The Exchange

Auto Added by WPeMatico

Auto Added by WPeMatico

Shares of Square are up this morning after the company announced its second-quarter earnings and that it will buy Afterpay, an Australian buy now, pay later (BNPL) player in a $29 billion deal. As TechCrunch reported this morning, Afterpay shareholders will receive 0.375 shares of Square in exchange for their existing equity.

Shares of Afterpay are sharply higher after the deal was announced thanks to its implied premium, while shares of Square are up 7% in early-morning trading.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Over the past year, we’ve written extensively about the BNPL market, usually from the perspective of earnings from companies in the space. Afterpay has been a key data source, along with the yet-private Klarna and U.S. public BNPL outfit Affirm. Recall that each company has posted strong growth in recent periods, with the United States arising as a prime competitive market.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

From that landscape, let’s explore the Square-Afterpay deal. We want to know what Afterpay brings to Square in terms of revenue, growth and reach. We also want to do some math on the price Square is willing to pay for the company — and what that might tell us about the value of BNPL and fintech revenues more broadly. Then we’ll eyeball the numbers and try to decide if Square is overpaying for Afterpay.

As with most major deals these days, Square and Afterpay released an investor presentation detailing their argument in favor of their combination. Let’s dig through it.

Square is a two-part company. It has a large consumer business via Cash App, and it has a large business division that offers payments tech and other fintech services to corporate customers. Recall that Square is also building out banking services for its business customers and that Cash App also serves some banking and investing functionality for consumers.

Powered by WPeMatico

Robinhood priced at $38 per share this week, opened flat and closed its first day’s trading yesterday worth $34.82 per share, or a bit more than 8% underwater. The company posted a mixed picture today, falling early before recovering to breakeven in late-morning trading.

It wasn’t the debut that some expected Robinhood to have.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

To close out the week, we’re not going to noodle on banned Chinese IPOs or do a full-week mega-round discussion. Instead, let’s parse some notes from a chat The Exchange had with Robinhood’s CFO about his company’s IPO and go over a few reasonable guesses as to why we’re not wondering how much money Robinhood left on the table by pricing its public offering lower than it closed on its first day.

Let’s not be dicks about it. The time for Twitter jokes was yesterday. We’ll put our thinking caps on this morning.

Let’s not be dicks about it. The time for Twitter jokes was yesterday. We’ll put our thinking caps on this morning.

Chatting with Robinhood CFO Jason Warnick earlier this week, we wanted to know why this was the right time for Robinhood to go public.

Now, no public company CEO or CFO will come out and directly say that they are going public because they think that they can defend — or extend — their most recent private valuation thanks to current market conditions.

Instead, execs on IPO day tend to deflect the question, pivoting to a well-oiled bon mot about how their public offering is a mere milestone on their company’s long-term trajectory. For some reason in our capitalist society, during an arch-capitalist event, by a for-profit company, leaders find it critical to downplay their IPO’s importance.1

With that in mind, Warnick did not say Robinhood went public because the IPO market has recently rewarded big-brand consumer tech companies like Airbnb and DoorDash with strong debuts. And he didn’t say that with tech shares near all-time highs and a taste for high-growth concerns, the company was likely set to enter a market that would be willing to price it at a valuation that it found attractive.

Powered by WPeMatico

The Exchange spent a little time on Friday ruminating on the impact of then-rumored regulation in China targeting its edtech sector. News that the Chinese government intended to crack down further on the education technology market hit shares of public, China-based edtech companies. It was a mess.

Then over the weekend, the rumors became reality, and the impact is still being felt today in the global markets.

But there’s more. China is also bringing new regulatory pressure on food-delivery companies and Tencent Music. More precisely, we’ve seen successive market-dynamic-changing moves from the Chinese government in the last few days, coming as 2021 had already proved to be a turbulent environment for China-based technology companies.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Today we have to do a little bit of work to understand precisely what is going on with the various regulatory changes. Why? Because the Chinese venture capital market is a key player in the global venture scene. And Chinese startups have gone public on both Chinese, Hong Kong and U.S. exchanges; there’s a lot of capital tied up in companies impacted today — and possibly tomorrow.

For startups, the regulatory changes aren’t a death blow; indeed, many Chinese tech startups won’t be affected by what we’ve seen thus far. And upstart tech companies in sectors less likely to be targeted by central authorities may become more attractive to investors than they were before the regulatory onslaught kicked off. But on the whole, it feels like the risk profile of doing business in China has risen. That could curb the pace at which capital is invested, cut valuations and lower interest in the Chinese startup market from private-market investors able to invest globally.

Let’s parse what’s changed, examine market reactions and then consider what could be next. We want to better understand today’s Chinese startup market and what its new form could mean for existing players and future performance.

