Earnings

Auto Added by WPeMatico

Auto Added by WPeMatico

The cloud market is coming into its own during the pandemic as the novel coronavirus forced many companies to accelerate plans to move to the cloud, even while the market was beginning to mature on its own.

This week, the big three cloud infrastructure vendors — Amazon, Microsoft and Google — all reported their earnings, and while the numbers showed that growth was beginning to slow down, revenue continued to increase at an impressive rate, surpassing $30 billion for a quarter for the first time, according to Synergy Research Group numbers.

Powered by WPeMatico

Wall Street darling Tesla is holding on to its recent gains today on the back of a bullish analyst report, despite some weakness in tech shares.

Tesla has seen its value skyrocket in recent quarters, rising from a 52-week low share price of $211 to $1,548.81 today. That figure, however, is low in the eyes of some. Enter Piper Sandler.

The Piper analyst report, which was first released late Monday, gives Tesla a new price target of $2,322, up from the group’s prior price target of a little over $900 per share. The stock still has room to run, some believe, perhaps explaining some of the mania that related companies have seen in recent weeks, including fellow electric car manufacturers Nikola, Nio and others.

It was enough to prompt a “wow” from Tesla CEO Elon Musk via a tweet Monday evening.

Wow

— Elon Musk (@elonmusk) July 14, 2020

The Piper report cites two key factors for its new Tesla price target: The company’s edge in manufacturing and resulting unit volume, and the possibility that software will allow the company to eventually generate operating margins in the mid-20s.

On the manufacturing front, Piper increased its 2020 delivery estimates based on Tesla’s recent second-quarter numbers. The firm believes Tesla can hit its original 2020 delivery guidance of 500,000 units, which it notes is impressive, given factory closures due to COVID-19.

Piper suggested Tesla can scale rapidly in the coming years. The constraint isn’t customer demand, but instead capacity, the analyst suggested. Of course, building out production capacity is no small and cheap feat. Still, with customer demand wide open, Piper sees big revenue gains moving forward.

The latter argument feels more speculative. A 25% operating margin implies that the automotive company’s gross margins would need to be far higher, a seeming stretch for a company that sells molded metal and plastic in a competitive market.

The basis of Piper’s argument centers on Tesla’s software, specifically its FSD, or “full self-driving” feature, an $8,000 add-on that provides advanced driver assistance over its standard Autopilot system.

Let us provide some quick backstory so that everyone understands: Today, Tesla vehicles come standard with Autopilot, an advanced driver assistance system that offers a combination of adaptive cruise control and lane steering. Tesla once charged for this feature as well, but made it standard in April 2019.

The more robust and higher-functioning version of Autopilot is called full self-driving. FSD includes the parking feature Summon as well as Navigate on Autopilot, an active guidance system that navigates a car from a highway on-ramp to off-ramp, including interchanges and making lane changes. The system now recognizes and responds to traffic lights, as well.

Still, Tesla vehicles are not self-driving cars. The system requires a human driver to remain engaged at all times.

Piper believes the FSD price will continue to rise, driving up margins. The firm predicted the cost of FSD could rise as high as $40,000.

“Thanks to the high-margin nature of the FSD package, we think that by the 2030s, Tesla could conceivably be selling vehicles at cost — or even below cost — while still achieving higher operating margins,” Piper wrote.

There is a very material catch to all of this. Tesla is able to recognize FSD revenue on its balance sheet as it rolls out more features. In other words, Tesla has to keep improving the product to be able to capture that entire line item.

In the first-quarter earnings call, Tesla CFO Zachary Kirkhorn explained that the company takes “roughly half” of the FSD as revenue. The other half of it goes into deferred revenue.

“Our deferred revenue balance is continuing to grow,” he said at the time. “It’s a little bit over $600 million. And so as we release features with time, at the end of every quarter, we take a look at what features have been released, associated value and then we can release that from the deferred revenue into our financials for that quarter. And then cars going forward, once the feature is released, we can recognize that revenue.”

