payments

Auto Added by WPeMatico

Auto Added by WPeMatico

It’s pretty easy for individuals to send money back and forth, and there are lots of cash apps from which to choose. On the commercial side, however, one business trying to send $100,000 the same way is not as easy.

Paystand wants to change that. The Scotts Valley, California-based company is using cloud technology and the Ethereum blockchain as the engine for its Paystand Bank Network that enables business-to-business payments with zero fees.

The company raised $50 million Series C funding led by NewView Capital, with participation from SoftBank’s SB Opportunity Fund and King River Capital. This brings the company’s total funding to $85 million, Paystand co-founder and CEO Jeremy Almond told TechCrunch.

During the 2008 economic downturn, Almond’s family lost their home. He decided to go back to graduate school and did his thesis on how commercial banking could be better and how digital transformation would be the answer. Gleaning his company vision from the enterprise side, Almond said what Venmo does for consumers, Paystand does for commercial transactions between mid-market and enterprise customers.

“Revenue is the lifeblood of a business, and money has become software, yet everything is in the cloud except for revenue,” he added.

He estimates that almost half of enterprise payments still involve a paper check, while fintech bets heavily on cards that come with 2% to 3% transaction fees, which Almond said is untenable when a business is routinely sending $100,000 invoices. Paystand is charging a flat monthly rate rather than a fee per transaction.

Paystand’s platform. Image Credits: Paystand

On the consumer side, companies like Square and Stripe were among the first wave of companies predominantly focused on accounts payable and then building business process software on top of an existing infrastructure.

Paystand’s view of the world is that the accounts receivables side is harder and why there aren’t many competitors. This is why Paystand is surfing the next wave of fintech, driven by blockchain and decentralized finance, to transform the $125 trillion B2B payment industry by offering an autonomous, cashless and feeless payment network that will be an alternative to cards, Almond said.

Customers using Paystand over a three-year period are able to yield average benefits like 50% savings on the cost of receivables and $850,000 savings on transaction fees. The company is seeing a 200% increase in monthly network payment value and customers grew two-fold in the past year.

The company said it will use the new funding to continue to grow the business by investing in open infrastructure. Specifically, Almond would like to reboot digital finance, starting with B2B payments, and reimagine the entire CFO stack.

“I’ve wanted something like this to exist for 20 years,” Almond said. “Sometimes it is the unsexy areas that can have the biggest impacts.”

As part of the investment, Jazmin Medina, principal at NewView Capital, will join Paystand’s board. She told TechCrunch that while the venture firm is a generalist, it is rooted in fintech and fintech infrastructure.

She also agrees with Almond that the B2B payments space is lagging in terms of innovation and has “strong conviction” in what Almond is doing to help mid-market companies proactively manage their cash needs.

“There is a wide blue ocean of the payment industry, and all of these companies have to be entirely digital to stay competitive,” Medina added. “There is a glaring hole if your revenue is holding you back because you are not digital. That is why the time is now.”

Powered by WPeMatico

The payments space — amazingly — remains up for grabs for startups. Yes, dear reader, despite the success of Stripe, there seems to be a new payments startup virtually every other day. It’s a mess out there! The accelerated growth of e-commerce due to the pandemic means payments are now a booming space. And here comes another one, with a twist.

WhenThen has built a no-code payment operations platform that, they claim, streamlines the payment processes “of merchants of any kind”. It says its platform can autonomously orchestrate, monitor, improve and manage all customer payments and payments ops.

The startup’s opportunity has arisen because service providers across different verticals increasingly want to get into open banking and provide their own payment solutions and financial services.

Founded six months ago, WhenThen has now raised $6 million, backed by European VCs Stride and Cavalry.

The founders, Kirk Donohoe, Eamon Doyle and Dave Brown, are three former Mastercard Payment veterans.

Based out of Dublin, CEO Donohoe told me: “We see traditional businesses embracing e-comm, and e-comm merchants now operating multiple business models such as trade supply, marketplace, subscription, and more. There is no platform that makes it easy for such businesses to create and operate multiple payment flows to support multiple business models in one place — that’s where we step in.”

He added: “WhenThen is helping e-commerce digital platforms build advanced payment flows and payment automation, in minutes as opposed to months. When you start to integrate different payment methods, different payment gateways, how you want the payment to move from collection through to payout gets very, very complex. I’ve been doing this for over a decade now, as an entrepreneur building different businesses that had to accept, collect and pay payments.”

