The Exchange

Auto Added by WPeMatico

Auto Added by WPeMatico

So much can change in a day.

This morning, news that a trial COVID-19 vaccine candidate had an effective rate of more than 90% shook the financial world. The Pfizer vaccine is reportedly so effective, the company “will have manufactured enough doses to immunize 15 to 20 million people” by the end of the year, according to the New York Times, appears to have given investors the green light to pile back into companies harmed by the pandemic.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The shift of money from shares that proved popular during the summer is massive and abrupt. Zoom and Peloton are down sharply this morning, while Uber and Lyft are soaring. Indeed, the Dow Jones Industrial Average and S&P 500 indices are up around 4.8% and 3.3% respectively, while SaaS and cloud share are off 3.5%.

Investors are taking money out of companies that were expected to do well thanks to the pandemic and moving that capital into firms that were weakened by the pandemic.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Short-term market movements do not always predict the future accurately, so we should not treat today’s trading as gospel.

That said, it’s not hard to draw some basic conclusions from the trading activity. Here’s what I think we can deduce from today’s stock market activity:

Powered by WPeMatico

This is The TechCrunch Exchange, a newsletter that goes out on Saturdays, based on the column of the same name. You can sign up for the email here.

Are you tired? I am. What a week. But, if you kept your eyes off American politics and instead focused on the stock market, this was not a week of stress at all. It was a celebration.

Yes, the election appears to be influencing stocks, with investors delighted at what could be a divided government. Their bet is that with different parties in control of different bits of the government, nothing will happen, and thus taxes and regulation won’t change. You can handicap that as you wish.

Regardless, this week’s stock market boom was a multifaceted affair. Software stocks rallied as the summer-era trade appeared to come back into vogue, in which investors pour capital into SaaS and cloud companies in hopes of parking their wealth into something with growth potential. Software earnings also look pretty good thus far (we chatted with JFrog and Ping Identity and BigCommerce), improving on their early performance.

Uber and Lyft drove their own rally as California voters decided that their long-standing labor arbitrage would stand. And then Uber failed to vomit on itself during its earnings report. Not bad.

Big tech stocks rose, as well. All this is to say that after some fear in the market a week ago, things are back to being heated for tech companies. And it is, as we expected, flushing out the next wave of IPOs.

Airbnb is expected to file publicly early next week (we have four questions here that we cannot wait to get answered), and Upstart actually filed this week, which you probably missed because you were watching something else. No worries. We are here for you.

Another notable possible include DoorDash, now unshackled from its expensive California regulatory battle. How many debuts shall we see? Hopefully many.

Upstart’s IPO filing brings a fintech IPO to the fore, and overall its numbers are pretty good if you discount worries about its customer concentration. Its debut could augur well for fintech as a whole, a segment of the startup population that, when viewed through the lens of PayPal’s earnings, is having a hell of a year.

Fintech VCs are active, as well, dropping over $10 billion into startups focusing on financial technology products and services in Q3. Payments, insurtech, wealth management and banking startups caught our eye as sectors to watch in that niche.

It was not a perfect week for fintech, however, as the U.S. government decided that the Visa-Plaid deal should not happen. Damn. As discussed on Equity, this deal could limit M&A interest for fintech startups from large players. Does that mean that fintech IPOs, then, have to carry the liquidity bucket for the sector?

Maybe! And if so, Upstart’s impending flotation seems to take on extra importance. We’ll keep you posted.

Sticking under our target word count for the first time in so long I nearly forgot what it is, here are a few iotas and crumbs for your weekend:

Have a good weekend. Stay safe. Fight COVID-19. And listen to this.

Powered by WPeMatico

During yesterday’s tense voting and this morning, shares of American-listed technology companies are shooting higher.

The tech-heavy Nasdaq composite is up around 3.35% this morning, more than double what the broad S&P 500 index is currently managing. SaaS and cloud stocks kicked off the day up a staggering 4.98%, a sharp rally in the value of smaller, more growth-oriented technology companies.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

For technology companies on the wings of the IPO market, it’s great news.

