Earnings

Auto Added by WPeMatico

Auto Added by WPeMatico

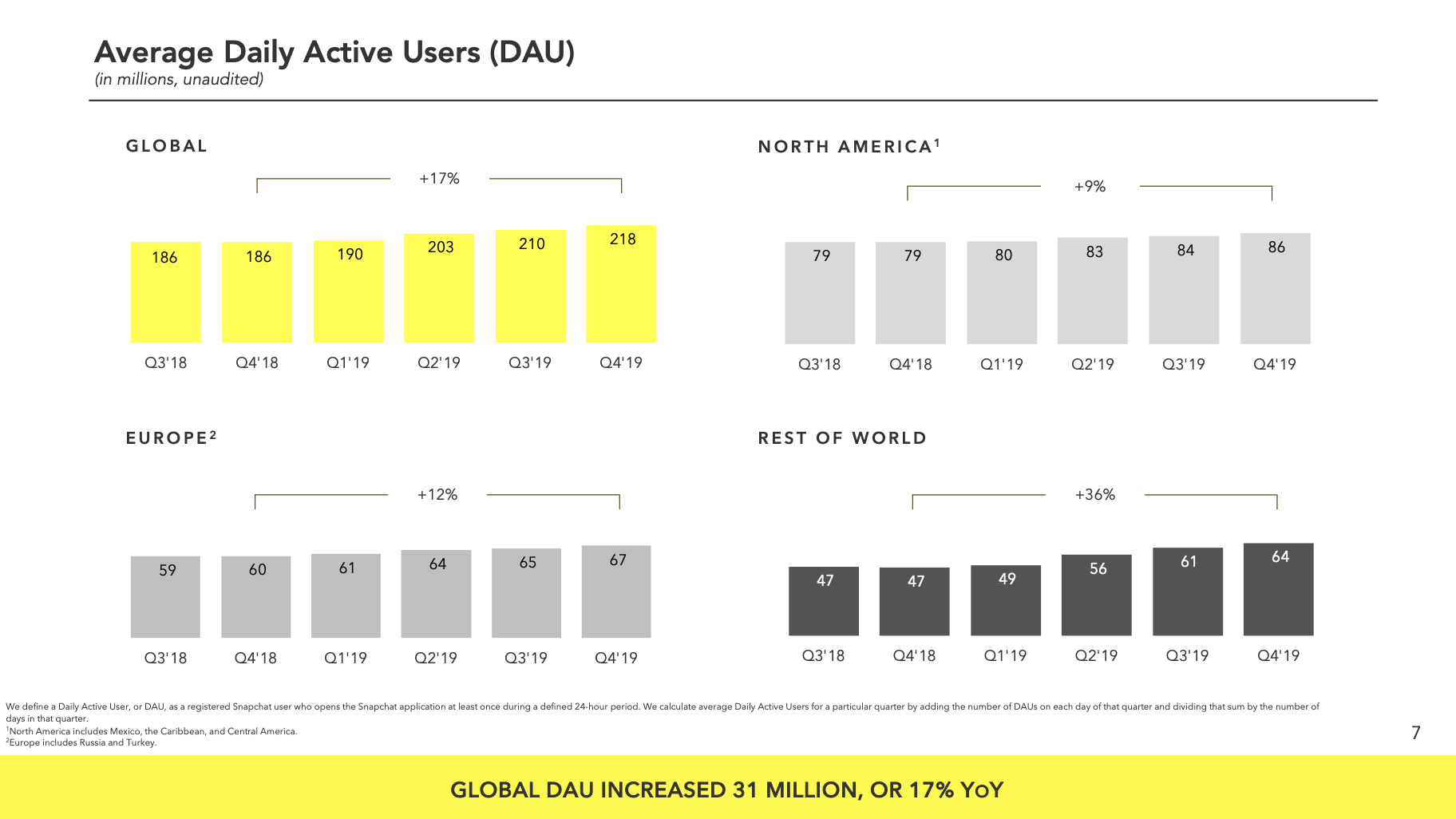

Snapchat still isn’t profitable nearly two years after its IPO. In Q4 2019, Snap lost $241 million on $560.8 million in revenue; that’s up 44% year-over-year and an EPS of $0.03. That comes from adding 8 million daily users to reach a total of 218 million up 3.8% this quarter from 210 million and 17% year-over-year.

The big problem was a one-time $100 million legal settlement that pushed it to lose $49 million more in Q4 2019 than Q4 2018. That comes from a shareholder lawsuit claiming Snap didn’t adequately disclose the impact of competition from Facebook on its business. The IPO was soured by weak user growth as people shifted from Snapchat Stories to Instagram Stories.

Snapchat had a mixed quarter compared to estimates, exceeding the EPS predictions but falling short on revenue. FactSet’s consensus predicted $563 million in revenue and a loss of $0.12 EPS. Estimize’s consensus came in at $568 million in revenue and an EPS gain of $0.02.