He said his founding team “had to build very complex payment flows for large merchants, airlines, hotels, issuers, and we just found it was ridiculous that you have to continue to do the same thing over and over again. So we decided to come up with WhenThen as a better way to be able to help you build those flows in minutes.”

Claude Ritter, managing partner at Cavalry, said: “Basic payment orchestration platforms have been around for some time, focusing mostly on maximizing payment acceptance by optimizing routing. WhenThen provides the first end-to-end payment flow platform to equip businesses with the opportunity to control every stage of the payment flow from payment intent to payout.”

WhenThen supports a wide range of popular payment providers such as Stripe, Braintree, Adyen, Authorize.net, Checkout.com, etc., and a variety of alternative and locally preferred payment methods such as Klarna Affirm, PayPal and BitPay.

“For brave merchants considering global reach and operating multiple business models concurrently, I believe choosing the right payment ops platform will become as important as choosing the right e-commerce platform. Building your entire e-comm experience tightly coupled to a single payment processor is a hard correction to make down the line — you need a payment flow platform like WhenThen”, added Fred Destin, founder of Stride.VC.

Powered by WPeMatico

The fintech sector has been hugely successful (and hugely profitable) for much of the last decade, and even more so during the pandemic. But it might come as a surprise to learn that many in the industry believe that the story is just beginning and the sector is poised to achieve much more, with fintech’s next decade expected to be radically different from the last 10 years.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Now that these initiatives are in place, however, we’re seeing that their effect goes way beyond opening up a gap for challenger banks. Since open banking requires that banks make valuable data available via APIs, it is leading to a revolution in the way that small and mid-size enterprises (SMEs) are funded — one in which data, and not hard capital, is the most important factor driving fintech success.

In order to understand the changes that are sweeping fintech and reconfiguring the way that the industry works with small businesses, it’s important to understand open banking. This is a concept that has really taken hold among governmental and supranational banking regulators over the past decade, and we are now beginning to see its impact across the banking sector.

Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

At its most fundamental level, open banking refers to the process of using APIs to open up consumers’ financial data to third parties. This allows these third parties to design, build and distribute their own financial products. The utility (and, ultimately, the profitability) of these products doesn’t rely on them holding huge amounts of capital — rather, it is the data they harvest and contain that endows them with value.

Open-banking models raise a number of challenges. One is that the banking industry will need to develop much more rigorous systems to continually seek consumer consent for data to be shared in this way. Though the early years of fintech have taught us that consumers are pretty relaxed when it comes to giving up their data — with some studies indicating that almost 60% of Americans choose fintech over privacy — the type and volume shared through open-banking frameworks is much more extensive than the products we have seen up until now.

Despite these concerns, the push toward open banking is progressing around the world. In Europe, the PSD2 (the Payment Services Directive) requires large banks to share financial information with third parties, and in Asia services like Alipay and WeChat in China, and Tez and PayTM in India are already altering the financial services market. The extra capabilities available through these services are already leading to calls for the U.S. banking system to embrace open banking to the same degree.

If the U.S. banking industry can be convinced of the utility of open banking, or if it is forced to do so via legislation, several groups are likely to benefit:

By far the biggest beneficiary of open banking, however, will be SMEs. This is not necessarily because open-banking frameworks offer specific new functionality that will be useful to small and medium-sized businesses. Instead, it is a reflection of the fact that SMEs have historically been so poorly served by traditional banks.

SMEs are underserved in a number of ways. Traditional banks have an extremely limited ability to view the aggregate financial position of an SME that holds capital across multiple institutions and in multiple instruments, which makes securing finance very difficult.

In addition, SMEs often have to deal with dated and time-consuming manual interfaces to upload data to their bank. And (perhaps worst of all) the B2B payment systems in use at most banks provide very limited feedback to the businesses that use them — a lack of information that can cost businesses dearly.

Given these deficiencies, it’s not surprising that fintech startups are keen to lend to small businesses, and that SMEs are actively looking for novel banking products and services. There have, of course, already been some success stories in this space, and the kinds of banking systems available to SMEs today (especially in Europe) are leagues ahead of the services available even 10 years ago.

However, open banking promises to accelerate this transformation and dramatically improve the financial services available to the average SME. It will do this in several ways. Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

Via APIs, fintech companies will be able to access information on different types of accounts, insurance, card accounts and leases, and consolidate data from multiple countries into one overall picture.

