Earnings

Auto Added by WPeMatico

Auto Added by WPeMatico

For being the richest company ever with $243 billion in cash, Apple sure cuts corners in the stingiest ways. The hardware giant became the first trillion-dollar company this week. Yet it’s tough to reconcile Apple earning $11 billion in profit per quarter with it still screwing us over on cords and keyboards. The “it just works” philosophy has slipped through the cracks of the money-printing machine. It’s not that Apple couldn’t afford to fix the problems, it’s just ensnared in hubris such that it doesn’t see them as important.

We still turn to Apple because it makes the best core products. But the edges of the customer experience have frayed like the wires of a Lightning cable. The key to Apple’s fortune is obviously selling high margin iPhones, not these ways it nickels and dimes us. But the company has an opportunity to raise its standards after this milestone, and win back the faith that could push it to a $2 trillion market cap.

Image via Sophia Cannon

Image via Notebookcheck

[Featured Image via Instructibles]

Powered by WPeMatico

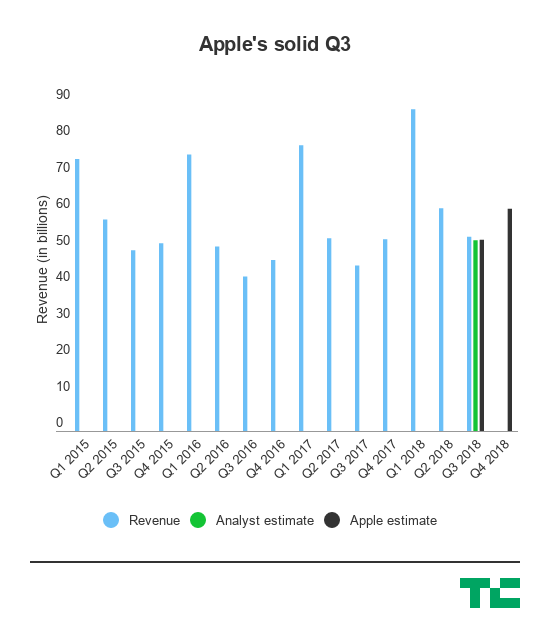

Apple is inching closer and closer to becoming a $1 trillion company today after posting third-quarter results that beat what analysts were expecting and bumping the stock another few percentage points — which, by Apple standards, is tens of billions of dollars.

The company’s stock is up around 2.5 percent this afternoon after the report, which at a prior market close with a market cap of around $935 billion, is adding nearly another $20-plus billion to its market cap. A few quarters ago we were talking about how Apple was in shooting distance of that $1 trillion mark, but now it seems more and more like Apple will actually hit it. Apple is headed into its most important few quarters as we hit the back half of the year, with its usual new lineup of iPhones and other products and its accompanying critical holiday quarter.

Here’s a quick breakdown of the numbers:

So in all, the shipment numbers were hit or miss at a granular level, but at the same time the iPhone is generating a lot more revenue than it did last year — implying that there might be a shifting mix toward more expensive iPhones. Apple’s strategy to figure out if it could unlock a more premium tier in consumer demand, then, may be panning out and helping once again drive the company’s growth. It’s then padding out the rest of that with growth in services and other products like it has in the past few quarters as Apple heads into the end of the year.

In the past year or so, Apple’s stock has continued to rise even though there may have been some dampened expectations for its latest super-premium iPhone, the iPhone X. Its shares are up more than 20 percent in the past year, and in the second quarter the company announced that it would return an additional $100 billion to investors in a new capital return program, which at the time also sparked a considerable jump in its stock. Apple hasn’t delivered a product that has entirely changed the market calculus like it did when it first started rolling out larger iPhones, but its strategy of incremental improvements and maneuvering in Wall Street continues to provide it some momentum as it heads toward $1 trillion.

Powered by WPeMatico

Adobe reported its Q2 FY’18 earnings yesterday and the news was quite good. The company announced $2.2 billion in revenue for the quarter up 24 percent year over year. That puts them on an impressive $8.8 billion run rate, within reach of becoming the next $10 billion software company (or at least on a run rate).

Revenue was up across all major business lines, but as has been the norm, the vast majority comes from the company’s bread and butter, Creative Cloud, which houses the likes of Photoshop, InDesign and Dreamweaver, among others. In fact digital media, which includes Creative Cloud and Document Cloud accounted for $1.55 billion of the $2.2 billion in total revenue. The vast majority of that, $1.30 billion was from the creative side of the house with Document Cloud pulling in $243 million.

