Earnings

Auto Added by WPeMatico

Auto Added by WPeMatico

Verizon just released its first quarter earnings report, with earnings per share that came in significantly ahead of analyst expectations, while revenue was right in line with predictions.

The company reported EPS of $1.22 per share (or $1.20 when adjusted to exclude a 2 cent benefit due to a pension re-measurement triggered by its recent voluntary redundancy program) and revenue of $32.1 billion, which was up 1.1 percent year-over-year. Analysts had predicted EPS of $1.17 and revenue of $32.15 billion.

Verizon also saw 61,000 net additions to its postpaid retail wireless business, including 174,000 net additions on the postpaid smartphone side.

The Verizon Media division (which owns TechCrunch) reported revenue of $1.8 billion, down 7.2 percent year-over-year. The company blames this decline on falling desktop ad revenue.

The report comes as Verizon begins its 5G rollout in Chicago and Minneapolis, with the company saying that the 5G network buildout was part of its $4.3 billion in capital expenditures.

“2019 is shaping up to be an exciting year for Verizon,” said chairman and CEO Hans Vestberg in a statement. “We are leading the world in the development of new technologies with the launch of our 5G Ultra Wideband network. Our ambition remains unchanged to provide the most advanced next-generation networks in the world.”

As of 8am Eastern, Verizon shares are up 0.72 percent in pre-market trading.

Powered by WPeMatico

Extra Crunch offers members the opportunity to tune into conference calls led and moderated by the TechCrunch writers you read every day. This week, TechCrunch’s Kirsten Korosec and Kate Clark led a deep-dive discussion into Lyft’s IPO and the outlook for the business going forward.

After skyrocketing nearly 10% on its first day hitting the public markets, Lyft stock has faded back down towards its IPO price as some investors grow more concerned over the company’s path to profitability (or lack thereof) and the long-term fundamentals of the business. But Lyft’s public listing is bigger than just the latest in increasingly common unicorn IPOs. As the first public “transportation-as-a-service” company, Lyft offers the first inside glimpse into the business model and its economics, and its development may ultimately act as the canary in the coal mine for the future of transportation.

“Lyft, hasn’t just survived, they’ve grown. 18.6 million people took at least one ride in the last quarter of 2018. That’s up from 16.6 million in late-2016. That illustrates the growth that the company has had. They’ve also said that they have 39% share of the ride-sharing market in the US. That’s up from 22% in 2016.

To me, the big question is let’s say they had Uber’s share, which is 66%, would they be able to make a profit? Is that the determination? And I’m not convinced that it is, which is why all these other aspects of the transportation-as-a-service business model [micromobility, AVs, etc.] are going to be really important.”

Image via Getty Images / Mario Tama

Kirsten and Kate dive deeper into what the market response to Lyft means for Uber and the timeline for its impending IPO. The two also elaborate on their skepticism of ride-hailing economics and debate which innovative transportation model will ultimately drive the path to profitability for Lyft, Uber and others.

For access to the full transcription and the call audio, and for the opportunity to participate in future conference calls, become a member of Extra Crunch. Learn more and try it for free.

Danny Crichton: Good afternoon and good morning everyone this is Danny Crichton, executive editor of Extra Crunch. Thanks so much for joining us today with TechCrunch reporters Kate and Kirsten.

I’ll start with a quick introduction for our two writers today. We have Kate Clark, our venture capital reporter. Kate has been with us for a while now covering everything in the startup and venture world. She’s also one of the hosts of TechCrunch’s podcast Equity and also writes our Startups Weekly newsletter.

Our other writer today is Kirsten, our intrepid automotive writer covering all things Elon Musk, Tesla, and everything else in the autonomous vehicle space. Kirsten has also been with us for quite some time and also writes a newsletter that she just introduced in the last couple of weeks, around transportation. So with that, I’m going to hand off the conversation to the two of them now.

Kirsten Korosec: Thanks so much Danny. This is Kirsten Korosec here. The newsletter is in a bit of a soft launch but it is being published Fridays and we hope to have an email subscription coming sometime in the future, so just keep an eye out for that.

I should also mention I too have a podcast centered around autonomous vehicles and future transportation called The Autonocast that comes out weekly. Thanks so much for joining the call and just a reminder, we want participation. So at about the halfway point, we’ll turn and open up the line and answer questions. Let’s get started.

Before we dig into all the hot takes out there, I think it’s worth providing a primer of sorts — a general timeline of events. We all probably know Lyft of course and most of us think of 2012 as the launch date when it came to San Francisco, but really Lyft was build out of the service of Zimride. Which is the ride-sharing company that John Zimmer and Logan Green founded in 2007.

A lot of attention has been placed on Lyft in 2018 with what happened in the past year, in the run-up to the IPO. But I think it is worth noting the intense activity and growth that happened between 2014 and 2016. These are critically important years for Lyft, just a frenzy of activity in a period where the company gained ground, investors, and partners.

To showcase the amount of activity that was happening; Lyft had two separate funding rounds, one for $530 million another for $150 million, just two months apart in 2015. You might also recall in early-2016 its partnership with GM and the automakers’ $500 million dollar investment as part of the Series F $1 billion dollar fundraising effort.

That was really interesting because GM’s president at the time Dan Ammann took a seat on the board, which he has since vacated. As Lyft and GM started realizing that they were competitors. Now, Dan is the CEO of GM Cruise which is the self-driving unit of GM.

2017 and 2018 were also big years, as Lyft launched their first international market in Toronto. They made big moves on the autonomous vehicle front, which we’ll talk about today, and in micromobility. Their scooter business launched in Denver in 2018. They bought Motivate, which is the oldest and largest electric bike share company in North America. Then, we finally get to the end of 2018, and this is when Lyft confidentially files a statement with the FDC and we’re off with the races to the IPO.

The last two months or three months is when Lyft unveiled its prospectus, met with investors, priced its IPO and made its public debut. So Kate what are the nuts and bolts of the IPO and what’s happening right now?

Kate Clark: Hi everybody this is Kate. So I’m just going to mention really quickly the timeline these last couple of months in the run-up to Lyft’s highly historical IPO. So going back to December, that’s when Lyft initially filed confidentially to go public. We later find out that they are going public on the NASDAQ when they eventually unveiled their S1 in early March.

