Earnings

Auto Added by WPeMatico

Auto Added by WPeMatico

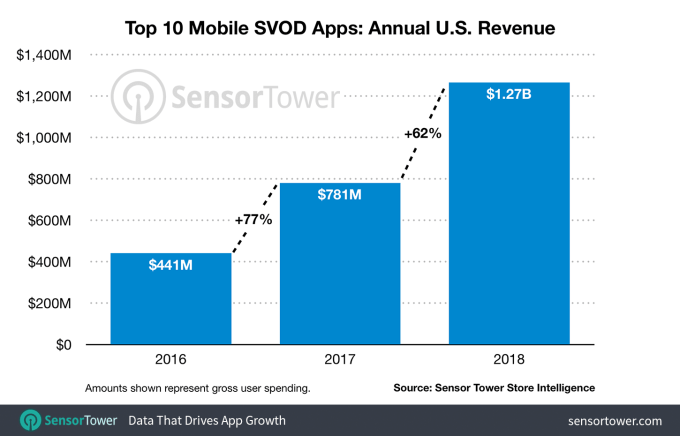

Subscriptions are booming on the app stores, and particularly subscription video apps, thanks to the growing number of cord cutters who are choosing to stream their TV shows and movies instead of paying for cable or satellite. In the U.S., the top 10 subscription video apps by revenue pulled in $1.27 billion in 2018 across both the iOS App Store and Google Play, according to new data from Sensor Tower — that’s a 62 percent increase over the $781 million spent in 2017.

It’s also three times higher than what was spent in these apps back in 2016.

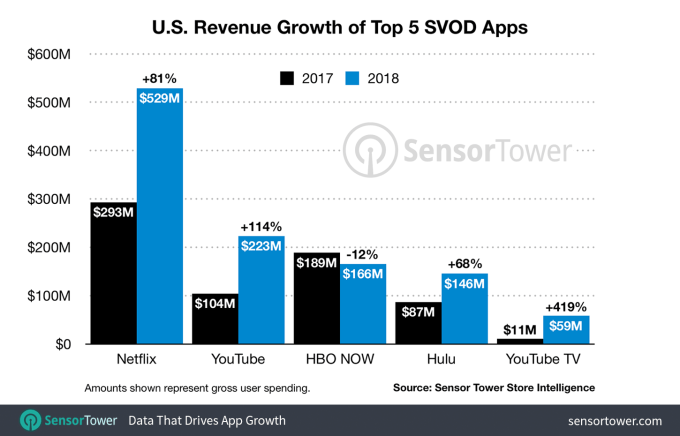

The top app, not surprisingly, was Netflix — which snagged the spot for the second year in a row. It earned an estimated $529 million in the U.S., the report found. However, Netflix won’t maintain the top spot in the rankings in 2019, as the company recently made a decision to keep more of its subscription revenue to itself.

Netflix in 2018 had dropped in-app subscription sign-ups in its Android app on Google Play, then did the same on the iOS App Store in December. That will decrease its in-app subscription revenues this year, though it won’t immediately go to zero because of revenues from existing subscribers.

The No. 2 top grossing app was YouTube, which is maybe more of a surprise to those who don’t realize that the app they use to watch free videos is making quite so much money through in-app purchases. But YouTube offers a couple of different types of in-app purchases, including subscriptions to its ad-free tier, YouTube Premium, as well as virtual currency to be used in Super Chat.

Sensor Tower says YouTube took in less than half as much revenue as Netflix at around $223 million, but it grew substantially in 2018 — up 114 percent from $104 million in 2017.

HBO NOW was the No. 3 top grossing app, even though its subscriber base declined. The app generated 12 percent less in 2018, at $166 million, down from $189 million. The reason, naturally, was that the app was without “Game of Thrones” to attract viewers. That doesn’t bode all that well for HBO’s future without “Thrones,” unless its spin-off becomes a hit.

Hulu and YouTube TV were the No. 4 and No. 5 apps, respectively. Hulu grew by 68 percent while YouTube TV jumped up a whopping 419 percent. CBS’s streaming app is doing decently, too, with 57 percent year-over-year growth in subscriber spending.

Much of that comes from streamers interest in the new “Star Trek” series. In fact, with the Season 2 premiere this month, CBS said its streaming service hit a new milestone across both subscription sign-ups and unique viewers in a weekend. While the network didn’t share exact numbers, it said the January 19 weekend, when the new season of “Star Trek: Discovery” aired, eclipsed 2017’s previous record from the series premiere by more than 72 percent, in terms of sign-ups.

