payments

Auto Added by WPeMatico

Auto Added by WPeMatico

Data is a gold mine for a company.

If managed well, it provides the clarity and insights that lead to better decision-making at scale, in addition to an important tool to hold everyone accountable.

However, most companies are stuck in Data 1.0, which means they are leveraging data as a manual and reactive service. Some have started moving to Data 2.0, which employs simple automation to improve team productivity. The complexity of crypto data has opened up new opportunities in data, namely to move to the new frontier of Data 3.0, where you can scale value creation through systematic intelligence and automation. This is our journey to Data 3.0.

The complexity of crypto data has opened up new opportunities in data, namely to move to the new frontier of Data 3.0, where you can scale value creation through systematic intelligence and automation.

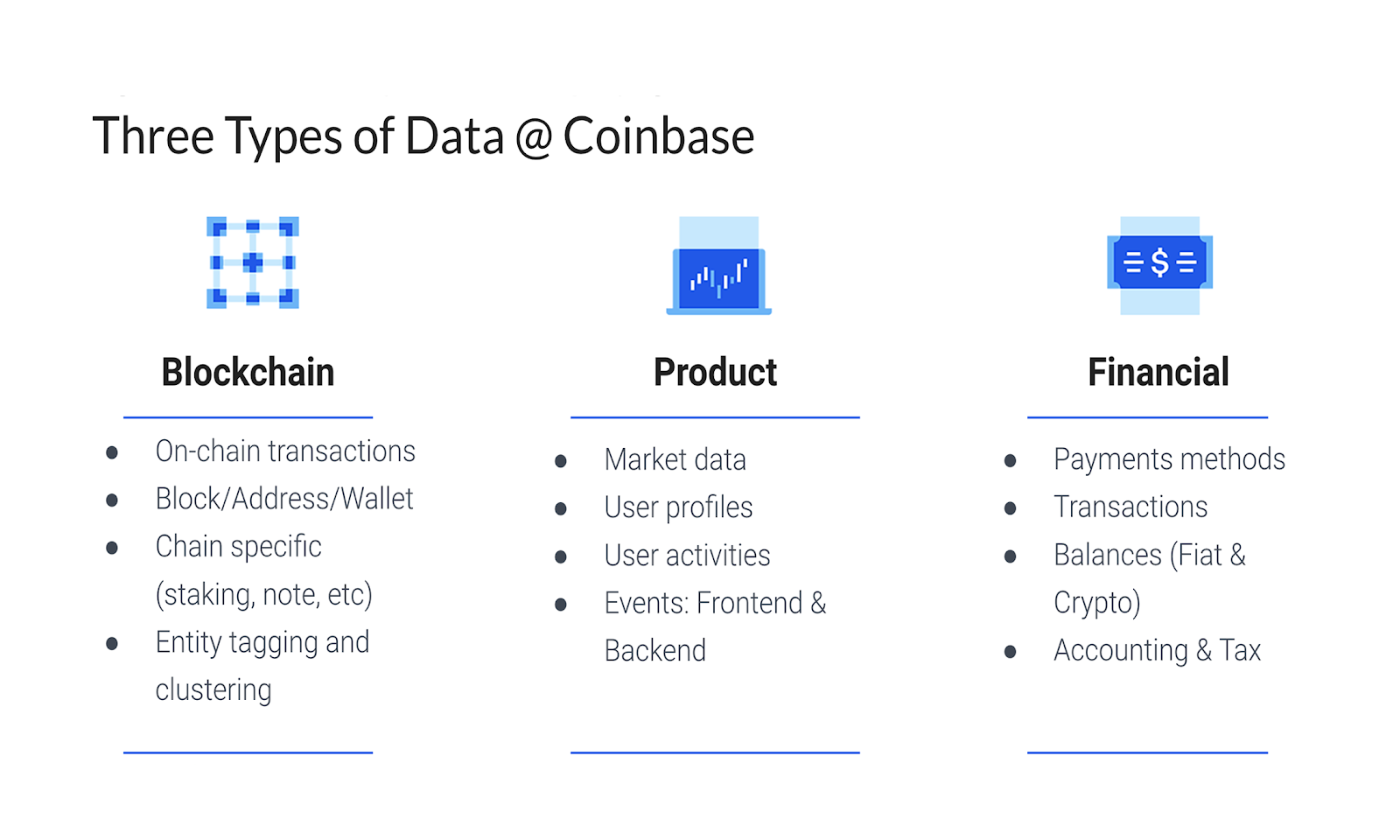

Coinbase is neither a finance company nor a tech company — it’s a crypto company. This distinction has big implications for how we work with data. As a crypto company, we work with three major types of data (instead of the usual one or two types of data), each of which is complex and varied:

Image Credits: Michael Li/Coinbase

Our focus has been on how we can scale value creation by making this varied data work together, eliminating data silos, solving issues before they start and creating opportunities for Coinbase that wouldn’t exist otherwise.

Having worked at tech companies like LinkedIn and eBay, and also those in the finance sector, including Capital One, I’ve observed firsthand the evolution from Data 1.0 to Data 3.0. In Data 1.0, data is seen as a reactive function providing ad-hoc manual services or firefighting in urgent situations.

Powered by WPeMatico

Eco, which has built out a digital global cryptocurrency platform, announced Friday that it has raised $26 million in a funding round led by a16z Crypto.

Founded in 2018, the SF-based startup’s platform is designed to be used as a payment tool around the world for daily-use transactions. The company emphasizes that it’s “not a bank, checking account, or credit card.”

“We’re building something better than all of those combined,” it said in a blog post. The company’s mission has also been described as an effort to use cryptocurrency as a way “to marry savings and spending,” according to this CoinList article.

Eco users can earn up to 5% annually on their deposits and get 5% cash back when transacting with merchants such as Amazon, Uber and others. Next up: The company says it will give its users the ability to pay bills, pay friends and more “all from the same, single wallet.” That same wallet, it says, rewards people every time they spend or save.

After a “successful” alpha test with millions of dollars deposited, the company’s Eco App is now available to the public.