This is after Lyft had raised $5 billion in debt and equity funding at a $15 billion dollar valuation, so there are a lot of people paying attention to what was the first ever rideshare IPO. So then in early-March, we’re able to get a closer look at Lyft’s S1, which tells us that the company has $911 million in losses in 2018 and revenues of $2.2 billion. So after calculating and pulling together some data, a lot of people were quick to find out that that means Lyft has some of the largest losses ever for any IPO. But also has some of the largest revenues ever for any pre-IPO company, just following Google and Facebook in that category.

So this is a really interesting IPO for a lot of people given these sky-high losses but also these huge, huge revenues. The next we see Lyft price their IPO between $62 and $68 dollars a share. Some people were quick to say that that was maybe a little underpriced, given that this was a highly anticipated IPO with a ton of demand. So on the second day of Lyft’s roadshow, the process, they say that their IPO is oversubscribed. So demand is apparently huge, their oversubscribed, so they decide we’re going to increase the price of our shares.

Image via GettyImages / maybefalse

So Lyft then says they gonna charge a max of $72 per share and then on the day of their IPO they charge $72 per share, the next day opening at $87 per share. So we see a huge IPO pop that I don’t think was particularly surprising given that they already spoke of this demand, and we had already known that there was a lot of demand on Wall Street. Not just for Lyft but just for unicorn IPO’s of this stature, given that there are so few of these. So Lyft began trading hitting $87 per share though, if you’ve been following the news that’s not were Lyft is today.

Kirsten: Yeah so I was just about to ask — Kate give me the latest numbers, you know a lot of focus is on that opening day but things haven’t exactly sustained. So what’s happened in the past few days?

Kate: Yeah it’s really tough to manage expectations after an IPO. I mean, I think there has been a lot of criticism towards Lyft now and I think it’s trading below its initial share price. So as I mentioned Lyft opened at $87 per share, it priced at $72, but almost immediately they began trading below that $72 price per share. So they closed Tuesday trading at $68.96 per share. Still boasting a market cap larger than $19 billion. So they’re still significantly valued at more than they were as a private company at $15 billion but it doesn’t look good to be trading below a price per share so quickly.

However, it actually did hit its IPO price for just a minute today, so maybe let’s give it a few more hours and see where it closes. It’s possible that it will sort of jump towards that $72, but it’s still trading quite significantly below that $87.

Kirsten: With IPOs like this, and especially such a high profile one, there’s going to be a ton of attention on share price and on volatility. And so I’m wondering, in your view, what did this first week, or first few days of volatility say to you? What does it say about Lyft’s future and, well certainly, its present?

Kate: Yeah. I mean, it’s hard to say. I think a lot of people were questioning if Wall Street was going to be interested in a company like Lyft that’s extremely unprofitable at this time and has years left before it will reach profitability, if indeed it ever reaches profitability.

So at this point you got to wonder, do some of these investors that did buy Lyft right off the bat, were they really long on Lyft? Because it does look like a lot of those investors have already sold their stock and perhaps weren’t as invested in Lyft’s long-term profitability plan, which involves a lot of very iffy things, like the future of autonomous vehicles, which we’ll talk about later in this call. And there’s a lot of uncertainty there.

But with that said, it’s not uncommon for a stock to experience volatility right off the bat, and you can’t assume the future of that stock price just because of some early volatility.

And we gathered some examples of IPOs where there was some early volatility that did not determine the long term future. So Carvana, for example, which is an online used car dealer in the automotive space, and it did experience volatility at first, with the stock sliding in the first few months but ultimately trended upward.

Kate: So Carvana opened at $13.50 a share, falling below its IPO price, so it didn’t even have the IPO pop. And then in 2018, it hit an all-time high of $65 per share. Today, it’s trading around $58 per share, so that’s ultimately a positive story to be told there.

And then another example on the other side of things is Snap, which actually took four months to dip beneath its 2017 IPO price, and we all know Snap has definitely not been a success story and it’s trading well below its offer price. But then finally, Facebook, for example, dropped below its IPO price on its second day of trading and then actually had a rough first year on the stock market before the stock ultimately took off and became a very obvious success.

Kirsten: So, Kate, I’m wondering why you think that there was that initial run up on that first day. Was it excitement? Was there something material that was pushing the price up? What was the cause?

Kate: I think there was a lot of excitement and demand around this IPO because it was very much one-of-a-kind, and there were a lot of investors that it seemed were really long on the possibility of Lyft becoming this hugely profitable company. And I think a lot of that was because in the S1, although you did see these really, really big losses — quite major, just ridiculously huge losses — you did see that they were shrinking over time and that there was definitely a path in which Lyft could take where it would reach profitability, say, in the next five years.

And I think Wall Street was really paying attention to that, and they were not paying attention to some of the other metrics. Now, they’ve taken off their rose-colored glasses and they’re looking at Lyft as a public company, and it’s just a little bit different now that it’s actually completed its debut.

Kirsten: Well, so, I mean, I like to view IPOs often times, and especially in Lyft’s case, as a measure of an investors’ faith in the company’s growth prospects, because this is a company that while it does have quite a bit of revenue, it has significant losses and it’s really planning not just for the present day but for the future. It’s been called a disruptive business for a reason, and it is certainly very forward-looking. So I’m wondering if you think it was a good strategy for Lyft. They wanted to open it up to “the everyman” when they actually went to market. They did a different approach, and do you think this might have had an effect? I mean, it’s very on-brand for them to do this, but I’m wondering if you thought that means that some of the investors aren’t as disciplined.

Kate: Do you mean with the fact they were providing bonuses to their employees and drivers to actually participate in the IPO as well?

Kirsten: Absolutely. That’s actually a really good point that maybe you can elaborate on. Lyft did a little bit of a more open approach for its IPO. Typically IPOs can be closed off to only large, institutional investors. So did this set them up perhaps to have more volatility?

Kate: Yeah, Lyft provided some of their drivers up to, I think, $10,000 to, in theory, actually buy stock in the IPO. Do I think that had a high impact? I don’t know. I think there’s not enough comparison, not enough data to really make a decision or to make a hot take on whether that really was part of the volatility. I think just given the uncertain nature of Lyft’s future and their big losses, I think their volatility was pretty inevitable, and I think people paying attention to this are probably not particularly surprised by how the stock has fared in these first couple days.

And I do want to add there’s this six-month lock-up period for the venture capital funds that own Lyft and as well as their employees, so I think we’re not sure what’s going to happen when that lock-up period ends and those holders can just sell their stock right then or how that will impact the stock price, as well.