Adobe has been mostly known as a creative tools company until recent years when it also moved into marketing, analytics and advertising. Recently it purchased Magento for $1.6 billion, giving it a commerce component to go with those other pieces. Clearly Adobe has set its sights on Salesforce, which also has a strong marketing component and is not coincidentally perhaps, the most recently crowned $10 billion software company.

Adobe CEO Shantanu Narayen speaking to analysts on the post-reporting earnings call sees Magento as filling in a key piece across understanding the customer from shopping to purchase. “The acquisition of Magento will make Adobe the only company with leadership in content creation, marketing, advertising, analytics and now commerce, enabling real-time personalized experiences across the entire customer journey, whether on the web, mobile, social, in-product or in-store. We believe the addition of Magento expands our available market opportunity, builds out our product portfolio, and addresses a key underserved customer need,” Narayen told analysts.

If Adobe could find a way to expand that marketing and commerce revenue, it could easily surpass that $10 billion revenue run rate threshold, but so far while it has been growing, it remains less than half of the Creative revenue at $586 million. Yes, it grew at an 18 percent year over year clip, but it seems as though there is potential for so much more there and clearly Narayen hopes that the money spent on Magento will help drive that growth.

Even while it was announcing its revenue, rival Salesforce was meeting with Marketing Cloud customers in Chicago at the Salesforce Connections conference, a move that presented an interesting juxtaposition between the two competitors. Both have a similar approach to the marketing side, while Salesforce concentrates on the customer including CRM and service components. Adobe differentiates itself with content, which shows up on the balance sheet as the majority of its revenue .

Both companies have growth in common too. Salesforce has been on quite a run over the last five years reaching $3 billion in revenue for the first time last quarter. Adobe hit $2 billion for the first time in November. Consider that prior to moving to a subscription model in 2013, Adobe had revenue of $995 billion. Since it moved to that subscription model, it has reaped the benefits of recurring revenue and grown steadily ever since.

Each has used strategic acquisitions to help fuel that growth with Salesforce acquiring 27 companies since 2013 and Adobe 13, according to Crunchbase data. Each has bought a commerce company with Adobe buying Magento this year and Salesforce grabbing Demandware two years ago.

Adobe has the toolset to keep the marketing side of its business growing. It might never reach the revenue of the creative side, but it could help push the company further than it’s ever been. Ten billion dollars seems well within reach if things continue along the current trajectory.

Powered by WPeMatico

")

Excited to announce that this year’s The Europas Unconference & Awards is shaping up! Our half day Unconference kicks off on 3 July, 2018 at The Brewery in the heart of London’s “Tech City” area, followed by our startup awards dinner and fantastic party and celebration of European startups!

The event is run in partnership with TechCrunch, the official media partner. Attendees, nominees and winners will get deep discounts to TechCrunch Disrupt in Berlin, later this year.

The Europas Awards are based on voting by expert judges and the industry itself. But key to the daytime is all the speakers and invited guests. There’s no “off-limits speaker room” at The Europas, so attendees can mingle easily with VIPs and speakers.

What exactly is an Unconference? We’re dispensing with the lectures and going straight to the deep-dives, where you’ll get a front row seat with Europe’s leading investors, founders and thought leaders to discuss and debate the most urgent issues, challenges and opportunities. Up close and personal! And, crucially, a few feet away from handing over a business card. The Unconference is focused into zones including AI, Fintech, Mobility, Startups, Society, and Enterprise and Crypto / Blockchain.

We’ve confirmed 10 new speakers including:

Eileen Burbidge, Passion Capital

Carlos Eduardo Espinal, Seedcamp

Richard Muirhead, Fabric Ventures

Sitar Teli, Connect Ventures

Nancy Fechnay, Blockchain Technologist + Angel

George McDonaugh, KR1

Candice Lo, Blossom Capital

Scott Sage, Crane Venture Partners

Andrei Brasoveanu, Accel

Tina Baker, Jag Shaw Baker

We’d love for you to ask your friends to join us at The Europas – and we’ve got a special way to thank you for sharing.

Your friend will enjoy a 15% discount off the price of their ticket with your code, and you’ll get 15% off the price of YOUR ticket.

That’s right, we will refund you 15% off the cost of your ticket automatically when your friend purchases a Europas ticket.

So you can grab tickets here.

Public Voting is still humming along. Please remember to vote for your favourite startups!

