Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

Chinese startups continue to weather tough times as private investors, caught in a cash crunch, are concentrating money into fewer deals.

China’s deal-making activity for startups in the six months ended June halved from a year ago to 1,910, according to data from consulting firm ChinaVenture’s research arm. The amount invested in domestic startups during the first half of 2019 plummeted 54% to $23.2 billion.

The slide in startup investment comes as the money behind the money shrinks amid a cooling economy in China that is exacerbated by a trade war with the U.S. Fundraising for investors was already showing signs of slowdown a year earlier. In the first half of this year, private equity and venture capital firms in China secured 30% less than what they had raised over the same period a year ago, amounting to a total of $54.44 billion; 271 funds managed to raise, down 52%.

That money from limited partners is also flowing to a small rank of investors. Twelve institutions accounted for 57% of all the capital landed by VCs and PEs in the period. Investment coffers that have gotten a big boost include the likes of TPG Capital, Warburg Pincus, DCG Capital, Legend Capital and Source Code Capital.

Healthcare was the most-backed sector during the six months, although proptech startups scored the biggest average deal size. Some of the highest funded companies from the period were artificial intelligence chip maker Horizon Robotics, shared housing upstart Danke and China’s Starbucks challenger, Luckin.

Powered by WPeMatico

Private equity firm Blackstone just announced that it has reached an agreement to acquire mobile advertising company Vungle.

The companies aren’t disclosing the financial terms, but as part of the transaction, Vungle has also reached a settlement with founder Zain Jaffer, who filed a wrongful termination lawsuit against the company earlier this year.

(Update: Multiple sources with knowledge of the deal said that the acquisition price was around — or north of — $750 million. One of those sources also said it was an all-cash transaction.)

“As a best-in-class performance marketing platform, Vungle represents a key growth engine for the mobile app ecosystem,” said Blackstone principal Sachin Bavishi in a statement. “Our investment will help deliver on the company’s tremendous growth potential and we look forward to partnering with management to extend Vungle’s strength across mobile gaming and other performance brands.”

Meanwhile, CEO Rick Tallman said the deal will allow the company to “further accelerate Vungle’s mission to be the trusted guide for growth and engagement, transforming how users discover and experience mobile apps.”

Vungle was founded back in 2011, and, according to the acquisition release, it’s currently working with 60,000 mobile apps worldwide, serving more than 4 billion video views per month and working with publishers like Rovio, Zynga, Pandora, Microsoft and Scopely.

Jaffer led Vungle as CEO until October 2017, when he was arrested on charges including performing a lewd act upon a child and assault with a deadly weapon. The charges were ultimately dropped, with the San Mateo County District Attorney’s office stating that it did “not believe that there was any sexual conduct by Mr. Jaffer that evening,” while “the injuries were the result of Mr. Jaffer being in a state of unconsciousness caused by prescription medication.”

In his lawsuit, Jaffer alleged that after the charges were dropped, “Vungle unfairly and unlawfully sought to destroy my career, blocked my efforts to sell my own shares or transfer shares to family members, and tried to prevent me from purchasing shares in the Company.”

In a statement today, Jaffer said, he is “pleased with the terms of the settlement, which are confidential.” He also commented on the acquisition:

It is extremely gratifying for me to see our early vision, execution and the hard work of so many talented people rewarded like this. From Day 1, Vungle has been at the forefront of the changing advertising landscape. Today, companies of all sizes, and in all industries, are utilizing in-app video ads as an integral part of their customer acquisition strategies.

The acquisition is expected to close later this year. According to Crunchbase, Vungle previously raised more than $25 million from Crosslink Capital, Thomvest Ventures, Seven Peaks Ventures, GV, AOL Ventures, Uncork Capital, 500 Startups and Angelpad, where the startup was incubated. (AOL Ventures was backed by TechCrunch’s parent company AOL, a.k.a. Oath, a.k.a. Verizon Media.)

