payments

Auto Added by WPeMatico

Auto Added by WPeMatico

If you’re a founder who finds yourself in a meeting with a VC, try to remember two things:

Even so, many entrepreneurs squander this opportunity, often because they direct questions or fail to understand their BATNA (best alternative to a negotiated agreement).

“As the venture landscape becomes more a meritocratic environment where resumes and institutional affiliations matter less, these strategies can make the difference between a successful fundraise and a fruitless meeting,” says Agya Ventures co-founder Kunal Lunawat.

Whether you’re already in the fundraising process or plan to be in the future, be sure to read “A crash course on corporate development” that Venrock VP Todd Graham shared with us this week.

“If you’re going to get acquired, chances are you’re going to spend a lot of time with corporate development teams,” says Graham. “With a hot stock market, mountains of cash and cheap debt floating around, the environment for acquisitions is extremely rich.”

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

On Wednesday, August 24 at 3 p.m. PDT/6 p.m. EDT/11 p.m GMT, Managing Editor Danny Crichton will host a conversation on Twitter Spaces with Eric Dean Wilson, author of “After Cooling: On Freon, Global Warming, and the Terrible Cost of Comfort.”

Wilson’s book explores the history of freon, a common refrigerant that was later banned due to its devastating impact on the ozone layer. After their discussion, they’ll take questions from the audience.

Thanks very much for reading Extra Crunch this week! I hope you have an excellent weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Carol Yepes (opens in a new window) / Getty Images

Apple iPhone, Apple Mail and Apple iPad account for nearly half of all email opens, but the privacy features included with iOS 15 will allow consumers to block marketers from seeing their physical location, IP address and tracking data like invisible pixels.

Email marketers rely heavily on these and other metrics, which means they should prepare now for the changes to come, advises Litmus CMO Melissa Sargeant.

In a detailed post, she shares several action items that will help marketing teams leverage their email analytics so they can “continue delivering personalized experiences consumers crave.”

Image Credits: Cimmerian (opens in a new window) / Getty Images

Venrock Vice President Todd Graham has some frank advice for founders at venture-backed startups: “It would be wise to generate a return at some point.”

With that in mind, he authored a primer on corporate development that lays out the three most common categories of acquisitions, tips for dealing with bankers, and explains why striking a partnership with a big company isn’t always the best way forward.

Regardless of the path you choose, “you need to take the meeting,” advises Graham.

“In the worst-case scenario, you’ll get a few new LinkedIn connections and you’re now a known quantity. The best-case scenario will be a second meeting.”

Image Credits: Nigel Sussman (opens in a new window)

The pandemic failed to slow the momentum of venture capitalists pouring money into startups, but Chicago stands out as an “outlying benefactor of accelerating venture capital activity and the rise of remote investing,” Alex Wilhelm and Anna Heim write for The Exchange.

When the world shut down and it didn’t matter if you were in NYC or SF (because everyone was on Zoom), the Windy City was ready to present itself as the venture champion of the Midwest.

Image Credits: Priscila Zambotto (opens in a new window) / Getty Images

The Brazilian Central Bank made a major reform to the way payments are processed that may throw the doors open for e-commerce in South America’s largest market.

Historically, merchants who accepted credit card payments had two options: Receive the full payment distributed over two to 12 installments, or offer a deep discount to receive a smaller sum up front.

But in June 2021, the BCB created new “registration entities” that permit “any interested receivables buyer/acquirer to make an offer for those receivables, forcing buyers to become more competitive in their discount offers,” says Leonardo Lanna, head of payment products at Monkey Exchange.

The new framework benefits consumers and sellers, but for the region’s startups, “it opens the door to a plethora of opportunities and new business models, from payments to credit.”

Image Credits: Nigel Sussman (opens in a new window)

An inflow of VC dollars, notable acquisitions and rising unicorn counts are all features of the Brazilian tech startup market, Anna Heim and Alex Wilhelm note in The Exchange.

“The IPO market in Brazil is changing,” they write. “TechCrunch noted last year that in the decade leading up to 2020, just two of the 56 IPOs in Brazil were technology companies. More recently, the number of technology companies listed in the country has swelled to at least 16, up from just four in 2019.”

Image Credits: Andriy Onufriyenko / Getty Images

“For good reason, security certifications like the SOC 3 really put you through the wringer,” Waydev CEO Alex Cercei writes in a guest column.

Waydev, a Git analytics tool that helps engineering leaders measure team performance automatically, just attained the SOC 3 certification.

“We learned so much from the process, we felt it was right to share our experience with others that might be daunted by the prospect,” Cercei writes.

“So here’s our advice on how teams can smoothly reach an SOC 3 while simultaneously balancing workloads and minimizing disruption to users.”

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

I’m on an H-1B living and working in the U.S. I want to apply for a green card on my own. I’m concerned about only relying on my current employer and I want to be able to easily change jobs or create a startup. I’ve been looking at the EB-1A and EB-2 NIW.

I’m not sure if I would qualify for an EB-1A, but since I was born in India, I face a much longer wait for an EB-2 NIW.

Any tips on how to proceed?

— Inventive from India

Image Credits: Cordelia Molloy Science Photo Library (opens in a new window) / Getty Images

Most startups could use an advisory board, but in health tech, it’s a core requirement.

Founders seeking to innovate in this area have a unique need for mentors who have experience navigating regulations, raising capital and managing R&D, to name just a few areas.

Based on his own experience, Patrick Frank, co-founder and COO of PatientPartner, shared some very specific ideas about who to recruit, where to find them and how to fit them into your cap table.

