Earnings

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re digging into SoftBank’s latest earnings slides. Not only do they contain a wealth of updates and other useful information, but some of them are gosh-darn-freaking hilarious. We all deserve a bit of levity after the last few months.

The visual elements we quote below come from SoftBank’s reporting of its own results from its fiscal year ending March 31, 2020. Much of the deck is made up of financial reporting tables and other bits of stuff you don’t want to read. We’ve cut all that out and left the fun parts.

Before we dive in, please note that we are largely giggling at some slide design choices and only somewhat at the results themselves. We are certainly not making fun of people who’ve been impacted by layoffs and other such things that these slides’ results encompass.

But we are going to have some fun with how SoftBank describes how it views the world, because how can we not? Let’s begin.

TechCrunch has a number of folks parsing SoftBank’s deck this morning, looking to do serious work. That’s not our goal. Sure, this post will tell you things like the fact that there are 88 companies in the Vision Fund portfolio, and that when it comes to unrealized gains and losses, the portfolio has seen $13.4 billion in gains and $14.2 billion in losses. $4.9 billion of gains have been realized, mind you, while just $200 million of losses have had the same honor.

And this post will tell you that the “net blended [internal rate of return] for SoftBank Vision Fund investors is -1%.”

Hell, you probably also want to know that Uber was detailed as Vision Fund’s worst-performing public company, generating a $1.46 billion loss for the group. In contrast, Guardant Health is good for a $1.67 billion gain, while 2019 IPO Slack has been good for $605 million in profits. Those were the two best companies in the Vision Fund’s public portfolio.

But what you really want is the good stuff. So, shared by slide number, here you go:

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

This week shares of SaaS and cloud companies reached new record highs as investors bid their equities higher following an earnings cycle that came in better than some expected.

SaaS stocks, as measured by the Bessemer-Nasdaq cloud index, closed at a 1,484.93 yesterday, a record, and just a hair under its intraday high of 1,491.59.

The raw numbers matter less than the index’s movement. From highs of around 1,400 in March, the index dropped to 892.60 during the early-year market selloff. Since then, SaaS and cloud companies have come roaring back. This is reflected in the new, higher valuation multiple that the companies are priced at by investors today, namley an enterprise value/revenue multiple of 14.7x.

So let’s take a look at why the SaaS cohort is the apple of Wall Street’s eye. There isn’t a single reason, but we have two that are worth considering. (Also up ahead: Notes on a chat with Alteryx’s CEO and a working definition of socialism. It’s Friday, let’s have some fun.)

Briefly, we observe movements in the value of public SaaS and cloud stocks because they inform private market investors about possible exit values for startups. This helps VCs price venture rounds. So, in a somewhat slow mechanism, public values of a stocks help price startups. Given the portion of venture capital dollars and the amount of startup effort that goes into the SaaS space (AI companies are often built using SaaS models, lots of consumer apps are SaaS, and business software is lucrative), we care a lot about the value of SaaS and cloud stocks.

So is the run-up in SaaS stocks, therefore, good for startups? Yep. Now let’s get into why clouds shares are going up.

Powered by WPeMatico

There’s something to be said for consistency through good times and bad, and one company that has had a staggeringly consistent track record is international data center vendor, Equinix. It just recorded its 69th straight positive quarter, according to the company.

That’s an astonishing record, and covers over 17 years of positive returns. That means this streak goes back to 2003. Not too shabby.

The company had a decent quarter, too. Even in the middle of an economic mess, it was still up 6% YoY to $1.445 billion and up 2% over last quarter. The company runs data centers where companies can rent space for their servers. Equinix handles all of the infrastructure providing racks, wiring and cooling — and customers can purchase as many racks as they need.

If you’re managing your own servers for even part of your workload, it can be much more cost-effective to rent space from a vendor like Equinix than trying to run a facility on your own.

Among its new customers this quarter are Zoom, which is buying capacity all over the place, having also announced a partnership with Oracle earlier this month, and TikTok. Both of those companies deal in video and require lots of different types of resources to keep things running.

This report comes against a backdrop of a huge increase in resource demand for certain sectors like streaming video and video conferencing, with millions of people working and studying at home or looking for distractions.

And if you’re wondering if they can keep it going, they believe they can. Their guidance calls for 2020 revenue of $5.877-$5.985 billion, a 6-8% increase over the previous year.

You could call them the anti-IBM. At one point Big Blue recorded 22 straight quarters of declining revenue in an ignominious streak that stretched from 2012 to 2018 before it found a way to stop the bleeding.

When you consider that Equnix’s streak includes the period of 2008-2010, the last time the economy hit the skids, it makes the record even more impressive, and certainly one worth pointing out.

