payments

Auto Added by WPeMatico

Auto Added by WPeMatico

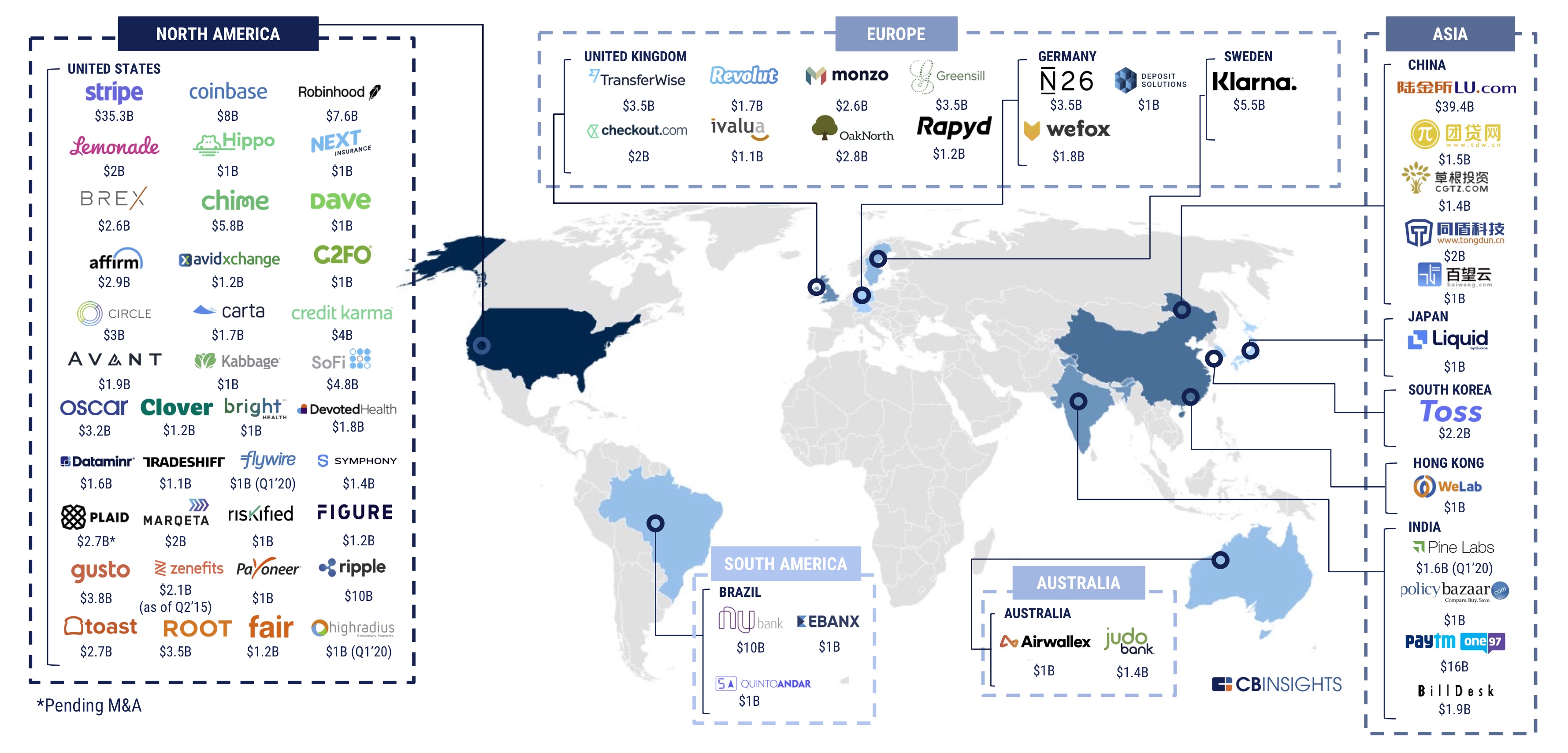

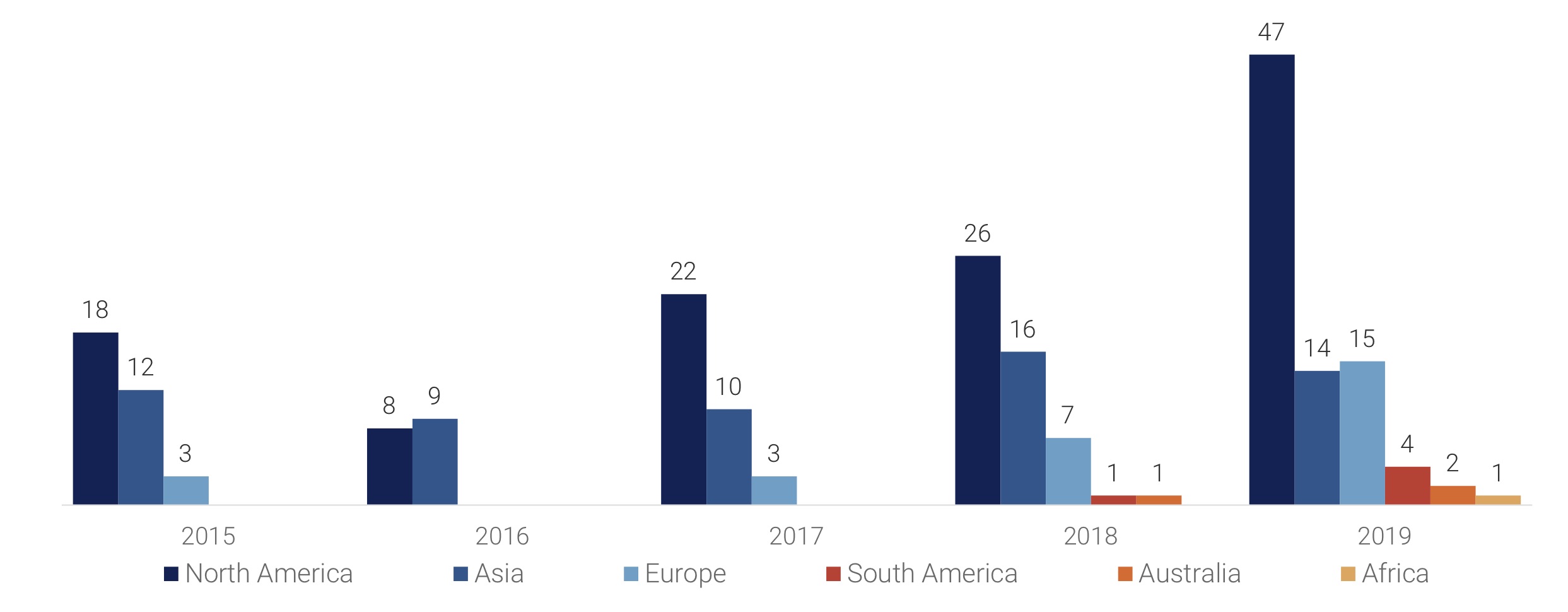

Financial services startups raised less money in 2019 than they did in 2018 as VC firms looked to back late stage firms and focused on developing markets, a new report has revealed.

According to research firm CB Insights’ annual report published this week, fintech startups across the world raised $33.9 billion* in total last year across 1,912 deals*, down from $40.8 billion they picked up by participating in 2,049 deals the year before.

It’s a comprehensive report, which we recommend you read in full here (your email is required to access it), but below are some of the key takeaways.

Early-stage deals dropped to a 12-quarter low as deal share globally shifts to mid- and late-stages (CB Insights)

The fintech market globally today has 67 unicorns as of earlier this month (CB Insights)

2019 saw 83 mega-rounds totaling $17.2B, a record year in every market except Europe

*CB Insights report includes a $666 million financing round of Paytm . It was incorrectly reported by some news outlets and the $666 million raise was part of the $1 billion round the Indian startup had revealed weeks prior. We have adjusted the data accordingly.

