payments

Auto Added by WPeMatico

Auto Added by WPeMatico

It’s raised $5.7 billion from Facebook. It’s taken $1.5 billion from KKR, another $1.5 billion from Vista Equity Partners, $1.5 billion from Saudi Arabia’s Public Investment Fund, $1.35 billion from Silver Lake, $1.2 billion from Mubadala, $870 million from General Atlantic, $750 million from Abu Dhabi Investment Authority, $600 million from TPG, and $250 million from L Catterton.

And it’s done all that in just nine weeks.

India’s Reliance Jio Platforms is the world’s most ambitious tech company. Founder Mukesh Ambani has made it his dream to provide every Indian with access to affordable and comprehensive telecommunications services, and Jio has so far proven successful, attracting nearly 400 million subscribers in just a few years.

The unparalleled growth of Reliance Jio Platforms, a subsidiary of India’s most-valued firm (Reliance Industries), has shocked rivals and spooked foreign tech companies such as Google and Amazon, both of which are now reportedly eyeing a slice of one of the world’s largest telecom markets.

What can we learn from Reliance Jio Platforms’s growth? What does the future hold for Jio and for India’s tech startup ecosystem in general?

Through a series of reports, Extra Crunch is going to investigate those questions. We previously profiled Mukesh Ambani himself, and in today’s installment, we are going to look at how Reliance Jio went from a telco upstart to the dominant tech company in four years.

Months after India’s richest man, Mukesh Ambani, launched his telecom network Reliance Jio, Sunil Mittal of Airtel — his chief rival — was struggling in public to contain his frustration.

That Ambani would try to win over subscribers by offering them free voice calling wasn’t a surprise, Mittal said at the World Economic Forum in January 2017. But making voice calls and the bulk of 4G mobile data completely free for seven months clearly “meant that they have not gotten the attention they wanted,” he said, hopeful the local regulator would soon intervene.

This wasn’t the first time Ambani and Mittal were competing directly against each other: in 2002, Ambani had launched a telecommunications company and sought to win the market by distributing free handsets.

In India, carrier lock-in is not popular as people prefer pay-as-you-go voice and data plans. But luckily for Mittal in their first go around, Ambani’s journey was cut short due to a family feud with his brother — read more about that here.

Powered by WPeMatico

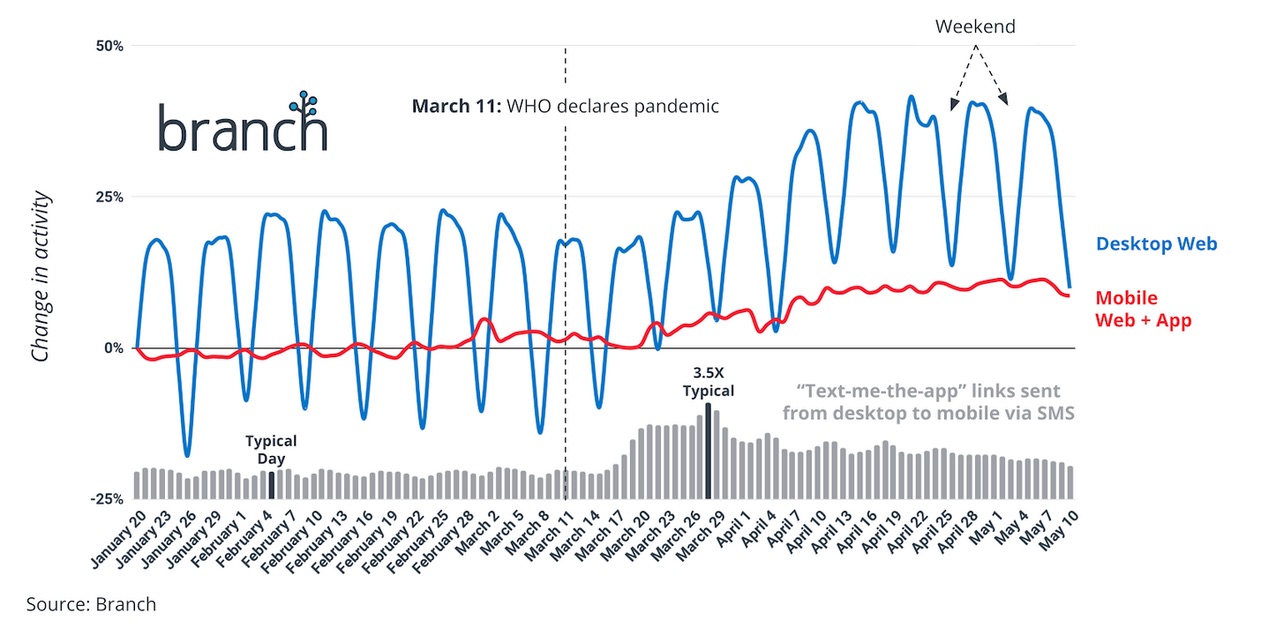

COVID-19 has transformed the way Americans use their phones and the way they spend their time and money online. These shifts present both a number of challenges and a raft of opportunities for savvy growth marketers.

