The Exchange

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Ready? Let’s talk money, startups and spicy IPO rumors.

Every quarter we dig into the venture capital market’s global, national, and sector-based results to get a feel for what the temperature of the private market is at that point in time. These imperfect snapshots are useful. But sometimes, it’s better to focus on a single story to show what’s really going on.

Enter AgentSync. I covered AgentSync for the first time last August, when the API-focused insurtech player raised a $4.4 million seed round. It’s a neat company, helping others track the eligibility of individual brokers in the market. It’s a big space, and the startup was showing rapid initial traction in the form of $1.9 million in annual recurring revenue (ARR).

But then AgentSync raised again in December, sharing at the time of its $6.4 million round that the valuation cap had grown by 4x since its last round. And that it had seen 4x revenue growth since the start of the pandemic.

All that must sound pretty pedestrian; a quickly-growing software company raising two rounds? Quelle surprise.

But then AgentSync raised again this week, with another grip of datapoints. Becca Szkutak and Alex Konrad’s Midas Touch newsletter reported the sheaf of data, and The Exchange confirmed the numbers with AgentSync CEO Niji Sabharwal. They are as follows:

That means AgentSync was worth $22 million when it raised $4.4 million, and the December round was raised at a cap of around $80 million. Fun.

Back to our original point, the big datasets can provide useful you-are-here guidance for the sector, but it’s stories like AgentSync that I think better show what the market is really like today for hot startups. It’s bonkers fast and, even more, often backed up by material growth.

Sabharwal also told The Exchange that his company has closed another $1 million in ARR since the term sheet. So its multiples are contracting even before it shared its news.

2021, there you have it.

Also this week I got to meet Ariana Thacker, who is building a venture capital fund. Her route to her own venture shop included stops at Rhapsody Venture Partners, and some time at Predictive VC. Now she’s working on Conscience.vc, or perhaps just Conscience.

Her new fund will invest in companies worth less than $15 million, have some form of consumer-facing business model (B2B and B2B2C are both fine, she said), and something to do with science, be it a patentable technology or other sort of IP. Why the science focus? It’s Thacker’s background, thanks to her background in chemical engineering and time as a facilities engineer for a joint Exxon-Shell project.

All that’s neat and interesting, but as we cover zero new-fund announcements on The Exchange and almost never mini-profile VCs, why break out of the pattern? Because unlike nearly everyone in her profession, Thacker was super upfront with data and metrics.

Heck, in her first email she included a list of her investments across different capital vehicles with actual information about the deals. And then she shared more material on different investments and the like. Imagine if more VCs shared more of their stuff? That would rock.

Conscience had its first close in mid-January, though more capital might land before she wraps up the fundraising process. She’s reached $4 million to $5 million in commits, with a cap of $10 million on the fund. And, she told The Exchange, she didn’t know a single LP before last summer and only secured an anchor investor last October.

Let’s see what Thacker gets done. But at a minimum I think she’ll be willing to be somewhat transparent as she invests from her first fund. That alone will command more attention from these pages than most micro-funds could ever manage.

The week was super busy, so I missed a host of things that I would have otherwise liked to have written about. Here they are in no particular order:

Various and Sundry

Closing, I learned a lot about software valuations here, got to noodle on the epic Roblox direct listing here, dug into fintech’s venture successes and weaknesses, and checked out the Global-e IPO filing. Oh, and M1 Finance raised again, while Clara and Arist raised small, but fun rounds.

Powered by WPeMatico

As 2021 kicked off, I reformulated a series of posts we published last year focused on startups that had reached the $100 million ARR (annual recurring revenue) mark. In our refreshed effort, we cut the target in half and dug up companies around the $50 million ARR threshold. The goal was to figure out what those firms were going through as they reached material scale, not after they had achieved effective pre-IPO status.

And the results were a bit medium.

While it was fun to chat with OwnBackup, Assembly, SimpleNexus and PicsArt, ultimately we were getting similar notes from each company: Hiring is incredibly important as a company scales, founders have to cede decision-making, and as startups grow from $30 million ARR to $50 million or more, they must harden internal systems and build business infrastructure.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

All that made sense, but it wasn’t entirely scintillating. I meant to keep the project going; I had publicly made noise about the effort and had a few interviews in the bag that were collecting dust (and emails from various PR folks).

But they wound up in the Google Docs graveyard as the news cycle somehow managed to keep accelerating, meaning that the time required to execute the somewhat effort-intensive series dried up as I held on for dear life as the early, middle, late and IPO-stage startup market stormed.