Powered by WPeMatico

After eBay, Visa, Stripe and other high-profile partners ditched the Facebook -backed cryptocurrency collective, Libra scored a win today with the addition of Shopify. The e-commerce platform will become a member of Libra Association, contributing at least $10 million and operating a node that processes transactions for the Facebook-originated stable coin.

If Libra manages to assuage international regulators’ concerns, which are currently blocking its roll out, Shopify could gain a way to process transactions without paying credit card fees. Libra is designed to move between wallets with zero or nearly-zero fees. That could save money for Shopify and the 1 million merchants running online shops on its platform.

Shopify stressed that helping merchants reduce fees and bringing commerce opportunities to developing nations as reasons it’s joining the Libra Association . “Much of the world’s financial infrastructure was not built to handle the scale and needs of internet commerce,” Shopify writes. Here are the most critical parts of its announcement:

Our mission is to make commerce better for everyone and to do that, we spend a lot of our time thinking about how to make commerce better in parts of the world where money and banking could be far better . . . As a member of the Libra Association, we will work collectively to build a payment network that makes money easier to access and supports merchants and consumers everywhere . . . Our mission has always been to support the entrepreneurial journey of the more than one million merchants on our platform. That means advocating for transparent fees and easy access to capital, and ensuring the security and privacy of our merchants’ customer data. We want to create an infrastructure that empowers more entrepreneurs around the world.

As part of the Libra Association, Shopify will become a validator node operator, gain one vote on the Libra Association council and can earn dividends from interest earned on the Libra reserve in proportion to its investment, which is $10 million at a minimum.

The Libra Association had lost much of its e-commerce expertise when a string of members abandoned the project in October amidst regulatory scrutiny. That included traditional payment processors like Visa and Mastercard, online processors like Stripe and PayPal and marketplaces like eBay. That threw into question whether Libra would have the right partners to make the cryptocurrency accepted in enough places to be useful to people.

As it works to convince regulators Libra is safe, Facebook has been working on its other payment plays, including Facebook Pay and WhatsApp Pay, that rely on traditional bank transfers or credit cards.

Shopify’s CEO Tobi Lutke tweeted that “Shopify spends a lot of time thinking about how to make commerce better in parts of the world where money and banking could be far better. That’s why we decided to become a member of the Libra Association.”

“We are proud to welcome Shopify, Inc. (SHOP) to the Libra Association. As a multinational commerce platform with over one million businesses in approximately 175 countries, Shopify, Inc. brings a wealth of knowledge and expertise to the Libra project,” writes Dante Disparte, the Libra Association’s head of Policy and Communications. “Shopify joins an active group of Libra Association members committed to achieving a safe, transparent, and consumer-friendly implementation of a global payment system that breaks down financial barriers for billions of people.”

A recent hire further tied the two companies together. Facebook’s former lead product manager for its payment platform and billing teams, Kaz Nejatian, in September became Shopify’s VP and GM of money.

Operating an e-commerce store can be difficult or impossible without a traditional bank account that can be tough to attain in some developing countries. Libra could allow these merchants to establish a Libra Wallet where payments are sent instantly, without steep credit card fees, and in theory could be cashed out at local brick-and-mortar establishments or ATMs for local fiat currency.

Shopify’s credit card readers

But for any of that to happen, the Libra Association will have to convince the U.S. government, the EU and more that it won’t help terrorists launder money, hurt people’s privacy or weaken nations’ power in the global financial system. “The French Finance Minister Bruno Le Maire said, “the monetary sovereignty of countries is at stake from a possible privatisation of money . . . we cannot authorise the development of Libra on European soil.”

Libra was initially slated to launch in 2020. We’ll see.

—

Here’s the full list of Libra Association members:

Current

Facebook’s Calibra, Shopify, PayU, Farfetch, Lyft, Spotify, Uber, Illiad SA, Anchorage, Bison Trails, Coinbase, Xapo, Andreessen Horowitz, Union Square Ventures, Breakthrough Initiatives, Ribbit Capital, Thrive Capital, Creative Destruction Lab, Kiva, Mercy Corps, Women’s World Banking.

Former members

Vodafone, Visa, Mastercard, Stripe, PayPal, Mercado Pago, Bookings Holdings, eBay.

Powered by WPeMatico

Remember when Zenefits imploded, and kicked out CEO Parker Conrad. Well, Conrad launched a new employee onboarding startup called Rippling, and now he’s going after another HR company called Gusto with a new billboard, “Outgrowing Gusto? Presto change-o.”

The problem is, Gusto got it taken down by issuing a cease & desist order to Rippling and the billboard operator Clear Channel Outdoor. That’s despite the law typically allowing comparative advertising as long as it’s accurate. Gusto sells HR, benefits and payroll software, while Rippling does the same but adds in IT management to tie together an employee identity platform.

Rippling tells me that outgrowing Gusto is the top reasons customers say they’re switching to Rippling. Gusto’s customer stories page lists no customers larger than 61 customers, and Enlyft research says the company is most often used by 10 to 50-person staffs. “We were one of Gusto’s largest customers when we left the platform last year. They were very open about the fact that the product didn’t work for businesses of our size. We moved to Rippling last fall and have been extremely happy with it,” says Compass Coffee co-founder Michael Haft.

That all suggests the Rippling ad’s claim is reasonable. But the C&D claims that “Gusto counts as customers multiple companies with 100 or more employees and does not state the businesses will ‘outgrow’ their platfrom at a certain size.”

In an email to staff provided to TechCrunch, Rippling CMO Matt Epstein wrote, “We take legal claims seriously, but this one doesn’t pass the laugh test. As Gusto says all over their website, they focus on small businesses.”

So rather than taking Gusto to court or trying to change Clear Channel’s mind, Conrad and Rippling did something cheeky. They responded to the cease & desist order in Shakespeare-style iambic pentameter.

Our billboard struck a nerve, it seems. And so you phoned your legal teams,

who started shouting, “Cease!” “Desist!” and other threats too long to list.Your brand is known for being chill. So this just seems like overkill.

But since you think we’ve been unfair, we’d really like to clear the air.

Rippling’s general counsel Vanessa Wu wrote the letter, which goes on to claim that “When Gusto tried to scale itself, we saw what you took off the shelf. Your software fell a little short. You needed Workday for support,” asserting that Gusto’s own HR tool couldn’t handle its 1,000-plus employees and needed to turn to a bigger enterprise vendor. The letter concludes with the implication that Gusto should drop the cease-and-desist, and instead compete on merit:

So Gusto, do not fear our sign. Our mission and our goals align.

Let’s keep this conflict dignified—and let the customers decide.

Rippling CMO Matt Epstein tells me that “While the folks across the street may find competition upsetting, customers win when companies push each other to do better. We hope our lighthearted poem gets this debate back down to earth, and we look forward to competing in the marketplace.”

Rippling might think this whole thing was slick or funny, but it comes off a bit lame and try-hard. These are far from 8 Mile-worthy battle rhymes. If it really wanted to let customers decide, it could have just accepted the C&D and moved on…or not run the billboard at all. It still has four others that don’t slam competitors running. That said, Gusto does look petty trying to block the billboard and hide that it’s unequipped to support massive teams.

We reached out to Gusto over the weekend and again today asking for comment, whether it will drop the C&D, if it’s trying to get Rippling’s bus ads dropped too and if it does in fact use Workday internally.

[Update 2pm Pacific: Gusto’s PR representative Paul Loeffler claims that “This is common business practice in maintaining a brand”, says that for Gusto “A core, but not exclusive focus, are small businesses”, and admits that “as Gusto itself has grown to become a large-scale company, we have different needs than many of our customers and transitioned to Workday.”

Finally, he declares that “We’re excited to see more companies create new solutions that make it easier for businesses to take care of and support their teams” despite theatening to sue one that was. If Gusto itself grew out of Gusto, an ad asking if its customers are too seems wholly accurate.]