Combined, 2018’s top 10 subscription streaming apps accounted for a sizable chunk — now 22 percent — of non-game app revenue on the app stores in the U.S. Their 62 percent revenue growth was also more than all the other non-game apps combined, which grew 56 percent year-over-year, the new report said.

Subscriptions — and not just for streaming apps — have become the new driver for non-game spending on the app stores, and that isn’t going to change anytime soon.

According to App Annie’s recent forecast for 2019, 10 minutes of every hour spent consuming media across TV and internet will come from streaming video on mobile. It estimates that total time in video streaming apps will increase 110 percent from 2016 to 2019, with consumer spend in entertainment apps rising by 520 percent over that same period. Most of those revenues will come from the growth in in-app subscriptions, the firm had said earlier.

Powered by WPeMatico

Video game revenue in 2018 reached a new peak of $43.8 billion, up 18 percent from the previous years, surpassing the projected total global box office for the film industry, according to new data released by the Entertainment Software Association and The NPD Group.

Preliminary indicators for global box office revenues published at the end of last year indicated that revenue from ticket sales at box offices around the world would hit $41.7 billion, according to comScore data reported by Deadline Hollywood.

The $43.8 billion tally also surpasses numbers for streaming services, which are estimated to rake in somewhere around $28.8 billion for the year, according to a report in Multichannel News.

Video games and related content have become the new source of entertainment for a generation — and it’s something that has new media moguls like Netflix chief executive Reed Hastings concerned. In the company’s most recent shareholder letter, Netflix said that Fortnite was more of a threat to its business than TimeWarner’s HBO.

“We compete with (and lose to) Fortnite more than HBO,” the company’s shareholder letter stated. “When YouTube went down globally for a few minutes in October, our viewing and signups spiked for that time…There are thousands of competitors in this highly fragmented market vying to entertain consumers and low barriers to entry for those with great experiences.”

“The impressive economic growth of the industry announced today parallels the growth of the industry in mainstream American culture,” said acting ESA president and CEO Stanley Pierre-Louis, in a statement. “Across the nation, we count people of all backgrounds and stages of life among our most passionate video game players and fans. Interactive entertainment stands today as the most influential form of entertainment in America.”

Gains came from across the spectrum of the gaming industry. Console and personal computing, mobile gaming, all saw significant growth, according to Mat Piscatella, a video games industry analyst for The NPD Group.

According to the report, hardware and peripherals and software revenue increased from physical and digital sales, in-game purchases and subscriptions.

| U.S. Video Game Industry Revenue | 2018 | 2017 | Growth Percentage |

| Hardware, including peripherals | $7.5 billion | $6.5 billion | 15% |

| Software, including in-game purchases and subscriptions |

$35.8 billion |

$30.4 billion |

18% |

| Total: | $43.3 billion | $36.9 billion | 18% |

Source: The NPD Group, Sensor Tower

Powered by WPeMatico

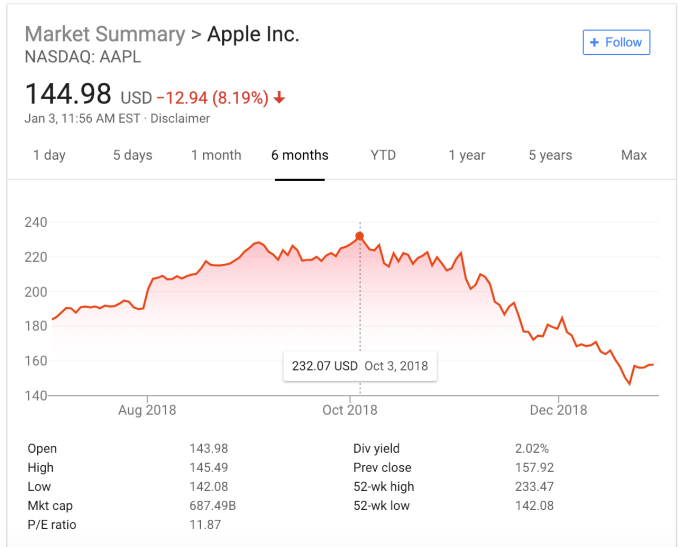

Apple stock was down more than 9 percent overnight and continued the downward trend in trading this morning. In fact, the company’s stock price is down a total of 38 percent since October. This, after the company halted trading yesterday afternoon to provide lower guidance for upcoming earnings. As the iPhone upgrade market softened, it was having a big impact on revenue, at least in the short term, and Apple stock took a big hit as a result.

On October 3, the stock was selling at 232.07 per share, and while the price has fluctuated and the market in general has plunged in that time period, the stock has been on a downward trend for the past couple of months and has lost approximately $87 a share since that October high point.

