payments

Auto Added by WPeMatico

Auto Added by WPeMatico

Bill.com went public today after pricing its shares higher than it initially expected. The B2B payments company sold nearly 10 million shares at $22 apiece, raising around $216 million in its IPO. Public investors felt that the company’s price was a deal, sending the value of its equity to $35.51 per share as of the time of writing.

That’s a gain of over 61%.

On the heels of its successful pricing run and raucous first day’s trading, TechCrunch caught up with Bill.com CEO René Lacerte to dig into his company’s debut. We wanted to know how pricing went, and whether the company (which possibly could have valued itself more richly during its IPO pricing, given its first-day pop) had considered a direct listing.

Lacerte detailed what resonated with investors while pricing Bill.com’s shares, and also did a good job outlining his perspective on what matters for companies that are going public. As a spoiler, he wasn’t super focused on the company’s first-day return.

For more on the Bill.com IPO’s nuts and bolts, head here. Let’s get into the interview.

The following interview has been edited for length and clarity. Questions have been condensed.

TechCrunch: How did your IPO pricing feel, and what did you learn from the process?

Lacerte: I think the whole experience has been an incredible learning experience from a capitalism perspective; that’s probably a broader conversation. But you know, it really came down to how our story resonated with investors, and so there’s three components that we kind of really talked to folks about.

Powered by WPeMatico

One share of Amazon stock costs more than $1,700, locking out less-wealthy investors. So to continue its quest to democratize stock trading, Robinhood is launching fractional share trading this week. This lets you buy 0.000001 shares, rounded to the nearest penny, or just $1 of any stock, with zero fee.

The ability to buy by millionth of a share lets Robinhood undercut Square Cash’s recently announced fractional share trading, which sets a $1 minimum for investment. Robinhood users can sign up here for early access to fractional share trading. “One of our core values is participation is power,” says Robinhood co-CEO Vlad Tenev. “Everything we do is rooted in this. We believe that fractional shares have the potential to open up investing for even more people.”

Fractional share trading ensures no one need be turned away, and Robinhood can keep growing its user base of 10 million with its war chest of $910 million in funding. As incumbent brokerages like Charles Schwab and E*Trade move to copy Robinhood’s free stock trading, the startup has to stay ahead in inclusive financial tools. In this case, though, it’s trying to keep up, since Schwab, Square, Stash and SoFi all launched fractional shares this year. Betterment has actually offered this since 2010.

Robinhood has a bunch of other new features aimed at diversifying its offering for the not-yet-rich. Today its Cash Management feature it announced in October is rolling out to its first users on the 800,000-person wait list, offering them 1.8% APY interest on cash in their Robinhood balance plus a Mastercard debit card for spending money or pulling it out of a wide network of ATMs. The feature is effectively a scaled-back relaunch of the botched debut of 3% APY Robinhood Checking a year ago, which was scuttled because the startup failed to secure the proper insurance it now has for Cash Management.

Additionally, Robinhood is launching two more widely requested features early next year. Dividend Reinvestment Plan (DRIP) will automatically reinvest into stocks or ETF cash dividends Robinhood users receive. Recurring Investments will let users schedule daily, weekly, bi-weekly or monthly investments into stocks. With all this, and Crypto trading, Robinhood is evolving into a full financial services suite that will be much harder for competitors to copy.

“We believe that if you want to invest, it shouldn’t matter how much money you have. With fractional shares, we’re opening up a whole universe of stocks and funds, including Amazon, Apple, Disney, Berkshire Hathaway, and thousands of others,” Robinhood product manager Abhishek Fatehpuria tells me.

Users will be able to place real-time fractional share orders in dollar amounts as low as $1 or share amounts as low as 0.000001 shares rounded to the penny during market hours. Stocks worth over $1 per share with a market capitalization above $25 million are eligible, with 4,000 different stocks and ETFs available for commission-free, real-time fractional trading.

“We believe that participation is power. Since day one, we’ve focused on breaking down barriers like trade commissions and account minimums to help people participate in the financial system,” says Fatehpuria. “We have a unique user base — half our customers tell us they’re first-time investors, and the median age of a Robinhood customer is 30. This means we have a unique opportunity to expand access to the markets for this new generation.”

Robinhood is racing to corner the freemium investment tool market before other startups and finance giants can catch up. It opened a waitlist for its U.K. launch next year, which will be its first international market. But in just the past month, Alpaca raised $6 million for an API that lets anyone build a stock brokerage app, and Atom Finance raised $12.5 million for its free investment research tool that could compete with Robinhood’s in-app feature. Meanwhile, Robinhood suffered an embarrassing bug, letting users borrow more money than allowed.

The move fast and break things mentality triggers new dangers when introduced to finance. Robinhood must resist the urge to rush as it spreads itself across more products in pursuit of a more level investment playing field.

