Earnings

Auto Added by WPeMatico

Auto Added by WPeMatico

Alibaba announced its earnings today, and the Chinese e-commerce giant got a nice lift from its cloud business, which grew 66% to more than $1.1 billion, or a run rate surpassing $4 billion.

It’s not exactly on par with Amazon, which reported cloud revenue of $8.381 billion last quarter, more than double Alibaba’s yearly run rate, but it’s been a steady rise for the company, which really began taking the cloud seriously as a side business in 2015.

At that time, Alibaba Cloud’s president Simon Hu boasted to Reuters that his company would overtake Amazon in four years. It is not even close to doing that, but it has done well to get to more than a billion a quarter in just four years.

In fact, in its most recent data for the Asia-Pacific region, Synergy Research, a firm that closely tracks the public cloud market, found that Amazon was still number one overall in the region. Alibaba was first in China, but fourth in the region outside of China, with the market’s Big 3 — Amazon, Microsoft and Google — coming in ahead of it. These numbers were based on Q1 data before today’s numbers were known, but they provide a sense of where the market is in the region.

Synergy’s John Dinsdale says the company’s growth has been impressive, outpacing the market growth rate overall. “Alibaba’s share of the worldwide cloud infrastructure services market was 5% in Q2 — up by almost a percentage point from Q2 of last year, which is a big deal in terms of absolute growth, especially in a market that is growing so rapidly,” Dinsdale told TechCrunch.

He added, “The great majority of its revenue does indeed come from China (and Hong Kong), but it is also making inroads in a range of other APAC country markets — Indonesia, Malaysia, Singapore, India, Australia, Japan and South Korea. While numbers are relatively small, it has also got a foothold in EMEA and some operations in the U.S.”

The company was busy last quarter adding more than 300 new products and features in the period ending June 30th (and reported today). That included changes and updates to core cloud offerings, security, data intelligence and AI applications, according to the company.

While the cloud business still isn’t a serious threat to the industry’s Big Three, especially outside its core Asia-Pacific market, it’s still growing steadily and accounted for almost 7% of Alibaba’s total of $16.74 billion in revenue for the quarter — and that’s not bad at all.

Powered by WPeMatico

Verizon reported its second quarter earnings this morning, and while revenue fell short of analyst predictions, the company had strong profits and subscriber growth.

Verizon reported consolidated revenue of $32.1 billion in Q2, down 0.4% year-over-year and lower than analyst estimates of $32.4 billion. However, it also reported adjusted earnings per share of $1.23, compared to analyst predictions of $1.20 (which was Verizon’s EPS a year ago).

The company saw significant growth in wireless subscribers, with a total net addition of 451,000 subscribers, including 420,000 net adds on the smartphone side and 245,000 on the phone side (compared to a net addition of 199,000 phone subscribers in Q2 2018).

Meanwhile, the Fios internet business saw 34,000 net additions, with revenue growing 1.9% year-over-year.

Breaking it down by business unit, Verizon Consumer revenue was $22.0 billion (flat year-over-year), Verizon Business revenue came in at $7.8 billion (down 1.1%) and Verizon Media (which owns TechCrunch) saw revenue of $1.8 billion, down 2.9%.

The earnings release also points to the carrier’s rollout of 5G, with a statement from CEO Hans Vestberg: “Verizon made history this quarter by becoming the first carrier in the world to launch 5G mobility. We are focused on optimizing our next-generation networks and enhancing the customer experience while we head into the second half of the year with great momentum.”

In an interview with CNBC, Vestberg predicted that half of the United States will have functioning 5G by 2020.

As of 11:16 am Eastern, Verizon shares were up 1.14% since the start of trading.

Powered by WPeMatico

Let’s start with the good news. LG actually had a pretty good quarter (on the strength of appliance sales). The LG Home Appliance & Air Solution division made $5.23 billion for Q2. Anyone who’s been following the company for the past several years can guess where the bad news comes.

Smartphone sales dipped 21.3% year over year for the South Korean company. The culprits are as you’d expect: an overall slowing of the smartphone market, coupled with aggressive undercutting from Chinese manufacturers. Huawei seems to lead the pack on that front, with a big increase in sales, in spite of a confluence of external factors.