A slew of other VC firms participated in Eco’s latest financing, including Founders Fund, Activant Capital, Slow Ventures, Coinbase Ventures, Tribe Capital, Valor Capital Group and more than one hundred other funds and angels. Expa and Pantera Capital co-led the company’s $8.5 million funding round.

CoinList co-founder Andy Bromberg stepped down from his role last fall to head up Eco. The startup was originally called Beam before rebranding to Eco “thanks to involvement by founding advisor, Garrett Camp, who held the Eco brand,” according to Coindesk. Camp is an Uber co-founder and Expa is his venture fund.

For a16z Crypto, leading the round is in line with its mission.

In a blog post co-written by Katie Haun and Arianna Simpson, the firm outlined why it’s pumped about Eco and its plans.

“One of the challenges in any new industry — crypto being no exception — is building things that are not just cool for the sake of cool, but that manage to reach and delight a broad set of users,” they wrote. “Technology is at its best when it’s improving the lives of people in tangible, concrete ways…At a16z Crypto, we are constantly on the lookout for paths to get cryptocurrency into the hands of the next billion people. How do we think that will happen? By helping them achieve what they already want to do: spend, save, and make money — and by focusing users on tangible benefits, not on the underlying technology.”

Eco is not the only crypto platform offering rewards to users. Lolli gives users free bitcoin or cash when they shop at over 1,000 top stores.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

Cryptocurrency exchange company Bitfinex is launching Bitfinex Pay, a cryptocurrency payment gateway. With this new product, online merchants can accept payments in various cryptocurrencies. It should make cross-border transactions easier in particular.

While there are a few crypto payment gateways already, Bitfinex Pay has the advantage of working seamlessly with the company’s exchange. Merchants can create a widget and start accepting payments in Ethereum and bitcoin. Payments are deposited on your exchange wallet.

Bitfinex’s widget works a bit like the “Buy Now with PayPal” button. When you click on the Bitfinex Pay button, you’re redirected to the cryptocurrency company’s website. Once your payment is approved, you’re redirected back to the original merchant website. Payments are capped at the equivalent of $1,000 in cryptocurrencies.

You don’t pay any fee with Bitfinex Pay transactions. Of course, there are some network fees involved with sending crypto tokens. Merchants will also end up paying fees if they want to convert their cryptocurrency holdings on the exchange and transfer fiat money out of their account.

Bitfinex Pay also lets you accept Tether payments. Tether is a stablecoin, which means that one unit of Tether is supposed to be worth one USD — it doesn’t fluctuate over time.

That statement has been challenged, as the attorney general in New York has concluded that Tethers weren’t fully backed by USD sitting in bank accounts at all times. At some point, Bitfinex couldn’t access $850 million held in a Panamanian bank.

As a result, Tether and Bitfinex are currently banned in the state of New York. So you’ll have to determine whether you trust Bitfinex enough to use it as part of your checkout process on your website.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

