Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

Hotels can be pricey, and travelers are often forced to leave their rooms for basic things, like food that doesn’t come from the minibar. Yet Airbnb accommodations, which have become the go-to alternative for travelers, can be highly inconsistent.

Domio, a two-year-old, New York-based outfit, thinks there’s a third way: apartment hotels, or “apart hotels,” as the company is calling them.

The idea is to build a brand that travelers recognize as upscale yet affordable, more tech friendly than boutique hotels and features plenty of square footage, which it expects will appeal to both families as well as companies that send teams of employees to cities and want to do it more economically.

Domio has a host of competitors, if you’ll forgive the pun. Marriott International earlier this year introduced a branded home-sharing business called Tribute Portfolio Homes wherein it says it vets, outfits and maintains to hotel standards homes of its choosing. And Marriott is among a growing number of hotels to recognize that customers who stay in a hotel for a business trip or a family vacation might prefer a multi-bedroom apartment with hotel-like amenities.

Property management companies have been raising funding left and right for the same reason. Among them: Sonder, a four-year-old, San Francisco-based startup offering “spaces built for travel and life” that, according to Crunchbase, has raised $135 million from investors, much of it this year; TurnKey, a six-year-old, Austin, Tex.-based home rental management company that has raised $72 million from investors, including via a Series D round that closed back in March; and Vacasa, a nine-year-old, Portland, Ore.-based vacation rental management company that manages more than 10,000 properties and which just this week closed on $64 million in fresh financing that brings its total funding to $207.5 million.

That’s saying nothing of Airbnb itself, which has begun opening hotel-like branded apartment complexes that lease units to both long-term renters and short-term visitors in partnership with development partner Niido.

Whether Domio can stand out from competitors remains to be seen, but investors are happy to provide it the financing to try. The company is today announcing it has raised $12 million in Series A equity funding led by Tribeca Venture Partners, with participation from SoftBank Capital NY and Loric Ventures. The round comes on the heels of Domio announcing a $50 million joint venture last month with the private equity firm Upper 90 to exclusively fund the leasing and operations of as many as 25 apartment-style hotels for group travelers.

Indeed, Domio thinks one advantage it may have over other home-share companies is that rather than manage the far-flung properties of different owners, it can shave costs and improve the quality of its offerings by entering five- to 10-year leases with developers and then branding, furnishing and operating entire “apart hotel” properties. (It even has partners in China making its furniture.)

As CEO and former real estate banker Jay Roberts told us earlier this week, the plan is to open 25 of these buildings across the U.S. over the next couple of years. The units will average 1,500 square feet and feature two to three bedrooms, and, if all goes as planned, they’ll cost 10 to 25 percent below hotel prices, too.

And if the go-go property management market turns? Roberts insists that Domio can “slow down growth if necessary.” He also notes that “Airbnb was founded out of the recession, supported by people who were interested in saving money. We’re starting to see companies that want to be more cost-effective, too.”

Domio had earlier raised $5 million in equity and convertible debt from angel investors in the real estate industry; altogether it has now amassed funding of $67 million.

Powered by WPeMatico

Now that “utility” tokens have become a popular and international way to fund major blockchain projects, a pair of investors are creating a new way to turn tokens into true equities. The investors, Jonathan Nelson and Laura Nelson, have created Hack Fund, an early stage investment vehicle that allows startups to launch what amounts to “blockchain stock certificates,” according to Jonathan.

“Our previous business model exchanged equity from startup companies for services, and wrapped that equity into funds that we then sold to investors. These fund investors have included family offices, institutions, and high net worth individuals,” said Jonathan. “However, Hack Fund represents a new business model. Because Hack Fund leverages the blockchain, investors all over the world at all levels can participate in startup investing by trading blockchain stock certificates. Also, its SEC compliant structure means that it is also available to a limited number of accredited investors in the US.”

The team originally created Hackers/Founders, a tech entrepreneur group in Silicon Valley, and they now support 300,000 members in 133 cities and 49 countries. Hack Fund is a vehicle to support some of the startups in the Hackers/Founders network.

“HACK Fund, through its Hackers/Founders heritage, has a large, unique global network,” said Jonathan. “This provides Hack Fund with unparalleled reach and deal flow across the global technology market. There are a few blockchain-based funds, but they are limited themselves to blockchain-only investments. Unlike typical venture funds, HACK Fund will provide quick liquidity for investors, leveraging blockchain technology to make typically illiquid private stocks tradeable.”

The idea behind Hack Fund is quite interesting. In most cases investing in a company leads to up to ten years of waiting for a liquidity event. However, with blockchain-based stock certificates investors can buy shares that can be bought and sold instantly while company performance drives the value up or down. In short, startups become liquid in an instant, which can be a good thing or a bad thing, depending on the founding team.

“HACK Fund is a publicly traded closed-end fund. The fund’s venture investments are valued on a quarterly basis by an independent third party, audited and posted to the blockchain for all token holders to review. There are no K-1 statements issued, there is no partnership/LLC, rather HACK Fund is an investment company akin to Berkshire Hathaway which invests in the same manner as early-stage venture capital,” said Jonathan.

The $100 million fund raise has already kicked off across Asia, Middle East, Latin America and to a small number of accredited investors in the US. The fund will be rounded out with $2 million from retail investors who will be able to buy some of the tokens on October 29th through BRD wallet.

Powered by WPeMatico

Zocdoc founder Cyrus Massoumi and Indiegogo founder Slava Rubin have created a new $30 million fund called Humbition aimed at early stage, founder-led companies in New York.