In 2020 it can be easy to forget, but tech stocks do not have to rise. They merely have in recent months, perhaps warming the waters for more technology debuts as the fourth quarter races toward its midpoint. The Exchange has heard whispers from several folks that the late-November/early-December period could be active for new filings, bringing rising stocks and pent-up demand together for a possible IPO run.

We’ll see. Today’s rally — and ballot measure results in California — could be the push companies like Airbnb and DoorDash needed to stop faffing around with private filings.

We’ll see. Today’s rally — and ballot measure results in California — could be the push companies like Airbnb and DoorDash needed to stop faffing around with private filings.

In pedestrian terms, the getting is good right now for public tech companies, so if you are going to go public, go get got while the getting stays good.

Today, let’s examine recent market gains for tech stocks and remind ourselves who is expected to go public next. Then, of course, chat about all the unicorns on the unofficial IPO list who could find a greased path ahead of them toward a flotation.

Big tech stocks are gaining, small stocks are up and software companies are hot. The NASDAQ is now less than 5% away from its all-time highs, and the Bessemer Cloud Index is now just 9% down from its own, a rebound from its prior status in correction territory. (A correction occurs when an index falls 10% or more from highs.)

So, who does the rally help? Let’s rock through a list:

Powered by WPeMatico

This is The TechCrunch Exchange, a newsletter that goes out on Saturdays, based on the column of the same name. You can sign up for the email here.

Over the past few months the IPO market made it plain that some public investors were willing to pay more for growth-focused technology shares than private investors. We saw this in both strong tech IPO pricing — the value set on companies as they debut — and in resulting first-day valuations, which were often higher.

One way to consider how far public valuations rose for tech startups, especially those with a software core in 2020, is to ask yourself how often you heard about a down IPO this year. Maybe a single time? At most? (You can catch up on 2020 IPO performance here, if you need to.)

IPO enthusiasm exposed a gap between what many venture capitalists and private investors were paying for tech shares, and what the public market was doing with its own valuation calculations. Insurtech startup Hippo’s $150 million private round from July is a good example. The company was valued at $1.5 billion in the round, a healthy uptick from its preceding private valuation. But if we valued it like the then-newly-public Lemonade, a related company, at the time, Hippo was priced inexpensively.

This week, however, the concept of private investors being more conservative than public investors in certain cases (some eight-figure private rounds happened this year at valuations that were even more bullish than public investor treatment of IPOs, to be clear) took a ding as most big tech companies lost ground, SaaS stocks sold off, and other tech firms struggled to keep up with investor enthusiasm.

Not only tech companies took a beating, but as I write to you on this Friday afternoon, the American stock markets were on a path for their worst week since March, CNBC reported, “led by major tech shares.”

A change in the wind? Perhaps.

Notable is that it was just in September that VCs seemed resigned to having startup valuations pulled higher by public markets’ endless optimism for related companies. Canaan’s Maha Ibrahim told me during Disrupt 2020 that it was a time when VCs had to “play the game” and pay up for startups, so long as companies were being “rewarded in the public markets for high growth the way that Snowflake” was at the time. A16z’s David Ulevitch concurred.

Perhaps that dynamic is changing as stocks dip. If so, startup valuations could decline en masse, along with the more exotic areas of startup-related finance. The SPAC boom, for example, may wane. Chatting with Hippo’s CEO Assaf Wand this week, he posited that SPACs were a market-response to the public-private valuation gap, an accelerant-cum-bridge to help startups get public while demand was hot for their equity.

Without the same red-hot demand for growth and risk, SPACs could cool. So, too, could private valuations that the hottest startups have taken for granted. Whether what we’re feeling in the wind this week is a hiccup or tipping point is not clear. But the public market’s fever for tech equities may have broken at a somewhat awkward time for Airbnb, Coinbase, DoorDash and other not-quite-yet-IPOs.

It started to snow this week where I live, putting a somewhat sad cap on an otherwise turbulent week. Still! There’s lots from our world to get into. Here’s our week’s market notes:

This week featured two IPOs that we cared about. MediaAlpha’s debut, giving the advertising-and-insurtech company a $19 per-share IPO price, quickly exploded out of the gate. Today the company is worth nearly $38 per share. Why? On its IPO day MediaAlpha CEO Steve Yi said that he had chosen the current moment because public markets had garnered an appreciation for insurtech. His share price growth seems to concur.

