through a $71 million secondary transaction. The cloud design company is now worth $15 billion, up from around $6 billion last June, per Crunchbase data. Even more, the company announced a few growth metrics worth sharing:

And it’s not going public. Yes, you can laugh. I got the company to ask its CEO Melanie Perkins why that’s the case, and here’s what we got back:

There’s no rush for us. We’re profitable and we’re very fortunate that we can still find investors that align to our vision and values. I often say that we’re just one percent of the way there with Canva. We have a huge vision to empower every team to achieve its goals through visual communication. We’ve still got a whole lot more to achieve and so no immediate plans for any public listing- there’s simply no rush for us right now.

Let me just say that you don’t only have to go public when there’s a rush to do so! You can do so merely to make us, the reporting class, excited about going to work, as there are new numbers to read!

I was off for a bit of this week to recharge, so some news and notes you might have expected in the above missive may be missing. Rest assured that The Exchange is going to get bigger and better and more number-y and full of jokes when I get back. Someone is joining the little team, so we have big plans.

Hugs,

Powered by WPeMatico

It appears that the slowdown in tech debuts is not a complete freeze; despite concerning news regarding the IPO pipeline, some deals are chugging ahead. This morning, we’re adding Alkami Technology to a list that includes Coinbase’s impending direct listing and Robinhood’s expected IPO.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

We are playing catch-up, so let’s learn about Alkami and its software, dig into its backers and final private valuation, and pick apart its numbers before checking out its impending IPO valuation. After all, if Kaltura and others are going to hit the brakes, we must turn our attention to companies that are still putting the hammer down.

We are playing catch-up, so let’s learn about Alkami and its software, dig into its backers and final private valuation, and pick apart its numbers before checking out its impending IPO valuation. After all, if Kaltura and others are going to hit the brakes, we must turn our attention to companies that are still putting the hammer down.

Frankly, we should have known about Alkami’s IPO sooner. One of a rising number of large tech companies based in nontraditional areas, the bank-focused software company is based in Texas, despite having roots in Oklahoma. The company raised $385.2 million during its life, per Crunchbase data. That sum includes a September 2020 round worth $140 million that valued the company at $1.44 billion on a post-money basis, PitchBook reports.

So, into the latest SEC filing from the software unicorn we go!

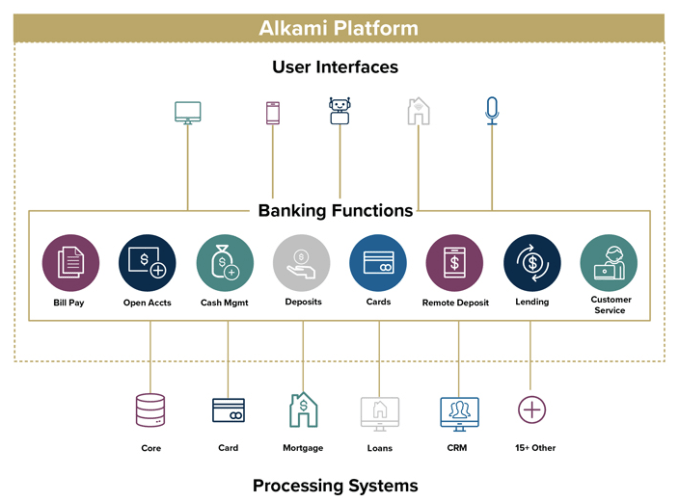

Alkami Technology is a software company that delivers its product to banks via the cloud, so it’s not a legacy player scraping together an IPO during boom times. Instead, it is the sort of company that we understand; it’s built on top of AWS and charges for its services on a recurring basis.

The company’s core market is all banks smaller than the largest, it appears, or what Alkami calls “community, regional and super-regional financial institutions.” Its service is a software layer that plugs into existing financial systems while also providing a number of user interface options.

In short, it takes a bank from its internal systems all the way to the end-user experience. Here’s how Alkami explained it in its S-1/A filing:

Image Credits: Alkami S-1

Simple enough!