“The fund is focused on connecting startups with investors and advisors experienced in building and growing successful businesses,” said Rubin.

“We are seeking to fill a void in NYC, where the vast majority of early stage investors have no significant experience building and scaling businesses,” he said. “The fund’s main areas of investment include marketplaces, consumer and health tech. But the primary criteria for investments is high quality founders. The fund is also seeking out mission-driven businesses because the companies that are socially responsible will be the most successful in the coming decades.”

The fund has brought on ClassPass founder Payal Kadakia, Warby Parker founder Neil Blumenthal, Charity: Water CEO and founder Scott Harrison, and Casper founder and CEO Philip Krim as advisors. They have already invested some of the $30 million raise in Burrow, a couch-on-demand service.

“New York City is home to a tremendous number of mission-driven startups that are simply not receiving the same level of support as their peers in the Bay Area. This void presents a unique opportunity for humbition to reach the incredible local talent who need the funding and guidance to build and grow their businesses in New York City,” said Rubin.

Powered by WPeMatico

In the days leading up to TechCrunch Disrupt SF 2018, The Economist published the cover story, ‘Why Startups Are Leaving Silicon Valley.’

The author outlined reasons why the Valley has “peaked.” Venture capital investors are deploying capital outside the Bay Area more than ever before. High-profile entrepreneurs and investors, Peter Thiel, for example, have left. Rising rents are making it impossible for new blood to make a living, let alone build businesses. And according to a recent survey, 46 percent of Bay Area residents want to get the hell out, an increase from 34 percent two years ago.

Needless to say, the future of Silicon Valley was top of mind on stage at Disrupt.

“It’s hard to make a difference in San Francisco as a single entrepreneur,” said J.D. Vance, the author of ‘Hillbilly Elegy’ and a managing partner at Revolution’s Rise of the Rest Fund, which backs seed-stage companies based outside Silicon Valley. “It’s not as a hard to make a difference as a successful entrepreneur in Columbus, Ohio.”

In conversation with Vance, Revolution CEO Steve Case said he’s noticed a “mega-trend” emerging. Founders from cities like Pittsburgh, Detroit or Portland are opting to stay in their hometowns instead of moving to U.S. innovation hubs like San Francisco.

“The sense that you have to be here or you can’t play is going to start diminishing.”

“We are seeing the beginnings of a slowing of what has been a brain drain the last 20 years,” Case said. “It’s not just watching where the capital flows, it’s watching where the talent flows. And the sense that you have to be here or you can’t play is going to start diminishing.”

J.D. Vance says that most entrepreneurs don’t need to move to Silicon Valley.

Here’s why. #TCDisrupt pic.twitter.com/0mFPeTuHLe

— TechCrunch (@TechCrunch) September 6, 2018

Farewell, San Francisco

“It’s too expensive to live here,” said Aileen Lee, the founder of seed-stage VC firm Cowboy Ventures, amid a conversation with leading venture capitalists Spark Capital general partner Megan Quinn and Benchmark general partner Sarah Tavel .

“I know that there are a lot of people in the Bay Area that are trying to work on that problem and I hope that they are successful,” Lee added. “It’s an amazing place to live and we’ve made it really challenging for people to live here and not worry about making ends meet.”

One of Cowboy’s portfolio companies opted to relocate from Silicon Valley to Colorado when it came time to scale their business. That kind of move would’ve historically been seen as a failure. Today, it may be a sign of strong business acumen.

Quinn said that of all 28 of Spark’s growth-stage portfolio companies, Raleigh, North Carolina-based Pendo has the easiest time recruiting folks locally and from the Bay Area.

She advises her Bay Area-based late-stage companies to open a second office outside of the Valley where lower-cost talent is available.

“We often say go to [flySFO.com], draw a three-hour circle around San Francisco where they have direct flights, find a city that has a university and open up a second office as quickly as possible,” Quinn said.

Still, all three firms invest in a lot of companies based in San Francisco. Of Benchmark’s 10 most recent investments, for example, eight were based in SF, according to Crunchbase.

“I used to believe really strongly if you wanted to build a multi-billion dollar company you had to be based here,” Tavel said. “I’ve stopped giving that soap speech.”

Aileen Lee (Cowboy Ventures), Megan Quinn (Spark Capital), and Sarah Tavel (Benchmark Capital) on whether or not Silicon Valley is on the wane for investors #TCDisrupt pic.twitter.com/SOpn7p0eNQ

— TechCrunch (@TechCrunch) September 5, 2018

Underestimated talent

A lot of Bay Area VCs have been blind to the droves of tech talent located outside the region. Believe it or not, there are great engineers in America’s small- and medium-sized markets too.

At Disrupt, Backstage Capital founder Arlan Hamilton announced the firm would launch an accelerator to further amplify companies led by underestimated founders. The program will have cohorts based in four cities; San Francisco was noticeably absent from that list.

Instead, the firm, which invests in underrepresented founders and recently raised a $36 million fund, will work with companies in Philadelphia, Los Angeles, London and one more city, which will be determined by a public vote. Aniyia Williams, the founder of Tinsel and Black & Brown Founders, will spearhead the Philadelphia effort.

“For us, it’s about closing that wealth gap to address inequity in tech,” Williams said. “There needs to be more active participation from everyone.”

Hamilton added that for her, the tech talent in LA and London is undeniable.

“There is a lot of money and a lot of investors … it reminds me of three years ago in Silicon Valley,” Hamilton said.