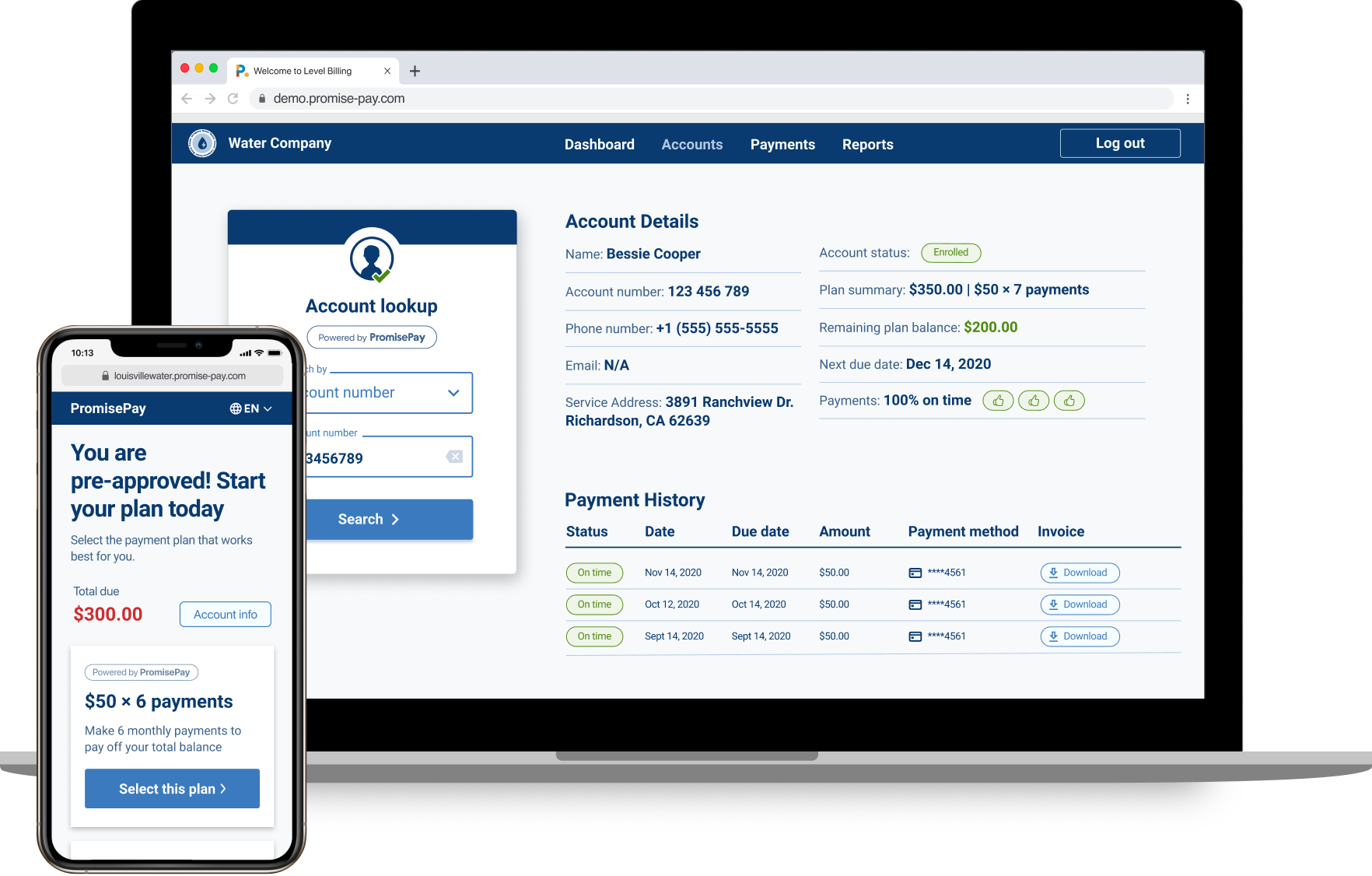

The last year has been one of financial hardship for billions, and among the specific hardships is the elementary one of paying for utilities, taxes and other government fees — the systems for which are rarely set up for easy or flexible payment. Promise aims to change that by integrating with official payment systems and offering more forgiving terms for fees and debts people can’t handle all at once, and has raised $20 million to do so.

When every penny is going toward rent and food, it can be hard to muster the cash to pay an irregular bill like water or electricity. They’re less likely to be shut off on short notice than a mobile plan, so it’s safer to kick the can down the road… until a few bills add up and suddenly a family is looking at hundreds of dollars of unpaid bills and no way to split them up or pay over time. Same with tickets and other fees and fines.

The CEO and co-founder of Promise, Phaedra Ellis-Lamkins, explained that this (among other places) is where current systems fall down. Unlike buying a TV or piece of furniture, where payment plans may be offered in a single click during online checkout, there frequently is no such option for municipal ticket payment sites or utilities.

“We have found that people struggling to pay their bills want to pay and will pay at extremely high rates if you offer them reminders, accessible payment options and flexibility. The systems are the problem — they are not designed for people who don’t always have a surplus of money in their bank accounts,” she told TechCrunch.

“They assume for example that if someone makes their first payment at 10 PM on the 15th, they will have the same amount of money the next month on the 15th at 10 PM,” she continued. “These systems do not recognize that most people are struggling with their basic needs. Payments may need to be weekly or split up into multiple payment types.”

Even those that do offer plans still see many failures to pay, due at least partly to a lack of flexibility on their part, said Ellis-Lamkins — failure to make a payment can lead to the whole plan being cancelled. Furthermore, it may be difficult to get enrolled in the first place.

“Some cities offer payment plans but you have to go in person to sign up, complete a multiple-page form, show proof of income and meet restrictive criteria,” she said. “We have been able to work with our partners to use self-certification to ease the process as opposed to providing tax returns or other documentation. Currently, we have over a 90% repayment rate.”

Promise acts as a sort of middleman, integrating lightly with the agency or utility, which in turn makes anyone owing money aware of the possibility of the different payment system. It’s similar to how you might see various payment options, including installments, when making a purchase at an online shop.

Image Credits: Promise

The user enrolls in a payment plan (the service is mobile-friendly because that’s the only form of internet many people have) and Promise handles that end of it, with reminders, receipts and processing, passing on the money to the agency as it comes in — the company doesn’t cover the cost up front and collect on its own terms. Essentially it’s a bolt-on flexible payment mechanism that specializes in government agencies and other public-facing fee collectors.

Promise makes money by subscription fees (i.e. SaaS) and/or through transaction fees, whichever makes more sense for the given customer. As you might imagine, it makes more sense for a utility to pay a couple bucks to be more sure of collecting $500, than to take its chance on getting none of that $500, or having to resort to more heavy-handed and expensive debt collection methods.

Lest you think this is not a big problem (and consequently not a big market), Ellis-Lamkins noted a recent study from the California Water Boards showing there are 1.6 million people with a total of $1 billion in water debt in the state — one in eight households is in arrears to an average of $500.

Those numbers are likely worse than normal, given the immense financial pressure that the pandemic has placed on nearly all households — but like payment plans in other circumstances, households of many incomes and types find their own reason to take advantage of such systems. And pretty much anyone who’s had to deal with an obtusely designed utility payment site would welcome an alternative.

The new round brings the company’s total raised to over $30 million, counting $10 million it raised immediately after leaving Y Combinator in 2018. The funding comes from existing investors Kapor Capital, XYZ, Bronze, First Round, YC, Village, and others.

Powered by WPeMatico

Three years ago, we released the first edition of the Matrix Fintech Index. We believed then, as we do now, that fintech represents one of the most exciting major innovation cycles of this decade. In 2020, all the long-term trends forcing change in this sector continued and even accelerated.

The broad movement away from credit toward debit, particularly among younger consumers, represents one such macro shift. However, the pandemic also created new, unforeseen drivers. Among them, millennials decamped from their rentals in crowded cities to accelerate their first home purchases to the benefit of proptech companies and challenger mortgage players alike.

E-commerce saw an enormous acceleration in growth rates, furthering adoption of online payments platforms. Lastly, low interest rates and looming inflation helped pave the way for the price of Bitcoin to charge toward $30,000. In short, multiple tailwinds combined to produce a blockbuster year for the category.

In this year’s refresh of the Matrix Fintech Index, we’ll divide our attention into three parts. First, a look at the public stocks’ performance. Second, liquidity. Third, we highlight one major trend in the sector: Buy Now Pay Later, or BNPL.

