payments

Auto Added by WPeMatico

Auto Added by WPeMatico

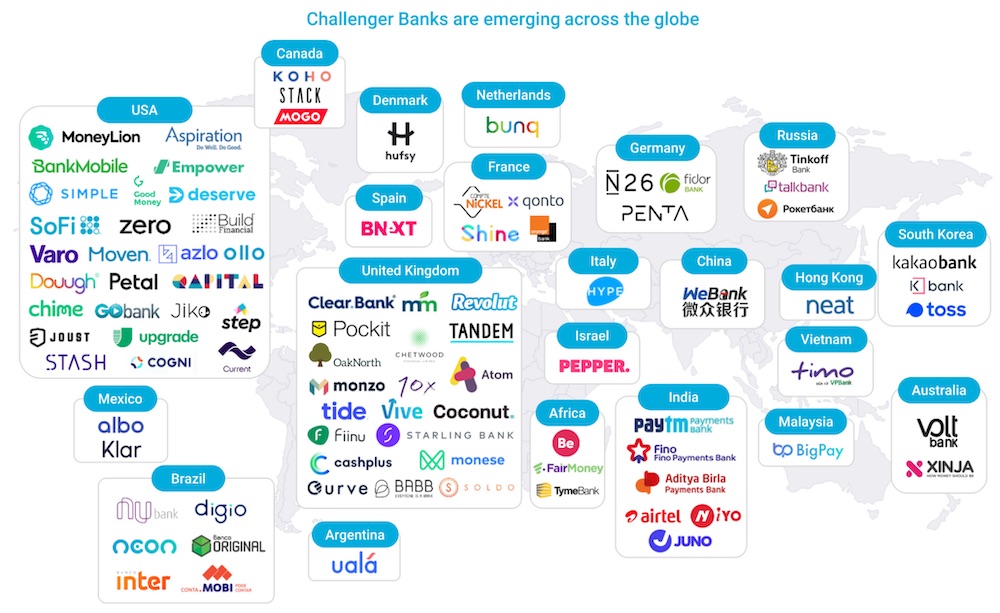

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

Shipping has long been one of the more antiquated, and least technological, segments in the world of commerce, with its physical aspects — rooted in massive cargo tankers, giant fleets of aircraft and trucks, and trains of linked-up containers — underscoring some of the more obvious analogue attributes of the business.

That has also made it a ripe opportunity for startups, and today, one called PayCargo, which has built a suite of cloud-based payment and financing services for the cargo industry, is announcing $35 million in funding to expand its business in the wake of COVID-19.

The investment is coming from a single, high-profile investor, Insight Partners, which back in April announced a monster $9.5 billon fund that it planned to use not just to support portfolio companies through the global health pandemic, but to seek out new opportunities emerging in the wake of it.

PayCargo appears to be one of the latter. Eduardo Del Riego, the CEO (PayCargo was co-founded by COO Juan Carlos Dieppa and chairman Sergio Lemme), said that while the cargo industry has faced a lot of turmoil with the pandemic — production in some places ground to a halt, social distancing rules created new challenges for how shippers could work and move physical goods — it also highlighted how solutions like PayCargo’s were essential in getting things working properly again.

“With COVID, there was tremendous uncertainty about the impact of the global supply chain,” he said in an interview, “and like many other industries, the pandemic accelerated the need and demand for a paperless and contactless solution, which in turn accelerated PayCargo’s business.”

And while many of us brace ourselves for more fallout about how the world economy is contracting, PayCargo is profitable and has been from its start, the company said, and it has been growing — which in itself could be a positive signal about how production is indeed picking up again.

PayCargo provides a platform that offers tools for payers to send payments, vendors to receive them, APIs to integrate the tools into an existing IT, and financing services for those who do not want to pay for the shipments up front. All of these, for the majority of those working in this area, still are fixed in paperwork and can take weeks to resolve, making it a prime area to tackle with electronic services.

