Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

The American Midwest has a long history of making stuff. During the 20th century, it was the manufacturing center for the nation, and indeed much of the world. It’s still where a surpassing majority of agricultural commodities are grown and processed. But is it also a major producer of technology startups? Maybe not as much as the coasts, but the Midwest’s bustling metropoli and vast expanses of rural land prove to be fertile ground for quite a bit of startup activity.

And that’s what we’re going to take a look at here. In a similar vein to our recent analysis of startup fundraising in the South, we’ll break down the region into its constituent parts, assessing deal and dollar volume trends in the Midwest’s two primary sub-regions, some of its individual states and the most active metropolitan areas in the U.S.’s midsection.

And, to be clear, this is not Crunchbase News’s first foray into the region. We’ve covered the region’s seed-stage interest in AI and hard tech, a few notable rounds and have always included the Midwest in all manner of data-spelunking expeditions. And to this, we’ll add a deep dive into the numbers.

Borders and boundaries are a deep well of disputes. To preempt debate, we use the U.S. Census Bureau’s definition of the Midwest region which, unlike its definition of the South, shouldn’t be too controversial. If you have something against Kansas or Ohio being included in this group, take it up with the Feds.

The good folks at the Census Bureau split the Midwest into two distinct — and rather unimaginatively named — sub-regions: the West North Central and East North Central states, which are separated by the Mississippi River. We’ve included the map below.

By splitting the Midwest into two distinct parts, we’ll be able to see where most of the startup and funding activity is concentrated. Spoiler alert: The farther west you go, the startup population (and the population itself) grows more scattered.

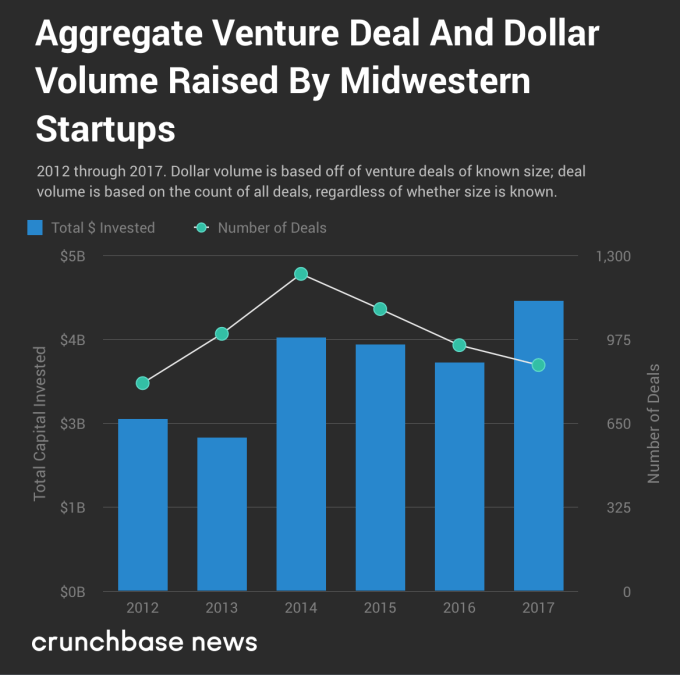

Based only on reported data in Crunchbase, the Midwest appears to be affected by the same phenomenon as the rest of the country. Crunchbase News has previously found that the number of seed and early-stage deals has gone off a cliff in the U.S., resulting in a top-heavy market featuring many large, late-stage deals. And this wouldn’t be a problem if it weren’t for a shortfall in new startups to fill the next cycle of early-stage funding. The “hollowing out” of the Midwestern venture deal pipeline becomes readily apparent when you look at funding data for the past several years, which you can find in the chart below.

To wit, deal volume is down markedly since 2014, as Crunchbase News reported in its Q4 2017 report of startup funding activity in the U.S. and Canada. But somewhat counterintuitively, the amount of money being invested into startups is on the rise in the Midwest and throughout many other parts of the country, reaching fresh multi-year highs in 2017. Almost one full quarter into 2018, the trend appears to continue unabated.

But this chart abstracts away a lot of nuance, so let’s take a closer look at the region and its states.

