payments

Auto Added by WPeMatico

Auto Added by WPeMatico

It’s a brutal time for marijuana startups. I’m hearing some are raising at one-fifth of their 2019 valuation amid rampant competition, tall taxes and slow legalization. The struggles for marijuana’s best-known startup, delivery service Eaze, continue as today it’s losing one of its top partners: $75 million-funded weed brand empire Caliva has dropped Eaze in favor of launching its own delivery system.

By partnering with Hypur banking to solve the marijuana payments legality issue, Caliva will be able to accept contactless mobile payments, unlike Eaze, which usually requires customers to pay in cash. Caliva buyers won’t have to worry about trips to the ATM, especially now during COVID-19 shelter-in-place orders, which the startup expects will boost their average order volume. Combined with verticalizing delivery in-house, plus its retail and wholesale operations, Caliva hopes it can grow its margins and survive this long winter for weed startups.

“Our mission at Caliva has always been to provide safe and easy access to plant-based solutions for health, happiness and healing,” said Caliva CEO Dennis O’Malley. “Together with Hypur, we are proud to offer our customers safe, compliant and convenient cashless payment options to improve and modernize their purchasing experience.” It hasn’t been so easy for Eaze, though.

Back in January, we reported that Eaze was in trouble, having suffered unannounced layoffs and executive departures. It burned cash on billboards, and never launched the services of a startup it acquired. There were questions about data security, and weed brands dropped Eaze due to delayed payments. It was almost out of money and in danger of vaporizing. It luckily managed to secure a $15 million bridge round to keep it alive, plus a $20 million Series D in February just before COVID-19 hit the fan, though I dread to think of the terms of that funding.

The plan for Eaze was to verticalize, buying and developing brands that it could sell through its existing delivery service to up its margins. Now it’s seeing former partner Caliva do the reverse, launching a delivery service to sell its own Fun Uncle, Deli and Caliva brands, as well as distribute other vape, edible and flower brands like Dosist and Kiva. Its menu breadth to attract customers and in-house brands to drive profits could be a winning combo. After limited pilots in SoCal, Caliva delivery is launching in LA and the Bay Area.

Unfortunately, traditional payment processors usually refuse to work with marijuana companies for fear of legal repercussions. That’s why most delivery services can’t accept credit or debit cards, or do so through sketchy legal workarounds that have led payment providers to be sued. Others like CanPay only offer ACH transfers, while Square only works with CBD sellers. “We spent time researching and evaluating all platforms that accept cannabis payments in the U.S., and found that Hypur has the best security, compliance and consumer experience” O’Malley tells me.

Although 400-person Caliva is now trying to raise a Series B, it may experience tough headwinds with shelter-in-place orders in effect in states where marijuana is legal. Stiff taxes on marijuana have meanwhile helped the black market continue to thrive, as California’s $3.1 billion in legal 2019 sales were overshadowed by an estimated $8.7 billion in illegal sales. Faster delivery and simpler payments could help. But enthusiasm for the industry has dwindled following the initial flood of entrants sought to exploit the end of prohibition. Is the Green Rush over?

Powered by WPeMatico

The fintech wars continue to heat up with another major exit in the space.

Consumer financial services platform SoFi announced today that it is acquiring payments and bank account infrastructure company Galileo for $1.2 billion in total cash and stock. The acquisition is dependent on customary closing conditions.

Salt Lake City-based Galileo was founded in 2000 by Clay Wilkes and was bootstrapped to profitability over the intervening two decades. My colleague Jon Shieber wrote a profile of Galileo back in November after the company announced its second round of external funding, a $77 million Series A check from Accel, which was led by growth partner John Locke. The company had previously raised an $8 million Series A round from Mercato Partners in April 2014.

Galileo provides APIs that allow fintech companies like Monzo and Chime to easily create bank accounts and issue physical and virtual credit cards, among myriad other services. While simple in theory, banking regulations and financial rules place a huge regulatory burden on fintech companies, burdens that Galileo takes on as part of its platform.

The company has found particular success in the United Kingdom, where all five of the country’s largest fintechs are customers. Globally, it processed an annualized $45 billion in transaction volume last month, up from $26 billion in October 2019 — nearly doubling in just six months.

From a strategic perspective, SoFi’s objective is that Galileo will help power its expanding suite of finance products and offer it another revenue source outside of consumer services. While SoFi was founded a decade ago to offer ways to secure better financial terms for student loans, it now offers a bevy of consumer financial options, including loan, investment and insurance products as well as cash and wealth management tools. With Galileo, it now has a clear B2B revenue component as well.

SoFi, which is now led by ex-Twitter COO Anthony Noto, has also raised hundreds of millions of new capital from the likes of Qatar in recent years. The company was most recently valued at $4.3 billion.

Galileo will operate as an independent division of SoFi, and will be continuing its operations with founder Wilkes remaining as chief executive.

As fintech valuations have rapidly expanded in recent years, the companies that empower those fintechs have increasingly become strategic for investors. Earlier this year, Visa bought Plaid for $5.3 billion, in what was considered a key exit for a finance infrastructure company. That exit brought acute investor and strategic interest to the space, interest that almost certainly accrued to Galileo, as well, and helps explain the company’s relatively quick exit from its funding round last year.

As for Accel, the firm has long had a strategy of investing in mostly bootstrapped companies, sometimes a decade or more after their founding, with examples outside of Galileo including 1Password, Qualtrics, Atlassian, GoFundMe and Tenable. Accel also led this type of round into payments platform Braintree, where the firm met the startup’s GM Juan Benitez, who also joined Galileo’s board in November along with Accel’s Locke.

Accel’s valuation of the deal was not publicly disclosed in November, but a source with knowledge of the acquisition today characterizes the firm’s return as more than 4x. Given that Accel held the equity for roughly half a year, that’s quite the IRR multiple in an otherwise challenging global macro context. Given that the acquisition of Galileo was for cash and stock, Accel likely now holds a stake in SoFi, making at least part of the return unrealized.