Image via TechCrunch/MRD

Kirsten: So something to keep an eye on. It reminds me a lot of a company I write a lot about, which is Tesla, and I’ve been covering them for years. And it’s one of the most volatile stocks, and their investors, they certainly have large, institutional investors, but the number of fanboys that they have with smaller investors, either prop up the share price sometimes or add to that volatility, and I’m kind of really curious to see if that happens with Lyft. If you go to a shareholder meeting at Tesla, for example, it’s filled with people who are passionate about the brand and its CEO, Elon Musk.

And Lyft and possibly Uber, if they end up finally going through with their IPO, you can see that potentially happening because people feel very strongly about the brand and also the service it provides. So I’m curious to see how this all sort of shakes out. And I tend to take the view that I invest personally in mutual funds and things like that. I don’t invest in any of these companies, but the long, patient view tends to be the better one, and trying to catch a falling knife, as investors have told me, is never really a good idea.

So I’m curious to see if investors sort of grow up and learn with Lyft, if they’ll become disciplined and just sort of wait it out and see them play out the growth prospects for the company in the long term. So, we’ve been talking about Lyft and I can’t not talk about Uber as a result. I’m wondering what you think this might mean for Uber. The big story initially was let’s beat Uber to IPO and I’m wondering what this means then. Is this indicative of what Uber is going to experience?

Kate: I think that question is really at the top of everyone’s mind right now, including my own. I will say that I still do think it was highly beneficial for Lyft to get out first. Because imagine if and when Uber does too experience volatility, which it probably will, if it were to have gone first, I think that would have frightened Lyft a lot more than Lyft’s volatility may or may not be frightening Uber. So, with that said, I think I’m of two minds right now with my thoughts on how this impacts Uber’s IPO. I think that if Lyft stock continues to be volatile and perhaps even falls lower than it already has. I do think that there is a chance Uber may ultimately decide to push its IPO back.

I think that for a few reasons, namely being that Uber is not in a huge rush to go public. They do have the ability to wait. They have filed to go public. So it’s likely to happen quite soon, but it may not happen in April as they are reportedly planning to do.

On the other hand, Lyft went public at like a $24 or $25 billion dollar market cap. Whereas Uber is going to debut at maybe a $120 billion dollar initial market cap. So these IPOs, although they are both ride hail IPOs and they are very similar companies in a lot of ways, they’re also very different and Uber is operating on an entirely different scale though it still is unprofitable. And has some of the same issues that, investors are probably noting about Lyft.

I think it’s either going to be that it’s maybe that they do decide to push it back or maybe that Uber is like, well we’re five times larger, six times larger. We have much larger statistics to show to investors. There’s just a chance it could go either way. I wish I had a better, more concrete answer, but I just don’t think we know yet.

Kirsten: Well I’m okay with not taking hot takes just a few days into this IPO. I think this is a good time to open it up to questions. While we wait for a question, I will do one quick follow up with you Kate. What do you think this means for Uber? Will it delay its IPO?

Kate: Right now, no, I don’t think they’re going to. But it’s like I said, it’s tough to say given that it’s only been a few days of Lyfts IPO. But no, I think you’ve got to imagine that they are ready to discuss the possibilities of Lyfts IPO and already planned ahead if there was volatility. They maybe already assumed that would happen, given that that’s not uncommon. So right now I’m going to say no, I don’t think they’re going to delay, but it’s certainly still a possibility.

Kirsten: Okay, great. I think another really interesting piece for Uber was their acquisition of Careem. This is a deal that was made right before their IPO, so it was shifting attention away from Lyft, just for a moment.

Why did Uber do this? Is this not a signal that they’re delaying their IPO? Is this just prepping for it? What are you hearing on it? I’m wondering if this might have just been a strategy to show the world investors, specifically potential shareholders, what the road ahead is going to look like. Or is it some other reason — Is it to justify their really big losses?

Image via Careem / Facebook

Kate: I think it’s the latter two things you said. Just to give some background Uber is paying about $3.1 billion to acquire Careem, which is a Middle Eastern ride-hailing company. So basically just the Uber of the Middle East. Uber does have a history of acquiring, smaller competitors like this in different markets where it’s not active, just as a way for Uber to quickly grow essentially.

So I do think it’s a big deal to make just before going public. So I guess we don’t know if they necessarily will go public in April, but I think it was a move to present to public market investors as a prep for an IPO, to show “we just acquired this company, here’s more evidence of future growth”. Like you mentioned, it’s definitely a justification of those huge losses that we know Uber has.

Kirsten: Thanks for that. Questions?

Caller Question: Hi there, so when we talk about looking ahead and moving towards profitability — what role, if any, do you think the acquisition of a scooter or other mobility companies will have for companies like Lyft and Uber?

Kirsten: That’s a great question. I think it’s going to be a huge piece of both of their businesses. A lot of people describe this as the first ride-hailing IPO. We need to stop calling this a ride-hailing company. These are transportation-as-a-service companies and they’re making money. But generating revenue as opposed to making profit is a totally different thing. When you start talking about ridesharing, it’s a tough business. With those it’s an asset-light business, right? They don’t own the cars and then they technically don’t employ these drivers.

But at the same time, as of 2016 only something like 1% of people in the US were using rideshare. So you see this opportunity, but they’re not pushing forward. There is a ton of car ownership still that’s happening. Yes, sharing has absolutely increased, but 17 million new cars were sold in the US last year. So scooters, bike share and other businesses are going to be key to their paths to profitability because ride-sharing alone is just difficult to make a profit. It’s not difficult to generate revenue. It’s difficult to make a profit on.

And I’m wondering, talking about that road to profitability, I do think it’s worth noting how much they have grown. Lyft, hasn’t just survived, they’ve grown. 18.6 million people took at least one ride in the last quarter of 2018. That’s up from 16.6 million in late 2016, that illustrates the growth that the company has had.

They’ve also said that they have 39% share of the ride-sharing market in the US. That’s up from 22% in 2016. To me, the big question is let’s say they had Uber’s share, which is 66%, would they be able to make a profit? Is that the determination? And I’m not convinced that it is, which is why all these other aspects of the transportation-as-a-service business model are going to be really important.

Kate: I think what you pointed out is important, about Lyft and Uber both becoming transportation businesses, not ride-hailing companies and I think their long-term visions involve scooters, bikes, autonomous vehicles, all sorts of different models of transportation beyond just car sharing.

Kirsten: I hate to be wishy-washy here and say, I don’t know, but I do really think that it’s going to come down to a variety of items all coming together. It’s just not going to be enough for Lyft to scale up its ride-hailing business. And I should point out that Uber should be treated in some ways the same way, but there are some distinct differences. But it’s important for us to think of Lyft as a transportation-as-a-service business. I mean they say in their prospectus that transportation is a massive market opportunity. The hard part of course is turning that into a profit. There might be opportunity there.