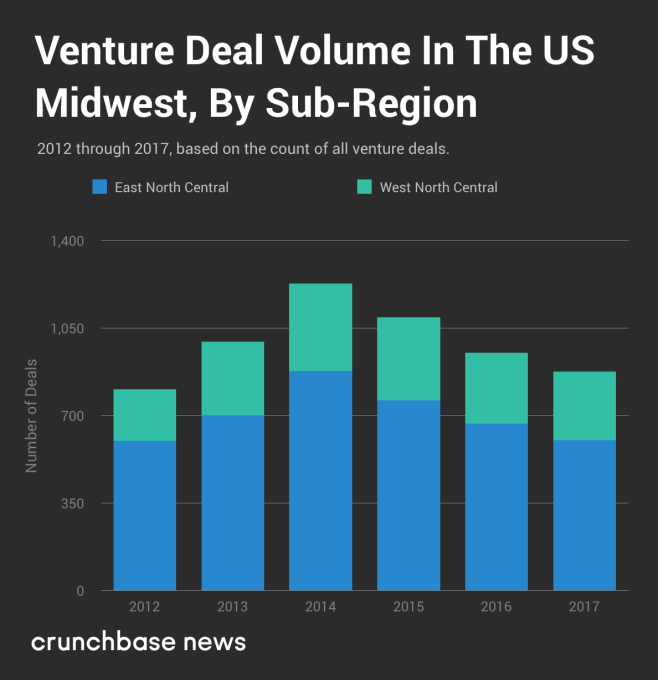

We’ll start first with deal volume, because that’s a fairly decent indicator of a geographic region’s level of startup activity. Below, we’ve plotted venture deal volume, divided by sub-region.

Again, based on the reported data from Crunchbase, we found that deal counts have been on a downward trend for several years. And though some of this may be attributable to reporting delays, projected deal volume data for the whole of the U.S. and Canada (fourth chart down in the Q4 quarterly report) shows a years’-long downtrend. There’s no reason to believe that startup activity in the Midwest is materially different from the rest of the U.S. and Canada.

But what about the relative “balance of power” between the two sub-regions? At least when it comes to deal volume, has one sub-region waxed while the other waned? To a limited extent, the answer is yes. Between 2012 and 2017, the percentage share of all Midwestern dealflow going to West North Central states like the Dakotas, Minnesota and Missouri has grown from 25.4 percent to 31.2 percent, up by nearly one-fifth in relative terms.

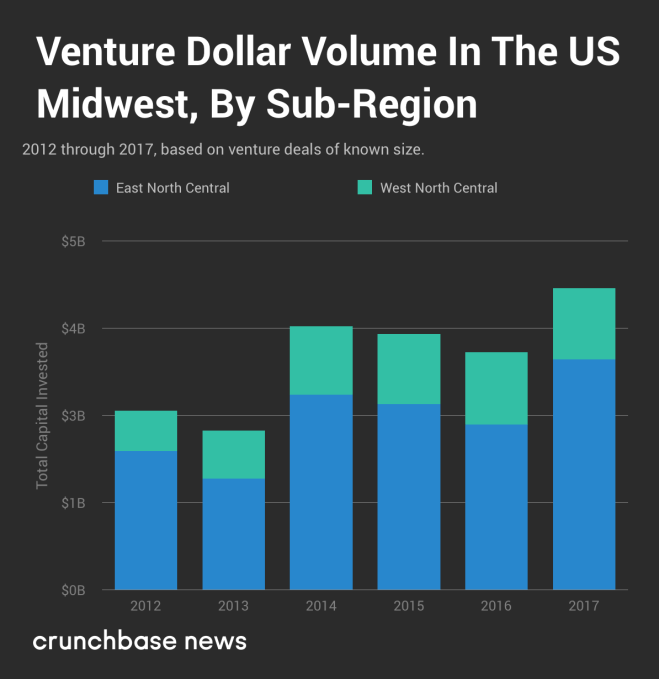

Now let’s check out dollar volume. The chart below displays aggregate reported venture capital dollar volume raised by startups in the Midwest.

As far as the amount of money Midwestern startups have raised over time, the trendline is generally up and to the right. But that’s not the only way this differs from the deal volume data we looked at earlier. For dollar volume, there appears to be no appreciable change in the “balance of power” between the two sub-regions since 2012. Depending on the year, East North Central states like Illinois, Michigan and Ohio raked in between 70 and 78 percent of total dollar volume, but that variance doesn’t appear in an orderly trend.