Powered by WPeMatico

It’s fair to say that even before the impact of COVID-19, companies had begun a steady march to the cloud. Maybe it wasn’t fast enough for AWS, as Andy Jassy made clear in his 2019 Re:invent keynote, but it was happening all the same and the steady revenue increases across the cloud infrastructure market bore that out.

As we look at the most recent quarter’s earnings reports for the main players in the market, it seems the pandemic and economic fall out has done little to slow that down. In fact, it may be contributing to its growth.

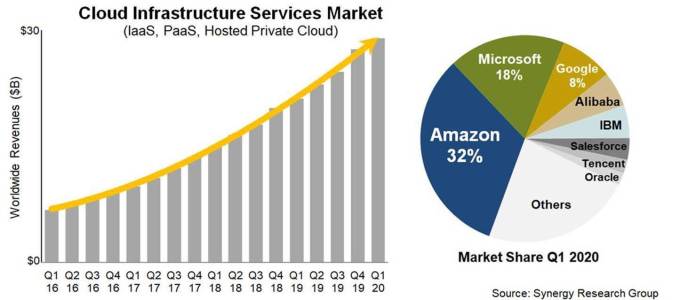

According to numbers supplied by Synergy Research, the cloud infrastructure market totaled $29 billion in revenue for Q12020.

Image Credit: Synergy Research

Synergy’s John Dinsdale, who has been watching this market for a long time, says that the pandemic could be contributing to some of that growth, at least modestly. In spite of the numbers, he doesn’t necessarily see these companies getting out of this unscathed either, but as companies shift operations from offices, it could be part of the reason for the increased demand we saw in the first quarter.

“For sure, the pandemic is causing some issues for cloud providers, but in uncertain times, the public cloud is providing flexibility and a safe haven for enterprises that are struggling to maintain normal operations. Cloud provider revenues continue to grow at truly impressive rates, with AWS and Azure in aggregate now having an annual revenue run rate of well over $60 billion,” Dinsdale said in a statement.

AWS led the way with a third of the market or more than $10 billion in quarterly revenue as it continues to hold a substantial lead in market share. Microsoft was in second, growing at a brisker 59% for 18% of the market. While Microsoft doesn’t break out its numbers, using Synergy’s numbers, that would work out to around $5.2 billion for Azure revenue. Meanwhile Google came in third with $2.78 billion.

If you’re keeping track of market share at home, it comes out to 32% for AWS, 18% for Microsoft and 8% for Google. This split has remained fairly steady, although Microsoft has managed to gain a few percentage points over the last several quarters as its overall growth rate outpaces Amazon.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

What a week it’s been. I’m exhausted. Not only are we another cycle deeper into the COVID-19 quarantine, but there seems to be more news than ever to sift through. I’ve fallen behind. So, today, this little column is taking look back at things that it missed but wanted to cover. (There may come a day when we run out of stuff to talk about, but it’s not coming any time soon.)

So let’s talk about a16z’s new crypto fund, recent economic data, the Ebang F-1, Lime’s layoffs, Procore’s IPO delay and fresh valuation, stocks, Luckin, and, if we have time, Twitter’s changing jobs data. Let’s get this all out of our heads and into the world.

To annoy my editors, we’re using bullet points this morning. Bullet points are great way to convey a bloc of information in a neat format. Let the haters hate, we have a lot of ground to cover:

Powered by WPeMatico

AWS, the cloud arm of Amazon, would be a pretty successful business on its own. Today, the company announced it has passed $10 billion for the quarter, putting the cloud business on an impressive run rate of more than $40 billion.

It was a bright spot for the company in an earnings report that saw it report net income of $2.5 billion, down $1 billion from a year ago.

Still, most companies would take that for the entire business, but AWS, which started off as kind of a side hustle for Amazon back in 2006, has grown into a powerful business all on its own. With a growth rate of 33%, it’s still growing briskly, even if it’s slowing down a bit as the law of large numbers begins to work against it.

Even though Microsoft has grown more quickly — in yesterday’s report Microsoft reported that Azure was growing at a 59% clip — AWS had such a big head start and controls a big chunk of the market share.

To give you a sense of how quickly this business has grown, Bloomberg’s Jon Erlichman tweeted the Q1 numbers for AWS since 2014, and it’s pretty amazing growth:

Amazon’s cloud revenue in Q1:

(Amazon Web Services)

Q1 2020: $10.2 billion

Q1 2019: $7.7 billion

Q1 2018: $5.4 billion

Q1 2017: $3.7 billion

Q1 2016: $2.6 billion

Q1 2015: $1.6 billion

Q1 2014: $1.1 billion— Jon Erlichman (@JonErlichman) April 30, 2020

In 2014, it was a $4 billion a year business. Today it is 9.1x that and still going strong. The good news for everyone involved is that this is a huge market, and while nobody could ever characterize the pandemic and it’s economic fall-out as good news for anyone, the fact is that it is forcing companies to move to the cloud faster than they might have wanted to go.