Last night, before the company briefly stopped trading to make its announcement, the stock stood at $157.92 a share. This morning as we went to publication, it was recovering a bit, but was still down 8.19 percent to $144.981.

D.A. Davidson senior analyst Tom Forte says yesterday’s announcement, while not completely unexpected, was surprising, given Apple’s traditionally strong position. “We knew that iPhone unit sales were weak, but just not how weak,” he said.

The biggest factor in yesterday’s announcement, in Forte’s view, was China, where he says the company generates 20 percent of its sales. As the U.S.-China trade war drags on, it’s having an impact on these sales. This could be because of a combination of factors, including a weakening Chinese economy as a result of the trade war, or patriotism on the part of Chinese consumers, who are choosing to buy Chinese brands over of the iPhone.

This also comes at a time when Apple had already indicated that iPhone sales were weak in other worldwide markets, including India, Russia, Brazil and Turkey. This already helped weaken the iPhone sales worldwide, although Forte still sees the Chinese market as the biggest factor in play here.

Forte says that in spite of the soft iPhone performance, the good news is the rest of the product portfolio is up 19 percent, and that could bode well for the future. What’s more, the company has set aside $100 billion for stock buy-back purposes. “They have the balance sheet. They have the stock buy-back program. They still generate very significant free cash flow, and if the individual investor won’t buy the stock, then the company will buy the stock,” he explained.

In a report released this morning, financial analysts Canaccord Genuity believe that in spite of yesterday’s report, the company is still fundamentally sound and they continue to recommend a BUY for Apple stock. “We maintain our belief Apple can expand its leading market share of the premium-tier smartphone market and the iPhone installed base (excluding refurbished iPhones) will exceed 700M in 2018. This impressive installed base should drive iPhone replacement sales and earnings, as well as cash flow generation to fund strong long-term capital returns. We reiterate our BUY rating but decrease our price target to $190 based on our lowered estimates,” the company wrote in a report released this morning.

Forte says the unknown-unknown here is how the U.S.-China trade war plays out, and as long as that situation remains fluid, the company might not recover that income in the near term in spite of stronger sales across the catalog.

Powered by WPeMatico

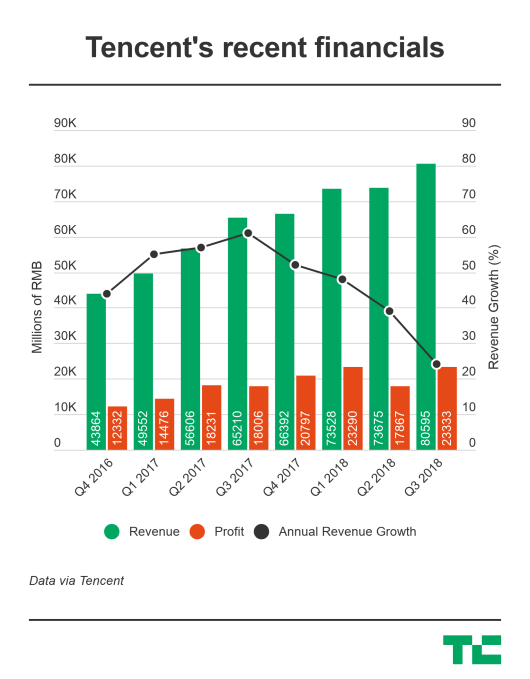

Chinese internet giant Tencent bounced back from a disappointing previous quarter, but for once the company didn’t have its gaming business to thank.

Tencent may be best known for conjuring up WeChat, China’s most popular messaging platform, but its revenue is driven by its gaming business, which includes top smartphone titles and a thriving PC unit. Its Q3 results, announced today, however, saw its gaming income slacken and other units, including a booming advertising business, step up.

The firm posted a net profit of RMB 23.3 billion ($3.4 billion) on total revenue of RMB 80.6 billion ($11.7 billion), up 30 percent and 24 percent, respectively. Profit growth was back on track, mainly thanks to increased net gains from investments, including a blockbuster IPO of Meituan in September.

Advertising increased by 47 percent and generated 20 percent of total revenues, marking the first time that the segment has reached that mark. The jump is in part a result of strong ad revenue growth on Tencent’s two main chat apps, WeChat and QQ.

These changes are a sign that Tencent has begun to aggressively monetize its massive network of social networking users. As of September, Tencent had 1.08 billion monthly active users on WeChat worldwide, though the app’s spectacular growth has slowed to 2.3 percent quarter-to-quarter.

Tencent underwent an internal reorganization in October that saw it merge several business groups, which have resulted in a more unified system of advertising sales platforms, the company explained in today’s report.

