Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

Brex, the fintech business that’s taken the startup world by storm with its sought after corporate card tailored for entrepreneurs, is raising millions in Series D funding less than a year after it launched, TechCrunch has learned.

Bloomberg reports Brex is raising at a $2 billion valuation, though sources tell TechCrunch the company is still in negotiations with both new and existing investors. Brex didn’t immediately respond to requests for comment.

Kleiner Perkins is leading the round via former general partner Mood Rowghani, who left the storied venture capital fund last year to form Bond alongside Mary Meeker and Noah Knauf. As we’ve previously reported, the Bond crew is still in the process of deploying capital from Kleiner’s billion-dollar Digital Growth Fund III, the pool of capital they were responsible for before leaving the firm.

Bond, which recently closed on $1.25 billion for its debut effort and made its first investment, is not participating in the round for Brex, sources confirm to TechCrunch. Bond declined to comment.

Brex, a graduate of Y Combinator’s winter 2017 cohort, has raised $182 million in VC funding, reaching a valuation of $1.1 billion in October 2018 three months after launching its corporate card for startups and less than a year after completing YC’s accelerator program.

Most recently, Brex attracted a $125 million Series C investment led by Greenoaks Capital, DST Global and IVP. The startup is also backed by PayPal founders Peter Thiel and Max Levchin, and VC firms such as Ribbit Capital, Oneway Ventures and Mindset Ventures, according to PitchBook.

The company’s pace of growth is unheard of, even in Silicon Valley where inflated valuations and outsized rounds are the norm. Why? Brex has tapped into a market dominated by legacy players in dire need of technological innovation and, of course, startup founders always need access to credit. That, coupled with the fact that it’s capitalized on YC’s network of hundreds of startup founders — i.e. Brex customers — has accelerated its path to a multi-billion-dollar price tag.

Brex doesn’t require any kind of personal guarantee or security deposit from its customers, allowing founders near-instant access to credit. More importantly, it gives entrepreneurs a credit limit that’s as much as 10 times higher than what they would receive elsewhere.

Investors may also be enticed by the fact the company doesn’t use third-party legacy technology, boasting a software platform that is built from scratch. On top of that, Brex simplifies a lot of the frustrating parts of the corporate expense process by providing companies with a consolidated look at their spending.

“We have a very similar effect of what Stripe had in the beginning, but much faster because Silicon Valley companies are very good at spending money but making money is harder,” Brex co-founder and chief executive officer Henrique Dubugras told me late last year.

Stripe, for context, was founded in 2010. Not until 2014 did the company raise its unicorn round, landing a valuation of $1.75 billion with an $80 million financing. Today, Stripe has raised a total of roughly $1 billion at a valuation north of $20 billion.

Dubugras and Brex co-founder Pedro Franceschi, 23-year-old entrepreneurs, relocated from Brazil to Stanford in the fall of 2016 to attend the university. They dropped out upon getting accepted into YC, which they applied to with a big dreams for a virtual reality startup called Beyond. Beyond quickly became Brex, a name in which Dubugras recently told TechCrunch was chosen because it was one of few four-letter word domains available.

Brex’s funding history

March 2017: Brex graduates Y Combinator

April 2017: $6.5M Series A | $25M valuation

April 2018: $50M Series B | $220M valuation

October 2018: $125M Series C | $1.1B valuation

May 2019: undisclosed Series D | ~$2B valuation

In April, Brex secured a $100 million debt financing from Barclays Investment Bank. At the time, Dubugras told TechCrunch the business would not seek out venture investment in the near future, though he did comment that the debt capital would allow for a significant premium when Brex did indeed decide to raise capital again.

In 2019, Brex has taken steps several steps toward maturation.Recently, it launched a rewards program for customers and closed its first notable acquisition of a blockchain startup called Elph. Shortly after, Brex released its second product, a credit card made specifically for ecommerce companies.

Its upcoming infusion of capital will likely be used to develop payment services tailored to Fortune 500 business, which Dubugras has said is part of Brex’s long term plan to disrupt the entire financial technology space.

Powered by WPeMatico

When SeedLegals launched in 2017 in the U.K., I’d say many of us thought, “why has that not been done before?” After all, two things have happened that make this an obvious idea for a startup: startup funding rounds are now so common that there is no reason large amounts of automation could not be done. If you can buy a divorce online, surely you can organise funding rounds?