Silicon Valley vs. China

Silicon Valley’s demise may not be just as a result of increased costs of living or investors overlooking talent in other geographies. It may be because of heightened competition abroad.

Doug Leone, an early- and growth-stage investor at Sequoia Capital, said at Disrupt that he’s noticed a very different work ethic in China.

Chinese entrepreneurs, he explained, are more ruthless than their American counterparts and they’re putting in a whole lot more hours.

Doug Leone of Sequoia Capital says founders in the US and China both want to change the world, but Chinese founders are a little more desperate (and you see it in the crazy work ethic they have).#TCDisrupt pic.twitter.com/dPxsRTbJoq

— TechCrunch (@TechCrunch) September 6, 2018

“I’ve had dinner in China until after 10 p.m. and people go to work after 10 p.m.,” Leone recalled.

“We don’t see that in the U.S. I’m not saying the U.S. founders oughta do that but those are the differences. They are similar in character. They are similar in dreams. They are similar in how they want to change the world. They are ultra-driven … The Chinese founders have a half other gear because I think they are a little more desperate.”

Much of this, however, has been said before and still, somehow, Silicon Valley remained the place to be for investors and startup entrepreneurs.

The reality is, those engaged in tech culture are always anxiously awaiting for the bubble to pop, the market to crash and for “peak Valley” to finally arrive.

Maybe, just maybe, Silicon Valley is forever.

Here’s more of our coverage of Disrupt 2018.

Powered by WPeMatico

Eventbrite is having one hell of a debut on the New York Stock Exchange this morning.

Shares of the ticketing startup, founded back in 2006, have shot up over 50 percent in trading on the NYSE. After pricing its shares at $23 in its initial offering, investors have bid up the stock to a whopping $37, putting the company’s valuation at nearly $3 billion.

$EB prices $23, opens $36 pic.twitter.com/cYgCuqbmh8

—

(@hunterwalk) September 20, 2018

That’s well above where the ticketing company had hoped to be when it initially set terms for the public offering earlier this month.

The company started trading priced above its share price and nearly doubled its valuation. And if Eventbrite can do it, really almost any later-stage startup should be thinking about the public markets right now.

Performance for the San Francisco ticketing company has been… somewhat lackluster. As we noted when wrote about the company’s offering:

Eventbrite is not profitable and has been losing money since 2016. According to the documents, it posted losses of $40.4 million in 2016 and $38.5 million in 2017. In the first six months of 2018, the company has posted a net loss of $15.6 million. The company is making changes to make up for some of those losses — at the end of August, it announced a new pricing scheme for its customers using the “Essentials” package.

Its revenue is rising though, increasing from $133 million in 2016 to $201 million last year.

Since the beginning of the year tech public offerings have been on a tear. As The Wall Street Journal noted in July, 120 companies had raised $35.2 billion on U.S. exchanges at that point — the best showing for public markets since 2014 and the fourth busiest year since 1995, according to the financial data and analysis service Dealogic.

We’ve noted before that it’s a bit mind-boggling that investors and their portfolio companies wouldn’t be taking more advantage of these heady times. Nothing lasts forever (not even cold November rain) and certainly not markets that have been this bullish for this long.

Some of the reasoning is likely thanks to a market that’s still awash in private equity, sovereign wealth and late-stage dollars. SoftBank has hundreds of billions to invest; private equity firms are beginning to look at growth-stage companies the way that I look at banana cream pies from Cassell’s; and venture firms are beefing up big time to keep up with the Joneses (or in this case, the Blackstoneses).

However, the fun is certainly going to come to an end, and likely sooner rather than later. Early-stage investors are beginning to dole out their advice on lowering cash burn (something that happens every time they see the beginning of the end of the beginning of the end).

Low burn rates have gone out of fashion, but I expect we’ll be reminded very quickly at the beginning of the next downturn why they’re so valuable for early-stage startups.

— Sam Altman (@sama) September 19, 2018

With that in mind, later-stage companies should be looking for the exit signs wherever they can find them. Right now, that’s an IPO window that seems to be wide open.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

After a long run of having guests climb aboard each week, we took a pause on that front, bringing together three of our regular hosts instead: Connie Loizos, Danny Chrichton, and myself.

Despite the fact that there were just three of us instead of the usual four, we got through a mountain of stuff. Which was good as it was a surprisingly busy week, and we didn’t want to leave too much behind.

Up top we dug into the latest in the land of crypto, which Danny had politely summarized for us in an article. The gist of his argument is that the analogies relating crypto as an industry to the Internet may work, but most people have their timelines wrong: Crypto isn’t like the Internet in the 90s, perhaps. More like the 80s.

On the same topic, crypto companies formed a team lobbying effort, and a high-flying crypto fund is struggling to once again post strong profit figures.

Moving along, Juul is back in the news. Not, however, for raising more money or posting quick growth. Well, sort of the latter, as the government is after it. The Food and Drug Administration has put Juul on a countdown to get its act together regarding teens and smoking. That the financially impressive unicorn is in as much trouble as it is, is nearly surprising.

Finally, we ran through the three most recent Chinese IPOs that hit our radar. Here they are:

And that was the end of things. Thanks for sticking with us, as always. Speaking of which, our 100th episode is coming up. Who should we bring onto the show to celebrate?

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

The dream of a startup founder can often be summarized by the following well-intentioned, and mostly delusional, quote: “We’ll raise a few rounds and in a few years we’ll IPO on Nasdaq.”