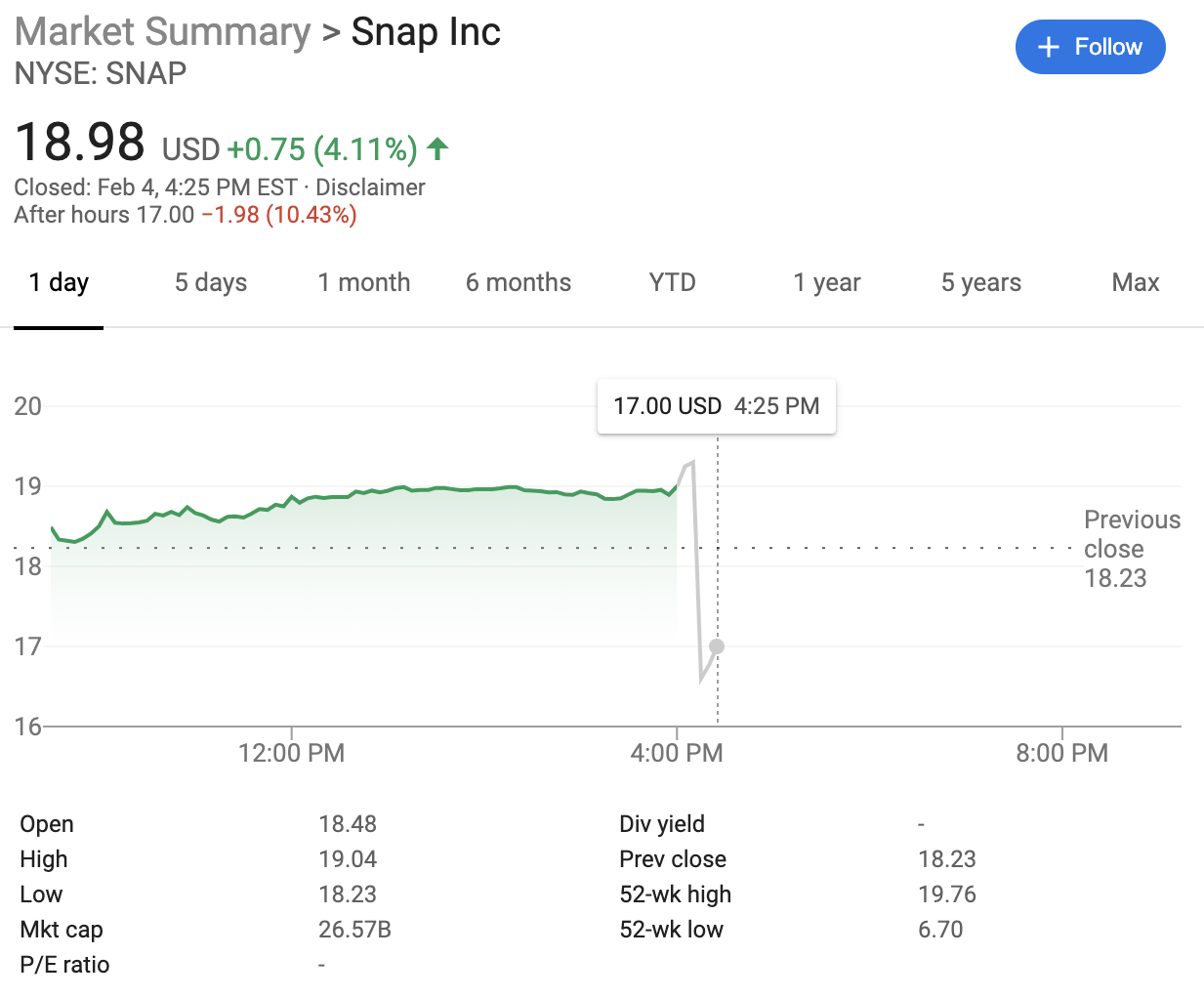

Snapchat shares plunged over 11% in after-hours trading following the announcement. Shares had closed up 4.17% at $18.99 today. That’s up from a low of $4.99 in December 2018 when its user count was shrinking under competition from Instagram Stories. It’s now hovering around its $17 IPO price, but it’s still under its post-IPO pop to $27.09.

Snap gave stronger than expected revenue guidance for Q1 2020 of $450 million to $470 million, and 224 million to 225 million users. The company’s CFO Derek Anderson says that “Q4 marked our first quarter of Adjusted EBITDA profitability at $42 million for the quarter, an improvement of $93 million over the prior year.” Still, he predicts an Adjusted EBITDA in Q1 of negative $90 million to negative $70 million. That’s manageable for Snap without raising more money, since it now has $2.1 billion in cash and marketable securities, down $148 million quarter-after-quarter.

“Throughout the course of 2019, we added 31 million daily active users, largely driven by investments in our core product and improvements to our Android application,” said Snapchat CEO Evan Spiegel . “We’ve recently completed our 2020 strategic planning process and have aligned our teams and resources around our goals of supporting real friendships on Snapchat, expanding our service to a broader global community, investing in our AR and content platforms, and scaling revenue while achieving profitability in order to self-fund our investments in the future.”

Some other highlights:

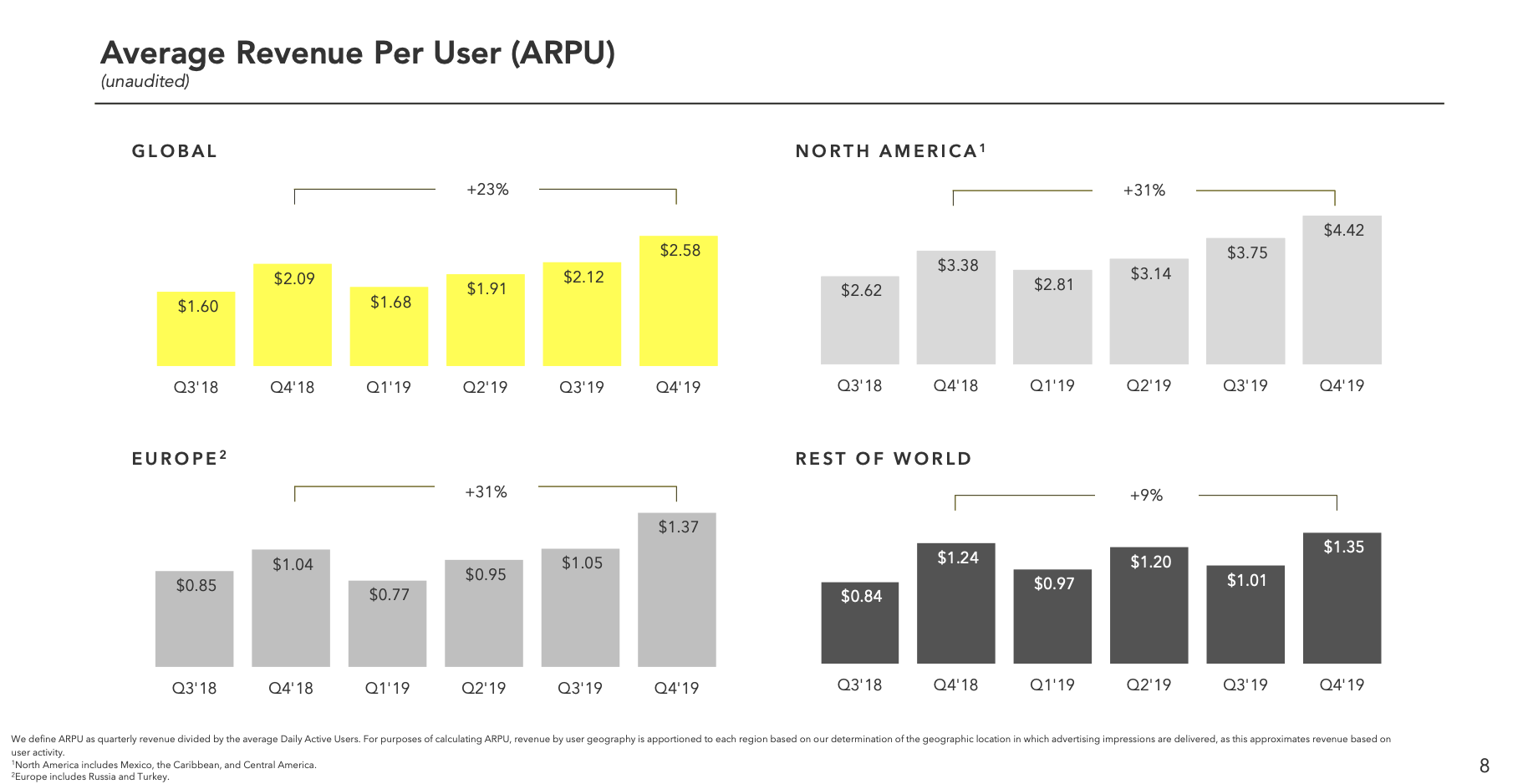

Snapchat’s user growth has been on a tear thanks to international penetration, especially in India, after it re-engineered its Android app for developing markets. It gained users in all markets. Crucially, it raised its average revenue per user 23% from $2.09 in Q4 2018 to $2.58, though only from $1.24 to $1.35 in the Rest of World region, where it’s growing user count the fastest. Snap will need to figure out how to squeeze more cash out of the international market to offset the costs of streaming tons of video to these users.

Q4 saw Snapchat readying several new products that could help boost engagement and therefore ad views. Cameos, first reported by TechCrunch, lets users graft their face onto an actor in an animated GIF like a lightweight deepfake. Bitmoji TV, which won’t run ads initially but could drive attention to Snapchat Discover, offers zany four-minute cartoons that star your Bitmoji avatar. We could see a bump to engagement from these starting in Q1 2020.

To retain its augmented reality filter creators, Snapchat has pledged $750,000 in payouts in 2020. It also expanded the use of product catalog ads, and now lets advertisers buy longer skippable ads.

Outside of the legal settlement, Snapchat is inching closer to profitability, but still has a ways to go. It has managed to develop a strong synergy between its popular chat feature that’s tougher to monetize, and the Stories and Discover content where it can inject ads. The big question is whether Facebook Messenger, Instagram and WhatsApp will get more serious about ephemeral messaging that’s at the core of Snapchat. If it can hold onto the market and maintain its place as where teens talk, it could ride out its costs and build revenue until it’s sustainable for the long-term.