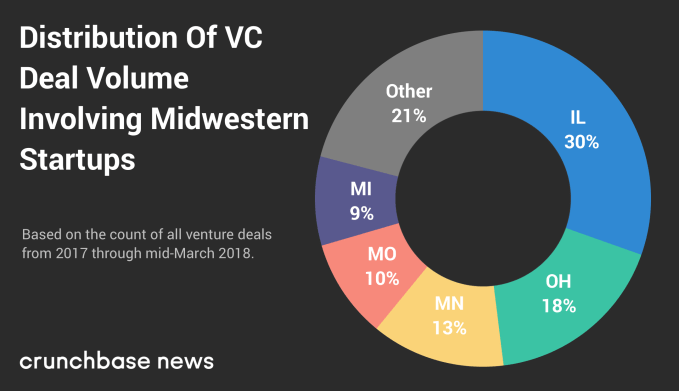

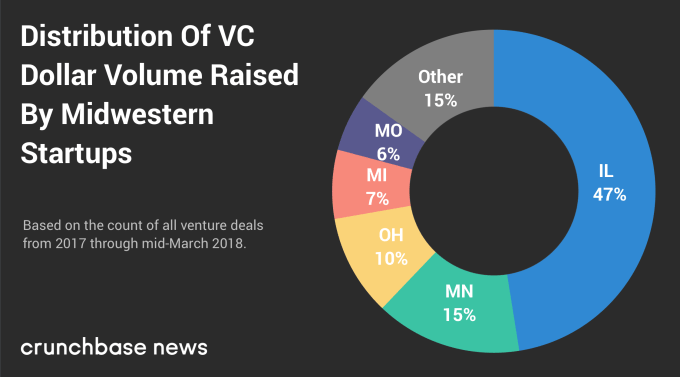

We started first at the regional level, then compared smaller groupings of states. Now, let’s see how deal and dollar volume is distributed on a state-by-state level. Doing so will point to the states that lead the region in venture-backed startup activity. Below, you’ll find a chart of how deal volume is split between the top five Midwestern states.

And here is how dollar volume is distributed.

As we saw with our analysis of the South, the top five Midwestern states for deal volume are the same five top-ranked states for dollar volume. But there is some notable variation in how these states rank among each other and the amount of deal and dollar volume they account for.

Considering that Illinois is home to Chicago and a number of downstate universities with deep tech startup roots, the fact that it places first for both metrics shouldn’t come as much of a surprise.

What might be more of a head-scratcher is Minnesota, which ranks third in deal volume but second in dollar volume. Why does it switch places with Ohio? The answer could lie in the industrial mix which, in the case of Minnesota, includes a disproportionately high number of medical device and other life sciences companies, which typically take a lot of capital to get off the ground.

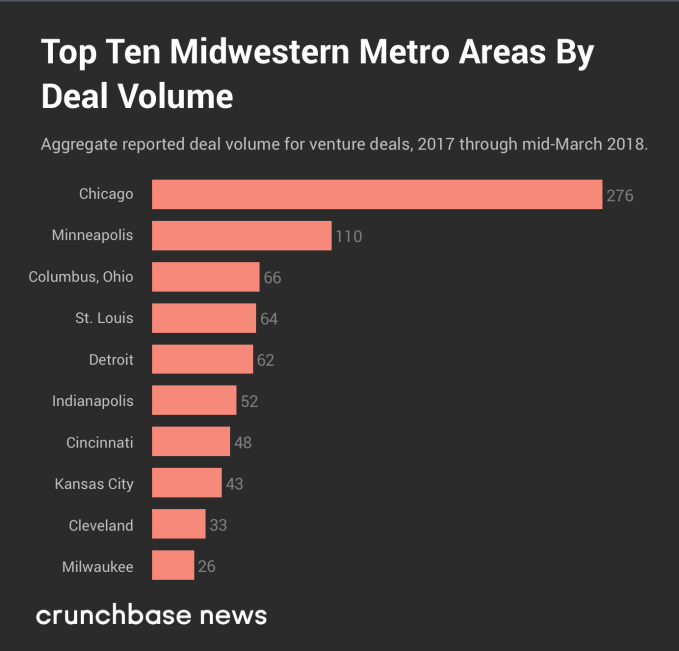

Longtime readers of Crunchbase News may remember a ranking of Midwestern startup cities we wrote back in August 2017. However, here we’re just focusing on deal and dollar volume over the past 15 months, since the start of 2017.

Let’s start first with the top 10 Midwestern cities as measured by number of startup funding rounds.