These days, PayCargo is processing some $4 billion in payments annually from some 12,000 shippers and carriers and a network of 4,000 vendors — customers span land, sea and air and include Kuehne + Nagel, DHL, DB Schenker, BDP, Seko Logistics, UPS, YUSEN Logistics and vendors like Hapag-Lloyd, MSC, Ocean Network Express, Alliance Ground, Swissport and Air France — with transaction volume up 80% over last year. By way of its APIs, PayCargo also works with a number of partners to serve customers, including the International Air Transport Association (IATA), Cargo Network Services (CNS), CHAMP Cargosystems, IBS, Accelya, Unisys and Kale Logistics.

We have written before about the very fragmented and analogue freight industry, which still bases a lot of transactions around faxes, actual paperwork physically exchanged between parties and people transferring not just goods but documents hand to hand. The same goes for the payments infrastructure that underpins it all.

That has spawned a number of other startups looking to tackle the market with tech. Emerge has been building a digital marketplace specifically for the trucking industry, while Cargo.com is targeting air freight; Europe’s Zencargo, FreightHub and Sennder are focusing on bringing cloud-based infrastructure into freight-forwarding (and Sennder is positioning itself as a consolidator in this market, recently acquiring Uber’s European business in this area); and Flexport has positioned itself as one to watch in its own take on shipping SaaS.

PayCargo itself also has a number of competitors, which might include those building bigger suites of services, of which payments is just one. In addition to all of the ones we’ve covered, there is GlobalTranz, CloudTrade and others. (Del Riego refused to name any competitors directly. “PayCargo is the premier and most robust solution in the marketplace,” he said flatly.)

Overall, CrunchBase estimates that some $5.5 billion has been invested in shipping-related tech companies looking to bring more updated processes to what is, at the end of the day, ultimately a very physical business.

But with the industry significantly bigger than that — one estimate forecasts that the shipping logistics market in the U.S. alone will be worth $1.3 trillion by 2023 — you can see how building and addressing that would be a lucrative opportunity.

“As the cargo industry rapidly shifts to electronic payments, PayCargo has established itself as the market leading platform for doing business by successfully automating the payments process and ensuring efficiency for both payers and vendors,” said Ryan Hinkle, managing director at Insight Partners, in a statement. “We are excited to work with PayCargo to continue to scale its global payments network and through our Insight Onsite team of ScaleUp and operational experts, help bring additional resources to its impressive list of customers.” Hinkle is joining the board with this round.

Powered by WPeMatico

Four years after the Great Recession, France’s newly elected socialist president François Hollande raised taxes and increased regulations on founder-led startups. The subsequent flight of entrepreneurs to places like London and Silicon Valley portrayed France as a tough place to launch a company. By 2016, France’s national statistics bureau estimated that about three million native-born citizens had moved abroad.

Those who remained fought back: The Family was an early accelerator that encouraged French entrepreneurs to adopt Silicon Valley’s startup methodology, and the 2012 creation of Bpifrance, a public investment bank, put money into the startup ecosystem system via investors. Organizers founded La French Tech to beat the drum about native startups.

When President Emmanuel Macron took office in May 2017, he scrapped the wealth tax on everything except property assets and introduced a flat 30% tax rate on capital gains. Station F, a giant startup campus funded by billionaire entrepreneur Xavier Niel on the site of a former railway station, began attracting international talent. Tony Fadell, one of the fathers of the iPod and founder of Nest Labs, moved to Paris to set up investment firm Future Shape; VivaTech was created with government backing to become one of Europe’s largest startup conference and expos.

Now, in the COVID-19 era, the government has made €4 billion available to entrepreneurs to keep the lights on. According to a recent report from VC firm Atomico, there are 11 unicorns in France, including BlaBlaCar, OVHcloud, Deezer and Veepee. More appear to be coming; last year Macron said he wanted to see “25 French unicorns by 2025.”