“You want to leverage these individuals so you are able to focus on the full view of the company to ensure it is something that both the market and investors want at scale,” says Frank.

Image Credits: Nigel Sussman (opens in a new window)

There’s no shortage of tech news to analyze, Alex Wilhelm notes, but this week, he took a fresh look at crypto.

How come?

“Because there are some rather bullish trends that indicate the world of blockchain is maturing and creating a raft of winning players,” he writes.

Image Credits: kentoh (opens in a new window) / Getty Images (Image has been modified)

In one recent survey, 58% of workers said they plan to quit if they’re not allowed to work remotely.

Startups that don’t offer employees work-from-home flexibility are at a competitive disadvantage, but figuring out how to pay hybrid workers raises a complex set of questions:

Powered by WPeMatico

Breef raised $3.5 million in funding to continue developing what it boasts as “the world’s first online marketplace” for transactions between brands and agencies.

Greycroft led the round and was joined by Rackhouse Ventures, The House Fund, John and Helen McBain, Lance Armstrong and 640 Oxford Ventures. Including the new round, the New York and Colorado-based company has brought in total funding of $4.5 million since its inception in 2019 by husband-and-wife co-founders George Raptis and Emily Bibb.

Bibb’s background is in digital marketing and brand building at companies like PopSugar, VSCO and S’well, while Raptis was on the founding team at fintech company Credible.com.

Both said they experienced challenges in finding agencies, which traditionally involved asking for referrals and then making a bunch of calls. There were also times when their companies would be in high demand for talent, but didn’t necessarily need a full-time employee to achieve the goal or project milestone.

While the concept of outsourcing is not new, Breef’s differentiator is its ability to manage complex projects: a traditional individual freelance project is less than $1,000 and takes a week or less. Instead, the company is working with team-based projects that average $25,000 with a length of engagement of about six months, Raptis said.

Breef’s platform is democratizing how brands and boutique agencies connect with each other in the process of planning, scoping, pitching and paying for projects, Raptis told TechCrunch.

“At the core, we are taking the agency online,” Bibb added. “We are building a platform to streamline a complicated process for outsourcing high-value work and allow users to find, pay for and work with agencies in days rather than months.”

Brands can draft their own brief to articulate what they need, and Breef will connect them to a short list of agencies that match those requirements. Rather than a one- or two-month search, the company is able to bring that down to five days.

Bibb and Raptis decided to seek venture capital after experiencing demand — millions of dollars in projects are being created on the platform each month — and some tailwinds from the shift to remote work. They saw many brands that may have originally utilized in-house teams or agencies of record turn to distributed or smaller teams.

Due to the nature of agency work being expensive, Breef is processing large amounts of money over the internet, and the founders want to continue developing the technology and hiring talent so that it is a secure and trustworthy system.

It also launched its buy now, pay later project funding service, Breef(pay), to streamline payments to agencies and reduce cash flow challenges. Users can construct their own payment terms, mix up the way they are paid and utilize a credit line or defer payments to control external spend.

To date, Breef has more than 5,000 vetted boutique agencies in 20 countries on its platform and is able to save its users an average of 32% in product costs compared with a traditional agency model. It boasts a customer list that includes Spotify, Brex, Shutterstock, Bluestone Lane and Kinrgy.

Kevin Novak, founder of Rackhouse Ventures, said he met Raptis through the Australian tech community. He recently launched his first fund targeting startups in novel applications of data.

“When they were talking to me about what they wanted to do, I got intrigued,” Novak said. “I like finding marketplaces where the idea is well understood by the people involved. Looking at the matching problem, Emily and George have found a unique way to find ad agencies that hasn’t existed before.”

Powered by WPeMatico

Danggeun Market, the publisher of South Korea’s hyperlocal community app Karrot, announced it has raised $162 million in a Series D round of funding with a valuation of $2.7 billion. (By the way, Danggeun means carrot in Korean.)

This round of funding was led by DST Global, with additional participation from Aspex Management, Reverent Partners and existing investors such as Goodwater Capital, Altos Ventures, SoftBank Ventures Asia, Kakao Ventures, Strong Ventures and Capstone Partners.

The latest funding officially makes Danggeun Market a unicorn, with $205 million total raised.

The company plan to strengthen its capabilities in local commerce with Danggeun Pay, or Karrot Pay, which is set to launch this year, and Danggeun’s platform Karrot enables approximately 300,000 local SMB partners to go digitalized by offering offline to online (O2O) service. Danggeun Market’s consumers access everything from fresh local produce delivery to essential services, including cleaning, education, real estate brokerage and used cars in their local communities.

The funding proceeds from the new round will be used for further global expansion, business diversification, R&D, investment in advanced artificial intelligence and machine learning technology and recruiting team talent.

“Danggeun Market plans to focus on accelerating further overseas market expansion for the next two years after closing Series D funding, and in South Korea, we will diversify our business, aiming to be a super app,” co-founder and co-CEO Gary Kim said in an exclusive conversation with TechCrunch.

Danggeun Market, which is short for “the market in your neighborhood,” was founded by Gary Kim and Paul Kim in 2015.

Danggeun Market also plans to launch its payment service Karrot Pay, expand offline to online (O2O) service for South Korean SMEs that use its platform Karrot and invest to develop advanced artificial intelligence and machine learning in its platform for suggesting personalized feeds for users to stay longer, Kim continued.

Danggeun Market is expected to get approval from South Korea’s financial supervisory service (FSS) as early as September for two licenses, such as payment gateway operator (PG) and prepaid payment means operator, to launch Danggeun Market’s payment service, Karrot Pay, this year, Kim said.