Galileo was represented by Qatalyst in the transaction.

Updated April 7 to include the $8 million Series A funding round led by Mercato Partners and more context on IRR.

Powered by WPeMatico

Vijay Shekhar Sharma, founder and chief executive of India’s most valuable startup, Paytm, posed an existential question in a recent press conference.

“What do you think of the commercial model for digital mobile payments. How do we make money?” Sharma asked Nandan Nilekani, one of the key architects of the Universal Payments Infrastructure that created a digital payments revolution in the country.

It’s the multi-billion-dollar question that scores of local startups and international giants have been scrambling to answer as many of them aggressively shift their focus to serving merchants and building lending products and other financial services .

New Delhi’s abrupt move to invalidate much of the paper bills in the cash-dominated nation in late 2016 sent hundreds of millions of people to cash machines for months to follow.

For a handful of startups such as Paytm and MobiKwik, this cash crunch meant netting tens of millions of new users in a span of a few months.

India then moved to work with a coalition of banks to develop the payments infrastructure that, unlike Paytm and MobiKwik’s earlier system, did not act as an intermediary “mobile wallet” to serve as an intermediary between users and their banks, but facilitated direct transaction between two users’ bank accounts.

Silicon Valley companies quickly took notice. For years, Google and the likes have attempted to change the purchasing behavior of people in many Asian and African markets, where they have amassed hundreds of millions of users.

In Pakistan, for instance, most people still run errands to neighborhood stores when they want to top up credit to make phone calls and access the internet.

With China keeping its doors largely closed for foreign firms, India, where many American giants have already poured billions of dollars to find their next billion users, it was a no-brainer call.

“Unlike China, we have given equal opportunities to both small and large domestic and foreign companies,” said Dilip Asbe, chief executive of NPCI, the payments body behind UPI.

And thus began the race to participate in the grand Indian experiment. Investors have followed suit as well. Indian fintech startups raised $2.74 billion last year, compared to 3.66 billion that their counterparts in China secured, according to research firm CBInsights.

And that bet in a market with more than half a billion internet users has already started to pay off.

“If you look at UPI as a platform, we have never seen growth of this kind before,” Nikhil Kumar, who volunteered at a nonprofit organization to help develop the payments infrastructure, said in an interview.

In October, just three years after its inception, UPI had amassed 100 million users and processed over a billion transactions. It has sustained its growth since, clocking 1.25 billion transactions in March — despite one of the nation’s largest banks going through a meltdown last month.

“It all comes down to the problem it is solving. If you look at the western markets, digital payments have largely been focused on a person sending money to a merchant. UPI does that, but it also enables peer-to-peer payments and across a wide-range of apps. It’s interoperable,” said Kumar, who is now working at a startup called Setu to develop APIs to help small businesses easily accept digital payments.

Vice-president of Google’s Next Billion Users Caesar Sengupta speaks during the launch of the Google “Tez” mobile app for digital payments in New Delhi on September 18, 2017 (Photo: Getty Images via AFP PHOTO / SAJJAD HUSSAIN)

The Google Pay app has amassed over 67 million monthly active users. And the company has found the UPI pipeline so fascinating that it has recommended similar infrastructure to be built in the U.S.

In August, the Federal Reserve proposed to develop a new inter-bank 24×7 real-time gross settlement service that would support faster payments in the country. In November, Google recommended (PDF) that the U.S. Federal Reserve implement a real-time payments platform such as UPI.

“After just three years, the annual run rate of transactions flowing through UPI is about 19% of India’s Gross Domestic Product, including 800 million monthly transactions valued at approximately $19 billion,” wrote Mark Isakowitz, Google’s vice president of Government Affairs and Public Policy.

Paytm itself has amassed more than 150 million users who use it every year to make transactions. Overall, the platform has 300 million mobile wallet accounts and 55 million bank accounts, said Sharma.

But despite on-boarding more than a hundred million users on their platform, payment firms are struggling to cut their losses — let alone turn a profit.

At an event in Bangalore late last year, Sajith Sivanandan, managing director and business head of Google Pay and Next Billion User Initiatives, said current local rules have forced Google Pay to operate in India without a clear business model.

Mobile payment firms never levied any fee to users as a strategy to expand their reach in the country. A recent directive from the government has now put an end to the cut they were receiving to facilitate UPI transactions between users and merchants.

Google’s Sivanandan urged the local payment bodies to “find ways for payment players to make money” to ensure every stakeholder had incentives to operate.

Paytm, which has raised more than $3 billion to date, reported a loss of $549 million in the financial year ending in March 2019.

The firm, backed by SoftBank and Alibaba, has expanded to several new businesses in recent years, including Paytm Mall, an e-commerce venture, social commerce, financial services arm Paytm Money and a movies and ticketing category.

This year, Paytm has expanded to serve merchants, launching new gadgets such as a stand that displays QR check-out codes that comes with a calculator and a battery pack, a portable speaker that provides voice confirmations of transactions and a point-of-sale machine with built-in scanner and printer.

In an interview with TechCrunch, Sharma said these devices are already garnering impressive demand from merchants. The company is offering these gadgets to them as part of a subscription service that helps it establish a steady flow of revenue.

The firm’s Money arm, which offers lending, insurance and investing services, has amassed over 3 million users. The head of Paytm Money, Pravin Jadhav, resigned from the company this week, a person familiar with the matter said. A Paytm spokeswoman declined to comment. (Indian news outlet Entrackr first reported the development.)

Flipkart’s PhonePe, another major player in India’s payments market, today serves more than 175 million users, and over 8 million merchants. Its app serves as a platform for other businesses to reach users, explained Rahul Chari, co-founder and CTO of the firm, in an interview with TechCrunch. The company is currently not taking a cut for the real estate on its app, he added.