The second trend is the sheer level of automation happening in legal software today. After all, we now have “Uber for Lawyers” (Lexoo, Linkilaw, Lawbite) and AI-driven legaltech (KIRA, Luminance, ThoughtRiver). (Eventually, we will have blockchain smart contracts do ALL the work, but that’s for another time…).

So it’s not surprising that today SeedLegals announces it has closed a $4 million Series A led by venture capital firm Index Ventures (London/SF/etc.) with participation from Kima Ventures (Paris/TelAviv), The Family (Paris) and existing investor Seedcamp (London).

SeedLegals says it now has 7,000 startups — capturing, it claims, 8% of all early-stage U.K. funding rounds — using its platform to manage the entire fundraising process and all related legal documents. The platform helps companies build and negotiate term sheets, shareholder agreements, cap tables, stock option allocations, EIS approvals, hiring agreements, NDAs and more.

It also has two new products: SeedFAST and Instant Investment, which enable startups to quickly top up investment between funding rounds.

If U.K. companies created more than 27,000 contracts on SeedLegals last year, the start-up reckons that saved them an estimated £4.5 million in legal costs. Normally, lawyers create custom documents for each transaction. That means 18 weeks, on average, to complete a funding round, with legal fees starting at £3,000 for a simple seed round to £20,000 and up for each side for later-stage rounds.

The platform replaces spreadsheets and Word docs with a database-driven platform. You enter data once and the system uses pre-built knowledge, deal data and document automation to dynamically build all the outputs.

Anthony Rose, co-founder and CEO at SeedLegals, says they have removed the “complexity, unnecessary middlemen, standardized and automated the processes, and that has really resonated with both founders and investors.”

Hannah Seal from Index Ventures, who joins the board with this round, commented: “SeedLegals

is making the complex process of fundraising straightforward for everyone involved.

“We closed this round on SeedLegals and have been impressed with the speed and ease of use. For startups who spend thousands on legal fees on agreements that vary little from company to company, this is an absolute no-brainer.”

SeedLegals was created by serial entrepreneur Anthony Rose, known in the tech industry for his work launching BBC iPlayer, and VC and angel investor Laurent Laffy, whose own portfolio includes consumer brands such as Graze and Secret Escapes .