Powered by WPeMatico

Every year hundreds of startups launch with dreams of becoming the next enterprise software unicorn. And it’s no wonder, given the $500 billion market and the rate at which the enterprise giants snap up emerging players. If you’re the founder of an early-stage enterprise startup, join us for TC Sessions: Enterprise in San Francisco on September 5 at the Yerba Buena Center for the Arts.

Even better, grab the opportunity by the horns and buy a Startup Demo Package. There is limited space available. This is your chance to plant your company in front of some of the most influential enterprise movers and shakers — we’re talking more than 1,000 attendees. Demo tables are reserved for startups with less than $3 million in funding and are available for $2,000, which includes four tickets to the event.

This day-long intensive event features speakers, panel discussions, demos, workshops and world-class networking. Get ready for a head-on, hype-free exploration of the considerable challenges enterprise companies face — regardless of their size.

TechCrunch editors will interview founders and leaders from both established and up-and-coming companies on topics ranging from intelligent marketing automation and the cloud to machine learning and AI. And they’ll question enterprise-focused VCs about where they’re directing their early, middle and late-stage investments.

The full roster of speakers is still to be announced, but here’s a quick hit of who you can expect at TC Sessions: Enterprise.

You’ll hear from Scott Farquhar, co-founder and co-CEO of Atlassian, a company that’s changed the way developers work. Want to hear more about enterprise and the cloud? Snowflake’s co-founder and president of product, Benoit Dageville, will be on hand to talk about the company’s mission to bring the enterprise database to the cloud.

Have someone you want to hear from our stage? Submit your speaker suggestion here.

Pro Tip: For each TC Sessions: Enterprise ticket you buy, we’ll register you for a complimentary Expo Only pass to TechCrunch Disrupt SF on October 2-4.

TC Sessions: Enterprise takes place September 5 at San Francisco’s Yerba Buena Center for the Arts. Don’t miss this opportunity to showcase your early-stage enterprise startup in front of leading enterprise software founders, investors and technologists. Buy your Startup Demo Package today.

Looking for sponsorship opportunities? Contact our TechCrunch team to learn about the benefits associated with sponsoring TC Sessions: Enterprise 2019.

Powered by WPeMatico

Three years ago, I met with a founder who had raised a massive seed round at a valuation that was at least five times the market rate. I asked what firm made the investment.

She said it was not a traditional venture firm, but rather a strategic investor that not only had no ties to her space but also had no prior investment experience. The strategic investor, she said, was looking to “get their hands dirty” and “get in on the ground floor.”

Over the next 2 years, I kept a close eye on the founder. Although she had enough capital to pivot her business focus multiple times, she seemed to be at odds, serving the needs of her strategic investor and her customer base.

Ultimately, when the business needed more capital to survive, the strategic investor didn’t agree with the founder’s focus, opted not to prop it up, and the business had to shut down.

Sadly, this is not an uncommon story as examples abound of strategic investors influencing startup direction and management decisions to the point of harm for the startup. Corporate strategics, not to be confused with dedicated funds focused on financial returns like a traditional venture investor like Google Ventures, often care less about return on investment, and more about a startup’s focus, and sector specificity. If corporate imperatives change, the strategic may cease to be the right partner or could push the startup in a challenging direction.

And yet, fortunately, as the disruptive power of technology is being unleashed on nearly every major industry, strategic investors are now getting smarter, both in terms of how they invest and how they partner with entrepreneurs.

From making strong acquisitive plays (i.e. GM’s purchase of Cruise Automation or Toyota’s early-stage investment in Uber) to building dedicated funds, to executing commercial agreements in tandem with capital investment, strategics are getting savvier, and by extension, becoming better partners. In some instances, they may be the best partner.

Negotiating a term sheet with a strategic investor necessitates a different set of considerations. Namely: the preference for a strategic to facilitate commercial milestones for the startup, a cautious approach to avoid the “over-valuation” trap, an acute focus on information rights, and the limitation of non-compete provisions.

Powered by WPeMatico

Private equity firms get a bad rap — and not without reason. In the prototypical example, a bunch of men in suits (and these folks always seem to be men for some reason) swoop in from Manhattan with Excel spreadsheets and pink slips, slashing and burning through an organization while ladening the balance sheet with debt in an algebraic alchemy of monetary extraction.