But these startups’ expansion into new categories means that they now have to face off even more rivals, and spend more money to gain a foothold. In the social commerce category, for instance, Paytm is competing with Naspers-backed Meesho and a handful of new entrants; and heavily-backed OkCredit and KhataBook today lead the bookkeeping market.

BharatPe, which raised $75 million two months ago, is digitizing mom and pop stores and granting them working capital. And PineLabs, which has already become a unicorn, and MSwipe have flooded the market with their point-of-sale machines.

A vendor holds an Mswipe terminal, operated by M-Swipe Technologies Pvt Ltd., in an arranged photograph at a roadside stall in Bengaluru, India, on Saturday, Feb. 4, 2017. (Photographer: Dhiraj Singh/Bloomberg via Getty Images)

“They have no choice. Payment is the gateway to businesses such as e-commerce and lending that you can monetize. In Paytm’s case, their earlier bet was Paytm Mall,” said Jayanth Kolla, founder and chief analyst at research firm Convergence Catalyst.

But Paytm Mall has struggled to compete with giants Amazon India and Walmart’s Flipkart. Last year, Mall pivoted to offline-to-online and online-to-offline models, wherein orders placed by customers are serviced from local stores. The company also secured about $160 million from eBay last year.

An executive who previously worked at Paytm Mall said the venture has struggled to grow because its goal-post has constantly shifted over the years. It has recently started to focus on selling fastags, a system that allows vehicle owners to swiftly pay toll fees. At least two more executives at the firm are on their way out, a person familiar with the matter said.

Kolla said the current dynamics of India’s mobile payments market, where more than 100 firms are chasing the same set of audience, is reminiscent of the telecom market in the country from more than a decade ago.

“When there were just four to five players in the telecom market, the prospect of them becoming profitable was much higher. They were scaling like crazy. They grew with the lowest ARPU in the world (at about $2) and were still profitable.

“But the moment that number grew to more than a dozen overnight, and the new players started offering more affordable plans to subscribers, that’s when profitability started to become elusive,” he said.

To top that off, the arrival of Reliance Jio, a telecom operator run by India’s richest man, in 2016 in the country with the cheapest tariff plans in the world, upended the market once again, forcing several players to leave the market, or declare bankruptcies, or consolidate.

India’s mobile payments market is now heading to a similar path, said Kolla.

If there were not enough players fighting for a slice of India’s mobile payments market that Credit Suisse estimate could reach $1 trillion by 2023, WhatsApp, the most popular app in the country with more that 400 million users, is set to roll out its mobile payments service in the country in a couple of months.

At the aforementioned press conference, Nilekani advised Sharma and other players to focus on financial services such as lending.

Unfortunately, the coronavirus outbreak that promoted New Delhi to order a three-week lockdown last month is likely going to impact the ability of millions of people to use such services.

“India has more than 100 million microfinance accounts, serviced in cash every week by gig-economy workers, who hawk vegetables on street corners or embroider saris sold in malls, among other things. Three out of four workers make a living by working casually for others or at their family firms and farms. Prolonged shutdowns will impair their ability to repay loans of 2.1 trillion rupees ($28.5 billion), putting the world’s largest microfinance industry at risk,” wrote Bloomberg columnist Andy Mukherjee.

Powered by WPeMatico

Google, Amazon and Microsoft are the landlords. Amidst the coronavirus economic crisis, startups need a break from paying rent. They’re in a cash crunch. Revenue has stopped flowing in, capital markets like venture debt are hesitant and startups and small-to-medium sized businesses are at risk of either having to lay off huge numbers of employees and/or shut down.

Meanwhile, the tech giants are cash rich. Their success this decade means they’re able to weather the storm for a few months. Their customers cannot.

Cloud infrastructure costs area amongst many startups’ top expense besides payroll. The option to pay these cloud bills later could save some from going out of business or axing huge parts of their staff. Both would hurt the tech industry, the economy and the individuals laid off. But most worryingly for the giants, it could destroy their customer base.

The mass layoffs have already begun. Soon we’re sure to start hearing about sizable companies shutting down, upended by COVID-19. But there’s still an opportunity to stop a larger bloodbath from ensuing.

That’s why I have a proposal: cloud relief.

The platform giants should let startups and small businesses defer their cloud infrastructure payments for three to six months until they can pay them back in installments. Amazon AWS, Google Cloud, Microsoft Azure, these companies’ additional infrastructure products, and other platform providers should let customers pause payment until the worst of the first wave of the COVID-19 economic disruption passes. Profitable SaaS providers like Salesforce could give customers an extension too.

There are plenty of altruistic reasons to do this. They have the resources to help businesses in need. We all need to support each other in these tough times. This could protect tons of families. Some of these startups are providing important services to the public and even discounting them, thereby ramping up their bills while decreasing revenue.

Then there are the PR reasons. After years of techlash and anti-trust scrutiny, here’s the chance for the giants to prove their size can be beneficial to the world. Recruiters could use it as a talking point. “We’re the company that helped save Silicon Valley.” There’s an explanation for them squirreling away so much cash: the rainy day has finally arrived.

But the capitalistic truth and the story they could sell to Wall Street is that it’s not good for our business if our customers go out of business. Look at what happened to infrastructure providers in the dot-com crash. When tons of startups vaporized, so did the profits for those selling them hosting and tools. Any government stimulus for businesses would be better spent by them paying employees than paying the cloud companies that aren’t in danger. Saving one future Netflix from shutting down could cover any short-term loss from helping 100 other businesses.

This isn’t a handout. These startups will still owe the money. They’d just be able to pay it a little later, spread out over their monthly bills for a year or so. Once mass shelter-in-place orders subside, businesses can operate at least a little closer to normal, investors can get less cautious and customers will have the cash they need to pay their dues. Plus interest, if necessary.

Meanwhile, they’ll be locked in and loyal customers for the foreseeable future. Cloud vendors could gate the deferment to only customers that have been with them for X amount of months or that have already spent Y amount on the platform. The vendors also could offer the deferment on the condition that customers add a year or more to their existing contracts. Founders will remember who gave them the benefit of the doubt.