“Our advertising, digital content, payment and cloud services sustained robust activity and revenue growth, and now account for the majority of our revenue,” chairman and CEO Pony Ma said in a statement.

In contrast, games, which have been Tencent’s major revenue driver for years, slid four percent this quarter due to a prolonged freeze on gaming licenses in China. The firm claims it has 15 games with monetization approval in its pipeline, which means that gaming revenues could rebound when it publishes those titles, although it said the same in the previous quarter, so a lack of progress is fairly ominous.

The firm also pointed out that while mobile games continued to fuel revenue growth, PC games suffered a decline.

When asked about the situation with gaming licenses on a call with investors, Tencent President Martin Lau said the company is “waiting for the government to start the approval process.”

Tencent appears to have found a potential interim solution, which involves allowing third-party publishers who secured a license before the freeze to publish games through its platform, but of course, that has limited use.

While games are the hot topic, Tencent was keen to push the story of its cloud computing business, which it said is a key to widening its focus into IOT and other areas.

Emboldened by the reorganization in October, which seemed aimed at shifting Tencent from a consumer-facing internet company into one that’s increasing serving industries, the firm said its cloud business more than doubled its revenue year-on-year. There was no raw revenue figure released for the quarter, but the company did disclose that the cloud unit has brought in more than RMB 6 billion, $860 million, over the last three quarters.

Furthermore, cloud computing and payment-related services helped its “Others” business increase its revenue 69 percent year-on-year to reach RMB 20.3 billion, $2.92 billion, for the quarter.

Powered by WPeMatico

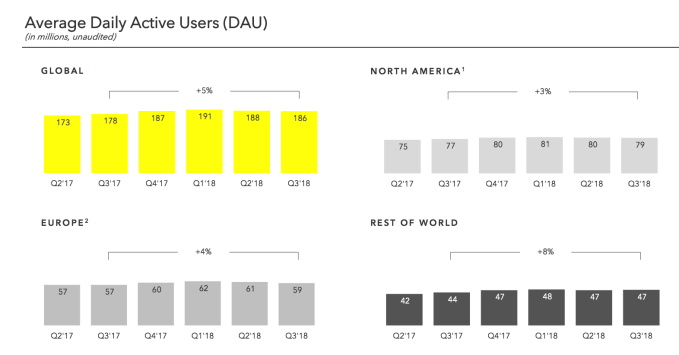

Snapchat continued to shrink in Q3 2018 but its business is steadily improving. Snapchat’s daily active user count dropped again, this time by 1 percent to 186 million, down from 188M and a negative 1.5 percent growth rate in Q2. User count is still up 5 percent year-over-year, though. Snapchat earned $298 million in revenue with an EPS loss of $0.12, beating Wall Street’s expectations of $283 million in revenue and EPS loss of $0.14, plus a loss of a half a million users.

Snap entered earnings with a $6.99 share price, close to its $6.46 all-time low and way down from its $24 IPO opening price. Snap lost $325 million this quarter compared to $353 million in Q2, so it’s making some progress with its cost cutting. That briefly emboldened Wall Street, which pushed the share price up 8.3 percent to around $7.57 right after earnings were announced.

But then Snap’s share price came crashing down to -9.3 percent to $6.31 in after-hours trading. The stock had been so heavily shorted by investors that it only needed modest growth in its business for shares to perk up, but the fear that Snap might shrink into nothing has investors weary. Projections that Snap will lose users again next quarter further scared off investors.

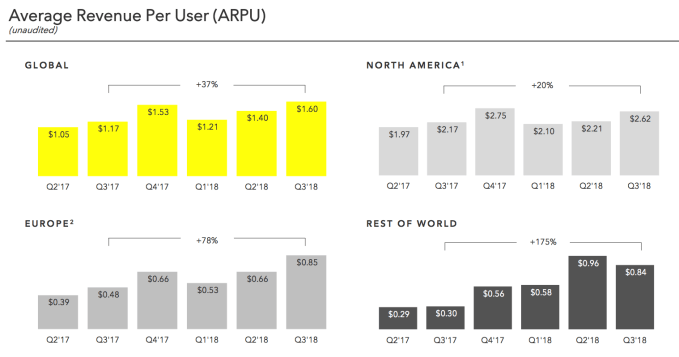

Worringly, Snapchat’s average revenue per user dropped 12.5 percent in the developing world this quarter. But strong gains in the US and Europe markets grew global ARPU by 14 percent. Snap projects $355 million to $380 million in holiday Q4 revenue, in line with analyst estimates.