The smartphone unit saw an operating loss of $268.4 million, in spite of a 6.8% increase in sales from the quarter prior. LG chalks up the loss to higher marketing on new models and April’s move from Seoul to Vietnam for smartphone production for longer-term cost cutting.

In spite of this, the company says it’s still bullish about smartphone sales for Q3. “The introduction of competitive mass-tier smartphones and growing demand for 5G products are expected to contribute to improved performance in the third quarter,” it writes in an earnings release.

LG is, of course, among the first companies to release a 5G handset, with the V50 ThinQ. The next-gen wireless technology is expected to increase stagnating global smartphone sales, though much of that will depend on the speed with which carriers are able to roll it out. It seems unlikely that 5G in and of itself will be a quick or even longer-term fix for a struggling category.

Powered by WPeMatico

The media has largely bought into Huawei’s “strong” half-year results today, but there’s a major catch in the report: the company’s quarter-by-quarter smartphone growth was zero.

The telecom equipment and smartphone giant announced on Tuesday that its revenue grew 23.2% to reach 401.3 billion yuan ($58.31 million) in the first half of 2019 despite all the trade restrictions the U.S. slapped on it. Huawei’s smartphone shipments recorded 118 million units in H1, up 24% year-over-year.

What about quarterly growth? Huawei didn’t say, but some quick math can uncover what it’s hiding. The company clocked a strong 39% in revenue growth in the first quarter, implying that its overall H1 momentum was dragged down by Q2 performance.

Huawei said its H1 revenue is up 23.2% year-on-year — but when you consider that Q1 revenue rose by 39%, Q2 must have been a real struggle…https://t.co/dFQo4gxEVbhttps://t.co/HABAQ6fmfK

— Jon Russell (@jonrussell) July 30, 2019

The firm shipped 59 million smartphones in the first quarter, which means the figure was also 59 million units in the second quarter. As tech journalist Alex Barredo pointed out in a tweet, Huawei’s Q2 smartphone shipments were historically stronger than Q1.

Huawei smartphones Q2 sales were traditionally much more stronger than on Q1 (32.5% more on average).

This year after Trump’s veto it is 0%. That’s quite the effect pic.twitter.com/x3dQlOePDA

— Alex B

(@somospostpc) July 30, 2019

And although Huawei sold more handset units in China during Q2 (37.3 million) than Q1 (29.9 million) according to data from market research firm Canalys, the domestic increase was apparently not large enough to offset the decline in international markets. Indeed, Huawei’s founder and chief executive Ren Zhengfei himself predicted in June that the company’s overseas smartphone shipments would drop as much as 40%.

The causes are multi-layered, as the Chinese tech firm has been forced to extract a raft of core technologies developed by its American partners. Google stopped providing to Huawei certain portions of Android services, such as software updates, in compliance with U.S. trade rules. Chip designer ARM also severed business ties with Huawei. To mitigate the effect of trade bans, Huawei said it’s developing its own operating system (although it later claimed the OS is primarily for industrial use) and core chips, but these backup promises may take some time to materialize.

Consumer products are just one slice of the behemoth’s business. Huawei’s enterprise segment is under attack, too, as small-town U.S. carriers look to cut ties with Huawei. The Trump administration has also been lobbying its western allies to stop purchasing Huawei’s 5G networking equipment.

In other words, being on the U.S.’s entity list — a ban that prevents American companies from doing business with Huawei — is putting a real squeeze on the Chinese firm. Washington has given Huawei a reprieve that allows American entities to resume buying from and selling to Huawei, but the damage has been done. Ren said last month that all told, the U.S. ban would cost his company a staggering $30 billion loss in revenue.

Huawei chairman Liang Hua (pictured above) acknowledged the firm faces “difficulties ahead” but said the company is “fully confident in what the future holds,” he said today in a statement. “We will continue investing as planned – including a total of CNY120 billion in R&D this year. We’ll get through these challenges, and we’re confident that Huawei will enter a new stage of growth after the worst of this is behind us.”

Powered by WPeMatico

Slack, the workplace messaging platform that has helped define a key category of enterprise IT, made its debut as a public company today with a pop. Trading as “WORK” on the New York Stock Exchange, it opened at $38.50 after setting a reference price last night of $26, valuing it at $15.7 billion, and then setting a bid/asking price of $37 this morning.