This, in turn, will have major effects on the way that credit-worthiness is assessed for SMEs. At the moment, there is a funding gap facing many SMEs, largely because banks have been hesitant to move away from the “balance sheet” model of assessing credit risk. By using real-time analytics on an SME’s current business activities, banks will be able to more accurately assess this risk and lend to more businesses.

In fact, this is already happening in countries where open banking is well advanced – in the U.K., Lloyds’ Business ToolBox offers unlimited credit checks on companies and directors in addition to account transaction data.

Open banking will also allow peer comparison analytics far ahead of what we have seen until now. APIs can be used to provide SMEs real-time feedback on how they are performing within their market sector. Again, this ability is already available in the U.K., with Barclays’ SmartBusiness Dashboard offering marketing effectiveness tools as part of a customizable business dashboard.

These capabilities will be so useful to SMEs that they are likely to drive the popularity of any fintech product that offers them. For SMEs, this value will lie mainly in intelligent data-analytics-based insights, recommendations and automatic prompts that can be built on top of account aggregation.

Then, additional insights generated from these same monitoring tools could enable banks and alternative lenders to be more proactive with their lending — offering preapproved lines of credit, in a timely manner, to SMEs that would have previously found it difficult to access funding.

Crucially for the fintech sector, it’s almost a certainty that SMEs will be willing to pay fees for data-analytics-based value-added services that help them grow. This is why some startups in this space are already attracting huge levels of funding, and why open banking is at the heart of the relationship between tech and the economy.

So if fintech has had a good year, this is likely to be just the start of the story. Backed by open-banking initiatives, the sector is now at the forefront of a banking revolution that will finally give SMEs the level of service they deserve and unleash their true potential across the economy at large.

Powered by WPeMatico

The gamification of payments is not a new concept.

A number of companies are attempting to combine gamification and payments in creative ways. And today, one such company, Play2Pay, has raised $13 million in a Series A round of funding.

The Miami-based startup has a straightforward mission. It wants to give consumers a way to reduce their bills — it claims by an average of 30%! — by playing games, watching videos and completing daily challenges, offers and surveys.

Play2Pay was bootstrapped for the first five years of its life, raising its first external capital in June of 2020 — a $7.5 million seed round from individual angel investors. Telesoft Partners led its Series A round, which included participation from Harbor Spring Capital and individual investors including former AT&T vice chairman Ralph de la Vega, former Reuters CEO Tom Glocer, Madison Dearborn Partners co-founder and senior advisor Jim Perry and Virtusa founder and former CEO, Kris Canekeratne.

The alternative payment platform says it brokers a “value exchange” between brands and consumers, converting attention and engagement into a currency, which can be redeemed for bill payment. Meanwhile, brands get a new way to promote their products and services.

Play2Pay founder and CEO Brian Boroff started the company in 2015 based on a vision that prepaid mobile phone users should have an alternative way to pay for their mobile phone service and that wireless carriers would adopt an ad-funded commercial model.

Today, the company claims to be positioned to be the world’s first “ad supported payment rail” directly integrated into payments platforms of major service providers and financial institutions. It also claims to be the only company that converts user engagement directly into bill payment.

Image Credits: Play2Pay

The “opt-in” offering is currently available to more than 100 million mobile subscribers across the United States, United Kingdom, Mexico, Brazil and Indonesia through partnerships with telecom companies such as AT&T Mexico, Cricket in the U.S., TIM in Brazil, lndosat Ooredoo in Indonesia and U.K.-based Lycamobile.

The rewarding approach seems to be resonating with users. From June 2020 to June 2021, the startup saw its ARR (annual recurring revenue) spike by nearly 300%, according to Boroff, a telecom veteran.

Among the users engaged on the platform, about 25% generated revenue daily, he said. And service providers realized up to 17% revenue expansion as a result of subscriber engagement on the Play2Pay platform, according to Boroff.

“Our distribution model is B2B2C, with Tier-1 service providers worldwide directly integrating our bill payment capability. We’re growing our audience through promotion of the service to their customer base,” he told TechCrunch.

End users, he added, can share their targeting preferences in exchange for value, giving mobile app developers and brands more information when promoting their own products and services to Play2Pay’s audience.

The platform is free for service providers and merchants, meaning the payment does not have costs or fees from interchange, acquirers, chargebacks or gateways.

Instead, Play2Pay generates revenue from mobile app developers and brands. Those developers and brands pay to access Play2Pay’s mobile audience in order to promote their products and services. For example, a mobile gaming company might pay Play2Pay $100 for every user that downloads their app from the Play2Pay app and plays the game for a period of time (such as two hours). Through its technology and partner network, Play2Pay has attribution tracking to ensure that the end user and mobile gaming company both know how much progress has been made toward completing that goal. Other formats include watching videos, completing surveys and more conventional native advertising in some areas.

