The Exchange

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to the working week. Are you ready to get our hands a little dirty this morning?

Good. We have an IPO to catch up on, one I should have kept up with in the past few weeks. Regardless, today we’re looking at Zeta Global’s latest IPO filing ahead of its eventual pricing.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Zeta Global is not a firm that I am very familiar with, but because Crunchbase notes that the New York-based startup has raised north of $600 million in private capital in the form of both equity financing and debt, it’s a unicorn worth understanding.

The gist is that Zeta ingests and crunches lots of data, helping its users market to their customers on a targeted basis throughout their individual buying lifecycles. In simpler terms, Zeta helps companies pitch customers in varied manners depending on their own characteristics.

You can imagine that, as the digital economy has grown, the sort of work Zeta Global supports has only expanded. So, has Zeta itself grown quickly? And does it have an attractive business profile? We want to know. We’ll also poke around its final private valuation so that we can see how much that number matches up — or doesn’t — to its recent financial results.

You can imagine that, as the digital economy has grown, the sort of work Zeta Global supports has only expanded. So, has Zeta itself grown quickly? And does it have an attractive business profile? We want to know. We’ll also poke around its final private valuation so that we can see how much that number matches up — or doesn’t — to its recent financial results.

Sound good? Let’s find out why Staley Capital, GCP Capital Partners, Franklin Square Group, GPI Capital and others backed the firm.

It can be useful to dissect a company’s marketing materials not just to see how well they describe themselves, but also to grok how they want to be perceived in the marketplace. Zeta is one such case.

Via its S-1 filings, here’s how it wants you to understand its business:

Zeta is a leading omnichannel data-driven cloud platform that provides enterprises with consumer intelligence and marketing automation software. We empower our customers to target, connect and engage consumers through software that delivers personalized marketing across all addressable channels, including email, social media, web, chat, connected TV (“CTV”) and video, among others.

If that didn’t make a lot of sense, it’s OK.

Powered by WPeMatico

While it would be nice to write about something other than yet another tech company looking to list via a SPAC, the deals keep dropping, so our more traditional fare of covering startup trends will remain on hold for at least one day more.

This morning, we’re looking at the Jam City deal to merge with DPCM Capital. Jam City is a bit like Zynga, but unless you are a mobile-gaming aficionado, you might not have heard of it.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

You likely have not heard of DPCM Capital, either, but you know more about it than you’d think.

As Jam City notes in a release, the SPAC is “led by Emil Michael.” Michael is most famous for his time at Uber, where he served as chief business officer. He left the firm, as The New York Times wrote in 2014, after a board-called “investigation into [the company’s] culture and business practices” led to a “recommendation for Mr. Michael to exit Uber.”

He’s the gentleman who floated the idea of funding a team to “dig up dirt” on Uber’s “critics in the media,” as BuzzFeed News reported in late 2014.

Regardless, we’re not here to go back through Uber and its various cultural messes. We’re here to dig into the Jam City SPAC deck to see if the company is similar to Zynga. Why do we want to know that? Because Zynga has done great in recent quarters, including posting record revenue and bookings in the first three months of 2021.

Regardless, we’re not here to go back through Uber and its various cultural messes. We’re here to dig into the Jam City SPAC deck to see if the company is similar to Zynga. Why do we want to know that? Because Zynga has done great in recent quarters, including posting record revenue and bookings in the first three months of 2021.

With lots of folks stuck at home in the last year, gaming has done well in aggregate. And mobile gaming is a huge chunk of the larger gaming world.

More broadly, why do we care about Jam City’s SPAC transaction? Because the mobile gaming concern has raised more than $300 million, including a $145 million round in 2019 that TechCrunch covered here.

The company attracted capital from Austin Ventures, Netmarble, Bank of America Merrill Lynch and JP Morgan Chase while private, per Crunchbase, so we’re very curious if Jam City has enjoyed a Zynga-like last few years and how it’s being valued as part of the SPAC deal. Let’s find out.

When Jam City raised that huge 2019 round, co-founder and CEO Chris DeWolfe said that the “global mobile games market [is] consolidating.” At the time, the company intended to use some of its new funding to acquire other mobile gaming companies.

Powered by WPeMatico

It’s Squarespace direct-listing day, and the SMB web hosting and design shop’s reference price has been set at $50 per share.