According to Station F, by the end of August, there had been 24 funding rounds led by international VCs and a few big transactions. Enterprise artificial intelligence and machine-learning platform Dataiku raised a $100 million Series D round, and Paris-based gaming startup Voodoo raised an undisclosed amount from Tencent Holdings.

We asked 12 Paris-based investors to comment on the state of play in their city:

What trends are you most excited about investing in, generally?

All the fintechs addressing SMBs to help them to focus more on their core business (including banks disintermediation by fintech, new infrastructures tech that are lowering the barrier to entry to nonfintech companies).

What’s your latest, most exciting investment?

77foods (plant-based bacon) — love that alternative proteins trend as well. Obviously, we need to transform our diet toward more sustainable food. It’s the next challenge for humanity.

What are you looking for in your next investment, in general?

Impact investment: Logistic companies tackling the life cycle of products to reduce their carbon footprint and green fintech that reinvent our spending and investment strategy around more sustainable products.

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

D2C products.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

100% investing in France as I’m managing Paris Saclay Seed Fund, a €53 million fund, investing in pre-seed and seed startups launched by graduates and researchers from the best engineering and business schools from this ecosystem.

Which industries in your city and region seem well-positioned to thrive, or not, long term? What are companies you are excited about (your portfolio or not), which founders?

Deep tech, biotech and medical devices. Paris, and France in general, has thousands of outstanding engineers that graduate each year. Researchers are more and more willing to found companies to have a true impact on our society. I do believe that the ecosystem is more and more structured to help them to build such companies.

How should investors in other cities think about the overall investment climate and opportunities in your city?

Paris is booming for sure. It’s still behind London and Berlin probably. But we are seeing more and more European VC offices opening in the city to get direct access to our ecosystem. Even in seed rounds, we start to have European VCs competing against us. It’s good — that means that our startups are moving to the next level.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

For sure startups will more and more push for remote organizations. It’s an amazing way to combine quality of life for employees and attracting talent. Yet I don’t think it will be the majority. Not all founders are willing/able to build a fully remote company. It’s an important cultural choice and it’s adapted to a certain type of business. I believe in more flexible organization (e.g., tech team working remotely or 1-2 days a week for any employee).

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

Travel and hospitality sectors are of course hugely impacted. Yet there are opportunities for helping those incumbents to face current challenges (e.g., better customer care and services, stronger flexibility, cost reduction and process automation).

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

Cash is king more than ever before. My only piece of advice will be to keep a good level of cash as we have a limited view on events coming ahead. It’s easy to say but much more difficult to put in practice (e.g., to what extend should I reduce my cash burn? Should I keep on investing in the product? What is the impact on the sales team?). Startups should focus only on what is mission-critical for their clients. Yet it doesn’t impact our seed investments as we invest pre-revenue and often pre-product.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

There is no reason to be hopeless. Crises have happened in the past. Humanity has faced other pandemics. Humans are resilient and resourceful enough to adapt to a new environment and new constraints.

Powered by WPeMatico

Startup incubator and investment group Y Combinator today held the first of two demo days for founders in its Summer 2020 batch.

So far, this cohort contains the usual mix of bold, impressive and, at times, slightly wacky ideas young companies so often show off.

This was Y Combinator’s second online demo day, its first all-virtual class and the first time that it held live, remote pitches. The event largely went well, with founders dialing in from around the globe to share a few paragraphs of notes and a single slide. There were few technical hiccups, given the sheer number of startups presenting.

But if you are not in the mood to parse through dozens (and dozens) of entries detailing each startup that showed off its problem, solution and growth, the TechCrunch crew has collected our own favorites based on how likely a company seems to succeed and how impressed we were with the creativity of their vision. For each entry, one staffer made the call that the startup in question was among their favorites.

We’re not investors, so we’re not pretending to sort the unicorns from the goats. But if what you need is a digest of some of the day’s best companies to get a good taste of what founders are building, we have your back.