Powered by WPeMatico

Orum, which aims to speed up the amount of time it takes to transfer money between banks, announced today it has raised $56 million in a Series B round of funding.

Accel and Canapi Ventures co-led the round, which also included participation from existing backers Bain Capital Ventures, Inspired Capital, Homebrew, Acrew, Primary, Clocktower and Box Group. The financing comes barely three months after Orum announced a $21 million Series A, and brings its total raised to over $82 million.

Orum CEO Stephany Kirkpatrick launched the company in 2019 after working for several years at LearnVest, a personal finance site founded by Alexa von Tobel that was acquired by Northwestern Mutual in 2015 for an estimated $375 million. Tobel went on to form Inspired Capital, a venture capital firm that put money in Orum’s $5.2 million seed round last August. Prior to that, the firm also provided Orum with an “inspiration check” that was the first money into the business.

“Most Americans are not familiar with the intricacies of ACH [automated clearing house) or why it takes multiple business days to move money between accounts,” Kirkpatrick said. “But none of us can allow money to wait 5-7 days to hit our accounts. It needs to be instant.”

Her mission with Orum is straightforward even if the technology behind it is complex. Put simply, Orum aims to use machine learning-backed APIs to “move money smartly across all payment rails, and in doing so, provide universal financial access.”

Orum’s first embeddable product, Foresight, launched in September of 2020. It’s an automated programming interface designed to give financial institutions a way to move money in real time. The platform uses machine learning and data science to predict when funds are available and to identify any potential risks. Its Momentum product “intelligently” routes funds across payments rails and is powered by banking providers JPMorgan Chase and Silicon Valley Bank.

“They power the back end of our Momentum platform that allows the money to move on a multirail basis,” Kirkpatrick told TechCrunch. “They power our access to real-time payments.”

Orum says it serves a range of enterprise partners, including Alloy, HM Bradley, First Horizon Bank and Zero Financial (which was recently acquired by Avant).

The volume of transactions being conducted with Orum is growing 100% month over month, Kirkpatrick said. Most of its early growth has come from word of mouth.

The remote-first company prides itself on diversity — in both its employee and investor base. For one, 48% of its 55-person headcount are female, and 48% are “nonwhite,” according to Kirkpatrick. Orum also recently joined the Cap Table Coalition — a partnership between high-growth startups and emerging investors who want to work to close the racial wealth gap — to allocate over 10% of its Series B round to underrepresented founders. For example, the financing includes investors such as the Neythri Features Fund, a group of South Asian women investing in the next generation of female founders and diverse teams.

Jeffrey Reitman, partner at Canapi Ventures (a firm whose LPs mostly consist of banks), told TechCrunch that those bank LPs conduct hundreds of millions of ACH transactions annually,

“They need a path to achieving a state where funds can be transferred instantly,” he said. “Orum’s product paves the path for many players in financial services and fintech — and beyond — to partake in faster money movement without compromising key risk principles.”

To Reitman, the company’s major differentiators are its team, which he describes as consisting of “the best group of data scientists and engineers in the space.”

“Many of their customers consider the team to be instrumental in helping to set the risk dials on how they fund transactions by teasing out key data and insights from historical transaction data,” he said. “Second, Orum is building one of the densest and most comprehensive data sets around the risks of money movement. Better data means better risk models, and it will be hard for other offerings to match Orum’s approach to building this rich data set.”

Accel Partner Sameer Gandhi, who joined Orum’s board as part of the latest financing, agrees. He believes that in an 18-month period, Orum has built “game-changing technology and an exceptional team.”

“Orum is tackling financial infrastructure from its foundation,” he said.

The headline was updated post-publication to reflect the correct funding amount.

Powered by WPeMatico

Mercuryo, a startup that has built a cross-border payments network, has raised $7.5 million in a Series A round of funding.

The London-based company describes itself as “a crypto infrastructure company” that aims to make blockchain useful for businesses via its “digital asset payment gateway.” Specifically, it aggregates various payment solutions and provides fiat and crypto payments and payouts for businesses.

Put more simply, Mercuryo aims to use cryptocurrencies as a tool for putting in motion next-gen, cross-border transfers or, as it puts it, “to allow any business to become a fintech company without the need to keep up with its complications.”