The edtech clampdown did not start last week. China’s edtech sector started to rack up penalties and fines in June, which led to what the Asia Times called “warning bells” in the sector. From there, things went from penalties to punishing regulatory changes.

Powered by WPeMatico

News that China’s government may force domestic tutoring-focused companies to go nonprofit is taking a huge bite out of the value of several technology companies. Bloomberg notes that the value of companies like New Oriental Education & Technology Group and TAL Education are tumbling in light of the news, which would constitute merely the latest salvo against tech companies in the autocratic country.

New Oriental’s Hong Kong-listed shares fell 44.22% in after-hours trading after the nonprofit news broke, while NYSE-shares of TAL are off an even sharper 51.75% in pre-market trading. With Yahoo Finance listing a roughly $13.8 billion market cap for TAL ahead of its impending declines at the market open, billions of equity value are about to get deleted. The list goes on: China Online Education Group is off 39.97% in after-hours trading, for example.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

A new decision by China’s government to exert more control over a sector of its domestic economy should not surprise. And we shouldn’t be shocked that online tutoring is in the country’s targets; today’s news is a follow-up to prior regulatory action in the sector from earlier in the year.

As China has become synonymous with edtech startups in recent years, the news impacts more than just public companies. The expected rules change may also hit a host of private, venture-backed companies.

For example, what will happen to Yuanfudao? The company was valued at $15.5 billion last year, offering what TechCrunch described as “live tutoring, an online Q&A arm and a math-problem-checking arm.” Will the company see its wings clipped?

Or how about Zuoyebang, which raised $1.6 billion in a single round last year? TechCrunch wrote that Zuoyebang offers “online courses, live lessons and homework help for kindergarten to 12th grade students.” Is it in trouble as well?

All this comes on the same day that shares in Zomato began to float, with the Indian online food delivery company seeing its shares close up nearly 65% in their first day’s trading. TechCrunch has viewed the Zomato IPO as a possible bellwether for the larger Indian startup market, and the results augur well for other growth-focused, loss-making unicorns in the country.

Powered by WPeMatico

Is the trading boom of 2020 and 2021 slowing?

That’s a question The Exchange has had on its mind since Robinhood released its latest IPO filing. The popular U.S. consumer-focused investing app told investors in the document that it expects revenues to decline in the third quarter compared to its Q2 performance. The company highlighted historically strong crypto volumes in preceding quarters as part of the reason for its anticipated revenue decline.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Naturally, we got to thinking about Coinbase.

It’s likely fair to say that Coinbase and Robinhood are bullish enough about the cryptocurrency market to be unbothered by short-term changes to crypto trading volumes. Coinbase discussed rising and falling consumer interest in trading cryptos in its own IPO filings, for example.

The now-public unicorn has lived through crypto ups and crypto downs. A decline in consumer interest in the next few months or quarters is not a huge deal, assuming one keeps a long enough perspective and the crypto-infused future that its fans expect comes to pass.

The boom in crypto demand among U.S. consumers lifted many a boat in recent quarters. Coinbase posted insanely good early-2021 results thanks to a bull run in cryptocurrency prices that drove retail interest and trading fees. Robinhood also saw a rush of crypto demand, something that TechCrunch explored here. And Square itself has seen crypto revenues explode.

The boom in crypto demand among U.S. consumers lifted many a boat in recent quarters. Coinbase posted insanely good early-2021 results thanks to a bull run in cryptocurrency prices that drove retail interest and trading fees. Robinhood also saw a rush of crypto demand, something that TechCrunch explored here. And Square itself has seen crypto revenues explode.

Sure, equities interest and demand for options also elevated the fortune of many consumer fintechs during the COVID-19 savings and investing boom. But crypto revenues had a big part to play. Let’s examine both situations through the lens of the latest from Robinhood.

There are some 316 mentions of “cryptocurrency” in Robinhood’s latest IPO filing. We’re going to stick to those we consider the most important.

As context, Robinhood shared preliminary Q2 data. We discussed it here if you want to go deeper into the aggregate figures. But after its disclosure of hard numbers, Robinhood had some interesting notes about the current quarter (emphasis TechCrunch):

Trading activity was particularly high during the first two months of the 2021 period, returning to levels more in line with prior periods during the last few weeks of the quarter ended June 30, 2021, and remained at similar levels into the early part of the third quarter. We expect our revenue for the three months ending September 30, 2021 to be lower, as compared to the three months ended June 30, 2021, as a result of decreased levels of trading activity relative to the record highs in trading activity, particularly in cryptocurrencies, during the three months ended June 30, 2021, and expected seasonality.