Given Gusto has raised $516 million — 10X what Rippling has — you’d think it could just outspend Rippling on advertising or invest in building the enterprise HR tools so customers really couldn’t outgrow it. They’re both Y Combinator companies with Kleiner Perkins as a major investor (conflict of interest?), so perhaps they can still bury the hatchet.

At least they found a way to make the HR industry interesting for an afternoon.

Powered by WPeMatico

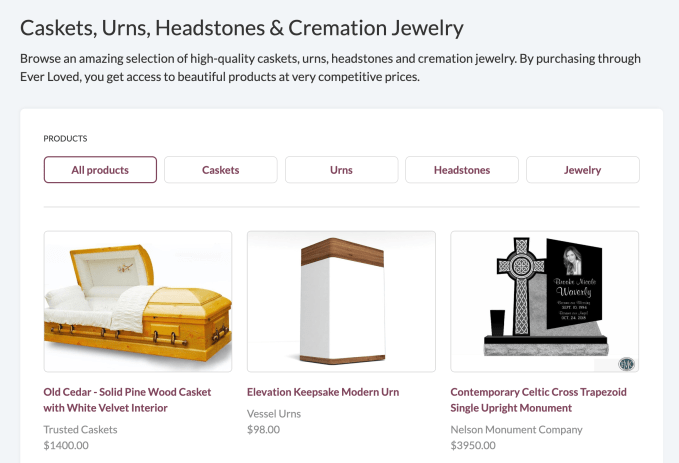

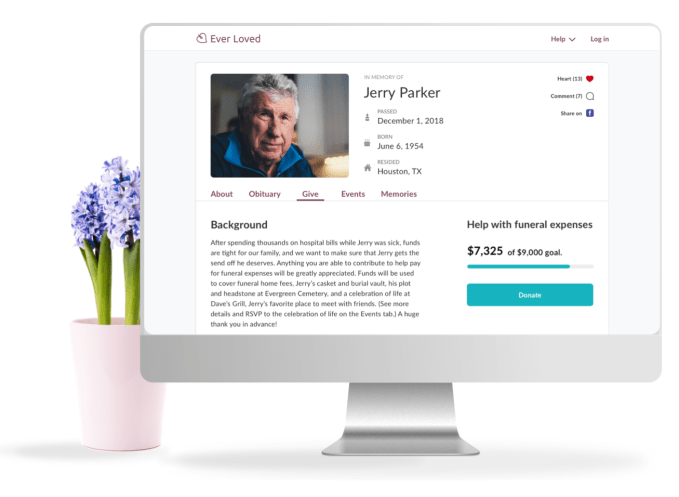

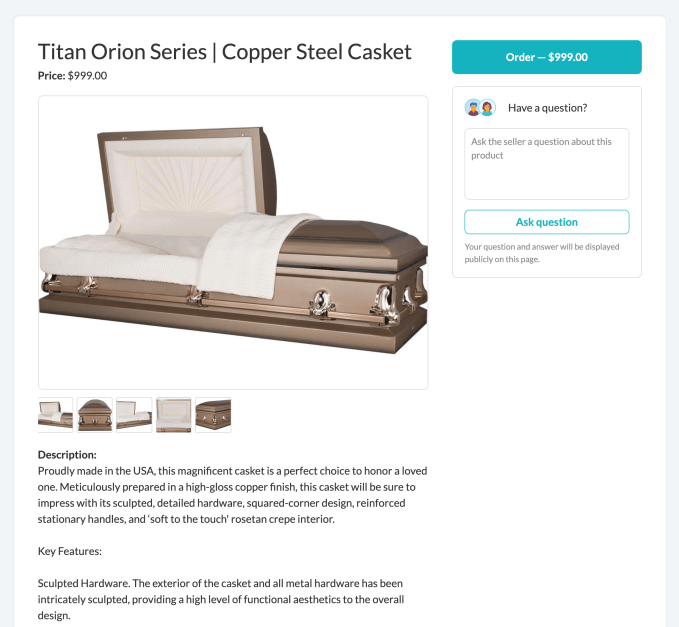

Fifty percent of families are scared they can’t cover the cost of a funeral. They end up overpaying because no one wants to comparison shop amidst a tragedy. That’s why ex-Googler Alison Johnston’s startup Ever Loved built a free funeral crowdfunding tool. Now it’s addressing one of the most expensive parts of saying goodbye: burial. Today Ever Loved launches its online marketplace for caskets, urns, headstones and memorial jewelry.

By sidestepping the overhead of a physical funeral home, Ever Loved can offer better prices while still earning a 10% margin. Its caskets cost 50% less than the average sold at a mortuary, according to the National Funeral Directors Association.

When I called a local San Francisco funeral home, the high markups came into focus. They quoted me $2,795 for a casket sold for $1,200 on Ever Loved.

“Most people don’t think to — or don’t want to — plan funerals in advance, which means that when someone passes away, the family is often scrambling,” Johnston tells me. “When this rush to make decisions is paired with extreme grief, many people don’t do anywhere close to the same amount of research as they would with another several-thousand-dollar purchase. When combined with the fact that most funeral homes don’t publish their prices online, it’s easy for families to spend much more than they need to.”

Johnston co-founded Ever Loved in late 2017 after a family member was diagnosed with terminal cancer. She discovered how few resources there were available for helping people plan and pay for funerals. She’d previously worked at Q&A app Aardvark through its acquisition by Google, then started online tutoring startup InstaEDU that eventually sold to Chegg. The consumer website building and e-commerce tools she’d grown used to weren’t available in the funeral industry, so she set out to build them. Ever Loved has raised seed funding from Social Capital and gone through Y Combinator.

Ever Loved co-founder and CEO Alison Johnston

“Tech too often merely makes life and work easier for those who already have it good,” she told me last year. “Tech that tempers tragedy is a welcome evolution for Silicon Valley.”

Ever Loved’s first focus was its funeral crowdfunding tool that let families ask the decedent’s loved ones to help contribute to offset the costs. Donors could leave a tip for Ever Loved, but otherwise it charged nothing beyond credit card processing fees. The tool was paired with a memorial website builder that families could use for distributing invites and collecting memories. Now Ever Loved is helping people plan thousands of funerals per month with revenue up nearly 20X year-over-year.

Now that it’s helping families raise money for remembrance services, Ever Loved wants to make sure they don’t get ripped off. The fact that there’s such low pricing transparency at funeral homes should clue you in that they try to pass off steep markups since customers might not have the energy to keep looking. “The average funeral home only helps with a funeral once every three days, meaning that many funeral homes need to charge high prices in order to cover their own fixed costs,” Johnston explains.

Remove the overhead costs and assist customers across geographies and there’s room for a strong business with more affordable prices. For example, a Stanford Blue Casket costs $990 on Ever Loved while one LA funeral home charges $1,600. The Last Supper Pieta Casket is $1,500 on Ever Loved but $6,580 from the funeral home. That funeral home had both of these listed under different names, further hindering the ability of customers to find a fair price.

Ever Loved can also more quickly adapt to the diversification of burial options. Between concerns about costs, land use, environmental impact and connection to family and nature, many are looking beyond caskets. Cremation became more popular than burial in the U.S. in 2017. Liquid cremation is now legal in 18 states, and Washington just began allowing body composting.

“We’re seeing a lot of independent providers popping up to do everything from turning your loved one’s ashes into a diamond ring to shooting their ashes into space to planting them under a tree in the forest,” says Johnston. Any single funeral home is unlikely to offer the breadth customers are looking for. “Our goal is to make all of your options available to you in an easily digestible format.”

Ever Loved’s business is protected by the FTC’s Funeral Rule that bars mortuaries from refusing or charging extra to handle a casket or urn purchased elsewhere. That means Ever Loved customers can combine shopping online with in-person memorial services from a local funeral home. Still, it’s a tough business. Startups like HaloLife, Clarity and After I Go have all shut down. Most others merely offer memorial sites, or funeral home search engines.