“The need for fast and efficient international payments, especially for businesses, is as relevant as ever,” said Petr Kozyakov, Mercuryo’s co-founder and CEO. While there is no shortage of companies enabling cross-border payments, the startup’s emphasis on crypto is a differentiator.

“Our team has a clear plan on making crypto universally available by enabling cheap and straightforward transactions,” Kozyakov said. “Cryptocurrency assets can then be used to process global money transfers, mass payouts and facilitate acquiring services, among other things.”

Image Credits: Left to right: Alexander Vasiliev, Greg Waisman, Petr Kozyakov / MercuryO

Mercuryo began onboarding customers at the beginning of 2019, and has seen impressive growth since with annual recurring revenue (ARR) in April surpassing over $50 million. Its customer base is approaching 1 million, and the company has partnerships with a number of large crypto players including Binance, Bitfinex, Trezor, Trust Wallet, Bithumb and Bybit. In 2020, the company said its turnover spiked by 50 times while run-rate turnover crossed $2.5 billion in April 2021.

To build on that momentum, Mercuryo has begun expanding to new markets, including the United States, where it launched its crypto payments offering for B2B customers in all states earlier this year. It also plans to “gradually” expand to Africa, South America and Southeast Asia.

Target Global led Mercuryo’s Series A, which also included participation from a group of angel investors and brings the startup’s total raised since its 2018 inception to over $10 million.

The company plans to use its new capital to launch a cryptocurrency debit card (spending globally directly from the crypto balance in the wallet) and continuing to expand to new markets, such as Latin America and Asia-Pacific.

Mercuryo’s various products include a multicurrency wallet with a built-in crypto exchange and digital asset purchasing functionality, a widget and high-volume cryptocurrency acquiring and OTC services.

Kozyakov says the company doesn’t charge for currency conversion and has no other “hidden fees.”

“We enable instant and easy cross-border transactions for our partners and their customers,” he said. “Also, the money transfer services lack intermediaries and require no additional steps to finalize transactions. Instead, the process narrows down to only two operations: a fiat-to-crypto exchange when sending a transfer and a crypto-to-fiat conversion when receiving funds.”

Mercuryo also offers crypto SaaS products, giving customers a way to buy crypto via their fiat accounts while delegating digital asset management to the company.

“Whether it be virtual accounts or third-party customer wallets, the company handles most cryptocurrency-related processes for banks, so they can focus more on their core operations,” Kozyakov said.

Mike Lobanov, Target Global’s co-founder, said that as an experiment, his firm tested numerous solutions to buy Bitcoin.

“Doing our diligence, we measured ‘time to crypto’ – how long it takes from going to the App Store and downloading the app until the digital assets arrive in the wallet,” he said.

Mercuryo came first with 6 minutes, including everything from KYC and funding to getting the cryptocurrency, according to Lobanov.

“The second-best result was 20 minutes, while some apps took forever to process our transaction,” he added. “This company is a game-changer in the field, and we are delighted to have been their supporters since the early days.”

Looking ahead, the startup plans to release a product that will give businesses a way to send instant mass payments to multiple customers and gig workers simultaneously, no matter where the receiver is located.

Powered by WPeMatico

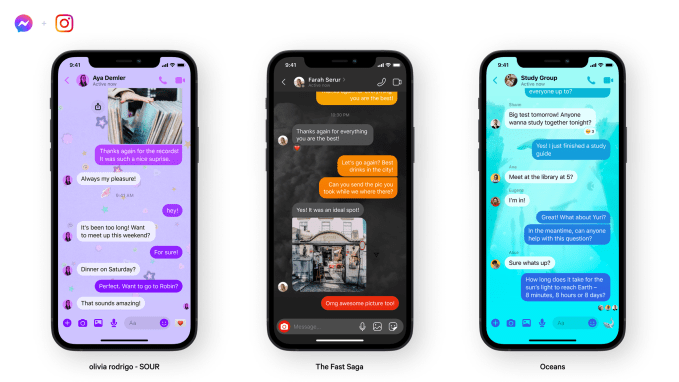

This spring, Facebook confirmed it was testing Venmo-like QR codes for person-to-person payments inside its app in the U.S. Today, the company announced those codes are now launching publicly to all U.S. users, allowing anyone to send or request money through Facebook Pay — even if they’re not Facebook friends.

The QR codes work similarly to those found in other payment apps, like Venmo.

The feature can be found under the “Facebook Pay” section in Messenger’s settings, accessed by tapping on your profile icon at the top left of the screen. Here, you’ll be presented with your personalized QR code which looks much like a regular QR code except that it features your profile icon in the middle.