We’ve seen COVID-19 affect a number of verticals. A number of industries have taken a hit (like music streaming and sports), while some are expanding due to the pandemic (groceries, media, video gaming). Others have found distinctive ways to adjust the way they position and sell their product, allowing them to take advantage of changes in buyer behavior.

The key to being able to read and react to changes in this still-tumultuous time and tailoring your growth marketing accordingly is to understand how public sentiment is reflected in new purchasing behaviors. Here’s an overview of the most important trends we’re seeing that will allow you to adjust your growth marketing effectively.

Virtually all of the data we’ve seen shows a marked difference in buyer behavior following the WHO’s declaration of a pandemic on March 11, 2020. With consumers encouraged to stay home to deter the spread of COVID-19, it’s no surprise that the biggest change is the spike in online activity.

Image Credits: Branch (opens in a new window)

Powered by WPeMatico

WhatsApp is adding support for in-app payments, Apple is upgrading the MacBook Pro and Mac Pro desktop and we argue about the future of startup hubs.

Here’s your Daily Crunch for June 15, 2020.

1. WhatsApp finally launches payments, starting in Brazil

After months of talks and trials, WhatsApp has finally pulled the trigger on payments. Users in Brazil will be the first to be able to send and receive money through the messaging app, using Facebook Pay.

WhatsApp says that the payments service — which currently is free for consumers to use, but comes with a 3.99% processing fee for businesses receiving payments — will work by way of a six-digit PIN or fingerprint to complete transactions.

2. Apple adds new MacBook Pro graphics option and Mac Pro SSD upgrade kit

A week before kicking off WWDC, Apple introduced a pair of upgrades to its pro-level hardware lines. Both the 16-inch MacBook Pro and the Mac Pro desktop are getting select internal upgrades, starting today.

3. 3 perspectives on the future of SF and NYC as startup hubs

Three TechCrunch writers address one of the big questions about the future: Will tech continue to centralize in hubs like San Francisco and New York City, or will remote work and all the other second-order effects lead to a more decentralized startup ecosystem? (Extra Crunch membership required.)

4. Interstellar Technologies’ privately developed MOMO-5 rocket falls short of reaching space

The company first launched a vehicle in 2017, but the launch didn’t go exactly as planned and failed to reach space. In 2019, its MOMO-3 sounding rocket did break the Karman line, though just barely, and unfortunately its MOMO-5 sounding rocket launched over the weekend did not make space, as planned.

5. Introducing The Exchange, your daily dive into the private markets

The Exchange is Alex Wilhelm’s regular dive into the financial side of the startup world, and how the public markets exert gravity (or lift) on private companies. These themes might sound familiar to Daily Crunch readers, since we’ve linked to plenty of Alex’s pieces, but now it’s an official column with an official name.

6. Tesla’s US-made Model 3 vehicles now come equipped with wireless charging and USB-C ports

Tesla Model 3 vehicles produced at its Fremont, Calif. factory will reportedly come standard with a wireless charging pad and USB-C ports, upgrades that were first spotted by Drive Tesla Canada.

7. This week’s TechCrunch podcasts

The latest full-length episode of Equity discusses Facebook’s new startup venture fund, while the Monday news roundup covers the latest problems at Quibi. Over at Original Content, we review the latest season of “Queer Eye.”

The Daily Crunch is TechCrunch’s roundup of our biggest and most important stories. If you’d like to get this delivered to your inbox every day at around 9am Pacific, you can subscribe here.

Powered by WPeMatico

Khatabook, a startup that is helping small businesses in India record financial transactions digitally and accept payments online with an app, has raised $60 million in a new financing round as it looks to gain more ground in the world’s second most populous nation.

The new financing round, Series B, was led by Facebook co-founder Eduardo Saverin’s B Capital. A range of other new and existing investors, including Sequoia India, Partners of DST Global, Tencent, GGV Capital, RTP Global, Hummingbird Ventures, Falcon Edge Capital, Rocketship.vc and Unilever Ventures, also participated in the round, as did Facebook’s Kevin Weil, Calm’s Alexander Will, CRED’s Kunal Shah and Snapdeal co-founders Kunal Bahl and Rohit Bansal.

The one-and-a-half-year-old startup, which closed its Series A financing round in October last year and has raised $87 million to date, is now valued between $275 million to $300 million, a person familiar with the matter told TechCrunch.

Hundreds of millions of Indians came online in the last decade, but most merchants — think of neighborhood stores — are still offline in the country. They continue to rely on long notebooks to keep a log of their financial transactions. The process is also time-consuming and prone to errors, which could result in substantial losses.

Khatabook, as well as a handful of young and established players in the country, is attempting to change that by using apps to allow merchants to digitize their bookkeeping and also accept payments.

Today more than 8 million merchants from over 700 districts actively use Khatabook, its co-founder and chief executive Ravish Naresh told TechCrunch in an interview.

“We spent most of last year growing our user base,” said Naresh. And that bet has worked for Khatabook, which today competes with Lightspeed -backed OkCredit, Ribbit Capital-backed BharatPe, Walmart’s PhonePe and Paytm, all of which have raised more money than Khatabook.

The Khatabook team poses for a picture (Khatabook)

According to mobile insight firm AppAnnie, Khatabook had more than 910,000 daily active users as of earlier this month, ahead of Paytm’s merchant app, which is used each day by about 520,000 users, OkCredit with 352,000 users, PhonePe with 231,000 users and BharatPe, with some 120,000 users.