Powered by WPeMatico

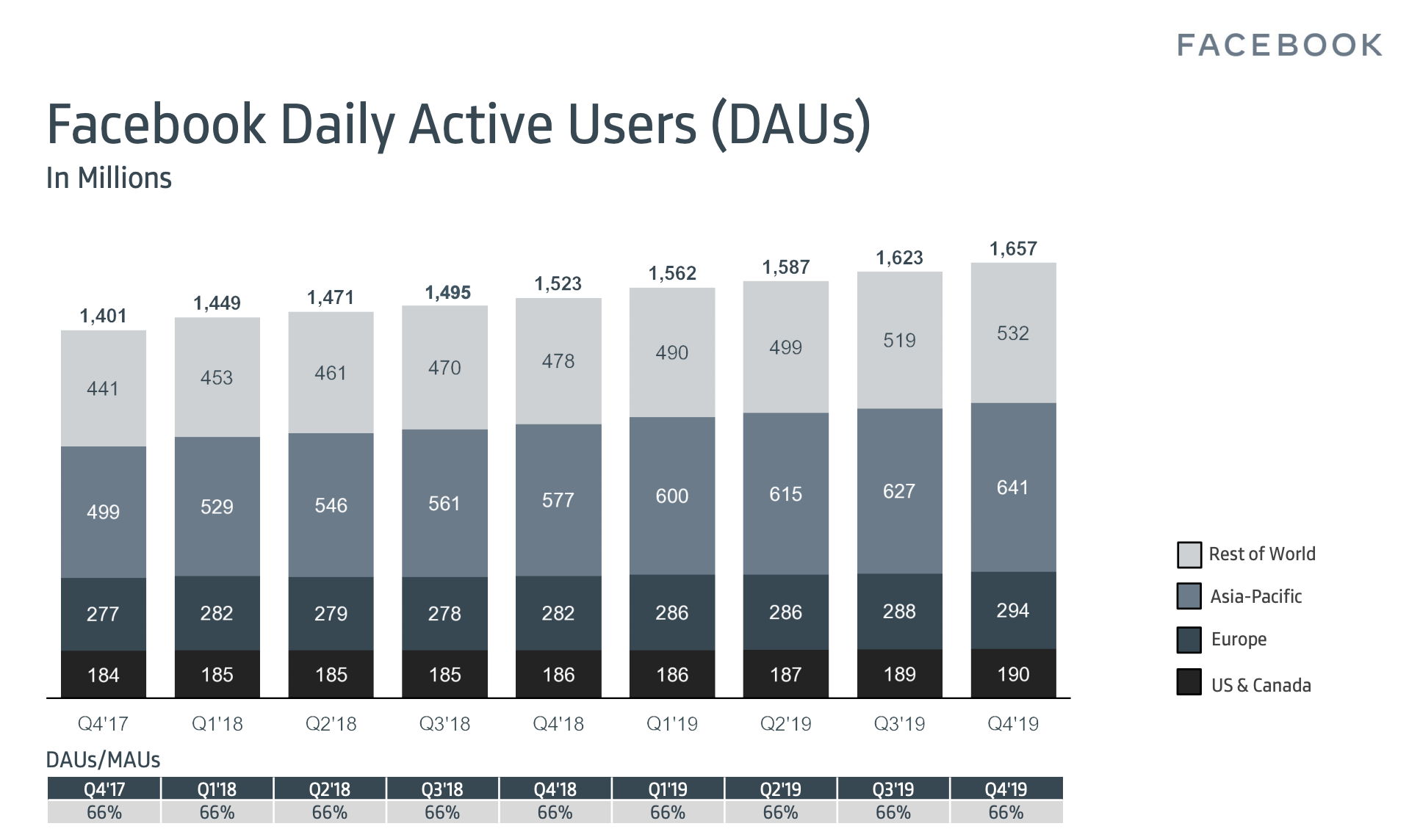

Facebook beat Wall Street estimates in Q4 but slowing profit growth beat up the share price. Facebook reached 2.5 billion monthly users, up 2%, from 2.45 billion in Q3 2019 when it grew 1.65%, and it now has 1.66 billion daily active users, up 2.4% from 1.62 billion last quarter when it grew 2%. Facebook brought in $21.08 billion in revenue, up 25% year-over-year, with $2.56 in earnings per share.

But net income was just $7.3 billion, up only 7% year-over-year compared to 61% growth over 2018. Meanwhile, operating margins fell from 45% over 2018 to 34% for 2019. Expenses grew to $12.2 billion for Q4 2019, up a whopping 34% from Q4 2018. For the year, Facebook’s $46 billion in expenses are up 51% vs 2018. One big source of those expenses? Headcount grew 26% year-over-year to 44,942, and Facebook now has over 1000 engineers working on privacy.

While Facebook’s user base keeps growing rather steadily, it’s having trouble squeezing more and more cash out of them with as much efficiency.

Facebook’s Q4 2019 earnings beat expectations compared to Zack’s consensus estimates of $20.87 billion in revenue and $2.51 earnings per share. Facebook shares fell over 7% in after-hours trading following the earnings announcement after closing up 2.5% at a peak $223.23 today. Still, Facebook remains near its previous share price high before this month.

Facebook CEO Mark Zuckerberg had previously warned that addressing hate speech, election interference, and other content moderation and safety issues would be costly. Still, expenses grew and profits shrunk faster than Wall Street seems to have expected. Facebook will have to hope its promise of using scalable AI to handle more of these jobs comes to fruition soon.

But some might see today as the proper reckoning for Facebook — penance for years of neglecting safety in favor of growth. Facebook’s CFO David Wehner confirms it has also just agreed to pay $550 million in a settlement over its violation of the Illinois Biometric Information Privacy Act. The class action suit stems from Facebook collecting users’ facial recognition data to power its Tag Suggestions feature that recommends friends tag you in photos in which you appear. The record-breaking settlement still falls far short of the $35 billion in potential penalties Facebook could have received.

Facebook’s executives are apparently bullish on its value despite the share price being at a peak, as today Facebook announced plans to grow its share-repurchase program by $10 billion, adding to its previous authorization of buying back up to $24 billion worth.

Facebook managed to add 1 million daily users in the U.S. & Canada region where it earns the most money after returning to growth there last quarter following a year of slow or no growth. Facebook’s stickiness, or daily to monthly active user ratio remained at 66% amidst competition from apps like TikTok and a resurgent Snapchat.

Facebook notes that there are now 2.26 billion users that open either Facebook, Messenger, Instagram, or WhatsApp each day, up from 2.2 billion last quarter. The family of apps sees 2.89 billion total monthly users, up 9% year-over-year.