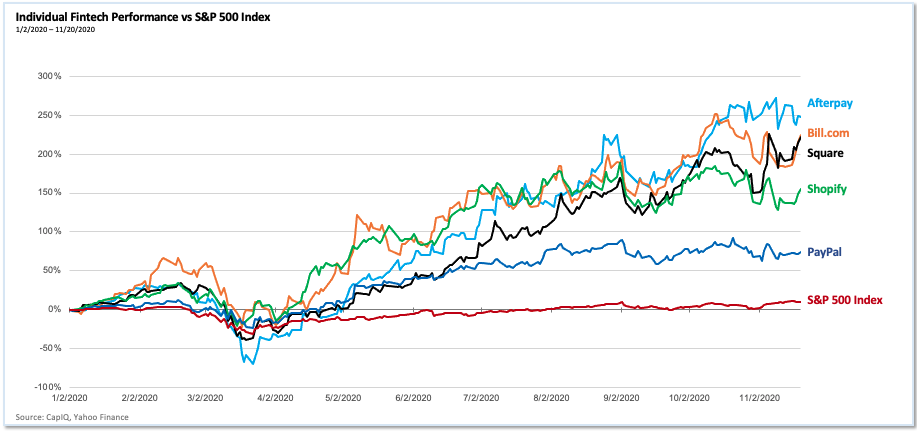

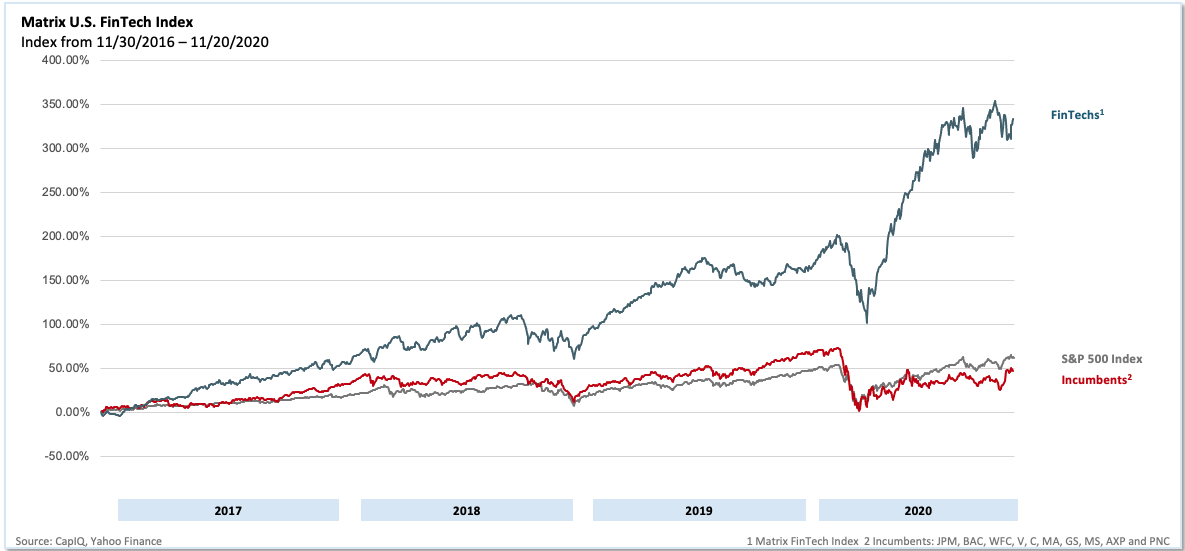

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index. While the underlying performance of these companies was strong, the pandemic further bolstered results as consumers avoided appearing in-person for both shopping and banking. Instead, they sought — and found — digital alternatives.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index.

Our own representation of the public fintechs’ performance is the Matrix Fintech Index — a market cap-weighted index that tracks the progress of a portfolio of 25 leading public fintech companies. The Matrix fintech Index rose 97% in 2020, compared to a 14% rise in the S&P 500 and a 10% drop for the incumbent financial service companies over the same time period.

2020 performance of individual fintech companies vs. SPX Image Credits: CapiQ, Yahoo Finance

Matrix U.S. Fintech Index, 2016 -2020 Image Credits: CapiQ, Yahoo Finance

E-commerce undoubtedly stood out as a major driver. As a category, retail e-commerce grew 35% YoY as of Q3, propelling PayPal and Shopify to add over $160 billion of market capitalization over the year. For its part, PayPal in the third quarter signed up 15 million net new active accounts (its highest ever).

Powered by WPeMatico

Payments for consumers have made a huge shift to the online world in the last year, a time when they have moved more of their purchasing to the internet to minimize in-person transactions in the midst of a virus-based health pandemic. Today, a startup that has built a similar kind of payments infrastructure — but specifically targeting small businesses and the payments they need to make — has raised a big round of funding to double down on its own slice of the market.

Melio, which provides a platform for SMBs to pay other companies electronically using bank transfers, debit cards or credit — along with the option of cutting paper checks for recipients if that is what the recipients request — has closed $110 million in funding at a valuation that the company said was now $1.3 billion.

The company’s focus to date has been building and growing a system to replace the paper invoices, snail mail and bank transfers that might take multiple days to clear and still dominate payments for small and medium enterprises. The company was founded in Israel but has to date focused a lot of its attention on the U.S. market, where it saw growth of 2,000% last year (it doesn’t disclose the actual number of customers that it has). CEO Matan Bar said that this is where the company will continue to focus for now.

This latest round was led by Coatue and also included participation from previous backers Accel, Aleph, Bessemer Venture Partners, Corner Ventures, General Catalyst and Latitude. It caps off a huge year for the company, which raised $130 million in 2020 (and $256 million overall), with other recent backers including others like American Express and Salesforce.

The latter two are strategic backers: AmEx is one of the options given to customers paying other businesses through Melio’s rails.

Salesforce, meanwhile, is not yet an integration partner, but Bar — who co-founded the company with Ilan Atias and Ziv Paz (respectively CTO and COO) — described its interest as similar to that of Intuit-owned accounting giant QuickBooks. QuickBooks connects with Melio so that users of one can seamlessly import activity from one platform into the other, and Bar hinted that there is an interest from the CRM giant, which provides a number of other business and productivity tools, to work together in a similar fashion.

Bar came to found Melio on the heels of years of experience in peer-to-peer payments focused on the consumer market. He previously ran PayPal’s business unit focused on peer-to-peer payments, which included Venmo in the U.S. and equivalent services (not branded Venmo) outside of it. He came to PayPal, which at the time was a part of eBay, through eBay’s acquisition of his previous startup, a social gifting platform called The Gifts Project.

As Bar describes it, PayPal “was the first time I experienced what the digitization of payments looked like as they were shifting from cash to mobile payments. Consumers were buying online instead of at brick-and-mortar stores, and even when they were getting physical items, they were paying online.” What he quickly realized, though, was that the same was not applying to the businesses themselves.