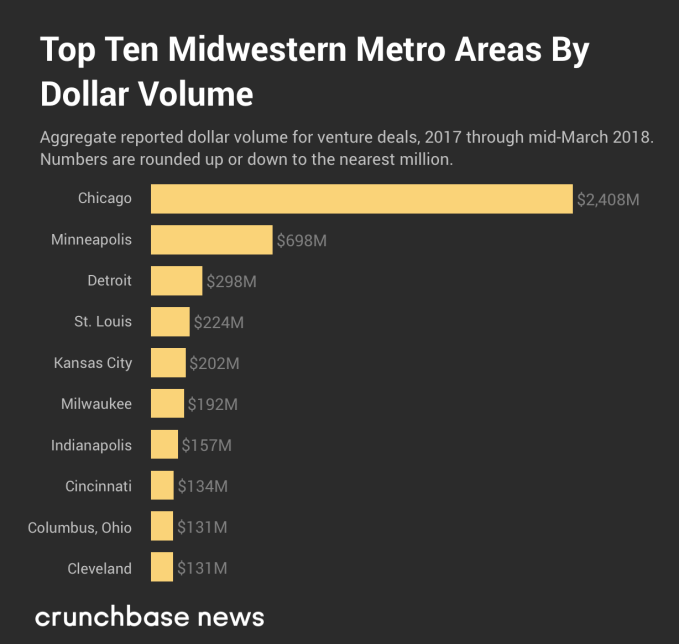

And in the chart below, you can see the top cities, as ranked by venture dollar volume, from the same period of time.

In both rankings, four of the top five cities are the same, but the odd one out appears to be Columbus, Ohio. Although there were a fairly large number of rounds raised by startups in that metro area, most of the rounds were fairly small by national standards. And one of the main reasons why Kansas City, Missouri jumped so much in the dollar volume rankings was a $100 million Series F round raised by C2FO.

But, again, as far as the Midwest goes, everything pales in comparison to Chicago alone.

For many, the Midwest is in a kind of Goldilocks zone. The East and West coasts seem to hold more or less equal sway over the culture and economy and most of its cities are neither too big nor too small. The only extreme it seems to occupy is its winter weather.

Powered by WPeMatico

Hip hop stars are taking their reputations to Wall Street and Sand Hill road.

Unlike their rock star brethren, who’ve historically been disinterested in dabbling with startups, quite a few hip hop artists have amassed good-sized portfolios. They’ve seen a few big hits too, most recently including a massive up round for zero-commission stock trading platform Robinhood, which counted Jay-Z, Nas and Snoop Dogg among its earlier backers.

But just how deep does the hip hop-startup relationship go and where is it headed? To shed some light on that question, we put together a review of Crunchbase data on the startup investment activity of famous musicians. We looked at both hip hop and pop stars, culling a list of 21 artists who are either active investors or have joined one or more rounds in recent years.

The general conclusion: Artists are doing more deals, raising more funds and backing more companies that graduate to up rounds and exits. Here are a few examples:

That’s not to say everything a star touches turns multi-platinum. We found quite a few flops in their portfolios and assembled a list here of 10 startups now shuttered that counted a hip hop or pop star among their backers.

Becoming and remaining famous requires many of the same skills and qualities as running an entrepreneurial venture, including an exceptional degree of tenacity.

Of course, flops are part of life for early-stage investors, so there’s no reason we’d expect celebrities to be an exception. Moreover, most of the now-shuttered companies were not heavily capitalized by venture standards.

However, there are some higher-profile or more heavily funded companies on the flop list. One is Washio, a laundry delivery service, which raised $17 million from Nas and 20 other investors before hanging itself out to dry in 2016. Another is Viddy, an app for shooting and sharing video clips backed by Roc Nation.

A number of venture pundits and pop culture mavens have previously pontificated why celebrities, and hip hop stars in particular, are drawn to startups.

One possibility is that rap music and startups resemble each other at the earliest stages, postulates Cam Houser, CEO of the 3 Day Startup Program. Rap music starts with a rapper and a producer. This duality, he says, is similar to the beginning stages of a startup, which commonly also brings together two people, a business and a technical co-founder.

Rap and startup entrepreneurship are also both longshot career tracks that celebrate raw ambition and unabashed self-promotion. To make it, however, both require an excellent grasp of what sells in the real world.

Branding is perhaps the most common rationale provided for the celebrity-startup connection. With their massive fan bases, swooning coverage and millions of social media followers, celebrities can certainly help get the word out about a new product or app. That said, the attention usually works only if said product also has compelling attributes of its own.