All of these firms have seen a decline in their daily active users base in recent months as India enforced a stay-at-home order for all its citizens and shut most stores and public places. But most of the aforementioned firms have only seen about 10-20% decline in their usage, according to AppAnnie.

Because most of Khatabook’s merchants stay in smaller cities and towns that are away from large cities and operate in grocery stores or work in agritech — areas that are exempted from New Delhi’s stay-at-home orders, they have been less impacted by the coronavirus outbreak, said Naresh.

Naresh declined to comment on AppAnnie’s data, but said merchants on the platform were adding $200 million worth of transactions on the Khatabook app each day.

In a statement, Kabir Narang, a general partner at B Capital who also co-heads the firm’s Asia business, said, “we expect the number of digitally sophisticated MSMEs to double over the next three to five years. Small and medium-sized businesses will drive the Indian economy in the era of COVID-19 and they need digital tools to make their businesses efficient and to grow.”

Khatabook will deploy the new capital to expand the size of its technology team as it looks to build more products. One such product could be online lending for these merchants, Naresh said, with some others exploring to solve other challenges these small businesses face.

Amit Jain, former head of Uber in India and now a partner at Sequoia Capital, said more than 50% of these small businesses are yet to get online. According to government data, there are more than 60 million small and micro-sized businesses in India.

India’s payments market could reach $1 trillion by 2023, according to a report by Credit Suisse .

Powered by WPeMatico

Starting today, TechCrunch readers can send an Extra Crunch annual membership as a gift to a friend, family member or co-worker. For a limited time we’re offering the gift at a discounted rate of $99/year (plus tax).

The gifting feature can be found here.

Extra Crunch membership is designed for startup teams, entrepreneurs, investors and business school students, and it includes more than 100 exclusive articles per month:

Extra Crunch membership can save you time time with an exclusive newsletter, no banner ads, Rapid Read mode and our List Builder tool. Annual and two-year members can also save money with discounts on events and access to Partner Perks. Our Partner Perks provide discounted access to services from companies like AWS, Brex, DocSend, Crunchbase, Typeform and more.

Gifting is currently supported in the U.S., Canada, U.K. and select countries in Europe. Purchases can be made through Visa, Mastercard and PayPal in all supported countries, but Amex support is limited to the U.S. and Canada.

If there are other features you’d like to see us add to Extra Crunch, please let us know by leaving a comment on this post or emailing me directly at travis@techcrunch.com.

TechCrunch readers can find the Extra Crunch gifting feature here.

Powered by WPeMatico

The economic effects of COVID-19 could delay Africa’s next big IPO — that of Nigerian fintech unicorn Interswitch.

If so, it wouldn’t be the first time the Lagos-based payments company’s plans for going public were postponed; the tech world has been anticipating Interswitch’s stock market debut since 2016.

For the continent’s innovation ecosystem, there’s a lot riding on the digital finance company’s IPO. After e-commerce venture Jumia, it would become only the second listing of a VC-backed African tech company on a major exchange. And Interswitch’s stock market debut — when it occurs — could bring more investor attention and less controversy to the region’s startup scene.

TechCrunch reached out to Interswitch on the window for listing, but the company declined to comment. The tech firm’s path from startup to IPO aspirant traces back to the vision of founder Mitchell Elegbe, a Nigerian electrical engineering graduate whose entire career has pretty much been Interswitch.

Africa’s tech scene is still fairly young, but it does have a timeline with several definitive points. An early one would be the success of mobile money in East Africa, with the launch of Safaricom’s M-Pesa in 2007. Another is the notable wave of VC-backed startups and founders that launched around 2010.

Interswitch CEO Mitchell Elegbe (Photo Credits: Interswitch)

With Interswtich, Elegbe pre-dated both by a number of years, founding his fintech company back in 2002 to connect Nigeria’s largely disconnected banking system. The firm became a pioneer of the infrastructure to digitize Nigeria’s economy.

Interswitch created the first electronic switch whereby Nigerian financial institutions could communicate and thereby operate ATMs and point of sales operations. The company now provides much of the rails for Nigeria’s online banking system.

Powered by WPeMatico

WhatsApp, which began testing its mobile payments feature in India two years ago, could offer at least one more financial service to people in its biggest market.

In a filing with the local regulator in India, the company has listed credit as one of the areas it will pursue in the country. The Facebook -owned service declared with the local regulator earlier this month providing credit or loans as one of the “main objects to be pursued by it in the country.” No other financial service is listed in the filing.

At an event in Bangalore late last year, Abhijit Bose, WhatsApp’s head in India, said he believed that the mobile payments market in India, which has attracted dozens of local and international firms in recent years, is still at a very early stage in the country and may eventually see firms move beyond just offering a way for people to send money to one another.

WhatsApp has yet to receive approval from New Delhi for a nationwide rollout of Pay in India. Local media reports claimed earlier this year that WhatsApp had started to expand Pay’s reach in the country in various phases.

Ajit Mohan, a Facebook VP and India head, told TechCrunch in an interview last week that only 1 million WhatsApp users in India, same as before, have access to its mobile payment service.

