Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

SalesWhale, a Singapore-based startup that uses AI to help marketers and salespeople generate leads, has announced a Series A round worth $5.3 million.

The investment is led by Monk’s Hill Ventures — the Southeast Asia-focused firm that led SalesWhale’s seed round in 2017 — with participation from existing backers GREE Ventures, Wavemaker Partners and Y Combinator. That’s right, SalesWhale is one a select few Southeast Asian startups to have been through YC, it graduated back in summer 2016.

SalesWhale — which calls itself “a conversational email marketing platform” — uses AI-powered “bots” to handle email. In this case, its digital workforce is trained for sales leads. That means both covering the menial parts of arranging meetings and coordination, and the more proactive side of engaging old and new leads.

Back when we last wrote about the startup in 2017, it had just half a dozen staff. Fast-forward two years and that number has grown to 28, CEO Gabriel Lim explained in an interview. The company is going after more growth with this Series A money, and Lim expects headcount to jump past 70; SalesWhale is deliberating opening an office in California. That location would be primarily to encourage new business and increase communication and support for existing clients, most of whom are located in the U.S., according to Lim. Other hires will be tasked with increasing integration with third-party platforms, and particularly sales and enterprise services.

The past two years have also seen SalesWhale switch gears and go from targeting startups as customers, to working with mid-market and enterprise firms. SalesWhale’s “hundreds” of customers include recruiter Randstad, educational company General Assembly and enterprise service business Unit4. As it has added greater complexity to its service, so the income has jumped from an initial $39-$99 per seat all those years ago to more than $1,000 per month for enterprise customers.

SalesWhale’s founding team (left to right): Venus Wong, Ethan Lee and Gabriel Lim

While AI is a (genuine) threat to many human jobs, SalesWhale sits on the opposite side of that problem in that it actually helps human employees get more work done. That’s to say that SalesWhale’s service can get stuck into a pile (or spreadsheet) of leads that human staff don’t have time for, begin reaching out, qualifying leads and sending them on to living and breathing colleagues to take forward.

“A lot of potential leads aren’t touched” by existing human teams, Lim reflected.

But when SalesWhale reps do get involved, they are often not recognized as the bots they are.

“Customers are often so convinced they are chatting with a human — who is sending collateral, PDFs and arranging meetings — that they’ll say things like ‘I’d love to come by and visit someday,’ ” Lim joked in an interview.

“Indeed, a lot of times, sales team refer to [SalesWale-powered] sales assistant like they are a real human colleague,” he added.

Powered by WPeMatico

When Zoom hit the public markets Thursday, its IPO pop, a whopping 81 percent, floored everyone, including its own chief executive officer, Eric Yuan.

Yuan became a billionaire this week when his video conferencing business went public. He told Bloomberg that he actually wished his stock hadn’t soared quite so high. I’m guessing his modesty and laser focus attracted Wall Street to his stock; well, that, and the fact that his business is actually profitable. He is, this week proved, not your average tech CEO.

I chatted with him briefly on listing day. Here’s what he had to say.

“I think the future is so bright and the stock price will follow our execution. Our philosophy remains the same even now that we’ve become a public company. The philosophy, first of all, is you have to focus on execution, but how do you do that? For me as a CEO, my number one role is to make sure Zoom customers are happy. Our market is growing and if our customers are happy they are going to pay for our service. I don’t think anything will change after the IPO. We will probably have a much better brand because we are a public company now, it’s a new milestone.”

“The dream is coming true,” he added.

For the most part, it sounded like Yuan just wants to get back to work.

Want more TechCrunch newsletters? Sign up here. Otherwise, on to other news…

You thought I was done with IPO talk? No, definitely not:

While I’m on the subject of Uber, the company’s autonomous vehicles unit did, in fact, raise $1 billion, a piece of news that had been previously reported but was confirmed this week. With funding from Toyota, Denso and SoftBank’s Vision Fund, Uber will spin-out its self-driving car unit, called Uber’s Advanced Technologies Group. The deal values ATG at $7.25 billion.

The TechCrunch staff traveled to Berkeley this week for a day-long conference on robotics and artificial intelligence. The highlight? Boston Dynamics CEO Marc Raibert debuted the production version of their buzzworthy electric robot. As we noted last year, the company plans to produce around 100 models of the robot in 2019. Raibert said the company is aiming to start production in July or August. There are robots coming off the assembly line now, but they are betas being used for testing, and the company is still doing redesigns. Pricing details will be announced this summer.