Until we look at Root, to some degree. Root, a neo-insurance provider focused on the automotive space, priced at $27 when it debuted this week, $2 above the top-end of its range. The company is now worth less than $24 per share. So, whatever wave MediaAlpha caught appears to have missed Root.

I honestly don’t know what to make of the difference in the two debuts, but please email in if you do know (you can just reply to this email, and I’ll get your note).

Regardless, I chatted with Root CEO Alex Timm after his company went public. The executive said that Root had laid down plans to go public a year ago, and that it can’t control market noise around the time of its debut. Timm stressed the amount of capital that Root added to its coffers — north of $1 billion — is a win. I asked how the company intended to not fuck up its newly swollen accounts, to which Timm said that his company was going to stay “laser focused” on its core automotive insurance opportunity.

Oh, and Root is based in Ohio. I asked what its debut might mean for Midwest startups. Timm was positive, saying that the IPO could highlight that there are a lot of smart folks and GDP in the middle of the country, even if venture capital tallies for the region remain underdeveloped.

Stay safe, and vote.

Powered by WPeMatico

Yesterday’s earnings deluge made plain that tech shares are not rocketing higher as 2020 comes to a close. Indeed, in pre-market trading this morning, Microsoft, Apple, Facebook and Amazon are all down.

Alphabet is the only member of the Big Five that is worth more today than yesterday. Strong advertising and cloud results helped the search giant post a return-to-form quarter. But in most other reports there were signs of weakness or underperformance compared to expectations that could undermine the relentlessly bullish attitude tech shares have enjoyed for several months.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The tailwinds that lifted much of tech this year remain. Every CEO I speak to still thinks that the COVID-19 bump to digital services demand has room to run, and that the digital transformation’s acceleration that has been a regular point of optimism for VCs, founders and public company leaders, will continue.

But that doesn’t mean all tech companies will benefit or post outsize results. Those facts don’t imply that pandemic-induced friction won’t add up.

But that doesn’t mean all tech companies will benefit or post outsize results. Those facts don’t imply that pandemic-induced friction won’t add up.

It’s not only the biggest companies that are treading water. We’re seeing valuations pause in tech’s hottest category — SaaS and cloud — despite continued growth in its constituent companies. The combined sentiment-and-share change could dampen enthusiasm for startup shares, perhaps undercutting some of the hype and FOMO that we keep hearing is driving private valuations higher.

Are we seeing a change in tech’s temperature while the weather changes? Let’s take a look.

Starting with the biggest tech companies, Alphabet’s results were pretty good. The company’s YouTube and cloud segments outperformed expectations, helping the company best expectations.

From there, things get choppier. Apple beat expectations, but its shares fell after investors were less than impressed with its aggregate results. Microsoft posted good calendar Q3 earnings, including strong Azure performance, but its guidance left investors underwhelmed and its shares also fell. Facebook beat expectations in the quarter, but rising costs seemed to dampen investor sentiment. It lost a little ground after earnings. Amazon’s Q3 was hot, but its Q4 should reduce operating income due to COVID-19 costs. It also lost ground after reporting.

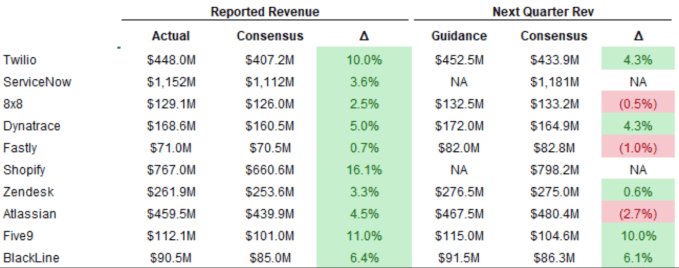

From that malaise we turn to the SaaS and cloud world. Redpoint’s Jamin Ball is doing his usual roundups, one of which we’re borrowing this morning. Here’s his digest of SaaS and cloud earnings thus far:

Takeaways? Every SaaS and cloud company crushed Q3, but Q4 is looking a bit more dicey. Beats look slim, some companies are declining to project and aside from an outlier or two, the numbers look slimmer overall.