One of the less controversial explanations is that becoming and remaining famous requires many of the same skills and qualities as running an entrepreneurial venture, including an exceptional degree of tenacity.

It’s also true that in venture capital and the music business, it’s the hits that matter. It helps that we’re seeing plenty of those.

Powered by WPeMatico

It seems like startup news is full of overnight success stories and sudden failures, like the scooter rental company that went from zero to a $300 million valuation in months or the blood-testing unicorn that went from billions to nearly naught.

But what about those other companies that mature more gradually? Is there such a thing as slow and successful in startup-land?

To contemplate that question, Crunchbase News set out to assemble a data set of top late-blooming startups. We looked at companies that were founded in or before 2010 that raised large amounts of capital after 2015, and we also looked at companies founded a least five years ago that raised large early-stage funds in the last year. (For more details on the rules we used to select the companies, check “Data Methods” at the end of the post.)

The exercise was a counterpoint to a data set we did a couple of weeks ago, looking at characteristics of the fastest growing startups by capital raised. For that list, we found plenty of similarities between members, including a preponderance of companies in a few hot sectors, many famous founders and a lot of cancer drug developers.

For the late bloomers, however, patterns were harder to pinpoint. The breakdown wasn’t too different from venture-backed companies overall. Slower-growing companies could come from major venture hubs as well as cities with smaller startup ecosystems. They could be in biotech, medical devices, mobile gaming or even meditation.

What we did find, however, was an interesting and inspiring collection of stories for those of us who’ve been toiling away at something for a long time, with hopes still of striking it big.

Even youthful startups have been known to make a major pivot or two. So it’s not surprising to see a lot of pivots among late bloomers that have had more time to tinker with their business models.

One that fits this mold is Headspace, provider of a popular meditation app. The company, founded in 2010 by a British-born Buddhist monk with a degree in circus arts, started as a meditation-focused events startup. But it turned out people wanted to build on their learning on their own time, so Headspace put together some online lessons. Today, Santa Monica-based Headspace has millions of users and has raised $75 million in venture funding.

For late bloomers, the pivot can mean going from a model with limited scalability to one that can attract a much wider audience. That’s the case with Headspace, which would have been limited in its events business to those who could physically show up. Its online model, with instant, global reach, turns the business into something venture investors can line up behind.

They say if you wait long enough, everything comes back in style. That mantra usually works as an excuse for hoarding ’80s clothes in the attic. But it also can apply to entrepreneurial companies, which may have launched years before their industry evolved into something venture investors were competing to back.

Take Vacasa, the vacation rental management provider. The company has been around since 2009, but it began raising VC just a couple of years ago amid a broad expansion of its staff and property portfolio. The Portland-based company has raised more than $140 million to date, all of it after 2016, and most in a $103 million October round led by technology growth investor Riverwood Capital.

CloudCraze, which was acquired by Salesforce earlier this week, also took a long time to take venture funding. The Chicago-based provider of business-to-business e-commerce software launched in 2009, but closed its first VC round in 2015, according to Crunchbase records. Prior to the acquisition, the company raised about $30 million, with most of that coming in just a year ago.

Meanwhile, some late bloomers have always been fashionable, just not necessarily as VC-funded companies. Untuckit, a clothing retailer that specializes in button-down shirts that look good untucked, had been building up its business since 2011, but closed its first venture round, a Series A led by VC firm Kleiner Perkins, last June.

So yes, there is still capital available for those who wait. However, the truth of the matter is most companies that raise substantial sums of venture capital secure their initial seed rounds within a couple years of founding. Companies that chug along for five-plus years without a round and then scale up are comparatively rare.

That said, our data set, which looks at venture and seed funding, does not come close to capturing the full ecosystem of slow-growing startups. For one, many successful bootstrapped companies could raise venture funding but choose not to. And those who do eventually decide to take investment may look at other sources, like private equity, bank financing or even an IPO.

Additionally, the landscape is full of slow-growing startups that do make it, just not in a venture home run exit kind of way. Many stay local, thriving in the places they know best.

On the flip side, companies that wait a long time to take VC funding have also produced some really big exits.

Take Atlassian, the provider of workplace collaboration tools. Founded in 2002, the Australian company waited eight years to take its first VC financing, despite plentiful offers. It went public two years ago, and currently has a market valuation of nearly $14 billion.

The moral: Those who take it slow can still finish ahead.