In his prepared remarks, CEO Evan Spiegel admitted that “While we have incredible reach among our core demographic of 13- to 34-year-olds in the US and Europe, there are billions of people worldwide who do not yet use Snapchat.” He explained that the 2 million user loss was mostly on Android where Snapchat doesn’t run as well as on iOS. Noticibly absent was an update on monthly active users in the US and Canada. Snap said that was over 100 million monthly users last quarter, probably in an effort to distract from the daily user shrinkage. The company didn’t update that stat, but did say the “over 100 million” stat was still accurate.

Snap CEO Evan Spiegel

Spiegel had said in a memo that his stretch goal was break-even this year and full-year profitability in 2019. But CFO Tim Stone said that “Looking forward to 2019, our internal stretch output goal will be an acceleration of revenue growth and full year free cash flow and profitability. Bear in mind that an internal stretch goal is not a forecast, and it’s not guidance.”

During the call, Spiegel responded to questions about the Android overhaul’s schedule saying, “Quality takes time. We’re going wait until we get it right”. But analysts piled on with inquiries about how Snap would turn things around in 2019. He admitted Snaps created per day had dropped from 3.5 billion to 3 billion per day, but tried to reassure investors by saying over 60% of our users are still creating snaps every day.

Spiegel said that expanding beyond the 13 to 34-year-old age group in the US and Europe, plus scoring more users in the developing world via the improved Android app would be how it restores momentum. But the problem is that courting older users could sour the perception of its younger users who don’t want their parents, teachers, or bosses on the app.

Now down to $1.4 billion in cash and securities, Snap will need to start reaching more of those international users or improving monetization of those it still has to keep afloat without outside capital.

Q3 saw Snapchat’s launch its first in-house augmented reality Snappable games, while plans for an third-party gaming platform leak. The Snappable Tic-Tac-Toe game saw 80 million unique users, suggesting gaming could be the right direction for Snap to move towards.

It launched Lens Explorer to draw more attention to developer and creator-built augmented reality experiences, plus its Storyteller program to connect social media stars to brands to earn sponsorship money. It also shut down its Venmo-like Snapcash feature. But the biggest news came from its Q2 earnings report where it announced it’d lost 3 million users. That scored it a short-lived stock price pop, but competition and user shrinkage has pushed Snap’s shares to new lows.

Snapchat is depending on the Project Mushroom engineering overhaul of its Android app to speed up performance, and thereby accelerate user growth and retention. Snap neglected the developing world’s Android market for years as it focused on iPhone-toting US teens. Given Snapchat is all about quick videos, slow load times made it nearly unusable, especially in markets with slower network connections and older phones.

Looking at the competitive landscape, WhatsApp’s Snapchat Stories clone Status has grown to 450 million daily users while Instagram Stories has reached 400 million dailies — much of that coming in the developing world, thereby blocking Snap’s growth abroad as I predicted when Insta Stories launched.. Snap Map hasn’t become ubiquitous, Snap’s Original Shows still aren’t premium enough to drag in tons of new users, Discover is a clickbait-overloaded mess, and Instagram has already copied the best parts of its ephemeral messaging. Snap could be vulnerable in the developing world if WhatsApp similarly copies its disappearing chats.

At this rate, Snap will run out of money before it’s projected to become profitable in 2020 or 2021. That means the company will likely need to sell new shares in exchange for outside investment or get acquired to survive.

Powered by WPeMatico

The Daily Crunch is TechCrunch’s roundup of our biggest and most important stories. If you’d like to get this delivered to your inbox every day at around 9am Pacific, you can subscribe here:

1. Tesla earns its first profit in two years

Tesla reported a profit in the third quarter, reversing seven consecutive quarters of losses. This is only the third time in the company’s history that it has achieved this milestone.

The turnaround was driven by sales of the Model 3. The company said customers are trading up their relatively cheaper vehicles to buy a Model 3, even though there is not yet a leasing option and the starting price was $49,000.

2. Trump has two ‘secure’ iPhones, but the Chinese are still listening

A new report by The New York Times puts a spotlight on the president’s array of devices and how he uses them. However, both Trump and a spokesperson for China’s foreign ministry have denied the story.

(BRENDAN SMIALOWSKI/AFP/Getty Images)

3. Red Dead Redemption 2 sets the bar high for the next generation of open world games

Tomorrow, Red Dead Redemption 2 goes live after months of breathless speculation. And according to Devin Coldewey and Jordan Crook, it’s as good as you’ve been hoping.

4. Facebook is building Lasso, a video music app to steal TikTok’s teens

Facebook is building a standalone product where users can record and share videos of themselves lip syncing or dancing to popular songs, according to information from current and former employees.