Underneath, you’ll be shown your personal Facebook Pay UR which is in the format of “https://m.me/pay/UserName.” This can also be copied and sent to other users when you’re requesting a payment.

Facebook notes that the codes will work between any U.S. Messenger users, and won’t require a separate payment app or any sort of contact entry or upload process to get started.

Users who want to be able to send and receive money in Messenger have to be at least 18 years old, and will have to have a Visa or Mastercard debit card, a PayPal account or one of the supported prepaid cards or government-issued cards, in order to use the payments feature. They’ll also need to set their preferred currency to U.S. dollars in the app.

After setup is complete, you can choose which payment method you want as your default and optionally protect payments behind a PIN code of your choosing.

The QR code is also available from the Facebook Pay section of the main Facebook app, in a carousel at the top of the screen.

Facebook Pay first launched in November 2019, as a way to establish a payment system that extends across the company’s apps for not just person-to-person payments, but also other features, like donations, Stars and e-commerce, among other things. Though the QR codes take cues from Venmo and others, the service as it stands today is not necessarily a rival to payment apps because Facebook partners with PayPal as one of the supported payment methods.

However, although the payments experience is separate from Facebook’s cryptocurrency wallet, Novi, that’s something that could perhaps change in the future.

Image Credits: Facebook

The feature was introduced alongside a few other Messenger updates, including a new Quick Reply bar that makes it easier to respond to a photo or video without having to return to the main chat thread. Facebook also added new chat themes including one for Olivia Rodrigo fans, another for World Oceans Day, and one that promotes the new F9 movie.

Powered by WPeMatico

On the heels of acquiring sales tax specialist TaxJar in April, today Stripe is making another big move in the area of tax. The $95 billion payments behemoth is launching a new product called Stripe Tax, which will provide automatic, updated sales tax calculations (covering sales tax, VAT and GST) and related accounting services to Stripe payments customers initially in some 30 countries and across the U.S.

Stripe Tax is a separate service from TaxJar, but the two are not unconnected. As Stripe Tax was being built out of Stripe’s offices in Dublin over the last several months, Stripe’s business lead for EMEA Matt Henderson told me that the team had identified TaxJar as a strong company in the field. That ultimately led to M&A between them.

Sales tax — and specifically a more seamless way to deal with charging and tracking sales tax — is a painful issue for people doing business online.

Digital and physical goods are taxed in over 130 countries, Stripe said, and within that there can be a huge amount of variation and compliance complexity, since codes get updated all the time, too. Mishandled sales tax, meanwhile, can result in pretty hefty fines, sometimes up to 30% interest on past-due amounts.

Unsurprisingly, a sales tax tool has been the most-requested feature from Stripe’s customers, Henderson said, a call that presumably only got louder in the last year, as e-commerce and digital transactions went through the roof with COVID-19.

Arguably, that makes Stripe Tax one of the company’s more significant product launches, not to mention the first since announcing its monster funding round earlier this year.

Previously, Stripe customers would have resorted to using a third-party service (like TaxJar) to work out sales tax. Or, more typically, those Stripe customers would have opted to limit the number of places they sold goods and services, in order to minimize the pain of dealing with multiple, complex and usually quite localized tax codes.

“No one leaps out of bed in the morning excited to deal with taxes,” said John Collison, co-founder and president of Stripe in a statement. “For most businesses, managing tax compliance is a painful distraction. We simplify everything about calculating and collecting sales taxes, VAT, and GST, so our users can focus on building their businesses.”

Stripe said that a survey of its customers found that two-thirds of respondents said the challenge of implementing sales tax actually limited their growth.

TaxJar has built a strong system for handling that, but the company — based out of Massachusetts but with a remote team — is primarily focused on the U.S. market, which has sales tax that is complicated enough (there are 11,000 different tax jurisdictions in the country).

That leaves a lot on the table for building out sales tax tools for the rest of the world: The wider focus of Stripe Tax thus fills a particular geographical gap for the company, regardless of how well TaxJar and Stripe integrate over time.

There is another key difference worth noting between the two.

TaxJar came to Stripe’s attention with an established operation — 23,000 customers at the time of the announcement. Stripe (wisely) bolted that on as a standalone business, which means that new and existing customers that use TaxJar can continue to use it as is. That is to say, at least for now, they do not need to be Stripe payments customers in order to use TaxJar, even if the integration between the two platforms will only improve over time.