Powered by WPeMatico

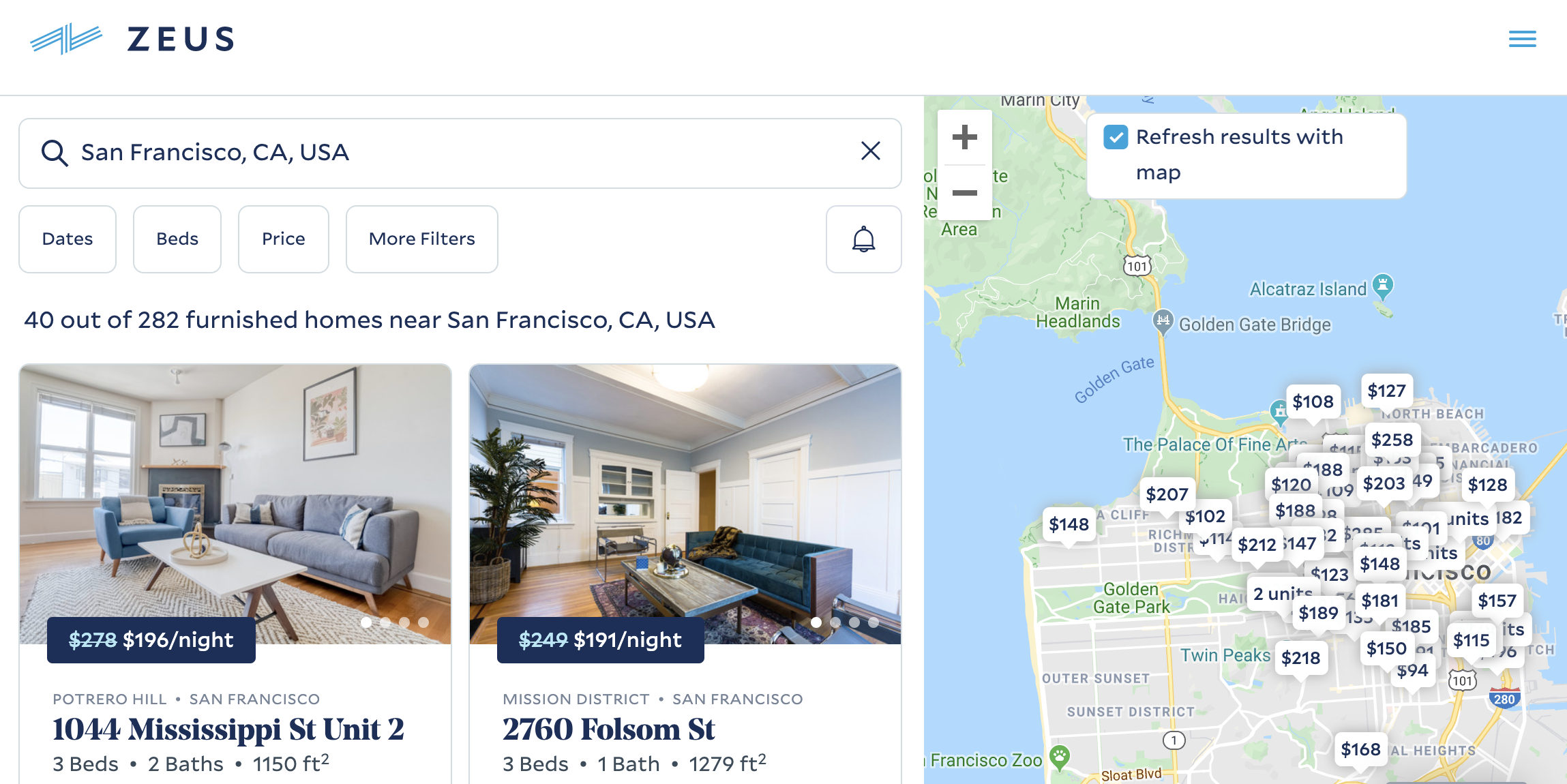

As Airbnb absorbs more and more of the demand for housing, it’s exploring how to monetize opportunities beyond vacation rentals. A marketplace for longer-term corporate housing could be a huge business, but rather than build that itself, Airbnb is making a strategic investment in one of the market leaders called Zeus Living, which will list its homes on the Airbnb site.

In just four years of redecorating landlords’ homes and renting them to relocated workers for 30-day stays (or longer), Zeus Living has grown to a $100 million revenue run rate. It boosted revenue 300% in 2019, and now has 250 employees and more than 2,000 homes under management. Zeus makes money by charging landlords one free month of usage, and marking up the rent charged to customers. It could rent out a $4,000 per month home for $5,000 plus take the extra month to earn $16,000 in a year.

Zeus CEO and co-founder Kulveer Taggar tells me, “I fundamentally believe that a lot of human potential is bound by location. At Zeus, we’re deeply committed to making it easier for people to live where opportunity takes them.” It’s already hosted 27,000 residents for a total of 650,000 nights.

Strong margins, swift momentum and that megatrend of more mobile workforces have earned Zeus Living a new $55 million Series B round it’s announcing on TechCrunch today. The funding comes from Airbnb, Comcast, CEAS Investments and TI Platform Management, plus existing investors Alumni Ventures Group, Initialized Capital, NFX and Spike Ventures. The funding comes at a $205 million post-money valuation.

“The opportunity here is huge, consumer spend is going toward housing and everyone needs to stay somewhere. But it’s Kulveer and Zeus’ go-to-market strategy that is impressive,” says Initialized co-founder and managing partner Garry Tan. “Zeus decided to start with corporate rentals, which we believe is the best go-to-market since it is the highest margin, and capital efficiency wins in a space with many competitors. Corporate needs are longer term, consistent and predictable, and partnering with Airbnb strengthens this approach as they expand to build a platform for every city.”

Zeus co-founder and CEO Kulveer Taggar

Zeus previously raised a $2.5 million seed and then an $11.5 million Series A led by Initialized, as well as $10 million in debt to cover taking on properties in the San Francisco Bay Area, Los Angeles, New York, Seattle and D.C. Now that it’s scaling up, Zeus could add a sizable debt facility to cover the risk of filling apartments with employees from clients like Brex, Disney, ServiceTitan and Samsara.

Instead of moving into a bland corporate housing block, struggling to find a place themselves or ending up in expensive long-term Airbnbs, workers moving to new cities can go to Zeus. It takes over apartments, handles maintenance and fills them with branded comforts like Parachute bedding and Helix mattresses that Zeus gets at bulk rates. The startup is betting that as workers move between jobs and cities more frequently, fewer will own furniture and instead look for furnished homes like those Zeus offers.

Thanks to the premium stays it provides, Zeus can charge clients a lucrative rate, while Taggar claims his service is still about half the price of standard corporate housing. For property owners, Zeus makes it easy to get a consistent rent paycheck with none of the traditional landlord work. Zeus takes care of cleaning and key exchanges so owners don’t need to do any chores like if they were running an Airbnb. Its goal is to get the first renters in within 10 days of taking on a property.

The new funding will help Zeus expand to more neighborhoods and cities while retaining a focus on breadth within each market so clients have plenty of homes from which to choose. The startup will be revamping its booking and invoicing tools for enterprise partners, and improving how it sources real estate. Meanwhile, it will be investing in customer care to maintain its high 70s NPS scores so relocated workers brag to their colleagues about how nice their new place is.

“Finding housing is stressful and time-consuming for both individuals and employers. As someone who has moved countries four times, I’ve lived through that tension,” says Taggar. “Zeus Living has built technology to remove complexity from housing, turning it into a service that enables a more mobile world.”

Taggar got into the real estate business early, remortgaging his mom’s house to buy a condo in Mumbai to rent out. After moving to the U.S., he built and sold Y Combinator-backed auction tool Auctomatic with co-founder and future Stripe starter Patrick Collison. It was while working on NFC-triggered task launcher Tagstand that Taggar recognized the hassle of both finding new corporate housing and reliably renting out one’s home. With Uber, Stripe and more startups growing huge by simplifying processes that move a lot of money around, he was inspired to do the same with Zeus Living.

“Modern professionals travel more frequently, stay longer and seek accommodations that feel like home. As more companies look to Airbnb for Work for extended-stay and relocation solutions, this segment remains a key focus for Airbnb,” says David Holyoke, global head of Airbnb for Work.

“We have great alignment with the Airbnb team in terms of serving the changing needs of business travelers that want the comforts of home when traveling for extended 30-day stays for work or a project,” Taggar follows. Airbnb can help Zeus drive demand thanks to all its inbound traffic, while Zeus offers Airbnb more supply for customers seeking longer stays.

Zeus Living’s co-founders

Zeus’ biggest threat is that it could get overextended, misjudge demand and end up on the hook to pay rent for two-year leases it can’t fill. And now with more funding, there will be added scrutiny regarding its margins, especially in the wake of the WeWork implosion.

Taggar recognizes these threats. “This is a business where we have to be focused on maximizing the gross profit we generate for the investments we make, with the least amount of risk. At Zeus Living, we’re continuously improving the ways we predict and secure demand.” He’s also building out teams on the ground in different markets to ensure regulatory compliance and push for more conducive laws around 30-day (or longer) rental stays.