And in a discussion of some other performance metrics, including funded accounts and the like, Robinhood had this to say (emphasis TechCrunch):

We anticipate the rate of growth in these Key Performance Metrics will be lower for the period ended September 30, 2021, as compared to the three months ended June 30, 2021, due to the exceptionally strong interest in trading, particularly in cryptocurrencies, we experienced in the three months ended June 30, 2021, and seasonality in overall trading activities.

Falling revenue and slowing KPM growth is not really the world’s best set of metrics to flash up during an IPO run. But a quick scan of Robinhood’s 2020 revenues indicates it’s unlikely that the unicorn will be able to post year-over-year growth in the final two quarters of 2021. Still, its period of rapid-fire revenue growth appears to have come to an end after Robinhood posted top-line expansion in every quarter since Q4 2019.

Powered by WPeMatico

In case you’ve not been paying attention, we’ll say it again: The global venture capital industry is on fire. The second quarter of 2021 was the largest single three-month period on record for dollars invested.

The data coming in points to a worldwide boom. The United States’ startup market had a huge Q2, and investors don’t expect the pace to slow in the country. Europe is also having one hell of a year. Around the world, 2021 is shaping up to be a breakout year for venture investment into startups. And that’s after several years of growing, record-breaking results.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

India is another good example of this trend. The country’s venture capital haul thus far in 2021 has nearly matched its 2020 total and is on pace for a record year. But as the third quarter gets underway, something perhaps even more important is going on: public-market liquidity.

The new trend is being spearheaded by Zomato, an Indian food delivery giant that could be valued at $8.6 billion in its public debut. Other major Indian unicorns are following it to the public markets, including fintech players like MobiKwik and Paytm, which is backed by Alibaba and its affiliate Ant Financial. The trio of companies could herald a rush of public offerings from Indian companies if their debuts prove lucrative and stable.

Today, The Exchange is taking a look at India’s recent venture capital results and digging more deeply into the country’s IPO pipeline, with help from VCs Kunal Bajaj of Blume Ventures and Manish Singhal of pi Ventures. We’ll also read the tea leaves when it comes to how Zomato’s IPO is performing thus far, and what we can learn from its early data. This will be fun!

Powered by WPeMatico

News broke this morning that Revolut, a U.K.-based consumer fintech player, raised a Series E round of funding worth $800 million at a valuation of $33 billion. Those figures are breathtaking not only due to their sheer scale, but also thanks to their radical divergence from Revolut’s preceding funding event.

At times, The Exchange, TechCrunch’s markets-and-startups column, runs into two topics worth exploring in a single day. Today is such a day. You can check out our earlier notes on the buy now, pay later startup market and Apple’s entrance into the BNPL space here. Now, let’s talk about neobanks.

As TechCrunch’s Ingrid Lunden wrote earlier today concerning the news:

This latest Series E is being co-led by Softbank Vision Fund 2 and Tiger Global, who appear to be the only backers in this round. It comes on the heels of rumors earlier this month Revolut was raising big. Revolut last raised about a year ago, when it closed out a Series D at $580 million, but what is stunning is how much its valuation has changed since then, growing 6x (it was $5.5 billion last year).

Stunning indeed.

Lunden also went on to report on the company’s changing financial picture based on Revolut’s recently released 2020 results. In this entry, we’re digging more deeply into those financial results and usage metrics detailed by the fintech megacorn.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The picture that emerges is one of a company with a rapidly improving financial image, albeit with some blank spaces regarding recent customer growth.

Powered by WPeMatico

In the wake of Coinbase’s direct listing earlier this year, other crypto companies may be looking to go public sooner than later. That appears to be the case with Circle, a Boston-based technology company that provides API-delivered financial services and a stablecoin.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Circle will not direct list or pursue a traditional IPO. Instead, the company is combining with Concord Acquisition Corp., a SPAC, or blank-check company. The transaction values the crypto shop at an enterprise value of $4.5 billion and an equity value of around $5.4 billion.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

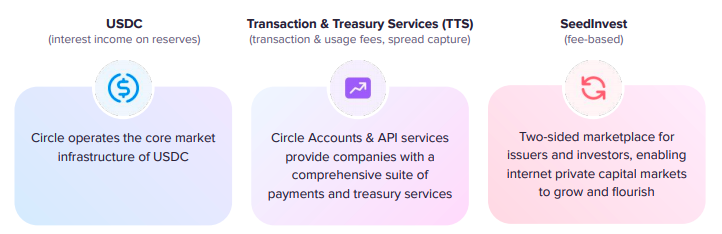

Circle’s SPAC presentation details a company whose core business deals with a stablecoin — a crypto asset pegged to an external currency, in this case, the U.S. dollar — and a set of APIs that provide crypto-powered financial services to other companies. It also owns SeedInvest, an equity crowdfunding platform, though Circle appears to generate the bulk of its anticipated revenues from its other businesses.