That means Ever Loved’s biggest competitors, beyond the standard just accepting the local mortuary’s prices, are Google and Amazon. Often they surface the same prices as Ever Loved with comparable shipping, though Google could sometimes find a slight discount by buying straight from the manufacturer, while Amazon was missing some top brands. Costco and Walmart sell funeral products too. But Johnston says “many people don’t feel like generic, mass-market stores are the appropriate place to purchase funeral products.” I agree it might feel disrespectful buying an urn from the same place you get toilet paper.

“We also put a huge focus on customer service, which you don’t get at Walmart, Costco or Amazon,” Johnston tells me. “When you’re grieving and spending thousands of dollars, we’ve found that this is very important.”

As the demographic planning funerals gets more tech-savvy over time and want personalized farewells rather than cookie-cutter conclusions, there’s a chance to change the status quo. Discussing death is becoming less taboo. Being smart about paying for it should too.

Powered by WPeMatico

Increasingly, the streets of Karachi and Lahore are being flooded with men riding bikes and wearing green T-shirts, a writer friend recently told me. In a sense, these men represent the emergence of Pakistan’s tech startups.

India now has more than 25,000 startups and raised a record $14.5 billion last year, according to government figures. But not all Asian countries are as large as India or have such a thriving startup ecosystem. Long overdue, things are beginning to change in bordering Pakistan.

Bykea, a three-year-old ride-hailing and delivery service, today has more than 500,000 bikes registered on its platform. It operates in some of Pakistan’s most populated cities, such as Karachi, Lahore and Islamabad, Muneeb Maayr, Bykea founder and CEO, told TechCrunch.

Maayr is one of the most recognized startup founders in Pakistan, and previously worked for Rocket Internet, helping the giant run fashion e-commerce platform Daraz in the country. While leading Daraz, he expanded the platform to cater to categories beyond fashion; Daraz was later sold to Alibaba.

Powered by WPeMatico

“We’re trying to shift cryptocurrency from this speculative asset class to driving real-world utility,” Coinbase CEO Brian Armstrong tells me. How? Through commerce and micropayments. But now Coinbase has the who to build it. Today the startup announced it has hired away former head of Product for Indian e-commerce giant Flipkart and Google Shopping VP of Product Surojit Chatterjee to become Coinbase’s chief product officer.

“I’ve always enjoyed being associated with technology that is on the brink of changing how we live” writes Chatterjee. “Google ads has helped democratize commerce, Flipkart and ecommerce has revolutionized life in India, and I believe Coinbase is going to turn conventional finance on its head.”

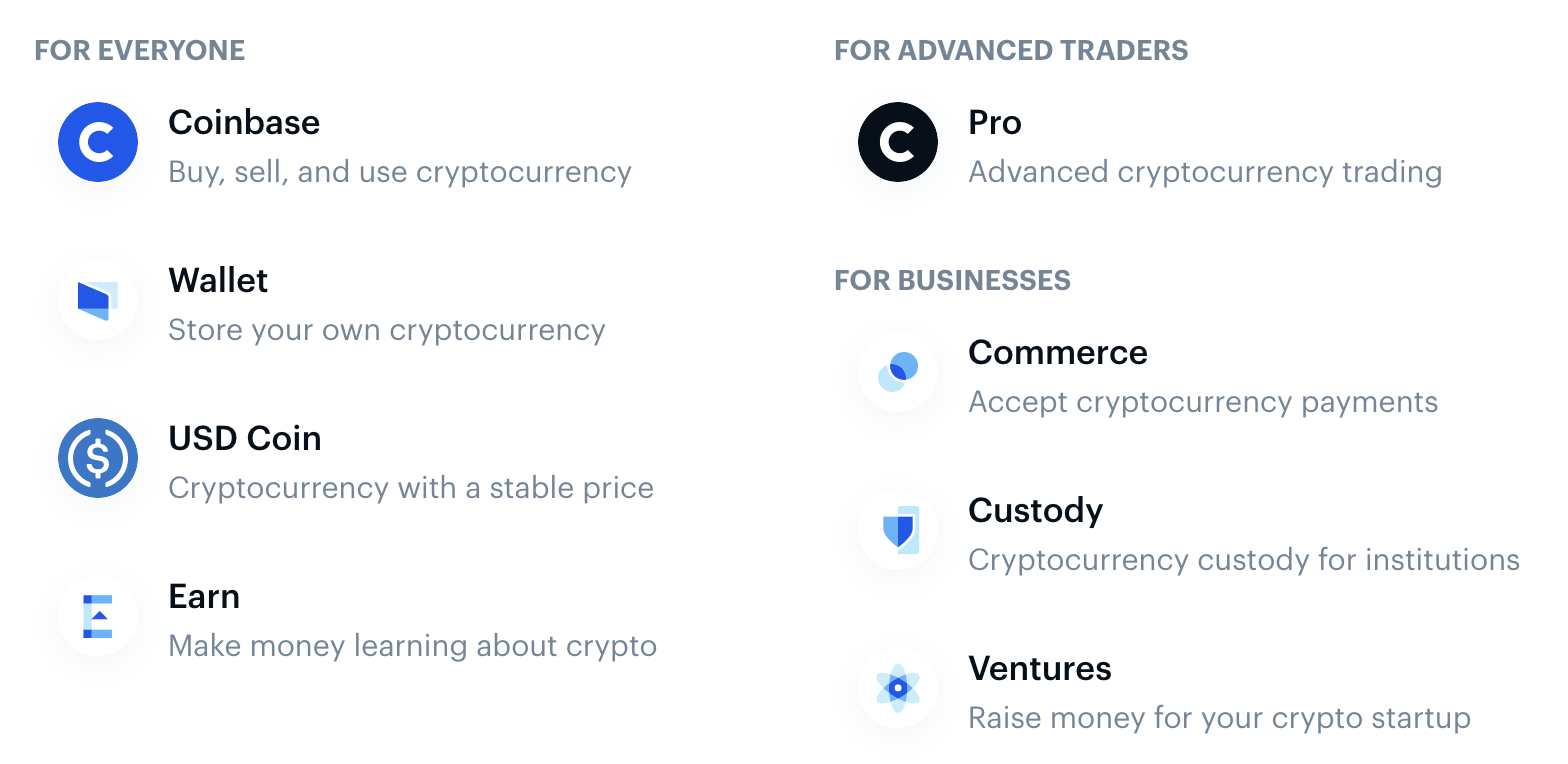

Chatterjee spent more than 11 years at Google over two stints, the first as a founding member of Google’s mobile search Ads product that’s grown to tens of billions in revenue per year. When he starts at Coinbase next week, Armstrong tells me he’ll help Coinbase organize its complex array of products, including its cryptocurrency exchange, wallet, stablecoin, incentivized crypto education platform Earn and Coinbase Commerce that lets businesses take payments in Bitcoin, Ethereum and more. Chatterjee replaces Jeremy Henrickson, the former Coinbase CPO who departed in December 2018.

“Surojit is a huge asset here because we’re a product-led company,” Armstrong says. “We have different leaders and they increasingly have responsibilities around P&L. Having one really experienced chief product officer that can mentor them and teach them to own revenues and budgets — really in the model of Google — that will professionalize Coinbase.”

One opportunity Armstrong hopes Chatterjee can help Coinbase seize on is building products for emerging markets where financial infrastructure is weak. “E-commerce is not equally distributed around the world. Micropayments don’t work that well … Him spending time living in India, a developing market, he deeply understands mobile money.” Given the explosion of phone-based payments, the demonetization and the prevalence of cash on delivery methods in India that Flipkart dealt with, “his background is kind of ideal from that worldly perspective,” Armstrong explains.

Chatterjee cites his upbringing as inspiration to deliver “economic freedom for everyone,” as Armstrong says is Coinbase’s mission. “Growing up in India in a poor middle-class household, I saw very closely what a lack of liquid cash does to a family’s lifestyle,” Chatterjee recalls.