Property tech has become a heated space, though, so Zeus will have heavy competition. There are traditional corporate housing providers, pure marketplaces that don’t deal with logistics and direct competitors like $66 million-funded Domio and juggernaut Sonder, which has raised a whopping $360 million. Zeus might also see its model copied abroad before it can get there. Over time, landlords and real estate investment trusts like Blackstone could force Zeus, Sonder and others to compete to pay them the most for leases, eating into all the startups’ margins.

At least with Airbnb as an investor, Zeus won’t have to fear a bitter battle with the tech giant over corporate housing. Instead, Airbnb could keep investing to coin off this adjacent market while listing Zeus properties, or potentially acquired the startup one day. For now though, Taggar just wants to prove startups can be accountable in the real world, acknowledging that taking over people’s homes is “a lot of responsibility! Our homes represent hundreds of millions of dollars of assets we manage and we take that very seriously.”

Powered by WPeMatico

In African fintech, the fourth quarter of 2019 brought big money to new entrants.

Chinese investors put $220 million into OPay and PalmPay — two fledgling startups with plans to scale in Nigeria and the broader continent. Several sources told me the big bucks had created anxiety for more than few payments ventures in Nigeria with similar strategies and smaller coffers. They may not need to fret just yet, however: lessons from Africa’s most successful mobile-money case study, M-Pesa, suggest that VC alone won’t buy scale in digital finance.

Over the last decade, Africa has been in the midst of a startup boom accompanied by big growth in VC and improvements in internet and mobile penetration.

Some definitive country centers for company formation, tech hubs and investment have emerged; Nigeria, South Africa and Kenya lead the continent in numbers for all those categories. Additional strong and emerging points for innovation and startups across Africa’s 54 countries and 1.2 billion people include Ghana, Tanzania, Ethiopia, and Senegal.

The continent surpassed $1 billion in VC to startups in 2018 and per research done by Partech and WeeTracker, fintech is the focus of the bulk of capital and deal-flow.

By several estimates, Africa is home to the largest share of the world’s unbanked and underbanked population.

This runs parallel to the region’s off-the-grid SME’s and economic activity — on display and in commercial motion through the street traders, roadside kiosks and open-air markets common from Nairobi to Lagos.

IMF estimates have pegged Africa’s informal economy as one of the largest in the world. Thousands of fintech startups have descended onto this large pool of unbanked and underbranked citizens and SMEs looking to grow digital finance products and market share.

In this race, the West African nation of Nigeria — home to Africa’s largest economy and population — is becoming an epicenter for VC. Many fintech-related companies are adopting a strategy of scaling there first before expanding outward.

That includes new entrants OPay and PalmPay, which raised so much capital in fourth quarter 2019. It’s notable that both were founded in 2019 and largely incubated by Chinese actors.

PalmPay, a consumer-oriented payments product, went live in November with a $40 million seed-round (one of the largest in Africa in 2019) led by Africa’s biggest mobile-phones seller — China’s Transsion. The startup was upfront about its ambitions, stating its goals to become “Africa’s largest financial services platform,” in a company statement.

![]() To that end, PalmPay conveniently entered a strategic partnership with its lead investor. The startup’s payment app will come pre-installed on Transsion’s mobile device brands, such as Tecno, in Africa — for an estimated reach of 20 million phones in 2020.

To that end, PalmPay conveniently entered a strategic partnership with its lead investor. The startup’s payment app will come pre-installed on Transsion’s mobile device brands, such as Tecno, in Africa — for an estimated reach of 20 million phones in 2020.

PalmPay also launched in Ghana in November and its U.K. and Africa-based CEO, Greg Reeve, confirmed plans to expand to additional African countries in 2020.

If PalmPay’s $40 million seed round got founders’ attention, OPay’s $120 million Series B created shock-waves, coming just months after the mobile-based fintech venture raised $50 million — making OPay’s $170 million capital haul equivalent to roughly a fifth of all VC raised in Africa in 2018.

Founded by Chinese owned consumer internet company Opera — and backed by 9 Chinese investors — OPay is the payment utility for a suite of Opera -developed internet based commercial products in Nigeria that include ride-hail apps ORide and OCar and food delivery service OFood.

With its latest Series A, OPay announced it would expand in Kenya, South Africa, and Ghana.

In Nigeria, OPay’s $170 million Series A and B announced in the span of months dwarfs just about anything raised by new and existing fintech players, with the exception of Interswitch.

The homegrown payments processing company — which pioneered much of Nigeria’s digital finance infrastructure — reached unicorn status in November when Visa took a reported $200 million minority stake in the venture.

A sampling of more common funding amounts for payments ventures in Nigeria includes established fintech company Paga’s $10 million Series B. Recent market entrant Chipper Cash’s May 2019 seed-round was $2.4 million.

There is a large disparity between fintech startups in Nigeria with capital raises in ones and tens of millions vs. OPay and PalmPay’s $40 and $120 million rounds. Conventional wisdom could be that the big-capital, big spending firms have an unmistakable advantage in scaling digital payments in Nigeria and other markets.

A look at Kenya’s M-Pesa may prove otherwise.

Powered by WPeMatico

$35 million-funded Omni is packing up and shutting down after struggling to make the economics of equipment rentals and physical on-demand storage work out. It’s another victim of a venture capital-subsidized business offering a convenient service at an unsustainable price.

The startup fought for a second wind after selling off its physical storage operations to competitor Clutter in May. Then sources tell me it tried to build a whitelabel software platform for letting brick-and-mortar merchants rent stuff like drills or tents as well as sell them so Omni could get out of hands-on logistics. But now the whole company is folding, with Coinbase hiring roughly 10 of Omni’s engineers.

“They realized that the core business was just challenging as architected” a source close to Omni tells TechCrunch. “The service was really great for the consumer but when they looked at what it would take to scale, that would be difficult and expensive.” Another source says Omni’s peak headcount was around 70.

The news follows TechCrunch’s report in October that Omni had laid off operations teams members and was in talks to sell its engineering team to Coinbase. Omni had internally discussed informing its retail rental partners ahead of time that it would be shutting down. Meanwhile, it frantically worked to stop team members from contacting the press about the startup’s internal troubles.

“We’ll be winding down operations at Omni and closing the platform by the end of this year. We are proud of what we built and incredibl y thankful for everyone who supported our vision over the past five and a half years” an Omni spokesperson says. Omni CEO Tom McLeod did not respond to multiple requests for comment. Oddly, Omni was still allowing renters to pay for items as of this morning, though it’s already shut down its blog and hasn’t made a public announcement about its shut down.

“Coinbase has reached an agreement with Omni to hire members of its engineering team. We’re always looking for top-tier engineering talent and look forward to welcoming these new team members to Coinbase” a Coinbase spokesperson tells us. The team was looking for more highly skilled engineers they could efficiently hire as a group, though it’s too early to say what they’ll be working on.