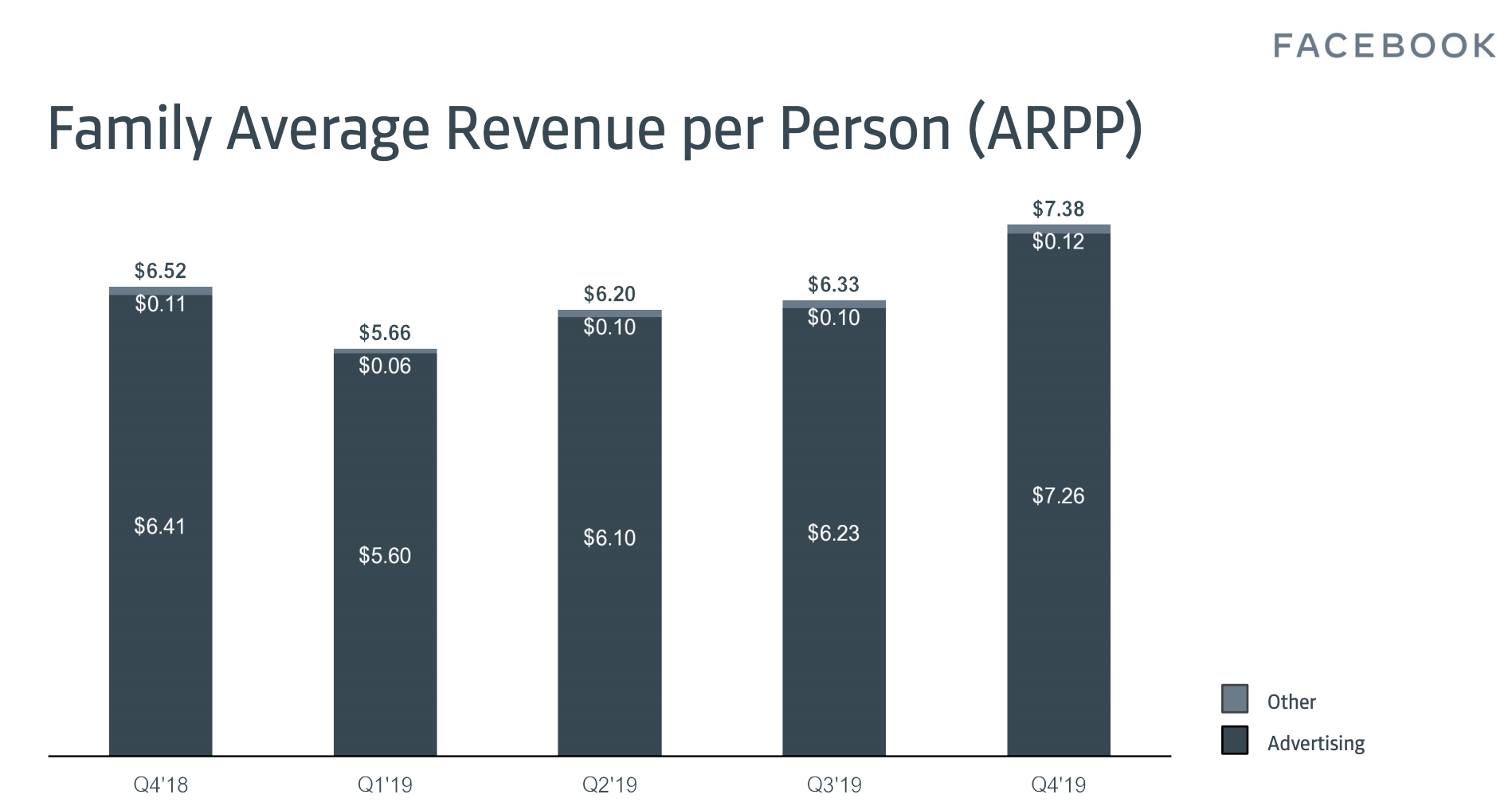

Facebook released a new stat with this earnings report: Family Average Revenue Per Person. That’s essentially the company’s total revenue divided by total users on Facebook, Messenger, Instagram, and WhatsApp. Clearly, the company is trying to use Instagram’s growing ad revenue to make the rest of the company look stronger. This might help mask changes in the Facebook app’s own revenue as teens look to more youthful content feeds. Wehner confirmed the company will cease sharing Facebook-only stats in favor of Family Of Apps stats in late 2020.

Sadly Facebook’s isn’t calling this metric FARPP

Zuckerberg stressed Facebook’s need to stay focused on addressing social issues and consequences of the company’s growth during the earnings call. He said Facebook will continue to make its apps more private and secure.

As for product updates, Zuckerberg seized on opportunities in commerce. Facebook is building out WhatsApp Pay, and he says “I expect this to start rolling out in a number of countries and for us to make a lot of progress here in the next six months.” 140 million small businesses now use its tools. People bought almost $5 million in content on the Oculus Store on Christmas Day, which Zuckerberg called a milestone. He says Facebook’s Spark AR platform is most used of its kind by developers, with hundreds of millions of people experiencing face filters built with it.

Regarding plans to integrate the family’s chat interfaces, Zuckerberg says Messenger, Instagram, and WhatsApp will retain their brands. He also noted they’re already quite integrated on the backend…which could be an attempt to persuade regulators it might be difficult to break up the company.

For guidance, Wehner said “we expect our year-over-year total reported revenue growth rate in Q1 to decelerate by low-to-mid single digit percentage points as compared to our Q4 growth rate. “Factors driving this deceleration include the maturity of our business, as well as the increasing impact from global privacy regulation and other ad targeting related headwinds.”

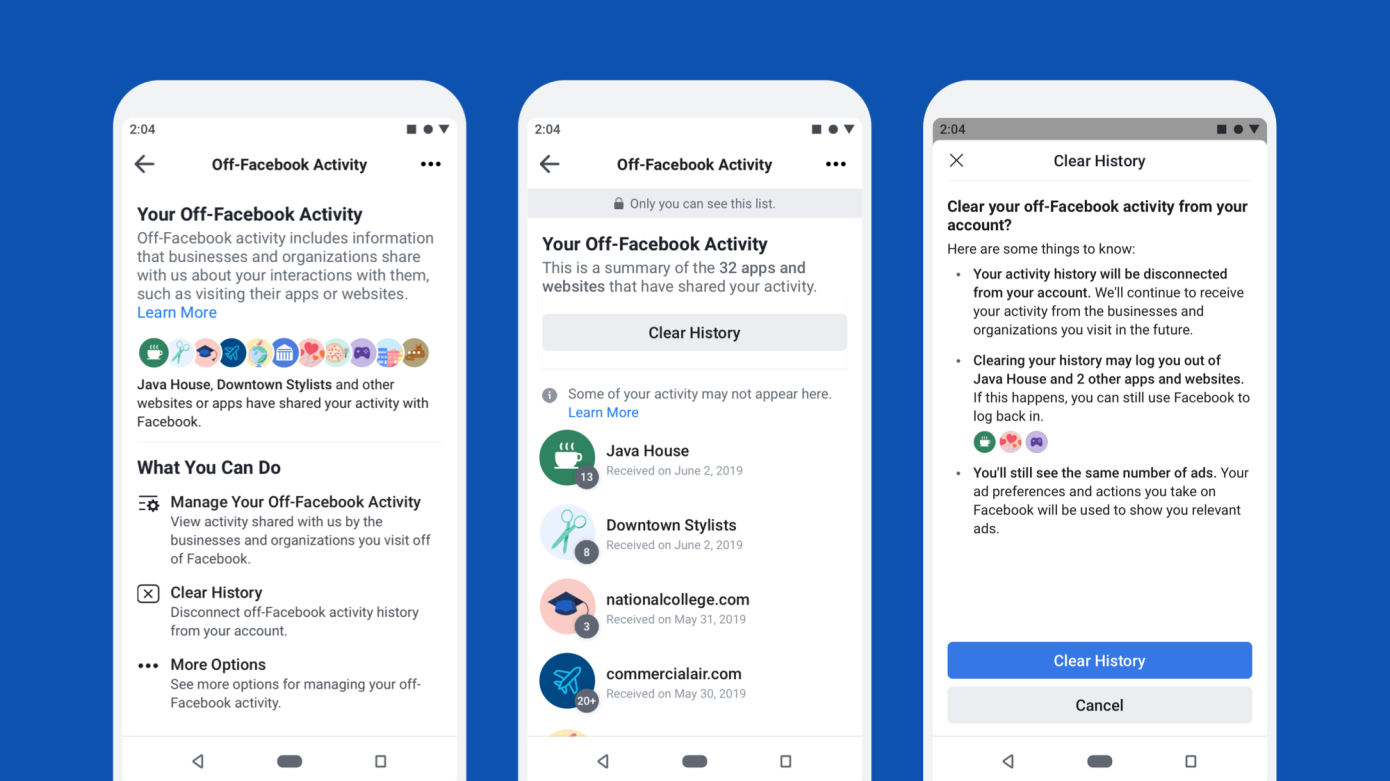

Wehner says to expect that the worst of these privacy headwinds are still to come due to regulatory initiatives like GDPR and CCPA, mobile operating systems and browser providers like Apple and Google limiting access to ad targeting singals, and Facebook’s own product changes like the new way to disconnect off-Facebook data from your acccount.