Consider it a marketing expense. Platforms often offer discounts or free trials to new customers. Now it’s existing customers that need a reprieve. Instead of airport ads, the giants could spend the money ensuring they’ll still have plenty of developers building atop them by the end of 2020.

Beyond deferred payment, platforms could just push the due date on all outstanding bills to three or six months from now. Alternatively, they could offer a deep discount such as 50% off for three months if they didn’t want to deal with accruing debt and then servicing it. Customers with multi-year contracts could offered the opportunity to downgrade or renegotiate their contracts without penalties. Any of these might require giving sales quota forgiveness to their account executives.

It would likely be far too complicated and risky to accept equity in lieu of cash, a cut of revenue going forward or to provide loans or credit lines to customers. The clearest and simplest solution is to let startups skip a few payments, then pay more every month later until they clear their debt. When asked for comment or about whether they’re considering payment deferment options, Microsoft declined, and Amazon and Google did not respond.

To be clear, administering payment deferment won’t be simple or free. There are sure to be holes that cloud economists can poke in this proposal, but my goal is to get the conversation started. It could require the giants to change their earnings guidance. Rewriting deals with significantly sized customers will take work on both ends, and there’s a chance of breach of contract disputes. Giants would face the threat of customers recklessly using cloud resources before shutting down or skipping town.

Most taxing would be determining and enforcing the criteria of who’s eligible. The vendors would need to lay out which customers are too big so they don’t accidentally give a cloud-intensive but healthy media company a deferment they don’t need. Businesses that get questionably excluded could make a stink in public. Executing on the plan will require staff when giants are stretched thin trying to handle logistics disruptions, misinformation and accelerating work-from-home usage.

Still, this is the moment when the fortunate need to lend a hand to the vulnerable. Not a hand out, but a hand up. Companies with billions in cash in their coffers could save those struggling to pay salaries. All the fundraisers and info centers and hackathons are great, but this is how the tech giants can live up to their lofty mission statements.

We all live in the cloud now. Don’t evict us. #CloudRelief

—

Thanks to Falon Fatemi, Corey Quinn, Ilya Fushman, Jason Kim, Ilya Sukhar and Michael Campbell for their ideas and feedback on this proposal.

Powered by WPeMatico

When Eliot Buchanan tried to use his credit card to pay his Harvard tuition bill, the payment was rejected because the university said it doesn’t accept credit. Realizing the same problem exists for thousands of different transactions like board, rent and vendor payments, he launched Plastiq. Plastiq helps people use credit cards to pay, or get paid, for anything.

Plastiq today announced that it has raised $75 million in venture capital in a Series D round led by B Capital Group. Kleiner Perkins, Khosla Ventures, Accomplice and Top Tier Capital Partners also participated in the round. The round brings the company’s total known venture capital raised to more than $140 million.

To use Plastiq, users enter their credit card information on Plastiq’s platform. In return, Plastiq will charge you a 2.5% fee and get your bills paid. While Plastiq was started with consumers in mind, SMBs have now accounted for 90% of the revenue, according to Buchanan. The new financing round will invest in building out features to give SMBs faster services around payments and processing.

Plastiq provides a way for SMBs and consumers to pay their bills and make sure they have reliable cash flow. For example, restaurants sometimes have a drop in revenue due to seasonality or, as we’re experiencing now with COVID-19, pandemic lockdowns. Or tourism companies for cities that are struggling to attract visitors. Those companies still need cash flow, and using Plastiq’s service, they can use credit cards to pay suppliers even in an off season.

There is no shortage of competition from other companies also trying to solve pain points in small-business cash flow. According to Buchanan, Plastiq’s biggest competitors are traditional lenders, as well as companies like Kabbage and Fundbox. Similar claims could be made about Brex, which offers a credit card for startups to access capital faster.

Kabbage provides funding to SMBs through automated business loans. The SoftBank-backed company landed $200 million in a revolving credit line back in July, fresh off of landing strong partnerships with banks and giants like Alibaba to access more customers. Kabbage loans out roughly $2-3 billion to SMBs every year.

Plastiq, according to its release, is also on track to make more than $2 billion in transactions. But unlike Kabagge, Plastiq doesn’t issue loans or credit, it just unlocks a payment opportunity.

“SMBs don’t need to be burdened with additional debt or additional loans,” Buchanan said. “So rather than trying to reinvent the wheel, let’s use a behavior they have already earned.”

Buchanan would not disclose Plastiq’s current valuation or revenue, but he did say that it’s not too far away from $100 million in revenue run rate. The company’s revenue has grown 150% from 2018 to 2019.

The company also noted that it has surpassed “well over 1 million users,” up 150% in unique new users from 2018 to 2019.

In terms of profitability, Buchanan said that “we could be profitable if we wanted to be,” noting that Plastiq’s revenue and margins could lead them toward profitability if they wanted to focus less on growth. But he added they don’t plan to “slow down” the growth engine any time soon — especially in the wake of the COVID-19 pandemic.

Because the Series D round closed at the end of 2019, Buchanan said the pandemic did not impact the deal. However, the company had planned to time the announcement with tax season. Now, as small businesses struggle to secure capital and stay afloat due to lockdowns across the country, Plastiq’s new raise feels more fitting.

“Our customers are more thankful for solutions like ours as traditional sources of lending are drying up and not as easy to access” Buchanan said. “Hopefully, we can measure how many businesses make it through this because of us.”

The 140-person company is currently hiring across product and engineering roles.