Awards by category:

Hottest Media/Entertainment Startup

Hottest E-commerce/Retail Startup

Hottest Marketing/AdTech Startup

Hottest Enterprise, SaaS or B2B Startup

Hottest Platform Economy / Marketplace

Hottest Cyber Security Startup

Hottest Internet of Things Startup

Fastest Rising Startup Of The Year

Hottest GreenTech Startup of The Year

Best Angel/Seed Investor of the Year

Hottest VC Investor of the Year

Hottest Blockchain/Crypto Startup Founder(s)

Hottest Blockchain Protocol Project

Hottest Corporate Blockchain Project

Hottest Blockchain ICO (Europe)

Hottest Financial Crypto Project

Hottest Blockchain for Good Project

Hottest Blockchain Identity Project

Hall Of Fame Award – Awarded to a long-term player in Europe

The Europas Grand Prix Award (to be decided from winners)

The Awards celebrates the most forward thinking and innovative tech & blockchain startups across over some 30+ categories.

Startups can apply for an award or be nominated by anyone, including our judges. It is free to enter or be nominated.

Instead of thousands and thousands of people, think of a great summer event with 1,000 of the most interesting and useful people in the industry, including key investors and leading entrepreneurs.

• No secret VIP rooms, which means you get to interact with the Speakers

• Key Founders and investors speaking; featured attendees invited to just network

• Expert speeches, discussions, and Q&A directly from the main stage

• Intimate “breakout” sessions with key players on vertical topics

• The opportunity to meet almost everyone in those small groups, super-charging your networking

• Journalists from major tech titles, newspapers and business broadcasters

• A parallel Founders-only track geared towards fund-raising and hyper-networking

• A stunning awards dinner and party which honors both the hottest startups and the leading lights in the European startup scene

• All on one day to maximise your time in London. And it’s PROBABLY sunny!

That’s just the beginning. There’s more to come…

Interested in sponsoring the Europas or hosting a table at the awards? Or purchasing a table for 10 or 12 guest or a half table for 5 guests? Get in touch with:

Petra Johansson

Petra@theeuropas.com

Phone: +44 (0) 20 3239 9325

Powered by WPeMatico

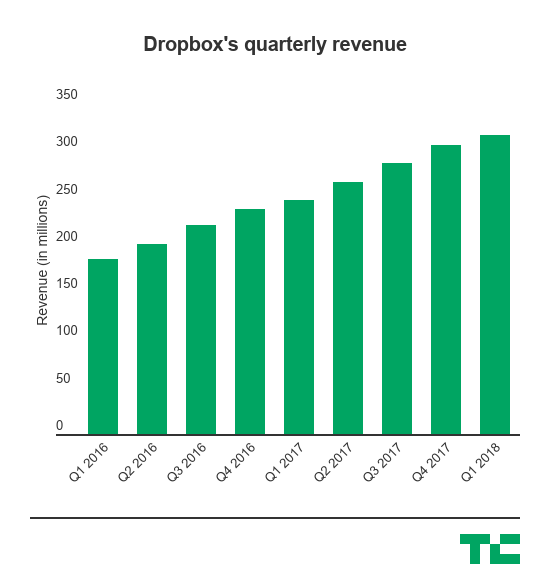

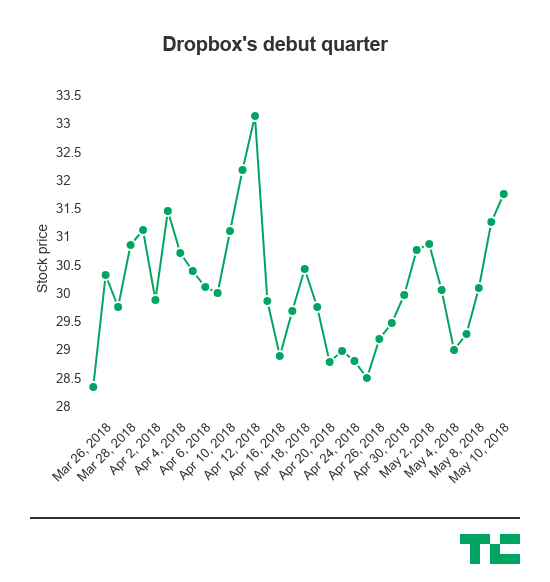

Dropbox made its debut as a public company earlier this year and today passed through its first milestone of reporting its results to public investors, and it more or less beat expectations set for Wall Street on the top and bottom line.

The company reported more revenue and beat expectations for earnings that Wall Street set, bringing in $316.3 million in revenue and appearing to pick up momentum among its paying user base. It also said it had 11.5 million paying users, a jump from last year. However, the stock was largely flat in extended trading. One small negative signal — and it definitely appears to be a small one — was that its GAAP gross margin slipped slightly to 61.9% from 62.3% a year earlier. Dropbox is a software company that’s supposed to have great margins as it begins to ramp up its own hardware, but that slipping margin may end up being something that investors will zero in on going forward. Still, as the company continues to ramp up the enterprise component of its business, the calculus of its business may change over time.