The trading climbed up quickly in its opening minutes and went as high as $42 and is now down to $38.95. We’ll continue to update this as the day goes on. These prices are pushing the market cap to around $20 billion.

Note: There was no “money raised” with this IPO ahead of today because Slack’s move into being a publicly traded company is coming by way of a direct listing — meaning the shares went directly on the market with no pre-sale. This is a less-conventional route that doesn’t involve bankers underwriting the listing (nor all the costs that come along with the roadshow and the rest). It also means Slack does not raise a large sum ahead of public trading. But it does let existing shareholders trade shares without dilution and is an efficient way of going public if you’re not in need of an immediate, large cash injection. It’s a route that Spotify also took when it went public last year, and, from the front-page article on NYSE.com, it seems that there might be growing interest in this process — or at least, that the NYSE would like to promote it as an option.

Slack’s decision to go slightly off-script is in keeping with some of the ethos that it has cultivated over the last several years as one of the undisputed juggernauts of the tech world. Its rocket ship has been a product that has touched on not one but three different hot growth areas: enterprise software-as-a-service, messaging apps and platform plays that, by way of APIs, can become the touchstone and nerve center for a seemingly limitless number of other services.

What’s interesting about Slack is that — contrary to how some might think of tech — the journey here didn’t start as rocket science.

Slack was nearly an accidental creation, a byproduct that came out of how a previous business, Tiny Speck, was able to keep its geographically spread-out team communicating while building its product, the game Glitch. Glitch and Tiny Speck failed to gain traction, so after they got shut down, the ever-resourceful co-founder Stewart Butterfield did what many founders who still have some money in the bank and fire in their bellies do: a pivot. He took the basic channel they were using and built it (with some help) into the earliest public version of what came to be known as Slack.

But from that unlikely start something almost surprising happened: the right mix of ease of use, efficient responsiveness and functionality — in aid of those already important areas of workplace communication, messaging and app integration — made Slack into a huge hit. Quickly, Slack became the fastest-growing piece of enterprise software ever in terms of adding users, with a rapid succession of funding rounds (raising over $1.2 billion in total), valuation hikes and multiple product improvements along the way to help it grow.

Today, like many a software-as-a-service business that is less than 10 years old and investing returns to keep up with its fast-growing business, Slack is not profitable.

In the fiscal year that ended January 31, 2019, it reported revenues in its S-1 of $400.6 million, but with a net loss of $138.9 million. That was a slight improvement on its net loss from the previous fiscal year of $140.1 million, with a big jump on revenue, which was $220.5 million.

But its growth and the buzz it has amassed has given it a big push. As of January 31, it clocked up over 10 million daily active users across 600,000 organizations, with 88,000 of them on paid plans and 550,000 using the free version of the app. It will be interesting to see how and if that goodwill and excitement outweighs some of those financial bum notes.

Or, in some cases, possibly other bum notes. The company has made “Work” not just its ticker but its mantra. Its slogan is “Where work happens” and it focuses on how its platform helps make people more productive. But as you might expect, not everyone feels that way about it, with the endless streams of notifications, the slightly clumsy way of handling threaded conversations and certain other distracting features raising the ire of some people. (Google “Slack is a distraction” and you can see some examples of those dissenting opinions.)

Slack has had its suitors over the years, unsurprisingly, and at least one of them has in the interim made a product to compete with it. Teams, from Microsoft, is one of the many rival platforms on the market looking to capitalise on the surge of interest for chat and collaboration platforms that Slack has helped usher in. Other competitors include Workplace from Facebook, Mattermost and Flock, along with Threads and more.