#TCRobotics pic.twitter.com/Vf4kUWH0fR

— Lucas Matney (@lucasmtny) April 19, 2019

Digital health investment is down

Despite notable rounds for digital health businesses like Ro, known for its direct-to-consumer erectile dysfunction medications, investment in the digital health space is actually down, reports TechCrunch’s Jonathan Shieber. Venture investors, private equity and corporations funneled $2 billion into digital health startups in the first quarter of 2019, down 19 percent from the nearly $2.5 billion invested a year ago. There were also 38 fewer deals done in the first quarter this year than last year, when investors backed 187 early-stage digital health companies, according to data from Mercom Capital Group.

Byton loses co-founder and former CEO, reported $500M Series C to close this summer

Lyric raises $160M from VCs, Airbnb

Brex, the credit card for startups, raises $100M debt round

Ro, a D2C online pharmacy, reaches $500M valuation

Logistics startup Zencargo gets $20M to take on the business of freight forwarding

Co-Star raises $5M to bring its astrology app to Android

Y Combinator grad Fuzzbuzz lands $2.7M seed round to deliver fuzzing as a service

Hundreds of billions of dollars in venture capital went into tech startups last year, topping off huge growth this decade. VCs are reviewing more pitch decks than ever, as more people build companies and try to get a slice of the funding opportunities. So how do you do that in such a competitive landscape? Storytelling. Read contributor’s Russ Heddleston’s latest for Extra Crunch: Data tells us that investors love a good story.

Plus: The different playbook of D2C brands

And finally, for the first of a new series on VC-backed exits aptly called The Exit. TechCrunch’s Lucas Matney spoke to Bessemer Venture Partners’ Adam Fisher about Dynamic Yield’s $300M exit to McDonald’s.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about rounds for Brex, Ro and Kindbody, plus special guest Danny Crichton joined us to discuss the latest in the chip and sensor world.

Powered by WPeMatico

Zoom, a relatively under-the-radar tech unicorn, has defied expectations with its initial public offering. The video conferencing business priced its IPO above its planned range on Wednesday, confirming plans to sell shares of its Nasdaq stock, titled “ZM,” at $36 apiece, CNBC reports.

The company initially planned to price its shares at between $28 and $32 per share, but following big demand for a piece of a profitable tech business, Zoom increased expectations, announcing plans to sell shares at between $33 and $35 apiece.

The offering gives Zoom an initial market cap of roughly $9 billion, or nine times that of its most recent private market valuation.

Zoom plans to sell 9,911,434 shares of Class A common stock in the listing, to bring in about $350 million in new capital.

If you haven’t had the chance to dive into Zoom’s IPO prospectus, here’s a quick run-down of its financials:

Zoom is backed by Emergence Capital, which owns a 12.2 percent pre-IPO stake; Sequoia Capital (11.1 percent); Digital Mobile Venture, a fund affiliated with former Zoom board member Samuel Chen (8.5 percent); and Bucantini Enterprises Limited (5.9 percent), a fund owned by Chinese billionaire Li Ka-shing.

Zoom will debut on the Nasdaq the same day Pinterest will go public on the NYSE. Pinterest, for its part, has priced its shares above its planned range, per The Wall Street Journal.

Powered by WPeMatico

I sat down with Menlo Ventures partner Shawn Carolan this week to talk about his early investment in Uber. Menlo, if you remember, led Uber’s Series B and has made a hefty sum over the year selling shares in the ride-hailing company. I’ll have more on that later; for now, I want to share some of the insights Carolan had on his experience ditching venture capital to become a founder.

Around when Menlo made its first investment in Uber, Carolan began taking a step back from the firm and building Handle, a startup that built tools to help people be more productive. Despite years of hard work, Handle was ultimately a failure. Carolan said he shed a lot of tears over its demise, but used the experience to connect more intimately with founders and to offer them more candid, authentic advice.

“People in the valley are always achievement-oriented; it’s always about the next thing and crushing it and whatever,” Carolan told TechCrunch. “When [Handle] shut down, I had this spreadsheet of all the people who I felt like I disappointed: Seed investors who invested in me, all the people at Menlo and my friends who had tweeted out early stuff. It was a long spreadsheet of like 60 people. And when I started a sabbatical, what I said was I’m going to go connect with everyone and apologize.”