Danggeun Market, which already launched its global version of hyperlocal community app Karrot in the U.K. in November 2019, currently operates the Karrot app in 72 local communities in four countries: the U.K., the U.S., Canada and Japan.

“We see some active transactions in Manchester, Birmingham and Toronto,” Kim said. Danggeun Market launched Karrot in Canada and the U.S. in September and October 2020, respectively. In February 2021, it opened in Japan, Kim said.

When asked regarding the next foreign market location, “Danggeun Market will not designate a particular country this time. We will change our overseas penetration strategy slightly by opening the app Karrot globally and monitor the countries that show organic growth and then we will narrow down specific countries and cities to focus on more,” Kim said.

The company will still seek the high population density areas in foreign markets and keep the distance limit set, Danggeun’s unique feature that only shows people listings from sellers located within 6 km radius in South Korea and 10 miles (about 15 km) maximum for the U.K. for providing hyperlocalized community service.

For the next round, Gary Kim said it depends on its global expansion growth. If its global business works well and Karrot draws more global users and reaches active MAU and transactions the company has set, Danggeun Market will definitely raise another funding in two years, Kim said. “We are not in a hurry for an IPO at this stage since we can raise enough capital in the private market now. We want to consider going public after we make stable profits,” Kim said.

Danggeun Market now claims its total registered users exceed 21 million (South Korea has a total of 20.92 million households) and has consistently experienced over 300 % year-on-year growth since 2018.

The company reached 1.8 million monthly active users (MAUs) in 2019, 4.8 million MAUs in 2020 and finally increased to 14.2 million MAUs in 2021, growing 3x every year over the past three years. According to global app analytics platform App Annie, Danggeun Market users spend an average of two hours and two minutes per month on the app.

“Over the past few years, Danggeun Market has demonstrated overwhelming dominance in the Korean C2C market… with unique user behavior from location-based communities, Danggeun Market continues to showcase its potential as the hyperlocal super app,” managing partner at DST Investment Management John Lindfors said.

“COVID-19 highlighted the importance of people wanting to connect to their neighbors and community. When meeting a friend for a simple coffee can no longer be taken for granted, we realize all the more importance of our relationships and community. Danggeun Market’s service bridges the offline and online world, enhancing both in-person interactions as well as purely digital ones. The core of Danggeun Market’s growth is its digital end-to-end platform that allows consumers to feel both genuinely part of their communities as well as have the comfort and safety of being part of a larger network that can grow together,” co-founder and managing partner at Goodwater Capital Eric Kim said.

Powered by WPeMatico

Reserve Trust, a Denver-based financial services provider, has raised $30.5 million in a Series A round led by QED Investors.

FinTech Collective, Ardent Venture Partners, Flywire CEO Mike Massaro and Quovo founder and CEO Lowell Putnam also participated in the financing, which included $17.9 million in secondary shares. It brings the startup’s total raised since its 2016 inception to $35.5 million.

Reserve Trust describes itself as “the first fintech trust company with a Federal Reserve master account.” What does that mean exactly? Basically, a federal reserve master account allows Reserve Trust to move dollars on behalf of its customers directly, via wire and ACH payment rails, without an intermediate or partner bank.

Historically, only banks were able to access these payment rails directly, which left both domestic and international fintechs “with limited partner options, poor technology and slow implementations when it came to embedding high-value B2B payments,” says COO Dave Cahill. Reserve Trust touts that its technology and services give companies all over the world the ability to “seamlessly move money via the first cloud-based payment system connected directly to the Federal Reserve” since it is not limited by legacy banking systems.

Image Credits: CEO Dave Wright and COO Dave Cahill / Reserve Trust

In conjunction with the fundraise, Reserve Trust is also announcing that Dave Wright has been named CEO and Cahill joined as COO. The pair worked together previously at SolidFire, a flash storage startup that Wright founded and sold to NetApp for $870 million in 2016.

Reserve Trust works with businesses that seek to embed domestic and cross-border B2B payment by offering them the ability to store funds in custody accounts that are backed by its Federal Reserve master account.

The history of the company relates back to the global financial crisis. After the crisis, banks in the U.S. went through a process called derisking, which meant they shed businesses that on a risk return basis weren’t as strong as other businesses. One of those included the handling of U.S. dollar payments, particularly in emerging countries.

“One of the consequences of this is that it became significantly more difficult and expensive for businesses and smaller economies to trade and move U.S. dollars around the world,” Wright told TechCrunch. “And the founders of Reserve Trust saw this opportunity to build a new type of financial institution that was focused on helping to provide U.S. dollar payment services, especially to emerging fintechs in markets around the world, and helping to reconnect those economies to global trade.”

But rather than start a bank, the founders (Dennis Gingold, Justin Guilder) navigated a previously unexplored part of regulatory waters to create a state-chartered trust company with a Federal Reserve master account.

“That’s something that had never really been done before,” Wright added. “Pretty much every other trust company has to work through banks for all their payment services. Reserve Trust is the first that has actually managed to get a Federal Reserve master account and can process payments directly with the Federal Reserve.”

The complex process took about three years, and in 2018, the company got a Federal Reserve master account and started providing U.S. dollar custody and payment services for fintechs all over the world. Reserve Trust began to see strong demand from payment and fintech companies that were struggling to develop strong partner bank relationships, even though fundamentally there wasn’t any reason the banks couldn’t work with them.

“They found working with banks to be a slow process, one that didn’t involve a lot of technology expertise on the side of the banks, and it was really inhibiting their ability to develop their technology,” Wright said. And that was even here in the U.S. Today, more than half of its business is from domestic fintechs, although Reserve Trust still has a strong international presence as well.