Powered by WPeMatico

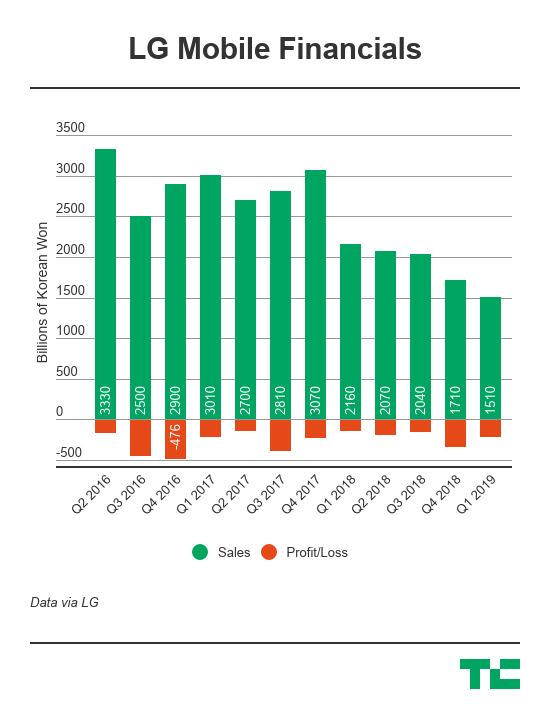

LG was once a stalwart of the smartphone industry — remember its collaboration with Facebook back in the day? — but today the company is swiftly descending into irrelevance.

The latest proof is LG’s Q1 financials, released this week, which show that its mobile division grossed just KRW 1.51 trillion ($1.34 billion) in sales for the quarter. That’s down 30% year-on-year and the lowest income for LG Mobile for at least the last eight years. We searched back eight years to Q1 2011 — before that LG was hit and miss with releasing specific financial figures for its divisions.

To give an indication of its decline, LG shipped more than 15 million phones in Q4 2015 when its revenue was 3.78 trillion RKW, or $3.26 billion. That’s 2.5 times higher than this recent Q1 2019 period.

Regular readers will be aware that LG mobile is a loss-making division. That’s the reason its activities — and consequently sales — have scaled down in recent years. But the losses are still coming.

LG put Brian Kwon, who leads its lucrative Home Entertainment business, in charge of its mobile division last November and his task remains ongoing, it appears.

LG Mobile recorded a loss of 203.5 billion KRW ($181.05 million) for Q1 which it described as “narrowed.”

It is true that LG Mobile’s Q1 loss is lower than the 322.3 billion KRW ($289.8 million) loss it carded in the previous quarter, but it is wider than one year previous. Indeed, the mobile division lost 136.1 billion KRW ($126.85 million) in Q1 2018.

LG said Mr. Kwon is presiding over “a revised smartphone launch strategy,” which is why the numbers are changing so drastically. Going forward, it said that the launch of its G7 ThinQ flagship phone and a new upgrade center — first announced last year — are in the immediate pipeline, but it is hard to see how any of this will reverse the downward trend.

LG Mobile is increasingly problematic because the parent company is seeing success in other areas, but that’s being countered by a poor-performing smartphone business. Last quarter, mobile dragged LG to its first quarterly loss in two years, for example.

Just looking at the Q1 numbers, LG’s overall profit was 900.6 billion KRW ($801.25 million) thanks to its home appliance business ($647.3 million profit) and that home entertainment business, which had a profit of $308.27 million. Its automotive business — which is, among other things, focused on EVs — did bite into the profits, but that is at least a business that is going places.

Powered by WPeMatico

Even as its solar business declined in step with its overall earnings, Tesla is bullish on the prospects for the energy side of its business over the course of the year.

The energy business is an unheralded part of Tesla — overshadowed by its headline-grabbing (and much larger) auto exploits — that chief executive Elon Musk thinks will generate an increasing share of revenue for the company over time.

Revenues from its solar power and energy storage business fell by 13 percent from the fourth quarter 2018 and 21 percent from a year ago period, down to $324.7 million from $371.5 million in the fourth quarter of 2018 and $410 million in the year ago quarter.

Solar energy deployments fell from 73 megawatts to 47 megawatts from the fourth to the first quarter, the company said. Those figures were offset by a slight increase in solar deployments.

The company actually introduced a new financing and purchasing model for solar installations in the second quarter — saying in its shareholder letter that residential solar customers can buy directly from the Tesla website, in standardized capacity increments.

“We aim to put customers in a position of cash generation after deployment with only a $99 deposit upfront. That way, there should be no reason for anyone not to have solar generation on their roof,” Musk and chief financial officer Zachary Kirkhorn wrote in the shareholder letter.

Tesla’s battery storage business was hit as the company shifted units from energy storage to installation in its own vehicles.