So there’s this asset-light business that they have right now, which is the ride-hailing, but then they are making acquisitions in the micromobility space and that is going to become more capital intensive. And that’s going to force them to change their business. And then there’s the autonomous vehicle piece. And then finally, I actually think that one of the pieces of their S1 that has really not received much attention at all is what they’re pursuing in terms of public transportation. And they have said that they, and Uber, intend on being a piece of the public transit ecosystem.

Now that doesn’t mean that they’re going to necessarily be operating buses, but there are people that I’ve talked to in the industry who actually feel like, in Uber’s case, they want to control every mode of transportation. For Lyft, I see them seeing more of the opportunity financially with the data piece and becoming more of a platform and becoming that one-stop shop where you use an app to figure out if you want to use the scooter or a bike, or ride-hailing or buy that ticket for the L in Chicago or the Bart System.

So I really think that the public transit piece often gets ignored and cities are having so much more control now and weighing in. We see this in New York City with congestion pricing. It’s going to force Lyft and Uber to take advantage of these opportunities and use their platform in a way that perhaps accelerates faster than they had intended.

Kate: I’m very interested in the public transportation element, but I’m also very skeptical of the scooters and bikes in the future for Lyft, I think, given the unit economics, I certainly wouldn’t rely on them to be Lyft’s path to profitability. I think autonomous vehicles are a much more interesting path towards profitability. So a lot of companies, Uber, Lyft, Waymo and more are focusing on autonomous vehicles and their development, whether that be with hardware or software. How does Lyft’s strategy with autonomous vehicles differentiate from some of their competitors or does it does differentiate?

Kirsten: It does differentiate, and the funny thing is, is that so you don’t see micromobility necessarily as the oath to profitability and are interested in AVs and I write about AVs, but I see that AVs as a harder path to profitability in a way because of the nuts and bolts that it takes to develop them.

So just to weigh in really quickly on the micromobility piece and then I’ll move on to AVs; To show the opportunity but also the volatility in a real-world example for micromobility, I was in Austin for South by Southwest, I think you were there too, and you probably saw scooters everywhere, right? 18 months ago there were no scooters or bike share in the city. Then bike share came first.

Image via Flickr / Austin Transportation / https://www.flickr.com/photos/austinmobility/41536051644/in/album-72157669223418248/

And I was talking to that mayor of Austin and one of the folks from Spin, which is a Ford owned business, and they told me something that was really remarkable that I hadn’t thought about, which was that scooters were disrupting the bike share business. So bikes share came in and then scooters came in and all of a sudden they’re pulling bikes off the streets because no one was using them or were not using them at the same level as scooters.

Lyft is going to go through these same exact growing pains and people are figuring out what works. And as you mentioned, the unit economics are an issue, the wear and tear on the scooters alone is driving up costs and driving down revenues certainly, but pretty much making it very difficult to make a profit on it.

But that’s a near term business, right? So it’s at least generating revenue right now. On the other hand, you have this other piece, which is the AV piece. Lyft is doing some really interesting things on the AV piece — they kind of have a two-prong approach.

So they basically created a ton of partnerships to use their platform. So this started a couple of years ago and companies like Aptiv, drive.ai, even Waymo and nuTtonomy, which Aptiv just recently bought about a year ago and GM, and Lyft basically allows developers to use their platform and connect to their autonomous vehicle and offer these rides.

And the best example of this, if you’ve been to CES or if you have been to Las Vegas I should say more specifically, is this partnership that Lyft has with Aptiv — and Aptiv as a tier one supplier, they used to be called Delphi, they spun out, they bought nuTonomy, and they’re Aptiv now. And this is taking Aptiv automated BMW, which are on the Lyft network. If you hail a ride, you might be asked if you want a self-driving car, or “are you okay with a self-driving car?” And they have a safety driver, no humans have been pulled away from it yet. But they provided about 35,000 rides since I want to say January 2018.

Then they’re also doing Level 5, a dedicated self-driving vehicle division that launched in 2017. And here they’re basically creating an open self-driving system or open SDS. On top of that, they have partnered with Magna, an auto parts producer, to develop these self-driving systems that can be manufactured at scale.

And so you just see a rush of partnerships and sort of dual approaches and all of that costs a lot of money. And I can’t emphasize the amount of money that it costs or will cost to develop these systems and deploy them commercially. And I hear from other companies figures like $5 billion to get self-driving vehicles. So developing the full stack, doing fleet management, maintenance, all of that — that’s a lot of money. And, I’m not sure where Lyft, will get that capital, will they get it from the open market or will they have to go and ask for more capital.

Kate: So when do you think then that Lyft will be able to commercialize autonomous vehicles?

Kirsten: The timeline? So depending on who you talk to, you can hear from any of these developers between five years and 30 years. I think it’s important to talk about language and how we talk about autonomous vehicles. So to be clear, there is currently not a single commercial autonomous vehicle deployment where a human being or safety driver has been pulled away from the wheel. It just doesn’t exist.

There are plenty of pilots and Waymo is probably considered the leader in that list, though it is a bit of a confusing one for me because they have so many partnerships and they’ve become competitors to some of those partnerships. The analogy I use is “Survivor,” the reality show. Everyone wants to make these alliances so they don’t get voted off the island.

And now we’re at that point where autonomous vehicle development has entered what we call the trough of disillusionment, which is heads down, “let’s get away from the hype, let’s do the hard work.” And I think we’re going to see a lot of those partnerships and headwinds really come up in the next year, 18 months. So to put a target date on Lyft, it’s really going to depend on which one of those partnerships really play out and are real. I think the one with Aptiv seems the most real to me based on what I know the company is doing and I can see them doing a lot more pilots in the next 18 months.

Does that mean commercial deployment without a human safety driver behind the wheel? I’m not sure I can see a lot more these pilots with a human safety driver expanding beyond Las Vegas. I see pilots happening absolutely in the next year to 18 months. The issue is going to be when is that human safety driver going to be pulled out and with which partner.

Kate: So should we open it up to questions again?

Caller Question: Hi, I was just wondering how we should think about the regulatory risks that might exist as these companies expand to new cities, new markets, or even the public transport use case you mentioned. Thanks.