Vultures, parasites, octopuses — these are folks who almost certainly won popularity contests in high school and now seem to be shooting for most unpopular person to be compared to a crustacean in the Finance section of the WSJ (and there is some damn strong competition in those pages).

Sometimes that restructuring can save an org, and yes, many companies need a Marie Kondo armed with a business plan. But it’s a model that works best for, say, retail chains, and traditionally has been wholly incompatible with the tech industry.

Tech is a tough place for private equity buyouts, as the biggest expense for most companies is talent (i.e. R&D), and cutting R&D is usually the quickest path to cutting the valuation of the asset you just acquired. Unlike retail or manufacturing, there are just fewer cost levers to manipulate to make the numbers look better, and so PE firms have generally shied away from big tech acquisitions.

So it was interesting talking to Simon Segars this week in New York. Segars is the CEO and longtime executive at ARM Holdings, the U.K.-headquartered chip designer that powers billions of devices worldwide. Over the past two decades, ARM has had an incredible run: Last year, its designs were imprinted on 22.9 billion chips, thanks largely to the now ubiquitous adoption of smartphones across the world.

That success has been under stress though. As Brian Heater analyzed in his State of the Smartphone, smartphone growth has slowed in most markets as consumers extend their upgrade cycles and the pace of innovation has slowed. Add in the ongoing trade kerfuffle between the U.S. and China, and suddenly being the worldwide leading designer of smartphone chips isn’t as enviable as it was even just a few years ago.

As a public company facing this landscape, ARM would have faced incredible pressure from investors to meet short-term revenue targets while cutting back on R&D — the very source of future growth the company has relied on its entire history. But ARM isn’t a public company — instead, SoftBank founder and CEO Masayoshi Son bought out the company entirely in 2016 for $32 billion.

Rather than being pegged to its stock price or a quick return to a PE shop, ARM is now seemingly evaluated on growth in its intellectual property and strategy for capturing new markets. “I’m in a very fortunate position where, despite the slowing of the smartphone market … I’ve got an owner that says, invest, you know, invest like crazy to make sure you capture these ways of growth in the future, which is what we’re doing,” Segars explained to TechCrunch.

The company could have just doubled down on its existing product lines, but SoftBank’s ownership has opened the floodgates to explore other areas that could use ARM expertise. The company is now focused (if one can focus on many things) on everything from 5G and networking to IoT and autonomous driving. “We look to be in the right place at the right time with the right technology to catch the upswing into the future,“ Segars said.

That strategy requires some serious audacity though. ARM’s EBITDA was $225 million last year (21% lower than the year before) on $1.8 billion in net sales, which year-over-year grew a paltry 0.2% according to SoftBank’s latest financials. Meanwhile, operating expenses are up from the addition of hundreds of new employees and a new headquarters campus in Cambridge, outside London. R&D isn’t cheap, nor does it payoff quickly.

Yet, that is exactly how Son and SoftBank approach this take-private transaction. “During the acquisition process, Masa said to me, ‘You run the business, I only care about long-term strategy, not going to interfere, you know, you know what you’re doing.’ … [and] Masa has been absolutely true to his word on that,” Segars said. “From a day-to-day basis, SoftBank leaves us completely alone.”

And unlike the bean counters that plague most PE shops, Son isn’t interested in detailed operational data from the firm. “When I give tactical updates… he’s asleep, [but] try stopping him when he’s talking about long-term strategy,” Segars said.

And unlike the PE model of dumping a bunch of high-interest corporate debt on the balance sheet to eke out returns, SoftBank has — at least, so far — avoided that particular tactic. While there were ruminations that SoftBank was considering cashing out some dollars from ARM using loans early last year, such rumors have apparently not panned out. Segars confirmed that “we have none” when we asked about leverage, which has otherwise plagued much of the rest of SoftBank Group and its various entities.