“Energy storage production in the second half of 2018 was limited by cell production as we routed all available Gigafactory 1 cell capacity to supply Model 3,” the company wrote in its letter. “Some Gigafactory 1 cell production has been routed back to the energy storage business, enabling us to increase production in Q1 by roughly 30% compared to the previous quarter.”

And Musk thinks that the energy business will grow significantly over the course of the year. “We hope that growth rate will continue and battery storage will become a bigger and bigger percentage over time,” Musk said on an analyst call following the earnings release. Potentially, Tesla thinks its energy business could grow by as much as 300 percent, Musk said.

Powered by WPeMatico

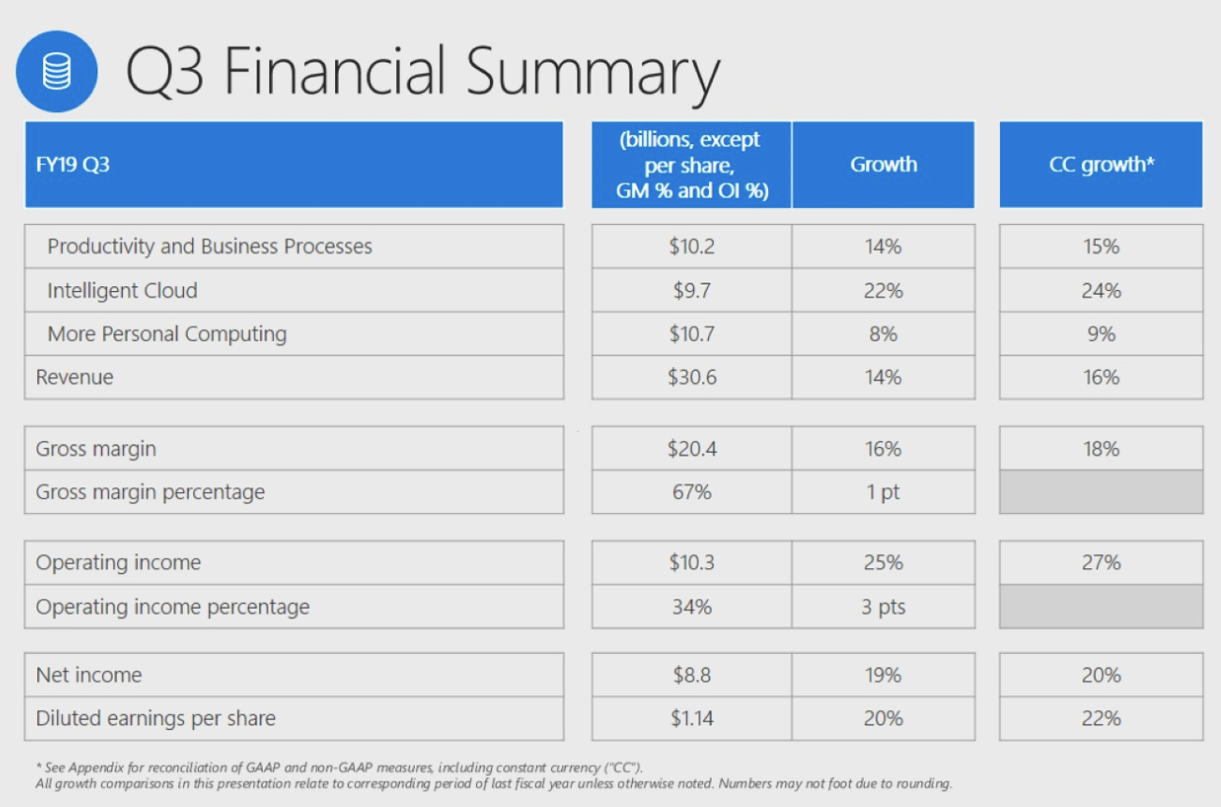

Microsoft reported its quarterly earnings for Q3 2019 today. Overall, Wall Street expected earnings of about $1 per share and revenue of $29.84 billion. The company handily beat this with revenue of $30.6 billion (up 14 percent from the year-ago quarter) and earnings per share of $1.14.

With Microsoft focusing heavily on its cloud business, with both Azure and its other cloud-based services, it’s no surprise that this is also what Wall Street really cares about. The expectation here, according to some analysts, was that the company’s overall commercial cloud business would hit a run rate of about $38.5 billion. Those analysts we’re off by only a tiny bit. Microsoft today reported that its commercial cloud run-rate hit $38.4 billion.