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday? Sign up here.

Happy Saturday, everyone. I do hope that you are in good spirits and in good health. I am learning to nap, something that has become a requirement in my life after I realized that the news cycle is never going to slow down. And because my partner and I adopted a third dog who likes to get up early, please join me in making napping cool for adults, so that we can all rest up for Vaccine Summer. It’s nearly here.

On work topics, I have a few things for you today, all concerning data points that matter: Q1 2021 M&A data, March VC results from Africa, and some surprising (to me, at least) podcast numbers.

On the first, Dan Primack shared a few early first-quarter data points via Refinitiv that I wanted to pass along. Per the financial data firm, global M&A activity hit $1.3 trillion in Q1 2021, up 93% from Q1 2020. U.S. M&A activity reached an all-time high in the first quarter, as well. Why do we care? Because the data helps underscore just how hot the last three months have been.

I’m expecting venture capital data itself for the quarter to be similarly impressive. But as everyone is noting this week, there are some cracks appearing in the IPO market, as the second quarter begins that could make Q2 2021 a very different beast. Not that the venture capital world will slow, especially given that Tiger just reloaded to the tune of $6.7 billion.

On the venture capital topic, African-focused data firm Briter Bridges reports that “March alone saw over $280 million being deployed into tech companies operating across Africa,” driven in part by “Flutterwave’s whopping $170 million round at a $1 billion valuation.”

The data point matters as it marks the most active March that the African continent has seen in venture capital terms since at least 2017 — and I would guess ever. African startups tend to raise more capital in the second half of the year, so the March result is not an all-time record for a single month. But it’s bullish all the same, and helps feed our general sentiment that the first quarter’s venture capital results could be big.

And finally, Index Ventures’ Rex Woodbury tweeted some Edison data, namely that “80 million Americans (28% of the U.S. 12+ population) are weekly podcast listeners, +17% year-over-year.” The venture capitalist went on to add that “62% of the U.S. 12+ population (around 176 million people) are weekly online audio listeners.”

As we discussed on Equity this week, the non-music, streaming audio market is being bet on by a host of players in light of Clubhouse’s success as a breakout consumer social company in recent months. Undergirding the bets by Discord and Spotify and others are those data points. People love to listen to other humans talk. Far more than I would have imagined, as a music-first person.

How nice it is to be back in a time when consumer investing is neat. B2B is great but not everything can be enterprise SaaS. (Notably, however, it does appear that Clubhouse is struggling to hold onto its own hype.)

TechCrunch Early Stage was this week, which went rather well. But having an event to help put on did mean that I covered fewer rounds this week than I would have liked. So, here are two that I would have typed up if I had had the spare hours:

And two more rounds that you also might have missed that you should not. Holler raised $36 million in a Series B. Per our own Anthony Ha, “[y]ou may not know what conversational media is, but there’s a decent chance you’ve used Holler’s technology. For example, if you’ve added a sticker or a GIF to your Venmo payments, Holler actually manages the app’s search and suggestion experience around that media.”

I feel old.

And in case you are not paying enough attention to Latin American tech, this $150 million Uruguayan round should help set you straight.

Finally this week, some good news. If you’ve read The Exchange for any length of time, you’ve been forced to read me prattling on about the Bessemer cloud index, a basket of public software companies that I treat with oracular respect. Now there’s a new index on the market.

Meet the Lux Health + Tech Index. Per Lux Capital, it’s an “index of 57 publicly traded companies that together best represent the rapidly emerging Health + Tech investment theme.” Sure, this is branded to the extent that, akin to the Bessemer collection, it is tied to a particular focus of the backing venture capital firm. But what the new Lux index will do, as with the Bessemer collection, is track how a particular venture firm is itself tracking the public comps for their portfolio.

That’s a useful thing to have. More of this, please.