Kirsten: The regulatory piece is an interesting one. Let’s talk about ride-hailing first. We’ve already seen the regulatory environment, in cities, push back against companies like Uber and Lyft. I think the congestion pricing model that just launched in New York City is going to be one to watch and could be something that will put pressure on, on businesses like Lyft.

Kate: I agree and just to speak, quickly on the scooters; I think the narrative around scooters has been pretty dominated by how cities have forced them out or cities push these strict regulatory barriers on them. And I think that’s still playing out very much. There are even some scooter providers that have had to pull out of cities that they worked very hard to get into in the first place. So I think that has slowed down some of the growth there. And given that Lyft has micromobility as such a key part of their road to profitability, I think that’s partially why I am a little bit skeptical of how that’s gonna play out.

Kirsten: One thing we’ve found, and something to consider for Uber as well, in the future, if any of these AV developers end up, filing for IPOs on their own — there’s been chit chat about Waymo someday doing that or GM cruise someday— the implications for all of these companies and their relationship with cities should not be ignored or undervalued.

And I think you see a bit of that playing out with the present day track we have, which is the ride-hailing scooters and bike share cities and transit agencies or the DOT of different counties finding that they are in a more powerful position than they’ve ever been before. And they are exerting that power.

And so you will see instances like Los Angeles where they have put forth a mandatory data sharing component if you want to operate in their city. This raises some privacy concerns by the way, but it also adds another cost to a company or certainly forces them to look at their business a little bit differently.

Then you start talking about AVs and where are they will operate, how they will operate, where are they will park, what type of vehicle will be allowed in the urban center. In places like Europe, there are strict emissions rules, so that’s going to go to an AV or hybrid profile. And it’s important to think about what that regulatory framework might be and acknowledge the fact that it’s really a mishmash.

There are voluntary guidelines on the federal level right now, but there were no mandates. And so it’s really left up to the cities, counties and states to decide how an AV might be deployed. It’s going to mean probably more lobbyists in DC working with federal folks to ensure that their business doesn’t get hamstrung as a result as well as more of a presence in those cities and states and counties.

But Kate, I’m wondering what is your view from a startup perspective? Do you think of Lyft as a startup anymore are they acting like a startup or are they acting like a company that could handle all of these different complicated, various challenges? I mean, we’ve got pricing pressure, regulatory pressure or you’ve got AV development, opportunities with scooters and all this other stuff. So are they acting like a company that is able to handle this?

Image via Getty Images / Jeff Swensen

Kate: That’s an interesting question. I mean, they’re definitely not a startup anymore by, by anybody’s definition. You maybe could have still used that word, if they were still private, but even then, I know many people would yell at you for using that term for a company worth $15 billion. But now it’s a public company. It’s not a startup. I don’t think they’re acting like a startup, no. I think that they are mature in the way that they’re handling all of these different, so-called paths to profitability.

But we need to wait and see. Let’s see how this year goes, let’s see how they handle all the criticism that they’re going to undoubtedly take from Wall Street or from everyone who’s either interested in buying or just taking a seat and watching how the stock favors and then we’ll know what kind of lessons they took from all those years as a private company. Then we can decide if their behavior is really that of a mature public company.

Kirsten: I do want to make one point that I think is an interesting one on Lyft’s strategy versus Uber is in terms of AVs. Let’s all put a big asterisk that says no, AVs are still a ways out. It is important to note the Lyft and Uber’s strategies for AVs are wildly different and Uber does not take this dual approach. Uber is throwing a ton of capital towards developing their own, self-driving stack and also they’ve done, some acquisitions as well.

They’ve also had quite a bit of trouble. Last year Uber had the first self-driving vehicle fatality that happened in Tempe, Arizona, which looked like it was going to derail their self-driving unit, but it did not. They’re back, testing in a very limited way, but Lyft’s is all about what they call the democratization of autonomous vehicles.

And we can look at that as marketing speech, but I do think that it’s important to look at those words because it shows what their business model is. Their business model is partnerships, alliances, opening up the platform and casting the widest net possible. What I’m very interested to find out is which approach will end up being the winner. It’s going to be a very long game. It’s not going to be anything that’s going to be determined in the next year. I think what Lyft’s proven is that when they look like they’re down and out, they come back.

We’ll see what the better approach is. Do you do everything in-house and launch your own robo-taxi service? Or take capital partners on or do the Lyft approach, with multiple partners? Are partnerships actually too complicated? As someone who covers the startup world, do you have a thought on which one might work or not?

Kate: I have no idea which will work better and I’m sort of excited to see where this all goes, especially as Uber and Lyft are now going to be public.

That’s a good spot to end the call on.

Kirsten: Thanks so much for joining. Thanks again for being Extra Crunch subscribers, we really appreciate it. Bye everyone.

Powered by WPeMatico

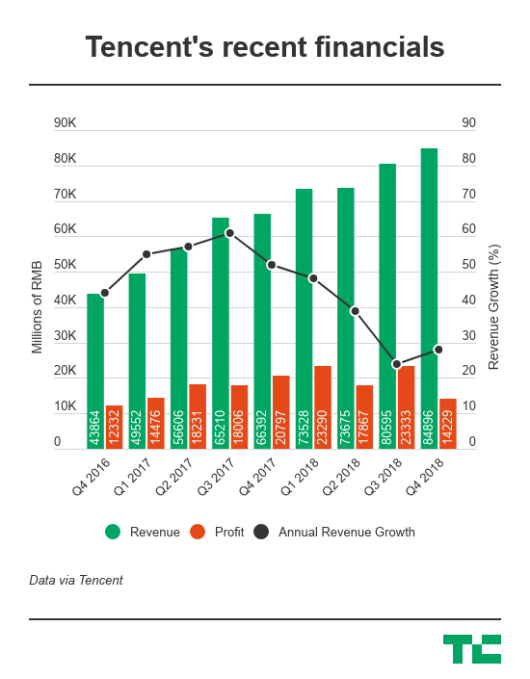

China’s Tencent reported disappointing profits in the fourth quarter on the back of surging costs but saw emerging businesses pick up steam as it plots to diversify amid slackening gaming revenues.

Net profit for the quarter slid 32 percent to 14.2 billion yuan ($2.1 billion), behind analysts’ forecast of 18.3 billion yuan. The decrease was due to one-off expenses related to its portfolio companies and investments in non-gaming segments like video content and financial technology.

Excluding non-cash items and M&A deals, Tencent’s net profit from the period rose 13 percent to 19.7 billion yuan ($2.88 billion). The company has to date invested in more than 700 companies, 100 of which are valued over $1 billion each and 60 of which have gone public.