Powered by WPeMatico

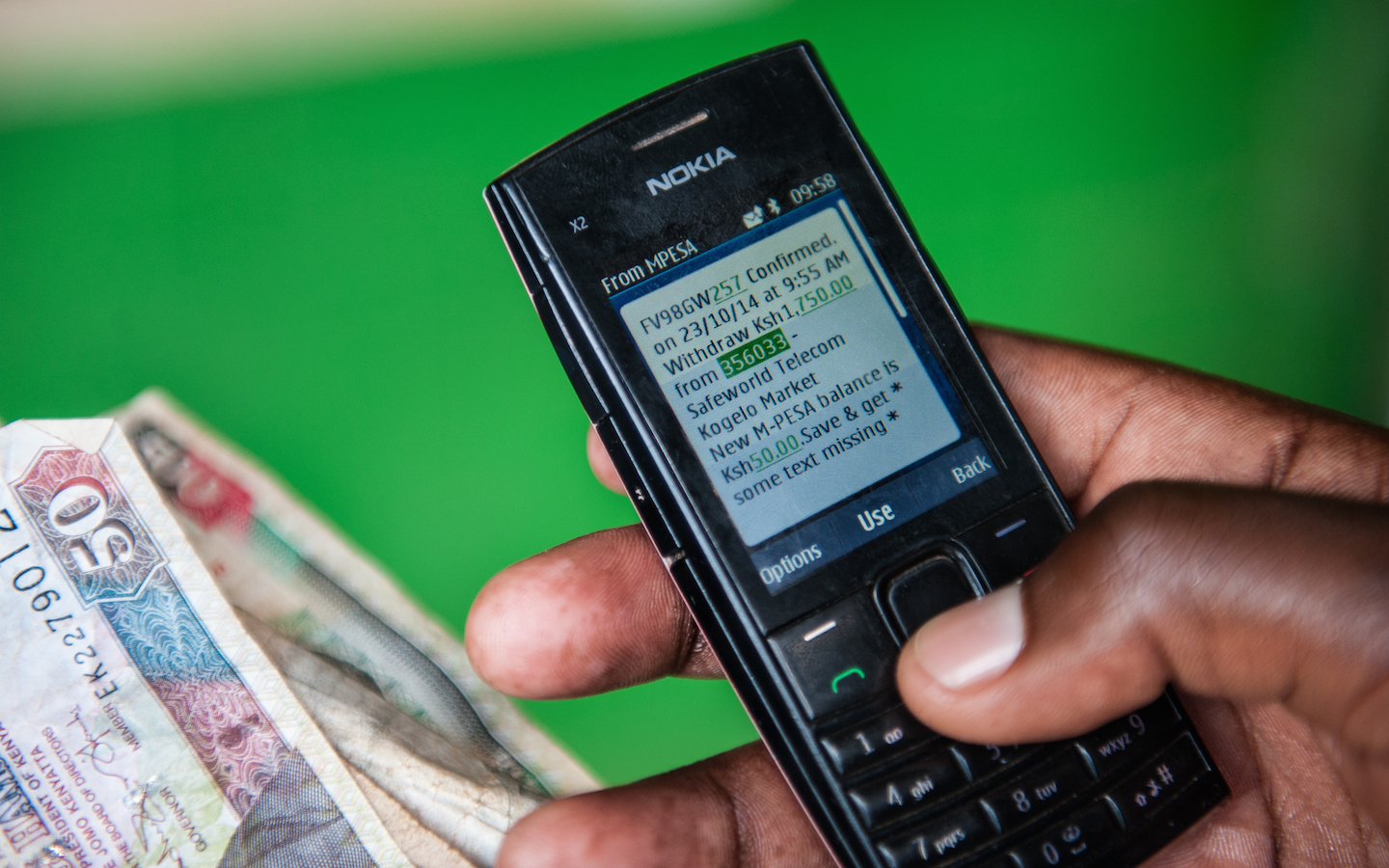

Kenya’s largest teleco, Safaricom, will implement a fee-waiver on East Africa’s leading mobile-money product, M-Pesa, to reduce the physical exchange of currency in response to the COVID-19 outbreak.

The company announced that all person-to-person (P2P) transactions under 1,000 Kenyan Schillings (≈ $10) would be free starting Tuesday for the next 90 days.

The move came after Safaricom met with the country’s Central Bank and per a directive from Kenya’s President Uhuru Kenyatta “to explore ways of deepening mobile-money usage to reduce risk of spreading the virus through physical handling of cash,” according to a release provided to TechCrunch from Safaricom.

To encourage the use of digital payments over cash, the East African telecom will also allow SMEs to increase their daily M-Pesa transaction limits from 70,000 Kenyan Schillings to 150,000 (≈ $700 to $1,500).

The measures represent the ability of the Kenyan government to use digital finance as a lever to influence social distancing and P2P transactions in an infectious health crisis.

M-Pesa has 20.5 million customers across a network of 176,000 agents and generates around one-fourth ($531 million) of Safaricom’s ≈ $2.2 billion annual revenues (2018). The company has held nearly 75% of the mobile-money market share in Kenya for nearly a decade and the country has the highest mobile-money usage rates in Africa.

In some respects, having all that output on one platform represents systemic risks to Kenya’s economy. But in the case of a global health pandemic spread by human contact, the dominance of mobile money in the country provides a policy tool to encourage digital versus physical contact on a wide scale through financial transactions.

Kenya has only three cases of COVID-19 (aka the coronavirus), according to Worldometer, but the country is taking cautionary measures. President Uhuru cancelled two foreign meetings due to the virus, the University of Nairobi shut down classes and a number of companies in the country are encouraging workers to telecommute, according to local sources and press reporting.

Powered by WPeMatico

Meet Alma, a French startup that helps you offer a new payment option for your expensive goods. Like Klarna, clients can choose to pay over three or four installments. But the comparison stops here, as Klarna isn’t available in France. Alma just raised a $14.1 million (€12.5 million) funding round.

Idinvest, ISAI and Picus Capital are investing in today’s funding round. Additionally, Alma has opened a $19.2 million (€17 million) credit line to finance merchant payments.

As a merchant, when you integrate Alma in your payment flow, your customers can choose Alma to make it less intimidating. Instead of getting charged when you pay, you can choose to buy now and pay over three or four installments. Merchants get paid instantly.