For Tesla shareholders, institutional and retail alike, Piper’s report is welcome. Now Tesla has to live up to raised expectations. The company reports earnings on July 22. TechCrunch will be tuned in.

Powered by WPeMatico

After a heated run, SaaS and cloud stocks dipped sharply during regular trading on Monday.

According to the category-tracking Bessemer cloud index, public SaaS and cloud stocks dropped around 6.5% today, a material blow to the value of some of the world’s most highly valued companies, measured by sector-averaged revenue multiples.

After recovering all their COVID-19-related losses earlier this year, SaaS and cloud stocks kept on rising, reaching new all-time highs with regularity. But earnings season is starting, meaning that the value of modern software and digital infrastructure companies will soon be tested against Q2 results — results that were recorded fully during the global pandemic.

To hear bulls — both private and public — tell the story, COVID-19 and its ensuing workplace disruptions have provided software companies with a huge boon. Namely, that customers current and future have radically changed their procurement models and will need more software solutions, more quickly, than they previously anticipated. (Stay tuned to The Exchange for more on this later in the week.)

The thought that there are more and better customers coming for SaaS and cloud companies made them relative safe havens in otherwise turbulent public markets; while other industries had uncertain demand curves, the thinking went, software companies were being pushed forward by an accelerating secular shift.

Today, however, the broader markets slipped from early-day positions of strength while SaaS and cloud shares dropped sharply. Prior patterns in investor behavior didn’t hold up, in other words.

Why today brought such sharp selling is not clear. No more, really, than reasons for prior days’ gains were clear at the time. Profit taking? Rotation to other sectors? Whatever you want to ascribe to the day’s declines you can make stick.

For our purposes here at TechCrunch, the dropping share prices of public software companies serves as an anti-signal for late-stage valuations in SaaS startups, and a general headwind toward venture investors making more early-stage bets in the sector. Of course, one day doesn’t change the game. But several days of sharp losses could begin to change sentiment, and days when shares of modern software companies drop by 6% are few and far between.

Earnings are next, but for many companies in the SaaS and cloud world, reporting their results just got easier. When expectations drop, everyone loses a bit of worry, right?

Powered by WPeMatico

After going private in 2016 after accepting a $32 per share, or $4.3 billion, price from Apollo Global Management, Rackspace is looking once again to the public markets. First going public in 2008, Rackspace is taking second aim at a public offering around 12 years after its initial debut.

The company describes its business as a “multicloud technology services” vendor, helping its customers “design, build and operate” cloud environments. That Rackspace is highlighting a services focus is useful context to understand its financial profile, as we’ll see in a moment.

But first, some basics. The company’s S-1 filing denotes a $100 million placeholder figure for how much the company may raise in its public offering. That figure will change, but does tell us that firm is likely to target a share sale that will net it closer to $100 million than $500 million, another popular placeholder figure.

Rackspace will list on the Nasdaq with the ticker symbol “RXT.” Goldman, Citi, J.P. Morgan, RBC Capital Markets and other banks are helping underwrite its (second) debut.

Similar to other companies that went private, only later to debut once again as a public company, Rackspace has oceans of debt.

The company’s balance sheet reported cash and equivalents of $125.2 million as of March 31, 2020. On the other side of the ledger, Rackspace has debts of $3.99 billion, made up of a $2.82 billion term loan facility, and $1.12 billion in senior notes that cost the firm an 8.625% coupon, among other debts. The term loan costs a lower 4% rate, and stems from the initial transaction to take Rackspace private ($2 billion), and another $800 million that was later taken on “in connection with the Datapipe Acquisition.”

The senior notes, originally worth a total of $1,200 million or $1.20 billion, also came from the acquisition of the company during its 2016 transaction; private equity’s ability to buy companies with borrowed money, later taking them public again and using those proceeds to limit the resulting debt profile while maintaining financial control is lucrative, if a bit cheeky.

Rackspace intends to use IPO proceeds to lower its debt-load, including both its term loan and senior notes. Precisely how much Rackspace can put against its debts will depend on its IPO pricing.