While ARM clearly has a bullish owner who somehow uses financial wizardry to give the company the resources it needs to grow, Son doesn’t have an infinite timeline for the company. Much like classic PE firms with five to seven-year time horizons to harvest returns, Son has already spoken out loud about pushing ARM back into the public markets in roughly five years’ time.

“I’m pretty sure, the night before we go public again, I’m going to be thinking ‘Man, I wish we’d had more time, you know, five years sounds like a lot,” Segars said. But “the way I talk about it within ARM is we’re in an investment phase now … and the goal is that by the time we re-list … the revenues from these new markets are taking off and that’s flowing to the bottom line and we get back to a world of growing top line and expanding margins.”

In other words, ARM is a classic PE deal, but with the focus on actually getting the fundamentals in the business right without that financial alchemy and employee firing sadness. Maybe the plan will work, or maybe it won’t, but it is the right approach to handling the growth of a tech company.

How many other tech companies could use such an approach? How many other companies are currently languishing if only they had more focused owners with a true growth mindset to invest in the future? Silicon Valley has created trillions of dollars in market value over the past two decades, but there is even more waiting to be unlocked. And the best part is, it doesn’t even require an Excel macro to make it happen.

Powered by WPeMatico

When starting a tech company, there seems to be a playbook that most entrepreneurs follow. While some may start with a bit of bootstrapping, most will dive straight into raising seed money through investors. In many cases, this is a great path. It’s a path I’ve taken twice myself, first with GroupMe, and then again with Fundera.

Ironically, though, my second venture-backed company is a business focused on helping entrepreneurs find debt financing—a process I’ve gone through only once myself. But after five years of building and scaling this business, it’s made me take a step back and consider the question of when and where debt financing might be a better option for a business than equity financing, and vice versa.

I view these financing vehicles differently now than I did half a decade ago, and think it’s time we start to think a bit wider and diversely about how we finance our growing endeavors.

After all, when entrepreneurs take venture capital, they usually sign up to provide a 10x return on an investor’s capital. This expectation ultimately influences how they operate their business in the short-term. Maybe they’re not always ready for that expectation.

Or maybe they know they need to focus on building a good business before a great one. In this case, debt may be the better vehicle, where the only expectation is to pay it back.

Whether it’s money to get your business off the ground, capital to fuel additional growth, or cash to cover a gap, and whether you’re guiding the growth of a burgeoning startup, a smaller business, or even consulting firm helping other entrepreneurs, you should think critically about how you finance your business.

Here’s what to consider.

Powered by WPeMatico

Where are all the biotechnology companies raising these days? We crunched some numbers to arrive at an answer.

Using funding rounds data from Crunchbase, we plotted the count of venture capital funding rounds raised by companies in the fairly expansive biotechnology category in Crunchbase. Click the chart below and you can hover over individual data points to see the number of venture rounds raised in a given metro area between the start of 2018 and late May 2019 (as of publication). Although there are biotechnology companies located throughout the world, we focused here on just the U.S.

Unlike in the software-funding business, where New York City (and its surrounding area) ranks second in overall deal volume, the greater Boston metro area outranks the Big Apple in biotech venture deal volume. The SF Bay Area (which includes both San Francisco and the towns in Silicon Valley north and west of San Jose) outranks Boston in biotech deal volume, but, then again, it’s also a much larger geographic area with a higher density of startups overall.

Crunchbase News recently covered a $120 million round raised by immunotherapy upstart AlloVir. In the software business, a raise that large would be notable; however, in the business of biology, not so much.

Just for reference, the average Series B round raised by U.S. enterprise software startups between 2018 and May 2019 was about $22.7 million. The average Series B for biotech companies from that same time period: just about $40 million on the dot.

Spinning up a cluster of cells at a lab bench is costlier, harder to do and the outcomes of experiments are less certain than the results of implementing a new software framework. Add to that the tremendous cost of performing clinical trials and clearing regulatory hurdles — all before costly sales and marketing campaigns to get treatments in front of doctors and end users — and it’s easy to understand why many biotechnology companies need to raise so much money in the early stages of the startup cycle.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a newsletter published every Saturday that dives into the week’s noteworthy venture capital deals, funds and trends. Before I dive into this week’s topic, let’s catch up a bit. Last week, I wrote about the sudden uptick in beverage startup rounds. Before that, I noted an alternative to venture capital fundraising called revenue-based financing. Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets.