Powered by WPeMatico

The first quarter of 2021 was a busy season for technology exits. Coming off a hot period in the final quarter of 2020, it was no surprise that tech upstarts pursued liquidity through a variety of mechanisms as the new year began.

There were IPOs, there were direct listings, there were PE deals. Hell, we even saw enough SPACs that we lost track of a few; amid all the noise, you’ll miss the occasional note no matter how well-tuned your ear.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Each path is still open for later-stage startups to pursue exits: The IPO market was welcoming until a few minutes ago and private equity firms are stacked with cash and willing to pay higher multiples than they might in more normal times. And there are sufficient SPACs to take the entire recent Y Combinator class public.

Choosing which option is best from a buffet’s worth of possibilities is an interesting task for startup CEOs and their boards.

DigitalOcean went public via a traditional IPO, raising a slug of capital in the process. The SMB-focused public cloud company likely felt like a somewhat obvious IPO candidate when you read its results. The Exchange spoke with the company’s CEO, Yancey Spruill, about the choice.

DigitalOcean went public via a traditional IPO, raising a slug of capital in the process. The SMB-focused public cloud company likely felt like a somewhat obvious IPO candidate when you read its results. The Exchange spoke with the company’s CEO, Yancey Spruill, about the choice.

Latch, in contrast, decided that a SPAC was its best route out the gate. The Exchange caught up with the company’s CFO, Garth Mitchell, about the transaction and why it made sense for his company.

And, finally, The Exchange spoke with AlertMedia’s founder and CEO, Brian Cruver, about his decision to sell his Texas-based company to a private equity firm.

To prevent this post from reaching an astronomic word count, we’ll give a brief overview of each deal and then summarize the company’s views about why their liquidity choice was the right one.

Kicking off with DigitalOcean, a few notes: First, the company has been pretty darn public about its growth in the last few years. We knew that it had an annualized run rate of around $200 million in 2018, $250 million in 2019 and around $300 million in the first half of 2020. It later announced that it hit that mark in May of last year.

So when DigitalOcean decided to go public, we weren’t bowled over. The company wound up pricing at $47 per share, the high end of its range. Since then, its stock has struggled somewhat, falling below $37 per share before recovering to $43.80 at the end of trading yesterday.

Enough of all that. Why did the company choose to go public via a traditional IPO? Spruill said his company looked at SPAC deals and direct listings. It selected the IPO route because it fit the company’s goals of generating a broad base of shareholders while creating a branding opportunity.

The cost of an IPO is comparable, he added, to other exit options. Spruill also praised the IPO process itself, noting that its rigorous requirements made DigitalOcean a better company.

Earlier in our chat, I asked Spruill a question that I put to every CEO on IPO day: How are you feeling? It’s a bit of a sop, but it sometimes elicits insights from executives and founders who, after weeks of discussing their companies’ inner workings, are asked a rare personal question.

Spruill said he felt incredible and that nothing could replicate an IPO as the culmination of so much work put into building a company and its team. If you add up the wins and losses over time, with more of the former than the latter, and can cross the finish line with the right metrics and market, you can earn a spot to be “grilled” by the “best investors,” he said.

Those investors put $750 million or so into his company, Spruill added. Funds that it can use to retire debt and free up more cash flow. Not a bad day, I’d say.

Powered by WPeMatico

The Exchange just yesterday discussed a downward revision in the impending Compass IPO and the disappointing Deliveroo flotation as signals that market demand for high-growth, unprofitable tech shares could be slipping. Recent news underscores the possibly chilling conditions. This morning, Kaltura, a technology company that provides video streaming software and services, delayed its IPO. JioForMe reports that the postponement comes after Kaltura’s “valuation demand was lower than expected.”

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

TechCrunch noted yesterday that Kaltura had not released a second, higher IPO price range. The fact stood out given how hot the public markets had proven in recent months for new tech offerings. Kaltura’s S-1 filing detailed accelerating revenue growth, which at the time we thought would be more than enough to fetch the company an attractive initial public valuation.