Those debts take a company that is comfortably profitable on an operating basis and make it deeply unprofitable on a net basis. Observe:

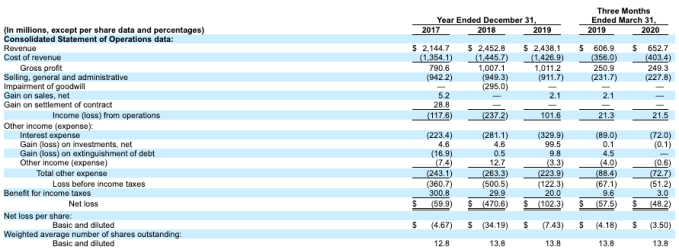

Image Credits: SEC

Looking at the far-right column, we can see a company with material revenues, though slim gross margins for a putatively tech company. It generated $21.5 million in Q1 2020 operating profit from its $652.7 million in revenue from the quarter. However, interest expenses of $72 million in the quarter helped lead Rackspace to a deep $48.2 million net loss.

Not all is lost, however, as Rackspace does have positive operating cash flow in the same three-month period. Still, the company’s multi-billion-dollar debt load is still steep, and burdensome.

Returning to our discussion of Rackspace’s business, recall that it said that it sells “multicloud technology services,” which tells us that its gross margins will be service-focused, which is to say that they won’t be software-level. And they are not. In Q1 2020 Rackspace had gross margins of 38.2%, down from 41.3% in the year-ago Q1. That trend is worrisome.

The company’s growth profile is also slightly uneven. From 2017 to 2018, Rackspace saw its revenue expand from $2.14 billion to $2.45 billion, growth of 14.4%. The company shrank slightly in 2019, falling from $2.45 billion in revenue in 2018 to $2.44 billion the next year. Given the economy that year, and the importance of cloud in 2019, the results are a little surprising.

Rackspace did grow in Q1 2020, however. The firm’s $652.7 million in first-quarter top-line easily bested in its Q1 2019 result of $606.9 million. The company grew 7.6% in Q1 2020. That’s not much, especially during a period in which its gross margins eroded, but the return-to-growth is likely welcome all the same.

TechCrunch did not see Q2 2020 results in its S-1 today while reading the document, so we presume that the firm will re-file shortly to include more recent financial results; it would be hard for the company to debut at an attractive price in the COVID-19 era without sharing Q2 figures, we reckon.

How to value Rackspace is a puzzle. The company is tech-ish, which means it will find some interest. But its slow growth rate, heavy debts and lackluster margins make it hard to pin a fair multiple onto. More when we have it.

Powered by WPeMatico

Despite record-setting COVID-19 infections, American equities rose today. All major indices gained ground during regular trading, while tech stocks did even better.

The Nasdaq Composite set new 52-week and all-time highs, touching 10,462.0 points before closing at 10,433.65, up 2.21% on the day. Similarly, a basket of SaaS and cloud companies that has risen and fallen more sharply than even the tech-heavy Nasdaq closed this afternoon at 1,908.30 after touching 1,952.39 points. Both results were 52-week and all-time highs.

Such is the mood on Wall Street regarding the health of technology companies. It’s not hard to find bullish sentiment, jockeying to push tech shares higher. Some examples of today’s enthusiasm paint the picture:

You can’t swing your arms without running into a reason why it makes sense for SaaS stocks to be trading at record valuation multiples, or why one company or another is actually reasonably valued over a long-enough time horizon.

It’s worth noting that this putatively rational public investor thinking doesn’t fit at all with what the tech set used to pound into my head about the public markets, namely that they are infamously impatient and thus utter bilge for most long-term value creation. Going public was garbage, I was told; you have to report every three months and no one looks out a few years.

Now, I’m being told by roughly the same people that the market is doing the very thing that they said it didn’t do, namely price firms for future results instead of trailing outcomes. Fine by me either way, frankly, but I’d like to know which story is true.

Happily, we’re about to see if all this high-fiving and enthusiasm is real.

Earnings season beckons, and it should bring with it a dose or two of clarity. If the digital transformation has managed to accelerate sufficiently that most tech companies have managed to greatly boost their near-term value, hats off to the cohort and bully for the startups that must also be enjoying similar revenue upswells.