And so after some reflection, it’s time to admit defeat.

And so after some reflection, it’s time to admit defeat.

For now, I’m hitting pause on the $50 million ARR series and whatever might have come from the $100 million ARR legacy effort. I may bring it back at some point, but for now, there are just more pressing and interesting things to work on.

What follows is what I believe to be the remainder of my notes from interviews that never saw the light of day. So, one last time, let’s discuss some big startups that are scaling quickly: Appspace, Synack and Druva. We’ll proceed in alphabetical order.

The Exchange caught up with Appspace a bit ago, chatting with a few of its executives, including CMO Scott Chao and CEO Brandon Miles. It’s an interesting company that sells a software platform that powers in-office displays and kiosks. You’ve seen office sign-in screens at a welcome desk, screens outside conference rooms showing how booked they are, or company messaging and the like on various large screens? That’s what Appspace’s software does.

And the company has an interesting vibe. Unlike nearly every other startup I’ve met, Appspace doesn’t think it is saving the world. In our chat, the company joked that its culture is to move quickly, but with the cognizance that they aren’t curing cancer.

Such modesty might feel odd, but it was actually refreshing. Appspace’s job is to white-label itself, let its customers speak to their workers through its various apps (including mobile) and services, and simply feature rock-solid uptime.

Powered by WPeMatico

We’re putting aside the IPO news cycle this morning to check in on the venture capital world and the fintech market in particular.

As we all know, fintech is booming: Between Robinhood and Public and M1 Finance raising competing rounds, payment-tech startup Finix moving to diversify its cap table, and ideas that work in one market finding purchase and capital in others, it’s a damn good time to build financial technology.

But perhaps even with all that recent knowledge, we’re still missing the point.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

A provisional report from data and research group CB Insights indicates that we’re not merely in a warm period for fintech funding — we are in a period of all-time record investment for so-called mega-rounds, or investments of $100 million or more inside the fintech realm.

The first quarter of 2020 had stiff competition to overcome to set a mega-round record. The preceding period, Q4 2020, for example, saw 30 fintech rounds across the globe that were worth nine figures. But, to date, Q1 2021 is ahead and is thus guaranteed to set a new record, having already bested the preceding all-time high.

The first quarter of 2020 had stiff competition to overcome to set a mega-round record. The preceding period, Q4 2020, for example, saw 30 fintech rounds across the globe that were worth nine figures. But, to date, Q1 2021 is ahead and is thus guaranteed to set a new record, having already bested the preceding all-time high.

This morning we’re talking big money and fintech, with a splash of early-stage digging. I asked a CB Insights analyst about what appears to be falling fintech seed deal volume. Is this the result of data reporting delays inherent to seed data, the impact of SAFEs and other sorts of notes limiting visibility into the earliest stages of venture, or just a plain-old slowdown? Let’s find out.

Per the interim CB Insights dataset, there have been some 33 fintech mega-rounds so far in 2021. For context, it’s more than 50% more such rounds in Q1 2020 and Q1 2019. Via the preliminary report, here’s the data:

Powered by WPeMatico

Olo, the New York-based fintech startup that provides order processing software to restaurants, shared its initial IPO price range this morning. The company’s debut comes ahead of the expected IPO of Toast, a Boston-based unicorn with a similar market remit.

Targeting $16 to $18 per share, Olo could raise as much as $372.6 million in its public offering.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Unlike most companies going public in recent quarters that we’ve tracked, Olo has a history of growth and profitability, making its impending pricing all the more interesting. It’s unknown if Toast is profitable, but because most venture-backed IPOs aren’t, we’re presuming it isn’t.

This morning, we’re doing our usual work: parsing the company’s pricing interval to get a valuation range for Olo. We’ll calculate both simple and fully diluted pricing and then do some quick work on its revenue scale to come to grips with its total scale.

Are investors willing to pay more for profits? And, if so, how much? This is a niche question because most IPOs look a bit more like Coursera than Olo, but it’s still worth answering.

If you’d like to follow along, you can read the new S-1 filing here. Our first look at Olo is here, and its fundraising history is here, per Crunchbase.

The company is targeting $16 to $18 per share with an expected sale of 18 million shares. The company is also reserving 2.7 million shares for its underwriters. At the upper end of its range, not counting shares reserved for its bankers, Olo could raise $324 million in its debut.