Here’s what I’ve been thinking about this week: Unicorn scarcity, or lack thereof. I’ve written about this concept before, as has my Equity co-host, Crunchbase News editor-in-chief Alex Wilhelm. I apologize if the two of us are broken records, but I think we’re equally perplexed by the pace at which companies are garnering $1 billion valuations.

Here’s the latest data, according to Crunchbase: “2018 outstripped all previous years in terms of the number of unicorns created and venture dollars invested. Indeed, 151 new unicorns joined the list in 2018 (compared to 96 in 2017), and investors poured more than $135 billion into those companies, a 52% increase year-over-year and the biggest sum invested in unicorns in any one year since unicorns became a thing.”

2019 has already coined 42 new unicorns, like Glossier, Calm and Hims, a number that grows each and every week. For context, a total of 19 companies joined the unicorn club in 2013 when Aileen Lee, an established investor, coined the term. Today, there are some 450 companies around the globe that qualify as unicorns, representing a cumulative valuation of $1.6 trillion.

We’ve clung to this fantastical terminology for so many years because it helps us classify startups, singling out those that boast valuations so high, they’ve gained entry to a special, elite club. In 2019, however, $100 million-plus rounds are the norm and billion-dollar-plus funds are standard. Unicorns aren’t rare anymore; it’s time to rethink the unicorn framework.

Petition to stop using the term “unicorn” unless the company is valued at more than $1 billion *and* profitable.

— Kate Clark (@KateClarkTweets) May 22, 2019

Last week, I suggested we only refer to profitable companies with a valuation larger than $1 billion as unicorns. Understandably, not everyone was too keen on that idea. Why? Because startups in different sectors face barriers of varying proportions. A SaaS company, for example, is likely to achieve profitability a lot quicker than a moonshot bet on autonomous vehicles or virtual reality. Refusing startups that aren’t yet profitable access to the unicorn club would unfairly favor certain industries.

So what can we do? Perhaps we increase the valuation minimum necessary to be called a unicorn to $10 billion? Initialized Capital’s Garry Tan’s idea was to require a startup have 50% annual growth to be considered a unicorn, though that would be near-impossible to get them to disclose…

While I’m here, let me share a few of the other eclectic responses I received following the above tweet. Joseph Flaherty said we should call profitable billion-dollar companies Pegasus “since [they’ve] taken flight.” Reagan Pollack thinks profitable startups oughta be referred to as leprechauns. Hmmmm.

The suggestions didn’t stop there. Though I’m not so sure adopting monikers like Pegasus and leprechaun will really solve the unicorn overpopulation problem. Let me know what you think. Onto other news.

Image by Rafael Henrique/SOPA Images/LightRocket via Getty Images

CrowdStrike has set its IPO terms. The company has inked plans to sell 18 million shares at between $19 and $23 apiece. At a midpoint price, CrowdStrike will raise $378 million at a valuation north of $4 billion.

Slack inches closer to direct listing. The company released updated first-quarter financials on Friday, posting revenues of $134.8 million on losses of $31.8 million. That represents a 67% increase in revenues from the same period last year when the company lost $24.8 million on $80.9 million in revenue.

Online lender SoFi has quietly raised $500M led by Qatar

Groupon co-founder Eric Lefkofsky just-raised another $200M for his new company Tempus

Less than 1 year after launching, Brex eyes $2B valuation

Password manager Dashlane raises $110M Series D

Enterprise cybersecurity startup BlueVoyant raises $82.5M at a $430M valuation

Talkspace picks up $50M Series D

TaniGroup raises $10M to help Indonesia’s farmers grow

Stripe and Precursor lead $4.5M seed into media CRM startup Pico

Maveron, a venture capital fund co-founded by Starbucks mastermind Howard Schultz, has closed on another $180 million to invest in early-stage consumer startups. The capital represents the firm’s seventh fundraise and largest since 2000. To keep the fund from reaching mammoth proportions, the firm’s general partners said they turned away more than $70 million amid high demand for the effort. There’s more where that came from, here’s a quick look at the other VCs to announce funds this week:

This week, I penned a deep dive on Slack, formerly known as Tiny Speck, for our premium subscription service Extra Crunch. The story kicks off in 2009 when Stewart Butterfield began building a startup called Tiny Speck that would later come out with Glitch, an online game that was neither fun nor successful. The story ends in 2019, weeks before Slack is set to begin trading on the NYSE. Come for the history lesson, stay for the investor drama. Here are the other standout EC pieces of the week.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I debate whether the tech press is too negative or too positive in its coverage of tech startups. Plus, we dive into Brex’s upcoming round, SoFi’s massive raise and CrowdStrike’s imminent IPO.

Powered by WPeMatico

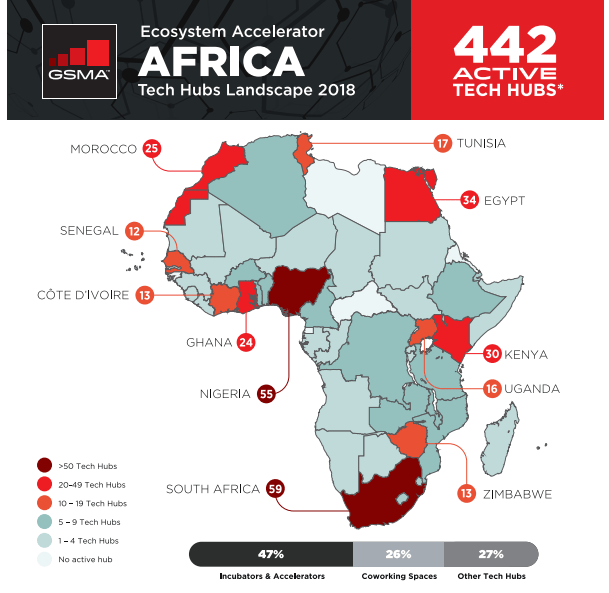

Jumia may be the first startup you’ve heard of from Africa. But the e-commerce venture that recently listed on the NYSE is definitely not the first or last word in African tech.

The continent has an expansive digital innovation scene, the components of which are intersecting rapidly across Africa’s 54 countries and 1.2 billion people.

When measured by monetary values, Africa’s tech ecosystem is tiny by Shenzen or Silicon Valley standards.

But when you look at volumes and year over year expansion in VC, startup formation, and tech hubs, it’s one of the fastest growing tech markets in the world. In 2017, the continent also saw the largest global increase in internet users—20 percent.

If you’re a VC or founder in London, Bangalore, or San Francisco, you’ll likely interact with some part of Africa’s tech landscape for the first time—or more—in the near future.

That’s why TechCrunch put together this Extra-Crunch deep-dive on Africa’s technology sector.

A foundation for African tech is the continent’s 442 active hubs, accelerators, and incubators (as tallied by GSMA). These spaces have become focal points for startup formation, digital skills building, events, and IT activity on the continent.

Prominent tech hubs in Africa include CcHub in Nigeria, Pan-African incubator MEST, and Kenya’s iHub, with over 200 resident members. More of these organizations are receiving funds from DFIs, such as the World Bank, and aid agencies, including France’s $76 million African tech fund.

Prominent tech hubs in Africa include CcHub in Nigeria, Pan-African incubator MEST, and Kenya’s iHub, with over 200 resident members. More of these organizations are receiving funds from DFIs, such as the World Bank, and aid agencies, including France’s $76 million African tech fund.

Blue-chip companies such as Google and Microsoft are also providing money and support. In 2018 Facebook opened its own Hub_NG in Lagos with partner CcHub, to foster startups using AI and machine learning.

Powered by WPeMatico

The Valley’s rocky history with cleantech investing has been well-documented.

Startups focused on non-emitting-generation resources were once lauded as the next big cash cow, but the sector’s hype quickly got away from reality.