The next wave of edtech startups is entering a market that demands a better remote-learning solution for younger learners. But that’s the obvious product gap, one that is already being tackled by the biggest names in the booming category.

The non-obvious product-market deficit is how teachers, also impacted by the pandemic, are searching for new ways to interact with students. Teachers are collaborating and cross-pollinating on successful lesson plans that work across stale Zoom screens, so why not monetize that same content?

Powered by WPeMatico

Max Levchin needs little introduction in the world of tech. As an entrepreneur, he’s been the co-founder of PayPal (now public), Slide (acquired by Google) and Affirm (reportedly about to go public), some of the hottest startups to have come out of Silicon Valley. And as an investor, he’s applied his power of observation and execution also towards helping many others build huge technology businesses.

We sat down with Levchin for a recent session of Extra Crunch Live, where he spoke at length about what he sees as some of the big opportunities in fintech. Here’s an edited version of the conversation. You can watch and listen to the whole discussion — which includes stories about Levchin’s coffee and cycling habits, and how many times he’s seen “The Seven Samurai” (hint: more than once) — here, also embedded below, and you can check out the rest of the pretty cool ECL program here.

Even going as far back as PayPal I think the industry has devolved. I think fintech had the promise of really bringing simplicity, honesty and transparency to the customer. Instead, we ended up putting a really nice user interface on products that are not designed with the user’s best interest in mind. I’m a big fan of throwing shade on credit cards, because I think fundamentally, their business model is remarkably similar to that of payday loans. You are allowed to borrow some money and don’t really know exactly what the terms are. It’s all in the fine print, don’t worry about it and then you just make the minimum payments and you stay in debt. Potentially forever.

Powered by WPeMatico

The COVID-19 pandemic has forced businesses to rethink how they accept and make payments. Paper invoices, checks and point-of-sale payments have given way to “corona-free payments” through mobile apps, electronic invoicing and ACH. Although significant, this is the sideshow to a more significant reshuffling of the payments industry.

Nearly $150 trillion in worldwide B2B and B2C transactions take place every year, but only a tiny portion are digital. A lot of technology companies want their piece of that massive pie. Until recently, though, only payment facilitators (aka, “payfacs”), gateways, banks and credit card companies had access to it.

That’s changing. Whether they know it yet or not, B2B tech platforms are becoming payments companies. Payfacs are competing to integrate their technology into these platforms, which drive an ever-growing number of transactions. Revenue-sharing deals are on the table, and payfacs are pushing the competitive advantages they can offer to the clients of these B2B platforms. Capabilities like cross-border payments, seamless customer onboarding, fraud protection, marketplace payments and B2B invoicing influence, which payfacs win in “integrated payments” (the jargon for this space) and which don’t.

B2B companies that use to leave the choice of gateway to their clients need to become savvy in payment technology, both to control the user experience and to tap this new business. There’s a massive amount of revenue on the table, and it’s just too easy to blow this opportunity and alienate clients in the process.

A decade ago, the revolution in cloud computing led to a wave of B2B tech platforms promising to “disrupt” every industry. Gyms got gym management platforms. Hospitals got clinic management platforms. Retailers got commerce management platforms. Media companies got subscription management platforms. Many of these fill-in-the-blank management platforms — all independent software vendors (ISVs) — helped clients manage their operations and interactions with consumers or other businesses.

But ISVs didn’t get involved in payments, which was odd, given how complementary payments were to their platforms and how much money was at stake. Mastercard says there is about $120 trillion annually in B2B payments worldwide, and paper checks still dominate about half of the U.S.’s $25 trillion payment volume. Meanwhile, retail e-commerce sales account for $4.2 trillion out of $26 trillion in total retail, or about 16.1%, according to eMarketer. Less than 8% of global commerce is thought to occur online.