It appears that Kaltura was also surprised that it was not trending toward a higher IPO price.

In another sign of how quickly the temperature for new tech flotations may have chilled, digital comms firm Intermedia Cloud Communications also delayed its IPO today. In a release, CEO Michael Gold said the decision is due “to challenging current conditions in the market for initial public offerings, especially for technology companies.”

In another sign of how quickly the temperature for new tech flotations may have chilled, digital comms firm Intermedia Cloud Communications also delayed its IPO today. In a release, CEO Michael Gold said the decision is due “to challenging current conditions in the market for initial public offerings, especially for technology companies.”

Challenging current conditions? For IPOs? For tech IPOs? That’s new.

Axios reporter Dan Primack noted this morning that SPAC formation appears to be slowing. Mix that into the delays and yesterday’s anemic-to-awful IPO news, and the market could be seeing a somewhat rapid retrenchment toward more historical valuations and demand levels for unprofitable equities.

Thinking out loud: We should expect SPAC formation and deal volume to fall the fastest of all the signals we’re tracking, including IPO pricing, the pace of S-1 filings and first-day trading performance. Why? Because it’s the most exotic of the various data points we’ve observed on the way up during the tech boom. Therefore, it should also be the thing most vulnerable to rising financial gravity.

Powered by WPeMatico

Substack didn’t invent the paid newsletter, but the startup’s early success with the model is enticing previous backers to more than double down on the media startup.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Last evening, Axios reported that Substack is “raising $65 million in new venture capital” at a valuation of “around $650 million.” As you’ve already guessed, Axios goes on to report that Andreessen Horowitz (a16z) will likely lead the investment.

That we’re seeing a16z pour more capital into what we could call the alt-media space is not a surprise. The investing group is ladling even more cash into its in-house media efforts and has put a small archipelago of capital into audio-based social media app Clubhouse. Its internal publishing schedule is in part an attempt to get around traditional media; the Clubhouse universe is an inverted one in which tech investors are celebrities, producers and gatekeepers. And Substack is a place where publications have bled some well-known talent, shifting the center of gravity in media.

You can detect the theme.

You can detect the theme.

Regardless, Substack’s new valuation and investment are eye-catching. This morning, I want to collect all that we can regarding Substack’s historical growth so that we can chew on its new valuation from the best vantage point. Let’s go!

A little history to kick us off. Crunchbase counts Substack’s total funding to date at $17.4 million. PitchBook puts the number at $21.21 million, inclusive of debt. Both sources agree that the company’s most recent round came in July 2019. PitchBook pegs the company’s valuation at $48.65 million at that date.

Raising $17 million in cash around 20 months ago, regardless of debt, is an amount of capital that the company could easily have burned through by now. Raising more funds is therefore not a surprise.

But the size of the new round is notable, as is its constituent valuation. Series A and B rounds have been growing in size in recent years. But a $65 million Series B would stand out, even by 2021 standards. Not shockingly so, but enough that any company raising that sum at its implied level of maturity would demand our attention. That we’re all familiar with Substack only makes the sum more curious.

Powered by WPeMatico

What happens to hot fintech startups that have benefited from a rise in consumer trading activity if regular folks lose interest in financial wagers?

That’s the question facing Robinhood, Coinbase and other trading platforms that have ridden an upward cycle. Each has performed well in recent quarters: Robinhood by securing huge payment-for-order-flow revenues, while Coinbase’s trading fees have proven incredibly lucrative, something we learned when it filed to go public.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

According to recent reporting, the consumer trading frenzy could be slowing: Bloomberg recently noted that options trading volume is slipping, Robinhood’s app store ranking is falling, and some alternative assets are also losing steam. Other reporting from the publication notes that many SPAC shares are underwater while Google trends data indicates falling consumer trading interest, perhaps limiting the inflow of new users for equities-focused apps.