On Facebook’s perception issues, Zuckerberg said “We’re also focused on communicating more clearly what we stand for. One critique of our approach for much of the last decade was that, because we wanted to be liked, we didn’t always communicate our views as clearly because we were worried about offending people. So this led to some positive but shallow sentiments towards us and towards the company. And my goal for this next decade isn’t to be liked, but to be understood, because in order to be trusted, people need to know what you stand for.”

The business aside, Facebook had another tough quarter under the scrutiny of journalists and regulators. Democratic presidential candidates have railed against Zuckerberg’s decision to continuing allowing misinformation in political ads. The company dropped out of the top 10 places to work, and pledged $130 million to fund an Oversight Board for its content policies.

The CEO was grilled on Capitol Hill about Facebook’s cryptocurrency Libra that seems stuck in its tracks as major partners like Visa and Stripe dropped out. Facebook took heat for how its treats content moderators and how it tried to cut off competitors from its developer platform. The FTC continued its anti-trust investigation and weighed an injunction that would halt Facebook intermingling its messaging app infrastructure.

But those headwinds didn’t stop Facebook’s march forward. Its four main apps took the top four spots amongst the most downloaded apps of the 2010s. It moved deeper into hardware sales with its new Portal TV attachable camera. It acquired gaming companies like Playgiga and the studio behind VR hit Beat Saber, while signing exclusive game streaming deals with influencers like Disguised Toast. It launched Facebook News, Facebook Pay, its dating feature in the US, and it tested a meme-making app called Whale.

Facebook’s share price remains near an all-time high despite today’s tumble. While the world may be increasingly uncomfortable with Facebook’s access to private data, there’s no debate about how incredibly valuable that data is.

Powered by WPeMatico

International Business Machines is living a case study of a large, established company vying to transform. Over the last decade, the technology elder has struggled to move into areas like cloud and AI. IBM has leaned on a combination of its own R&D abilities and deep pockets to push into modern markets, but has struggled to turn them into revenue growth.

At one point, Big Blue posted 22 sequential quarters of falling revenue, a mind-boggling testament to how hard it can be to turn around a juggernaut. More recently, IBM shrank for another five consecutive quarters, a streak it broke with yesterday’s news that it had beat analyst expectations.

The quarter brought modest, but welcome revenue growth. Perhaps more importantly, the company’s top line expansion was co-led by the old IBM mainframe business and its newest champion, Red Hat.

IBM can be happy for the positive financial news, for now at least, but it needs to repeat the result. The challenge it faces moving forward will include finding a way to continue revenue growth while modernizing its product line and ensuring that its huge Red Hat purchase continues to perform.

Powered by WPeMatico

Indian tech startups secured nearly $14 billion in 2019, more than they have raised in any other year. This is a major rebound since 2016, when startups in the nation had bagged just $4.3 billion.

But even as more VC funds — many with bigger checks — arrive in India, the financial performance of startups remains a cause for concern.

Whether it’s mobile payments or education learning apps, each startup today faces dozens of competitors in their category. Many of these sectors, such as social commerce and digital bookkeeping, are just beginning to see traction in India, which has resulted in investors backing a large number of similar players.

This has meant more marketing spends; to create awareness among consumers (or merchants) and stand out in a crowd, many firms are heavily marketing their services and offering lofty cashbacks to win users.

What is especially troublesome for startups is that there is no clear path for how they would ever generate big profits. Silicon Valley companies, for instance, have entered and expanded into India in recent years, investing billions of dollars in local operations, but yet, India has yet to make any substantial contribution to their bottom lines.

If that wasn’t challenging enough, many Indian startups compete directly with Silicon Valley giants, which while impressive, is an expensive endeavor.

How expensive? Here’s an exhaustive look at the financial performance of several notable startups and major firms in India as disclosed by them to local regulators in recent weeks. These are Financial Year 2019 figures, which ended on March 31, 2019. Some of the filings were provided to TechCrunch by business intelligence platform Tofler.

Flipkart, which sold a majority stake to Walmart for $16 billion last year, posted a consolidated revenue of $6.11 billion for the financial year that ended in March. Its revenue is up 42% since last year, and its loss, at $2.4 billion, represents a 64% improvement during the same period. The ecommerce giant this year has expanded into many new categories, including food retail.

BigBasket delivers groceries and perishables across India and became a unicorn this year after it raised a $150M Series F led by Mirae Asset-Naver Asia Growth Fund, the U.K.’s CDC Group and Alibaba. The startup posted revenue of $386 million, up from $221 million last year. Its loss, however, more than doubled to $80 million from $38 million during the same period.

BigBasket rival Grofers, which raised $200 million in a financing round led by SoftBank Vision Fund, reported $62.6 million on revenue of $169 million. The company’s chief executive and co-founder, Albinder Dhindsa, has said that the startup is on track to sell goods worth $699 million by the end of FY 2020.

Milkbasket, a micro-delivery startup that allows users to order daily supplies, reported revenue of $11.8 million, up from $4 million last year. During this period, its loss widened to $1.3 million, from $130,000 last year.

Lenskart is an omni-channel retailer for eyewear products. Earlier this month, it raised $275 million this month from SoftBank Vision Fund. It posted a revenue of $68 million — and its loss shrank from $16.5 million to $3.8 million in one year.

Rivigo, a five-year-old startup that is attempting to build a more reliable and safer logistics network, raised $65 million in July this year. Its revenue increased 42% to $143.8 million while its loss also increased to $83 million.

SoftBank-backed logistics firm Delhivery, which raised $413 million earlier this year from SoftBank and others, said its revenue has grown 58% to $237 million since FY18, while its loss has almost tripled to $249 million.

Powered by WPeMatico

Yesterday, Adobe submitted its quarterly earnings report — and the results were quite good. The company generated a tad under $3 billion for the quarter, at $2.99 billion, and reported that revenue exceeded $11 billion for FY 2019, its highest-ever mark.

“Fiscal 2019 was a phenomenal year for Adobe as we exceeded $11 billion in revenue, a significant milestone for the company. Our record revenue and EPS performance in 2019 makes us one of the largest, most diversified, and profitable software companies in the world. Total Adobe revenue was $11.17 billion in FY 2019, which represents 24% annual growth,” Adobe CEO Shantanu Narayen told analysts and reporters in his company’s post-earnings call.

Adobe made a couple of key M&A moves this year that appear to be paying off, including nabbing Magento in May for $1.7 billion and Marketo in September for $4.75 billion. Both companies fit inside its “Digital Experience” revenue bucket. In its most recent quarter, Adobe’s Digital Experience segment generated $859 million in revenue, compared with $821 million in the sequentially previous quarter.

Obviously buying two significant companies this year helped push those numbers, something CFO John Murphy acknowledged in the call:

Key Q4 highlights include strong year-over-year growth in our Content and Commerce solutions led by Adobe Experience Manager and success with cross-selling and up-selling Magento; Adoption of Adobe Experience Platform, Audience Manager and Real-Time CDP in our Data & Insights solutions; and momentum in our Marketo business, including in the mid-market segment, which helped fuel growth in our Customer Journey Management solutions.