Dozens of payment services in India have expanded to credit, or online lending, in recent quarters as they search for a business model in the country. A number of firms, including Paytm, India’s most-valued startup, and MobiKwik today offer small ticket credit to millions of users in India.

Tens of millions of users have started to digitally transact money in India in recent years. But the local payments body has removed most of the fees they could levy on banks and merchants to make money. The move has resulted in firms exploring other financial services, such as credit and insurance and target merchants to make money.

This year, Paytm has expanded to serve merchants, launching new gadgets such as a stand that displays QR check-out codes that comes with a calculator and a battery pack, a portable speaker that provides voice confirmations of transactions and a point-of-sale machine with built-in scanner and printer.

The Alibaba and SoftBank-backed company is offering these gadgets as part of a subscription service that helps it establish a steady flow of revenue. Paytm’s Money arm, which offers lending, insurance and investing services, has amassed more than 3 million users.

Flipkart’s PhonePe, another major player in India’s payments market, today serves more than 175 million users and over 8 million merchants. Its app serves as a platform for other businesses to reach users. The company is currently not taking a cut for the real estate on its app.

WhatsApp’s expansion in mobile payments in India, estimated to grow to $1 trillion by 2023 (according to Credit Suisse), could create new challenges for the aforementioned players.

Facebook, which like other American tech giants counts India as one of its biggest markets but makes considerably less revenue in the world’s second largest market, “reaffirmed” its commitment to India this month.

The social giant invested $5.7 billion in Reliance Jio Platforms this month to acquire a 9.99% stake in the Indian telecom giant. Over the weekend, JioMart, an e-commerce venture run by Jio’s parent firm, began testing an “ordering system” on WhatsApp, teasing the first peek at the collaboration between Facebook and Indian telecom giant Reliance Jio Platforms.

Powered by WPeMatico

At a time when more transactions than ever are happening online, payments behemoth Stripe is announcing three new features to continue expanding its reach.

The company today announced that it will now offer card issuing services directly to businesses to let them in turn make credit cards for customers tailored to specific purposes. Alongside that, it’s going to expand the number of accepted local, large card networks to cut down some of the steps it takes to make transactions in international markets. And finally, it’s launching a “revenue optimization” feature that essentially will use Stripe’s AI algorithms to reassess and approve more flagged transactions that might have otherwise been rejected in the past.

Together the three features underscore how Stripe is continuing to scale up with more services around its core payment processing APIs, a significant step in the wake of last week announcing its biggest fundraise to date: $600 million at a $36 billion valuation.

The rollouts of the new products are specifically coming at a time when Stripe has seen a big boost in usage among some (but not all) of its customers, said John Collison, Stripe’s co-founder and president, in an interview. Instacart, which is providing grocery delivery at a time when many are living under stay-at-home orders, has seen transactions up by 300% in recent weeks. Another newer customer, Zoom, is also seeing business boom. Amazon, Stripe’s behemoth customer that Collison would not discuss in any specific terms except to confirm it’s a close partner, is also seeing extremely heavy usage.

But other Stripe users — for example, many of its sea of small business users — are seeing huge pressures, while still others, faced with no physical business, are just starting to approach e-commerce in earnest for the first time. Stripe’s idea is that the launches today can help it address all of these scenarios.

“What we’re seeing in the COVID-19 world is that the impact is not minor,” said Collison. “Online has always been steadily taking a share from offline, but now many [projected] years of that migration are happening in the space of a few weeks.”

Stripe is among those companies that have been very mum about when they might go public — a state of affairs that only become more set in recent times, given how the IPO market has all but dried up in the midst of a health pandemic and economic slump. That has meant very little transparency about how Stripe is run, whether it’s profitable and how much revenues it makes.

But Stripe did note last week that it had some $2 billion in cash and cash reserves, which at least speaks to a level of financial stability. And another hint of efficiency might be gleaned from today’s product news.

While these three new services don’t necessarily sound like they are connected to each other, what they have underpinning them is that they are all building on top of tech and services that Stripe has previously rolled out. This speaks to how, even as the company now handles some 250 million API requests daily, it’s keeping some lean practices in place in terms of how it invests and maximises engineering and business development resources.

The card issuing service, for example, is built on a card service that Stripe launched last year. Originally aimed at businesses to provide their employees with credit cards — for example to better manage their own work-related expenses, or to make transactions on behalf of the business — now businesses can use the card issuing platform to build out aspects of its customer-facing services.

For example, Stripe noted that the first customer, Zipcar, will now be placing credit cards in each of its vehicles, which drivers can use to fuel up the vehicles (that is, the cards can only be used to buy gas). Another example Collison gave for how these could be implemented would be in a food delivery service, for example for a Postmates delivery person to use the card to pay for the meal that a customer has already paid Postmates to pick up and deliver to them.

Collison noted that while other startups like Marqeta have built big businesses around innovative card issuing services, “this is the first time it’s being issued on a self-serving basis,” meaning companies that want to use these cards can now set this up more quickly as a “programmatic card” experience, akin to self-serve, programmatic ads online.