“As a kid I would go with my mom to a local bank to withdraw money. And believe me when I tell you that the process was epic!” It included withdrawal slips, tokens and anxiously trying to match current signatures to versions decades old. When India demonetized and made everyone exchange their cash, “My dad, who was almost 80 at that time, stood in a queue for five hours to get 2000 Rs, which was the per-day limit for the first week. That’s less than $30!” Digital money could ensure people always have access to everything they own.

Surojit Chatterjee (far right) rides along for a Flipkart delivery to understand the consumer commerce experience

In developed countries, Armstrong sees a chance for Chatterjee to enable digital content creators to turn their passion into their profession. “There’s lots of people who lurk on Reddit or Stack Overflow and answer questions … If there was real money on these things, these could be their full time jobs — contributing content on user-generated social sites,” Armstrong predicts. “I think you’d see a lot more contributions, as well.”

Now might be the perfect time to hire Chatterjee since we’re in a lull period for cryptocurrency in the wake of the rush at the end of 2018. “Crypto is always challenging to navigate. In these periods when it’s relatively quiet, we tend to do really well,” Armstrong says. The company grew market share, volume and app installs versus competitors between 50% and 100%, according to the CEO. Referencing ancient war strategy, Armstrong concludes that, “There’s years where you just want to train the soldiers and stockpile resources and you’re basically just preparing. We’re building the company, not just responding to crazy hype.”

Powered by WPeMatico

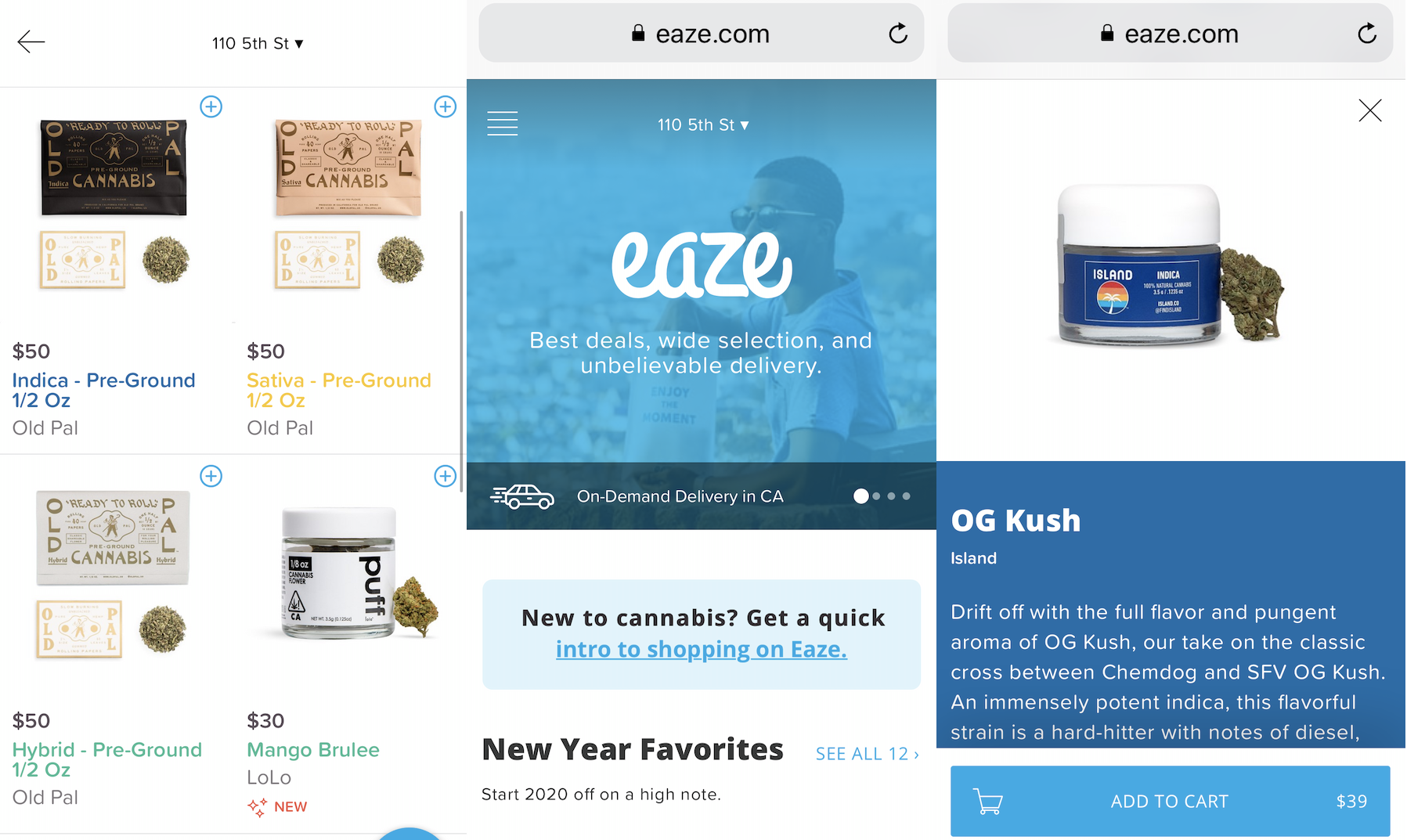

The first cannabis startup to raise big money in Silicon Valley is in danger of burning out. TechCrunch has learned that pot delivery middleman Eaze has seen unannounced layoffs, and its depleted cash reserves threaten its ability to make payroll or settle its AWS bill. Eaze was forced to raise a bridge round to keep the lights on as it prepares to attempt major pivot to ‘touching the plant’ by selling its own marijuana brands through its own depots.

TechCrunch spoke with nine sources with knowledge of Eaze’s struggles to piece together this report. If Eaze fails, it could highlight serious growing pains amid the ‘green rush’ of startups into the marijuana business.

Eaze, the startup backed by some $166 million in funding that once positioned itself as the “Uber of pot” — a marketplace selling pot and other cannabis products from dispensaries and delivering it to customers — has recently closed a $15 million bridge round, according to multiple source. The funding was meant to keep the lights on as Eaze struggles to raise its next round of funding amid problems with making decent margins on its current business model, lawsuits, payment processing issues, and internal disorganization.

An Eaze spokesperson confirmed that the company is low on cash. Sources tell us that the company, which laid off some 30 people last summer, is preparing another round of cuts in the meantime. The spokesperson refused to discuss personnel issues but noted that there have been layoffs at many late stage startups as investors want to see companies cut costs and become more efficient.

From what we understand, Eaze is currently trying to raise a $35 million Series D round according to its pitch deck. The $15 million bridge round came from unnamed current investors. (Previous backers of the company include 500 Startups, DCM Ventures, Slow Ventures, Great Oaks, FJ Labs, the Winklevoss brothers, and a number of others.) Originally, Eaze had tried to raise a $50 million Series D, but the investor that was looking at the deal, Athos Capital, is said to have walked away at the eleventh hour.

Eaze is going into the fundraising with an enterprise value of $388 million, according to company documents reviewed by TechCrunch. It’s not clear what valuation it’s aiming for in the next round.

An Eaze spokesperson declined to discuss fundraising efforts but told TechCrunch, “The company is going through a very important transition right now, moving to becoming a plant-touching company through acquisitions of former retail partners that will hopefully allow us to more efficiently run the business and continue to provide good service to customers.

The news comes as Eaze is hoping to pull off a “verticalization” pivot, moving beyond online storefront and delivery of third-party products (rolled joints, flower, vaping products and edibles) and into sourcing, branding and dispensing the product directly. Instead of just moving other company’s marijuana brands between third-party dispensaries and customers, it wants to sell its own in-house brands through its own delivery depots to earn a higher margin. With a number of other cannabis companies struggling, the hope is that it will be able to acquire brands in areas like marijuana flower, pre-rolled joints, vaporizer cartridges, or edibles at low prices.