Omni originaly launched in 2015, offering to send a van to your house to pick up and index any of your possession, drive them to a nearby warehouse, store them, and bring them back to you whenever you needed for just a few dollars per month. It seemed too good to be true and ended up being just that.

Eventually Omni pivoted towards letting you rent out what you were storing so you and it could earn some extra cash in 2017. Sensing a better business model there, it sold its storage business to Softbank-funded Clutter and moved to helping retail stores run rental programs. But that simply required too big of a shift in behavior for merchants and users, while also relying on slim margins.

One major question is whether investors will get any cash back. Omni raised $25 million from cryptocurrency company Ripple in early 2018. Major investors include Flybridge, Highland, Allen & Company, and Founders Fund, plus a slew of angels.

The implosion of Omni comes as investors are re-examining business fundamentals of startups in the wake of Uber’s valuation getting cut in half in the public markets and the chaos at WeWork ahead of its planned IPO. VCs and their LPs want growth, but not at the cost of burning endless sums of money to subsidize prices just to lure customers to a platform.

It’s one thing if the value of the service is so high that people will stick with a startup as prices rise to sustainable levels, as many have with ride hailing. But for Omni, ballooning storage prices pissed off users as on-demand became less afforable than a traditional storage unit. Rentals were a hassle, especially considering users had to pick-up and return items themselves when they could just buy the items and get instant delivery from Amazon.

Startups that need a ton of cash for operations and marketing but don’t have a clear path to ultra-high lifetime value they can earn from customers may find their streams of capital running dry.

Powered by WPeMatico

Paidy, a Japanese financial tech startup that provides instant credit to consumers in Japan, announced today that it has raised a total of $143 million in new financing. This includes a $83 million Series C extension from investors including PayPal Ventures and debt financing of $60 million. The funding will be used to advance Paidy’s goals of signing large-scale merchants, offering new financial services and growing its user base to 11 million accounts by the end of 2020.

In addition to PayPal Ventures, investors in the Series C extension also include Soros Capital Management, JS Capital Management and Tybourne Capital Management, along with another undisclosed investor. The debt financing is from Goldman Sachs Japan, Mizuho Bank, Sumitomo Mitsui Banking Corporation and Sumitomo Mitsui Trust Bank. Earlier this month, Paidy and Goldman Sachs Japan established a warehouse facility valued at $52 million. Paidy also established credit facility worth $8 million with the three banks.

This is the largest investment to date in the Japanese financial tech industry, according to data cited by Paidy and brings the total investment the company has raised so far to $163 million. A representative for the startup says it decided to extend its Series C instead of moving onto a D round to preserve the equity ratio for existing investors and issue the same preferred shares as its previous funding rounds.

Launched in 2014, Paidy was created because many Japanese consumers don’t use credit cards for e-commerce purchases, even though the credit card penetration rate there is relatively high. Instead, many prefer to pay cash on delivery or at convenience stores and other pickup locations. While this makes online shopping easier for consumers, it presents several challenges for sellers, because they need to cover the cost of merchandise that hasn’t been paid for yet or deal with uncompleted deliveries.

Paidy’s solution is to make it possible for people to pay for merchandise online without needing to create an account first or use their credit cards. If a seller offers Paidy as a payment method, customers can check out by entering their mobile phone numbers and email addresses, which are then authenticated with code sent through SMS or voice. Paidy covers the cost of the items and bills customers monthly. Paidy uses proprietary machine learning models to score the creditworthiness of users, and says its service can help reduce incomplete transactions (or items that buyers ultimately don’t pick up and pay for), increase conversion rates, average order values and repeat purchases.

Powered by WPeMatico

Brazil continued to churn out unicorns this month, with Curitiba-based Ebanx becoming the first startup from the southern part of the country to top a $1 billion valuation. U.S.-based FTV Capital provided the investment but did not disclose the amount invested nor the exact valuation of Ebanx after the investment.

Ebanx is an end-to-end payment processor that helps international companies receive payments in the Latin American market, similar to Stripe. Their clients include Airbnb, AliExpress, Pipedrive, Spotify, Uber and Wish, and more than 50 million Latin Americans have conducted transactions with more than 1,000 companies through the Ebanx platform. This investment comes on the heels of exciting partnerships with Uber Pay, Shopify, Spotify and Visa to expand cross-border payment processing across the region.

Ebanx has operations in Brazil, Mexico, Argentina, Colombia, Chile, Peru, Ecuador and Bolivia, and will expand their local payment solution, Ebanx Pay, into Colombia in 2020. The company has grown its user base by offering a full-service product that includes market research, 24/7 customer service and anti-fraud technology.

The Ebanx investment is part of a growing interest in Latin American payments startups. Brazil’s PagSeguro and StoneCo had successful IPOs last year, while Mexico’s Conekta and Ecuador’s Kushki have raised large rounds to try to unite the region under a single processor as Latin America rapidly adopts e-commerce.

The acquisition of the Chilean-Mexican grocery delivery startup Cornershop has been an emotional roller coaster for Latin American entrepreneurs and investors throughout 2019. First Walmart announced a $225 million deal that would be one of the bigger exits of the region, then the acquisition was blocked by Mexican antitrust institution COFECE. This announcement dealt a blow to the ecosystem as entrepreneurs and VCs had eagerly awaited this boost in liquidity in the local market.

Last-mile delivery and logistics became a very competitive space in Latin America in 2018.

Then in mid-October 2019, Uber announced it would take a 51% stake in Cornershop for a reported $450 million, quadrupling the startup’s value in the four months since the COFECE decision. This deal will consist of cash, investment in Cornershop’s growth and stock in Uber, which IPO’d earlier this year.

However, this deal must also be approved by the Chilean and Mexican antitrust boards, which are expected to release their decisions within the next two weeks. In the meantime, Cornershop will continue its expansion into the Colombian market after it added Peru and Canada in 2019.

Last-mile delivery and logistics became a very competitive space in Latin America in 2018, and many of the players are sitting on enormous pools of capital. Colombia’s Rappi raised $1 billion from SoftBank in early 2019, breaking records for startup investment for the region. Brazil’s iFood raised $500 million from Naspers at the end of 2018. However, delivery continues to be a cash-intensive business, with many of these companies burning through capital quickly to gain market share. Cornershop was an exception and had raised less than $50 million before the acquisition.

Despite the WeWork crash, SoftBank has continued investing consistently in Brazilian startups. In early October 2019, the Japanese investor led an undisclosed Series B round for Brazilian collaborative bus chartering startup Buser. Buser’s team will invest more than $73 million in growth over the next 12 months to create new alliances for their network of operating partners.

Buser helps coordinate groups of people to charter buses at convenient times and lower prices, disrupting the bureaucratic, anti-competitive and inefficient bus system. The company has grown 1,500% over the past nine months and serves more than 3,000 people per day. While Buser has been popular with locals, traditional bus drivers are calling for regulation to slow the company’s meteoric growth. Buser plans to add more than 100 direct jobs in 200 cities over the next 12 months, and SoftBank’s most recent investment will help power this growth.