And indeed, Microsoft Azure had a pretty good quarter, with revenue growing 73 percent. That’s a bit lower than last quarter’s results, but only by a fraction, and shows that there is plenty of growth left for Microsoft’s cloud infrastructure business.

Azure’s growth slowed somewhat in recent quarters. In some ways, that’s to be expected, though. Microsoft’s cloud is now a massive business, and posting 100 percent growth when you have a run rate of almost $40 billion becomes a bit harder.

“Demand for our cloud offerings drove commercial cloud revenue to $9.6 billion this quarter, up 41 percent year-over-year,” said Amy Hood, executive vice president and chief financial officer of Microsoft. “We continue to drive growth in revenue and operating income with consistent execution from our sales teams and partners and targeted strategic investments.”

The company’s “intelligent cloud” segment, which includes Azure and other cloud- and server-based products, reported revenue of $9.7 billion, up 22 percent from the year-ago quarter.

Microsoft’s productivity applications also fared well, with total revenue up by 14 percent to $10.2 billion. Here, revenue from LinkedIn also increased by 27 percent and the company highlighted that LinkedIn sessions also increased 24 percent.

Other highlights of the report include an increase in Surface revenue of 21 percent, which was expected, given the number of new devices the company released in recent quarters.

“Leading organizations of every size in every industry trust the Microsoft cloud. We are accelerating our innovation across the cloud and edge so our customers can build the digital capability increasingly required to compete and grow,” said Satya Nadella, CEO of Microsoft.

For more financial details, you can find the full report here.

Powered by WPeMatico

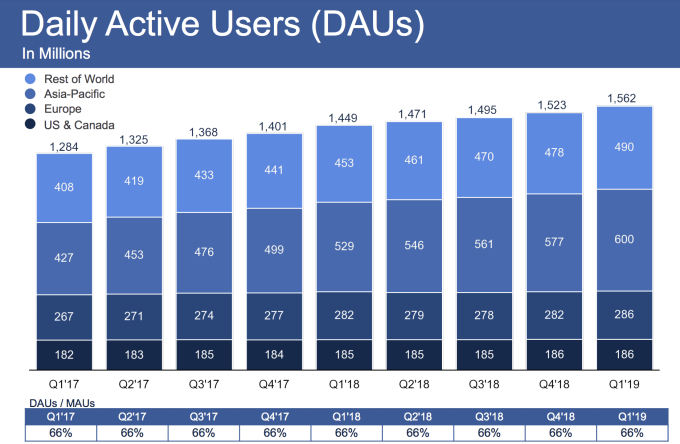

A massive penalty hangs over Facebook’s head, but it otherwise had a very strong Q1 earnings report. Facebook reached 2.38 billion monthly users, up 2.5 percent from 2.32 billion in Q4 2018 when it grew 2.2 percent, and it now has 1.56 billion daily active users, up 2.63 percent from 1.52 billion last quarter when it grew 2 percent. Facebook pulled in $15.08 in revenue, up 26 percent year-over-year compared to Refinitiv’s consensus estimates of $14.98 billion in revenue.

Facebook recorded earnings per share of $0.85 compared to estimates of $1.63 EPS. However, that’s because Facebook has set aside $3 billion to cover a potential FTC fine that it’s still resolving. Without that fine, it would have had an EPS of $1.89. Despite the set-aside, Facebook still earned $2.429 billion in profit, though that’s down from $4.988 a year ago and $6.8 billion in Q4 2018.

Facebook’s share price rose 8.3 percent to $197.84 after closing before earnings at $182.58, way up from its recent low of $124.06 in December. Wall Street seems to have already priced in the potential FTC fine. Facebook has agreed to strict oversight of how it handled user privacy in a 2011 deal with the FTC. It promised to not misrepresent its privacy practices or change privacy controls without user permission, and it’s now negotiating the fine for potentially breaking those terms.