But a more likely scenario looks something like this:

You invest a few years of hard work to build something of value. One day you receive an acquisition offer out of the blue. You’re elated. And you’re not prepared. You drop everything to focus on this opportunity. Exclusive due diligence starts. Your company is a mess (IP, contracts, burn). Days become weeks; weeks become months. You’ve neglected business and fundraising. You’re running out of money. M&A is now your one and only option. The buyer says they found a bunch of cockroaches in the walls and drops the price. Now what?

Sound unlikely?

This is still a favorable situation: You had an offer! Think about how much time you invested in your various funding rounds. The hundreds of names and Google spreadsheet or Streak-powered quasi-CRM process.

Have you spent even a fraction of that on understanding exit paths? If you’d rather not live the situation described above, read along.

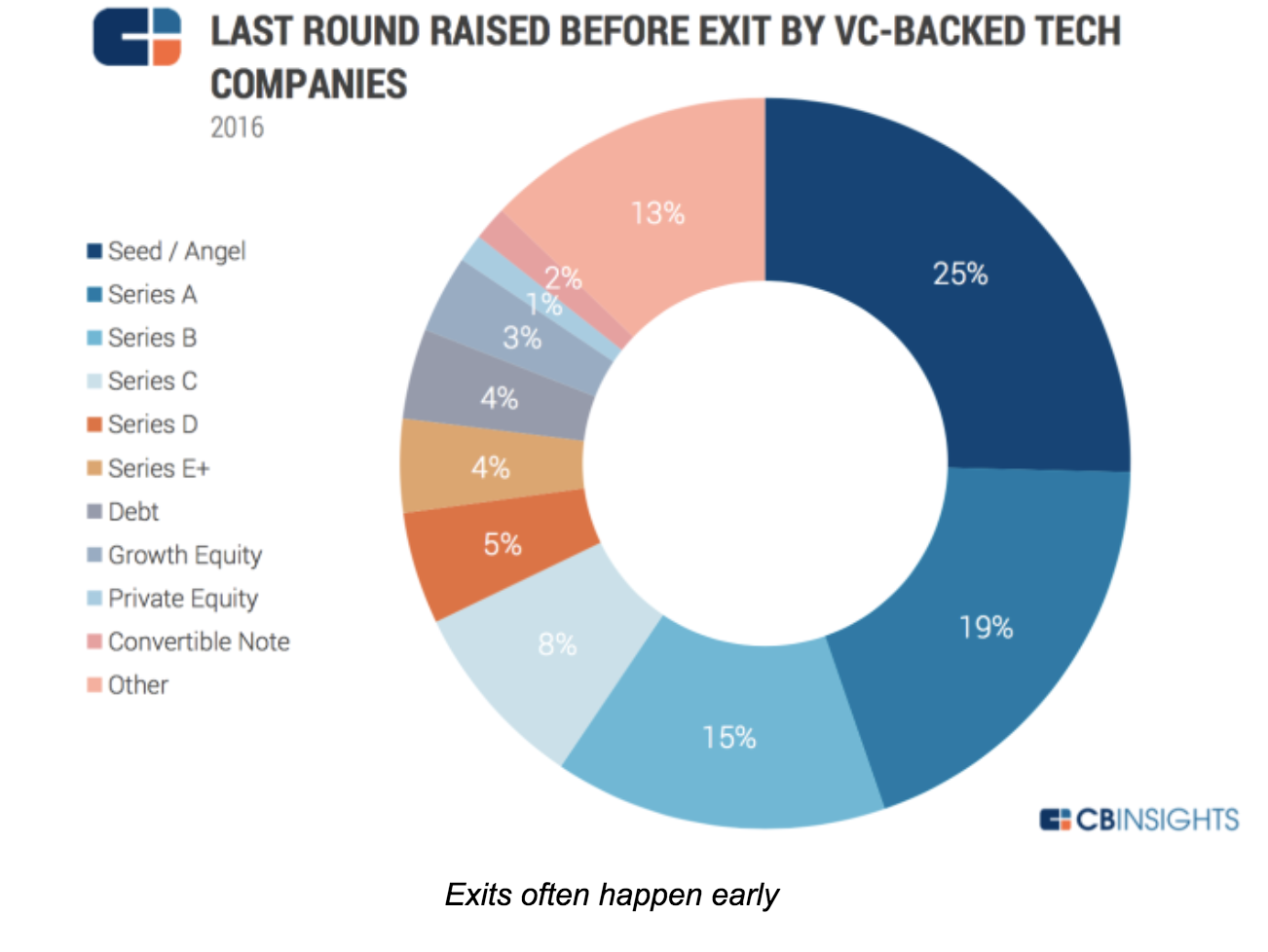

Investors live by exits, but many founders keep dreaming of unicornization and avoid the “E-word” until it’s too late. Yet, in 2016, 97 percent of exits were M&As. And most happened before Series B.

Exits matter because that’s when you, your team and your investors get paid. Oddly enough, and to use a chess metaphor, we hear a lot about the “opening game” (lean startup) and the “mid-game” (growth), but very little about this “end game.”

As a result, founders miss opportunities or leave money on the table. This is a shame. Our fund has more than 700 companies in portfolio. We want the best possible exit for each of them. And fortune favors the prepared! Now, how to get 700 exits (and counting)?

To explore the topic, we organized a series of Master Classes tapping corporate buyers, bankers, investors, lawyers and startup CEOs with M&A or IPO experience in San Francisco. It was a group that included the founders of Guitar Hero — bought by Activision; JUMP Bikes — a SOSV portfolio company bought by Uber, Ubiquisys — bought by Cisco and Withings — bought by Nokia. Each one for hundreds of millions.