This is a pretty important moment for the company, as it was a darling in Silicon Valley and rocketed to a $10 billion valuation in the early phases of the Web 2.0 era but began to face a ton of criticism as to whether it could be a robust business as larger companies started to offer cloud storage as a perk and not a business. Dropbox then found itself going up against companies like Box and Microsoft as it worked to create an enterprise business, but all this was behind closed doors — and it wasn’t clear if it was able to successfully maneuver its way into a second big business. Now the company is beholden to public shareholders and has to show all this in the open, and it serves as a good barometer of not just storage and collaboration businesses, but also some companies that are looking to drastically simplify workflow processes and convert that into a real business (like Slack, for example).

Here’s the final scorecard for the company:

(The GAAP and non-GAAP comparison is typically related to share-based compensation, which is a key component of employee compensation and retention.)

Dropbox was largely considered to be a successful IPO, rising more than 40% in its trading debut. That does mean that it may have left some money on the table, but its operating losses have been largely stable, even as it looks to woo larger enterprise customers as it — which is a bit of a taller order than its typical growth amid consumers that’s heavily driven by organic growth. Those larger enterprise customers offer more stable, and larger, revenue streams than a consumer base that faces a variety of options as many companies start to offer free storage. The company is now worth well over that original $10 billion valuation as a public company. Dropbox says it has more than 500 million users.

Since going public, the stock has had its ups and downs, but for the most part hasn’t dipped below that significant jump it saw from day one. Keeping that number propped up — and growing — is an important part of growing a business as a public company as it waves off more intense scrutiny and pressure for change from public shareholders, as well as offering competitive compensation packages for incoming employees in order to attract the best talent. It’s also good for morale as it offers a kind of grade for how the company is doing in the eyes of the public, though CEOs of companies often say they are committed toward long-term goals. The company’s shares are up around 11% since going public.

While there have been a wave of enterprise IPOs this year, including zScalar and Pluralsight’s upcoming IPO, Dropbox was largely considered to be a potential gauge of whether the IPO window was still open this year because of its hybrid nature. Dropbox started off as a consumer company based around a dead-simple approach of hosting and sharing files online, and used that to build a massive user base even as the cost of cloud storage was rapidly commoditized. But it also is building a robust enterprise-focus business, and continues to roll out a variety of tools to woo those businesses with consistent updates to products like its document tool Paper. Last month, the company started rolling out templates, as it looked to make traditional workflow processes easier and easier for companies in order to capture their interest much in the same way it captured the interest of consumers at large.