Brazil’s e-commerce marketplace integrator Olist also received investment from SoftBank for its Series C, coming in around $46 million. Redpoint eVentures and Valor Capital also participated in the round.

This investment signals the increased interest by traditional retailers in startups that are slowly chipping away at their market share across the region.

Olist connects small businesses to larger product marketplaces to help entrepreneurs sell their products to a larger customer base. They will reportedly use this investment to investigate the development of financial products and look for collaboration with SoftBank’s other companies, like Rappi and Loggi. Based in Curitiba, Olist was founded in 2015 to help small merchants gain market share across the country through a SaaS licensing model to small brick and mortar businesses.

Today, Olist has more than 7,000 customers and uses a drop-shipping model to send products directly from stores to clients around the country, allowing them to grow with a capital-light model. They will use the investment to add up to 100 new employees.

Grocery chain Carrefour acquired a large stake in Brazil-based Ewally after it completed Village Capital’s first regional acceleration program.

Ewally improves financial inclusion in Brazil through a mobile wallet app that allows unbanked clients to pay bills and make purchases online through the blockchain. Carrefour will reportedly use the acquisition to accelerate digital transformation and improve online payment mechanisms throughout Brazil.

Carrefour did not disclose the amount invested and the deal is still subject to approval by Brazilian financial regulation authorities. However, this investment signals the increased interest by traditional retailers in startups that are slowly chipping away at their market share across the region.

Startups in Brazil, Colombia and Argentina raised several rounds this month, ranging from $1.5 million to $13 million. Brazil’s Xerpa, Colombia’s Sempli, Brazil’s Gorilla and Argentina’s Bitso and Worcket were among those that raised capital from local and international investors in October 2019.

Brazilian human resource management platform Xerpa raised $13 million from Vostok Emerging Finance to continue to help companies like MercadoLibre, iFood and QuintoAndar provide benefits for their employees. Previous investors include Nubank’s David Velez, Kaszek Ventures and QED Investors.

Sempli, an online lending platform for small businesses in Colombia, raised an $8 million Series A from new investors Oikocredit and Incofin CVSO, as well as previous investors BID LAB, XTPI Fund, Generación Exponencial, and Impulsum Ventures. To date, Sempli has raised more than $24 million in equity funding. The founders will use this round to grow their portfolio and improve their risk assessment technology to provide more small business loans in Colombia.

Brazil’s Quicko, an alternative mobility startup that uses big data, raised $10 million in October from Brazilian transport company CCR. Quicko’s technology integrates all mobility options — from bicycles to Uber and 99 — to help people get where they need to go as quickly and inexpensively as possible.

Also in Brazil, startup Gorilla Invest raised $8.4 million from Ribbit Capital, Monashees and Iporanga. Gorilla aggregates financial assets so that investors can review all their commitments in one place, and currently manages more than $1.2 billion for 40,000 clients.

Mexican cryptocurrency exchange Bitso raised an undisclosed round from Argentine startup Ripple to expand into the Southern Cone, especially Argentina and Brazil. Other investors in the round included Pantera Capital, Digital Currency Group, Jump Capital and Coinbase.

Looking ahead to November, with unsettled politics in several countries across the region, tech startups are growing despite governmental changes. Some of these changes will likely have a positive effect on the regional ecosystem as people push for more sustainable and equal economic growth.

What to watch next? Last year, Q4 was marked by a wave of large investments as funds and startups look to end the year strong. IFood raised its record-breaking $500 million round in December 2018. We may well see a similar uptick this year as mega-funds like SoftBank have been consistently investing multi-million dollar rounds since June. There is no sign international investment in Latin America will slow through the end of the year, so we can likely look forward to several more growth-stage rounds before the year is out.

Powered by WPeMatico

Submit campaign ads to fact checking, limit microtargeting, cap spending, observe silence periods or at least warn users. These are the solutions Facebook employees put forward in an open letter pleading with CEO Mark Zuckerberg and company leadership to address misinformation in political ads.

The letter, obtained by The New York Times’ Mike Isaac, insists that “Free speech and paid speech are not the same thing . . . Our current policies on fact checking people in political office, or those running for office, are a threat to what FB stands for.” The letter was posted to Facebook’s internal collaboration forum a few weeks ago.

The sentiments echo what I called for in a TechCrunch opinion piece on October 13th calling on Facebook to ban political ads. Unfettered misinformation in political ads on Facebook lets politicians and their supporters spread inflammatory and inaccurate claims about their views and their rivals while racking up donations to buy more of these ads.

The social network can still offer freedom of expression to political campaigns on their own Facebook Pages while limiting the ability of the richest and most dishonest to pay to make their lies the loudest. We suggested that if Facebook won’t drop political ads, they should be fact checked and/or use an array of generic “vote for me” or “donate here” ad units that don’t allow accusations. We also criticized how microtargeting of communities vulnerable to misinformation and instant donation links make Facebook ads more dangerous than equivalent TV or radio spots.

The Facebook CEO, Mark Zuckerberg, testified before the House Financial Services Committee on Wednesday October 23, 2019 in Washington, D.C. (Photo by Aurora Samperio/NurPhoto via Getty Images)

More than 250 employees of Facebook’s 35,000 staffers have signed the letter, which declares, “We strongly object to this policy as it stands. It doesn’t protect voices, but instead allows politicians to weaponize our platform by targeting people who believe that content posted by political figures is trustworthy.” It suggests the current policy undermines Facebook’s election integrity work, confuses users about where misinformation is allowed, and signals Facebook is happy to profit from lies.

The solutions suggested include:

A combination of these approaches could let Facebook stop short of banning political ads without allowing rampant misinformation or having to police individual claims.

Facebook’s response to the letter was “We remain committed to not censoring political speech, and will continue exploring additional steps we can take to bring increased transparency to political ads.” But that straw-man’s the letter’s request. Employees aren’t asking politicians to be kicked off Facebook or have their posts/ads deleted. They’re asking for warning labels and limits on paid reach. That’s not censorship.

Zuckerberg had stood resolute on the policy despite backlash from the press and lawmakers, including Representative Alexandria Ocasio-Cortez (D-NY). She left him tongue-tied during a congressional testimony when she asked exactly what kinds of misinfo were allowed in ads.

But then Friday, Facebook blocked an ad designed to test its limits by claiming Republican Lindsey Graham had voted for Ocasio-Cortez’s Green Deal he actually opposes. Facebook told Reuters it will fact-check PAC ads.

One sensible approach for politicians’ ads would be for Facebook to ramp up fact-checking, starting with presidential candidates until it has the resources to scan more. Those fact-checked as false should receive an interstitial warning blocking their content rather than just a “false” label. That could be paired with giving political ads a bigger disclaimer without making them too prominent-looking in general and only allowing targeting by state.