There are other indications that the red-hot speculative consumer market is cooling. Bitcoin is off around 10% in the last week after a blistering rise in recent quarters. Hot stocks like Peloton, once a darling of traders, fell more than 10% yesterday alone.

But looking past price declines and other signals of market chop, volume itself at some well-known exchanges could be falling.

There’s a historical precedent for such declines. Coinbase’s historical revenues, to pick an example, have proved variable based on consumer interest in cryptocurrencies, with the company benefiting from rising demand and trading activity and seeing its top line decline in periods of restrained enthusiasm.

Robinhood and its fellow free trading apps have yet to undergo a similar rise-and-fall in trading volume, I’d reckon. At least of the sort of extreme up-and-down that Coinbase endured after the 2017-2018 bitcoin boom. Our question is, what would happen to Robinhood and its cohorts if the apparent cooling in consumer trading demand continues? Let’s talk about it.

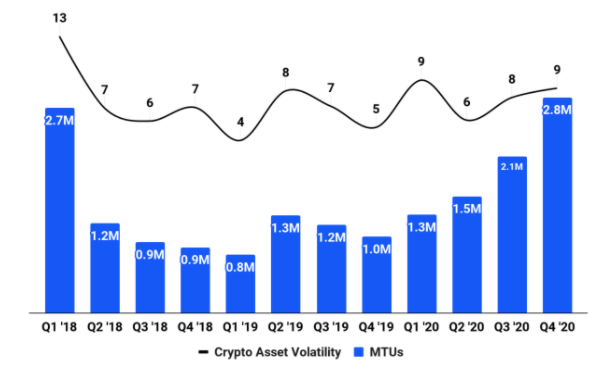

Coinbase was a famously lucrative organization during the 2017-2018 bitcoin boom.

Indeed, we can see from the following chart from its S-1 filing that the company’s monthly transacting users (MTUs) dropped sharply into 2018. The percentage decline from 2.7 million to 800,000 is just over 70%.

Image Credits: Coinbase

And in case you think we’re being rude, we have a related chart from the same SEC filing that shows trading volume falling over the same period, not merely MTUs. We’re not picking a loose proxy to merely infer that trading revenue dipped at Coinbase. We can show it:

Powered by WPeMatico

Covering YC Demo Day yesterday was good fun, but I missed a few items while watching several hundred startup pitches. A few years ago, these stories might have been the biggest news of the week.

But with the venture capital market redlining its engines while public markets remain sympathetic to growing, unprofitable companies, there’s lots going on. So, as a follow-up to our first late-stage roundup that we published yesterday morning, here’s another.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

This time we’re discussing IPO news from DigitalOcean (context), Kaltura (context), Robinhood (context) and Zymergen, and big rounds for Lattice and goPuff. That’s a lot to chew on, but I’ll be brief and to the point.

We’ll commence with the IPO news and then pivot into the late-stage rounds, just in case more drops this morning while we’re typing our way through yesterday’s news. Let’s go!

We’ll commence with the IPO news and then pivot into the late-stage rounds, just in case more drops this morning while we’re typing our way through yesterday’s news. Let’s go!

Today’s most pressing news is that DigitalOcean, a provider of cloud services to small businesses, priced its IPO at $47 per share last night. That was right at the top of its public-offering price range of $44 to $47. Before counting shares reserved for its underwriters, DigitalOcean is worth just under $5 billion.

And the company raised a gross $775.5 million in the offering, giving DigitalOcean a massive war chest to pursue its vision. As the company has proved increasingly unprofitable on a GAAP basis in recent years, the extra cash isn’t a problem: DigitalOcean plans to reduce its aggregate debt load with some of the proceeds, which will improve its profitability.

The company won’t trade for hours, so we’re done with DigitalOcean for now. File it in your mind as a win, as the company raised $50 million last year at a $1.1 billion valuation (PitchBook data). That’s a quick 5x.