“We handle risk and cash advance in house,” co-founder and CEO Louis Chatriot told me. “When it comes to the risk of non-payment, we have implemented a series of verifications, filters and algorithms in order to detect fraud and high-risk profiles.”

The company creates multiple categories depending on your profile. It can ask for more information if Alma has some doubts, such as API access to your bank statement. Assessing risk is particularly difficult in France, as there’s no central credit scoring system.

Merchants can choose to pay the processing fees in full — 3.8% of the transaction for a payment in three intallments, 4.2% for a payment in four installments. But they also can share the processing fees with the end customer.

Alma is compatible with most e-commerce platforms, such as Shopify, Magento and Prestashop. Merchants can also offer Alma as a payment option in retail stores.

Over 1,000 merchants are using Alma already — the startup processes tens of millions of euros of transactions per year. Clients include Bobbies, Asphalte, Cowboy, Weebot, The Cool Republic and The Socialite Family.

With today’s funding round, the company wants to attract more merchants and launch two new payment options — pay later and a more traditional option to pay now. In addition to that, Alma currently redirects customers to its own checkout page. The startup wants to integrate its payment widget directly on e-commerce websites.

Powered by WPeMatico

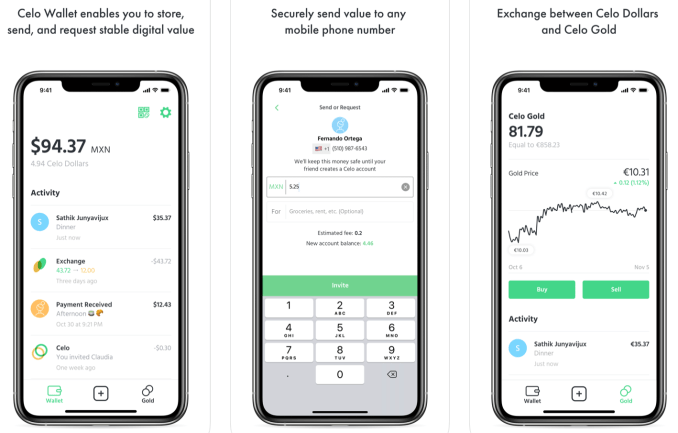

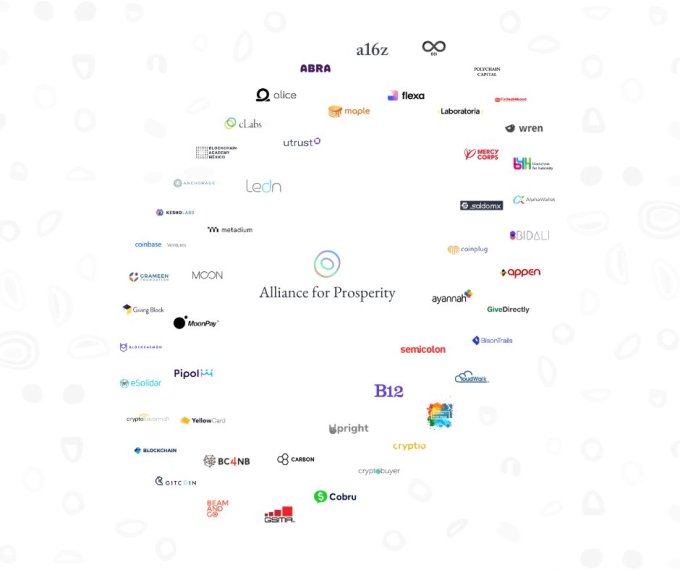

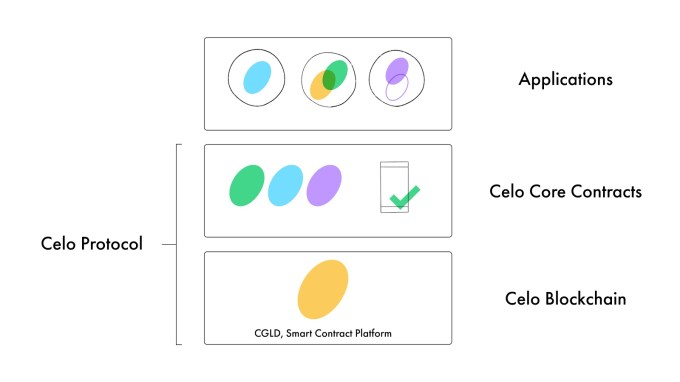

Some Libra Association members like Andreessen Horowitz and Coinbase Ventures are double-dipping, backing a competing cryptocurrency developer platform. Launching today with over 50 partners, non-profit The Celo Foundation’s ‘Alliance For Prosperity’ offers a way for developers to build decentralized mobile apps that are based on Celo’s blockchain platform and USD stablecoin.

The open-source Celo platform is still in testing with plans to officially launch its mainnet in April. The non-profit founded in 2017 has raised $36.4 million, including its Series A where Andreessen Horowitz’s a16z Crypto bought $15 million worth of Celo Gold tokens.

The biggest differentiator of Celo’s network versus other blockchains is that payments in the Celo Dollar stablecoin can be sent to people’s phone numbers rather than complicated addresses. The goal is to make delivering utility via blockchain easier by building a flexible network of applications that doesn’t scare regulators like Libra has.

The Alliance For Prosperity includes Andreessen Horowitz (which funded Celo), Coinbase (Ventures), Bison Trails, Anchorage, and Mercy Corps — all of which are also Libra Association members. That could potentially create a conflict of interest regarding which cryptocurrency and developer platform they promote to their portfolio companies, integrate into their products, or focus on for delivering financial services to the needy.