Their observations can be summarized below.

“Founders must be aware of what contributes to an exit. This means understanding partnerships and how they are formed in the business space the entrepreneur is working in,” said one Master Class participant.

As founders, you build your product, your company and… optionality. You need to understand the options open to your company, and take steps to enable them.

The most likely one is an acquisition, but there are others like IPO (including small cap), RTO, SBO, LBO, Equity Crowdfunding and even ICO.

“Exit is not a goal per se, but as a CEO it is something you should think about as early in your cycle as possible, while being business-focused,” said the London-based investor Frederic Rombaut, of Seraphim Capital.

Indeed, most participants said that exits should always be on the chief executive’s agenda, no matter how early in the process. “Exits should be on the CEO agenda. Not front and center, but on the agenda. M&A is a by-product of a great business and targeted BD. IPOs are always an option once you’ve built significant cashflow forecasting.”

It’s important to ask questions like: How many “strategic engagements” with potential buyers have you had this month? Is your message and value clear in their eyes? Have you considered an acquisition track in parallel to a fundraise?

It doesn’t stop there:

One thing is sure: The time to exit is not when you’re running out of money.

Unicorn or not, the most likely exit is an acquisition.

As George Patterson, managing director at HSBC in New York said, “Good tech companies are bought, not sold. The question is thus: how to get bought?”

Patterson says it’s important to understand how mergers and acquisitions actually work; how to prepare a startup for an exit; and how to develop a “feel” for the market you’re exiting through and into.

Hearing from corp dev veterans from Cisco, Logitech, Dassault and IBM, a few key ideas emerged:

Motivations vary

It could be from least to most expensive, or as a mix, as listed by Mark Suster, managing partner at Upfront Ventures:

How corporates find you

Corporates find deals via the development of partnerships, investment (CVC), their business units, corp dev research, media and investor connections.

Asked about the best approach, Todd Neville, manager of Corporate Business Development and Strategy at IBM (who gave the most detailed description of the corp dev process), said, “Do something cool to one of the IBM customers. If they rave about even a POC, we’re interested.”

In other words, business development is corporate development.

Get the house in order

Buyers typically want to know three things:

For IP, they will check your contracts (staff and contractors), and run some automated code analysis for proprietary code and open source use. They will evaluate potential IP infringement. No point buying you if you end up costing more in lawsuits!

For your team skills: Sitting down with your engineers will tell them plenty enough without understanding the details of this or that algorithm. The last thing a corporate wants is to be accused of stealing!

Lawyers engaged early can help. The later the clean-up, the more costly and painful.

Develop a feel for your “market”

Develop relationships and create champions within corporates. It will help promote your deal when the time comes, and will let you keep your finger on the pulse of corporate strategy to time your moves.

Do you read the earning calls of Cisco or IBM (or others relevant to you)? This is where strategies are presented. Are your keywords coming up there or in their press releases?

Chris Gilbert, former CEO of Ubiquisys (sold to Cisco for more than $300 million) was very deliberate in planning his exit.

“Selling starts on day one and is a leadership-only function — work out who will be your buyer. Only the CEO can do this. Constantly articulate why a company should buy you,” Gilbert said. Bring clear messages into the acquiring company so it can be presented upwards: give them the presentation you would like them to show their boss! When the time is right, force decisions through competition. If you know they have to buy you, your starting position is strong.”

The dark art of price discovery

There are dozens of formulas (from DCF to comparables) to evaluate a deal — which also means none is “correct.” What matters is: How much would you sell for, and how much is the buyer ready to pay?

Gilbert, at Ubiquisys, described how close interactions with his banker helped drive the price up among the bidders assembled.

Just like buyers, we meet bankers and lawyers too rarely at startup events, but there is much to learn with them. They make deals happen, avoid value erosion and optimize price. They often also make introductions before you engage them, to build goodwill and earn your business.

And if you worry about fees, the right banker handsomely pays for itself by finding more bidders and playing “bad cop” for you, avoiding direct confrontation with your future employer. Do you want a slice of the watermelon or the whole grape?

When asked about what happens after an M&A or IPO, buyers said they generally hoped the founders would stay with them for many years. Often using re-vesting, earn-outs or shares of the acquiring company to incentivize them. Neville, from IBM, mentioned a security company they acquired whose founder is now the head of one of the largest IBM divisions.

In the case of IPOs, supposedly the ultimate “exit,” any block of shares sold by founders would face extreme scrutiny and might cause a price drop.

So who’s exiting during those deals? Investors (and not always).

Eventually, if the average age of a startup at exit is 8-10 years, the active duty period of founders (if not replaced in the meantime) extends even more. Better love the problem you’re solving, and your customers!

Thanks to speakers, participants and supporters of this Master Class series:

London: Frederic Rombaut (Seraphim Capital), Joe Tabberer (FirstBank), Chris Gilbert (Ubiquisys), Jonathan Keeling (Crowdcube), Fred Destin, Tony Fish (AMF Ventures, James Clark (London Stock Exchange), Denise Law (SGCIB).

Paris: Frederic Rombaut (Seraphim Capital), Manuel Gruson (Dassault Systemes), Pierre-Henri Chappaz (Rothschild Global Advisory), Christine Lambert-Goue (All Invest), Olivier Younes (EXPEN), Eric Carreel (Withings), Fabien Bardinet (Balyo), Xavier Lazarus (Elaia Partners), Pierre-Eric Leibovici(Daphni). Jean de La Rochebrochard (Kima Ventures), Jeremy Sartre (SmartAngels), Gwen Regina Tan (Entrepreneur First).