Per the company, its total number of Class A and B shares outstanding after its IPO would come to 142,012,926, or what we calculate to be 144,712,926 shares, including its underwriters’ option. Using the latter — because we tend to look for valuation extremes — Olo would be worth $2.32 billion to $2.6 billion.

But what about its fully diluted valuation? Adding in shares that are currently tied to unexercised but vested stock options bring Olo to around 188,085,714 shares. Add in the underwriters’ option and the total rises to 190,785,714 shares.

Using the latter figure, at $16 and $18 per share Olo could be worth $3.05 billion to $3.43 billion on a fully diluted basis.

Let’s find out! Digging back into Olo’s growth, we can see a business with rapidly expanding software incomes. And the same software revenues are improving in quality over time. From 2019 to 2020, for example, Olo’s “platform” revenues — a mix of subscription and transaction top line from software — grew from $45.1 million to $92.8 million. Over the same time, the company’s platform revenue saw its gross margin improve from 73.6% to 84.5%.

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Ready? Let’s talk money, startups and spicy IPO rumors.

Despite some recent market volatility, the valuations that software companies have generally been able to command in recent quarters have been impressive. On Friday, we took a look into why that was the case, and where the valuations could be a bit more bubbly than others. Per a report written by few Battery Ventures investors, it stands to reason that the middle of the SaaS market could be where valuation inflation is at its peak.

Something to keep in mind if your startup’s growth rate is ticking lower. But today, instead of being an enormous bummer and making you worry, I have come with some historically notable data to show you how good modern software startups and their larger brethren have it today.

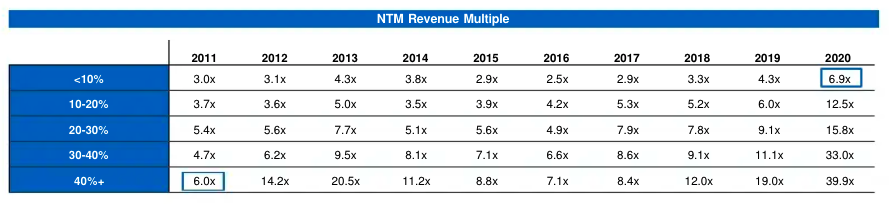

In case you are not 100% infatuated with tables, let me save you some time. In the upper right we can see that SaaS companies today that are growing at less than 10% yearly are trading for an average of 6.9x their next 12 months’ revenue.

Back in 2011, SaaS companies that were growing at 40% or more were trading at 6.0x their next 12 month’s revenue. Climate change, but for software valuations.

One more note from my chat with Battery. Its investor Brandon Gleklen riffed with The Exchange on the definition of ARR and its nuances in the modern market. As more SaaS companies swap traditional software-as-a-service pricing for its consumption-based equivalent, he declined to quibble on definitions of ARR, instead arguing that all that matters in software revenues is whether they are being retained and growing over the long term. This brings us to our next topic.

I’ve taken a number of earnings calls in the last few weeks with public software companies. One theme that’s come up time and again has been consumption pricing versus more traditional SaaS pricing. There is some data showing that consumption-priced software companies are trading at higher multiples than traditionally priced software companies, thanks to better-than-average retention numbers.

But there is more to the story than just that. Chatting with Fastly CEO Joshua Bixby after his company’s earnings report, we picked up an interesting and important market distinction between where consumption may be more attractive and where it may not be. Per Bixby, Fastly is seeing larger customers prefer consumption-based pricing because they can afford variability and prefer to have their bills tied more closely to revenue. Smaller customers, however, Bixby said, prefer SaaS billing because it has rock-solid predictability.

I brought the argument to Open View Partners Kyle Poyar, a venture denizen who has been writing on this topic for TechCrunch in recent weeks. He noted that in some cases the opposite can be true, that variably priced offerings can appeal to smaller companies because their developers can often test the product without making a large commitment.

So, perhaps we’re seeing the software market favoring SaaS pricing among smaller customers when they are certain of their need, and choosing consumption pricing when they want to experiment first. And larger companies, when their spend is tied to equivalent revenue changes, bias toward consumption pricing as well.

Evolution in SaaS pricing will be slow, and never complete. But folks really are thinking about it. Appian CEO Matt Calkins has a general pricing thesis that price should “hover” under value delivered. Asked about the consumption-versus-SaaS topic, he was a bit coy, but did note that he was not “entirely happy” with how pricing is executed today. He wants pricing that is a “better proxy for customer value,” though he declined to share much more.