Quarterly revenue edged up 28 percent to 84.9 billion yuan ($12.4 billion) beating expectations.

The Hong Kong-listed company is best known for its billion-user WeChat messenger but had for years relied heavily on a high-margin gaming business. That was until a months-long freeze on games approvals last year that delayed monetization for new titles, spurring a major reorg in the firm to put more focus on enterprise services, including cloud computing and financial technology.

Tencent has received approvals for eight games since China resumed the licensing process, although its blockbusters PlayerUnknown Battlegrounds and Fortnite have yet to get the green light. The firm also warned of a “sizeable backlog” for license applications in the industry, which means its “scheduled game releases will initially be slower than in some prior years.”

Video games for the quarter contributed 28.5 percent of Tencent’s total revenues, compared to 36.7 percent in the year-earlier period. Despite the domestic fiasco, Tencent remains as the world’s largest games publisher by revenue, according to data compiled by NewZoo. The firm has also gotten more aggressive in taking its titles global.

Social network revenues rose 25 percent on account of growth in live streaming and video subscriptions. The segment made up 22.9 percent of total revenues. Tencent has in recent years spent heavily on making original content and licensing programs as it competes with Baidu’s iQiyi video streaming site. Tencent claimed 89 million subscribers in the latest quarter, compared with iQiyi’s 87.4 million.

Tencent has been relatively slow to monetize WeChat in contrast to its western counterpart Facebook, though it’s under more pressure to step up its game. Tencent’s advertising revenue from the quarter grew 38 percent thanks to expanding advertising inventory on WeChat. Ads accounted for 20 percent of the firm’s quarterly revenues.

All told, WeChat and its local version Weixin reached nearly 1.1 billion monthly active users; 750 million of them checked their friends’ WeChat feeds, and Tencent recently introduced a Snap Story-like feature to lock users in as it vies for eyeball time with challenger TikTok.

The “others” category, composed of financial technology and cloud computing, grew 71.8 percent to generate 28.5 percent of total revenues. WeChat’s e-wallet, which is going neck-and-neck with Alibaba affiliate Alipay, saw daily transaction volume exceed 1 billion last year. During the fourth quarter, merchants who used WeChat Pay monthly grew more than 80 percent year-over-year.

Meanwhile, cloud revenues doubled to 9.1 billion yuan in 2018, thanks to Tencent’s dominance in the gaming sector as its cloud infrastructure now powers over half of the China-based games companies and is following these clients overseas. Tencent meets Alibaba head-on again in the cloud sector. For comparison, Alibaba’s most recent quarterly cloud revenue was 6.6 billion yuan. Just yesterday, the e-commerce leader claimed that its cloud business is larger than the second to eight players in China combined.

Powered by WPeMatico

Razer is summoning a big gun as it bids to develop its mobile gaming strategy. The Hong Kong-listed company — which sells laptops, smartphones and gaming peripherals — said today it is working with Tencent on a raft of initiatives related to smartphone-based games.

The collaboration will cover hardware, software and services. Some of the objectives include optimizing Tencent games — which include megahit PUBG and Fortnite — for Razer’s smartphones, mobile controllers and its Cortex Android launcher app. The duo also said they may “explore additional monetization opportunities for mobile gaming,” which could see Tencent integrate Razer’s services, which include a rewards/loyalty program, in some areas.

The news comes on the same day as Razer’s latest earnings, which saw annual revenue grow 38 percent to reach $712.4 million. Razer recorded a net loss of $97 million for the year, down from $164 million in 2017.

The big-name partnership announcement comes at an opportune time for Razer, which has struggled to convince investors of its business. The company was among a wave of much-championed tech companies to go public in Hong Kong — Razer’s listing raised more than $500 million in late 2017 — but its share price has struggled. Razer currently trades at HK$1.44, which is some way down from a HK$3.88 list price and HK$4.58 at the end of its trading day debut. Razer CEO Min Liang Tan has previously lamented a lack of tech savviness within Hong Kong’s public markets despite a flurry of IPOs, which have included names like local services giant Meituan.

Nabbing Tencent, which is one of (if not the) biggest games companies in the world, is a PR coup, but it remains to be seen just what impact the relationship will have at this stage. Subsequent tie-ins, and potentially an investor, would be notable developments and perhaps positive signals that the market is seeking.

Still, Razer CEO Min Liang Tan is bullish about the company’s prospects on mobile.

The company’s Razer smartphones were never designed to be “iPhone-killers” that sold on volume, but there’s still uncertainty around the unit with recent reports suggesting the third-generation phone may have been canceled following some layoffs. (Tan declined to comment on that.)

Mobile is tough — just ask past giants like LG and HTC about that… and Razer’s phone and gaming-focus was quickly copied by others, including a fairly brazen clone effort from Xiaomi, to make sales particularly challenging. But Liang maintains that, in doing so, Razer created a mobile gaming phone market that didn’t exist before, and ultimately that is more important than shifting its own smartphones.

“Nobody was talking about gaming smartphones [before the Razer phone], without us doing that, the genre would still be perceived as casual gaming,” Tan told TechCrunch in an interview. “Even from day one, it was about creating this new category… we don’t see others as competition.”

With that in mind, he said that this year is about focusing on the software side of Razer’s mobile gaming business.

Tan said Razer “will never” publish games as Tencent and others do, instead, he said that the focus is on helping discovery, creating a more immersive experience and tying in other services, which include its Razer Gold loyalty points.

Outside of gaming, Razer is also making a push into payments through a service that operates in Southeast Asia. Fueled by the acquisition of MOL one year ago, Razer has moved from allowing people to buy credit over-the-counter to launch an e-wallet in two countries, Malaysia and Singapore, as it goes after a slice of Southeast Asia’s fintech boom, which has attracted non-traditional players that include AirAsia, Grab and Go-Jek, among others.