Today, Carolan encourages founders to own their vulnerabilities.

“It’s OK to admit when you’re wrong,” he said. “Now I can see it on [founders’] faces, I can see when they’re scared. And they’re not going to say they’re scared but I know it’s tough. This is one of the toughest things that you’re going to go through. Now I can be there emotionally for these founders and I can say ‘here’s how you do it, here’s how you talk to your team and here’s what you share.’ A lot of founders feel like they have to do this alone and that’s why you have to get comfortable with your vulnerability.”

After Handle shuttered, Carolan returned to Menlo full time and made the firm a boatload of money from Roku’s IPO and now Uber’s. Anyway, thought those were some nice anecdotes that should be shared since most of our feeds are dominated by Silicon Valley hustle porn.

Want more TechCrunch newsletters? Sign up here. Ok, on to other news…

IPO corner

There were so many fund announcements this week; here’s a quick list.

Lots of great new exclusive content for our Extra Crunch subscribers is on the site, including this deep dive into the challenges of transportation startup profits. Plus: When to ditch a nightmare customer, before they kill your startup; The right way to do AI in security; and The definitive Niantic reading guide.

Sinema, that one MoviePass competitor, has run into its fair share of bumps in the road. TechCrunch’s Brian Heater hopped on the phone with the startup’s CEO this week to learn more about those bumps, why its terminating accounts en masse, a class-action lawsuit its battling and more.

Photo by Stephen McCarthy / RISE via Sportsfile

TechCrunch’s Startup Battlefield brings the world’s top early-stage startups together on one stage to compete for non-dilutive prize money, and the attention of media and investors worldwide. Here’s a quick update on some of our BF winners and finalists:

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm, myself and Phil Libin, the founder of Evernote and AllTurtles, chat about the importance of IPOs. Plus, in a special Equity Shot, Alex and I unpack the Uber S-1.

Powered by WPeMatico

Hundreds of billions of dollars in venture capital went into tech startups last year, topping off huge growth this decade. Here at DocSend, we’re seeing the downstream effects in our data: investors who receive DocSend links are reviewing more pitch decks than ever, as more people build companies and try to get a slice of the funding opportunities.

So it stands to reason that making your pitch deck stand out is critical to raising a round. But how do you do that in such a competitive landscape?

After analyzing both successful and failed fundraising pitch decks, we’ve learned that storytelling matters and this hasn’t changed over the last few years. This makes intuitive sense — who doesn’t love a good story?

But does telling a story help founders raise capital successfully? And more importantly, do you fail to fundraise if you don’t tell a story? In this post, I’m going to share some hard evidence.

It follows up on my post over on TechCrunch, looking at three big mistakes we see in failed pitch decks.

Before we start diving into the data, here’s why we know: our document sharing and tracking platform is used every day by thousands of startups to share their decks securely with investors, with visits to pitch decks shared via DocSend having grown 4x from 2017 to 2018. Controlling for DocSend’s growth, we estimate that investors are viewing 35% more decks in 2018 than they did in 2017.

In total, over 100,000 users have shared over 2.2 million links through DocSend since we launched in 2014, and these documents have received over 220 million views; while we’ve grown quickly among sales, business development and customer success teams, startup pitch decks have continued to be a popular use-case. We’ve also been analyzing the pitch data in a collaboration with Harvard Business School since 2015, so we’re experienced at analyzing and interpreting this data.

The old adage “you only get one chance to make a first impression” is true when it comes to pitch decks, and in fact that was the case for our company’s own fundraising process. When I pitched DocSend for our seed round, I knew what we were up against — why will this be a big business? And, why won’t Google build this? Our product was still in private beta, and we had no revenue. However, we had an MVP and those who were using our product, including our potential investors, found the product to be very useful.

Powered by WPeMatico

The SoftBank Vision Fund has been screaming from the venture headlines the last few months, driven by eye-popping rounds (and valuations!) into some of the most notable startups around the world. Yet, SoftBank isn’t the only player rapidly buying up the cap tables of top startups. Indeed, another firm, more than a century old, has been fighting for that late-stage equity crown.

… Who the what?