“There are still trillions being transferred via paper checks in the B2B space,” he said, with paper invoices and paper checks dominating the market. “The space is way behind other payment areas. I would be talking with SMB owners who would be using fancy Square or PayPal point of sale devices, but when they had to pay, say, a coffee bean supplier, they stuffed checks in envelopes. That’s very intriguing obviously, and it triggered our interest.”

Interestingly this isn’t a problem that hasn’t been identified before, but many of the solutions, such as Bill.com or Tipalti, are really designed for larger enterprises. “They are too overwhelming for SMBs,” he said. “Even their names say it all: Accounts Payable Automation Solutions. It’s about tens of thousands of payments, and accounting departments, not an order from a wine shop.”

That formed the basis of what the startup started to build, which has been, in essence, a very pared-down version of these other payments platforms with SMB needs in mind.

The first of these is a focus on cashflow, Bar said. Specifically, the Melio platform lets payments be made automatically but businesses themselves can delay the timing on when money actually leaves their accounts: “Buyers keep cash longer, vendors get paid faster,” is how Bar describes it.

This is in part enabled by the tech that Melio has built, which builds in risk assessment, as well as fraud management, and balances payments across the whole of its platform to send money in and out without the need for the company to raise debt to back up those payments.

“We leverage data to assess risk,” said Bar. “Every dollar in this round is going towards R&D and sales and marketing. We don’t need the capital in our model.” It also works with the likes of AmEx and its own credit system in cases where people are paying on credit, but Bar also noted that currently most of the transactions that happen on its platform are not credit based. Most are bank transfers.

While others like Stripe have also built B2B payment services to pay out suppliers, Bar points out that what it has created is unique in that it is a standalone service: no need to be a part of Stripe’s wider ecosystem of services to use this if you already use another payments provider you are happy with.

Given that focus on cashflow for SMBs, what’s also interesting is the low bar to entry that Melio has built into its platform. Specifically, the service is completely free for businesses to use — that is, no fee is charged — as long as companies are making bank transfers or using debit cards. It takes a 2.9% fee when a business elects to use a credit card for a transaction (and even then Melio says that the fee is tax deductible in the U.S.).

He noted that one of the reasons that Melio has to date targeted the U.S. market is because of how antiquated it still is. “The average bank transfer still takes three to four business days, if you don’t want to take any risk,” he said. “We have developed models to do it same day. We take the risk that the buyer might not have the funds in that account but think about how that impacts cash flows. With Melio you still pay in three days, but money will be delivered the same day. That is how you can keep cash longer, without a payments risk.”

Targeting a market that remains very underserved at a time when so much has gone virtual in payments is why investors are also interested.

“Melio has identified both the opportunity and duty to help small businesses manage their finance remotely and improve cash flow, in normal times as well as during this crisis, as physical payments supply chains are interrupted and overwhelmed,” said Michael Gilroy, a general partner at Coatue, in a statement. “Going digital is the only way small businesses can compete against larger rivals and stay ahead of the curve.”

In terms of more product development, Bar said that the company has received “a lot of incoming interest from partners to enable B2B payments within their products on their product,” similar to what QuickBooks is doing and Salesforce is likely to do. “Payments are contextual and they want to enable a quicker way to get there. The SMB is underserved. And yes, from a unit economics it’s much better to go after Nike. But this is also to really create some financial inclusion. We want to enable services for the small shop that the big guys already have.”

Powered by WPeMatico

French startup Alma is raising a $59.4 million Series B funding round (€49 million). The company has been building a new payment option for expensive goods. You can choose to pay over three or four installments. This product sounds familiar if you’ve used Klarna in the past. But Klarna isn’t available in France.

Cathay Innovation, Idinvest, Bpifrance’s Large Venture fund, Seaya Ventures and Picus Capital are participating in today’s funding round. In addition to today’s equity round, Alma is raising a credit line of $25.5 million (€21 million) to finance merchant payments.

What makes Alma attractive to merchants is that the startup is handling 100% of the risk involved with a payment over multiple installments. When a customer buys a bike over four installments, they’ll get charged over several months. But the merchant gets paid on day one.

Since I first covered Alma, the startup has launched the ability to pay later. You enter your card information right now but you get charged 15 days or a month later. It can be particularly useful if you’re unsure about something you’re buying and if you think there’s a chance you’ll send it back.

And it’s an attractive option in France where debit cards are the norm — not credit cards. Alma also plans to offer longer plans, such as the ability to buy now and pay over 6, 10 or 12 installments.

Thanks to the new influx of cash, the startup plans to triple the size of its team and reach €1 billion in annual payment volume within two years. It’s also going to expand to other countries, but with a specific focus on helping French merchants reach European customers living in other European countries.

Powered by WPeMatico

Some time ago, I gave up on the idea of finding a thread that connects each story in the weekly Extra Crunch roundup; there are no unified theories of technology news.

The stories that left the deepest impression were related to two news pegs that dominated the week — Visa and Plaid calling off their $5.3 billion acquisition agreement, and sizzling-hot IPOs for Affirm and Poshmark.

Watching Plaid and Visa sing “Let’s Call The Whole Thing Off” in harmony after the U.S. Department of Justice filed a lawsuit to block their deal wasn’t shocking. But I was surprised to find myself editing an interview Alex Wilhelm conducted with with Plaid CEO Zach Perret the next day in which the executive said growing the company on its own is “once again” the correct strategy.

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

In an analysis for Extra Crunch, Managing Editor Danny Crichton suggested that federal regulators’ new interest in antitrust enforcement will affect valuations going forward. For example, Procter & Gamble and women’s beauty D2C brand Billie also called off their planned merger last week after the Federal Trade Commission raised objections in December.

Given the FTC’s moves last year to prevent Billie and Harry’s from being acquired, “it seems clear that U.S. antitrust authorities want broad competition for consumers in household goods,” Danny concluded, and I suspect that applies to Plaid as well.

In December, C3.ai, Doordash and Airbnb burst into the public markets to much acclaim. This week, used clothing marketplace Poshmark saw a 140% pop in its first day of trading and consumer-financing company Affirm “priced its IPO above its raised range at $49 per share,” reported Alex.