Data methods

We primarily looked at companies founded in 2010 or earlier in the U.S. and Canada that raised a seed, Series A or Series B round sometime after the beginning of last year, and included some that first raised rounds in 2015 or later and went on to substantial fundraises. We also looked at companies founded in 2012 or earlier that raised a seed or Series A round after the beginning of last year and have raised $30 million or more to date. The list was culled further from there.

Powered by WPeMatico

In the world of mobile apps, numbers come in two sizes: big and bigger. More than one billion people use Facebook’s mobile app every day. But what about the financial side of the mobile business; specifically, venture investment and returns? By looking at the numbers behind two different ends of the startup life cycle, a reasonable understanding of the mobile market today can be had. Read More

In the world of mobile apps, numbers come in two sizes: big and bigger. More than one billion people use Facebook’s mobile app every day. But what about the financial side of the mobile business; specifically, venture investment and returns? By looking at the numbers behind two different ends of the startup life cycle, a reasonable understanding of the mobile market today can be had. Read More

Powered by WPeMatico

Scaleworks, a private equity firm based in San Antonio, Texas, apparently couldn’t wait until after the holidays to share the news of its latest purchase. The firm announced it was acquiring Keen IO in a Medium blog post yesterday. Terms of the deal were not disclosed, and neither company was available for comment beyond the blog post, but Keen has raised close to $30 million since it… Read More

Scaleworks, a private equity firm based in San Antonio, Texas, apparently couldn’t wait until after the holidays to share the news of its latest purchase. The firm announced it was acquiring Keen IO in a Medium blog post yesterday. Terms of the deal were not disclosed, and neither company was available for comment beyond the blog post, but Keen has raised close to $30 million since it… Read More

Powered by WPeMatico

For driverless car startups, raising capital seems to happen on autopilot. Investors and acquirers have put billions into the space over the past couple of years in the race for early-mover advantage. They’ve shown no desire to hit the brakes lately either, as indicated by a spate of recent deals. Read More

For driverless car startups, raising capital seems to happen on autopilot. Investors and acquirers have put billions into the space over the past couple of years in the race for early-mover advantage. They’ve shown no desire to hit the brakes lately either, as indicated by a spate of recent deals. Read More

Powered by WPeMatico

A year ago the Midwest seemed on the cusp of a renaissance. Small towns and cities from Pittsburgh to Omaha had perfected the YC model of accelerator creation and low-cost/high-impact funding. The ecosystems have cropped up everywhere there is a coffee shop or an artisanal sandwich truck and the idea of “doing a startup” vs. going to work for some corporate behemoth is a well-worn… Read More

A year ago the Midwest seemed on the cusp of a renaissance. Small towns and cities from Pittsburgh to Omaha had perfected the YC model of accelerator creation and low-cost/high-impact funding. The ecosystems have cropped up everywhere there is a coffee shop or an artisanal sandwich truck and the idea of “doing a startup” vs. going to work for some corporate behemoth is a well-worn… Read More

Powered by WPeMatico

Ian Rountree, the twenty something captain at the helm of Cantos Ventures, an SF-based micro-fund, is characteristic of a new breed of venture capitalists in tech — a group of small funds looking to go toe-to-toe with some of the valley’s most entrenched seed funds like First Round Capital and SV Angel. Rountree is experimenting with a strategy so antithetical to the venture… Read More

Ian Rountree, the twenty something captain at the helm of Cantos Ventures, an SF-based micro-fund, is characteristic of a new breed of venture capitalists in tech — a group of small funds looking to go toe-to-toe with some of the valley’s most entrenched seed funds like First Round Capital and SV Angel. Rountree is experimenting with a strategy so antithetical to the venture… Read More

Powered by WPeMatico

First names, foods and animals have been quite popular lately with founders choosing startup names. Meanwhile, other naming styles are getting more fashionable. We take a look at what’s hot now and what might be in vogue next.

First names, foods and animals have been quite popular lately with founders choosing startup names. Meanwhile, other naming styles are getting more fashionable. We take a look at what’s hot now and what might be in vogue next.  What do you get if you combine the Internet of Things with the business of home insurance? U.K. startup Neos is hoping the answer is damage and/or theft prevention rather than just after-the-unfortunate-fact payouts.

What do you get if you combine the Internet of Things with the business of home insurance? U.K. startup Neos is hoping the answer is damage and/or theft prevention rather than just after-the-unfortunate-fact payouts.