When our fintech contributor Gregg Schoenberg interviewed Charles Plowden, the firm’s joint senior partner, about the firm’s prodigious investing, we realized that we have never gone in-depth on one of the most influential investors in Silicon Valley. So here goes.

Baillie Gifford is a 110-year-old asset management firm based out of Edinburgh, Scotland, and has long had a penchant for pre-IPO tech companies. The firm was an early investor into some of the world’s most valuable private and public tech companies, boasting a roster of portfolio companies that includes unicorns from nearly all generations in modern tech, including everything from Amazon, Google and Salesforce to Tesla, Airbnb, Spotify, newly public Lyft, Palantir and even SpaceX.

Baillie Gifford’s reach stretches way beyond the 280/101 corridor. The firm has an extensive history of investing across geographies, with one of its first and most successful investments coming from an early entry into Chinese e-commerce titan Alibaba. More recently, Baillie Gifford even held a stake in recently IPO’d Chinese electric autonomous vehicle manufacturer NIO, and one the firm’s largest current holdings is South African internet conglomerate Naspers — which itself is an active investor and developer of emerging market tech infrastructure.

The firm’s low profile belies its aggressive capital deployment strategy. According to data from PitchBook, Baillie Gifford was involved in roughly 20 deals in 2018 and was involved as a lead or participant in transactions worth over $21 billion in aggregate total deal size — beating out behemoth Tiger Global, which tallied roughly $13.25 billion on the same metric.

The firm has about $2 billion focused on private companies, so while it is aggressive in getting into later-stage rounds, it is not nearly operating at the scale of say the Vision Fund or Tiger Global. While the asset manager primarily focuses on public-equity investing, the firm has participated in investment rounds as early as Series A, according to PitchBook and Crunchbase data.

Overall, the firm manages $221 billion in assets under management as of January 2019.

As one of the earliest asset managers to invest in pre-IPO tech companies, Baillie Gifford has sourced investments through its longstanding reputation as an investor. The firm first began really diving into private tech investing in the wake of the dot-com bubble. The firm doubled down on the tech sector at a time when few others were investing and sifted through the blood bath to find cheap entryways into companies that are now amongst the world’s largest.

Today, however, the landscape is undoubtedly much different. Tech companies now make up four of the top five largest companies in the world by market cap, and seven out of the top 10. Now, everyone wants a piece of the pie and there seem to be more checks being thrown at founders than most can even fit in their wallets.

With more capital at their fingertips than ever before, founders are opting to keep their startups private for longer in order to avoid the stress of having to deal with short-term public market investors who are more often than not looking for the first opportunity to cash out. So why, amongst so much choice, do companies continue to partner with Baillie Gifford?

Plowden has some insights on that front in our interview, but the summary is that Baillie Gifford just sees itself as a partner. Unlike its peers and most investment managers, Baillie Gifford has no outside shareholder owners to report to. As a partnership, wholly owned and run by just 44 partners, the firm doesn’t face the organizational constraints that beset most firms that manage billions and billions in assets.

The result? In short, Baillie Gifford has quietly been making a killing, and probably drinking some good Scotch along the way, as well.

Powered by WPeMatico

“It is our contention that the investment industry may be experiencing a peak of its own, in this case the point of the maximum rate at which it extracts value from its clients’ assets. Let’s call it Peak Gravy.” That’s a recent quote from Tom Coutts, who is one of a few dozen partners at Baillie Gifford (See Arman Tabatabai’s profile here). It’s also typical of the provocative sentiments offered by this band of fund managers who are based in Edinburgh, but scour the world looking for opportunities.

In an effort to distinguish its world view, the firm has introduced the somewhat eyebrow-raising tagline, “We’re actual investors.” For many US technology observers, though, Baillie Gifford is known for its investments in unicorns. But as Extra Crunch’s executive editor Danny Crichton and I found out in a recent conversation with Charles Plowden (one of two senior partners and the overseer of the firm’s investment departments), there’s a lot more to the story and motivations behind this unique 110-year-old partnership that’s still going strong.

Powered by WPeMatico

Let’s start this week’s newsletter with some data. Nationally, startups pulled in $30.8 billion in the first quarter of 2019, up 22 percent year-on-year, according to Crunchbase’s latest deal round-up.