An Eaze spokesperson confirmed that the company plans to announce the pivot in the coming days, telling TechCrunch that it’s “a pretty significant change from provider of services to operating in that fashion but also operating a depot directly ourselves.”

The startup is already making moves in this direction, and is in the process of acquiring some of the assets of a bankrupt cannabis business out of Canada called Dionymed — which had initially been a partner of Eaze’s, then became a competitor, and then sued it over payment disputes, before finally selling part of its business. These assets are said to include Oakland dispensary Hometown Heart, which it acquired in an all-share transaction (“Eaze effectively bought the lawsuit,” is how one source described the sale). This will become Eaze’s first owned delivery depot.

In a recent presentation deck that Eaze has been using when pitching to investors — which has been obtained by TechCrunch — the company describes itself as the largest direct-to-consumer cannabis retailer in California. It has completed more than 5 million deliveries, served 600,000 customers and tallied up an average transaction value of $85.

To date, Eaze has only expanded to one other state beyond California, Oregon. Its aim is to add five more states this year, and another three in 2021. But the company appears to have expected more states to legalize recreational marijuana sooner, which would have provided geographic expansion. Eaze seems to have overextended itself too early in hopes of capturing market share as soon as it became available.

An employee at the company tells us that on a good day Eaze can bring in between $800,000 and $1 million in net revenue, which sounds great, except that this is total merchandise value, before any cuts to suppliers and others are made. Eaze makes only a fraction of that amount, one reason why it’s now looking to verticatlize into more of a primary role in the ecosystem. And that’s before considering all of the costs associated with running the business.

Eaze is suffering from a problem rampant in the marijuana industry: a lack of working capital. Since banks often won’t issue working capital loans to weed-related business, deliverers like Eaze can experience delays in paying back vendors. Another source says late payments have pushed some brands to stop selling through Eaze.

Another drain on its finances have been its marketing efforts. A source said out-of-home ads (billboards and the like) allegedly were a significant expense at one point. It has to compete with other pot purchasing options like visiting retail stores in person, using dispensaries’ in-house delivery services, or buying via startups like Meadow that act as aggregated online points of sale for multiple dispensaries.

Indeed, Eaze claims that its pivot into verticalization will bring it $204 million in revenues on gross transactions of $300 million. It notes in the presentation that it makes $9.04 on an average sale of $85, which will go up to $18.31 if it successfully brings in ‘private label’ products and has more depot control.

The poor margins are only one of the problems with Eaze’s current business model, which the company admits in its presentation have led to an inconsistent customer experience and poor customer affinity with its brand — especially in the face of competition from a number of other delivery businesses.

Playing on the on-demand, delivery-of-everything theme, it connected with two customer bases. First, existing cannabis consumers already using some form of delivery service for their supply; and a newer, more mainstream audience with disposable income that had become more interested in cannabis-related products but might feel less comfortable walking into a dispensary, or buying from a black market dealer.

It is not the only startup that has been chasing that audience. Other competitors in the wider market for cannabis discovery, distribution and sales include Weedmaps, Puffy, Blackbird, Chill (a brand from Dionymed that it founded after ending its earlier relationship with Eaze), and Meadow, with the wider industry estimated to be worth some $11.9 billion in 2018 and projected to grow to $63 billion by 2025.

Eaze was founded on the premise that the gradual decriminalisation of pot — first making it legal to buy for medicinal use, and gradually for recreational use — would spread across the US and make the consumption of cannabis-related products much more ubiquitous, presenting a big opportunity for Eaze and other startups like it.

It found a willing audience among consumers, but also tech workers in the Bay Area, a tight market for recruitment.

“I was excited for the opportunity to join the cannabis industry,” one source said. “It has for the most part has gotten a bad rap, and I saw Eaze’s mission as a noble thing, and the team seemed like good people.”

Eaze CEO Ro Choy

That impression was not to last. The company, this employee was told when joining, had plenty of funding with more on the way. The newer funding never materialised, and as Eaze sought to figure out the best way forward, the company cycled through different ideas and leadership: former Yammer executive Keith McCarty, who cofounded the company with Roie Edery (both are now founders at another Cannabis startup, Wayv), left, and the CEO role was given to another ex-Yammer executive, Jim Patterson, who was then replaced by Ro Choy, who is the current CEO.

“I personally lost trust in the ability to execute on some of the vision once I got there,” the ex-employee said. “I thought that on one hand a picture was painted that wasn’t the truth. As we got closer and as I’d been there longer and we had issues with funding, the story around why we were having issues kept changing.” Several sources familiar with its business performance and culture referred to Eaze as a “shitshow”.

The quick shifts in strategy were a recurring pattern that started well before the company got tight financial straits.

One employee recalled an acquisition Eaze made several years ago of a startup called Push for Pizza. Founded by five young friends in Brooklyn, Push for Pizza had gone viral over a simple concept: you set up your favourite pizza order in the app, and when you want it, you pushed a single button to order it. (Does that sound silly? Don’t forget, this was also the era of Yo, which was either a low point for innovation, or a high point for cynicism when it came to average consumer intelligence… maybe both.)

Eaze’s idea, the employee said, was to take the basics of Push for Pizza and turn it into a weed app, Push for Kush. In it, customers could craft their favourite mix and, at the touch of a button, order it, lowering the procurement barrier even more.

The company was very excited about the deal and the prospect of the new app. They planned a big campaign to spread the word, and held an internal event to excite staff about the new app and business line.

“They had even made a movie of some kind that they showed us, featuring a caricature of Jim” — the CEO at a the time — “hanging out of the sunroof of a limo.” (I’ve been able to find the opening segment of this video online, and the Twitter and Instagram accounts that had been created for Push for Kush, but no more than that.)

Then just one week later, the whole plan was scrapped, and the founders of Push for Pizza fired. “It was just brushed under the carpet,” the former employee said. “No one could get anything out of management about what had happened.”

Something had happened, though: the company had been taking payments by card when it made the acquisition, but the process was never stable and by then it had recently gone back to the cash-only model. Push for Kush by cash was less appealing. “They didn’t think it would work,” the person said, adding that this was the normal course of business at the startup. “Big initiatives would just die in favor of pushing out whatever new thing was on the product team’s radar.”

Eaze’s spokesperson confirmed that “we did acquire Push For Pizza . . but ultimately didn’t choose to pursue [launching Push For Kush].”

Payments were a recurring issue for the startup. Eaze started out taking payments only in cash — but as the business grew, that became increasingly problematic. The company found itself kicked off the credit card networks and was stuck with a less traceable, more open to error (and theft) cash-only model at a time when one employee estimated it was bringing in between $800,000 and $1 million per day in sales.

Eventually, it moved to cards, but not smoothly: Visa specifically did not want Eaze on its platform. Eaze found a workaround, employees say, but it was never above board, which became the subject of the lawsuit between Eaze and Dionymed. Currently the company appear to only take payments via debit cards, ACH transfer, and cash, not credit card.

Another incident sheds light on how the company viewed and handled security issues.

At one point, employees allegedly discovered that Eaze was essentially storing all of its customer data — including users’ signatures and other personal information — in an Azure bucket that was not secured, meaning that if anyone was nosing around, it could be easily discovered and exploited.

The vulnerability was brought to the company’s attention. It was something that was up to product to fix, but the job was pushed down the list. It ultimately took seven months to patch this up. “I just kept seeing things with all these huge holes in them, just not ready for prime time,” one ex-employee said of the state of products. “No one was listening to engineers, and no one seemed to be looking for viable products.” Eaze’s spokesperson confirms a vulnerability was discovered but claims it was promptly resolved.

Today, the issue is a more pressing financial one: the company is running out of money. Employees have been told the company may not make its next payroll, and AWS will shut down its servers in two days if it doesn’t pay up.