If you aren’t thinking about this conversation and you run a startup, what’s up with that? More to come on this topic, including notes from an interview with the CEO of BigCommerce, who is betting on SaaS over the more consumption-driven Shopify.

Next Insurance bought another company this week. This time it was AP Intego, which will bring integration into various payroll providers for the digital-first SMB insurance provider. Next Insurance should be familiar because TechCrunch has written about its growth a few times. The company doubled its premium run rate to $200 million in 2020, for example.

The AP Intego deal brings $185.1 million of active premium to Next Insurance, which means that the neo-insurance provider has grown sharply thus far in 2021, even without counting its organic expansion. But while the Next Insurance deal and the impending Hippo SPAC are neat notes from a hot private sector, insurtech has shed some of its public-market heat.

Stocks of public neo-insurance companies like Root, Lemonade and MetroMile have lost quite a lot of value in recent weeks. So, the exit landscape for companies like Next and Hippo — yet-private insurtech startups with lots of capital backing their rapid premium growth — is changing for the worse.

Hippo decided it will debut via a SPAC. But I doubt that Next Insurance will pursue a rapid ramp to the public markets until things smooth out. Not that it needs to go public quickly; it raised a quarter billion back in September of last year.

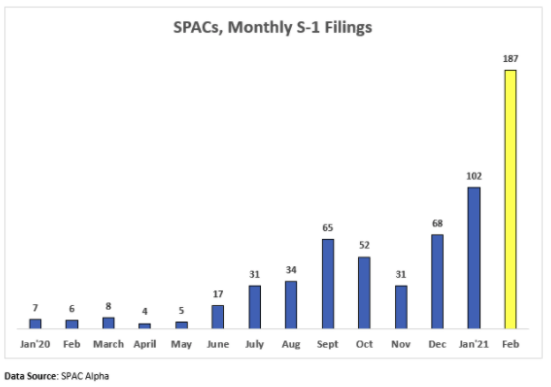

What else? Sisense, a $100 million ARR club member, hired a new CFO. So we expect them to go public inside the next four or five quarters.

And the following chart, which is via Deena Shakir of Lux Capital, via Nasdaq, via SPAC Alpha:

Powered by WPeMatico

We’re not digging into another IPO filing today. You can read all about AppLovin’s filing here, or ThredUp’s document here.

This morning, instead, we’re talking about an old favorite: software valuations. The folks over at Battery Ventures have compiled a lengthy dive into the 2020 software market that’s worth our time — you can read along here; I’ll provide page numbers as we go — because it helps explain some software valuations.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

There’s little doubt that there is some froth in the software market, but it may not be where you think it is.

The Battery report has a lot of data points that we’ll also work through in this week’s newsletter, but this morning, let’s narrow ourselves to thinking about rising aggregate software multiples, the breakdown of multiples expansion through the lens of relative growth rates, and cap it off with a nibble on the importance, or lack thereof, of cash flow margins for the valuation of high-growth software companies.

We’ll look at the changing public market perspective, and then ask ourselves if the aggregate image that appears is good or not good for software startups.

I chatted through pieces of the report with its authors, Battery’s Brandon Gleklen and Neeraj Agrawal. So, we’ll lean on their perspective a little as we go to help us move quickly. This is our Friday treat. Or at least mine. Let’s get into it.

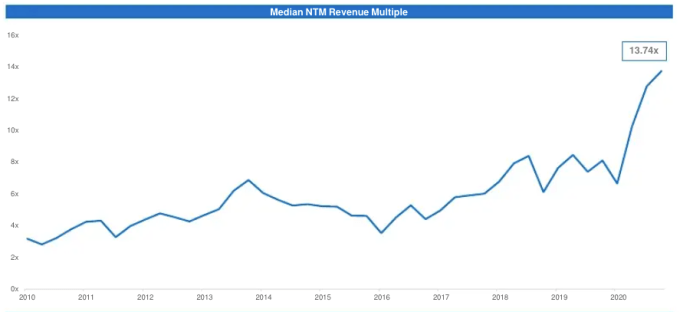

Let’s start with an affirmation. Yes, software valuations have risen to record-high multiples in recent years. Here’s the Battery chart that makes the change clear:

Page 31, Battery report. Image Credits: Battery Ventures

Powered by WPeMatico

Another day, another venture-backed IPO filing. Today it’s ThredUp, a used-goods marketplace that is approaching the public markets in the wake of Poshmark’s own strong debut.