5. One-year-old Ribbon raises $225m to remove the biggest stress of home buying

The startup wants to replace the incredible stress of securing a mortgage during the home-buying process with a Ribbon Offer: If a buyer can’t secure a mortgage in time for close, Ribbon will pay for the house itself and give the buyer extra time to get financing.

6. Twitter beats Wall St Q3 estimates with $758M in revenue

Twitter reported a 29 percent increase in ad revenue to $650 million, and the company says total ad engagements increased 50 percent year over year. However, user growth didn’t quite match expectations.

7. Confirmed: ShopRunner acquires Spring, raises $40M

ShopRunner is announcing its first infusion of venture funding under CEO Sam Yagan, plus an acquisition of the shopping app Spring. Sources also say it’s readying a major overhaul of its mobile app.

Powered by WPeMatico

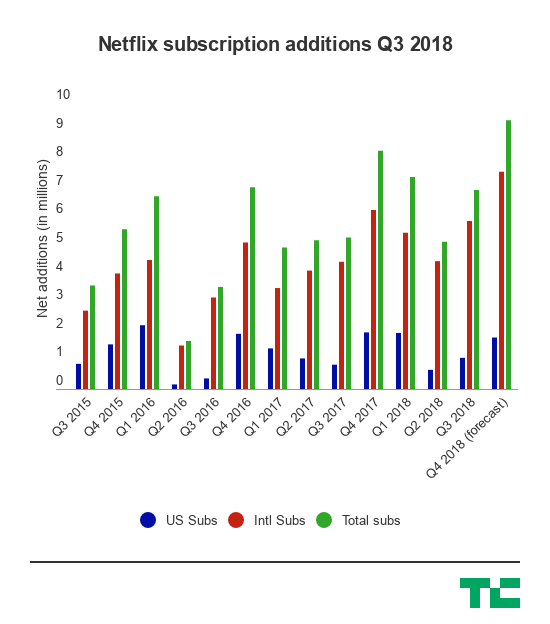

After a disappointing second quarter, Netflix is back in Wall Street’s good graces. The company just released its third-quarter earnings report, and as of 5:30pm East Coast time, the stock is up 12 percent in after-hours trading.

The most important number here is subscriber growth, and that’s where Netflix came in way ahead of expectations, with 6.96 million net additions, compared to the 5.07 million that analysts predicted. The service now has a total of 137 million members, and 130 million paying members.

The company also reported earnings of 89 cents per share on revenue of $4 billion — analysts had predicted EPS of 68 cents.

In addition to reporting on the latest financials, Netflix’s letter to shareholders also offers an update on its original content strategy. It distinguishes between two different types of Netflix Originals — the ones like “Orange Is the New Black,” where Netflix gets the first window for distribution, and others like “Stranger Things,” where it actually owns the content.

The company says:

Today, we employ hundreds of people in physical production, working on a wide variety of owned titles spread across scripted and unscripted series, kids, international content, standup, docs and feature films from all over the world. To support our efforts, we’ll need more production capacity; we recently announced the selection of Albuquerque, New Mexico as the site of a new US production hub, where we anticipate bringing $1 billion dollars in production over the next 10 years and creating up to 1,000 production jobs per year. Our internal studio is already the single largest supplier of content to Netflix (on a cash basis).

Netflix also says romance has been big recently, thanks to its “Summer of Love” slate of original films, which have been watched by more than 80 million accounts. Apparently “To All The Boys I’ve Loved Before” did particularly well, becoming one of Netflix’s most-watched original films, “with strong repeat viewing.”

The service plans to release “Gravity” director Alfonso Cuarón’s new film “Roma” in December, which has already been getting rave reviews at film festivals. While Netflix’s original movies generally have a minimal presence in theaters, the company says “Roma” (like Paul Greengrass’ “22 July”) will be released on more than 100 screens worldwide — not a blockbuster rollout, but not a perfunctory release, either.

The company is forecasting the addition of 9.4 million new members in the fourth quarter.

Powered by WPeMatico

When Cisco bought Ann Arbor, Michigan security company, Duo for a whopping $2.35 billion earlier this month, it showed the growing value of security and security startups in the view of traditional tech companies like Cisco.

In yesterday’s earnings report, even before the ink had dried on the Duo acquisition contract, Cisco was reporting that its security business grew 12 percent year over year to $627 million. Given those numbers, the acquisition was top of mind in CEO Chuck Robbins’ comments to analysts.

“We recently announced our intent to acquire Duo Security to extend our intent-based networking portfolio into multi- cloud environments. Duo’s SaaS delivered solution will expand our cloud security capabilities to help enable any user on any device to securely connect to any application on any network,” he told analysts.