Powered by WPeMatico

The American venture capital world has staged an impressive comeback from the early months of the COVID-19 pandemic. For a moment, there was worry that startups would struggle to raise for quarters, leading to layoffs, slowed hiring and budget cuts.

But as the pandemic accelerated plans to shift operations online, many startups wound up more popular than expected. Those tailwinds helped the venture capital world get back into its own game in a big way, leading to Q3 being an outsized quarter for domestic venture capital activity.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Today, in a first, we have two editions of The Exchange for you. Get hype.

As The Exchange reported last week, “How much money was raised by U.S.-based startups in Q3 2020? $36.5 billion, according to CBInsights, $37.8 billion according to PitchBook. [The former data provider] calls the number a seven-quarter high, up 22% from the Q3 2019 number and 30% from the Q2 2020 result.”

This lends itself to a question: What’s up with venture debt during all of this?

Venture debt, in various forms, is a type of capital provided to startups that may or may not have raised equity-based funds, like venture capital. One variety comes from institutions like Silicon Valley Bank, which might provide a growing startup with well-known backers an additional fraction of its last raise in debt, allowing the young company to take on more total capital than it otherwise might without greater dilution.

Other forms of venture debt, like revenue-based financing, share startup income streams to repay borrowings. And there are other, more exotic forms of the capital source.

I’ve been curious about the space for a few quarters now. So, when some survey data on the venture debt market from Runway Growth Capital came in, I started collecting my notes into a single entry.

Venture debt has a place in today’s market, but while venture capital is back to setting records, it appears that its less-known sibling won’t manage to match its last few years’ worth of results, according to new PitchBook data. Let’s talk about it.

Runway Growth is a venture debt player that did $41.5 million in “funded loans” in Q3 2020, it told TechCrunch. That’s for your own reference. Its new survey of 493 entrepreneurs who had raised venture capital and 50 providers of startup capital from the VC and lending worlds noted that 60% of founders felt that “venture debt has become more founder-friendly,” which you might think would imply that more venture debt was being used, overall.

That was my read, at least.

From the same survey, two related data points explain why venture debt has a place in the market: 86% of providers felt that “venture debt was key to extend the company’s runway to reach an important milestone,” while just over a quarter of founders agreed. Regardless of who is right on that point, venture debt has seen impressive growth in recent years.

Via PitchBook, here are updated venture debt metrics for the United States through 2019:

Powered by WPeMatico

Last night neo-insurance provider and former startup Root priced its IPO at $27 per share, $2 per share ahead of its $22 to $25 target price range.

According to Root, it sold 26,830,845 shares in its IPO, including 24,249,330 from the company itself. Its underwriting banks have the option to buy another 4,024,626 at the IPO price, less “underwriting discounts and commissions.” The remaining shares are being sold by existing shareholders.

At $27 per share, Root raised $654,731,910, but that figure will rise to $763,396,812 if its underwriters exercise their option in full, using the full $27 price for our calculation. Per its S-1 filings, both Dragoneer and Silver Lake will purchase $250 million of Root stock at the IPO price once the IPO has closed.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Today, in a first, we have two editions of The Exchange for you. Get hype.

Root will therefore raise north of $1 billion in its IPO, once all shares sold are counted. Doing some loose math, Root is worth around $6.8 billion at its IPO price, though Renaissance Capital, an IPO specialist, puts the figure at $7.1 billion on a fully diluted basis.

For the Midwest, Ohio-based Root’s IPO is a win. The company shows that it is possible to build high-growth technology companies worth billions of dollars far from coastal hubs. For the broader insurtech space, Root’s IPO is a win. The company follows Lemonade to the public markets, setting a strong valuation mark again for the neo-insurance startup market.

For similar companies like Clearcover, MetroMile and all startups that related to Root and Lemonade, it’s a good day. Let’s get into what we can learn from Root’s pricing.