It seems also to be good news for investors. “Stripe Issuing is a big step forward,” said Alex Rampell, general partner at Andreessen Horowitz, in a statement. “Not just for the millions of businesses running on Stripe, but for credit cards as a fundamental technology. Businesses can now use an API to create and issue cards exactly when and where they need them, and they can do it in a few clicks, not a few months. As investors, we’re excited by all the potential new companies and business models that will emerge as a result.”

Meanwhile, the revenue “optimization” engine that Stripe is rolling out is built on the same machine learning algorithms that it originally built for Radar, its fraud prevention tool that originally launched in 2016 and was extended to larger enterprises in 2018. This makes a lot of sense, since oftentimes the reason transactions get rejected is because of the suspicion of fraud. Why it’s taken four years to extend that to improve how transactions are approved or rejected is not entirely clear, but Stripe estimates that it could enable a further $2.5 billion in transactions annually.

One reason why the revenue optimization may have taken some time to roll out was because while Stripe offers a very seamless, simple API for users, it’s doing a lot of complex work behind the scenes knitting together a lot of very fragmented payment flows between card issuers, banks, businesses, customers and more in order to make transactions possible.

The third product announcement speaks to how Stripe is simplifying a bit more of that. Now, it’s able to provide direct links into six big card networks — Visa, Mastercard, American Express, Discover, JCB and China Union Pay, which effectively covers the major card networks in North and Latin America, Southeast Asia and Europe. Previously, Stripe would have had to work with third parties to integrate acceptance of all of these networks in different regions, which would have cut into Stripe’s own margins and also given it less flexibility in terms of how it could handle the transaction data.

Launching the revenue optimization by being able to apply machine learning to the transaction data is one example of where and how it might be able to apply more innovative processes from now on.

While Stripe is mainly focused today on how to serve its wider customer base and to just help business continue to keep running, Collison noted that the COVID-19 pandemic has had a measurable impact on Stripe beyond just boosts in business for some of its customers.

The whole company has been working remotely for weeks, including its development team, making for challenging times in building and rolling out services.

And Stripe, along with others, is also in the early stages of piloting how it will play a role in issuing small business loans as part of the CARES Act, he said.

In addition to that, he noted that there has been an emergence of more medical and telehealth services using Stripe for payments.

Before now, many of those use cases had been blocked by the banks, he said, for reasons of the industries themselves being strictly regulated in terms of what kind of data could get passed across networks and the sensitive nature of the businesses themselves. He said that a lot of that has started to get unblocked in the current climate, and “the growth of telemedicine has been off the charts.”

Powered by WPeMatico

Meet Libeo, a French startup that just raised a $4.4 million (€4 million) funding round led by LocalGlobe, with Breega and various business angels also participating. The company has built a service that helps you pay your providers much more easily. You no longer have to manually keep track of invoices, log into your banking interface, enter banking information and transfer money.

Libeo targets small and medium companies that don’t necessarily have a dedicated accounting team. It wants to simplify payment processes as much as possible.

It starts by collecting invoices from your suppliers. You can import invoices to your Libeo account directly on Libeo by forwarding emails to a special address, by connecting Libeo to popular services, such as Amazon, or by connecting Libeo with your existing accounting platform, such as QuickBooks or Receipt Bank.

Once your invoices are all on Libeo, the startup automatically fills out payment information based on information on the invoice. It also can identify duplicates and keep track of VAT payments.

After that, Libeo wants to simplify payments. When you sign up, you share your company’s IBAN with Libeo so that it can take money from your account using direct debits. Whenever there’s an outstanding invoice in your Libeo account, you can decide to pay it now or schedule payment for later. Libeo transfers money to your recipient and collects money from your bank account at the same time.

What if it’s a new supplier and you don’t have their banking information? Instead of going back and forth with your supplier to get their IBAN, your supplier receives an email from Libeo with a link. The supplier drags and drops their bank details on Libeo’s web page. Libeo then checks that everything matches with the invoice and automatically adds the IBAN information to the payment.

Over time, if you use Libeo, you get an address book of all your suppliers. You can see how much you’re spending with a specific supplier, track your cash flow and more.

Like modern software-as-a-service tools, Libeo lets you collaborate on your invoices. Multiple people can have a Libeo account with different rights. You can set up an approval workflow as well.

There’s a free plan, but it’s limited to five payments per month. You can then pay to access advanced features and get bigger limits. Five thousand companies are currently using Libeo four months after the initial release. The company has facilitated €2 million in payments.