In a post titled A theory about the current IPO market, he identified eight key ingredients for brewing a debut with a big first-day pop, which includes “exist in a climate of near-zero interest rates” and “keep companies private longer.” Truly, words to live by!

Come back next week for more coverage of the public markets in The Exchange, an interview with Bustle CEO Bryan Goldberg where he shares his plans for taking the company public, a comprehensive post that will unpack the regulatory hurdles facing D2C consumer brands, and much more.

If you live in the U.S., enjoy your MLK Day holiday weekend, and wherever you are: thanks very much for reading Extra Crunch.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman (opens in a new window)

After spending much of the week covering 2021’s frothy IPO market, Alex Wilhelm devoted this morning’s column to studying the OKR-focused software sector.

Measuring objectives and key results are core to every enterprise, perhaps more so these days since knowledge workers began working remotely in greater numbers last year.

A sign of the times: this week, enterprise orchestration SaaS platform Gtmhub announced that it raised a $30 million Series B.

To get a sense of how large the TAM is for OKR, Alex reached out to several companies and asked them to share new and historical growth metrics:

“Some OKR-focused startups didn’t get back to us, and some leaders wanted to share the best stuff off the record, which we grant at times for candor amongst startup executives,” he wrote.

Image Credits: Ezra Shaw (opens in a new window)

For our latest investor survey, Matt Burns interviewed five VCs who actively fund consumer electronics startups:

“Consumer hardware has always been a tough market to crack, but the COVID-19 crisis made it even harder,” says Matt, noting that the pandemic fueled wide interest in fitness startups like Mirror, Peloton and Tonal.

Bonus: many VCs listed the founders, investors and companies that are taking the lead in consumer hardware innovation.

Digital generated image of abstract multi colored curve chart on white background.

If you’re looking for insight into “why everything feels so damn silly this year” in the public markets, a post Alex wrote Thursday afternoon might offer some perspective.

As someone who pays close attention to late-stage venture markets, he’s identified eight factors that are pushing debuts for unicorns like Affirm and Poshmark into the stratosphere.

TL;DR? “Lots of demand, little supply, boom goes the price.”

Image Credits: Nigel Sussman (opens in a new window)

Clothing resale marketplace Poshmark closed up more than 140% on its first trading day yesterday.

In Thursday’s edition of The Exchange, Alex noted that Poshmark boosted its valuation by selling 6.6 million shares at its IPO price, scooping up $277.2 million in the process.

Poshmark’s surge in trading is good news for its employees and stockholders, but it reflects poorly on “the venture-focused money people who we suppose know what they are talking about when it comes to equity in private companies,” he says.

financial stock market graph on technology abstract background represent risk of investment

This week, Visa announced it would drop its planned acquisition of Plaid after the U.S. Department of Justice filed suit to block it last fall.

Last week, Procter & Gamble called off its purchase of Billie, a women’s beauty products startup — in December, the U.S. Federal Trade Commission sued to block that deal, too.

Once upon a time, the U.S. government took an arm’s-length approach to enforcing antitrust laws, but the tide has turned, says Managing Editor Danny Crichton.

Going forward, “antitrust won’t kill acquisitions in general, but it could prevent the buyers with the highest reserve prices from entering the fray.”

Image Credits: Sophie Alcorn

Dear Sophie:

I’m a grad student currently working on F-1 STEM OPT. The company I work for has indicated it will sponsor me for an H-1B visa this year.

I hear the random H-1B lottery will be replaced with a new system that selects H-1B candidates based on their salaries.

How will this new process work?

— Positive in Palo Alto

OLYMPUS DIGITAL CAMERA

After news broke that Visa’s $5.3 billion purchase of API startup Plaid fell apart, Alex Wilhelm and Ron Miller interviewed several investors to get their reactions:

Zach Perret, chief executive officer and co-founder of Plaid Technologies Inc., speaks during the Silicon Slopes Tech Summit in Salt Lake City, Utah, U.S., on Friday, Jan. 31, 2020. The summit brings together the leading minds in the tech industry for two-days of keynote speakers, breakout sessions, and networking opportunities. Photographer: George Frey/Bloomberg via Getty Images

Alex Wilhelm interviewed Plaid CEO Zach Perret after the Visa acquisition was called off to learn more about his mindset and the company’s short-term plans.

Perret, who noted that the last few years have been a “roller coaster,” said the Visa deal was the right decision at the time, but going it alone is “once again” Plaid’s best way forward.

Image Credits: Nigel Sussman (opens in a new window)

In Tuesday’s edition of The Exchange, Alex Wilhelm took a closer look at blank-check offerings for digital asset marketplace Bakkt and personal finance platform SoFi.

To create a detailed analysis of the investor presentations for both offerings, he tried to answer two questions:

Spotlit Multi Colored Coil Toy in the Dark.

Growth-stage startups in search of funding have a new option: “flexible VC” investors.

An amalgam of revenue-based investment and traditional VC, investors who fall into this category let entrepreneurs “access immediate risk capital while preserving exit, growth trajectory and ownership optionality.”

In a comprehensive explainer, fund managers David Teten and Jamie Finney present different investment structures so founders can get a clear sense of how flexible VC compares to other venture capital models. In a follow-up post, they share a list of a dozen active investors who offer funding via these non-traditional routes.

Image Credits: Anton Petrus (opens in a new window) / Getty Images

For some consumers, “cannabis has always been essential,” writes Matt Burns, but once local governments allowed dispensaries to remain open during the pandemic, it signaled a shift in the regulatory environment, and investors took notice.

Matt asked five VCs about where they think the industry is heading in 2021 and what advice they’re offering their portfolio companies:

Powered by WPeMatico

Bangalore-based CRED is kickstarting the new year on a high note.

The two-year-old startup, led by high-profile entrepreneur Kunal Shah, said on Monday it has raised $81 million in a new financing round and bought shares worth $1.2 million (about 90 million Indian rupees) from employees.

The Series C financing round, as first reported by TechCrunch in late November, was led by DST Global. Existing investors Sequoia Capital, Ribbit Capital, Tiger Global and General Catalyst also participated in the round, and so did a few new names, including Satyan Gajwani of Indian conglomerate Times Internet, Sofina and Coatue.