A closer look at the numbers shows a big drop in angel funding and a slight decrease in mega-rounds, or financings larger than $100 million. The number of mega-rounds fell to 57 deals in Q1 and deal value was down too. With that said, mega-rounds still accounted for $16.4 billion, making Q1 2019 the second-best quarter on record for mega-rounds.

The bottom line is these monstrous deals represented a big chunk (29 percent) of all the dollars invested in U.S. startups in Q1. As investors move downstream and startups opt to stay private longer and longer, we’ll continue to see a greater pick up in mega rounds.

Want more TechCrunch newsletters? Sign up here.

OK, on to other news…

Once trading after the pink confetti was swept up off the floor, analysts and investors had a different story to tell about one of the first unicorns to make its public debut. Lyft began the week struggling to hit its IPO price, closing several days under that $72, despite opening with a 20 percent pop at $86. What’s going on? People are shorting the Lyft stock, looking to profit off the company’s sinking value. Things are looking up though; on Friday as I typed this newsletter, Lyft was trading at about $74 per share.

.@Uber sent @Lyft a whole bunch of cakes on IPO day, how nice. pic.twitter.com/hbZC5HOxbL

— Kate Clark (@KateClarkTweets) April 5, 2019

In other IPO, or shall I say, direct listing news, Slack has reportedly chosen the NYSE for its upcoming exit. A quick reminder why Slack has opted to go public via direct listing: The company doesn’t need any IPO cash thanks to the hundreds of millions of dollars on its balance sheet, but its longtime employees and investors need the liquidity. A direct listing allows it to go public without listing any new shares, with no lockup period and no intermediary bankers. The process saves it some money and expedites the process. OK, that wasn’t as brief as I intended, moving on…

Saying goodbye to venture capital

In a story that sent the entirety of Silicon Valley into a frenzy, Forbes reported that Andreessen Horowitz was denouncing its status as a venture capital firm and would register all its employees as financial advisors. For those inclined, Crunchbase News’ Alex Wilhelm and I unpacked what this means in the latest episode of Equity; for those less inclined, here’s the TLDR: For a16z to have the freedom to make riskier bets, like buying public company stock or heaps of cryptocurrency, the title of financial advisor gives them that ability.

Femtech, defined as any software, diagnostics, products and services that leverage technology to improve women’s health, has attracted some $250 million in VC funding so far this year, according to PitchBook. That puts the sector on pace to secure nearly $1 billion in investment by year-end, greatly surpassing last year’s record of $650 million. For more historical context, startups in the space brought in only $62 million in 2012, $225 million in 2014 and $231 million in 2016.

Alternative financier Clearbanc says it will invest $1 billion in 2,000 e-commerce startups in 2019. Here’s the catch: Until the companies have paid back 106 percent of Clearbanc’s investment, Clearbanc takes a percentage of their revenues every month. Clearbanc’s goal is to help companies preserve equity, favoring a revenue share model rather than the traditional VC model, which eats equity in startups in exchange for capital. I spoke to Clearbanc co-founder Michele Romanow to learn more about Clearbanc’s attempt to disrupt venture capital.

TechCrunch’s Megan Rose Dickey authored the be-all-end-all story on the shared-electric-scooter business. Here’s a quick passage: “The startup ecosystem had become accustomed to the ethos of begging for forgiveness, rather than asking for permission. But that’s not the case with electric scooters. These companies have found their entire businesses to be contingent on the continued approval from individual cities all over the world. That inherently creates a number of potential conflicts.” Extra Crunch subscribers can read the full story here.

Plus, we dropped the Niantic EC-1, in which Greg Kumparak dives deep into the history of the maker Pokemon Go, contributor Sherwood Morrison looked at remote workers and nomads, who represent the next tech hub.

TechCrunch has confirmed that Airbnb has invested between $150 million to $200 million in Indian hotel startup Oyo. Airbnb confirmed the existence of the deal but not the exact amount. The home-sharing giant is continuing to widen its focus beyond “unconventional” hotels as it prepares to begin selling pubic market investors on its long-term vision. Remember, this deal comes right after its big acquisition of HotelTonight.

WeWork acquired Managed by Q this week, a VC-backed startup that helps office managers and other decision-makers handle supply stocking, cleaning, IT support and other non-work related tasks in the office by simply using the Managed by Q dashboard. The company was most recently valued at $250 million, having raised a total of $128.25 million from investors such as GV, RRE and Kapor Capital.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about the future of a16z, Jumia’s IPO, the Midas list and more of this week’s headlines.