For more on the deal itself, TechCrunch’s Romain Dillet has a piece focused on the transaction. Here, we’ll dig into the company’s investor presentation, talk about its business model, and riff on its historical and anticipated results and valuation multiples.

In short, we get to have a little fun. Let’s begin.

As noted above, Circle has three main business operations. Here’s how it describes them in its deck:

Image Credits: Circle investor presentation

Let’s consider each one, starting with USDC.

Stablecoins have become popular in recent quarters. Because they are pegged to an external currency, they operate as an interesting form of cash inside the crypto world. If you want to have on-chain buying power, but don’t want to have all your value stored in more volatile, and tax-inducing, cryptos that you might have to sell to buy anything else, stablecoins can operate as a more stable sort of liquid currency. They can combine the stability of the U.S. dollar, say, and the crypto world’s interesting financial web.

Powered by WPeMatico

Shares of Chinese ride-hailing business Didi are off 22% this morning after the company was hit by more regulatory activity over the holiday weekend. The recently public company traded as high as $18.01 per share since it held an IPO last week; today, shares of Didi are worth just $12.09, off around a third from their 52-week high.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The decline in value follows a review by a Chinese cybersecurity agency that led to Didi being unable to onboard new users, a decision that arrived as last week rolled to a close.

Over the weekend, Didi was hit with more regulatory action. This time, the Cyberspace Administration of China said, via an internet translation, that “after testing and verification, the ‘Didi Travel’ App [was found to have] serious violations of laws and regulations in collecting and using personal information,” which led the agency to command app stores “to remove the ‘Didi Travel’ app, and required [the company] to strictly follow the legal requirements and refer to relevant national standards to seriously rectify existing problems.”

Over the weekend, Didi was hit with more regulatory action. This time, the Cyberspace Administration of China said, via an internet translation, that “after testing and verification, the ‘Didi Travel’ App [was found to have] serious violations of laws and regulations in collecting and using personal information,” which led the agency to command app stores “to remove the ‘Didi Travel’ app, and required [the company] to strictly follow the legal requirements and refer to relevant national standards to seriously rectify existing problems.”

Being yanked from relevant app stores was enough for Didi to alert investors that its mobile app “had the problem of collecting personal information in violation of relevant PRC laws and regulations.” Didi said that the change in its app availability “may have an adverse impact on its revenue in China.”

Understatement of the year, I reckon.

But there’s more going on than what Didi is enduring. As CNBC reported:

Powered by WPeMatico

Shares of Chinese ride-hailing provider Didi are sharply lower this morning after news broke that its domestic regulators are investigating the newly public company. A loose translation of the probe’s official notice indicates that the cybersecurity review is “in order to prevent national data security risks, maintain national security and protect the public interest.”

Yesterday, regulators ordered Didi to stop registering new users during the investigation.

The move comes amid a larger reset of relations between China’s burgeoning technology sector and its autocratic government. Other fallouts from the campaign included the effective silencing of Jack Ma, the embarrassing cancellation of the Ant IPO and a crackdown on data collection from technology companies more broadly.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

China is not the only nation grappling with its technology sector; India has made consistent noise in recent months regarding tech firms inside its borders, for example. And there is effort inside the U.S. Congress to put some cap on Big Tech’s scale and power, though of the trio, the United States appears the least likely to take a real swipe at technology companies’ market influence.

That Didi has run afoul of China’s regulatory bodies is not a surprise; it’s a well-known tech company in the country with lots of consumer data. Similar data-rich tech shops in the country have come under increased scrutiny as well.

But to see Didi get taken to task mere days after its U.S. debut puts a bad taste in our mouths.

The way that this saga reads from the cynical perspective is that the Chinese Communist Party was willing to let the company go public in the United States, allowing it to raise billions of dollars from foreign sources. And that the ruling party was then content to leave them holding a midsized bag by announcing its cybersecurity probe.

Hanlon’s Razor is at play in this situation, naturally.

Didi has not published a new SEC filing since June 30, and, as of the time of writing, its investor relations page is devoid of any information regarding today’s news.

While going public, it’s worth noting that Didi did warn investors that it faces a host of risks relating to its status as a Chinese company, namely its government, and as a Chinese company going public in the United States. Observe the following risk factors that it shared while going public (emphasis added) that dealt with the company’s business operations:

- Our business is subject to numerous legal and regulatory risks that could have an adverse impact on our business and future prospects.

- Our business is subject to a variety of laws, regulations, rules, policies and other obligations regarding privacy, data protection and information security. Any losses, unauthorized access or releases of confidential information or personal data could subject us to significant reputational, financial, legal and operational consequences.

Powered by WPeMatico