San Francisco: Natasha Ligai (Logitech), Matt Cutler (Cisco),Will Hawthorne, (CODE Advisors), Ryan Rzepecki (JUMP Bikes), Charles Huang (Guitar Hero), Jeff Thomas (Nasdaq), Shahin Farshchi (Lux Capital), Ammar Hanafi (Moment Ventures), Adam J. Epstein (Third Creek Advisors), Nathan Harding (EKSO Bionics), Kate Whitcomb, Anthony Marino and Ethan Haigh (SOSV).

New York: Todd Neville (IBM), George Patterson (HSBC), Ryan Rzepecki (JUMP Bikes), Aaron Kellner (SeedInvest), Jeremy Levine (Bessemer Venture Partners), Taylor Greene (Collaborative Fund), Adam Rothenberg (BoxGroup), Eli Curi (Fenwick & West), Ian Engstrand and Salil Gandhi (Goodwin), Warren Spar(Sparring Partners Capital), Duncan Turner, Vivian Law and Sheng Ge (SOSV).

Powered by WPeMatico

CEOs of funded startups tend to be a well-educated bunch, at least when it comes to university degrees.

Yes, it’s true college dropouts like Mark Zuckerberg and Bill Gates can still do well. But Crunchbase data shows that most startup chief executives have an advanced degree, commonly from a well-known and prestigious university.

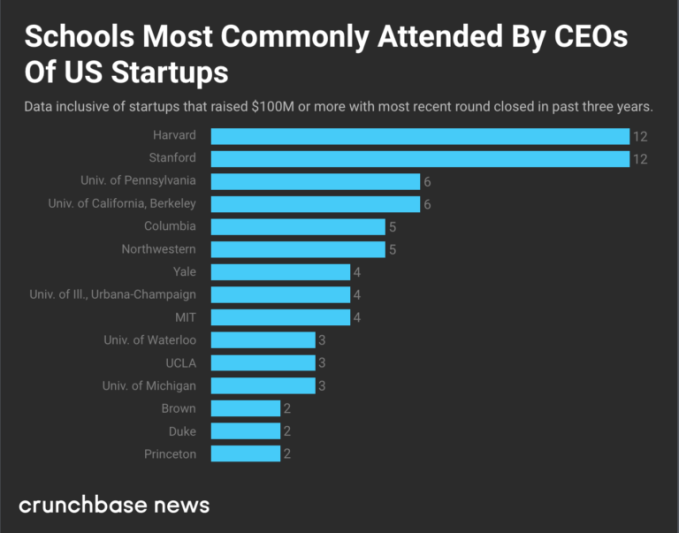

Earlier this month, Crunchbase News looked at U.S. universities with strong track records for graduating future CEOs of funded companies. This unearthed some findings that, while interesting, were not especially surprising. Stanford and Harvard topped the list, and graduates of top-ranked business schools were particularly well-represented.

In this next installment of our CEO series, we narrowed the data set. Specifically, we looked at CEOs of U.S. companies funded in the past three years that have raised at least $100 million in total venture financing. Our intent was to see whether educational backgrounds of unicorn and near-unicorn leaders differ markedly from the broad startup CEO population.

Here’s the broad takeaway of our analysis: Most CEOs of well-funded startups do have degrees from prestigious universities, and there are a lot of Harvard and Stanford grads. However, chief executives of the companies in our current data set are, educationally speaking, a pretty diverse bunch with degrees from multiple continents and all regions of the U.S.

In total, our data set includes 193 private U.S. companies that raised $100 million or more and closed a VC round in the past three years. In the chart below, we look at the universities most commonly attended by their CEOs:1

The rankings aren’t hugely different from the broader population of funded U.S. startups. In that data set, we also found Harvard and Stanford vying for the top slots, followed mostly by Ivy League schools and major research universities.

For heavily funded startups, we also found a high proportion of business school degrees. All of the University of Pennsylvania alum on the list attended its Wharton School of Business. More than half of Harvard-affiliated grads attended its business school. MBAs were a popular credential among other schools on the list that offer the degree.