Powered by WPeMatico

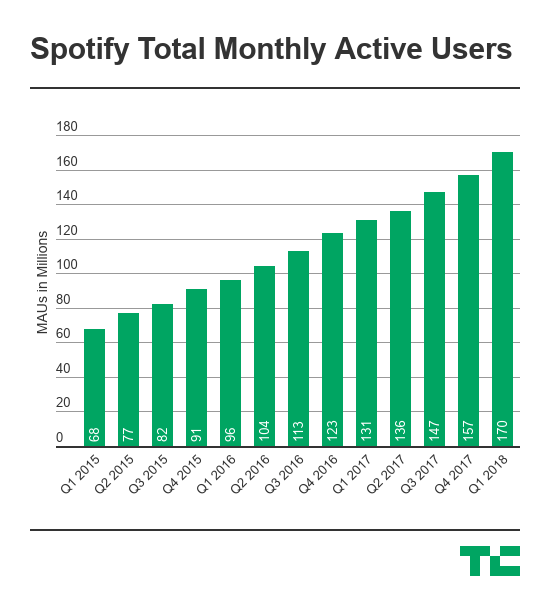

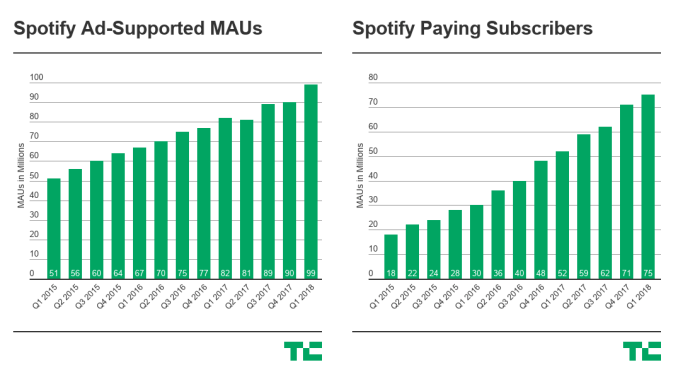

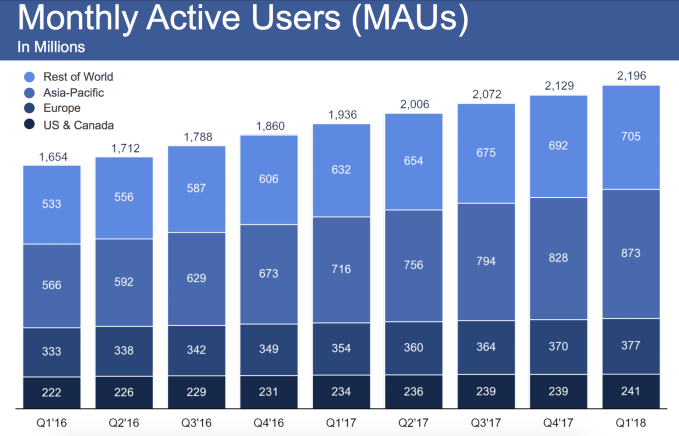

In Spotify’s first ever earnings report, the streaming music came up a little short, pulling in $1.36 billion revenue in Q1 2018. That’s compared to Wall Street’s estimates of $1.4 billion in revenue and an adjusted EPS loss of $0.34. Spotify hit 170 million monthly active users, up 6.9 percent from 159 million in Q4 2017 and 99 million ad-supported users. It also hit 75 million Premium Subscribers, up 30 percent year-over-year, and 75 million paid subscribers, up 5.6 percent from 71 million in Q4 and up 45 percent YoY.

Interestingly, the MAU count indicates that 4 million of Spotify’s 75 million subscribers pay but don’t listen. Spotify confirmed as much. For reference, Apple Music has roughly 40 million subscribers.

Spotify’s results were in line with the guidance it gave yet Wall Street was still disappointed. Spotify shares promptly fell over 8 percent in after-hours trading to around $156, beneath its IPO pop a month ago but still above its $149 day one closing price and $132 IPO pricing.

Spotify’s Gross Margin was 24.9 percent in Q1, over the top of its guidance range of 23-24 percent. Its operating loss was $48.9 million, which improved significantly, and come in under the $59 million to $95 million operating loss Spotify warned of. The music company now has $1.91 billion in cash and cash equivalents at the end of Q1.

As for Q2 guidance, Spotify expects 175 to 180 million MAU, 79 to 83 million paid subscribers, and $1.3 to $1.55 billion in revenue, excluding the impoact of foreign exchange rates. It’s planning an operating loss of $71 million to $167 million, in part due to a $35 million to $42 million expense related to its direct listing debut on the public markets.

During the earnings call, CEO Daniel Ek said he hasn’t seen any significant impact from increased promotion by its competitor Apple Music. In fact, churn hit an all-time low of 4.7 percent, and lifetime value to customer acquisition cost ratio is holding firm at 2.7:1. But overall, “We don’t see this as a winner takes all market” Ek says.

As for voice-activated smart speakers, Ek said “We view it longterm as an opportunity not a threat” since Spotify is available on Google Home and Amazon Alexa devices.

Spotify is hoping to boost paid subscriber numbers by first luring more users to its free ad-supported service. Last month it unveiled a revamped free tier that lets users listen to songs on-demand on particular Spotify-controlled playlists instead of only being able to play in shuffle mode. The idea is that once users get a taste of on-demand listening, they’ll pay to upgrade so they can listen to whatever they want across the whole catalog.

That strategy could not only boost subscriber numbers, but also give Spotify more leverage over the record labels. More than 30 percent of all Spotify listening now happens on its owned playlists. That gives it the power to choose what will become a hit, and in turn means record labels need to play nice. This could help Spotify secure more exclusive content and a better bargaining position in royalty negotiations.

Powered by WPeMatico

Samsung’s latest earnings report is a succinct lesson in hoping for the best and preparing for the worst. The actual news here is pretty positive, as the company reports a record operating profit, courtesy of high demand for its components and flagship handsets.

But a statement tied to the news mentions “slow demand” no fewer than seven times, as the company looks to temper investor expectations, Those warnings largely revolve around the company’s display panel offerings and a perceived stagnations in the mobile sector in general.