The round gave CRED — which operates an eponymous app to reward customers for paying their credit card bill on time and offers deals from interesting online brands — a post-money valuation of $806 million.

In an interview with TechCrunch, Shah said that about 10% of CRED’s cap table is currently allocated to employees, and those who held vested stocks were eligible to sell up to 50% of their shares back to the startup in its first ESOP liquidity program. “We believe that startups should think about creating wealth for every shareholder, including employees.”

CRED has nearly doubled its customer base to about 5.9 million in the past year, or about 20% of the credit card holder base in India. The startup said that the median credit score of its customer was about 830, and about 30% of its customer base today holds a premium credit card. (On a side note, more than 50% of CRED customers pay their bills using UPI.)

CRED is one of the most talked-about startups in India, in part because of the scale at which its valuation has soared and the amount of capital it has been able to raise in such a short period.

One of the biggest questions surrounding CRED is just how it makes money, given how most fintech startups in the country — and there are many of them — are struggling to find a business model.

Shah said CRED makes money by cross-selling financing products — for which it has a revenue-sharing arrangement with banks and other financial institutions — and levies a similar cut from merchants who are on the platform today. More than 1,300 brands — including big names Starbucks, TAGG, Eat.Fit, Nykaa and emerging premium direct-to-consumer brands such as The Man Company, Sleepy Cat and Crossbeats –have joined the platform in recent years.

Direct-to-consumer market in India is still in its nascent stage, though some estimates say it could be worth $100 billion by 2025.

“I don’t think we were very deliberate to make D2C happen. It just so happened that in the early days when we offered rewards for D2C brands, they started to see huge traction,” he said, adding that CRED drove more than 30% sales for some brands.

“We realized that we were able to solve the discovery problem for customers. We are approaching this with themes — work-from-home and coffee — and it’s working out well. We are now playing matchmaking role between customers and brands that otherwise had to spend a lot of money in marketing.”

One of the biggest propositions of CRED is that it has been able to court some of the most sought-after customers in India. Unlike many other startups and giants such as Google and Facebook, CRED is not going after the next billion users.

“About 20 million customers account for 90% of all online consumption in India. These are the customers we are focusing on,” said Shah, who previously ran financial services firm Freecharge and delivered one of the rare successful exits in the country. The core challenge in chasing customers in smaller cities and towns in India is that very few people have the financial capacity to buy things, Shah said.

For that model to work, the GDP of India — where the average annual income of an individual is about $2,000 — needs to grow. And for that, we need more participation from females, said Shah. Less than 10% of the female population in India are currently part of the workforce, compared to over 90% in China.

An interesting use case for CRED today is that it could potentially license to venture firms data about the traction D2C brands are seeing on its platform, which could use it as a signal to inform their investment decisions.

Shah cautioned that the startup is “extraordinarily sensitive about data” but said the team is thinking about ways to help venture firms discover these firms. “We are planning to create a newsletter to showcase many of these brands to the investor world,” he said.

And finally, will CRED launch a credit card or other banking products? “Can we partner with banks to cross-sell every product that they today offer? The answer is yes,” said Shah, though he cautioned that the startup is in no hurry to supercharge its offerings.

Powered by WPeMatico

The rest of the world may be slowing down as we prepare for Christmas and the new year, but we are not taking our foot off the gas.

Alex Wilhelm keeps a close watch on the public markets in his column The Exchange, but this week, he branched out to look at some of the metrics underpinning soaring cryptocurrency prices and turned his gaze on StockX, the consumer reseller marketplace that just raised $275 million in a Series E that values the company at approximately $2.8 billion.

“Selling a tenth of your company for north of a quarter-billion may be somewhat common among late-stage software startups with tremendous growth,” he says, but “don’t laugh — the round actually makes pretty OK sense.”

Our staff continues to file their end-of-year stories: We ran a post this morning by Manish Singh that studies India’s massive total addressable market for retail. The nation has more than 60 million mom-and-pop neighborhood stores, and companies like Walmart and Amazon are eager to offer help with payments, logistics and inventory management — as are hundreds of native and foreign startups.

In an interview with author and MIT professor Sinan Aral, Managing Editor Danny Crichton discussed some of the debates currently swirling around the desire in some quarters to regulate social media platforms. In “The Hype Machine,” Aral explores topics like neuroscience, economics and misinformation before offering potential solutions for resolving what he calls “a full-blown social media crisis.”

The stories that follow are an overview of Extra Crunch from the last five days. Complete articles are only available to members, but you can use discount code ECFriday to save 20% off a one or two-year subscription. Details here.

Thank you very much for reading Extra Crunch this week; I hope you have a safe, relaxing weekend!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman (opens in a new window)

How did fashion marketplace Poshmark go from posting regular losses in 2019 to generating net income in 2020?

After the company filed a public S-1 last night, Alex Wilhelm pondered the question this morning in The Exchange.

Like many e-commerce platforms, Poshmark saw a surge in activity during the COVID-19 pandemic, but it also slashed its marketing spend, which helped boost profits. As the cash-rich company prepares its road show, “Poshmark is valuable,” Alex concluded.

“How valuable the market will decide. But who will it enrich with its final pricing decision?”

WASHINGTON, D.C. – APRIL 22, 2018: A statue of Albert Gallatin, a former U.S. Secretary of the Treasury, stands in front of The Treasury Building in Washington, D.C. The National Historic Landmark building is the headquarters of the United States Department of the Treasury. (Photo by Robert Alexander/Getty Images)

The breach of FireEye and SolarWinds by hackers working on behalf of Russian intelligence is “the nightmare scenario that has worried cybersecurity experts for years,” reports Zack Whittaker.

The intrusion began several months ago, but news of the breach wasn’t made public until this week.

“Given that potential victims include defense contractors, telecoms, banks, and tech companies, the implications for critical infrastructure and national security, although untold at this point, could be significant,” said Erin Kenneally, director of cyber risk analytics at Guidewire, an industry platform for insurance carriers.