Stripe Tax, on the other hand, is being built from the ground up as a product aimed specifically at increasing touchpoints and stickiness with Stripe customers.

Stripe Tax provides real-time tax calculation based on customer location and product sold; transparent itemizing for customers; tax ID management in areas (like Europe) where business customers can provide their code and get a reverse charge on tax if they are under a certain turnover threshold themselves; and reconciliation and reporting across all transactions to make filing and remittance easier.

But there is for now no way to use Stripe Tax outside of Stripe payments.

This could pose some problems for some customers. These days, many of the strongest retailers will take an “omnichannel” approach that might cover selling through marketplaces, selling through websites, selling through social media and more — and not all of those experiences may be powered by Stripe. It will be worth watching whether future iterations of Stripe Tax can account for that.

Stripe’s most significant product launch prior to Stripe Tax — Stripe Treasury last December — underscores how the company is currently very focused on diversifying outside of its basic payments business and opening the platform to much wider, more scaled transactions.

Treasury, which is still in invite-only mode, saw Stripe partner with established banks to provide a business banking service, providing a way for its customers to handle money that they generate from their Stripe-powered businesses.

The full country list where Stripe Tax is launching is Australia, Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, New Zealand, the Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, Switzerland, the United States and the United Kingdom.

Updated to correct the number of customers TaxJar has to 23,000.

Powered by WPeMatico

The agriculture sector is ripe for technological improvements, but beyond satellite-based crop management and bees-as-a-service, the actual people who work in the fields should be benefiting as well. Ganaz, empowered by a $7 million A round, aims to change how people with little documentation and no bank account get paid and send money with a modern workforce stack that embraces low tech as well.

Growers — that is to say, the companies that own and operate the fields and sell the crops — are under pressure from multiple directions as wages rise, regulations increase and willing workers dwindle. They need to save money to make money, but they can’t do so by paying less; in addition to being cruel to a marginalized class of people, it would only exacerbate the labor shortage in the sector.

There are plenty of companies out there that help save costs by automating things like payroll and onboarding, but the agriculture business has some unique limitations.

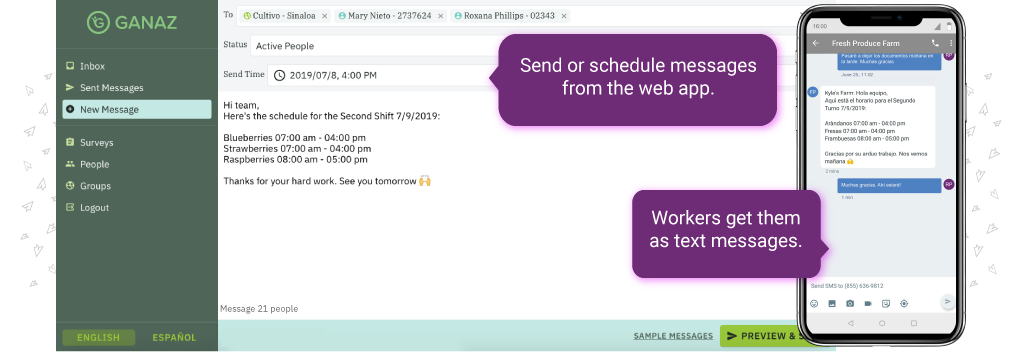

“It’s still operating like it’s the ’80s,” explained Ganaz founder and CEO Hannah Freeman. The number one service these workers rely on is check cashing or payday loans, and fees from these, currency exchange, ATM fees and remittances eat up a significant portion of each paycheck. “The workforce in our world definitely doesn’t have corporate email and rarely uses personal email. They have trouble downloading and using mobile apps, don’t use usernames. But they’re very conversant in WhatsApp and SMS — so you have to kind of know how to build for them.”

Image Credits: Ganaz

The ecosystem has parallels to other regions that have stuck with older, cheaper technologies instead of adopting the latest and most expensive tech. Entire markets in Africa and South America, for instance, run on text-based commerce taking place on aging and unreliable infrastructure.

Ganaz has opted for a hybrid approach. The company’s platform offers several services on both the worker and employer side.

Onboarding and basic training can be done simply and intuitively for people who may not be highly literate, via tablets loaded with apps that also operate offline. The most common alternative seems to be file folders served out of a crate in the back of a pickup — that’s not a dig, it’s just what has made sense for years for this highly fluid, distributed workforce.

Payment and balance checks all happen over SMS or WhatsApp with workers, but for sensitive information they are shunted to a web app; similarly, integrated remittance partnerships are coming that will keep things simple and reduce fees.