“For the second quarter,” the company writes in a statement, “Samsung expects the Memory Business to maintain its strong performance, but generating overall earnings growth across the company will be a challenge due to weakness in the Display Panel segment and a decline in profitability in the Mobile Business amid rising competition in the high-end segment.”

The slow down, it seems, has already had an impact on the display side, though Samsung’s weathered much worse than this already. Keep in mind how the whole Note 7 debacle didn’t make a dent in the company’s profitability. Samsung is the consumer electronics poster child from the importance of product diversity.

There’s some Apple shade implied here as well. After all, Samsung provides the OLED panel for its chief competitor’s ultra premium handset, leaving Wall Street to infer that less than stellar iPhone X sales was a contributor here. Samsung’s forecast also includes warnings around slowed demand for its own handsets in the next quarter.

“In the Mobile Business,” Samsung writes, “profitability is expected to decline QoQ due to stagnant sales of flagship models amid weak demand and an increase in marketing expenses.” That’s due, at least in part, to a natural cycle as the initial hype dies down — though there also appears to be a larger global smartphone slow down at play here as well. But the company says it believes that will be buoyed in part by increased summer demand for TVs and air conditioners. People might not be buying as many new smartphones in the future, but hey, climate change will make sure we always need ACs.

Powered by WPeMatico

Amongst massive criticism over data privacy, Facebook showed the resiliency of its advertising machine by beating Wall Street’s $11.41 billion revenue estimate in its Q1 2018 earnings report by raking in $11.97 billion in revenue with $1.69 EPS compared to the $1.35 estimate.

Facebook added 48 million daily active users to hit 1.449 billion, up 3.42 percent to revive Facebook’s growth after slower 2.18 percent growth last quarter. But Facebook only added 70 million monthly active users to reach 2.196 billion, a 3.14 percent growth rate that was a little slower than last quarter’s 3.39 percent growth. Both daily and monthly users are up 13 percent year-over-year, showing Facebook’s troubles haven’t paralyzed its growth.

This was perhaps the most tumultuous quarter since Facebook went public. Facebook faced intense criticism regarding the Cambridge Analytica scandal and its data privacy practices, leading a massive pull-back of developer capabilities as Zuckerberg headed to testify before Congress. Last quarter saw Facebook’s first-ever decline in users in a market, with a 700,000 user drop in the U.S. & Canada market following changes to promote well-being that reduced the prevalence of viral videos.

Facebook was able to revive its U.S. & Canada user growth this quarter, perking back up to 185 million, from 184 million last quarter — though that’s just a return to where it was in Q3 2017. Monthly active user count in the market went from 239 to 241 million. That shows that while people might disagree with Facebook’s approach to privacy, they aren’t about to give up their News Feeds.

Demonstrating Facebook’s declining web presence, mobile made up $10.7 billion, or 91 percent of all ad revenue, up from 89 percent last quarter. Facebook reached $4.98 billion in profit, up from a weak $4.26 billion last quarter. Average Revenue Per User reached $5.53, up 30 percent year-over-year thanks to strong gains this quarter in Europe and Asia-Pacific. Facebook’s headcount has swelled 48 percent year-over-year as it’s now half-way to its promise of doubling its security and content moderation staff from 10,000 to 20,000 in 2018.

The recent scandals have put a lot of downward pressure on its share price, but apparently the company thinks it’s a good buy. It’s increased the amount authorized under a share repurchase program by an additional $9 billion, on top of an original $6 billion plan, of which it’s spent $4 billion. It’s partly to offset big stock distributions for employees, but CFO David Wehner also said it was “opportunistic,” aka related to Facebook perceiving its price as too low. Wall Street apparently liked the earnings report as shares are up over 4.38 percent to $166.68 in after-hours trading.

The question is whether the new ads transparency requirements, developer platform crackdown and Facebook’s quest to make using it healthier will show up in next quarter’s earnings. These changes could deter advertisers, give users less functionality to play with and remove low-quality viral content that might make users feel bad but keeps them scrolling.

CEO Mark Zuckerberg wrote that, “Despite facing important challenges, our community and business are off to a strong start in 2018. We are taking a broader view of our responsibility and investing to make sure our services are used for good. But we also need to keep building new tools to help people connect, strengthen our communities, and bring the world closer together.” We’ll get to hear more from him at 2pm Pacific during the earnings call, so stay tuned here.

Updates from the earnings call:

Powered by WPeMatico

Alphabet, Google’s parent company, reported another pretty solid beat this afternoon for its first quarter as it more or less has continued to keep its business growing substantially — and is growing even faster than it was a year ago today.