According to quick math from the IPO-watching group Renaissance Capital, Squarespace is worth $7.4 billion at that price, calculated using a fully diluted share count. The company’s new valuation is sharply under where Squarespace raised capital in March, when it added $300 million to its accounts at a $10 billion post-money valuation, according to Crunchbase data.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The company’s reference price, however, is just that: a reference. It doesn’t mean that much. As we’ve seen from other notable direct listings, a company’s opening price does not necessarily align with its formal reference price. Until Squarespace opens, whether it will be valued at a discount to its final private price is unclear.

While the benefits of a direct listing are understood, the post-listing performance for well-known direct listings is less obvious. Indeed, Coinbase is currently under its reference price after starting its life as a public company at a far-richer figure, and Spotify’s share price is middling at best compared to its 2018-era direct-listing reference price.

While the benefits of a direct listing are understood, the post-listing performance for well-known direct listings is less obvious. Indeed, Coinbase is currently under its reference price after starting its life as a public company at a far-richer figure, and Spotify’s share price is middling at best compared to its 2018-era direct-listing reference price.

This morning, we’re going over Squarespace’s recently disclosed Q2 and full-2021 guidance. Then we’ll ask how its expectations compare to its reference price-defined pre-trading valuation. Finally, we’ll set some stakes in the ground regarding historical direct-listing results and what we might expect from the company as it adds a third set of data to our quiver.

This will be lots of fun, so let’s get into the numbers!

Per Squarespace’s own reporting, it expects revenues between $186 million and $189 million in Q2 2021, which it calculates as a growth rate of between 24% and 26%. That pace of growth at its scale is perfectly acceptable for a company going public.

For all of 2021, Squarespace expects revenues of $764 million to $776 million, which works out to a very similar 23% to 25% growth rate.

In profit terms, Squarespace only shared its “non-GAAP unlevered free cash flow,” which is a technical thing I have no time to explain. But what matters is that the company expects some non-GAAP unlevered free cash flow in Q2 2021 ($10 million to $13 million), and lots more in all of 2021 ($100 million to $115 million).

Powered by WPeMatico

At long last, the Monday.com crew dropped an F-1 filing to go public in the United States. TechCrunch has long known that the company, which sells corporate productivity and communications software, has scaled north of $100 million in annual recurring revenue (ARR).

The countdown to its IPO filing — an F-1, because the company is based in Israel, rather than the S-1s filed by domestic companies — has been ticking for several quarters, so seeing Monday.com drop the document on this Monday morning was just good fun.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The Exchange has been riffling through the document since it came out, and we’ve picked up on a few things to explore. We’ll start by looking at the company’s revenue growth on a historical basis to see if it has accelerated in recent quarters thanks to the pandemic. Then, we’ll turn to profitability, cash burn, share-based compensation expenses and product vision.

We’ll wrap at the end with a summary of what we’ve learned and also make sure to check out the company’s marketing spend, because I’m sure you’ve seen its digital ads.

It’s a lot to chew through, so no more dilly-dallying. Into the numbers!

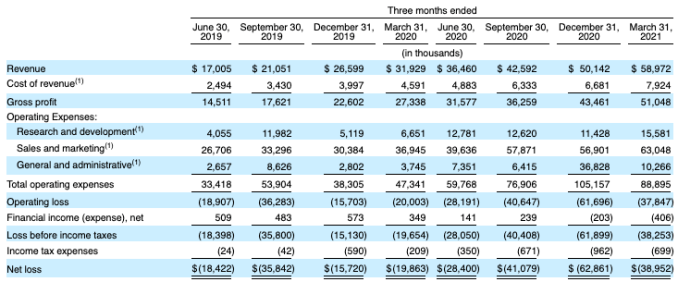

As always, we’re starting with revenue growth because it’s still the single most important thing about any venture-backed company.

This is great news for the startup, its employees and its investors. From 2019 to 2020, Monday.com grew its revenues from $78.1 million to $161.1 million, or 106%.

From Q1 2020 to Q1 2021, the company’s revenues grew from $31.9 million to $59 million. That’s about 85% growth. So, by what measure do we mean that the company’s revenue growth is accelerating? Its sequential-quarter revenue growth is picking up. Observe the following:

Image Credits: Monday.com F-1 filing

From Q2 2019 to Q3 2019, the company added around $4 million in revenue. From Q2 2020 to Q3 2020, that number was $6.1 million. More recently, the company’s revenue added $7.6 million from Q3 2020 to Q4 2020, which accelerated to $8.8 million from the final quarter of 2020 to the first quarter of 2021. Of course, from an ever-larger base, the company’s growth rate may decline. But the super clean and obvious expanding sequential revenue gains at the company are solid.