Powered by WPeMatico

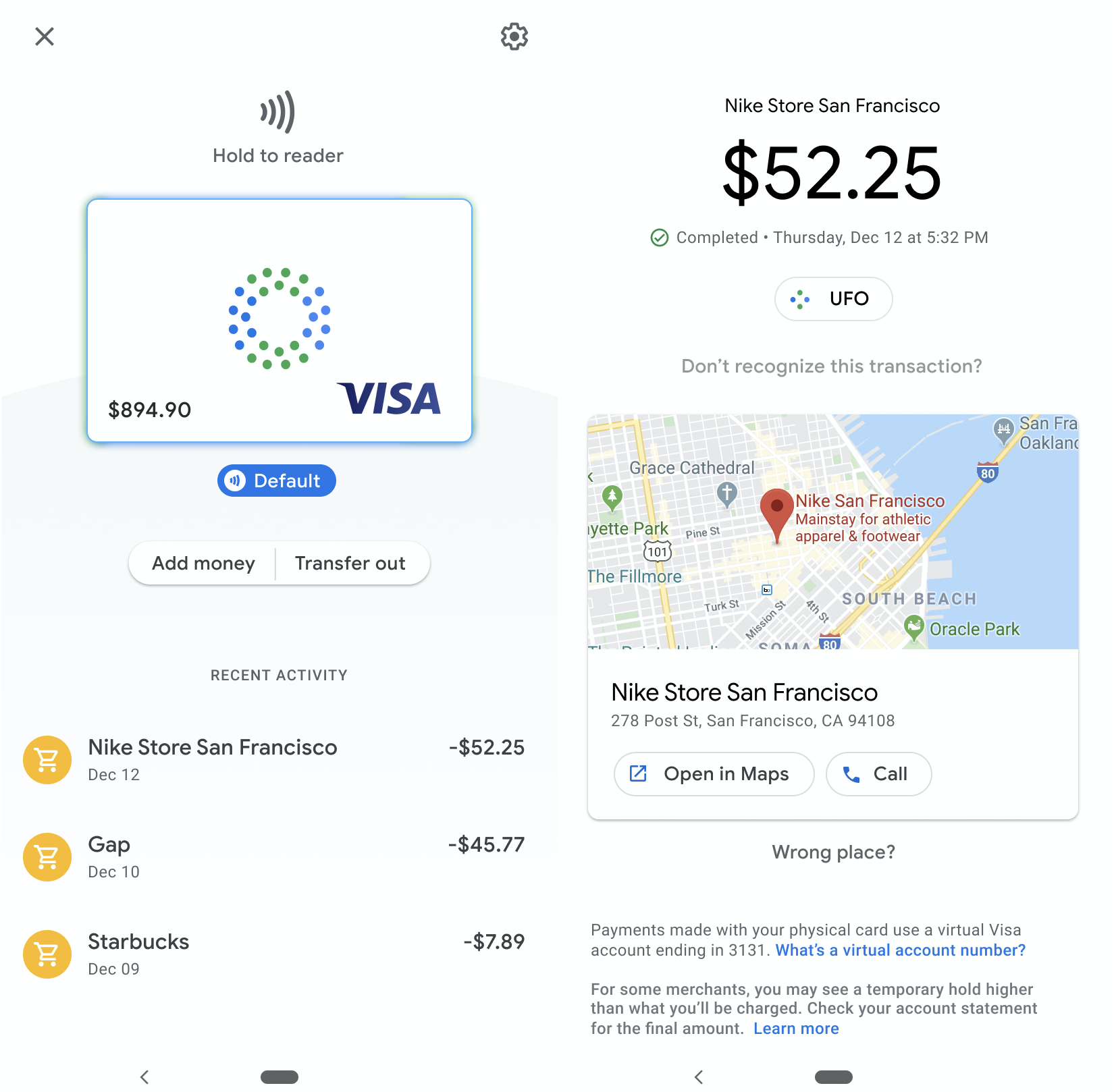

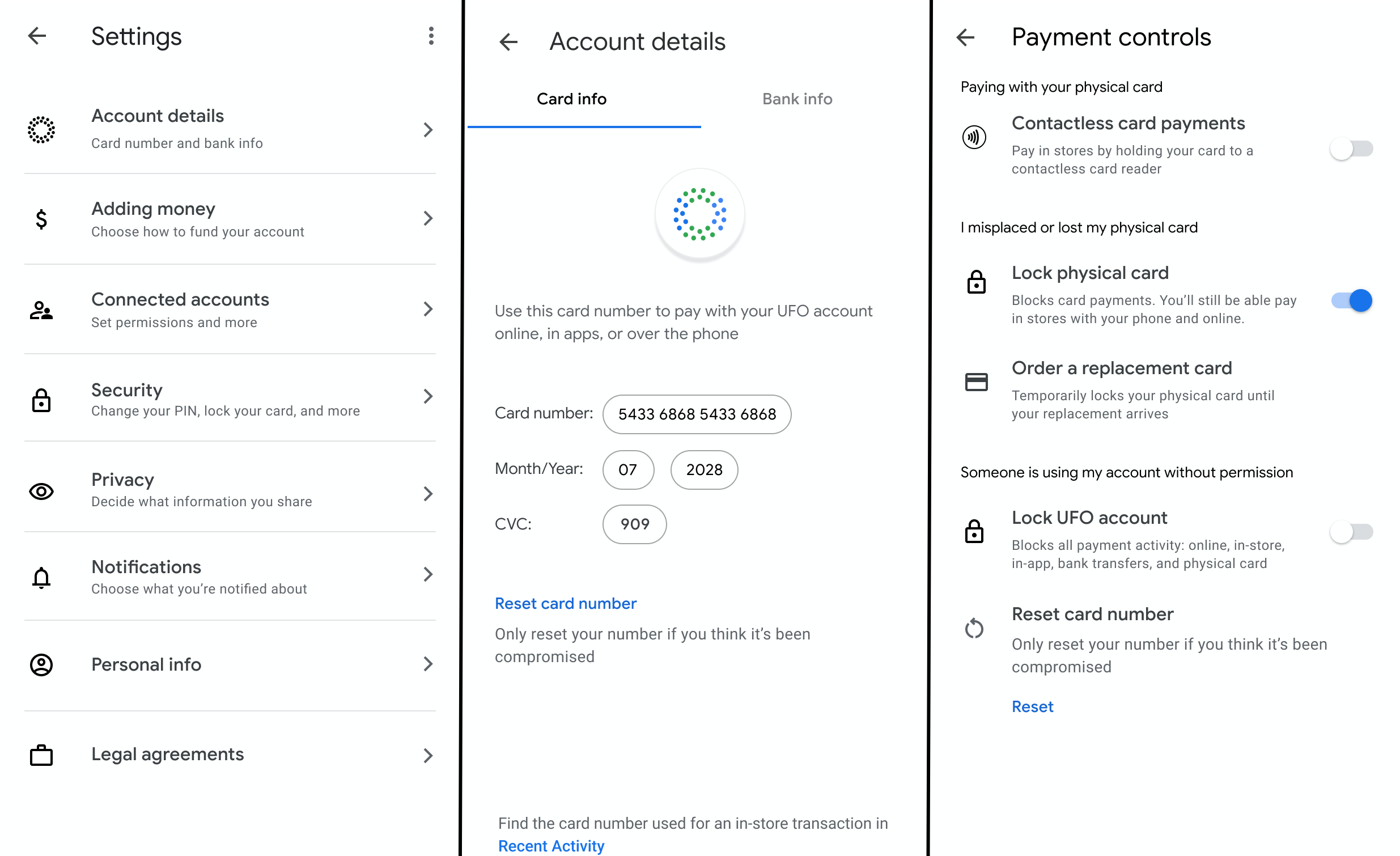

Would you pay with a “Google Card?” TechCrunch has obtained imagery that shows Google is developing its own physical and virtual debit cards. The Google card and associated checking account will allow users to buy things with a card, mobile phone or online. It connects to a Google app with new features that let users easily monitor purchases, check their balance or lock their account. The card will be co-branded with different bank partners, including CITI and Stanford Federal Credit Union.

A source provided TechCrunch with the images seen here, as well as proof that they came from Google. Another source confirmed that Google has recently worked on a payments card that its team hopes will become the foundation of its Google Pay app — and help it rival Apple Pay and the Apple Card. Currently, Google Pay only allows online and peer-to-peer payments by connecting a traditionally issued payment card. A “Google Pay Card” would vastly expand the app’s use cases, and Google’s potential as a fintech giant.

By building a smart debit card, Google has the opportunity to unlock new streams of revenue and data. It could potentially charge interchange fees on purchases made with the card or other checking account fees, and then split them with its banking partners. Depending on its privacy decisions, Google could use transaction data on what people buy to improve ad campaign measurement or even targeting. Brands might be willing to buy more Google ads if the tech giant can prove they drive a sales lift.

The long-term implications are even greater. While once the industry joke was that every app eventually becomes a messaging app, more recently it’s been that every tech company eventually becomes a financial services company. A smart debit card and checking accounts could pave the way for Google offering banking, stock brokerage, financial advice or robo-advising, accounting, insurance or lending.