Powered by WPeMatico

During my recent conversation with Peter Kraus, which was supposed to be focused on Aperture and its launch of the Aperture New World Opportunities Fund, I couldn’t help veering off into tangents about the market in general. Below is Kraus’ take on the availability of alpha generation, the Fed, inflation versus Amazon, housing, the cross-ownership of U.S. equities by a few huge funds and high-frequency trading.

Gregg Schoenberg: Will alpha be more available over the next five years than it has been over the last five?

To think that at some point equities won’t become more volatile and decline 20% to 30%… I think it’s crazy.

Peter Kraus: Do I think it’s more available in the next five years than it was in the last five years? No. Do I think people will pay more attention to it? Yes, because when markets are up to 30 percent, if you get another five, it doesn’t matter. When markets are down 30 percent and I save you five by being 25 percent down, you care.

GS: Is the Fed’s next move up or down?

PK: I think the Fed does zero, nothing. In terms of its next interest rate move, in my judgment, there’s a higher probability that it’s down versus up.

Powered by WPeMatico

Less than a decade ago IPOs, acquisitions and global expansion by African startups were more possibility than reality. March saw all three from the continent’s tech scene.

Pan-African e-commerce company Jumia filed for an IPO on the New York Stock Exchange, per SEC documents and confirmation from chief executive Sacha Poignonnec.

In an updated filing, (since the March 12 original) Jumia indicated it will offer 13,500,000 ADR shares, for an offering price of $13 to $16 per share to trade under the ticker symbol “JMIA.” The IPO could raise up to $216 million for Jumia.

Since our first story (and reflected in the latest SEC docs), Mastercard Europe agreed upfront to buy $50 million in Jumia ordinary shares.

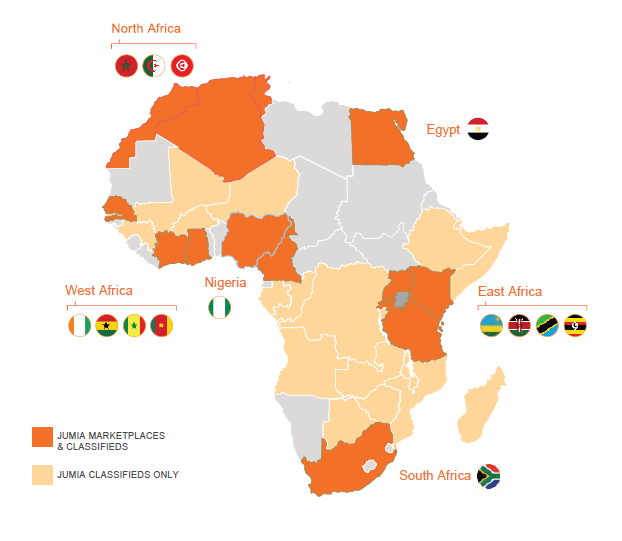

With a smooth filing process, Jumia will become the first African startup to list on a major global exchange. The company is incorporated in Germany, but maintains its headquarters in Nigeria, and operates exclusively in Africa, with 4,000 employees on the continent.

The pending IPO creates another milestone for Jumia. The venture became the first African startup unicorn in 2016, achieving a $1 billion valuation after a funding round that included Goldman Sachs, AXA and MTN.

Founded in Lagos in 2012 with Rocket Internet backing, Jumia now operates multiple online verticals in 14 African countries. Goods and services lines include Jumia Food (an online takeout service), Jumia Flights (for travel bookings) and Jumia Deals (for classifieds). Jumia processed more than 13 million packages in 2018, according to company data. The company has started to generate annual revenues over $100 million, but like many burn-rate startups, has done so while racking up big losses.

There’ll be a lot more to cover, analyze and debate pre and post Jumia’s NYSE bell toll — which could happen in coming weeks or months. For example, can Jumia generate a profit; is it really an African startup; will Jumia become an acquisition target for a big outside name or an acquirer of smaller startups in African e-commerce? Stay tuned for continuing TechCrunch coverage.

On the acquisition front, Lagos-based online lending startup OneFi bought Nigerian payment solutions company Amplify for an undisclosed amount.