The new funds will mainly go toward helping the company scale to handle what Wright describes as “a fairly overwhelming amount of demand” and toward building out the team, the technology and the services it needs to address the payment needs of larger, faster growing fintechs around the world.

“Most of our customers today are small and midsize fintechs, but now we’re seeing demand for much larger fintechs that have much higher payment volumes and are involved in embedded banking and B2B payments,” Wright said. “They are looking for a stronger banking partner than what they’ve been able to find among the role of traditional banks.” Customers include Unlimint and VertoFX, among others.

QED Investors partner Amias Gerety and FinTech Collective principal Matt Levinson are bullish both on Reserve Trust’s history and its potential.

The pair point to payments giant Stripe as an example of how far Reserve Trust can go.

“Stripe has significant market share doing merchant acquiring and processing e-commerce payments for the consumer,” Levinson said. “B2B payments is significantly bigger in terms of volume, so we’re talking about well over $20 trillion of addressable payment flow. But there’s no real technology company that’s brought the modern payments platform to market without being beholden to legacy banks. And that’s why we’re so excited about this business.”

Reserve Trust, he added, is giving businesses a way to facilitate B2B payments that “are smarter, faster and cheaper.”

Gerety agrees.

“Despite all the excitement around digital payments and infrastructure, there is still no fintech that can offer direct integration with the U.S. payment system,” he said. “With Reserve Trust, we are creating foundational infrastructure to hold and move payments globally and at scale.”

Powered by WPeMatico

On Sunday Square announced it was gobbling up Afterpay in a deal worth $29 billion at the time of announcement. Alex followed up yesterday with more details on why the deal made sense for Square and Afterpay over here, but we wanted to ask some notable VCs what it means for the startup market.

For context, the Square deal follows a ton of money and interest flowing into the BNPL market. Just this year, VCs have invested in companies like Alma ($59.4 million, January 2021), Scalapay ($48 million, January 2021), Wisetack ($19 million, February 2021), Zilch ($80 million, April 2021) and Dividio ($30 million, June 2021).

Most of the investors we reached out to were generally bullish on the Square and Afterpay integration, but they were less excited about opportunities for other consumer BNPL businesses to emerge.

Then there’s Klarna, which raised $639 million at a post-money valuation of $45.6 billion in June, after raising $1 billion in March at a post-money valuation of $31 billion.

There’s also interest from some major public companies. After a slow start, PayPal is aggressively pushing BNPL services with merchants that offer it as a payment option. And there are reports that Apple is building its own BNPL offering through Apple Pay.

We reached out to Commerce Ventures founder and GP Dan Rosen, Better Tomorrow Ventures founding partner Jake Gibson, Fika Ventures partner TX Zhuo, and Matthew Harris of Bain Capital Ventures to see what they thought of the deal, as well as what it might mean for the opportunity for other BNPL companies and startups.

The main takeaways? “Buy now, pay later” may be effective at driving retail conversion, but scale matters and long-term margins look slim for BNPL startups.

Now, let’s hear from the venture community.

Why is the BNPL market so hot?