Powered by WPeMatico

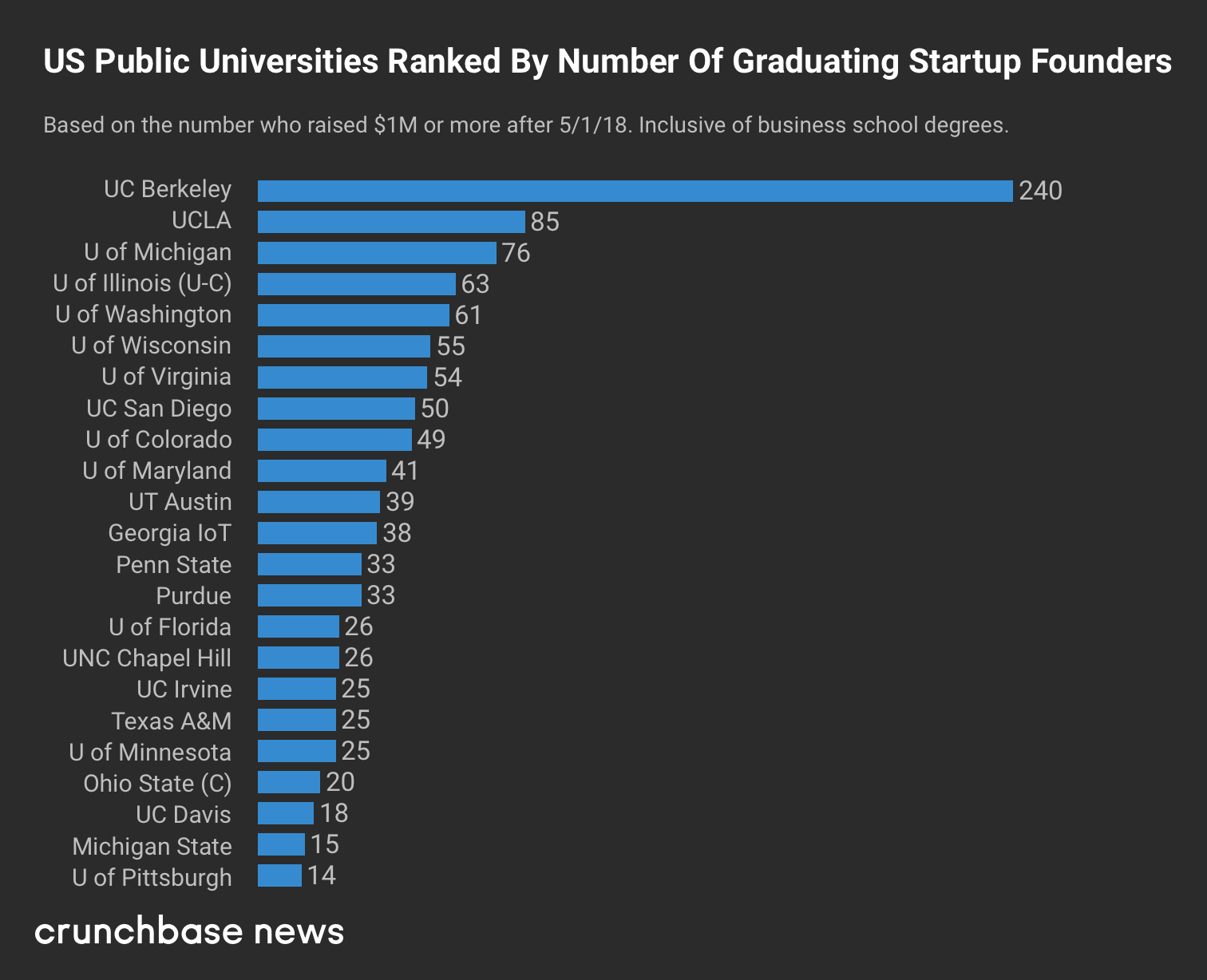

A lot of students attend public universities to lessen the financial burden of higher education. At last tally, tuition and fees at American public colleges and universities averaged around $6,800 a year, per the federal government. That’s far below the $32,600 mean price tag for private, nonprofit institutions.

Yet when it comes to public universities, the old adage “you get what you pay for” clearly does not apply. Leading public research universities in particular have a track record of turning out enviably knowledgeable and successful graduates. That includes a whole lot of funded startup founders.

And that leads us to our latest ranking. At Crunchbase News, we’ve been tracking the intersection of alumni affiliation and startup funding for the past few years. In a story published earlier this week, we looked at which U.S. universities graduated the most founders of startups that raised $1 million or more in roughly the past year.

For today’s follow-up, we’re focusing exclusively on public universities. Starting with a list of top-ranking research universities, we looked to see which have graduated the highest number of funded founders.

For the most part, we used the same criteria as the public-and-private list, focusing on startups that raised $1 million or more after May, 2018. The public list, however, does not separate out business school grads.

Without further ado, here’s the list:

Looking at the list above, a few things stand out. First, our top ranker, University of California at Berkeley, is multiples above the rest of the field when it comes to graduating funded founders.

Berkeley is a school that’s generally hard to get into, prominent in STEM and located in the VC-rich San Francisco Bay Area. So seeing it top the list isn’t necessarily surprising. However, the magnitude of its lead — with nearly three times the funded founders of runner-up UCLA — does warrant attention.

Big Midwestern schools also did well, with University of Michigan and University of Illinois, Urbana-Champaign nabbing the third and fourth spots.

More broadly, the list includes schools from all U.S. regions, including the East Coast, West Coast, South, Midwest and Southwest. So no particular region has a lock on graduating funded entrepreneurs. That’s also not surprising. But it’s good to have some more numbers to back up that notion.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a newsletter published every Saturday that dives into the week’s most noteworthy venture deals, fundraises, M&A transactions and trends. Let’s take a quick moment to catch up. Last week, I wrote about an alternative to venture capital called revenue-based financing and before that, I jotted down some notes on one of VCs’ favorite spaces: cannabis tech. Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets.