Insurance multiples are hot. Key from Root’s IPO is the fact that we can now see insurance revenue being treated similarly to software revenue. How so? In multiples terms. Let me explain.

Root generated $245.4 million in revenue during the first and second quarters of 2020. That’s a run rate of around $491 million. At $7 billion, that’s a 14x revenue multiple. For an insurance provider with scant gross margins! Wild. Given Root’s weak-looking Q3 2020 revenues, that number isn’t going to fall anytime soon.

For companies that are not pure-play software outfits and want to go public, Root’s strong, above-range pricing makes it plain that there is investor demand for more than one type of revenue growth.

Investors are betting that Root’s history of growth will continue. In the first half of 2019, the company’s revenues were a mere 42% of what it pulled off during the same period in 2020. If the company can more than double again next year, then, hey, maybe all the numbers work. But to see public shareholders take such a growth-and-valuation flyer on an insurtech player is notable.

Kyle Nakatsuji, co-founder and CEO of Clearcover, another neo-insurance provider, explained to TechCrunch via email what he thinks is going on: “It’s clear that the market is aware of the massive opportunity for technology-enabled disruption in the category and it is rewarding those companies that focus on customer-oriented, digital innovation. The rapid growth of key players in the space is now proving this will play out and the winners will be consumers seeing lower prices and investors seeing better returns. ”

Powered by WPeMatico

TechCrunch recently covered Databricks’ financial performance in 2020, contrasting its recent performance to some historical 2019 data that the company shared.

The data-and-analysis-focused unicorn grew its annual run rate 75% to $350 million, compared to its year-ago quarter, meaning that the firm is growing well at scale. TechCrunch described it as “an obvious IPO candidate” at the time, a little under two weeks ago.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Since that point, Bloomberg reported that Databricks is indeed charging ahead with an IPO, a transaction that could come as soon as the first half of 2021, writing that it “has held talks with banks but has yet to hire underwriters” for its flotation.

That is enough news for us to have fun with. So, this morning let’s collate all that we know about the company’s financial performance, mix in some current market valuation metrics, and do some light projecting of Databricks’ growth. Our question? What might the company be worth at the end of Q1 or Q2 next year.

Of course, there are some worrying signs on the horizon that the stock market is about to shift lower, but, hey, there’s no need to be a pessimist this early on a Monday morning. Let’s get into the math.

Starting with some history, Databricks was worth $6.2 billion after its September, 2019 Series F round of capital. The company raised $400 million in the transaction, its largest round to-date by $150 million. That capital should get the company to an H1 2020 IPO, provided that its spending didn’t go all old-school Dropbox.

Powered by WPeMatico

This is The TechCrunch Exchange, a newsletter that goes out on Saturdays, based on the column of the same name. You can sign up for the email here.

Back in August during Y Combinator’s two-day demo extravaganza, TechCrunch noted a number of startups from India that stood out from the batch. Names like Bikayi (e-commerce tools), Decentro (consumer banking APIs), Farmako Healthcare (digital health records) and MedPiper Technologies (helping hire health professionals) joined our list of favorites from the batch.

Seeing so many India-focused startups in the mix wasn’t a fluke. Data shows that India’s venture capital scene has grown sharply in recent years. 2019 was the country’s biggest ever in terms of venture dollars invested, with Bain counting $10 billion during the year.

In 2020, the third quarter brought the country’s venture capital scene back to form. After a somewhat average start to the year, Indian startups saw their venture capital investment fall to just $1.5 billion in Q2, the lowest quarterly tally since 2016. But data via KPMG and PitchBook make it plain that Q3 was a rebound, with $3.6 billion invested into Indian startups during the three-month period.

That figure was not a historical record, mind; the Q3 total looks to be only the fourth-biggest VC quarter in India’s startup history since at least 2013 and, perhaps, ever. But it was a good bounce-back during a crippling pandemic all the same. The country’s VC deal count also rebounded a bit in the third quarter, with some of that money landing in big chunks, including a $500 million investment into Byju’s this September.