That should bode well for all the cloud infrastructures vendors, even as the economy shrinks, the kinds of services these vendors offer should be in more demand than ever, and that means these numbers could just keep growing for some time.

Powered by WPeMatico

Today after the bell, Zoom reported its Q4 earnings. The company’s recorded revenue of $188.3 million and its adjusted per-share profit of $0.15 were ahead of expectations, including $176.55 million in revenue and earnings per share of $0.07, according to Yahoo Finance averages.

Down several points during a broad market rally, Zoom has been a hot company to track in recent months. Its profile was heightened due to its position as an incidental benefactor of the world’s grappling with the novel coronavirus — as more countries and companies stressed staying home and working remotely, respectively, Zoom’s video conferencing tool was expected to see rising usage and demand.

The company’s shares were down sharply after reporting its earnings.

What follows is a dive into Zoom’s Q4 earnings, its expectations for the coming period and what those figures may have to say about the infection and its impacts. We’ll wrap with notes from startups that are building remote-work friendly products, sharing what they are seeing on the ground regarding demand for their services during this bleakly fascinating period of history.

Powered by WPeMatico

When Keith Block joined Salesforce from Oracle in 2013, the CRM giant was already a successful SaaS vendor on a billion-dollar quarterly revenue cadence. When the co-CEO announced he was stepping down yesterday, the company reported revenue of $4.9 billion for the quarter.

During his tenure, the company’s revenue more than quadrupled, earning an impressive $17.1 billion last year, and, as Block announced at the earnings call, the company he was leaving was forecasting revenue of $21 billion for FY2021.

Consider that it was not that long ago (in May 2017) that we wrote about the company reaching the $10 billion mark. It’s perilously easy to get lost in these numbers, to take them for granted and think they don’t mean as much as they do. It’s hard work to build a billion-dollar SaaS business, never mind $10 billion or $20 billion.

Yet Salesforce is embarking on unchartered territory for a SaaS company. It’s approaching $20 billion in revenue for a single year.

Granted, the company keeps growing revenue by making big deals like buying MuleSoft for $6.5 billion in 2018 or Tableau for $15.7 billion in 2019, or just this week buying Vlocity for a mere $1.33 billion. That means the company spent more than $25 billion over a couple of years to buy substantial companies that will help them build their business.

Block took a moment to brag a bit about his accomplishments, including how some of those purchases performed, during his swan song call with Salesforce, calling it a capstone of his time at Salesforce:

In Q4, we grew 32% in the Americas, 28% in APAC and 47% in EMEA in constant currency. Now that includes our recent acquisitions. And at the close of FY 2020, the number of Salesforce customers spending $20 million annually grew 34%.

Think about that last number for just a minute. This a SaaS vendor with the number of customers spending $20 million growing by 34%. Block helped orchestrate that growth and worked with the executive team to help determine which companies it should be targeting.

At a press conference in 2016 at Dreamforce, he discussed Salesforce’s acquisition strategy. At the time, it had bought 10 of 12 companies it would end up acquiring that year. It would buy only one in 2017, before revving up again in 2018. Here’s what he said about what they look for in a company, as we reported in an article at the time:

We look at culture. Will it be a good cultural fit? Is it a good product fit? Is there talent? Is there financial value? What are the risks of assimilating the company into our company?

There is no word on what Block will do next beyond acting as an advisor to his former co-CEO Marc Benioff, who took time in the earnings call to thank his colleague for his time at Salesforce. As well he should.

As Ray Wang, founder and principal analyst at Constellation Research point outs, Block leaves a big hole as he steps away. “If there is no equivalent replacement, you will see a significant impact in sales. Keith brought industries and sales discipline,” Wang told TechCrunch

It will be interesting to watch what he does next, and who, if anyone, will benefit from his vast experience helping to build the most successful pure SaaS company on the planet.

Powered by WPeMatico

Alibaba issued its latest earnings report yesterday, and the Chinese eCommerce giant reported that cloud revenue grew 62 percent to $1.5 billion U.S., crossing the RMB10 billion revenue threshold for the first time.

Alibaba also announced that it had completed its migration to its own public cloud in the most recent quarter, a significant milestone because the company can point to its own operations as a reference to potential customers, a point that Daniel Zhang, Alibaba executive chairman and CEO, made in the company’s post-earnings call with analysts.

“We believe the migration of Alibaba’s core e-commerce system to the public cloud is a watershed event. Not only will we ourselves enjoy greater operating efficiency, but we believe, it will also encourage others to adopt our public cloud infrastructure,” Zhang said in the call.