All of that added up to growth across the Digital Experience category.

But Adobe didn’t simply buy its way to new market share. The company also continued to build a suite of products in-house to help grow new revenue from the enterprise side of its business.

“We’re rapidly evolving our CXM product strategy to deliver generational technology platforms, launch innovative new services and introduce enhancements to our market-leading applications. Adobe Experience Platform is the industry’s first purpose-built CXM platform. With real-time customer profiles, continuous intelligence and an open and extensible architecture, Adobe Experience Platform makes delivering personalized customer experiences at scale a reality,” Narayan said.

Of course, the enterprise is just part of it. Adobe’s creative tools remain its bread and butter, with the creative tools accounting for $1.74 billion in revenue and Document Cloud adding another $339 million this quarter.

The company is talking confidently about 2020, as its recent acquisitions mature and become a bigger part of the company’s digital experience offerings. But Narayan feels good about the performance this year in digital experience: “When I take a step back and look at what’s happened during the year, I feel really good about the amount of innovation that’s happening. And the second thing I feel really good about is the alignment across Magento, Marketo and just call it the core DX business in terms of having a more unified and aligned go-to-market, which has not only helped our results, but it’s also helped the operating expense associated with that business,” he said.

It is no small feat for any software company to surpass $11 billion in trailing revenue. Consider that Adobe, which was founded in 1982, goes back to the earliest days of desktop PC software in the 1980s. Yet it has managed to transform into a massive cloud services company over the last five years under Narayan’s leadership.

Powered by WPeMatico

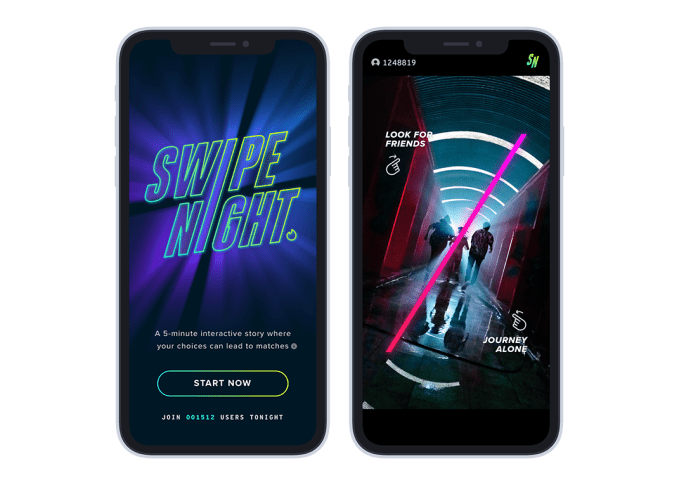

Tinder’s big experiment with interactive content — the recently launched in-app series called “Swipe Night” — was a success. According to Tinder parent company Match during its Q3 earnings this week, “millions” of Tinder users tuned in to watch the show’s episodes during its run in October, and this drove double-digit increases in both matches and messages. As a result, Match confirmed its plans to launch Tinder’s new show outside the U.S. in early 2020.

Swipe Night’s launch was something of a departure for the dating app, whose primary focus has been on connecting users for dating and other more casual affairs.

The new series presented users with something else to do in the Tinder app beyond just swiping on potential matches. Instead, you swiped on a story.

Presented in a “choose-your-own-adventure”- style format that’s been popularized by Netflix, YouTube and others, Swipe Night asked users to make decisions to advance a narrative that followed a group of friends in an “apocalyptic adventure.”

The moral and practical choices you made during Swipe Night would then be shown on your profile as a conversation starter, or as just another signal as to whether or not a match was right for you. After all, they say that the best relationships come from those who share common values, not necessarily common interests. And Swipe Night helped to uncover aspects to someone’s personality that a profile would not — like whether you’d cover for a friend who cheated, or tell your other friend who was the one being cheated on?

The moral and practical choices you made during Swipe Night would then be shown on your profile as a conversation starter, or as just another signal as to whether or not a match was right for you. After all, they say that the best relationships come from those who share common values, not necessarily common interests. And Swipe Night helped to uncover aspects to someone’s personality that a profile would not — like whether you’d cover for a friend who cheated, or tell your other friend who was the one being cheated on?

The five-minute episodes ran every Sunday night in October from 6 PM to midnight.

Though early reports on Tinder’s plans had somewhat dramatically described Swipe Night as Tinder’s launch into streaming video, it’s more accurate to call Swipe Night an engagement booster for an app from which many people often find themselves needing a break. Specifically, it could help Tinder address issues around declines in open rates or sessions per user — metrics that often hide behind what otherwise looks like steady growth. (Tinder, for example, added another 437,000 subscribers in the quarter, leading to 5.7 million average subscribers in Q3).

Ahead of earnings, there were already signs that Swipe Night was succeeding in its efforts to boost engagement.

Tinder said in late October that matches on its app jumped 26% compared to a typical Sunday night, and messages increased 12%.

On Tinder’s earnings call with investors, Match presented some updated metrics. The company said Swipe Night led to a 20% to 25% increase in “likes” and a 30% increase in matches. And the elevated conversation levels that resulted from user participation continued for days after each episode aired. Also importantly, the series helped boost female engagement in the app.

“This really extended our appeal and resonated with Gen Z users,” said Match CEO Mandy Ginsberg. “This effort demonstrates the kind of creativity and team we have at Tinder and the kind of effort that we’re willing to make.”

The company says it will make Season 1 of Swipe Night (a hint there’s more to come) available soon as an on-demand experience, and will roll out the product to international markets early next year.

Swipe Night isn’t the only video product Match Group has in the works. In other Match-owned dating apps, Plenty of Fish and Twoo, the company is starting to test live streaming broadcasts. But these are created by the app’s users, not as a polished, professional product from the company itself.

Match had reported better-than-expected earnings for the third quarter, with earnings of 51 cents per share — above analysts’ expectations for earnings of 42 cents per share. Match’s revenue was $541 million, in line with Wall Street’s expectations.

But its fourth-quarter guidance came in lower than expectations ($545 million-$555 million, below the projected $559.3 million), sending the stock dropping. Match said it would have to take on about $10 million in expenses related to it being spun out from parent company IAC.

Powered by WPeMatico

Better than expected revenues couldn’t divert investor attention from the fact that Uber still managed to lose more than $1 billion in the most recent quarter as the company’s stock fell in after-hours trading.

There are bright spots in the latest earnings report, not least that the company managed to stanch the bleeding that had cost the company over $5 billion in the previous quarter.

Revenue grew to $3.8 billion, up from $2.9 billion in the year-ago period, representing a 30% boost. But even as Uber’s core business shows signs of stabilizing and its core markets continue to show growth, its other business units appear to be hemorrhaging cash at increasingly high rates.

“Our results this quarter decisively demonstrate the growing profitability of our Rides segment,” said Dara Khosrowshahi, the company’s chief executive, in a statement. “Rides Adjusted EBITDA is up 52% year-over-year and now more than covers our corporate overhead. Revenue growth and take rates in our Eats business also accelerated nicely. We’re pleased to see the impact that continued category leadership, greater financial discipline, and an industry-wide shift towards healthier growth are already having on our financial performance.”

Losses in earnings at the company’s Uber Eats business grew 67% to $316 million from $189 million in the year-ago period. And performance in the company’s freight division looks even worse. Losses in freight ballooned by 161%, growing to $81 million from $31 million in the same quarter of 2018.

Also contributing to the company’s losses for the quarter were stock-based compensation expenses, which added another $401 million to the tallies against the company.