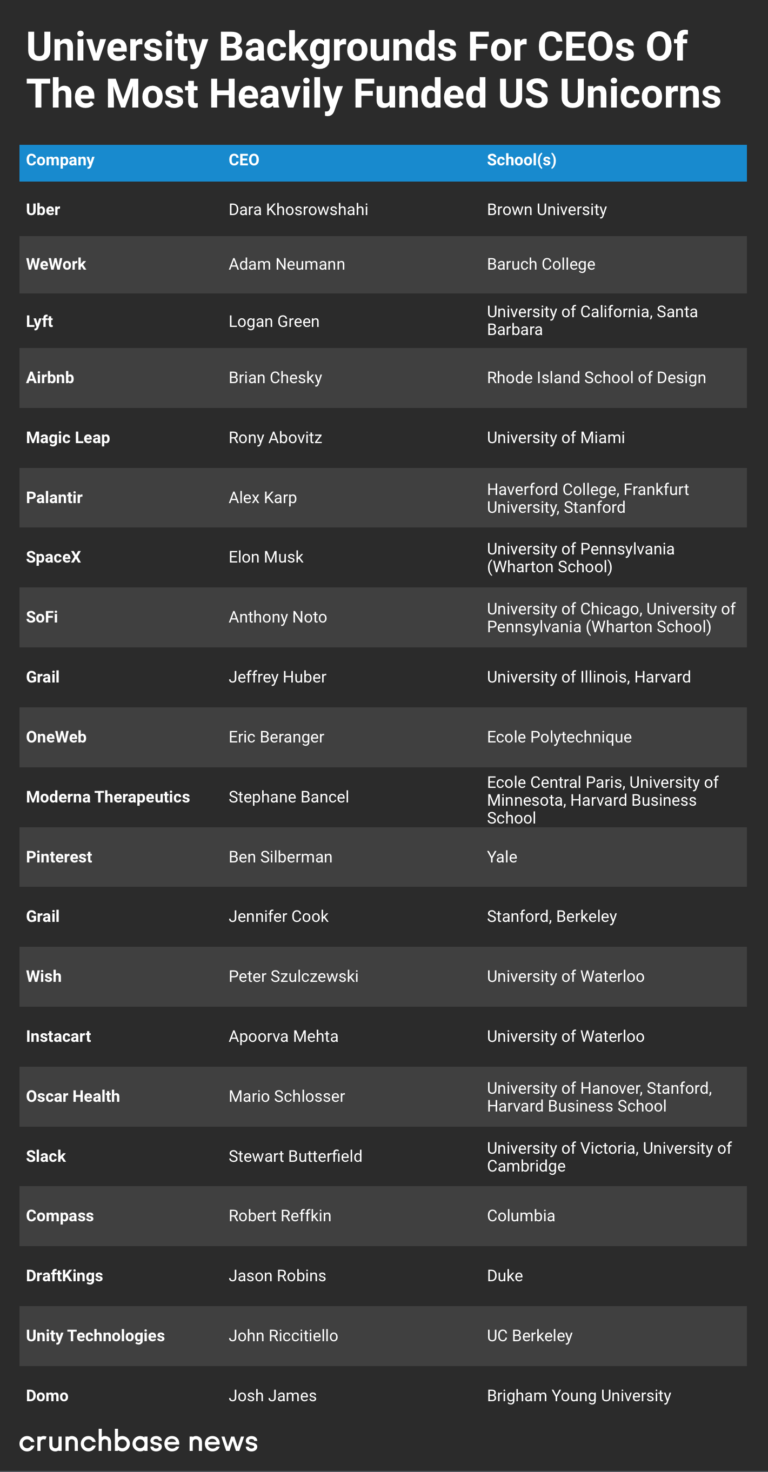

When it comes to the most heavily funded startups, the degree mix gets quirkier. That makes sense, given that we looked at just 20 companies.

In the chart below, we look at alumni affiliations for CEOs of these companies, all of which have raised hundreds of millions or billions in venture and growth financing:

One surprise finding from the U.S. startup data set was the prevalence of Canadian university grads. Three CEOs on the list are alums of the University of Waterloo . Others attended multiple well-known universities. The list also offers fresh proof that it’s not necessary to graduate from college to raise billions. WeWork CEO Adam Neumann just finished his degree last year, 15 years after he started. That didn’t stop the co-working giant from securing more than $7 billion in venture and growth financing.

Powered by WPeMatico

Why has San Francisco’s startup scene generated so many hugely valuable companies over the past decade?

That’s the question we asked over the past few weeks while analyzing San Francisco startup funding, exit, and unicorn creation data. After all, it’s not as if founders of Uber, Airbnb, Lyft, Dropbox and Twitter had to get office space within a couple of miles of each other.

We hadn’t thought our data-centric approach would yield a clear recipe for success. San Francisco private and newly public unicorns are a diverse bunch, numbering more than 30, in areas ranging from ridesharing to online lending. Surely the path to billion-plus valuations would be equally varied.

But surprisingly, many of their secrets to success seem formulaic. The most valuable San Francisco companies to arise in the era of the smartphone have a number of shared traits, including a willingness and ability to post massive, sustained losses; high-powered investors; and a preponderance of easy-to-explain business models.

No, it’s not a recipe that’s likely replicable without talent, drive, connections and timing. But if you’ve got those ingredients, following the principles below might provide a good shot at unicorn status.

First, lose money until you’ve left your rivals in the dust. This is the most important rule. It is the collective glue that holds the narratives of San Francisco startup success stories together. And while companies in other places have thrived with the same practice, arguably San Franciscans do it best.

It’s no secret that a majority of the most valuable internet and technology companies citywide lose gobs of money or post tiny profits relative to valuations. Uber, called the world’s most valuable startup, reportedly lost $4.5 billion last year. Dropbox lost more than $100 million after losing more than $200 million the year before and more than $300 million the year before that. Even Airbnb, whose model of taking a share of homestay revenues sounds like an easy recipe for returns, took nine years to post its first annual profit.

Not making money can be the ultimate competitive advantage, if you can afford it.

Industry stalwarts lose money, too. Salesforce, with a market cap of $88 billion, has posted losses for the vast majority of its operating history. Square, valued at nearly $20 billion, has never been profitable on a GAAP basis. DocuSign, the 15-year-old newly public company that dominates the e-signature space, lost more than $50 million in its last fiscal year (and more than $100 million in each of the two preceding years). Of course, these companies, like their unicorn brethren, invest heavily in growing revenues, attracting investors who value this approach.

We could go on. But the basic takeaway is this: Losing money is not a bug. It’s a feature. One might even argue that entrepreneurs in metro areas with a more fiscally restrained investment culture are missing out.