Complex underlying science, severe capital intensity, slow-moving customers and high-cost business models outside the comfort zones of typical venture capital ultimately caused a swath of venture-backed companies and investors in the cleantech boom to fall flat.

Yet, decarbonization and sustainability are issues that only seem to grow more dire and more galvanizing for founders and investors by the day, and more company builders are searching for new ways to promote environmental resilience.

While funding for cleantech startups can be hard to find nowadays, over time we’ve seen cleantech startups shift down the stack away from hardware-focused generation plays toward vertical-focused downstream software.

A far cry from past waves of venture-backed energy startups, the downstream cleantech companies offered more familiar technology with more familiar business models, geared toward more recognizable verticals and end users. Now, investors from less traditional cleantech backgrounds are coming out of the woodwork to take a swing at the energy space.

An emerging group of non-traditional investors getting involved in the clean energy space are those traditionally focused on fintech, such as New York and Europe-based venture firm Anthemis — a financial services-focused team that recently sat down with our fintech contributor Gregg Schoenberg and I (check out the full meat of the conversation on Extra Crunch).

The tie between cleantech startups and fintech investors may seem tenuous at first thought. However, financial services have long played a significant role in the energy sector and is now becoming a more common end customer for energy startups focused on operations, management and analytics platforms, thus creating real opportunity for fintech investors to offer differentiated value.

Though the conversation around energy resources and decarbonization often focuses on politics, a significant portion of decisions made in the energy generation business is driven by pure economics — is it cheaper to run X resource relative to resources Y and Z at a given point in time? Based on bid prices for request for proposals (RFPs) in a specific market and the cost-competitiveness of certain resources, will a developer be able to hit their targeted rate of return if they build, buy or operate a certain type of generation asset?

Alternative generation sources like wind, solid oxide fuel cells or large-scale or even rooftop solar have reached more competitive cost levels — in many parts of the U.S., wind and solar are in fact often the cheapest form of generation for power providers to run.

Thus as renewable resources have grown more cost competitive, more infrastructure developers and other new entrants have been emptying their wallets to buy up or build renewable assets like large-scale solar or wind farms, with the American Council on Renewable Energy even forecasting cumulative private investment in renewable energy possibly reaching up to $1 trillion in the U.S. by 2030.

A major and swelling set of renewable energy sources are now led by financial types looking for tools and platforms to better understand the operating and financial performance of their assets, in order to better maximize their return profile in an increasingly competitive marketplace.

Therefore, fintech-focused venture firms with financial service pedigrees, like Anthemis, now find themselves in pole position when it comes to understanding cleantech startup customers, how they make purchase decisions, and what they’re looking for in a product.

In certain cases, fintech firms can even offer significant insight into shaping the efficacy of a product offering. For example, Anthemis portfolio company kWh Analytics provides a risk management and analytics platform for solar investors and operators that helps break down production, financial analysis and portfolio performance.

For platforms like kWh analytics, fintech-focused firms can better understand the value proposition offered and help platforms understand how their technology can mechanically influence rates of return or otherwise.

The financial service customers for clean energy-related platforms extends past just private equity firms. Platforms have been and are being built around energy trading, renewable energy financing (think financing for rooftop solar) or the surrounding insurance market for assets.

When speaking with several of Anthemis’ cleantech portfolio companies, founders emphasized the value of having a fintech investor on board that not only knows the customer in these cases, but that also has a deep understanding of the broader financial ecosystem that surrounds energy assets.

Founders and firms seem to be realizing that various arms of financial services are playing growing roles when it comes to the development and access to clean energy resources.

By offering platforms and surrounding infrastructure that can improve the ease of operations for the growing number of finance-driven operators or can improve the actual financial performance of energy resources, companies can influence the fight for environmental sustainability by accelerating the development and adoption of cleaner resources.

Ultimately, a massive number of energy decisions are made by financial services firms and fintech firms may often know the customers and products of downstream cleantech startups more than most. And while the financial services sector has often been labeled as dirty by some, the vital role it can play in the future of sustainable energy offers the industry a real chance to clean up its image.

Powered by WPeMatico