The fact that it added so much top line in recent quarters also helps explain why Monday.com is going public now. Sure, the markets are still near record highs and the pandemic is fading, but just look at that consistent growth! It’s investor catnip.

Powered by WPeMatico

After years in the backwaters of venture capital, edtech had a booming 2020. Not only did its products become must-haves after schools around the globe went remote, but investors also poured capital into leading projects. There was even some exit activity, with well-known edtech players like Coursera going public earlier this year.

But despite a rush of private capital — which has continued into this year, as we’ll demonstrate — edtech stocks have taken a hammering in recent weeks. So while venture capitalists and other startup investors are pumping more capital into the space in hopes of future outsize returns, the stock market is signaling that things might be heading in the other direction.

Who’s right? One investor that The Exchange spoke to noted that market turbulence is just that, and that he’s tuning into activity but not yet changing his investment strategy. At the same time, the recent volatility is worth tracking in case it’s a preview of edtech’s slowdown.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Let’s look at the changing value of edtech stocks in recent months, parse some preliminary data via PitchBook that provides a good feel for the directional momentum of edtech venture capital, and try to see if there’s irrational exuberance among private investors.

You could argue that it’s public investors who are suffering from irrational pessimism and that private-market investors have the right of it. But since public markets price private markets, we tend to listen to them. Let’s go!

We’re sure that you want to get into the private-market data, so we’ll be brief in describing the public-market carnage. What follows is a digest of edtech stocks and their declines from recent highs:

Powered by WPeMatico

As far as I can tell, low-code and no-code services are rapidly proving that prior models for products as broad as enterprise app creation and AI-powered data analytics were lackluster. My evidence? A mix of public- and private-market low- and no-code companies are putting up impressive results.

The Exchange caught up with Appian CEO Matt Calkins after his enterprise app software company reported its first-quarter performance to discuss the low-code market and what he’s hearing in customer meetings. To round out our general thesis — and shore up our somewhat bratty headline — we’ve compiled a list of recent low-code and no-code venture capital rounds, of which there are many.

As we’ll show, the pace at which venture capitalists are putting funds into companies that fall into our two categories is pretty damn rapid, which implies that they are doing well as a cohort. We can infer as much because it has become clear in recent quarters that while today’s private capital market is stupendous for some startups, it’s harder than you’d think for others.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The dividing factor? Signs of impressive present-day traction: Startups that are growing very fast have nearly unlimited access to capital, while those that are growing at merely fast rates are often finding it difficult to find a dance partner.

So if we can show that a huge, diverse set of no-code and low-code startups are raising oodles of capital, we can infer something relatively sturdy about market demand for their products. (It also doesn’t hurt that no-code automation service Zapier is growing like a weed and has reached IPO scale. In other news, Appian just dropped a new version of its low-code automation platform, for whatever that is worth.)

First Appian’s CEO, then a venture capital roundup. This should be fun.

Briefly, Appian reported $88.9 million in Q1 2021 revenue, of which $39.1 million came from its cloud subscription business. The latter figure rose 38% in the quarter compared to the year-ago period. Appian also swung to adjusted EBITDA profit in the period. Investors responded by hammering the company’s stock in the wake of the results. From an April share-price range in the mid-$130s, Appian is now trading in the mid-$80s, though only some of those declines came post-earnings.

But the company’s stock price is only so important. Precisely how conservative any one public company’s guidance is for the current year and how those forecasts play with investor expectations during a period of generally excessive valuations is not our game. What does matter is what the company’s CEO had to say about the low-code space itself.

Powered by WPeMatico

People have been discussing the importance of expanding opportunities for women in venture capital and startup entrepreneurship for decades. And for some time it appeared that progress was being made in building a more diverse and equitable environment.

The prospect of more women writing checks was viewed as a positive for female founders, a cohort that has struggled to attract more than a fraction of the funds that their male peers manage. All-female teams have an especially tough time raising capital compared to all-male teams, underscoring the disparity.

Then COVID-19 arrived and scrambled the venture and startup scene, creating a risk-off environment during the end of Q1 and the start of Q2 2020. Following that, the venture world went into overdrive as software sales became a safe harbor in the business world during uncertain economic times. And when it became clear that the vaunted digital transformation of businesses large and small was accelerating, more capital appeared.