What’s also noteworthy is the propensity of so many city startups to wreak havoc on existing, profitable industries without generating big profits themselves. Craigslist, a San Francisco nonprofit, may have started the trend in the 1990s by blowing up the newspaper classified business. Today, Uber and Lyft have decimated the value of taxi medallions.

Not making money can be the ultimate competitive advantage, if you can afford it, as it prevents others from entering the space or catching up as your startup gobbles up greater and greater market share. Then, when rivals are out of the picture, it’s possible to raise prices and start focusing on operating in the black.

You can’t lose money on your own. And you can’t lose any old money, either. To succeed as a San Francisco unicorn, it helps to lose money provided by one of a short list of prestigious investors who have previously backed valuable, unprofitable Northern California startups.

It’s not a mysterious list. Most of the names are well-known venture and seed investors who’ve been actively investing in local startups for many years and commonly feature on rankings like the Midas List. We’ve put together a few names here.

You might wonder why it’s so much better to lose money provided by Sequoia Capital than, say, a lower-profile but still wealthy investor. We could speculate that the following factors are at play: a firm’s reputation for selecting winning startups, a willingness of later investors to follow these VCs at higher valuations and these firms’ skill in shepherding portfolio companies through rapid growth cycles to an eventual exit.

Whatever the exact connection, the data speaks for itself. The vast majority of San Francisco’s most valuable private and recently public internet and technology companies have backing from investors on the short list, commonly beginning with early-stage rounds.

Generally speaking, you don’t need to know a lot about semiconductor technology or networking infrastructure to explain what a high-valuation San Francisco company does. Instead, it’s more along the lines of: “They have an app for getting rides from strangers,” or “They have an app for renting rooms in your house to strangers.” It may sound strange at first, but pretty soon it’s something everyone seems to be doing.

It’s not a recipe that’s likely replicable without talent, drive, connections and timing.

A list of 32 San Francisco-based unicorns and near-unicorns is populated mostly with companies that have widely understood brands, including Pinterest, Instacart and Slack, along with Uber, Lyft and Airbnb. While there are some lesser-known enterprise software names, they’re not among the largest investment recipients.

Part of the consumer-facing, high brand recognition qualities of San Francisco startups may be tied to the decision to locate in an urban center. If you were planning to manufacture semiconductor components, for instance, you would probably set up headquarters in a less space-constrained suburban setting.

While it can be frustrating to watch a company lurch from quarter to quarter without a profit in sight, there is ample evidence the approach can be wildly successful over time.

Seattle’s Amazon is probably the poster child for this strategy. Jeff Bezos, recently declared the world’s richest man, led the company for more than a decade before reporting the first annual profit.

These days, San Francisco seems to be ground central for this company-building technique. While it’s certainly not necessary to locate here, it does seem to be the single urban location most closely associated with massively scalable, money-losing consumer-facing startups.

Perhaps it’s just one of those things that after a while becomes status quo. If you want to be a movie star, you go to Hollywood. And if you want to make it on Wall Street, you go to Wall Street. Likewise, if you want to make it by launching an industry-altering business with a good shot at a multi-billion-dollar valuation, all while losing eye-popping sums of money, then you go to San Francisco.

Powered by WPeMatico

Elliott Management, an investment firm long known for its activist streak, set it sights on Commvault today, purchasing a 10.3 percent stake and nominating four Elliott-friendly members to the company’s board of directors. It likely means that Elliott is ready to push the company to change direction and cut costs, if it sticks to its regular MO.

As an older public company founded in 1988 with a strong product, but weak stock performance, Commvault represents just the kind of company Elliott tends to target. In its letter outlining why it acquired its stake in Commvault, it presented a stark picture of a company in decline.

As just one small example, Elliott discussed the stock performance and it didn’t pull punches or mince words when it stated:

“Commvault’s strategy, operations, execution and leadership over the past eight years have failed to generate returns to shareholders, despite a leadership position in a growing market with a product set that customers like and competitors respect. Commvault’s underperformance has been so profound that an investor would have been better off buying the NASDAQ index instead of Commvault’s stock on 99% of trading days in the last eight years. …”

Ouch.

As it is wont to do, Elliott buys a stake and then forces its way onto the board of directors and this deal is no different where it will be adding 4 members:

“Given the long-term issues at the Company, we believe the Board would benefit from fresh perspectives, primarily in the area of operational execution, software go-to-market experience and current technology expertise. The level of required change at the Company is significant and requires a Board with new and relevant experiences to guide the Company’s turnaround. We have been involved in dozens of similar situations and have worked constructively with many companies to add top-tier, C-suite executives and experienced Board members to these companies. For Commvault, we are submitting a group of highly qualified director nominees with what we believe is the right experience to help guide the Company on its path forward.”

As some examples of that past experience it alluded to in the letter, Elliott bought a stake in EMC in 2014 and began to pressure the Board to sell its stake in VMware. The company turned back the attempt and eventually sold out to Dell for $67 billion, still giving Elliott a nice return on its one percent investment in the company, no doubt.

More recently, it bought a 6.5 percent stake in Akamai in December. At the next earnings call in February, the company announced it was laying off 400 employees, which accounted for almost 5 percent of the worldwide workforce. The layoffs are consistent with cost cutting that tends to happen when Elliott buys a stake in a company.

What happens next for Commvault is difficult to say, but investors obviously think there is going to be some movement as the stock is up over 11 percent as of this writing. Chances are they are onto something, and given Elliott’s track record they are probably right.

Powered by WPeMatico