Powered by WPeMatico

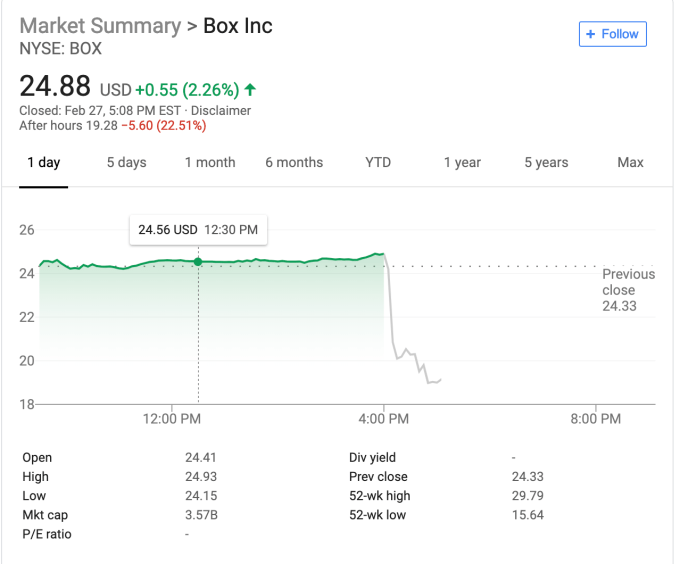

By most common sense measurements, Box had a pretty good earnings report today, reporting revenue up 20 percent year over year to $163.7 million. That doesn’t sound bad, yet Wall Street was not happy with the stock getting whacked, down more than 22 percent after hours as we went to press. It appears investors were unhappy with the company’s guidance.

Part of the problem, says Alan Pelz-Sharpe, principal analyst at Deep Analysis, a firm that watches the content management space, is that the company failed to hit its projections, combined with weaker guidance; a tough combination, but he points out the future does look bright for the company.

“Box did miss its estimates and got dinged pretty hard today; however, the bigger picture is still of solid growth. As Box moves more and more into the enterprise space, the deal cycle takes longer to close and I think that has played a large part in this shift. The onus is on Box to close those bigger deals over the next couple of quarters, but if it does, then that will be a real warning shot to the legacy enterprise vendors as Box starts taking a chunk out of their addressable market,” Pelz-Sharpe told TechCrunch.

This fits with what company CEO Aaron Levie was saying. “Wall Street did have higher expectations with our revenue guidance for next year, and I think that’s totally fair, but we’re very focused as a company right now on driving reacceleration in our growth rate and the way that we’re going to do that is by really bringing the full suite of Box’s capabilities to more of our customers,” Levie told TechCrunch.

Holger Mueller, an analyst with Constellation Research says failing to hit guidance is always going to hurt a company with Wall Street. “It’s all about hitting the guidance, and Box struggled with this. At the end of the day, investors don’t care for the reasons, but making the number is what matters. But a booming economy and the push to AI will help Box as enterprises need document automation solutions,” Mueller said.

On the positive side, Levie pointed out that the company achieved positive non-GAAP growth rate for the first time in its 14-year history, with projections for the first full year of non-GAAP profitability for FY20 that it just kicked off.

The company was showing losses on a cost per share of 14 cents a share for the most recent quarter, but even that was a smaller loss than the 24 cents a share from the previous fiscal year. It would seem that the revenue is heading generally in the correct direction, but Wall Street did not see it that way, flogging the cloud content management company.

Chart: Box

Wall Street tends to try to project future performance. What a company has done this quarter is not as important to investors, who are apparently not happy with the projections, but Levie pointed out the opportunity here is huge. “We’re going after 40 plus billion dollar market, so if you think about the entirety of spend on content management, collaboration, storage infrastructure — as all of that moves to the cloud, we see that as the full market opportunity that we’re going out and serving,” Levie explained.

Pelz-Sharpe also thinks Wall Street could be missing the longer-range picture here. “The move to true enterprise started a couple of years back at Box, but it has taken time to bring on the right partners and infrastructure to deal with these bigger and more complex migrations and implementations,” Pelz-Sharpe explained. Should that happen, Box could begin capturing much larger chunks of that $40 billion addressable cloud content management market, and the numbers could ultimately be much more to investor’s liking. For now though, they are clearly not happy with what they are seeing.

Powered by WPeMatico

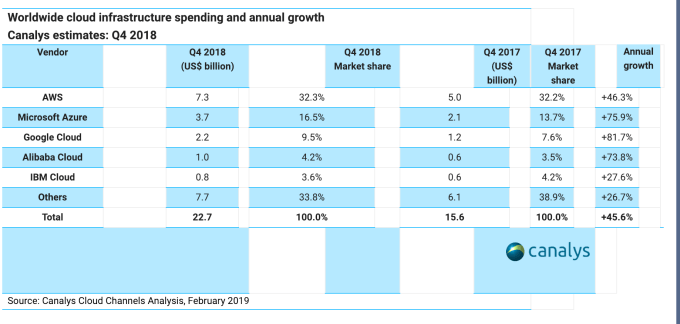

Google has shared its cloud revenue exactly once over the last several years. Silence tends to lead to speculation to fill the information vacuum. Luckily there are some analyst firms who try to fill the void, and it looks like Google’s cloud business is actually trending in the right direction, even if they aren’t willing to tell us an exact number.

When Google last reported its cloud revenue, last year about this time, they indicated they had earned $1 billion in revenue for the quarter, which included Google Cloud Platform and G Suite combined. Diane Greene, who was head of Google Cloud at the time, called it an “elite business.” but in reality it was pretty small potatoes compared to Microsoft’s and Amazon’s cloud numbers, which were pulling in $4-$5 billion a quarter between them at the time. Google was looking at a $4 billion run rate for the entire year.

Google apparently didn’t like the reaction it got from that disclosure so it stopped talking about cloud revenue. Yesterday when Google’s parent company, Alphabet, issued its quarterly earnings report, to nobody’s surprise, it failed to report cloud revenue yet again, at least not directly.

Google CEO Sundar Pichai gave some hints, but never revealed an exact number. Instead he talked in vague terms calling Google Cloud “a fast-growing multibillion-dollar business.” The only time he came close to talking about actual revenue was when he said, “Last year, we more than doubled both the number of Google Cloud Platform deals over $1 million as well as the number of multiyear contracts signed. We also ended the year with another milestone, passing 5 million paying customers for our cloud collaboration and productivity solution, G Suite.”

OK, it’s not an actual dollar figure, but it’s a sense that the company is actually moving the needle in the cloud business. A bit later in the call, CFO Ruth Porat threw in this cloud revenue nugget. “We are also seeing a really nice uptick in the number of deals that are greater than $100 million and really pleased with the success and penetration there. At this point, not updating further.” She is not updating further. Got it.

That brings us to a company that guessed for us, Canalys. While the firm didn’t share its methodology, it did come up with a figure of $2.2 billion for the quarter. Given that the company is closing larger deals and was at a billion last year, this figure feels like it’s probably in the right ballpark, but of course it’s not from the horse’s mouth, so we can’t know for certain. It’s worth noting that Canalys told TechCrunch that this is for GCP revenue only, and does not include G Suite, so that would suggest that it could be gaining some momentum.