Other high-profile Alliance partners include Carbon, GiveDirectly, Grameen Foundation, Maple, and Polychain. Partners have made a somewhat vague commitment to “backing development efforts of the project, building infrastructure, implementing desired use cases on the platform, integrating Celo assets in their projects, or collaborating on education campaigns in their communities to further advance the use of blockchain technology” according to Chuck Kimble, Celo’s cLabs head of business development and head of the Alliance. Anyone can apply to join the open network, and there’s no minimum financial investment like Libra’s $10 million prerequisite.

Celo isn’t trying to replace the dollar with its own synthetic currency, and its reserve is backed with other cryptocurrencies rather than fiat cash. That might make it more acceptable to regulators who were worried that Libra’s token and fiat currency bundle-backed reserve could impact the global financial system. The first of the decentralized apps on the platform, the Celo Wallet, is already available for iOS and Android.

Like many blockchain projects, there are some lofty intentions for social impact with Celo. Use cases include “powering mobile and online work, enabling faster and affordable remittances, reducing the operational complexities of delivering humanitarian aid, facilitating payments, and enabling microlending” says Kimble. The real driver of this potential is Celo’s promise of much lower transaction fees than traditional middlemen charge.

When asked what the biggest threats to Celo’s success are, he told me “Banking infrastructure improving faster than we expect” and “Mobile adoption or LTE data not expanding on their current trajectory.” He did not mention the developer fatigue, regulatory scrutiny, technical complexity, or slow adoption of blockchain utilities that have plagued other crypto for good projects.

Here’s the full list of members working towards these goals:

Abra, Alice, AlphaWallet, Anchorage, Appen, Ayannah, Andreessen Horowitz, B12, BC4NB (Blockchain for the Next Billion), BeamAndGo, Bidali, Bison Trails, Blockchain Academy Mexico, Blockchain.com, Blockchain for Humanity (b4h), Blockchain for Social Impact (BSIC), Blockdaemon, Carbon, cLabs, CloudWalk Inc, Cobru, Coinbase, Coinplug, Cryptio, Cryptobuyer, CryptoSavannah, eSolidar, Fintech4Good, Flexa, Gitcoin, GiveDirectly, Grameen Foundation, GSMA, KeshoLabs, Laboratoria, Ledn, Maple, Mercy Corps, Metadium, Moon, MoonPay, Pipol, Pngme, Polychain, Project Wren, SaldoMX, Semicolon Africa, The Giving Block, Utrust, Upright, Yellow Card, and 88i. [Update: Ledger joined this morning.]

“Many of these organizations have on-the-ground operations that will begin to get Celo into the hands of those who have been underserved by the current global financial system” Andreessen Horowitz general partner Katie Haun told me. “Our hope is that this partnership will start unlocking the potential of internet money”. To spur adoption, the Alliance will distribute ‘Prosperity Gifts’ in the form of financial grants to developers proposing Celo products that would benefit society.

There are also some peculiar characteristics of Celo’s system. People exchange other cryptocurrencies for Celo Gold, then exchange that for Celo Dollars they can spend. The reserve is backed with other cryptocurrencies like bitcoin and ethereum rather that fiat, and isn’t fully collateralized. That could make it vulnerable to a Celo bank run or crash in price of those currencies. Celo also lets arbitrageurs pocket the difference if Celo Gold and Celo Dollars get out of sync.

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including Marek Olszewski and Rene Reinsberg who spun out machine learning startup Locu from MIT and sold it to GoDaddy, as well as EigenTrust inventor and former MIT Media Lab professor Sep Kamvar.

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including Marek Olszewski and Rene Reinsberg who spun out machine learning startup Locu from MIT and sold it to GoDaddy, as well as EigenTrust inventor and former MIT Media Lab professor Sep Kamvar.

So far, 130 teams have expressed interest in building on the Celo platform. For reference, Libra said 1,500 organizations had said they wanted to work on that project four months after its reveal. Celo Camp and Blockchain for Social Impact Incubator will also be fostering projects for the blockchain.

Celo could make banking cheaper and more accessible while power new fintech innovation. But for any of that to happen, it will need to get enough developers building truly useful products, make the blockchain and currency exchange simple enough for mainstream audiences in developing nations, and grow adoption to meaningful levels few cryptocurrency projects have yet achieved. The Alliance For Prosperity will have to throw their weight into this project, not just their names, if it’s going to succeed.

Powered by WPeMatico

Podium, a Utah-based SaaS company focused on small business customer interactions, added payments technology to its product suite today. The move accretes a new income stream to the company’s quickly growing annual recurring revenue (ARR).

While I tend to stay away from product news, Podium’s decision to add payment technology to its service hit a number of themes that we’ve recently explored, like the rise of payments technology players (Finix, for example) and how it is increasingly common to see fintech and finservices solutions find their way into new places.

And Podium is one of SaaS’s fastest-growing companies. Cribbing from some prior reporting, Podium’s ARR reached roughly $30 million at the end of 2017. It expected to reach $60 million by the end of 2018, and had $100 million in its sights for 2019. Those figures, collected in November, are now decidedly out of date. But they illustrate how quickly Podium was growing before it added payments to its arsenal.

Update: Adding a little clarification here. The addition of payments to Podium’s tech allows its customers (the companies using its software) to collect payments from their own customers. This gives Podium customers the ability to charge folks for their goods and services in a manner that is integrated into the rest of the software company’s service.

I wanted to dig into the news, so I emailed with Eric Rea, the company’s CEO. What follows is an email exchange (due to scheduling difficulties). We’ll chat after about what was said.

TechCrunch: Did Podium build out its own payments tech or does it employ third-party tech like Finix?

Podium: Podium has a great relationship with Stripe, a fellow Y Combinator company, which was partnered with our own technology to make it work best for our customers. This was key in order to create a payment tool that actually works in the kinds of businesses we work with. [The] majority of businesses who operate from a physical location, from dentist offices and home services companies to larger retail stores, have very specific needs that haven’t been met by traditional card present or POS systems. As a result, many of them rely on mailing paper invoices or awkward conversations where someone gives their card info over the phone. Putting Podium’s platform technology alongside Stripe’s best-in-class processing tech was able to finally meet this need for the companies that create roughly a third of the US non-farming GDP.