But that doesn’t have to happen. There are possible earnings result sets that can cause investors to dump tech shares, as Slack learned a month ago.

The background to all of this is that there are good reasons to have some doubts about the current health of the national economy. And, sure, most people are willing to allow that the stock market and the aggregate domestic economy are not perfectly linked — this is no less than partially true — but each day the stock market steps higher and COVID-19 surges again leading to re-closings around the nation makes you to wonder if this is all for real.

Earnings season is here soon. Let’s find out.

Powered by WPeMatico

In another up for technology shares, software companies saw their values reach new heights today.

The day’s trading comes after a sell-off last week eased some of technology companies’ rebounds from their COVID-19 lows; stocks in tech companies have more than made up for their early-year declines in mid-2020, with the Nasdaq reaching 10,000 points before giving up some ground.

Today the Nasdaq Composite index rose 0.15% to 9,910.53 points, just a few bips short of its all-time highs. A thematic tech index focused on fintech also saw their values recover to a mote under previous highs. The S&P 500 fell 0.36% to close at $3,113.41 and the Dow Jones Industrial Average Index decreased 0.65% to $26,119.13.

But software companies, tech’s highest fliers, set new records as measured by the Bessemer cloud index. According to the Financial Times, the software-and-cloud tracking index has seen gains of more than 45% during the last year, a sharp advance during a year of economic uncertainty and occasional stock market carnage.

Looking around more broadly, tech shares with a bit more of a value flavor — GAAP profitability, regular dividends, etc. — performed well, with Apple setting new record highs as well. The smartphone giant and services shop is worth more than $1.5 trillion, underscoring how attractive stable-tech has proved in 2020. On the same theme, Microsoft is a few points from all-time highs, and is worth around $1.48 trillion.

But while software’s growth has proved attractive, as has the stability of megacorp tech shops, less certain bets have also proved attractive. Nikola, an electric vehicle company that went public recently in a reverse debut, is still worth around $26 billion despite having no reported revenue. On a similar theme, Tesla shares are up from around $225 a year ago to over $993 today, a gain of 340% or so. In Q1 2020 the company posted 38% year-over-year growth.

$420 per share feels like a long time ago.

Speaking of transportation, Uber and Lyft had separate announcements Wednesday that should have primed the ol’ investor pump. Instead, shares of both companies bopped from flat to slightly down throughout the day.

Uber announced Wednesday that it will manage an on-demand service for Marin County in the San Francisco Bay area, marking the company’s broader push to Software as a Service and public transit.

Transportation Authority of Marin (TAM) will pay Uber a subscription fee to use its management software to facilitate requesting, matching and tracking of its high-occupancy vehicle fleet, starting with a service that operates along the Highway 101 corridor. Marin Transit trips will show up in the Uber app and let users book and even share rides.

This fundamental piece of news should have appealed to investors. Today they responded with a resounding “meh,” even though it represents the first steps into generating a new stream of revenue.

Uber shares closed down 0.60% to $33.29.

Meanwhile, rival Lyft pledged Wednesday that every car, truck and SUV on its platform will be all electric or powered by another zero-emission technology by 2030, a commitment that will require the company to coax drivers to shift away from gas-powered vehicles.

The target, which Lyft plans to pursue with help from the Environmental Defense Fund, will stretch across multiple programs. It will include the company’s autonomous vehicles, the Express Drive rental car partner program for rideshare drivers, consumer rental cars for riders and personal cars that drivers use on the Lyft app.

Perhaps investors understand that even with a decade-long timeline, the target could be difficult to meet.

Lyft shares closed at $35.32, down 3.79%.

TechCrunch has slowed its public market coverage as tech equities have returned to a more stable period; that they have made back lost ground has been worth noting, but lower volatility has lowered the market’s newsworthiness. Still, from time-to-time when new all-time highs are hit, it’s worth putting our toes back into the water. And on days when different blocs of public tech set records, we can’t help but make a public note.

Tech and tech-ish stocks: still in fashion.