Frankly, I’m a little baffled why Alphabet’s shareholders actually let the company get away with this complete lack of transparency. It seems like people would want to know exactly what they are making on that crucial part of the business, wouldn’t you? As a cloud market watcher, I know I would, and if the company is truly beginning to pick up steam, as Canalys data suggests, the lack of openness is even more surprising. Maybe next quarter.

Powered by WPeMatico

Snap has finally begun publicly testing the engineering overhaul of its slow and buggy Android app that for years has cost Snapchat users. Promising early results and reduction in app startup time could help Snapchat fix its growth problem after daily active users sank in Q2 and Q3 before staying put at 186 million in Q4, Snap announced in its earnings report today.

“We ended the year with user engagement stabilizing and have started rolling out the new version of our Android application to a small percentage of our community,” CEO Evan Spiegel wrote. “Early tests show promising results especially on less performant devices, including a 20 percent reduction in the average time it takes to open Snapchat.” The problem is that because “Our engineering team remains focused on rebuilding our Android application,” they haven’t been dedicated to fixing the existing version. That means that despite iOS daily active users and average time spent growing faster than last year, Android dragged Snapchat again to see no total daily user growth.

Interim Chief Financial Officer Lara Sweet noted that, “While we are not going to give specific guidance on daily active users, we are cautiously optimistic and we do not foresee a sequential decline in daily active users in Q1 2019.” It seems Snap believes the new year is going well and the Android rollout could stem losses so it might finally grow its user count again, or at least stop shrinking.

Powered by WPeMatico

Nintendo has cut its ambitious annual Switch sales forecast despite enjoying a strong Christmas Q3 quarter.

The Japanese games giant recorded a 104.21 billion JPY ($958 million) net profit on revenue of 608.39 billion JPY ($5.59 billion) between October and December 2018. Revenue was up 26 percent year-on-year, which is an impressive feature given that quarter was a successful one for Nintendo, yielding its biggest operating profit in a Q3 for eight years.

The Nintendo Switch is now closing down on lifetime sales of the N64. Nintendo shifted a record 9.41 million consoles during the three-month period, up 30 percent annually, to take it to 14.49 million this financial year, which began in April 2018. However, despite a success last quarter, likely helped in no small amount by Christmas, Nintendo has trimmed its ambitious goal to sell 20 million Switch units this financial year. Instead, the target is 17 million, which means it is estimating around 2.5 million sales during January, February and March.

In terms of games, a bunch of new releases performed well in the last quarter. Pokémon: Let’s Go sold million titles since its November release, Super Smash Bros. Ultimate sold 12.08 million since its December launch and Super Mario Party, released in October, reached 5.3 million sales. Total game sales jumped by 101 percent to reach 94.64 million sales during the period.

Nintendo’s retro consoles — the NES Classic and Super NES Classic — sold 5.83 million. But there is bad news for Nintendo loyalists, the upcoming Mario Kart Tour mobile game won’t ship in March — its revised launch date is this summer.

Powered by WPeMatico

Samsung Electronics reported its largest quarterly profit decline in two years during its earnings report today. As the Galaxy maker warned in its earnings guidance earlier this month, its results were hurt by slower-than-expected demand for semiconductors, which had bolstered its earnings in previous quarters even when smartphone sales were slow.

Samsung’s forecast was also dour, at least for the first half of the year. It said annual earnings will decline thanks to continuing weak demand for chips, but expects demand for memory products and OLED panels to improve during the second half.

The company’s fourth-quarter operating profit was 10.8 trillion won (about $9.7 billion), a 28.7 percent decrease from the 15.15 trillion won it recorded in the same period one year ago. Revenue was 59.27 trillion won, a 10.2 percent drop year over year.

Broken out by business, Samsung’s semiconductor unit recorded quarterly operating profit of 7.8 trillion won, down from 10.8 trillion won a year ago. Its mobile unit’s operating profit was 1.5 trillion won, compared to 2.4 trillion won a year ago.

Smartphone makers, including Samsung rival Apple, have been hit hard by slowing smartphone sales around the world, especially in China. Upgrade cycles are also becoming longer as customers wait to buy newer models.

This hurt both Samsung’s smartphone and chip sales, as “overall market demand for NAND and DRAM drop[ped] due to macroeconomic uncertainties and adjustments in inventory levels by customers including data center companies and smartphone makers,” said the company’s earnings report.

Samsung expects chip sales to be sluggish during the first quarter because of weak seasonality and inventory adjustments by its biggest customers. The company was optimistic about the last two quarters of 2019, when it expects demand for chips and OLED panels to pick up thanks to seasonal demand and customers finishing their inventory adjustments.

Powered by WPeMatico

Apple’s Q1 earnings are in, and things don’t look too rosy for the iPhone. Revenue for the handset has declined 15 percent year over year for the quarter. It’s a pretty hefty drop for a device that’s been flying high for so long, but you can’t say Apple didn’t warn us. Earlier this month, Tim Cook noted that the company was lowering its guidance, thanks in no small part to smartphone figures.

In its earlier report, the company put much of the blame at the feet of the Chinese market. There are a lot of factors on that front, including slowing economic growth in the world’s largest smartphone market, and a general trend toward prolonged upgrade cycles, as users are holding onto devices for longer. That’s been a large part of the reason that smartphone sales are down nearly across the board, marking the first contraction of the category since analysts began tracking it.

Last year’s arrival of the XS marked a less dramatic refresh than the iPhone X, but Apple also introduced a new budget handset with the XR. That device has reportedly been a disappointment, though Apple has repeatedly noted that the device has been the best selling iPhone since its October launch.

Notably, those numbers are offset somewhat by growth in other categories. The iPad grew 17 percent on the strength of new models, while Mac/Wearables and Home/Accessories each grew, at 9 and 33 percent, respectively. Services, meanwhile, saw the biggest uptick at 19 percent to $10.9 billion — an all-time high for the category.

“While it was disappointing to miss our revenue guidance, we manage Apple for the long term, and this quarter’s results demonstrate that the underlying strength of our business runs deep and wide,” Cook said in a statement. “Our active installed base of devices reached an all-time high of 1.4 billion in the first quarter, growing in each of our geographic segments. That’s a great testament to the satisfaction and loyalty of our customers, and it’s driving our Services business to new records thanks to our large and fast-growing ecosystem.”

Powered by WPeMatico