You’d think B2B software companies would find a way to generate revenue on some of that $146 trillion in transactions, but most did not. Payment processing is its own, messy, complicated niche. Payfacs go through a grueling underwriting process to provision a merchant account, which includes know-your-customer (KYC) and anti-money laundering (AML) checks. If a merchant defaults, the payfac is next in line to make good on the transactions.

When you run a venture-backed B2B platform, you have enough to worry about already.

So, B2B platforms stayed clear. They formed integrations with a basket of payfacs (Stripe, PayPal, Square, my company BlueSnap, etc.) and then let their clients choose which one to use. That’s a lot of integrations to maintain.

Powered by WPeMatico

“Animal Crossing: New Horizons” is a bonafide wonder. The game has been setting new records for Nintendo, is adored by players and critics alike and provides millions of players a peaceful escape during these unprecedented times.

But there’s been something even more extraordinary happening on the fringe: Players are finding ways to augment the game experience through community-organized activities and tools. These include free weed-pulling services (tips welcome!) from virtual Samaritans, and custom-designed items for sale — for real-world money, via WeChat Pay and AliPay.

Well-known personalities and companies are also contributing, with “Rogue One: A Star Wars Story” scribe Gary Whitta hosting an A-list celebrity talk show using the game, and luxury fashion brand Marc Jacobs providing some of its popular clothing designs to players. 100 Thieves, the white-hot esports and apparel company, even created and gave away digital versions of its entire collection of impossible-to-find clothes.

This community-based phenomenon gives us a pithy glimpse into not only where games are inevitably going, but what their true potential is as a form of creative, technical and economic expression. It also exemplifies what we at Forte call “community economics,” a system that lies at the heart of our aim in bringing new creative and economic opportunities to billions of people around the world.

Formally, community economics is the synthesis of economic activity that takes place inside, and emerges outside, virtual game worlds. It is rooted in a cooperative economic relationship between all participants in a game’s network, and characterized by an economic pluralism that is unified by open technology owned by no single party. And notably, it results in increased autonomy for players, better business models for game creators, and new economic and creative opportunities for both.

The fundamental shift that underlies community economics is the evolution of games from centralized entertainment experiences to open economic platforms. We believe this is where things are heading.

Powered by WPeMatico

We’re excited to announce that Extra Crunch is now available to readers in Argentina, Brazil and Mexico. That adds to our existing support in the U.S., Canada, the U.K., and select European countries.

You can sign for Extra Crunch here.

Latin America has always caught the eye of big tech. For companies like Facebook, Amazon and Uber, Latin America has represented a massive growth opportunity. But it’s not just big tech that’s investing in Latin America. The startup scene is booming. According to Crunchbase, VCs invested billions into Latin America in 2018 and 2019.

In 2018, the TechCrunch team took a trip to São Paulo, Brazil to host Startup Battlefield Latin America. We knew about the hot startup scene and massive investments, and wanted to meet the founders fueling the fire in person.

The excitement, wit, creativity and energy of the entrepreneurs in Latin America was impressive. We were dazzled by the pitches from budding startup teams, and we were enlightened by the investors sharing their wealth of knowledge about the ecosystem. What we saw in person helped us tie the funding to the faces of the teams building the future. The entrepreneurial mentality of Silicon Valley doesn’t have borders; it’s alive and well across Latin America.

We wanted to bring Extra Crunch to Latin America to help support the startups and investors in this market because community has always been our top priority. We hope that Extra Crunch’s deep analysis and company-building resources will help the Latin America tech community grow even stronger than it is today.

We’ve been polling our audience about expanded country support for over a year now, and Argentina, Brazil and Mexico have always been near the top of the list. Now, we’re delivering on the promise to bring Extra Crunch to everyone who asked for it.

We’re optimistic that Extra Crunch will be a big hit in Latin America, and we hope entrepreneurs and investors in the region who have not yet heard of TechCrunch will give it a try.

You can sign for Extra Crunch here.