Deciding on potential spending limits and silent periods would be more messy. Low limits could even the playing field and broad silent periods, especially during voting periods, and could prevent voter suppression. Perhaps these specifics should be left to Facebook’s upcoming independent Oversight Board that acts as a supreme court for moderation decisions and policies.

Zuckerberg’s core argument for the policy is that over time, history bends toward more speech, not censorship. But that succumbs to utopic fallacy that assumes technology evenly advantages the honest and dishonest. In reality, sensational misinformation spreads much further and faster than level-headed truth. Microtargeted ads with thousands of variants undercut and overwhelm the democratic apparatus designed to punish liars, while partisan news outlets counter attempts to call them out.

Zuckerberg wants to avoid Facebook becoming the truth police. But as we and employees have put forward, there is a progressive approach to limiting misinformation if he’s willing to step back from his philosophical orthodoxy.

The full text of the letter from Facebook employees to leadership about political ads can be found below, via The New York Times:

We are proud to work here.

Facebook stands for people expressing their voice. Creating a place where we can debate, share different opinions, and express our views is what makes our app and technologies meaningful for people all over the world.

We are proud to work for a place that enables that expression, and we believe it is imperative to evolve as societies change. As Chris Cox said, “We know the effects of social media are not neutral, and its history has not yet been written.”

This is our company.

We’re reaching out to you, the leaders of this company, because we’re worried we’re on track to undo the great strides our product teams have made in integrity over the last two years. We work here because we care, because we know that even our smallest choices impact communities at an astounding scale. We want to raise our concerns before it’s too late.

Free speech and paid speech are not the same thing.

Misinformation affects us all. Our current policies on fact checking people in political office, or those running for office, are a threat to what FB stands for. We strongly object to this policy as it stands. It doesn’t protect voices, but instead allows politicians to weaponize our platform by targeting people who believe that content posted by political figures is trustworthy.

Allowing paid civic misinformation to run on the platform in its current state has the potential to:

— Increase distrust in our platform by allowing similar paid and organic content to sit side-by-side — some with third-party fact-checking and some without. Additionally, it communicates that we are OK profiting from deliberate misinformation campaigns by those in or seeking positions of power.

— Undo integrity product work. Currently, integrity teams are working hard to give users more context on the content they see, demote violating content, and more. For the Election 2020 Lockdown, these teams made hard choices on what to support and what not to support, and this policy will undo much of that work by undermining trust in the platform. And after the 2020 Lockdown, this policy has the potential to continue to cause harm in coming elections around the world.

Proposals for improvement

Our goal is to bring awareness to our leadership that a large part of the employee body does not agree with this policy. We want to work with our leadership to develop better solutions that both protect our business and the people who use our products. We know this work is nuanced, but there are many things we can do short of eliminating political ads altogether.

These suggestions are all focused on ad-related content, not organic.

1. Hold political ads to the same standard as other ads.

a. Misinformation shared by political advertisers has an outsized detrimental impact on our community. We should not accept money for political ads without applying the standards that our other ads have to follow.

2. Stronger visual design treatment for political ads.

a. People have trouble distinguishing political ads from organic posts. We should apply a stronger design treatment to political ads that makes it easier for people to establish context.

3. Restrict targeting for political ads.

a. Currently, politicians and political campaigns can use our advanced targeting tools, such as Custom Audiences. It is common for political advertisers to upload voter rolls (which are publicly available in order to reach voters) and then use behavioral tracking tools (such as the FB pixel) and ad engagement to refine ads further. The risk with allowing this is that it’s hard for people in the electorate to participate in the “public scrutiny” that we’re saying comes along with political speech. These ads are often so micro-targeted that the conversations on our platforms are much more siloed than on other platforms. Currently we restrict targeting for housing and education and credit verticals due to a history of discrimination. We should extend similar restrictions to political advertising.

4. Broader observance of the election silence periods

a. Observe election silence in compliance with local laws and regulations. Explore a self-imposed election silence for all elections around the world to act in good faith and as good citizens.

5. Spend caps for individual politicians, regardless of source

a. FB has stated that one of the benefits of running political ads is to help more voices get heard. However, high-profile politicians can out-spend new voices and drown out the competition. To solve for this, if you have a PAC and a politician both running ads, there would be a limit that would apply to both together, rather than to each advertiser individually.

6. Clearer policies for political ads

a. If FB does not change the policies for political ads, we need to update the way they are displayed. For consumers and advertisers, it’s not immediately clear that political ads are exempt from the fact-checking that other ads go through. It should be easily understood by anyone that our advertising policies about misinformation don’t apply to original political content or ads, especially since political misinformation is more destructive than other types of misinformation.

Therefore, the section of the policies should be moved from “prohibited content” (which is not allowed at all) to “restricted content” (which is allowed with restrictions).

We want to have this conversation in an open dialog because we want to see actual change.

We are proud of the work that the integrity teams have done, and we don’t want to see that undermined by policy. Over the coming months, we’ll continue this conversation, and we look forward to working towards solutions together.

This is still our company.

Powered by WPeMatico

“I don’t control Libra” was the central theme of Facebook CEO Mark Zuckerberg’s testimony today in Congress. The House of Representatives unleashed critiques of his approach to cryptocurrency, privacy, encryption and running a giant corporation during six hours of hearings. Zuckerberg tried to assuage their fears while stoking concerns that if Facebook doesn’t build Libra, the world will end up using China’s version. Yet Facebook won’t stop shaking up society, with Zuckerberg saying its News tab feature will be announced this week.

During the hearing before the House Financial Services Committee that you can watch here, Zuckerberg recommitted to only releasing Libra with full U.S. regulatory approval. But given the tone of the questioning and Zuckerberg’s lack of fresh answers since Facebook’s David Marcus testified about Libra in July, Libra now looks even less likely to launch in 2020.

The hearing started tensely, with Rep. Maxine Waters (D-CA) declaring that “Perhaps you believe that you’re above the law, and it appears that you are aggressively increasing the size of your company, and are willing to step over anyone, including your competitors, women, people of color, you own users, and even our democracy to get what you want . . . In fact, you have opened up a serious discussion about whether Facebook should be broken up.“

However, some members of Congress used their time to advocate for American dominance instead of heavy regulation. Rep. Patrick McHenry (R-NC) said “the question is, are we going to spend our time trying to devise ways for government planners to centralize and control as to who, when and how innovators can innovate.” Many Republicans complimented Zuckerberg on his business acumen, though none showed outright support for Libra.

With few highlights or positive moments coming from the hearing, here are the major takeaways followed by a chronicle of the top exchanges between Zuckerberg and Congress:

Zuckerberg tried to leverage nationalist sentiment to deflect scrutiny. “As soon as we put forward the white paper around the Libra project, China immediately announced a public private partnership, working with companies . . . to extend the work that they’ve already done with AliPay into a digital Renminbi as part of the Belt and Road Initiative that they have, and they’re planning on launching that in the next few months.” He later said that for Libra, “Chinese companies would be the primary competitors.”