Facebook wrote in its earnings release about the FTC fine that:

“In the first quarter of 2019, we reasonably estimated a probable loss and recorded an accrual of $3.0 billion in connection with the inquiry of the FTC into our platform and user data practices, which accrual is included in accrued expenses and other current liabilities on our condensed consolidated balance sheet. We estimate that the range of loss in this matter is $3.0 billion to $5.0 billion. The matter remains unresolved, and there can be no assurance as to the timing or the terms of any final outcome.”

It’s possible Facebook escapes with a lesser fine that would likely still dwarf Google’s $22.5 million penalty for violating an FTC privacy deal. But it also might have to drag down a future quarter of earnings if the fine ranges as high as $5 billion or larger. Though Facebook does have $45.2 billion in cash and securities on hand to pay that fine and make any necessary acquisitions. Facebook’s headcount grew 36% year-over-year to 37,773 as it staffs up its security team, but it still has a 22 percent operating margin.

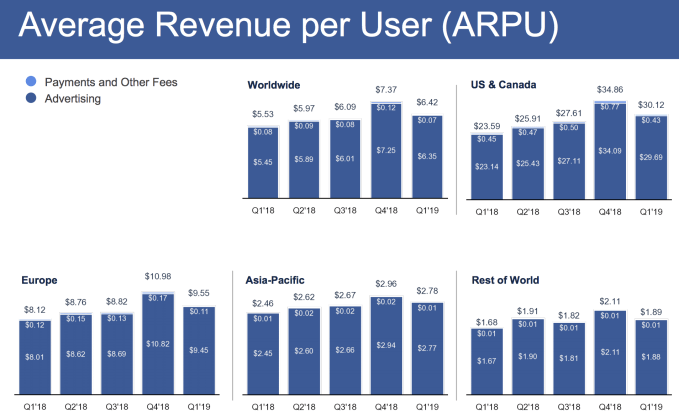

Facebook has managed to hold on to its 66 percent daily to monthly user ratio, showing people aren’t necessarily using it less despite all the backlash. It added 39 million daily users, compared to Snapchat’s addition of 4 million in Q1. But Facebook failed to grow past its 186 million daily user count in the US & Canada where it got stuck last quarter, but at least it added 4 million in its lucrative Europe market, plus it had atypically large gains in Asia-Pacific and the Rest Of World regions. As for monetization, Facebook made modest gains in average revenue per user across markets compared to Q3 2018 (excluding the holiday-laden Q4). Europe did especially well, growing ARPU 8.2 percent.

Zooming out, Facebook now has over 2.7 billion total mothly users across its family of Facebook, Messenger, Instagram, and WhatsApp, the same as last quarter. 2.1 billion people use at least one of those apps daily, up from 2 billion last quarter. Instagram Stories, WhatsApp Status, and Facebook Stories on Facebook and Messenger combined each now have 500 million daily users. Facebook also now has 3 million advertisers buying Stories ads across its apps, so the ephemeral format will likely start to contribute meaningful revenue soon.

In March, Zuckerberg announced plans for a massive privacy-centric overhaul of Facebook to turn it from just a townsquare into also a “living room”. That means unifying its messaging apps with a backend that supports end-to-end encryption, and promoting ephemerality in content sharing and communication. That could help deter calls for regulation, make Facebook harder to break up, and help it stay ahead of competitors like Snapchat, but will also be a massive product and engineering undertaking.

Today, Zuckerberg focused on providing more details to this plan to expand privacy, encryption, impermanence, safety, interoperability, and secure data storage. He stressed that given people traditionally spend more time communicating and consuming content privately than publicly, strengthening Facebook’s “living room” could boost its business. Zuckerberg noted that since Facebook already doesn’t use messaging content for ad targeting and recent content is more useful for its business, encryption and impermanence shouldn’t be a big risk either. Refusing to store data in countries with poor records of privacy could lead to Facebook being banned there, which Zuckerberg admitted is a major business threat, but one it’s grappled with over content policies for years.

In fact, impermanence is already earning money for Facebook. It said that Instagram Stories was the greatest contributor of additional ad impressions this quarter. And while the Facebook and Instagram feeds are already jammed full of ads with little room for more, Facebook says there’s still room to significantly increase Instagram Stories ad load.