In his analysis for Extra Crunch, Zack breaks down the rippling effects of supply-chain attacks that can compromise platforms like SolarWinds, which is used by more than 420 of the Fortune 500.

Image Credits: dowell (opens in a new window) / Getty Images

Embedded finance connects services like payment processing with everyday activities like grabbing a coffee before unlocking an e-scooter.

“The ability to be at the right place at the right time, supporting consumers and merchants alike, where they want it, how they want it and when they want it — cannot be understated,” says Simon Wu, an investment director with Cathay Innovation.

In a post that identifies embedded finance’s top providers and enablers, he offers advice for startups and established brands that are hoping to “earn and build customer loyalty while generating new revenue streams.”

Image Credits: Nigel Sussman (opens in a new window)

Bitcoin is at an all-time high.

CoinMarketCap reports that crypto market values have reached almost $659 billion; that figure was just $140 billion in March 2020.

“These gains have created a huge amount of wealth for crypto holders,” Alex Wilhelm wrote yesterday.

To get a better handle on why crypto values are sky-bound, he parsed some basic industry metrics, including the number of unique bitcoin addresses, fees paid and transactions per day.

“Do the price gains make sense in the short term? Who knows,” he wrote, “but they are not based on nothing.”

Stage Light on Black. Image Credits: Fotograzia / Getty Images

For his year-end Extra Crunch story, security reporter Zack Whittaker looked back at the myriad security challenges and vulnerabilities COVID-19 brought to the fore.

The hacks of Fire Eyes and SolarWinds were just one link in the chain: How well is your company prepared to deal with file-encrypting malware, hackers backed by nation-states or employees accessing secure systems from home?

“With 2020 wrapping up, much of the security headaches exposed by the pandemic will linger into the new year,” says Zack.

Zoox Fully Autonomous, All-electric Robotaxi. Image Credits: Zoox

After six years of research and development, autonomous vehicle company Zoox this week unveiled an electric robotaxi that can carry four people at a maximum speed of 75 miles per hour.

Automotive writer Kirsten Korosec interviewed Zoox co-founder and CTO Jesse Levinson to learn more about the vehicle’s development and how the company overcame a series of technical and legal challenges.

“I would say that if you have a big idea and you’re confident that it makes sense, you should at least explore the idea, rather than giving up because the current regulations aren’t designed for it,” said Levinson.

Kirsten only had 15 minutes to interview Levinson, but this comprehensive interview covers topics like regulatory compliance, Zoox’s relationship with parent company Amazon and the highest (and lowest) moments he experienced along the way.

Fairy dust flying in gold light rays. Computer-generated abstract raster illustration. Image Credits: gonin / Wikimedia Commons

In one of the largest enterprise acquisitions of 2020, Visa Equity Partners this week purchased Utah-based edtech startup Pluralsight for $3.5 billion.

According to the entrepreneurs and investors reporter Natasha Mascarenhas spoke to, this deal “shows the strength of edtech’s capital options as the pandemic continues.”

“What’s happening in edtech is that capital markets are liquidating,” a major change from “the old days where the options to exit were very narrow,” says Deborah Quazzo, a managing partner at GSV Advisors and seed investor in Pluralsight.

Image Credits: Sophie Alcorn

Dear Sophie:

I’m on an F1 OPT and am about to incorporate a startup with my two American co-founders.

What were the biggest immigration changes in 2020 affecting us?

—Ambitious in Albany

High angle view of young man walking towards white doorways on blue background Image Credits: Klaus Vedfelt / Getty Images

Founders and the VCs who back them may not be friends, but they’re usually friendly.

Investors are on a first-name basis with entrepreneurs from their portfolio companies and frequently have candid conversations with them about life, work and the world in general. In the before times, they might even have shared a meal or attended a baseball game together.

But make no mistake, it is a top-down relationship — the investor will always have the upper hand. When an entrepreneur accepts a check, they are hiring their next boss.

In an Extra Crunch guest post, Quiq CEO and founder Mike Myer poses two questions for founders who are considering a new relationship with a VC:

NEW DELHI, INDIA – 2011/12/18: Rice is sold at a night market in Paharganj, the urban suburb opposite New Delhi Railway Station. (Photo by Frank Bienewald/LightRocket via Getty Images)

In India, about 90% of consumers buy their everyday goods from neighborhood-based kirana stores instead of supermarkets.

As a result, U.S. retail giants like Walmart and Amazon have adopted an “if you can’t beat them, join them” approach, offering the nation’s 60 million mom-and-pop shops software for inventory control, payments and e-commerce.

India’s retail market will be worth an estimated $1.3 trillion by 2025, but e-commerce represents just 3% of that activity today, reports Manish Singh.

For his final Extra Crunch story of 2020, he looked at the startups and major players who are hoping to carve out their niche in one of the world’s largest retail ecosystems.

Image Credits: PM Images / Getty Images

Earlier this year, business productivity software startup ClickUp raised a $35 million Series A.

Now, just six months later, the company has closed a second round of $100 million that values the San Diego-based startup at $1 billion.

Lucas Matney interviewed CEO Zeb Evans this week to learn more about how the company was buoyed by pandemic-based behavior shifts that doubled its customer base and multiplied revenue by a factor of nine.

“I think that the biggest thing that we’ve always focused on is shipping a new version of ClickUp every week. That is our differentiation,” he said. “We’ve kind of created these iterative cycles called natural product-market fit and it’s been hard to keep up with that.”

Multi Colored Bling Bling Dollar Sign Shape Bokeh Backdrop on Dark Background, Finance Concept. Image Credits: MirageC / Getty Images.

In 2018, the total value of the year’s 10 top enterprise mergers and acquisitions reached $87 billion; last year, that figure fell to just $40 billion.

But in 2020, 10 M&A deals accounted for $165.2 billion.

“Last year’s biggest deal — Salesforce buying Tableau for $15.7 billion — would have only been good for fifth place on this year’s list,” notes enterprise reporter Ron Miller. “And last year’s fourth largest deal, where VMware bought Pivotal for $2.7 billion, wouldn’t have even made this year’s list at all.”

Powered by WPeMatico