Smaller startups are also seeing strong results. Bikayi is one such startup. TechCrunch caught up with the company via email, digging into its post-Demo Day results. Its monthly recurring revenue (MRR) grew 60% in August from its July results, it said. And in late August the company told TechCrunch that it was on track to reach $1 million annual recurring revenue (ARR) by the end of the year.

Bikayi said more recently that it recorded 100% growth in the number of merchants it supports, and 100% revenue growth in September. So the WhatsApp-focused Shopify-for-India is racing ahead. October results, Bikayi CEO Sonakshi Nathani added, are looking “promising” as well.

To get a better handle on the Indian startup market more broadly, The Exchange got ahold of Accel investors Arun Mathew (based in the United States), and Prayank Swaroop (based in India), for a bit of digging.

Historically, falling bandwidth and smartphone costs along with improved Internet reliability helped lay the foundation for the recent Indian startup wave, according to Swaroop. Mathew added that some high-profile successes like Flipkart made startups a more attractive option, with the ecommerce company’s success helping to “change the tenor” of the conversation around founding tech firms in recent years.

It also helps, Swaroop added, that seasoned folks from existing Indian tech companies are branching out and starting companies of their own, recycling knowledge into new, smaller companies. This is a key method by which Silicon Valley has managed to create an outsized number of hits over time; a concentration of operators who have built big startups are key grist in the unicorn mill. And there’s more money being raised to help power new Indian tech companies.

All told, 2019 was a huge year for the Indian startup market in venture capital terms, and 2020’s recovery is underway. Let’s see what gets built.

The Exchange spent a lot of this week digging into venture capital data and trends, something that we love to do. If you need to catch up, here’s our look at the U.S. venture capital scene in Q3, and here are our notes on the more global picture. And we touched on India above. What more could there be?

Well, some data on healthcare-focused companies is just what we need. Per a new report from CB Insights, there are 41 healthcare-focused unicorns today. More importantly, startups focused on health-related matters (telemedicine, mental health, AI, etc.) just had a record quarter. Even for a pandemic, $21.8 billion went into the space across 1,539 global rounds in the third quarter. That’s far more activity than I would have guessed.

And with that, we’re cutting Market Notes short this week for some important TechCrunch news:

Hey y’all. It’s Megan Rose Dickey busting into Alex’s newsletter for a couple of quick news items. First, I officially launched my newsletter, Human Capital! It covers labor and diversity and inclusion in tech. Also, I relaunched the Mixtape podcast with my colleague Henry Pickavet. You can check out our first episode of Season 3 about California’s gig worker ballot measure Prop 22 here.

Megan is amazing and you should check out her pod and newsletter.

As always, there was more good stuff to share here than I can possibly fit, so let’s get right into the data, takes, links and other delicacies.

Wrapping, a survey from Salesforce shows that enterprise cloud CEOs are reporting better-than-anticipated revenue growth and lower-than-anticipated churn, when compared to their March estimates. That is probably why earnings haven’t been a disaster and so many unicorns were able to go public in Q3.

That and valuations in the public sphere are higher than what private investors are dishing up, inverting the market’s last few years.

See you Monday,

Powered by WPeMatico

Earlier this week I asked startups to share their Q3 growth metrics and whether they were performing ahead or behind of their yearly goals.

Lots of companies responded. More than I could have anticipated, frankly. Instead of merely giving me a few data points to learn from, The Exchange wound up collecting sheafs of interesting data from upstart companies with big Q3 performance.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Naturally, the startups that reached out were the companies doing the best. I did not receive a single reply that described no growth, though a handful of respondents noted that they were behind in their plans.

Regardless, the data set that came together felt worthy of sharing for its specificity and breadth — and so other startup founders can learn from how some of their peer group are performing. (Kidding.)

Let’s get into the data, which has been segmented into buckets covering fintech, software and SaaS, startups focused on developers or security and a final group that includes D2C and fertility startups, among others.

Obviously, some of the following startups could land in several different groups. Don’t worry about it! The categories are relaxed. We’re here to have fun, not split hairs!

Powered by WPeMatico