Powered by WPeMatico

Earlier this week, TechCrunch covered a grip of earnings reports showing that some companies helping other businesses move to modern software solutions are seeing accelerated growth. Inside the Software as a Service (SaaS) world, this is known as the digital transformation. Based on how many software companies are talking about it, the pace of change is only picking up.

But since we published that first entry, a number of SaaS companies that have posted financial results seemed to disappoint investors. Seeing some companies in the high-flying sector struggle made us sit back and think. What was going on?

Today we’re going to explore how the digital transformation’s acceleration seems real enough, but how it’s not landing equally. We’ll start by going over a short run of earnings results, talk to Yext CEO Howard Lerman about what his B2B SaaS company is seeing, and wrap with notes on what could be coming next from software shops.

We all hear about digital transformation, but it’s hard to define. Generally, it’s a broad area that includes digitization of manual processes, modern software development practices like continuous delivery and containerization and a general way of moving faster via technology — especially in the cloud.

Speaking last month on Extra Crunch Live, Box CEO Aaron Levie defined the term as he sees it. “The way that we think about digital transformation is that much of the world has a whole bunch of processes and ways of working — ways of communicating and ways of collaborating where if those business processes or that way we worked were able to be done in digital forms or in the cloud, you’d actually be more productive, more secure and you’d be able to serve your customers better. You’d be able to automate more business processes.” he said.

What we’re seeing now is that the pandemic has accelerated the rate of change much faster than many had anticipated. Efforts to slow the spread of COVID-19 and its related workplace disruptions have accelerated what would have been a normal timetable. But on its own, that doesn’t mean the market is seeing equal results across every company and industry that might be part of that trend.

Lots of SaaS companies reported earnings this week, but two sets of returns stuck out as we reviewed the results, those from Slack and Smartsheet.

Powered by WPeMatico

As the pandemic surged and companies moved from offices to working at home, they needed tools to ensure the continuity of their business operations. SaaS companies have always been focused on allowing work from anywhere there’s access to a computer and internet connection, and while the economy is reeling from COVID-19 fallout, modern software companies are thriving.

That’s because the pandemic has forced companies that might have been thinking about moving to the cloud to find tools what will get them there much faster. SaaS companies like Zoom, Box, Slack, Okta and Salesforce were there to help; cloud security companies like CrowdStrike also benefited.

While it’s too soon to say how the pandemic will affect work long term when it’s safe for all employees to return to the office, it seems that companies have learned that you can work from anywhere and still get work done, something that could change how we think about working in the future.

One thing is clear: SaaS companies that have reported recent earnings have done well, with Zoom being the most successful example. Revenue was up an eye-popping 169% year-over-year as the world shifted in a big way to online meetings, swelling its balance sheet.

There is a clear connection between the domestic economy’s rapid transition to the cloud and the earnings reports we are seeing — from infrastructure to software and services. The pandemic is forcing a big change to happen faster than we ever imagined.

Zoom and CrowdStrike are two companies expected to grow rapidly thanks to the recent acceleration of the digital transformation of work. Their earnings reports this week made those expectations concrete, with both firms beating expectations while posting impressive revenue growth and profitability results.

Powered by WPeMatico

Today after the bell, video-chat service Zoom reported its Q1 earnings. The company disclosed that it generated $328.2 million in revenue, up 169% compared to the year-ago period. The company also reported $0.20 per-share in adjusted profit during the three-month period.

Analysts, as averaged by Yahoo Finance, expected Zoom to report $202.48 million in revenue, and a per-share profit of $0.09. After its earnings smash, shares of Zoom were up slightly Update: Zoom shares are now up 2.3% ahead of its earnings call; investors had priced in this outsized-performance, it seems.

Zoom grew 78% in its preceding quarter on an annualized basis. The company’s growth acceleration is notable.

Investors were expecting big gains. Before its earnings, shares in the popular business-to-business service were up by more than 3x during the year; Zoom has found itself in an updraft due in part to COVID-19 driving workers and others to stay home and work remotely. Zoom’s software has also seen large purchase amongst consumers hungry for a video chatting solution that was simple and that works.