Both companies have a related market focus, albeit different approaches to selling used goods. Poshmark allows users to sell clothing items through its app. ThredUp, in contrast, acquires goods from users and sells them itself.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But while Poshmark had profits to brag about in its own IPO filing, ThredUp does not and is also growing more slowly, expanding revenues just 13.6% in 2020. Reading its S-1 filing, it’s clear ThredUp did not have the best 2020, thanks in part to COVID-19.

This morning, let’s get into the numbers posted by the company backed by Trinity Ventures, Redpoint, Highland Capital Partners and Goldman Sachs to decide if it’s just merely to catch Poshmark’s wave, or if its business is a fine machine in its own right.

To understand ThredUp’s business, we have to get into the mechanics of how it sells things. The company has two methods: direct sales and consignment. In the former, ThredUp buys goods and sells them. It then “recognize[s] revenue on a gross basis” and generates gross profit after deducting “inventory cost, inbound shipping and inventory write-downs, as well as outbound shipping, outbound labor and packaging costs.”

That is the model that ThredUp is leaving behind. After shifting to “primarily consignment sales” in 2019, the company’s business has skewed sharply in that direction. Consignment works by having consumers send ThredUp their goods, which it holds, and perhaps sells, remitting to the user a portion of the sale price. The method reduces write-downs and boosts gross margins.

Consignment sales at ThredUp “recognize revenue net of seller payouts,” deducting “outbound shipping, outbound labor and packaging costs” to reach gross profit results.

The revenue-mix focus change can be seen in how ThredUp generated gross profit in 2018, 2019 and 2020. In those years, consignment gross profit came to 38%, 67% and 81% of total gross profit. ThredUp’s business today is effectively a large, digital consignment effort.

What impact has that shift had on the company’s financial health? Let’s find out.

ThredUp posted $129.6 million in 2018 revenue, a figure that grew to $163.8 million in 2019 and $186 million in 2020. The company’s growth slowed from 26.4% in 2019 to 13.6% in 2020, a sharp deceleration. But at the same time, the portion of ThredUp revenues that came from consignment sales grew to 74% from 60%. Did that change have a material impact on the company’s gross margins, thus rendering its slow growth more palatable?

Not really. The company’s gross margins came to 68.7% in 2019 and 68.9% in 2020. That’s about as flat as Texas. And notably the number stayed flat despite the company noting that consignment revenues had stronger gross margins in 2019 and 2020 (77% and 75%, respectively) than its other model (57% and 51%, respectively).

Powered by WPeMatico

AppLovin released its S-1 filing yesterday, bringing the Palo Alto-based mobile-app-focused software company a step closer to joining the public markets.

The business results detailed in the document are generally impressive. While some companies going public in recent months have detailed pandemic-fueled growth to lean against or membership in a sector hotter than individual results, AppLovin’s filing tells the story of a rapidly growing company that has managed to scale adjusted profit as it has grown.

And now, with annual revenue north of $1 billion, AppLovin is also a very large company, meaning that its IPO will be widely watched.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

So this morning we’re rifling through its IPO filing and yanking out what matters as we add one more name to our IPO lists.

The Exchange has a lengthy list of non-IPO topics that we’d like to get to. If everyone could stop going public for a few days, we’d love to write about something else! OK, let’s get into it!

As a short introduction, the company’s products are designed to help developers find users and monetize their apps. AppLovin has its own in-house suite of mobile apps, what its S-1 calls a “globally diversified portfolio of over 200 free-to-play mobile games run by 12 studios.” Those apps have 32 million global daily actives, the document added.

It’s a pretty neat company to dig into if you’re into mobile apps at all. Regardless, what we care about today are its numbers. So let’s talk growth, revenue quality, profits, cash consumption and capital structure. Most of the news is good, even if there are some downsides to AppLovin’s capital structure.

Recall that KKR bought a chunk of AppLovin back in mid-2018 at a valuation of around $2 billion. That number appears comically low, given that the company posted $483.4 million in revenue that year, a figure that it roughly doubled in 2019 to $994.1 million. Growth slowed in percentage terms in 2020, when AppLovin saw total revenues of $1.45 billion, though the company managed similar growth in gross-dollar terms.

In percentage terms, AppLovin grew 106% from 2018 to 2019, and 46% from 2019 to 2020. How KKR got to buy into the company at 4x revenues when it was growing at 100% is not clear.