Eaze’s spokesperson tried to remain optimistic while admitting the dire situation the company faces. “Eaze is going to continue doing everything we can to support customers and the overall legal cannabis industry. We’re excited about the future and acknowledge the challenges that the entire community is facing.”

As medicinal and recreational marijuana access became legal in some states in the latter 2010s, entrepreneurs and investors flocked to the market. They saw an opportunity to capitalize on the end of a major prohibition — a once in a lifetime event. But high government taxes, enduring black markets, intense competition, and a lack of financial infrastructure willing to deal with any legal haziness have caused major setbacks.

While the pot business might sound chill, operations like Eaze depend on coordinating high-stress logistics with thin margins and little room for error. Plenty of food delivery startups from Sprig to Munchery went under after running into similar struggles, and at least banks and payment processors would work with them. With the odds stacked against it, Eaze has a tough road ahead.

Powered by WPeMatico

PayU is acquiring a controlling stake in fintech startup PaySense at a valuation of $185 million and plans to merge it with its credit business LazyPay as the nation’s largest payments processor aggressively expands its financial services offering.

The Prosus-owned payments giant said on Friday that it will pump $200 million — $65 million of which is being immediately invested — into the new enterprise in the form of equity capital over the next two years. PaySense, which employs about 240 people, has served more than 5.5 million consumers to date, a top executive said.

Prior to today’s announcement, PaySense had raised about $25.6 million from Nexus Venture Partners, and Jungle Ventures, among others. PayU became an investor in the five-year-old startup’s Series B financing round in 2018. Regulatory filings show that PaySense was valued at about $48.7 million then.

The merger will help PayU solidify its presence in the credit business and become one of the largest players, said Siddhartha Jajodia, global head of Credit at PayU, in an interview with TechCrunch. “It’s the largest merger of its kind in India,” he said. The combined entity is valued at $300 million, he said.

PaySense enables consumers to secure long-term credit for financing their new vehicle purchases and other expenses. Some of its offerings overlap with those of LazyPay, which primarily focuses on providing short-term credit to consumers to facilitate orders on food delivery platforms, e-commerce websites and other services. Its credit ranges between $210 and $7,030.

Cumulatively, the two services have disbursed more than $280 million in credit to consumers, said Jajodia. He aims to take this to “a couple of billion dollars” in the next five years.

PaySense’s Prashanth Ranganathan and PayU’s Siddhartha Jajodia pose for a picture

As part of the deal, PaySense and LazyPay will build a common and shared technology infrastructure. But at least for the immediate future, LazyPay and PaySense will continue to be offered as separate services to consumers, explained Prashanth Ranganathan, founder and chief executive of PaySense, in an interview with TechCrunch.

“Over time, as the businesses get closer, we will make a call if a consolidation of brands is required. But for now, we will let consumers direct us,” added Ranganathan, who will serve as the chief executive of the combined entity.

There are about a billion debit cards in circulation in India today, but only about 20 million people have a credit card. (The official government figures show that about 50 million credit cards are active in India, but many individuals tend to have more than one card.)

This has meant that most Indians don’t have a traditional credit score, so they can’t secure loans and a range of other financial services from banks. Scores of startups in India today are attempting to address this opportunity by using other signals and alternative data of users — such as the kind of a smartphone a person has — to evaluate whether they are worthy of being granted some credit.

Digital lending is a $1 trillion opportunity (PDF) over the next four and a half years in India, according to estimates from Boston Consulting Group.

PayU’s Jajodia said PaySense and LazyPay will likely explore building new offerings, such as credit for small and medium businesses. He did not rule out the possibility of getting stakes in more fintech startups in the future. PayU has already invested north of half a billion dollars in its India business. Last year, it acquired Wibmo for $70 million.

“At PayU, our ambition is to build financial services using data and technology. Our first two legs have been payments [processing] and credit. We will continue to scale both of these businesses. Even this acquisition was about getting new capabilities and a strong management team. If we find more companies with some unique assets, we may look at them,” he said.

PayU leads the payments processing market in India. It competes with Bangalore-based RazorPay. In recent years, RazorPay has expanded to serve small businesses and enterprises. In November, it launched corporate credit cards and other services to strengthen its neo banking play.

Powered by WPeMatico

Two years ago, we created the Matrix FinTech Index to highlight what we saw as the beginnings of a 10+ year mega innovation wave in financial services.

The trillion-dollar financial services industry was going to be turned on its head over the next decade, and we were just getting started. At the time, the top 10 publicly traded U.S. fintech companies had just surpassed the $100 billion mark in terms of total market capitalization, 12 unicorns had emerged in the category, and the U.S. VC industry had just poured in $6.7B — a record at the time.

As we predicted last year, the innovation cycle continues, and we are transitioning into its mid-phase. So what happened in U.S. fintech in 2019? In short, monster growth.

On the public side, fintechs delivered resoundingly. PayPal alone gained $26B in market capitalization. On a return basis, the public Matrix FinTech Index continued to crush every major equity index as well as the financial services incumbents. Nicely matching our forecasts, our Index delivered 213% returns over the last three years. The Index outperformed the financial services incumbents by 151 percentage points and the S&P 500 by 170 percentage points.

Powered by WPeMatico

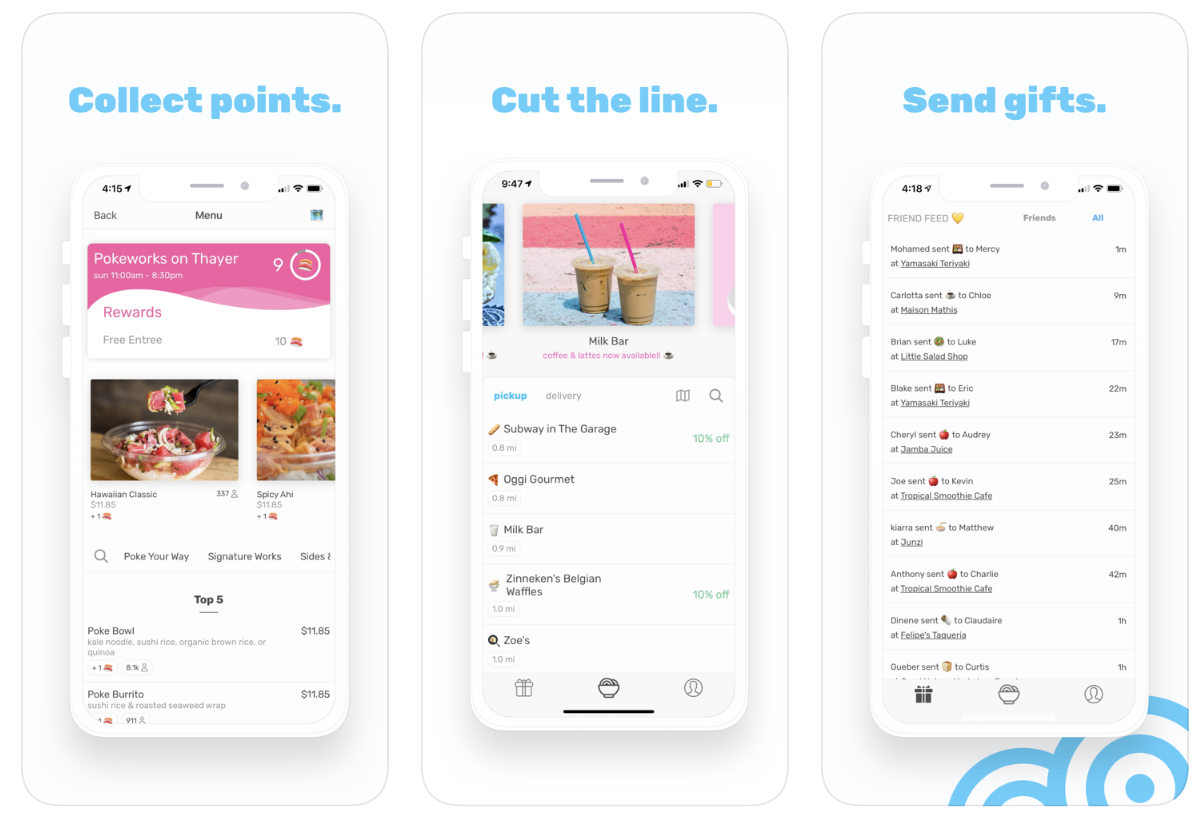

“We were in the back washing blenders so they could keep taking Snackpass orders,” recalls co-founder and CEO Kevin Tan. The team from order-ahead food startup Snackpass was willing to get their hands dirty to keep up with demand at one of their first restaurant partners, Tropical Smoothie Cafe on the Yale University campus.