Given that the lock-up period is about to end for institutional investors, that could spell even more trouble for the company — as institutional investors who bought into the company before its public offering may look to sell.

That said, Uber has taken a number of steps to correct its course and put the company on a path to profitability, which Khosrowshahi says should happen in the next two years.

In October, the company announced the last of three rounds of sweeping layoffs at the company that saw 1,185 staffers lose their jobs. Khosrowshahi called the layoffs a chance to ensure that the company was “structured for success for the next few years.” In an email to staff, he wrote, “This has resulted in difficult but necessary changes to ensure we have the right people in the right roles in the right locations, and that we’re always holding ourselves accountable to top performance.”

With the layoffs behind it, Uber can now focus on some of the big operational challenges it had set for itself through the reorganization that the company has announced. That includes adding new features and technologies to its Uber Eats delivery program (despite what recent losses at GrubHub may imply about the food delivery business) and pressing forward with another darling of the tech set these days — the company’s financial services platform.

The launch of this new platform, coupled with a slew of announcements from the company in September, show that Uber may have dialed back on its ambitions, but not by much. As Khosrowshahi said at the event, “We want to be the operating system for your everyday life…. A one-click gateway to everything that Uber can offer you.”

Powered by WPeMatico

Despite ongoing public relations crises, Facebook kept growing in Q3 2019, demonstrating that media backlash does not necessarily equate to poor business performance.

Facebook reached 2.45 billion monthly users, up 1.65%, from 2.41 billion in Q2 2019 when it grew 1.6%, and it now has 1.62 billion daily active users, up 2% from 1.587 billion last quarter when it grew 1.6%. Facebook scored $17.652 billion of revenue, up 29% year-over-year, with $2.12 in earnings per share.

Facebook’s earnings beat expectations compared to Refinitiv’s consensus estimates of $17.37 billion in revenue and $1.91 earnings per share. Facebook’s quarter was mixed compared to Bloomberg’s consensus estimate of $2.28 EPS. Facebook earned $6 billion in profit after only racking up $2.6 billion last quarter due to its SEC settlement.

Facebook shares rose 5.18% in after-hours trading, to $198.01 after earnings were announced, following a day where it closed down 0.56% at $188.25.

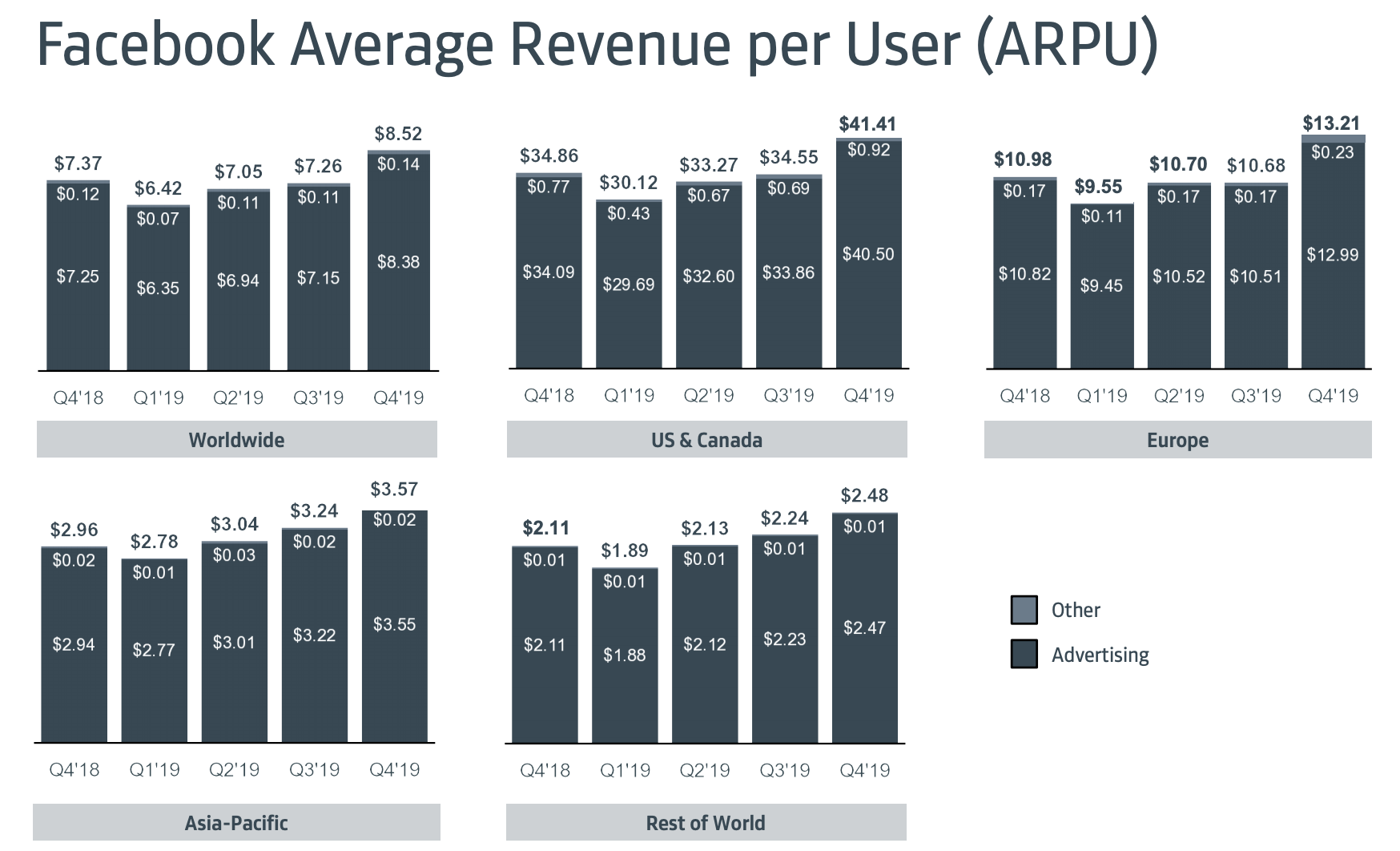

Notably, Facebook gained 2 million users in each of its core U.S. & Canada and Europe markets that drive its business, after quarters of shrinkage, no growth or weak growth there in the past two years. Average revenue per user grew healthily across all markets, boding well for Facebook’s ability to monetize the developing world where the bulk of user growth currently comes from.

Facebook says 2.2 billion users access Facebook, Instagram, WhatsApp or Messenger every day, and 2.8 billion use one of this family of apps each month. That’s up from 2.1 billion and 2.7 billion last quarter. Facebook has managed to stay sticky even as it faces increased competition from a revived Snapchat, and more recently TikTok. However, those rivals might more heavily weigh on Instagram, for which Facebook doesn’t routinely disclose user stats.

Facebook’s earnings announcement was somewhat overshadowed by Twitter CEO Jack Dorsey announcing it would ban all political ads — something TechCrunch previously recommended social networks do. That move flies in the face of Facebook CEO Mark Zuckerberg’s staunch support for allowing politicians to spread misinformation without fact-checks via Facebook ads. This should put additional pressure on Facebook to rethink its policy.

Zuckerberg doubled-down on the policy, saying “I believe that the better approach is to work to increase transparency. Ads on Facebook are already more transparent than anywhere else,” he said. Attempting to dispel that the policy is driven by greed, he noted Facebook expects political ads to make up “less than 0.5% of our revenue next year.” Because people will disagree and the issue will keep coming up, Zuckerberg admitted it’s going to be “a very tough year.”

Facebook also announced that lead independent board member Susan D. Desmond-Hellmann has resigned to focus on health issues.