The company is growing well, but is AppLovin accreting revenue of high quality? Yes, but we need to scrape some grime off the numbers to understand them. Turning to the company’s yearly results, AppLovin’s cost of revenue rose steadily as a percentage of revenue from 2018 to 2020. Indeed, the numbers went from 11% in 2018 to 24% in 2019 and 38% in 2020. That’s an awful progression, and if we lacked more information we’d posit that the company’s overall revenue quality was sharply declining.

It’s not that bad. There’s about $1 million in share-based compensation inside the 2020 cost of revenue figure and $228.3 million of “amortization expense related to acquired intangibles.” If we yank out those from the cost-of-revenue line item, AppLovin’s gross margin for 2020 grows from 62% to 77.5%. That’s much better.

Powered by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Ready? Let’s talk money, startups and spicy IPO rumors.

Kicking off with a tiny bit of housekeeping: Equity is now doing more stuff. And TechCrunch has its Justice and Early-Stage events coming up. I am interviewing the CRO of Zoom for the latter. And The Exchange itself has some long-overdue stuff coming next week, including $50M and $100M ARR updates (Druva, etc.), a peek at consumption based pricing vs. traditional SaaS models (featuring Fastly, Appian, BigCommerce CEOs, etc.), and more. Woo!

This week both DoorDash and Airbnb reported earnings for the first time as public companies, marking their real graduation into the ranks of the exited unicorns. We’re keeping our usual eye on the earnings cycle, quietly, but today we have some learnings for the startup world.

Some basics will help us get started. DoorDash beat growth expectations in Q4, reporting revenue of $970 million versus an expected $938 million. The gap between the two likely comes partially from how new the DoorDash stock is, and the pandemic making it difficult to forecast. Despite the outsized growth, DoorDash shares initially fell sharply after the report, though they largely recovered on Friday.

Why the initial dip? I reckon the company’s net loss was larger than investors hoped — though a large GAAP deficit is standard for first quarters post-debut. That concern might have been tempered by the company’s earnings call, which included a note from the company’s CFO that it is “seeing acceleration in January relative to our order growth in December as well as in Q4.” That’s encouraging. On the flip side, the company’s CFO did say “starting from Q2 onwards, we’re going to see a reversion toward pre-COVID behavior within the customer base.”

Takeaway: Big companies are anticipating a return to pre-COVID behavior, just not quite yet. Firms that benefited from COVID-19 are being heavily scrutinized. And they expect tailwinds to fade as the year progresses.

And then there’s Airbnb, which is up around 16% today. Why? It beat revenue expectations, while also losing lots of money. Airbnb’s net loss in Q4 2020 was more than 10x DoorDash’s own. So why did Airbnb get a bump while DoorDash got dinged? Its large revenue beat ($859 million, instead of an expected $748 million), and potential for future growth; investors are expecting that Airbnb’s current besting of expectations will lead to even more growth down the road.

Takeaway: Provided that you have a good story to tell regarding future growth, investors are still willing to accept sharp losses; the growth trade is alive, then, even as companies that may have already received a boost endure increased scrutiny.

For startups, valuation pressure or lift could come down to which side of the pandemic they are on; are they on the tail end of their tailwind (remote-work focused SaaS, perhaps?), or on the ascent (restaurant tech, maybe?). Something to chew on before you raise.

It was one blistering week for funding rounds. Crunchbase News, my former journalistic home, has a great piece out on just how many massive rounds we’re seeing so far this year. But even one or two steps down in scale, funding activity was super busy.

A few rounds that I could not get to this week that caught my eye included a $90 million round for Terminus (ABM-focused GTM juicer, I suppose), Anchorage’s $80 million Series C (cryptostorage for big money), and Foxtrot Market’s $42 million Series B (rapid delivery of yuppie and zoomer essentials).

Sitting here now, finally writing a tidbit about each, I am reminded at the sheer breadth of the tech market. Termius helps other companies sell, Anchorage wants to keep your ETH safe, while Foxtrot wants to help you replenish your breakfast rosé stock before you have to endure a dry morning. What a mix. And each must be generating venture-acceptable growth, as they have not merely raised more capital but raised rather large rounds for their purported maturity (measured by their listed Series stage, though the moniker can be more canard than guide.)

I jokingly call this little section of the newsletter Market Notes, a jest as how can you possibly note the whole market that we care about? These companies and their recent capital infusions underscore the point.