But data indicate that the torrent of new capital has not been distributed equally — indeed, some of the progress that female founders made in recent years may have eroded.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

During a time of plenty, many female founders are still going without. The Exchange reached out to a number of American and European investors and founders to get their perspective on how today’s venture market treats female founders.

Recurring among the responses was a general view that more women venture capitalists would help lessen the gender gap in investments, and that VCs became more conservative due to COVID-19 and its constituent economic disruption, reverting to offering capital to repeat founders and their existing networks, both groups that are less diverse than the pool of new founders.

Our collection of founders and investors also said that women have been especially double-tasked during the pandemic to take on more domestic responsibilities in part due to sexist societal expectations, adding that that sexism more generally remains a problem that either isn’t improving or is improving too slowly.

But before we get into the core issues that prevent improvements in gender equity in venture funding, let’s check in on the data from last year and contrast it to its antecedents.

While there have already been reports on gender disparities in funding, Nokia-backed VC firm NGP Capital made a great contribution to research on the topic with its 2021 dossier.

Powered by WPeMatico

The public markets give, and the public markets take away. Earlier this morning, enterprise cloud storage and productivity company Box got into a more public spat with some of its shareholders upset with its performance and management decisions. But while Box endures the more difficult chapters of being a public company, other companies are racing to join the ranks of the listed concerns of the world.

If it feels like IPO news slowed for a few weeks at the start of the second quarter, your gut is correct. Investors previously told The Exchange that the first, third and fourth quarters of 2021 would be hot periods for public debuts, but that Q2 would be slower. Their argument revolved around reporting cadences and how long it takes for certain periods of accounting work to be completed.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

So we weren’t surprised when the second quarter’s IPO cycle began to feel a bit soft compared to the rapid-fire first quarter. And, as we’ve all heard in recent days, the great SPAC rush is slowing.

But that hasn’t stopped a number of firms from defying expectations and going public all the same. Online hosting and website builder Squarespace has not only filed but filled in its public filing with notes on its anticipated direct listing. We have to talk about its choice to list directly in light of new financial information we have concerning its recent performance.

But there’s more: Expensify filed to go public yesterday, albeit privately. And the SmartRent SPAC combination, though now slightly dated, is also worth a moment of our time.

But there’s more: Expensify filed to go public yesterday, albeit privately. And the SmartRent SPAC combination, though now slightly dated, is also worth a moment of our time.

The final element in the current IPO landscape is the recent Darktrace IPO in the United Kingdom, which, after that market had a rough start to its tech IPO calendar, is now seeing better results. So, let’s discuss IPOs to fully understand where we stand today in the realm of unicorn liquidity.

When The Exchange first dug into Squarespace’s IPO filing, we did our best to parse its full-year results because we lacked its quarterly details. This leaves us with two things to chew on: Why is Squarespace pursuing a direct listing over another listing technique, and what can its current and more granular operating results tell us about the choice?

On the first count, if Squarespace is direct listing, we can presume that it doesn’t need more cash to operate. So, how much cash does the company have on hand? A good chunk of change: $183.3 million.

Powered by WPeMatico

It’s a big morning for fintech startups today: Flywire, a Boston-based magnet for venture capital, has filed to go public.

Flywire is a global payments company that attracted more than $300 million as a startup, according to Crunchbase, most recently raising a $60 million Series F last month. We don’t have its most recent valuation, but PitchBook data indicates that the company’s February 2020, $120 million round valued Flywire at $1 billion on a post-money basis.

So what we’re looking at here is a fintech unicorn IPO. A great way to kick off the week, to be honest, though I’d thought that Robinhood would be the next such debut.

Fintech venture capital activity has been hot lately, which makes the Flywire IPO interesting. Its success or failure could dictate the pace of fintech exits and fintech startup valuations in general, so we have to care about it.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Regardless, we’re doing our regular work this morning. First, what does Flywire do and with whom does it compete? Then, a closer look at its financial results as we hope to get our hands around its revenue quality, aggregate economics and growth prospects.

After that, we’ll discuss valuations and which venture capital groups are set to do well in its flotation. The company had a number of backers, but Spark Capital, Temasek, F-Prime Capital and Bain Capital Ventures made the major shareholder list, along with Goldman Sachs. So, a number of firms and funds are hoping for a big Flywire exit. Let’s dig in.