Facebook expects revenue deceleration to be pronounced in Q4. But CFO David Wehner provided some hope, saying “we would expect our revenue growth deceleration in 2020 versus the Q4 rate to be much less pronounced.” That led Facebook’s share price to spike from around $191 to around $198.

However, Facebook will maintain its aggressive hiring to moderate content. While the company has touted how artificial intelligence would increasingly help, Zuckerberg said that hiring would continue because “There’s just so much content. We do need a lot of people.”

Regarding Libra’s regulatory pushback, Zuckerberg explained that Facebook was already diversified in commerce if that doesn’t work out, citing WhatsApp Payments, Facebook Marketplace and Instagram shopping.

On anti-trust concerns, Zuckerberg reminded analysts that Instagram’s success wasn’t assured when Facebook acquired it, and it has survived a lot of competition thanks to Facebook’s contributions. In a new talking point we’re likely to hear more of, Zuckerberg noted that other competitors had used their success in one vertical to push others, saying “Apple and Google built cameras and private photo sharing and photo management directly into their operating systems.”

Overall, it was another rough quarter for Facebook’s public perception as it dealt with outages and struggled to get buy-in from regulators for its Libra cryptocurrency project. Former co-founder Chris Hughes (who I’ll be leading a talk with at SXSW) campaigned for the social network to be broken up — a position echoed by Elizabeth Warren and other presidential candidates.

The company did spin up some new revenue sources, including taking a 30% cut of fan patronage subscriptions to content creators. It’s also trying to sell video subscriptions for publishers, and it upped the price of its Workplace collaboration suite. But gains were likely offset as the company continued to rapidly hire to address abusive content on its platform, which saw headcount grow 28% year-over-year, to 43,000. There are still problems with how it treats content moderators, and Facebook has had to repeatedly remove coordinated misinformation campaigns from abroad. Appearing concerned about its waning brand, Facebook moved to add “from Facebook” to the names of Instagram and WhatsApp.

It escaped with just a $5 billion fine as part of its FTC settlement that some consider a slap on the wrist, especially since it won’t have to significantly alter its business model. But the company will have to continue to invest and divert product resources to meet its new privacy, security and transparency requirements. These could slow its response to a growing threat: Chinese tech giant ByteDance’s TikTok.

Powered by WPeMatico

Tesla CEO Elon Musk forecast that the company’s energy business will eventually be the same size as — or even bigger than — its automotive sector, the latest sign that the company plans to put more time and resources to scaling up its solar and storage products.

“It could be bigger, but it will certainly be of a similar magnitude,” Musk said during an earnings call Wednesday. The company surprised Wall Street by reporting a return to profitability in the third quarter.

The bulk of Tesla’s revenue is generated from sales of its Model S, Model X and Model 3 electric vehicles. In the third quarter, automotive revenues were $5.35 billion. The company doesn’t break out revenue generated from solar, energy storage or other products and services. However, the total revenue in the third quarter was $6.3 billion, which gives some indication of the size of automotive compared to its other businesses.

Tesla’s energy and solar businesses languished for nearly two years as attention and resources were directed to the Model 3. That diversion of resources included redirecting to the car battery cell production lines meant for its home Powerwall and commercial Powerpack energy storage products because the company didn’t have enough cells.

“We had to do it because if we didn’t solve the Model 3, Tesla wouldn’t survived,” he said. “So, unfortunately that shorted other parts of the company.”

Now, the company is committed to scaling up energy storage and solar. Kunal Girotra, who initially joined Tesla in 2015 as a senior product manager for Powerwall, was promoted to senior director of the company’s energy operations.

In the third quarter, Tesla deployed 43 megawatts of solar, a 48% increase from the previous quarter. Solar installations are still 54% lower than the same period last year.

Energy storage deployments have continued to grow, reaching an all-time high of 477 MWh in the third quarter, according to earnings posted Wednesday.

Part of this new effort includes its solar roof tile product, which was originally unveiled in 2016. Musk said that a new, third iteration of its solar roof tile will debut Thursday afternoon.

Powered by WPeMatico

The Snap-back continues. Snapchat blew past earnings expectations for a big beat in Q3, as it added 7 million daily active users this quarter to hit 210 million, up 13% year-over-year. Snap also beat on revenue, notching $446 million, which is up a whopping 50% year-over-year, at a loss of $0.04 EPS. That flew past Bloomberg’s consensus of Wall Street estimates that expected $437.9 million in revenue and a $0.05 EPS loss.

Snap has managed to continue cutting losses as it edges toward profitability. Net loss improved to $227 million from $255 million last quarter, with the loss decreasing $98 million versus Q3 2018.

CEO Evan Spiegel made his case in his prepared remarks for why Snapchat’s share price should be higher: “We are a high-growth business, with strong operating leverage, a clear path to profitability, a distinct vision for the future and the ability to invest over the long term.”

Snapchat’s share price had closed down 4% at $14, and had fallen roughly 4.6% in after-hours trading as of 1:50 pm Pacific, to $13.35, despite the earnings beat. It remains below its $17 IPO price but has performed exceedingly well this year, rising from a low of $4.99 in December.

That’s partially because of the high cost of Snapchat’s growth relative average revenue per user. While it notes that it saw user growth in all regions, 5 million of the 7 million new users came from the Rest of World, with just 1 million coming from the North America and Europe regions. That’s in part thanks to better than expected growth and retention on its re-engineered Android app that’s been a hit in India. But since Snapchat serves so much high-definition video content but it earns just $1.01 average revenue in the Rest of World, it has to hope it can keep growing ARPU so it becomes profitable globally.

Some other top-line stats from Snapchat’s earnings:

Interestingly, Spiegel noted that “We benefited from year-over-year growth in user activity in Q3 including growth in Snapchatters posting and viewing Stories.” Snapchat hadn’t indicated Stories was growing in at least the past two years, as it was attacked by clones, including Instagram Stories that led Snapchat to start shrinking in user count a year ago before it recovered.

Since Stories viewership is critical to total ad view on Snapchat, we may see analysts insisting to hear more about that metric in the future. Snap also said users opened the app 30 times per day, up from 25 times per day as of July 2018, showing it’s still highly sticky and being used for rapid-fire visual communication.

The other major piece of Snapchat’s ad properties is Discover, where total time spent watching grew 40% year-over-year. And rather than being driving by just a few hits, more than 100 Discover channels saw over 10 million viewers per month in Q3. With Instagram’s IGTV a flop, Discover remains Snapchat’s best differentiated revenue driver, and one it needs to keep investing in and promoting. With Instagram trying to compete more heavily on chat with its new close friends-only Threads app, Snapchat can’t rely on ephemeral messaging to keep it special.

TikTok buys ads on Snapchat that could steal its users

Surprisingly, Spiegel said that “We definitely see TikTok as a friend” when asked about why it allowed the competitor to continue buying ads on Snapchat. The two apps are different, with Snapchat focused on messaging and biographical social media while TikTok is about storyboarded, premeditated social entertainment. But this could be a dangerous friendship for Snapchat, as TikTok may be taking time away that users might spend watching Snapchat Discover, and its growth could box Snapchat out of the social entertainment space.

Looking forward, in Q4 Snap is estimating 214 to 215 million daily active users and $540 million to $560 million in revenue. It’s expecting between break even and positive $20 million for adjusted EBITDA. That revenue guidance was below estimates for the holiday Q4, contributing to the share price fall.

Snap has a ways to go before reaching profitability. That milestone would let it more freely invest in long-term projects, specifically its Spectacles camera-glasses. Spiegel has said he doesn’t expect augmented reality glasses to be a mainstream consumer product for 10 years. That means Snap will have to survive and spend for a long time if it wants a chance to battle Apple, Facebook, Magic Leap and more for that market.

Powered by WPeMatico