Finally, two notes from earnings calls. The first from Root, which is a head scratcher, and the second from Booking Holdings’ results.

I chatted with Alex Timm, Root Insurance’s CEO this week moments after it dropped numbers. As such I didn’t have much context in the way of investor response to its results. My read was that Root was super capitalized, and has pretty big expansion plans. Timm was upbeat about his company’s improving economics (on a loss ratio and loss-adjusted expenses basis, for the insurtech fans out there), and growth during the pandemic.

But then today its shares are off 16%. Parsing the analyst call, there’s movement in Root’s economic profile (regarding premium-ceding variance over the coming quarters) that make it hard to fully grok its full-year growth from where I sit. But it appears that Root’s business is still molting to a degree that is almost refreshing; the company could have gone public in 2022 with some of its current evolution behind it, but instead it raised a zillion dollars last year and is public now.

Sticking our neck out a bit, despite fellow neo-insurnace player Lemonade’s continued, and impressive valuation run, MetroMile’s stock is also softening, while Root’s has lost more than half its value from its IPO date. If the current repricing of some neo-insurance players continues, we could see some private investment into the space slow. (Fewer things like this?) It’s a possible trend we’ll have eyes on this year.

Next, Booking Holdings, the company that owns Priceline and other travel properties. Given that Booking might have notes regarding the future of business travel — which we care about for clues regarding what could come for remote work and office culture, things that impact everything from startup hub locations to software sales — The Exchange snagged a call slot and dialed the company up.

Booking Holdings’ CEO Glenn Fogel didn’t have a comment as to how his company is trading at all-time highs despite suffering from sharp year-over-year revenue declines. He did note that the pandemic has shaken up expectations for conversations, which could limit short-term business travel in the future for meetings that may now be conducted on video calls. He was bullish on future conference travel (good news for TechCrunch, I suppose), and future travel more generally.

So concerning the jetting perspective, we don’t know anything yet. Booking Holdings is not saying much, perhaps because it just doesn’t know when things will turn around. Fair enough. Perhaps after another three months of vaccine rollout will give us a better window into what a partial return to an old normal could look like.

And to cap off, you can read Apex Holdings’ SPAC presentation here, and Markforged’s here. Also I wrote about the buy-now-pay-later space here, riffed on the Digital Ocean IPO with Ron Miller here, and doodled on Toast’s valuation and the Olo debut here.

Hugs, and have a lovely weekend!

Powered by WPeMatico

Amidst all the hype that Lemonade (IPO), Root (IPO), Metromile (SPAC-led debut) and other insurtech players have generated in the last year, it’s been easy to forget about Oscar Health. But now that the company founded in 2012 is approaching the public markets, one of the early tech-themed insurance companies is catching up on the attention front.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

So this morning we’re digging into Oscar Health’s first IPO pricing interval, hoping to understand how the market is valuing its unprofitable health-insurance enterprise.

Recall that Oscar Health was valued at around $3.2 billion in March of 2018. That datapoint, via PitchBook, is dated. Oscar Health raised hundreds of millions since (per several venture-capital tracking databases, including Crunchbase) but we lack a final private valuation for the company.

Recall that Oscar Health was valued at around $3.2 billion in March of 2018. That datapoint, via PitchBook, is dated. Oscar Health raised hundreds of millions since (per several venture-capital tracking databases, including Crunchbase) but we lack a final private valuation for the company.

Regardless, with Oscar Health now targeting a $32 to $34 per-share IPO range, we can get our hands dirty.

Let’s get some valuation numbers and then decide if Oscar Health feels cheap or expensive at that price.

Oscar Health is looking to reap as much as $1.21 billion in its IPO, a huge sum. The company is selling 30,350,920 shares, with 4,650,000 additional shares reserved for its underwriters. Existing shareholders are selling another 649,080 shares.

This means that after the IPO, Oscar Health will have 197,037,445 Class A and B shares in circulation, or 201,687,445 after counting shares reserved for its underwriters.

Using the company’s $32 to $34 per-share range, we can calculate a valuation minimum of $6.31 billion for the company (lower share count, low-end of price range) and $6.86 billion (higher share count, high-end of price range). That’s the company’s simple IPO valuation.

Oscar Health may also sell up to $375 million of its shares at its IPO price to three different funds. The company advises that the “indication of interest is not a binding agreement or commitment to purchase,” so we can ignore it for now.

Powered by WPeMatico