Indeed, security is going to continue to take center stage moving forward. “Security continues to be our customers number one concern and it is a top priority for us. Our strategy is to simplify and increase security efficacy through an architectural approach with products that work together and share analytics and actionable threat intelligence,” Robbins said.

That fits neatly with the Duo acquisition, whose guiding philosophy has been to simplify security. It is perhaps best known for its two-factor authentication tool. Often companies send a text with a code number to your phone after you change a password to prove it’s you, but even that method has proven vulnerable to attack.

What Duo does is send a message through its app to your phone asking if you are trying to sign on. You can approve if it’s you or deny if it’s not, and if you can’t get the message for some reason you can call instead to get approval. It can also verify the health of the app before granting access to a user. It’s a fairly painless and secure way to implement two-factor authentication, while making sure employees keep their software up-to-date.

Duo Approve/Deny tool in action on smartphone.

While Cisco’s security revenue accounted for a fraction of the company’s overall $12.8 billion for the quarter, the company clearly sees security as an area that could continue to grow.

Cisco hasn’t been shy about using its substantial cash holdings to expand in areas like security beyond pure networking hardware to provide a more diverse recurring revenue stream. The company currently has over $54 billion in cash on hand, according to Y Charts.

Cisco spent a fair amount money on Duo, which according to reports has $100 million in annual recurring revenue, a number that is expected to continue to grow substantially. It had raised over $121 million in venture investment since inception. In its last funding round in September 2017, the company raised $70 million on a valuation of $1.19 billion.

The acquisition price ended up more than doubling that valuation. That could be because it’s a security company with recurring revenue, and Cisco clearly wanted it badly as another piece in its security solutions portfolio, one it hopes can help keep pushing that security revenue needle ever higher.

Powered by WPeMatico

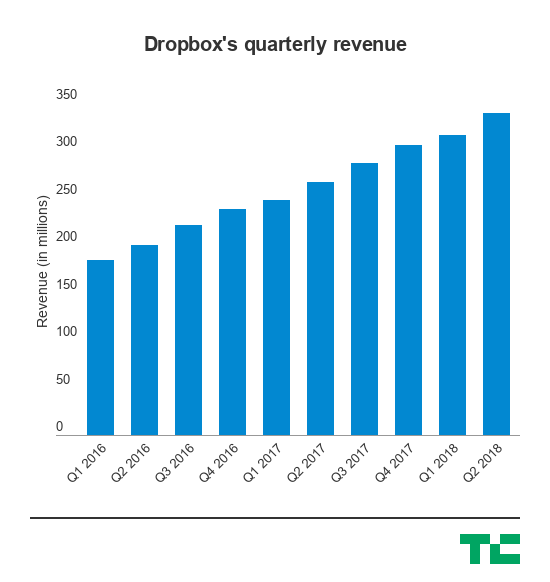

Back when Dennis Woodside joined Dropbox as its chief operating officer more than four years ago, the company was trying to justify the $10 billion valuation it had hit in its rapid rise as a Web 2.0 darling. Now, Dropbox is a public company with a nearly $14 billion valuation, and it once again showed Wall Street that it’s able to beat expectations with a now more robust enterprise business alongside its consumer roots.

Dropbox’s second quarter results came in ahead of Wall Street’s expectations on both the earnings and revenue front. The company also announced that Dennis Woodside will be leaving the company. Woodside joined at a time when Dropbox was starting to figure out its enterprise business, which it was able to grow and transform into a strong case for Wall Street that it could finally be a successful publicly traded company. The IPO was indeed successful, with the company’s shares soaring more than 40 percent in its debut, so it makes sense that Woodside has essentially accomplished his job by getting it into a business ready for Wall Street.

“I think as a team we accomplished a ton over the last four and a half years,” Woodside said in an interview. “When I joined they were a couple hundred million in revenue and a little under 500 people. [CEO] Drew [Houston] and Arash [Ferdowsi] have built a great business, since then we’ve scaled globally. Close to half our revenue is outside the U.S., we have well over 300,000 teams for our Dropbox business product, which was nascent there. These are accomplishments of the team, and I’m pretty proud.”

The stock initially exploded in extended trading by rising more than 7 percent, though even prior to the market close and the company reporting its earnings, the stock had risen as much as 10 percent. But following that spike, Dropbox shares are now down around 5 percent. Dropbox is one of a number of SaaS companies that have gone public in recent months, including DocuSign, that have seen considerable success. While Dropbox has managed to make its case with a strong enterprise business, the company was born with consumer roots and has tried to carry over that simplicity with the enterprise products it rolls out, like its collaboration tool Dropbox Paper.