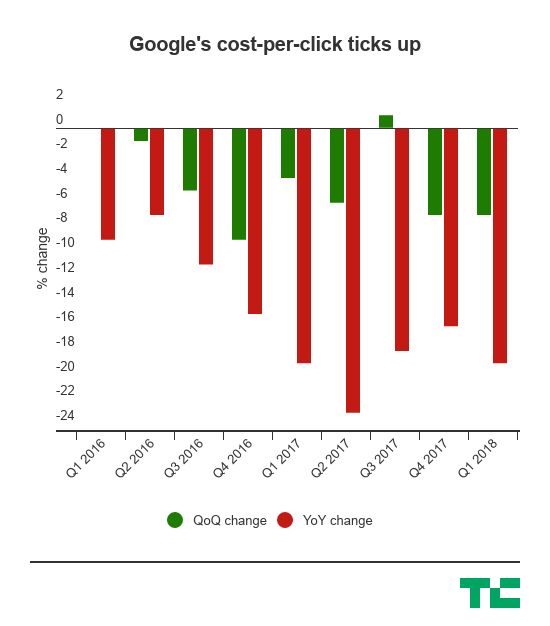

Google said its revenue grew 26% year-over-year to $31.16 billion in the first quarter this year. In the first quarter last year, Google said its revenue had grown 22% between Q1 of 2016 and Q1 of 2017. All this is a little convoluted, but the end result is that Google is actually growing faster than it was just a year ago despite the continued trend of a decline in its cost-per-click — a rough way of saying how valuable an ad is — as more and more web browsing shifts to mobile devices. Last year, Google said it recorded $24.75 billion in the first quarter.

Once again, Alphabet’s “other bets” — its fringe projects like autonomous vehicles and balloons — showed some additional health as that revenue grew while the losses shrank. That’s a good sign as it looks to explore options beyond search, but in the end it still represents a tiny fraction of Google’s overall business. This was also the first quarter that Google is reporting its results following a settlement with Uber, where it received a slice of the company as it ended a spat between its Waymo self-driving division and Uber.

Here’s the final scorecard:

In the end, it’s a beat compared to what Wall Street wanted, and it’s getting a very Google-y response. Investors were looking for earnings of $9.35 per share on $30.36 billion in revenue. Google’s stock is up around 2% in extended trading, which for Google is adding more than $10 billion in value as it races alongside Microsoft and Amazon to chase Apple as the most valuable company in the world by market cap. Google jumped as much as 5% in extended trading, though it’s flattened out

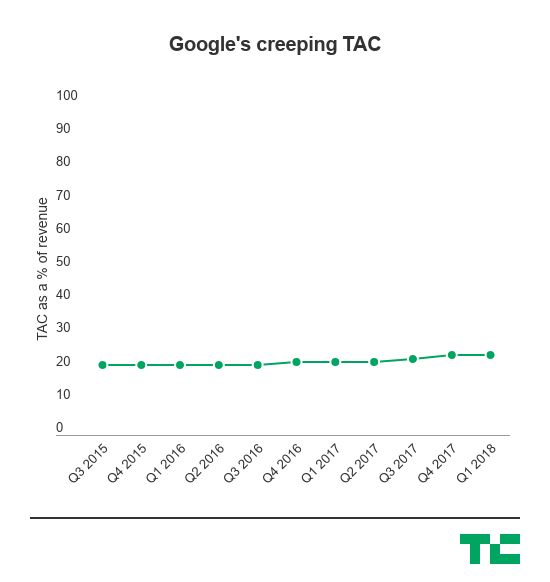

Google’s traffic acquisition cost, or TAC, appears to also remain stable as a percentage of its revenue. This is a little bit of a sticking point for observers for the company and a potential negative signal for investors as more and more web browsing shifts to mobile. It’s ticked up very slowly over the past several years, but is now sitting at around 24% of its total revenue.

Google, at its core, is an advertising company that is going to make money off its billions of users across all of its properties. But as everything goes to mobile devices, the actual value of those ads is going to drop off over time simply because mobile browsing has a different set of behaviors. Google’s business has always been to offset that cost-per-click with a growing number of impressions — and, indeed, it seems like the status quo is sticking around for this one.

While Google’s advertising business continues to chug along, that diversification of revenue streams is going to be increasingly important for the company as a hedge against any potential threats to its advertising income. Already there is some chaos when it comes to what’s happening with user data following a massive scandal where information on as many as 87 million Facebook users ended up with a political research firm, Cambridge Analytica. That backlash centered around user privacy may end up tapping Google, which dominates most of how information travels across the web with Gmail and Search among its other products.