Powered by WPeMatico

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

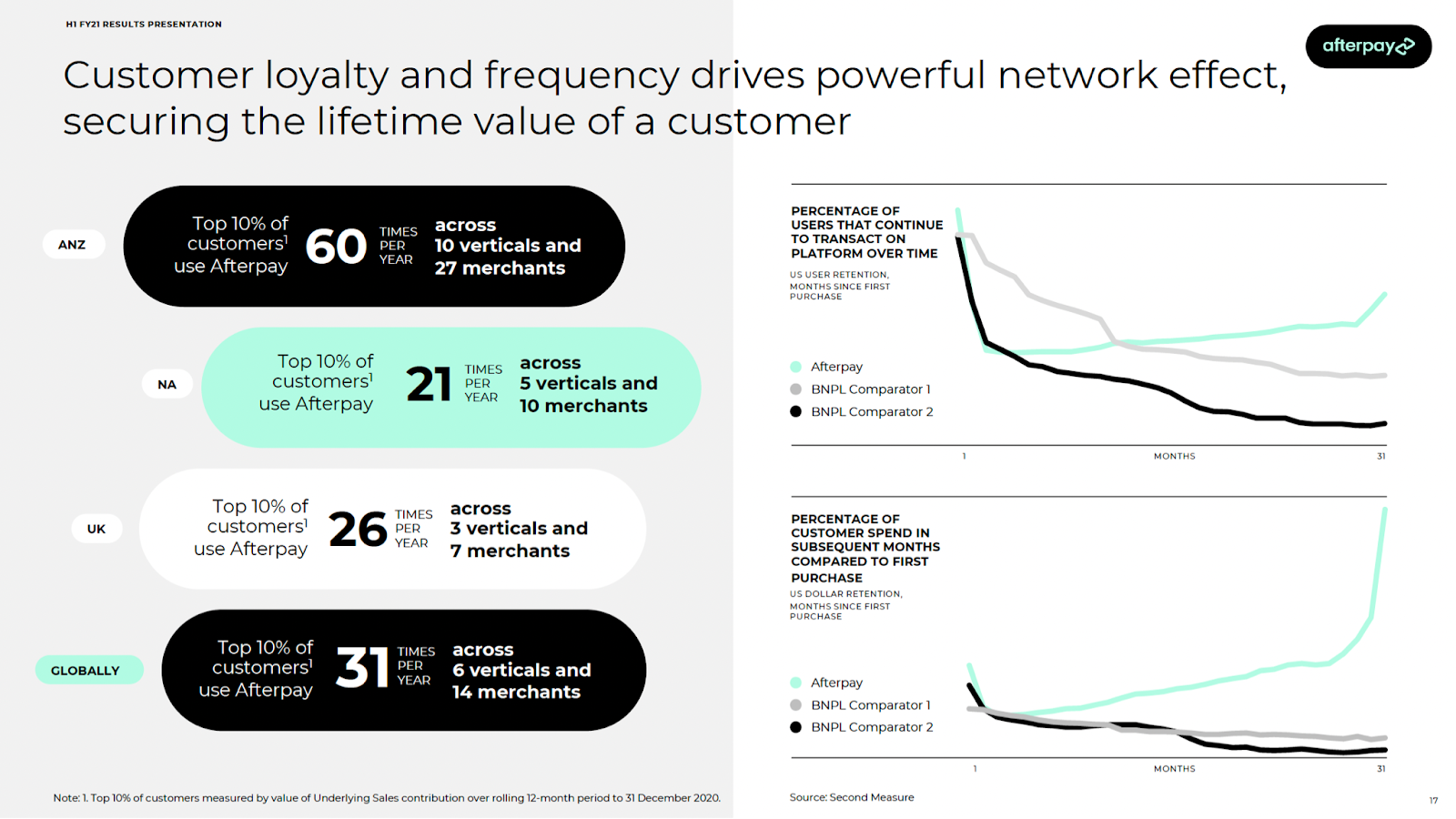

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

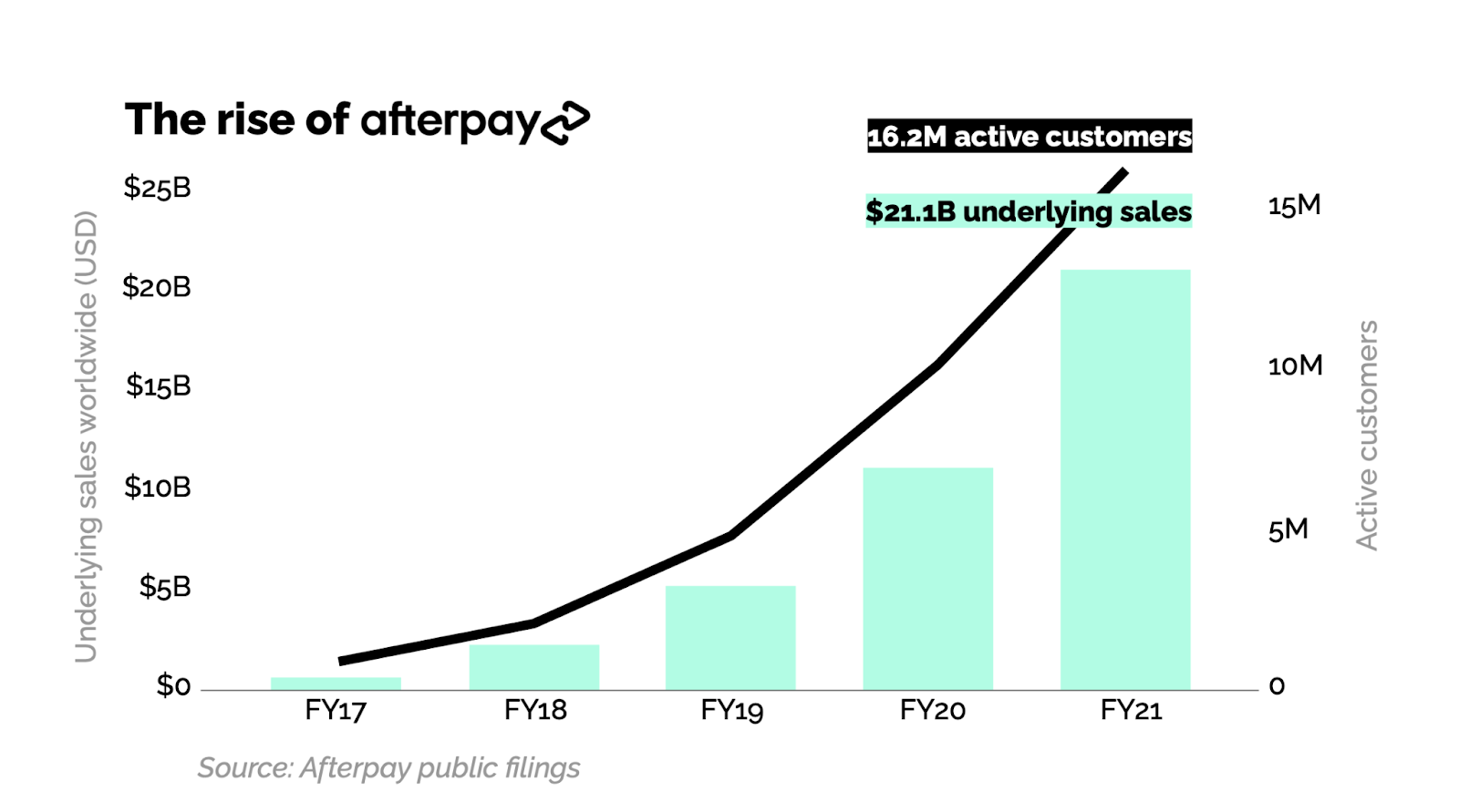

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

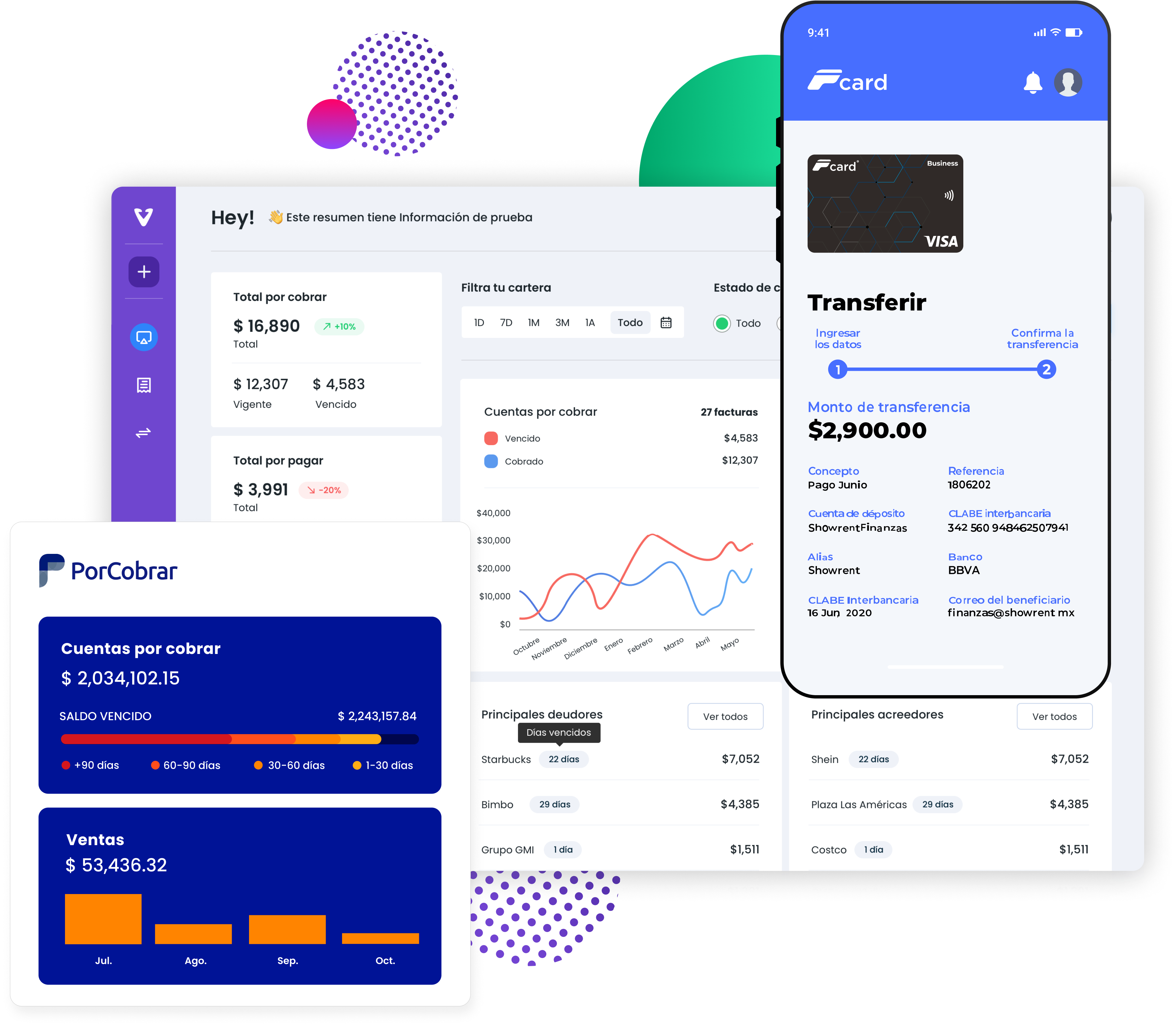

It’s no secret that the technology for easy business-to-business payments has not yet caught up to its peer-to-peer counterparts, but Yaydoo thinks it has the answer.

The Mexico City-based B2B software and payments company provides three products, VendorPlace, P-Card and PorCobrar, for managing cash flow, optimizing access to smart liquidity, and connecting small, midsize and large businesses to an ecosystem of digital tools.

Sergio Almaguer, Guillermo Treviño and Roberto Flores founded Yaydoo — the name combines “yay” and “do” to show the happiness of doing something — in 2017. Today, the company announced the close of a $20.4 million Series A round co-led by Base10 Partners and monashees.

Joining them in the round were SoftBank’s Latin America Fund and Leap Global Partners. In total, Yaydoo has raised $21.5 million, Almaguer told TechCrunch.

Prior to starting the company, Almaguer was working at another company in Mexico doing point-of-sale. His large enterprise customers wanted automation for their payments, but he noticed that the same tools were too expensive for small businesses.

The co-founders started Yaydoo to provide procurement, accounts payable and accounts receivables, but in a simpler format so that the collection and payment of B2B transactions was affordable for small businesses.

Image Credits: Yaydoo

The idea is taking off, and vendors are adding their own customers so that they are all part of the network to better link invoices to purchase orders and then connect to accounts payable, Almaguer said. Yaydoo estimates that the automation workflows reduced 80% of time wasted paying vendors, on average.

Yaydoo is joining a sector of fintech that is heating up — the global B2B payments market is valued at $120 trillion annually. Last week, B2B payments platform Nium announced a $200 million in Series D funding on a $1 billion valuation. Others attracting funding recently include Paystand, which raised $50 million in Series C funding to make B2B payments cashless, while Dwolla raised $21 million for its API that allows companies to build and facilitate fast payments.

The new funding will enable the company to attract new hires in Mexico and when the company expands into other Latin American countries. Yaydoo is also looking at future opportunities for its working capital business, like understanding how many invoices customers are setting, the access to actual payments, and how money flows out and in so that it can provide insights on working capital funding gaps. The company will also invest in product development.