Extra Crunch is a membership program from TechCrunch that features research and reporting, reader utilities and savings on software services and events. We deliver more than 100 exclusive articles per month, with a focus on startup teams and investors.

Our weekly Extra Crunch investor surveys will help members find out where startup investors plan to write their next checks. Extra Crunch subscribers will be able to build a company better with how-tos and interviews from experts on fundraising, growth, monetization and other key work topics. Readers can also learn about the best startups through our IPO analysis, late-stage deep dives and other exclusive reporting delivered daily.

Here’s a taste of the articles you can expect to see in Extra Crunch:

Beyond articles, Extra Crunch also features a series of reader utilities and discounts to help save time and money. This includes an exclusive newsletter, no banner ads on TechCrunch.com, Rapid Read mode, List Builder tool and more. Committing to an annual or two-year Extra Crunch membership will unlock discounts on TechCrunch events and access to Partner Perks. Our Partner Perks can help you save on services like AWS, Brex, Canva, DocSend, Zendesk and more.

Thanks to all of our readers who voted on where to expand support for Extra Crunch, and thanks to all who participated in the Extra Crunch beta in Latin America. If you haven’t voted and you want to see Extra Crunch in your local country, let us know here. We’re actively working on expanding support to more countries, and input from readers is greatly appreciated.

You can sign up or learn more about Extra Crunch here.

Powered by WPeMatico

Salt Lake City’s Spiff has announced a $10 million round of funding to expand the sales and marketing efforts for its service that automates commission payments for sales people.

Some of the biggest names in startup tech are using the service to pay their sales force, including Brex, Workfront, Algolia and the publicly traded startup Qualys.

The idea at Spiff is to create a new software category around sales compensation management, and it’s gotten buy-in from investors at Norwest Venture Partners, Next World Ventures and Epic Ventures. Seed investors, including Kickstart Album Ventures, Pipeline Capital and Peterson Ventures, returned to invest in the company as well.

“Commissions are a major cause of anxiety for teams who don’t understand or trust their incentive plan and many waste hours every month correcting mistakes or arguing with finance, which hits bottom lines,” said Spiff chief executive, Jeron Paul. “Norwest’s investment will help us automate commission calculations so sales teams have one less thing to worry about in these challenging times.”

Paul, a serial entrepreneur whose most recent business, Capshare, was sold to Solium in 2017, has spent the better part of his professional career developing services businesses for enterprises.

“The world of sales compensation software is long overdue for a revamp,” said Sean Jacobsohn, partner at Norwest Venture Partners, in a statement. “With 85 percent of companies still calculating sales commissions manually in Google Sheets or Excel, I’m excited to partner with Spiff to help transform the way people think about sales compensation and provide sales teams with a deeper level of visibility into their commissions.”

Powered by WPeMatico

The fintech revolution is just getting started.

At least that’s the impression we got after a conversation with Plaid co-founder Zach Perret. He appeared on Extra Crunch Live last week to talk about his company’s announced exit to Visa and the larger fintech landscape.

Perret and Plaid announced a deal to sell the company to Visa earlier this year for $5.3 billion, a transaction that highlighted the company’s central position in the fintech world. Plaid provides APIs that link consumer bank accounts to apps and other financial services, making it the connective tissue of the fintech boom.

It’s probably no surprise, then, that Perret is bullish: “You’ve heard it a million times, but the quote of software eating the world [is true], and my corollary to that is [that] every company is a fintech company. And certainly every financial services company should be a fintech company.”

He said there’s lots of room left for fintech and finservices companies to create new products, which is not a bad view of the future if you want to be cheered up. Perret also noted that there are widespread opportunities for fintech companies to help underbanked people in the U.S. and abroad, which indicates a massive, untapped total addressable market.

To make sure you can take your own notes, we’ve included the full session below and excerpted a few passages from the transcript. (You can sign up for Extra Crunch here if you need access.)

First up, here’s the full call:

Powered by WPeMatico