If the company could sustain its valuation gains going into this earnings report was an open question that has now been answered.

Zoom’s growth in its Q1 fiscal 2021 generated some notable profit results for the firm. The firm’s net income, an unadjusted profit metric, rose from $0.2 million in the year-ago quarter to $27.0 million in its most recent three months.

And Zoom’s cash generation was astounding. Here’s how the company described its results:

Net cash provided by operating activities was $259.0 million for the quarter, compared to $22.2 million in the first quarter of fiscal year 2020. Free cash flow was $251.7 million, compared to $15.3 million in the first quarter of fiscal year 2020.

It’s difficult to recall another company that has managed such growth in cash generation in such a short period of time, driven mostly by operations and not other financial acts. Zoom’s customer numbers were similarly sharp, with the firm reporting that it had 265,400 customers with more than 10 seats (employees) at the end of the quarter, which was up 354% from the year-ago period.

Though not all news for Zoom was good. Indeed, the company’s gross margin fell sharply in the quarter, compared to its year-ago result. In is Q1 fiscal 2020, Zoom reported a gross margin of around 80%. In its most recent quarter that number slipped to around 68%. In short, the company managed to convert many free users to paying customers, but still had to carry the costs of free usage of its product, something that has exploded in recent months.

Looking ahead, Zoom expects the current quarter to be another blockbuster period. The company noted in its release that it expects “between $495.0 million and $500.0 million” in revenue for Q2 of its fiscal 2021 (the current period). Looking ahead for the full fiscal year, Zoom anticipates revenues “between $1.775 billion and $1.800 billion,” numbers that take into account “the demand for remote work solutions for businesses” and “increased churn in the second half of the fiscal year” when some customers might no longer need Zoom if they can return to their offices.

Its shares might have priced in these results, but the numbers themselves are simply massive. Just three months ago Zoom turned in revenues of just $188.3 million. That’s less than it generated in free cash flow during its next three months.

Powered by WPeMatico

In spite of a positive quarter with record revenue that beat analysts’ estimates, Salesforce stock was taking a hit today because of lighter guidance. Wall Street is a tough audience.

The stock was down $8.29/share, or 4.58%, as of 2:15 pm ET.

The guidance, which was a projection for next quarter’s earnings, was lighter than what the analysts on Wall Street expected. While Salesforce was projecting revenue for next quarter in the range of $4.89 to $4.90 billion, according to CNBC, analysts had expected $5.03 billion.

When analysts see a future that is a bit worse than what they expected, it usually results in a lower stock price, and that’s what we are seeing today. It’s worth noting that Salesforce is operating in the same economy as everyone else, and being a bit lighter on your projections in the middle of a pandemic seems entirely understandable.

In yesterday’s report, CEO Marc Benioff indicated that the company has been offering some customers some flexibility around payment as they navigate the economic fallout of COVID-19, and the company’s operating cash took a bit of a hit because of this.

“Operating cash flow was $1.86 billion, which was largely impacted by delayed payments from customers while sheltering in place and some temporary financial flexibility that we granted to certain customers that were most affected by the COVID pandemic,” president and CFO Mark Hawkins explained in the analyst call.

Still, the company reported revenue of $4.87 billion for the quarter, putting it on a run rate of $19.48 billion.

In a statement, David Hynes, Jr. of Canaccord Genuity remained high on Salesforce. “If you step back and think about what Salesforce is actually providing, tools that help businesses get closer to their customers are perhaps more important than ever in a slower-growth, socially distanced world. We have long reserved a spot for CRM among our top names in large cap, and we feel no differently about that view after what we heard last night. This is a high-quality firm with many levers to growth, and as such, we believe CRM is a good way to get a bit of defensive exposure to the favorable trends at play in software.”

The company is, after all, still firmly on the path to $20 billion in revenue. As Hynes points out, overall the kinds of tools that Salesforce offers should remain in demand as companies look for ways to digitally transform much more rapidly in our current situation, and look to companies like Salesforce for help.

Powered by WPeMatico