Here’s a quick rundown of the numbers:

So, not only is Dropbox able to show that it can continue to grow that revenue, the actual value of its users is also going up. That’s important, because Dropbox has to show that it can continue to acquire higher-value customers — meaning it’s gradually moving up the Fortune 100 chain and getting larger and more established companies on board that can offer it bigger and bigger contracts. It also gives it the room to make larger strategic moves, like migrating onto its own architecture late last year, which, in the long run could turn out to drastically improve the margins on its business.

“We did talk earlier in the quarter about our investment over the last couple years in SMR technology, an innovative storage technology that allows us to optimize cost and performance,” Woodside said. “We continue to innovate ways that allow us to drive better performance, and that drives better economics.”

The company is still looking to make significant moves in the form of new hires, including recently announcing that it has a new VP of product and VP of product marketing, Adam Nash and Naman Khan, respectively. Dropbox’s new team under CEO Drew Houston are tasked with continuing the company’s path to cracking into larger enterprises, which can give it a much more predictable and robust business alongside the average consumers that pay to host their files online and access them from pretty much anywhere.

In addition, there are a couple executive changes as Woodside transitions out. Yamini Rangan, currently VP of Business Strategy & Operations, will become Chief Customer Officer reporting to Houston, and comms VP Lin-Hua Wu will also report to Houston.

Dropbox had its first quarterly earnings check-in and slid past the expectations that Wall Street had, though its GAAP gross margin slipped a little bit and may have offered a slight negative signal for the company. But since then, Dropbox’s stock hasn’t had any major missteps, giving it more credibility on the public markets — and more resources to attract and retain talent with compensation packages linked to that stock.

“Our retention has been quite strong,” Woodside said. “We see strong retention characteristics across the customer set we have, whether it’s large or small. Obviously larger companies have more opportunity to expand over time, so our expansion metrics are quite strong in customers of over several hundred employees. But even among small businesses, Dropbox is the kind of product that has gravity. Once you start using it and start sharing it, it becomes a place where your business is small or large is managing all its content, it tends to be a sticky experience.”

Powered by WPeMatico

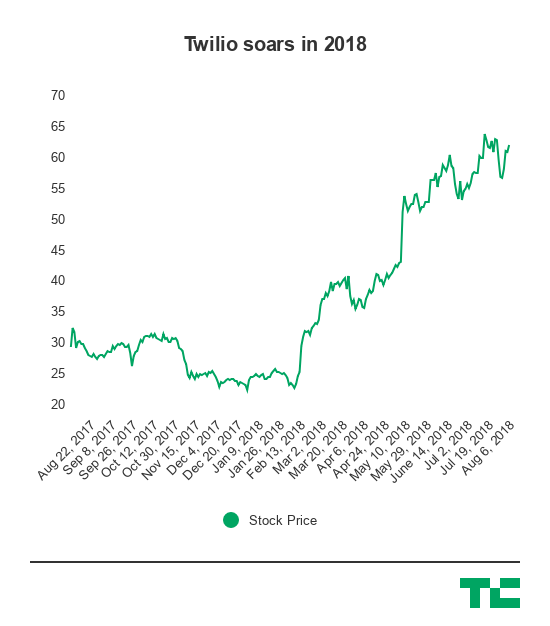

Twilio today reported a positive quarter that brought it to profitability — on an adjusted basis — ahead of schedule for Wall Street, sending the stock soaring 16 percent in extended hours after the release came out.

While according to traditional accounting principles Twilio still lost money (this usually includes stock-based compensation, a key component of compensation packages), the company is still showing that it has the capability of being profitable. Born as a go-to tool for startups and larger companies to handle their text- and telephone-related operations, Twilio was among a wave of IPOs in 2016 that has more or less continued into this year. The company’s stock has more than doubled in the past year, and is up nearly 170 percent this year alone. Twilio also brought in revenue ahead of Wall Street expectations.

Still, as a services business, Twilio has to show that it can continue to scale its business while absorbing the cost of the infrastructure required and acquire new customers. It also has to ensure that those customers aren’t leaving, or at least that it’s bringing on enough new developers more quickly than they are leaving. Larger enterprises, as a result, can be more attractive because they’re more predictable and can lead to bigger buckets of revenue for the company — and, well, most larger companies still need communications support in some way still today.

On an adjusted basis, Twilio said it earned 3 cents per share, ahead of the loss of 5 cents that analysts were expecting. It said it brought in $147.8 million in revenue compared to $131.1 million analysts were expecting, so it’s a beat on both lines, and more importantly shows that Twilio may be able to morph its toolkit into a mainline business that can end up as the backbone of any company’s communication with their customers or users.

Powered by WPeMatico