Facebook’s executives have repeatedly leaned on this “let us, or China will” argument we chronicle here.

What if the Libra Association chooses to add the Chinese currency to the basket used to back Libra and reduces the U.S. dollar’s fraction of the basket? “I think it would be completely reasonable for our regulators to try to [implement] a restriction that says that it has to be primarily U.S. dollars,” Zuckerberg responded in one of his most substantial answers of the day. Zuckerberg was receptive to feedback that the Libra Association should keep its white paper updated.

As for why Libra isn’t just backed 100% with the U.S. dollar, Zuckerberg explained that “I think from a U.S. regulatory perspective, it would probably be significantly simpler. But because we’re trying to build something that can also be a global payment system that works in other places, it may be less welcome in other places if it’s only 100% based on the dollar.” Still, Zuckerberg said he would leave his children their inheritance in Libra because it’s backed one-to-one by the Libra reserve.

Zuckerberg wouldn’t commit to blocking anonymous Libra wallets that could facilitate money laundering, only saying Facebook’s own Calibra wallet would have strong identity checks. He did say Libra was exploring whether it could encode “know your customer” protections at the network level instead of relying on developers to build this into their wallets.

On whether Facebook will increasingly seek to verify users’ identities through government ID, Zuckerberg was enthusiastic. “This is an area where I think we are going to do a lot more in the years to come. We started with political ads . . . over the coming years for anything that people are doing that is sensitive, we’re likely going to increasingly require verification either by government ID or other things so we can have a clear sense of people’s authentic identity.”

Rep. Dean Phillips (D-MN) mentioned this could be a competitive advantage, implying Facebook’s size and resources might allow it to embark on a verification initiative other companies couldn’t.

Facebook has assured regulators that Calibra’s data would be kept separate from the social network. But Facebook said the same when it acquired WhatsApp, then reneged and integrated its data. This time around, Congresswoman Nydia Velázquez declared that “we’re going to need to make sure that . . . you learned that you should not lie.”

When pushed on why Libra Association members like Visa, Stripe and eBay left the organization, Zuckerberg admitted, “I think because it’s a risky project and there’s been a lot of scrutiny.” Zuckerberg struck back at finance incumbents, saying “I think that the U.S. financial industry . . . is just frankly behind where it needs to be to innovate and continue American financial leadership going forward.”

In an awkward moment, Zuckerberg could not answer which Libra members were run by women, minorities or LGBTQ+ people. “Is it true that the overwhelming majority of persons associated with this endeavor are white men?,” Rep. Al Green (D-TX) asked. “Congressman, I don’t know off the top of my head,” Zuckerberg responded.

Zuckerberg was criticized for trying to profit and potentially helping money laundering while claiming Libra is designed to help the unbanked. Zuckerberg said the Libra Association “hadn’t nailed down policies” about whether anonymous payments are allowed.

Rep. Brad Sherman (D-CA) said “for the richest man in the world to come here and hide behind the poorest people in the world, and say that’s who you’re really trying to help. You’re trying to help those for whom the dollar is not a good currency — drug dealers, terrorists.” Some members of Congress like Sherman chose to use their entire time monologuing instead of actually asking questions.

Zuckerberg got a chance to clear up a major snafu from Marcus’ testimony, where he said the Libra Association was in contact with the Swiss data regulator, which CNBC reported hadn’t heard from Libra. Zuckerberg explained today that the Libra Association had been in contact with the primary Swiss Financial Market Supervisory Authority instead. He says Facebook plans to earn money from Libra on ads from small businesses if cheap transactions lead to more e-commerce.

In one revealing exchange, Rep. Lance Gooden (R-TX) asked if the Libra Association still planned to offer profit incentives by offering dividends based on interest earned on currency in the Libra reserve after expenses are paid. Zuckerberg said the idea had either been “modified or abandoned.”

The highlighted section detailing how Libra Association members earn dividends on Libra reserve interest has been removed from the Libra whitepaper

Throughout the testimony, Zuckerberg tried to distance himself and Facebook from the Libra Association’s decision making process. “We might be required to pull out if the Association independently decides to move forward on something that we’re not comfortable with,” Zuckerberg said. That means if Facebook can’t launch Libra, it could still theoretically launch without the social network, though it does most of the engineering heavy-lifting.

The strategy was crystallized by Zuckerberg’s response to whether he could commit to moving Libra’s headquarters from Switzerland to the U.S. “At this point, we do not control the independent Libra Association so I don’t think we can make that decision.” Rep. Ayanna Pressley (D-MA) refuted this position, stating, “Mr. Zuckerberg, Libra is Facebook, and Facebook is you.”

The Facebook CEO, Mark Zuckerberg, testified before the House Financial Services Committee on Wednesday October 23, 2019 Washington, D.C. (Photo by Aurora Samperio/NurPhoto via Getty Images)

The “we don’t control Libra” argument provides Facebook and Libra an escape hatch from criticism, because any member and even the newly appointed chairperson and board can’t unilaterally control or make promises about its actions.

Many Congress members remain fixated on Facebook’s recently solidified policy of refusing to submit political ads for fact-checking. Rep Sean Casten (D-IL) asked if in Zuckerberg’s recent meeting with President Trump, “Did anyone discuss the policy change along the exemption of political figures and parties from misinformation prohibition on Facebook?” Zuckerberg responded, “Congressman, that did not come up,” quieting theories that Trump pushed for the policy that would exempt false claims in his ads.

Zuckerberg defended the policy to Rep. Alexandria Ocasio-Cortez (D-NY), saying “I think lying is bad, and I think if you were to run an ad that had a lie, that would be bad,” but that outside of calls for violence or voter suppression, Facebook thinks it’s best to leave lies in ads from politicians so they can be scrutinized by the press and public. Yet that too heavily leans on the media to scrutinize thousands of ad variants being run as part of multi-hundred-million-dollar political ad campaigns.

Rep. Ann Wagner (R-MO) chided Zuckerberg, saying “you’re not working hard enough” to stop the spread of child exploitation imagery online despite Facebook submitting millions of reports. She brought up worries that Facebook moving entirely to encrypted messaging could hide child abusers, and Zuckerberg merely said “I think we work harder than any other company.” He failed to explain how Facebook would continue improving detection through encryption.

Oddly, Zuckerberg was directly confronted about his views on vaccines since Facebook works to hide vaccine hoaxes and avoid recommending groups spreading unverified information about them. “I don’t think it would be possible for anyone to be 100% confident, but my understanding of the scientific consensus is that it is important that people get their vaccines,” Zuckerberg said, defending Facebook’s decision to hide some of this content.

In another strange moment, Rep. Madeleine Dean (D-PA) demanded if Facebook had bought blocks of hotel rooms at Trump properties but never used them just to curry favor with the president. Zuckerberg said he’d never heard of that and would be surprised if it was true.