The company has grown to over 800 customers, up from 200 in the first quarter of 2020. Its headcount also grew to 100 from 30 during the same time. In the last 12 months, over 70,000 companies have transacted on the Yaydoo network, and total payment volume grew to hundreds of millions of dollars.

Yaydoo is a SaaS subscription model, but the new funding will also enable the company to create a pool of potential customers with a “freemium” offering with the goal of converting those customers into the subscription model as they grow, Almaguer said.

Rexhi Dollaku, partner at Base10 Partners, said the firm saw the way B2B payments were becoming modernized and “was impressed” by the Yaydoo team and how it built a complicated infrastructure, but made it easy to use.

He believes Latin America is 10 years behind in terms of B2B payments but will catch up sooner than later because of the digital transformation going on in the region.

“We are starting to see early signs of the network being built out of the payments product, and that is a good indication,” Dollaku said. “With the funding, Yaydoo will be also able to provide more financial services options for businesses to address a working fund gap.”

Powered by WPeMatico

Business-to-business payments platform Nium announced Monday that it raised more than $200 million in Series D funding and saw its valuation rise above $1 billion.

The company, now Singapore-based but shifting to the Bay Area, touted the investment as making it “the first B2B payments unicorn from Southeast Asia.”

Riverwood Capital led the round, in which Temasek, Visa, Vertex Ventures, Atinum Capital, Beacon Venture Capital and Rocket Capital Investment participated, along with a group of angel investors like DoorDash’s Gokul Rajaram, FIS’ Vicky Bindra and Tribe Capital’s Arjun Sethi. Including the new funding, Nium has raised $300 million to date, Prajit Nanu, co-founder and CEO, told TechCrunch.

The B2B payments sector is already hot, yet underpenetrated, according to some experts. To give an idea just how hot, Nium was seeking $150 million for its Series D round, received commitments of $300 million from eager investors and settled on $200 million, Nanu said.

“This is our fourth or fifth fundraise, but we have never had this kind of interest before — we even had our term sheets in five days,” he added. “I believe this interest is because we’ve successfully managed to create a global platform that is heavily regulated, which gives us access to a lot of networks. This is an environment where payment is visible, and our core is powering frictionless commerce and enabling anyone to use our platform.”

Nium’s new round adds fuel to a fire shared by a number of companies all going after a global B2B payments market valued at $120 trillion annually: last week, Paystand raised $50 million in Series C funding to make B2B payments cashless, while Dwolla raised $21 million for its API that allows companies to build and facilitate fast payments. In March, Higo brought in $3.3 million to do the same in Latin America, while Balance, developing a B2B payments platform that allows merchants to offer a variety of payment methods. raised $5.5 million in February.

Nium’s approach is to provide access to a global payment infrastructure, including card issuance, accounts receivable and payable, and banking-as-a-service through a single API. The company’s network enables customers to then send funds to more than 100 countries, pay out in more than 60 currencies, accept funds in seven currencies and issue cards in more than 40 countries, Nanu said. The company also boasts money transfer, card issuances and banking licenses in 11 jurisdictions.

Francisco Alvarez-Demalde, co-founding partner and managing partner at Riverwood, said in an email that the combination of software — plus regulatory licenses — and operating a fintech infrastructure platform on behalf of neobanks and corporates is a global trend experiencing hyper-growth.

Riverwood followed Nium for many years, and its future vision was what got the firm interested in being a part of this round. Alvarez-Demalde said that “Nium has the incredible combination of a great market opportunity, a talented founder and team, and we believe the company is poised for global growth based on underlying secular technology trends like increasing real-time payment capabilities and the proliferation of cross border commerce.

“As a central payment infrastructure in one API, Nium is a catalyst that unlocks cross-border payments, local accounts and card issuance with a network of local market licenses, partners and banking relationships to facilitate moving money across the world,” he added. “Enterprises of all types are embedding financial services as part of their consumer experience, and Nium is a key global enabler of this trend.”

Nanu said the new funding enables the company to move to the United States, which represents 3% of Nium’s revenue. He wants to increase that to 20% over the next 18 months, as well as expand in Latin America. The investment also gives the company a 12- to 18-month runway for further M&A activity. In June, Nium acquired virtual card issuance company Ixaris, and in July acquired Wirecard Forex India to expose it to India’s market. He also plans to expand the company’s payments network infrastructure, invest in product development and add to Nium’s 700-person headcount.

Nium already counts hundreds of enterprise companies as clients and plans to onboard thousands more in the next year. The company processes $8 billion in payments annually and has issued more than 30 million virtual cards since 2015. Meanwhile, revenue grew by over 280% year over year.

All of this growth puts the company on a trajectory for an initial public offering, Nanu said. He has already spoken to people who will help the company formally kick off that journey in the first quarter of 2022.

“Unlike other companies that raise money for new products, we aim to expand in the existing sets of what we do,” Nanu said. “The U.S. is a new market, but we have a good brand and will use the new round to provide a better experience to the customer.”

Powered by WPeMatico

Sila announced Monday it raised $13 million in Series A funding for its banking and payment platform that gives software teams tools to build the next generation of financial products and services.

Revolution Ventures led the round and was joined by existing investors Madrona Venture Group, Oregon Venture Fund and Mucker Capital, as well as Wise co-founder Taavet Hinrikus. The funding brings the total investment to date for Portland, Oregon-based Sila to $20 million.

The company was founded in 2018 by Shamir Karkal, Angela Angelovska, Isaac Hines and Alex Lipton to simplify digital payments and storage in a regulatory compliant way and build on blockchain technology. CEO Karkal has a long history in the fintech space, co-founding Simple, an app unifying various accounts into one accessible bank card, in 2009. It was acquired by BBVA in 2014 for $117 million and shuttered earlier this year.