TechCrunch: Does the majority of the economics (profit/margin) from the payments product accrue to the Podium client, or Podium itself?

Podium: The genius behind this product is just how immense the economic impact is for these companies. For many of them, they are able to create a whole new convenient way to serve their customers through conversational commerce, and in doing so, they are able to be more successful.

One of our major furniture retailers that participated in the beta of Payments told me about how there has been a completely new selling motion that has opened up for their stores through this product. One of their biggest leaks was when customers would come in and look at a couch or dresser, but didn’t know if dimensions would work in their home. Once they left, there was a steep drop off getting them back into the store to actually make the purchase.

Now, with Payments, they are able to give all the info to their customer, have them check it out in their home and then text them if it works or not. They can then use Payments to collect payment in the very same text conversation and the delivery crew can complete the purchase all in the same day without having the customer return to the store. So it’s not just shifting where they are processing their payments, but opening up new revenue that they would never have had before they started using Payments.

Then consider the ancient process that businesses are still using who invoice for services, like a dentist or a home services provider. A majority are still using mailed statements and invoices or phone conversations. Believe it or not, the expenses for these are immense. Not only that, but the turnaround and success rates are abysmal, meaning these businesses have to wait weeks to months in order to receive payment, if at all. With Payments, it is as quick as a seamless text.

In our beta, Payments tripled the conversion rates over invoices and reduced employee workload related to payment by 80%. In healthcare, for example, 40% of customers send payment within 48 hours. To get that same level through their legacy operations, it would take 14 days to get to that point. The economic impact on that speed and completion is astounding for these businesses.

On the processing, Podium sees the profit on the transaction cost.

TechCrunch: Does Podium anticipate that payments will provide material revenue over the next 18 months? 36?

Podium: Yes. We see this as being the second major phase of the Podium platform. We have been proud to have created one of the fastest-growing SaaS companies in history through our existing products. We have 43,000 businesses currently using Podium, and one of the biggest things they have all been telling us is how much they need a tool like this. Just in our existing customer base and verticals, they are creating more than $100B in gross processing volume annually in payments that are better suited to be done through this tool.

TechCrunch: How long did it take to build out the tech?

Podium: This product actually took the longest of all of our products to develop, given the unique expectations and requirements it took on the technology side. This product has been about a year in the making. When it comes to the business of making money and us being the facilitator of that, we take it very seriously to ensure the tool is secure and stable.

TechCrunch: What percent of Podium customers are good candidates to use the tech?

Podium: Almost universal. We gave a lot of intention behind making this a tool that would work across market verticals so that our customers could provide a better experience for their customers and get paid faster at the same time.

TechCrunch: What is the fee and cost structure?

Podium: We charge a flat rate for processing, which is intentional to allow transparency and consistency in their fees.

It’s not a surprise that Podium is taking the economics of the payment processing (with Stripe doing well at the same time). This means that Podium’s business itself will grow thanks to its addition.

At the same time, the clients using Podium’s platform also do well. If the feature can assist as many companies as Podium expects, then it could help a host of small, local firms boost their sales by improving their respective close rates. Even merely faster payments could help smaller shops better manage their cash flow.

So this feels a bit like a win-win. And it goes to show that the addition of payments to other bits of tech is more than hype (Finix will like that). Instead, it feels like adding the ability for transactions to flow directly through one’s platform is going to rise in popularity. Podium is not the first to the trend, and it won’t be the last. But it is a company that could accelerate the trend thanks to its scale and, so far at least, success.

What we’d love to see, frankly, is an S-1 from Podium this year; that would allow us to better dissect its business. Now at least we’ll have one more thing to look for when we do get the document.

Powered by WPeMatico

TechCrunch has learned that $28 million-funded crypto startup Tagomi will be the newest member of the Libra Association that governs the Facebook-backed Libra stablecoin. A formal announcement is slated for Friday or next week.

Tagomi offers a platform that helps large traders and funds easily access cryptocurrency markets. The news comes days after Libra added Shopify, a reversal of dwindling membership after major partners like Visa, PayPal and Stripe dropped out late last year.

We’ve reached out to the Libra Association and have been promised a response by Facebook’s communications team.

Joining Libra means Tagomi will be expected to contribute at least $10 million toward developing the cryptocurrency, with that investment eligible to reap dividends from interest earned on money kept in the Libra Reserve. Tagomi will also operate a node that validates transactions coming through the Libra blockchain.

Tagomi was founded by Jennifer Campbell, a former investor at Union Square Ventures, which is also a Libra Association Member. The company has 25 employees across five offices. Tagomi will be the 22nd member of the Libra Association, according to information from the startup’s press representative, who was apparently supposed to hold this news until later. “Tagomi is joining the Libra Foundation and Jennifer will be the newest member,” they emailed TechCrunch. We’ll update this story following our interview with Campbell tomorrow.

Campbell and Tagomi will offer technical and policy support to Libra in an effort to make the cryptocurrency more safe and compliant with international law. That will be critical for the Libra Association to get the green light from regulators for a launch in 2020 like it originally planned. Lawmakers in the U.S. and EU have slammed Libra in hearings and the press over its potential to facilitate money laundering, harm privacy and destabilize the global financial system.

The full membership of the Libra Association is now:

Current Members:

Facebook’s Calibra, Tagomi, Shopify, PayU, Farfetch, Lyft, Spotify, Uber, Illiad SA, Anchorage, Bison Trails, Coinbase, Xapo, Andreessen Horowitz, Union Square Ventures, Breakthrough Initiatives, Ribbit Capital, Thrive Capital, Creative Destruction Lab, Kiva, Mercy Corps, Women’s World Banking.

Former Members:

Vodafone, Visa, Mastercard, Stripe, PayPal, Mercado Pago, Bookings Holdings, eBay.

Powered by WPeMatico