Next up from the IPO treadmill is Kaltura, which released a first guess of its market value as a public company. Targeting $14 to $16 per share in its impending debut, the video software company is worth around $2 billion at the top end of its range, not counting shares reserved for its underwriting banks or other shares tied up in vested options and recruited stock units (RSUs).

Powered by WPeMatico

It’s demo day for the current Y Combinator class, so we’ll have a largely early-stage focus at TechCrunch today. But there’s also a host of late- and super-late-stage news this morning that matters.

Let’s get to all of it before we start to talk accelerators, overheated pre-seed valuations and the like.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

There are three things to discuss. First, the possible $10 billion exit of Discord to Microsoft. Discord is a well-financed unicorn that has raised oodles of capital and reportedly sports rapidly expanding revenues. Our goal will be to vet whether the price tag in question makes any sense, or if it is too low.

Second: Real estate tech company Compass has set an IPO price range we need to explore. Is its resulting valuation strong? Does it line up with its recent financial performance?

And, third, Intermedia Cloud Communications has priced its IPO. We’re behind on this entire debut, so we’ll take a second to riff on what the company does and what it is worth.

It’s a lot. But if we don’t get through it all now, we’ll fall behind and feel silly later. Let’s get to work!

Microsoft might be getting good at community, which is an odd thing to say about the enterprise software and cloud computing giant. The company’s Xbox gaming ecosystem has survived the test of time, Github is doing fine under Microsoft’s auspices, and Minecraft seems unharmed by Redmond’s stewardship.

That means gamers, developers and kids are all content to hang with Satya Nadella and company. Adding Discord to the mix might give Microsoft even more tooling to augment its existing communities, or perhaps tie them more closely together. But that’s all product news, which isn’t our remit. Let’s talk numbers.

The New York Times reported that Discord has “held deal talks with Microsoft for a transaction that could top $10 billion.” That figure has been widely reported, so we’ll use it for our work.

With a possible valuation in hand, we need revenue numbers to figure out if the possible sale price makes any sense. Happily, we have somewhat fresh numbers: The Wall Street Journal reported earlier this month that Discord “generated $130 million in revenue [in 2020], up from nearly $45 million in 2019.”

Powered by WPeMatico

A big story in the finance world this morning is that the Nasdaq composite index lost ground in pre-market trading while bond yields rose. The concern is that inflation could rise, which led to bonds selling off and falling valuations for expensive stocks. So, tech stocks were broadly lower this morning.

Unlike last night, when New York-based restaurant software company Olo priced its IPO at $25 per share, sharply above its raised IPO target price range.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Today, we’re checking in on the price investors paid for a block of Olo shares before it began trading. The resulting valuation and its new revenue multiples will help us answer several questions.

First, how hot is the market for high-growth tech shares that also feature profitability? And, second, is Olo pricing ahead of, or behind, known comps? If the latter is true, it could point to a cooling enthusiasm among public investors for tech IPOs, even if the headline numbers coming from the Olo IPO are impressive.

Then we’re going to chat about Coinbase’s latest S-1/A filing, which helps provide a bit of guidance regarding how its direct listing is scooting along.

Ready to get caught up on the public-private divide that the most successful startups cross? Let’s get into it!

As a quick reminder, Olo initially targeted a $16 to $18 per-share IPO price interval. That was raised, as expected, to $20 to $22 per share. Pricing at $25, then, is a strong 56.25% greater per-share value than the low end of the company’s first estimate.

As Olo featured rapid growth (an acceleration in year-over-year revenue from 59.4% in 2019 to 94.2% in 2020), and GAAP profits (a 2019-era net loss of $8.3 million became 2020 net income of $3.1 million) in its IPO filings, the first price range it rolled out felt a bit light. The second, however, felt more appropriate.

At $25 per share, we have to do new math. Using a simple share count inclusive of the company’s underwriters’ option, Olo is worth $3.62 billion. That figure swells to $4.6 billion when a fully diluted valuation is calculated, per IPO watch group Renaissance Capital.

Powered by WPeMatico