On the employer side, the workers and all their vital stats and documents are tracked centrally in the kind of interface companies have grown to expect. And Ganaz works as an intermediary to send text alerts and questions.

Image Credits: Ganaz

So far Ganaz has 75 employers signed up, one of which is a Costco supplier group, and all told around 175,000 workers on the platform. Their ARR and user count both approximately tripled year over year, so they’re clearly on to something.

The company has tempered its rapid growth with designation as a public benefit corporation, which emphasizes the intention to do more than grow shareholder value. I asked about the tension between needing to show a profit and working in the service of a marginalized group.

“This keeps me up at night,” admitted Freeman. “We try to make sure to set ourselves up to be true to our mission. That means the folks we hire, our board of directors… we want to make sure we’re empathizing and honoring the trust we’ve built with people.”

That includes investors as well, and Freeman noted that the company ended up going with Trilogy as lead for this round partly because of that firm’s experience with Remit.ly.

For instance, Freeman noted, while it would be easy to juice profits by bumping ATM fees, that directly harms the people they’re trying to help. Instead, when they issue their payroll Mastercard later this year, that will allow workers to skip the check cashing step and its fees, and then Ganaz gets a share of the normal card transaction fee. “We can be equally successful that way,” said Freeman, and it doesn’t just replace another predatory structure.

After the cards the plan is to automate remittances, so a user can easily choose to send money to their family in a way that minimizes handling fees and so on. And there will be other options, accessible via text, to choose where money goes if not to the card.

Ganaz’s main market is the U.S. and Mexico, since the agriculture business and workforce are both largely binational, but there are other targets on the horizon. First, though, the company wants to solidify its position and feature set here. “There’s no breakaway winner yet, so we want to be that winner,” said Freeman.

The $7 million round also had participation from Bessemer Venture Partners, Founders’ Co-op, Taylor Ventures, AgFunder and Techstars. Rapid expansion and aggressive pursuit of the roadmap are next up for Ganaz.

“We are conscious of both the huge opportunity ahead of us to digitize billions of dollars in payroll, as well as the responsibility to build inclusive, low-cost, wealth-building tools for workers,” said Freeman.

Powered by WPeMatico

Just about every week there’s a blockbuster round coming out of South America, but in certain countries such as Ecuador, things have been more hush-hush. However, Kushki, a Quito-based fintech, is bringing attention to the region with today’s announcement of an $86 million Series B and a $600 million valuation.

“We never thought that we would return home [from the U.S.] and build a company that was more valuable in Ecuador than we had built in the U.S.,” said Aron Schwarzkopf, CEO and co-founder of Kushki.

Schwarzkopf and his business partner, Sebastián Castro, previously built and sold a fintech called Leaf in the U.S. in 2014. The two are originally from Ecuador but moved to Boston for college, where they met watching soccer.

Unlike many other fintechs in LatAm that are out to help the unbanked, Kushki works behind the scenes building the tech infrastructure that companies like Nubank use to transfer money. Some of the functionalities they build enable both local and cross-border payment players in credit and debit cards, bank transfers, digital cash, mobile wallets and other alternative payment methods.

“We realized there was a gigantic opportunity to democratize and create infrastructure to move money,” Schwarzkopf told TechCrunch.

The company, which was founded in 2017, already has operations in Mexico, Colombia, Ecuador, Peru and Chile. The Series B will be used to accelerate growth and expand to Brazil and nine other markets in Central America.

Generally, expanding to Brazil is an expensive proposition, and therefore not a path that all companies can take, even though it can be an extremely profitable move if done right. Some of the challenges include the need to translate everything into Portuguese followed by the varying financial regulations.

That’s why Kushki’s approach has to be somewhat custom in each country.

“We focus on going into the markets and we basically rebuild an entire infrastructure, so we put everything into one API,” said Schwarzkopf.

Products similar to Kushki have been successful in other regions around the world, such as in India with Pine Labs, Africa with Flutterwave and Checkout.com, which now has 15 international offices.

To build all this infrastructure, Kushki, which means “cash” in a native Andes dialect, has raised a total of $100 million from SoftBank and an undisclosed global growth equity firm, as well as previous investors including DILA Capital, Kaszek Ventures, Clocktower Ventures and Magma Partners.

“From now until 2060, people will need servers and ways to move money, and we knew that the existing payment infrastructure couldn’t support that,” said Schwarzkopf.

Powered by WPeMatico