Why were people so eager to pay for takeout through Snackpass? Because it lets them earn loyalty points to redeem for free food — both for themselves and as gifts for their friends. Sending people Snackpass rewards became a new way to flirt or show gratitude at Yale. And through the Venmo-esque Snackpass social feed, users could keep up with a fresh form of gossip while discovering restaurants.

“Anywhere someone is standing in line to order something, we can solve that with Snackpass,” says Tan. “Consumer spending will be social in the future.”

That future is already taking hold. Two years after launch, Snackpass is on 11 college campuses across the U.S., often boasting a 75% penetration rate amongst students within six months. It takes a cut of every order and keeps margins high because users pick up the food themselves rather than waiting for delivery. While other food ordering startups battle to offer discounts as marauding users deal-hop between apps, Snackpass keeps users coming back through its loyalty program.

Its momentum, retention and opportunity to expand from colleges to dense cities has now won Snackpass a $21 million Series A led by Andreessen Horowitz partner Andrew Chen. The round was joined by other heavy hitters, like Y Combinator, General Catalyst, Inspired Capital and First Round, plus angels, including musician Nas, NFL star Larry Fitzgerald and legendary talent agent Michael Ovitz. Building on Snackpass’ $2.7 million seed, the cash will go toward hiring up with the goal of reaching 100 campuses in two years.

Its momentum, retention and opportunity to expand from colleges to dense cities has now won Snackpass a $21 million Series A led by Andreessen Horowitz partner Andrew Chen. The round was joined by other heavy hitters, like Y Combinator, General Catalyst, Inspired Capital and First Round, plus angels, including musician Nas, NFL star Larry Fitzgerald and legendary talent agent Michael Ovitz. Building on Snackpass’ $2.7 million seed, the cash will go toward hiring up with the goal of reaching 100 campuses in two years.

“Takeout is an important market because it’s huge — also in the hundreds of billions — and fragmented,” writes Chen. “The opportunity complements the food delivery market in a big way: For the average restaurant, there are 6 takeout orders for every delivery order!”

Like many of the best startup ideas, Snackpass was born out of the founders’ own needs at Yale. Slow and expensive food delivery services didn’t make sense for smaller orders like a coffee, ice cream or a pepperoni slice on campuses small enough for customers to walk or bike to the restaurant. Tan says, “I was dabbling in several side projects, including helping a friend who managed a local pizza shop build a website to help better reach the local student community.” He realized how tough it was for restaurants around colleges to retain and reward customers, especially as regulars graduated.

Tan joined up with neuroscience student and Thiel Fellow Jamie Marshall, who became Snackpass’ COO. “I had grown up calling in every order,” Marshall tells me. “Waiting in line didn’t make sense for me. I used every order-ahead platform and thought this was the future.” Jonathan Cameron, a serial entrepreneur who’d built his own order-ahead app called Happy Hour, rounded out the founding team.

Snackpass founders (from left): Jamie Marshall and Kevin Tan

Snackpass offers users a list of nearby restaurants from which they can order ahead, with special tags for ones offering deals. Menu items include counts of how many people have ordered them and how many rewards points you’ll earn buying them. You pay in the app, skip the line at the restaurant and grab your order from the counter. Each restaurant can configure their own rewards system with how much items earn and cost, such as giving you a free coffee for every 10 you buy.

Users can then spend their points to get themselves free menu items, or send a virtual Snackpass gift card to any of their phone contacts or people they find via search. This gives Snackpass a way to grow virally that most food apps lack. Thankfully, you can block people on Snackpass if they get creepy showering you with gifts.

Each purchase and gift on Snackpass shows up in its social feed unless you make it private. “That’s become its own language. People use it to flirt with each other, or bond and connect with someone new,” Tan tells me. “There’s some drama or intrigue there seeing who’s sending gifts to who. People even look at the feed in the way they look at someone’s Instagram to see what’s going on with them.”

Snackpass has also done some integration work specifically for the college market that sets it apart from other order-ahead and delivery services. It can sync with students’ campus meal plans so they can spend them through the app. And student groups from clubs to fraternities can pre-load and replenish accounts for their members. Snackpass works with the same organizations to launch on new campuses. “We host parties, sponsor tailgates and make it feel like a student-led effort so it grows organically across campus communities,” Tan explains. “These efforts, combined with the social feed which would give anyone FOMO if they’re not in the app.”

With all the competition in the space, restaurants can be inundated with apps to manage, some of which just exacerbate spikes in demand that overwhelm kitchens. “There is certainly a risk that local restaurants will start to get platform fatigue, finding that using some apps will take too big of a bite out of their margins,” says Tan. That’s why Snackpass built features that let restaurants batch orders and control how many come in at a certain time so dine-in patients and non-app users aren’t stuck with unreasonable delays.

With all the competition in the space, restaurants can be inundated with apps to manage, some of which just exacerbate spikes in demand that overwhelm kitchens. “There is certainly a risk that local restaurants will start to get platform fatigue, finding that using some apps will take too big of a bite out of their margins,” says Tan. That’s why Snackpass built features that let restaurants batch orders and control how many come in at a certain time so dine-in patients and non-app users aren’t stuck with unreasonable delays.

Snackpass has recruited talent from Uber Eats and an advisor from Yelp’s executive team to help it navigate the tricky SMB sales process. One ace up its sleeve is that it can offer to send push notifications to announce recently signed partners or specials they’re launching, driving the new customers restaurants are desperate for. Tan says his startup is considering if it could charge for this kind of promotion down the line. Most customers who walk into restaurants are effectively in incognito mode, but Snackpass provides its partners with analytics to help them improve their own businesses.

“At the surface level there is a lot of competition in this space,” Tan admits. “The social aspect of the app has been the key differentiator for us. Other companies have been focused on creating the fastest, cheapest, most efficient delivery service, but it’s really hard to make those margins work and consumers are trained to shop around on different apps to get the best deal or fastest delivery time . . . Eating food is supposed to be fun and social, and our generation grew up online and in social networks. We’re combining the social aspect of eating with the utility of order ahead, which has helped us build loyalty and enable retention amongst our users.”

It will still be a battle to overtake long-running competitors like Allset, Level Up and Ritual, plus incumbents that offer takeout pickup like Uber and Grubhub. Logistics is a cut-throat business, and plenty of startups have already failed in the restaurant loyalty space.

Having Andreessen Horowitz’s support could give Snackpass some extra firepower. “A16z has better support and services for their portfolio companies than any other VC we’ve come across and they’ve delivered,” Tan tells me. “We knew that Andrew Chen understands growth and marketplaces from his blog and his Twitter.” That’s critical in a crowded space where such a precise balance of customer acquisition and lifetime value is necessary.

Snapchat, TikTok and Fortnite have all tapped into the youth market with a lighthearted nature that keeps users coming back until they develop network effect. Snackpass is managing to do the same, not with a messaging app or game, but a commerce platform. “We play up creativity, silliness and delight in areas where most companies focus on utility and convenience,” Tan concludes. “We built Snackpass for ourselves and our friends. We’ve carried on this philosophy: if something makes us laugh, we put it in the app.”

Powered by WPeMatico