Karkal told TechCrunch that the idea for Sila was born out of frustration while starting another bank. He saw a need for financial application development, but was hindered by a banking system “still stuck in the 20th century.” He thought consumers expected a different level of service, which is why many flock to fintechs.

However, whenever a business tried to connect existing banking systems, fintechs and cryptocurrency innovators, as it built and scale, would always run into technology and compliance issues, Karkal said.

“The problem with working with banks, is that you have to figure out how to integrate with their mainframe,” he added. “In the process, you end up having to also be compliance experts just to be able to do it.”

Whereas it took Karkal three years to get bank processes set up for other companies, it took Sila 18 months. Its banking APIs enable developers to create their own digital wallets, replacing the need to integrate with legacy financial institutions. Sila also has partnerships with fintech platforms, including Plaid, Alloy, Lithic and Arcus to move money, and is backed by Evolve Bank and Trust.

Sila can now get customers up-and-running in six to eight weeks. And unlike competitors that focus almost exclusively on e-commerce, most of Sila’s customers are doing regulated payments within the fintech, insurtech, commercial real estate and cryptocurrency spaces that tend to be more complex from a compliance basis, Karkal said.

Since the company launched its platform, business was building steadily, and took off in the second half of 2020. The company raised a $7.7 million seed round earlier in the year. In the last 12 months, Sila grew its revenue 10 times and customers’ end users grew over 500% in the last seven months.

Sila will use the new funding to increase headcount, target additional partners and expand product features, including its Ethereum MainNet stablecoin issuance and interoperability between FedWire and the Nacha Automated Clearing House network.

“There is a massive wave of fintechs emerging in the U.S., and we have barely scratched the surface,” Karkal said. “Places like India, Africa and Latin America could accelerate at the same time because they are mainly starting from zero. We are here to ‘arm the rebels’ and help those innovators build applications to give all end users a much better financial experience.”

As part of the investment, Clara Sieg, partner at Revolution Ventures, is joining the company’s board. She told TechCrunch she met the company’s co-founders through the Portland ecosystem.

Revolution tends to look at fintech startups from a consumer angle. Recognizing that the problem with building infrastructure meant dealing with banks, the firm set out how to find a company building the pipes to solve it, she said.

In the landscape of fintech, she considers Dwolla to be a competitor to Sila. Last week, the company raised $21 million to continue developing its API that allows companies to build and facilitate fast payments, specifically with a focus on ACH. However, it comes down to actually signing up customers, and that competitive landscape is pretty thin, Sieg added.

“Sila is building an easy way for people to program money and taking a regulatory eye to things,” Sieg said. “When Shamir was building Simple, he could see how challenging it was for incumbents to provide the tools developers need to embed financial services, and this is why we have confidence in his ability to win.”

Powered by WPeMatico

Paystone, a payments and integrated software company, secured another strategic investment this year, this time $23.8 million ($30 million CAD) from Crédit Mutuel Equity, the private equity arm of Crédit Mutuel Alliance Fédérale.

The Canada-based company got its start in 2008 as the payment processing company Zomaron, and rebranded itself as Paystone in 2019. Today it provides electronic payments and customer engagement technology to businesses, particularly those that provide services, CEO Tarique Al-Ansari told TechCrunch.

“Paystone is on a mission to help businesses grow, and we were enthralled by their commitment to that mission and their focus on service-oriented verticals,” said Léa Perge, investor at Crédit Mutuel Equity in Canada, via email.

While most of the company’s peers focus on product companies, Al-Ansari saw how underserved the service side was: their needs are different, and unlike retail, aren’t looking to sell online. Rather, they need an online presence and digital marketing to engage with customers, but their focus is being findable and having content that tells people why they should do business with them.

Paystone provides the marketing through content, help with reviews and with loyalty and rewards programs. However, rather than reward for spending, Paystone rewards for behavior. Refer a friend, get a reward. Write a review, get a reward. Al-Ansari calls it “payments as a benefit.” Referrals and reviews are how businesses become more findable, and the more content that’s out there, the more it helps people consider the business trustworthy, he added.

The new funding gives Canada-based Paystone total funds raised in 2021 of $78.8 million in a mix of debt and equity. It raised $54.9 million in January, funds that were barely touched as of yet, Al-Ansari said.

Though he wasn’t actively seeking new funds, Al-Ansari had been speaking with Crédit Mutuel Equity, which used to be CIC Capital Canada, prior to the pandemic, and their deal was put on hold.

Crédit Mutuel Equity came back with similar interest, and taking into account the kind of talent Paystone wanted to go after and its acquisition strategy — the company has already acquired five companies — Al-Ansari decided to take the additional funds. He said it gives the company options to hire more and double down on building the company, as well as enough capital to look for more acquisitions.

This year, Paystone entered the U.S. market for the first time and will do a proper launch later this year. The company has over 30,000 merchant locations on its platform throughout North America, and Al-Ansari expects that to grow by 5,000 this year. The company has 150 employees currently, and another 50 are expected to come on board by the end of the year.

In addition, Al-Ansari expects growth to accelerate for the rest of the year. The company processes around $6 billion in credit card payments and is on track to bring in $55.7 million in revenue this year. It is cash flow positive, residuals from the company’s origins of being bootstrapped, he said.

“We want to become the go-to destination for service businesses to set up a digital presence to accept payments and provide loyalty and rewards,” Al-Ansari said. “We will do this by solidifying our market position and growing our platform with the tools that customers want.”

Powered by WPeMatico