It’s worth noting that the company also warned that the Coronavirus gripping China could have impact on the company’s retail business this year, but it didn’t mention the cloud portion specifically.

Yesterday’s revenue report puts Alibaba on a $6 billion U.S. run rate, good for fourth place in the cloud infrastructure market share race, but well behind the market leaders. In the most recent earnings reports, Google reported $2.5 billion in revenue, Microsoft reported $12.5 billion in combined software and infrastructure revenue and market leader AWS reported a tad under $10 billion for the quarter.

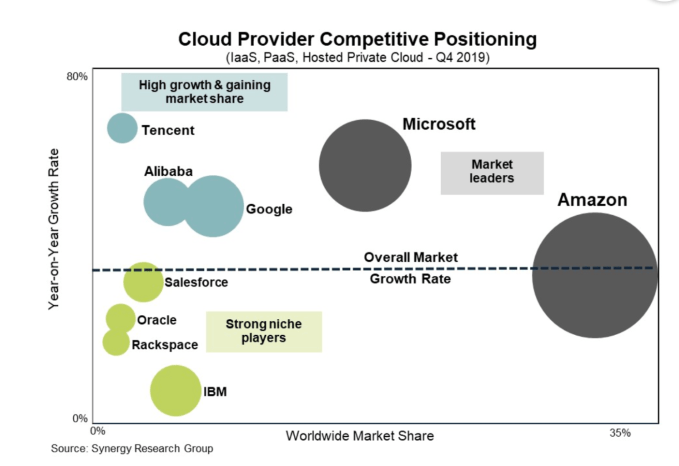

As with Google, Alibaba sits well in the back of the pack, as Synergy Research’s latest market share data shows. The chart was generated before yesterday’s report, but it remains an accurate illustration of the relative positions of the various companies.

Alibaba has a lot in common with Amazon. Both are eCommerce giants. Both have cloud computing arms. Alibaba, however, came much later to the cloud computing side of the house, launching in 2009, but really only beginning to take it seriously in 2015.

At the time, cloud division president Simon Hu boasted to Reuters that his company would overtake Amazon in the cloud market within 4 years. “Our goal is to overtake Amazon in four years, whether that’s in customers, technology, or worldwide scale,” he said at the time.

They aren’t close to achieving that goal, of course, but they are growing steadily in a hot cloud infrastructure market. Alibaba is the leading cloud vendor in China, although AWS leads in Asia overall, according to the most recent Synergy Research data on the region.

Powered by WPeMatico

Hello and welcome back to our regular look at private companies, public markets and the gray space in between.

This afternoon we’re digging into Lyft’s earnings results, unpacking the company’s performance, the market’s expectations and why shares in the American ride-hailing giant are off in after-hours trading.

Lyft’s earnings — following Uber’s own results that promised investors a quicker-than-anticipated path to (adjusted) profits — and the market’s reaction to its performance, provide a good frame for evaluating investors’ appetite for profits against growth. It’s a topic that’s important for startup founders and private-market investors alike.

Our investigation today is contentedly straightforward. We’ll start with the big numbers, drill into comparative performance and then weigh what the market is telling us.

In the fourth quarter of 2019, Lyft’s revenue came in at $1.017 billion, a gain of 52% compared to its year-ago result of $669.5 million. Sticking to the growth side of things, the company’s “active rider” count rose from 18.59 million to 22.91 million from Q4 2018 to Q4 2019, a gain of 23%. Lyft’s active riders also spent 23% more year-over-year, reaching $44.40 in the final quarter of last year.

Turning to losses, Lyft’s net loss (a metric that includes all costs) was $356.0 million in the quarter, a sharply worse result than its $248.9 million net loss in Q4 2018. The company’s adjusted net loss, however, was $121.4 million, an improvement from its year-ago $238.5 million adjusted net loss.

Turning to adjusted EBITDA, a heavily adjusted profit metric, Lyft lost $130.7 million in Q4 2019, an improvement on its Q4 2018 adjusted EBITDA loss of $251.1 million.

Investors had expected Lyft to report just $985.8 million in revenue and an adjusted EBITDA loss of $163.2 million. The street had also anticipated 100,000 fewer active riders and slightly slimmer revenue per active rider. So, Lyft beat expectations regarding growth, user count and health and for adjusted losses.

And yet Lyft’s shares are off over 4% in after-hours trading. While Lyft’s stock has recovered from lows set in October, 2019, the company’s equity is now more than $20 down from its IPO price, taking into account its post-earnings movement.

Why Lyft’s stock should fall after beating expectations and not changing its profit forecast might appear a bit confusing. It’s not.

Powered by WPeMatico