Image Credits: jossnatu / Getty Images

Google’s vast access to data could allow it to more accurately manage risk than traditional financial institutions. Its deep connection to consumers via apps, ads, search and the Android operating system gives it ample ways to promote and integrate financial services. With the COVID-19 downturn taking shape, high-margin finance products could help Google develop efficient revenue opportunities and build its share price back up.

When TechCrunch asked Google for confirmation, it did not dispute our findings or assertions. The company offered us a statement it provided reporters following a November story, wherein Google told The Wall Street Journal’s Peter Rudegeair and Liz Hoffman it was experimenting in the checking account space. TechCrunch is the first to report Google’s debit card plans:

We’re exploring how we can partner with banks and credit unions in the US to offer smart checking accounts through Google Pay, helping their customers benefit from useful insights and budgeting tools, while keeping their money in an FDIC or NCUA-insured account. Our lead partners today are Citi and Stanford Federal Credit Union, and we look forward to sharing more details in the coming months.

For now, Google’s strategy is to let partnered banks and credit unions provide the underlying financial infrastructure and navigate regulation while it builds smarter interfaces and user experiences. It’s forseeable that one day Google might cut out the banks and take all the spoils for itself. Google launched a Wallet debit card in 2013 as an extension of its old payment app Google Wallet, but shut the card down in 2016. Given Google’s penchant for renaming or shutting down then reviving products, building a new debit card feels on-brand.

With people around the world suddenly more concerned about their finances amidst the coronavirus economic disaster, a debit card with more transparency and controls could be appealing.