OneFi is taking over Amplify’s IP, team and client network of more than 1,000 merchants to which Amplify provides payment processing services, OneFi CEO Chijioke Dozie told TechCrunch.

The purchase of Amplify caps off a busy period for OneFi. Over the last seven months the Nigerian venture secured a $5 million lending facility from Lendable, announced a payment partnership with Visa and became one of the first (known) African startups to receive a global credit rating. OneFi is also dropping the name of its signature product, Paylater, and will simply go by OneFi (for now).

Collectively, these moves represent a pivot for OneFi away from operating primarily as a digital lender, toward becoming an online consumer finance platform.

“We’re not a bank but we’re offering more banking services…Customers are now coming to us not just for loans but for cheaper funds transfer, more convenient bill payment, and to know their credit scores,” said Dozie.

OneFi will add payment options for clients on social media apps, including WhatsApp, this quarter — something in which Amplify already holds a specialization and client base. Through its Visa partnership, OneFi will also offer clients virtual Visa wallets on mobile phones and start providing QR code payment options at supermarkets, on public transit and across other POS points in Nigeria.

On the back of the acquisition, OneFi is in the process of raising a round and will look to expand internationally, considering Senegal, Côte d’Ivoire, DRC, Ghana and Egypt and Europe for Diaspora markets.

On African startups expanding globally, FlexClub — a South African venture that matches investors and drivers to cars for ride-hailing services — announced it will expand in Mexico in a partnership with Uber after closing a $1.2 million seed round led by CRE Venture Capital.

The move comes as Africa’s tech-transit space continues to produce unique mobility solutions shaped around local needs.

FlexClub touts itself as a “gig economy investment platform” that is creating new asset classes in emerging markets, according to chief executive and co-founder Tinashe Ruzane.

That asset class, for now, is ride-hail vehicles. FlexClub allows investors to go on the site and purchase a car (ultimately managed and serviced by FlexClub). The startup then connects that car to an Uber driver who uses earnings to pay a weekly rental charge.

Those fees generate monthly fixed-rate interest income for the investor. The driver has the option of buying the car after 12 months, with a descending purchase price over time.

FlexClub’s platform manages the investment, rental income and disbursement of funds across all parties. The startup also handles insurance, maintenance and upkeep of the cars.

Ruzane envisions this as a model to finance multiple asset classes in emerging markets — where lending options are fewer for individuals who may not have credit histories.

“Our goal is to make this completely passive… where investors can invest in different kinds of assets on our platform, login to a dash, and see this is how my five cars in South Africa are doing, my vans in Mexico, my motorbikes in Indonesia — with a diversified portfolio around the world,” he explained.

FlexClub will begin work matching investors to cars and Uber drivers in Mexico in April. The startup sees opportunities to move into other mobility classes, such as Africa’s ride-hail motorcycle taxi and three-wheel tuk-tuk market, CEO Tinashe Ruzane told TechCrunch in this feature.

And finally, francophone Africa will see a boost in funds and support for startups. The Dakar Network Angels group launched last month, making its first investment to cleantech venture Coliba — an Ivorian startup that uses a mobile app to coordinate waste recycling

The deal is part of Dakar Network Angels’ mission of convening experts and capital to bridge the resource gap for startups in French-speaking Africa — or 24 of the continent’s 54 countries.

The organization — which goes by DNA for short — will offer seed fund investments of between $25,000 to $100,000 to early-stage ventures with high growth potential. These rounds will come with the entrepreneurial guidance of DNA’s angel network.

Launched in Senegal, the organization’s founder Marieme Diop — a VC investor at Orange Digital Ventures — named the goal of bridging VC disparities between francophone and non-francophone Africa as the primary driver for DNA. She pointed to funding data by Partech, indicating that 76 percent of investment to African startups goes to three English-speaking countries — Nigeria, Kenya and South Africa.

To gain consideration for DNA investment, startups must gain referral by a member. DNA will take a minority stake (less than 10 percent) in ventures that receive seed funds and provide program mentorship until exits, Diop told TechCrunch.

To become an angel, members must commit to investing a minimum of $10,000 a year (for those coming on as individuals), $20,000 (for corporates) and be on hand to support the portfolio startups, according to DNA’s Corporate Membership Charter.

More Africa Related Stories @TechCrunch

African Tech Around The Net

Powered by WPeMatico