But that still comes at a pretty significant cost. It’s made major investments into tools like Google Cloud (or GCP), but tucked into the earnings report is a line item that shows its “purchases of property and equipment” more than doubled year-over-year to around $7.3 billion, up from $2.5 billion in the first quarter this year. Of course this can encompass a ton of things, but Google still has to actually buy servers if it’s going to run a cloud platform that can compete with AWS or Microsoft’s Azure.

All that feeds into its “other income” stream, which grew from $3.2 billion in Q1 last year to $4.35 billion in the first quarter this year. Amazon’s cloud business is already more than a $10 billion business annually, and that first-mover advantage has served it well as it began a huge shift to how businesses operate on cloud servers. But it also exposed a massive business opportunity for Google, which continues to invest in that.

Powered by WPeMatico

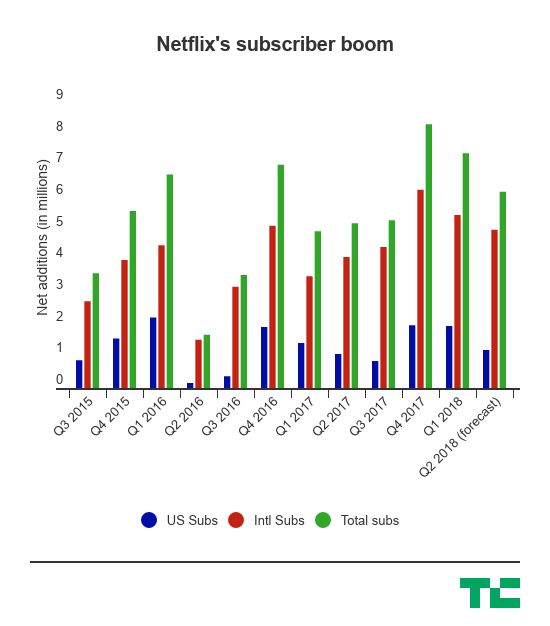

Just last quarter Netflix passed a $100 billion market cap — and we might already be talking about it as a $150 billion company before too long with yet another big financial quarter that sent its stock soaring.

Netflix, again, beat out some expectations Wall Street held for the first quarter and provided a pretty good outlook for the next quarter as well, where it said it expected to add around 6.2 million new subscribers. In the first quarter, Netflix added 7.41 million new subscribers — around 2 million of them domestic and the rest internationally. The company continued to see some pretty strong streaming revenue growth, which was up around 43% year-over-year in the first quarter this year, to around $3.6 billion.

With all this, Netflix now has nearly 119 million paid streaming memberships — and it wasn’t all that long when Netflix finally said just over two years ago that it would begin opening up in hundreds of new countries internationally. The company’s shares are up around 6% in extended trading, sending its market cap up north of $140 billion. And all this subscriber growth, too, comes before we’re seeing a new tie-up with Comcast’s cable subscriptions that may end up driving that even more. As usual, Netflix expects to lose a ton of money and says it expects between -$3 billion to -$4 billion in free cash flow, but that’s usually not what investors are looking for.

One of the big questions Netflix still has right now is what kind of price tag it will carry as a tack-on to a Comcast subscription. Earlier this week, the companies announced that Comcast would bundle Netflix in to its cable subscriptions, offering yet another entry point for Netflix to ferret up potential consumers that haven’t quite cut the cord yet but still might be interested in Netflix’s content. Netflix normally carries a price tag of around $13.99, but the companies have not said what its price will be as part of a cable bundle yet.

Following Netflix’s last earnings report — which it, as you might expect, included some blowout subscriber numbers — the company rocketed past a market cap of $100 billion. Since then it’s only been an upward trend for Netflix, which prior to its first-quarter report was worth more than $130 billion. Despite increasing spend on original content, that subscriber number is still mostly where it gets its market value because it’s a forward predictor of its revenue.

Netflix late last year said it expected to spend between $7 billion and $8 billion on original content this year, a number that seems to periodically get an upward revision and is still a dramatic step up from 2017. The company in its report today said it expected to spend between $7.5 billion and $8 billion on original content, and expects that marketing and content spend to weight toward the second half of 2018.

But it has to continue to invest in original content because it is a way to attract new subscribers, and also because it’s content that it can more easily distribute across different geographies and itself has control of the rights and what happens to it. It relies on shows like Stranger Things or Altered Carbon to bring in new users, which then hopefully stick around and eventually help recoup the cost of those shows — and then the cycle starts anew.

Powered by WPeMatico