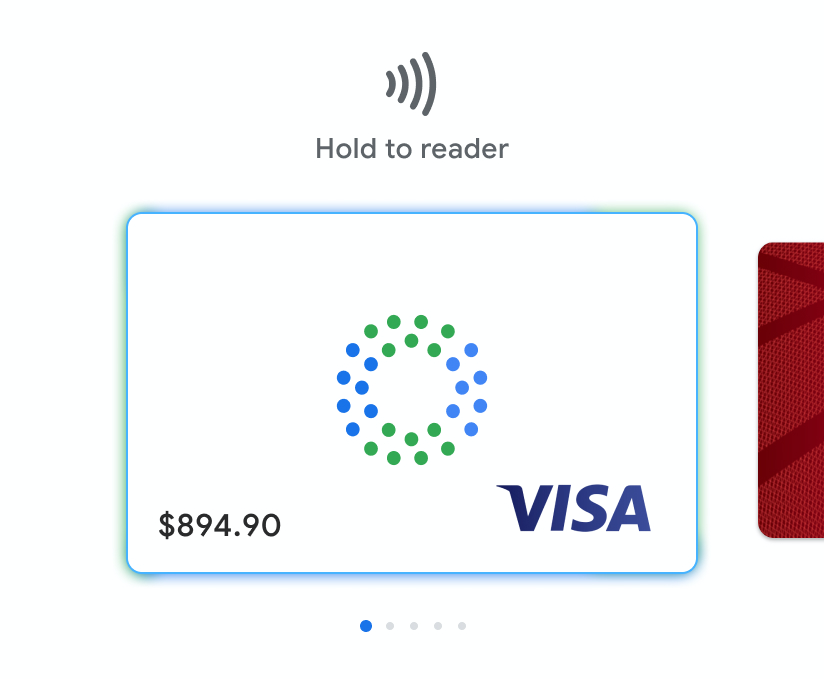

Traditional banking products can be clunky, often requiring phone communication with customer service or sifting through cluttered websites to address security issues. Google hopes to make financial management as intuitive as its email and mapping apps. The card and app designs shown here are not final, and it’s unclear when Google’s debit card may launch. But let’s take a look at what these internal Google materials reveal about its ambitions for its payment instrument.

The Google debit card will come co-branded with the Google name and its partnered bank, though the exact name of the product is still unknown. In the designs, it’s a chip card on the Visa network, though Google could potentially support other networks like Mastercard. Users are able to add money or transfer funds out of their account from the connected Google app, which is likely to be Google Pay, and use a fingerprint and PIN for account security.

Once connected to their bank or credit union account, users could pay for purchases in retail stores with a physical Google debit card, including with contactless payments, by just holding it up to a card reader. A virtual version of the card that lives on a user’s phone can also be used for Bluetooth mobile payments. Meanwhile, a virtual card number can be used for online or in-app payments.

Users are shown a list of recent transactions, with each including the merchant name, date and price. They can dig into each transaction to see the location on a map, get directions or call the store. If users don’t recognize a transaction, it’s easy to protect themselves with the card’s vast security options.

If a customer suspects foul play because they lost their card, they can lock it and optionally order a replacement while still being able to pay with their phone or online, thanks to Google’s virtual card number system that’s different than the one on their physical card. If instead they suspect their virtual card number was stolen by a hacker, they can quickly reset it. And if they believe someone has gained unauthorized access to their account, they can lock it entirely to block all types of payments and transfers.

The settings reveal options for notifications and privacy controls to “decide what information you share,” though we don’t have imagery of what’s contained in those menus. It’s unclear how much power Google will give customers to limit the company or merchant’s data access. Google’s decisions there could impact how transaction data might fuel its other businesses.

Google is a relative late-comer to offering its own card. Apple launched its Apple Card in August, offering a slickly designed titanium Mastercard credit card backed by Goldman Sachs. It charges minimal customer fees, comes with a virtual card for use through Apple Pay and generates interest.

Apple Card

Apple does collect interchange fees from merchants, though, which Google could similarly gather to earn revenue. Last month, Apple changed the Card’s privacy settings to share more data with Goldman Sachs that might also help the two provide additional financial services. Apple Pay now accounts for 5% of global card transactions, and is forecast to hit 10% by 2024, according to Bernstein research. The underlines the gigantic market Google is gunning for here.

The stock brokerage and robo-advisor apps have also joined the payments race. Wealthfront launched cash accounts and debit cards last February, bringing in $1 billion in assets in two months and doubling the company’s total holdings to $20 billion by September. Betterment launched its checking product in October 2019 with a Visa debit card, but it doesn’t generate interest.

Robinhood botched the December 2018 launch of its checking accounts due to ineligible insurance, but relaunched in October 2019 with debit card withdrawls from 75,000 ATMs and a solid interest rate. It’s unclear how Google’s card will work with ATMs or how its checking accounts will generate interest.

Robinhood’s debit cards

The appeal for Google and the rest is clear. It seems whenever companies help move people’s money around, some of it inevitably “falls off the truck” and lands in their pockets. Financial services are typically low-overhead ways to generate revenue. That could be especially enticing, as Google has found many of its side hustle “other bets” to be unsustainable. It’s moved to prune some of these tertiary projects, such as its Makani wind energy kites.

Google may never find businesses as lucrative as its core in search and advertising, but it has the advantages to become a serious player in fintech. Its vast sums of cash, deep bench of engineering talent, experience building complex utilities, numerous consumer touch points and near-bottomless well of data could give it an edge over stodgier old banks and scrappier startups. And while Facebook slams into regulatory scrutiny and is forced to scale back its Libra cryptocurrency, Google’s more familiar approach via debit cards could pay off.

Powered by WPeMatico