On deepfakes, Zuckerberg confirmed that “I think deepfakes are clearly one of the emerging threats that we need to get in front of and develop policy around to address. We’re currently working on what the policy should be to differentiate between media that has manipulated and been manipulated by AI tools like deepfakes, with the intent to mislead people.” Zuckerberg later said the doctored Nancy Pelosi video should have been flagged sooner, and highlighted Facebook needs a separate deepfakes policy. Yet Facebook’s policy allows politicians’ ads to mislead people, weakening faith that it will properly address this new problem.

Questions about Facebook’s fair practices led Zuckerberg to reiterate his call for regulation, saying “I think we need federal privacy legislation. I think we need data portability legislation. I think clear rules on elections-related content would be helpful too because it’s not clear to me that we want private companies making so many decisions on these important areas by themselves.”

Regarding housing discrimination via Facebook ads, Zuckerberg committed to working with regulators to provide information under subpoena, noted Facebook has banned discriminatory housing ads, and said “Nobody wants to redline and I’m sure that was accidental.”

Zuckerberg received his heaviest criticism of the day from Rep. Joyce Beatty (D-OH), who grilled him about not knowing if diverse bankers manage Facebook’s cash or if diverse law firms handle its court cases. She chastised Facebook for a lack of diverse leadership, saying “this is appalling and disgusting to me.” Of COO Sheryl Sandberg, who leads Facebook’s civil rights task force, Beatty said “we know she’s not really civil rights.”

WASHINGTON, DC – OCTOBER 23: Facebook co-founder and CEO Mark Zuckerberg arrives to testify before the House Financial Services Committee in the Rayburn House Office Building on Capitol Hill October 23, 2019 in Washington, DC. Zuckerberg testified about Facebook’s proposed cryptocurrency Libra, how his company will handle false and misleading information by political leaders during the 2020 campaign and how it handles its users’ data and privacy. (Photo by Chip Somodevilla/Getty Images)

Some of the day’s most astute questioning came from Congresswoman Katherine Porter (D-CA). She hammered Zuckerberg about Facebook lawyers fighting to avoid liability over data breaches. Then she trapped Zuckerberg on the issue of the mental health harms of being a Facebook content moderator that reviews horrific and graphic violence.

“Would you be willing to commit to spending one hour a day for the next year, watching these videos and acting as a content monitor and only accessing the same benefits available to your workers?,” she asked. “I’m not sure that would serve our community for me to spend my time,” Zuckerberg said. “What you’re saying is you’re not willing to do it,” she replied.

Rep. Katie Porter challenges Mark Zuckerberg to work as a content moderator and view the same violent, disturbing videos Facebook contractors do https://t.co/iVB9nAcvHO pic.twitter.com/TfPuXkiJp8

— Bloomberg Technology (@technology) October 23, 2019

There’ll be more major launches from Facebook that could raise questions about its impact on society, Zuckerberg revealed. “Later this week we actually have a big announcement coming up on launching a big initiative around news and journalism, where we’re partnering with a lot of folks to build a new product that’s supporting high-quality journalism.” Facebook plans to launch a News section featuring headlines from top outlets, though only some will be paid.

“I think that there’s an opportunity within Facebook in our services to build a dedicated surface, a tab within the apps for example, where people who really want to see high quality curated news, not just social content . . . I’m looking forward to discussing that in more length in the coming days.” That service is sure to trigger debates about whether Facebook is trustworthy enough to be a formal conduit for news.

Overall, the questioning today was much more intelligent than the vague and easily-Googleable queries launched at Zuckerberg by Congress in April 2018. We had no “Senator, we run ads” moments. Instead, it was Zuckerberg who repeatedly used the separation between Facebook and the Libra Association plus the fact that Libra’s policies are still being defined to avoid giving many substantial answers. Combined with the short five-minute Q&A period per member of Congress, Zuckerberg was often able to just repeat existing talking points.

WASHINGTON, DC – OCTOBER 23: Facebook co-founder and CEO Mark Zuckerberg testifies before the House Financial Services Committee in the Rayburn House Office Building on Capitol Hill October 23, 2019 in Washington, DC. Zuckerberg testified about Facebook’s proposed cryptocurrency Libra, how his company will handle false and misleading information by political leaders during the 2020 campaign and how it handles its users’ data and privacy. (Photo by Chip Somodevilla/Getty Images)

In one of the few lighthearted moments of the day, Rep. Juan Vargas recognized the tough position Zuckerberg has gotten himself into. “It’s good to have someone that’s sturdy and resilient. You’re probably the right person at the right time to take this beating.” Yet Rep. McHenry depressingly concluded that, after six hours, “I’m not sure we’ve learned anything new here.”

The question is what array of Libra and Facebook executives would Congress need to have testify together to get real answers to critical questions about how to keep the two from harming the global economy.

The hearing is ongoing and we’ll continue to update this article with major take-aways.

Powered by WPeMatico

South Korean startup True Balance, which operates an eponymous financial services app aimed at tens of millions of users in small cities and towns in India, has closed a new financing round as it looks to court more first-time users in the world’s second largest internet market.

True Balance said on Tuesday that it has raised $23 million in its Series C financing round from seven Korean investors — NH Investment & Securities, IBK Capital, D3 Jubilee Partners, SB Partners, Shinhan Capital and existing partners IMM Investment and HB Investment.

TechCrunch reported earlier this year that True Balance — which has raised $65 million to date, including the $38 million that it closed in its previous financing round — was looking to raise as much as $70 million in its Series C round.

True Balance began its life as a tool to help users easily find their mobile balance, or top up pre-pay mobile credit. But in its four-year journey, its ambition has significantly grown beyond that. Today, it serves as a digital wallet app that helps users pay their mobile and electricity bills, and offer credit to customers so that they can pay later for their digital purchases.

The startup says it has amassed more than 60 million registered users in India, most of whom live in small cities and towns — or dubbed India 2 and India 3. Most of these users are coming online for the first time and True Balance says it has an army of local agents — who get certain incentives — to help first-time internet users understand the benefit of online transactions and start using the app.

True Balance says it clocks more than 300,000 digital transactions on its app each day. The startup, which recently introduced e-commerce shopping services on its app to sell products like smartphones, has clocked $100 million in GMV sales in the country to date.

Charlie Lee, founder of True Balance, said the startup will use the fresh capital to bulk up the offerings on the app. Some of the features that True Balance intends to add before the end of this fiscal year include the ability to purchase bus and train tickets, digital gold and book cooking gas cylinders.

True Balance will also expand its lending and e-commerce services, Lee said. Its lending feature was used 1 million times in three months when it was introduced earlier this year. “We aim to strengthen our data and alternative credit scoring strategy to provide better financial services to our target — the next billion Indian users. Our goal is to reach 100 million digital touch points and become one of the top fintech companies in India by 2022,” he added in a statement.

Even as more than 600 million users in India are online today, just about as many remain offline. In recent years, many major companies in India have started to customize their services to appeal to users in India 2 and India 3 — who also have limited financial power.

Powered by WPeMatico