Flywire is a global payments company. Or, as it states in its S-1 filing, it’s “a leading global payments enablement and software company.” And it thinks that its market, and by extension itself, has lots of room to grow. While “substantial strides [have been] made in payments technology in the retail and e-commerce industries,” the company wrote, “massive sectors of our global economy—including education, healthcare, travel, and business-to-business, or B2B, payments—are still in the early stages of digital transformation.”

That’s the same logic behind Stripe’s epic valuation and the rising value of payments-focused companies like Finix.

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. If you want it in your inbox every Saturday morning, sign up here. Ready? Let’s talk money, startups and spicy IPO rumors.

TechCrunch isn’t a public-market-focused publication. We care about startups. But public tech companies can, at times, provide interesting insights into how the broader technology market is performing. So we pay what we might call minimum-viable attention to former startups that made it all the way to an IPO.

Then there are the Big Tech companies. In the United States the list is well-known: Facebook, Alphabet, Microsoft, Apple and Amazon. And, in a series of results that could indicate a hot market for startup growth, they had a smashingly good first quarter of 2021. You can read our notes on their results here and here, but that’s just part of the story.

Yes, the Big Tech financial results were good — as they have been for some time — but lost amid the usual earnings deluge of numbers is how shockingly accretive Big Tech’s recent performances have proven for their valuations.

Microsoft fell as low as the $135 per-share range last March. Today it’s worth $252 and change. Alphabet traded down to around $1,070 per share. Today the search giant is worth $2,410 per share.

The result of the huge share-price appreciation is that Apple is now worth $2.21 trillion, Microsoft $1.88 trillion, Amazon $1.76 trillion, Alphabet $1.60 trillion and Facebook $0.93 trillion. That’s around $8.4 trillion for the five companies.

Back in July of 2017, I wrote a piece noting that their aggregate value had reached the $3 trillion mark. That became $4 trillion in mid-2018. And then in the next three years or so it more than doubled again.

Why?

Myles Udland, a reporter at our sister publication Yahoo Finance, has at least part of the puzzle in a piece he wrote this week. Here’s Udland:

And while it seems that almost every earnings story has sort of followed this same arc, data also confirms that this is not just our imagination: corporate earnings have never been this far out of line with expectations.

Data out of the team at Refinitiv published Thursday showed the rate at which companies were beating estimates and the magnitude by which they were beating expectations through Thursday morning’s results were the best on record.

So earnings are beating the street’s guesses more frequently, and at a higher differential, than ever? That makes recent stock-market appreciation less worrisome, I suppose. And it helps explain why startups have been able to raise so much capital lately in the United States, as they have in Europe, and why private-market investors are pouring so much capital into fintech startups. And it’s probably why Zomato is going public and why we’re still waiting for the Robinhood debut.

This is what a market feels like when the underlying businesses are firing on all cylinders, it appears. Just don’t forget that no business cycle is unending, and no boom is forever.

Extending The Exchange’s recent reporting regarding fintech funding, and our roundup from last week of insurtech startup rounds, a few more notes on the latter startup niche, which can be broadly viewed as part of the larger financial technology world.

This time we’ll hear from Accel’s John Locke regarding his investments in The Zebra — which recently raised even more capital — and the insurtech space more broadly.

Asked why insurtech marketplaces like The Zebra have been able to raise so very much money in the last year, Locke said that it’s a mix of “insurance carriers […] finally embracing marketplaces and willing to design integrated consumer experiences with marketplaces,” along with more consumer “comparison shopping” and, finally, growth and revenue quality.

The Zebra, Locke said, is “still growing north of 100% at ~$120M+ revenue run-rate.” That means it can go public whenever it wants.

But on that matter, there has been some weakness in the stock market for some public insurtech companies. Is Locke worried about that? He’s neutral-to-positive, saying that his firm does not “think all the companies in the market will work but still thinks ‘insurtechs’ will take market share from incumbents over the next decade.” Fair enough.

And Accel is still considering more deals in the space, as are others. Locke said that the venture market for insurtech investments is “definitely more aggressive” this year than last.

Closing today, a few notes on things that we didn’t get to that matter:

A long, weird week. Make sure to follow the second denizen of The Exchange’s writing team: Anna Heim. Okay! Chat next week!

Powered by WPeMatico