Another highlight of the call was Zuckerberg’s discussion of Facebook’s payments strategy. He confirmed that Facebook plans to build out ways for people to pay merchants through its messaging apps. “So I think that what we’re going to end up seeing is building out payments, which is going to end up being something that we do country by country . . . The goal is to have something where you could do discovery through the broader townsquare-like platforms like Instagram and Facebook, and then you can complete the transactions and follow up with businesses individually and have an ongoing relationship through Messenger and WhatsApp.”

This is the first earnings report of a full quarter following Facebook’s worst-ever security breach in September that impacted 50 million users, shaking confidence in the social network’s privacy and security. It’s also the first full quarter in which Facebook sold its own branded hardware — its Portal video chat device that was well received by critics except for the fact that it was made by Facebook.

Yet the defining story continues to be Facebook’s struggle with claims that its user research and developer platform efforts endangered user privacy and steamrolled competitors in search of growth. That includes TechCrunch’s big scoop that Facebook was paying teens to snoop on their data with a VPN app, which eventually led Facebook to shut down its Onavo user surveillance apps. The fact that Facebook isn’t losing massive numbers of users after years of sustained scandals is a testament to how deeply it’s woven itself into people’s lives.

Powered by WPeMatico

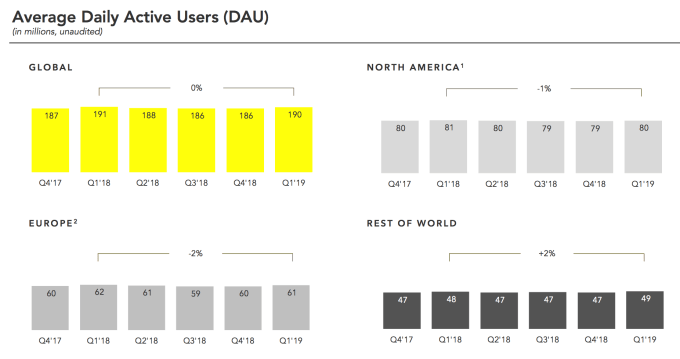

After a year of its user count shrinking or staying flat, Snapchat is finally growing again, and more growth is likely on the way. That’s because it’s finally completed the rollout of Project Mushroom, aka a backend overhaul of its Android app that’s 25 percent smaller and 20 percent faster. Designed for India and other emerging markets where iPhones are too expensive, Snapchat saw an immediate 6 percent increase in the number of people on low-end devices sending Snaps within the first week of upgrading to the new Android app.

Snapchat grew from 186 million daily active users in Q4 2018 to 190 million in Q1 2019, adding 1 million in North America, 1 million in Europe and 2 million in the Rest of World, where the Android app makes the biggest difference despite rolling out near the end of the quarter. It has been a long wait, as Snap first announced the Android reengineering project in November 2017.

“As of the end of Q1, our new Android application is available to everyone,” Snap CEO Evan Spiegel wrote in his prepared remarks for today’s estimate-beating earnings report. “While these early results are promising, improvements in performance and new user retention will take time to compound and meaningfully impact our top-line metrics. There are billions of Android devices in the world that now have access to an improved Snapchat experience, and we look forward to being able to grow our Snapchat community in new markets.”

Some of the growth stemmed from tweaks to Snapchat’s ruinous redesign, including better personalized ranking of Stories and Discover content, as well as new premium video Shows. Now with the Android app humming, though, we might see significant growth in the Rest of World region in Q2.

Unfortunately, since Snapchat uses bandwidth and storage-heavy video, more usage also means more Amazon AWS and Google Cloud expenditures. That’s partly why Snapchat is predicting a slight increase in adjusted EBITDA losses from $123 million in Q1 to between $125 million and $150 million in Q2. Rest of World users only earn Snap about one-third as much money as North American users, but cost nearly as much to support.

We first highlighted Snap’s neglect of the international teen Android market when Instagram Stories launched in August 2016. Spiegel and Snap were too focused on cool American teens, squandering this market that was snapped up by Facebook’s Instagram and WhatsApp. Now Snapchat will have a much harder time winning emerging markets as they’re not the first to bring Stories there. But if it can double-down on ephemeral messaging, premium video and its augmented reality platform that are leagues ahead of Facebook’s offerings, it could finally creep toward that 200 million DAU milestone.

Come see Snap CEO Evan Spiegel speak at TechCrunch Disrupt SF on October 2nd-4th. Get your tickets here.

Powered by WPeMatico