This week, I want to share some thoughts — questions, rather — on beverages. Just as my inbox has been full of cannabis-related pitches, it’s also been packed with descriptions of new…drinks. Perhaps the most noted so far is Liquid Death, canned water for the punk rock crowd, because why not? Liquid Death has attracted nearly $2 million in funding from angel investors like Away co-founder Jen Rubio and Twitter co-founder Biz Stone. Before I tell you about a few other up-and-coming beverage makers, I must beg the question: Does the beverage industry need disrupting?

Founders say yes. Why? For one, because millennials, according to various studies, are consuming less alcohol than previous generations and are therefore seeking non-alcoholic beverage alternatives. Enter Seedlip, a non-alcoholic spirits company, for example. Or Haus, launching this summer, an all-natural apéritif distilled from grapes that has a lower alcohol content than most hard liquors. Haus, like any good consumer startup in 2019, is shipped directly to your door.

Beverages are being disrupted, there’s no stopping it. pic.twitter.com/DMEg88t4iO

— Kate Clark (@KateClarkTweets) May 21, 2019

Bev, a canned wine business that recently raised $7 million in seed funding from Founders Fund, thinks marketing in the alcohol industry is the problem. Founder Alix Peabody designed a line of female-focused canned rosé. If you’re wondering why alcohol needs to be gendered in such a way, you’re not alone. Peabody explained most alcohol brands cater to men, and that’s a problem.

“The joke I like to make is there’s a go-to type of alcohol for every type of bro and we just don’t have that for women,” Peabody told TechCrunch earlier this year.

Finally, the wellness movement is taking over, driving VCs toward some odd upstarts. From wellness chat and journaling apps to therapy substitutes to fitness companies, stick wellness in a pitch and investors will take a second look. More Labs, for example, is backed with $8 million in VC funding. The company is readying the launch of Liquid Focus, a biohacking-beverage that claims to “solve modern-day stressors without the negative side effects.” Finally, Elements, “an elevated functional wellness beverage formulated with clinical levels of adaptogens to give your body exactly what it needs in four categories (focus, vitality, calm, and rest) for specific cognitive functions” (damn, what copy), recently launched. It doesn’t appear to be funded yet, but let’s just give it a few months.

There’s more where that came from, but I’m done for now. On to other news.

I almost skipped IPO corner this week because no big-name companies dropped or amended their S-1s or completed a highly anticipated IPO, as has been the case basically every week of 2019. But I decided I better give a quick update on Luckin Coffee’s tough second week on the stock market. Luckin Coffee, if you aren’t familiar, is Starbucks’ Chinese rival. The company raised more than $550 million after pricing at $17 per share a little over a week ago. Immediately the stock skyrocketed 20 percent to a roughly $5 billion market cap; then came concerns of the company’s lofty valuation, major cash burn and uncertain path to profitability. Luckin has dropped around 25 percent since closing its debut trading day. It closed Friday down 3 percent.

Y Combinator, the popular accelerator program and investment firm announced this week that it has promoted longtime partner Geoff Ralston to president. This comes two months after former president Sam Altman stepped down to focus his efforts full-time on OpenAI. The promotion of Ralston is an unsurprising choice for YC, an organization that employs roughly 60 people, many of whom have been affiliated with it in one way or another for years.

Automattic acquires subscription payment company Prospress

Shopify quietly acquires Handshake, an e-commerce platform for B2B wholesale purchasing

Streem buys Selerio in an effort to boost its AR conferencing tech

As Amex scoops up Resy, a look at its acquisition history

The Los Angeles ecosystem is $76 million stronger this week as Fika Ventures, a seed-stage venture capital firm, announced its sophomore investment fund. Fika invests roughly half of its capital exclusively in startups headquartered in LA, with a particular fondness for B2B, enterprise and fintech companies. The firm was launched in 2017 by general partners Eva Ho and TX Zhuo, formerly of Susa Ventures and Karlin Ventures, respectively. The pair raised $41 million for the debut effort, opting to nearly double that number the second time around as a means to participate in more follow-on fundings.

DoorDash raises $600M at a $12.7B valuation

TransferWise completes $292M secondary round at a $3.5B valuation

Auth0 raises $103M, pushes its valuation over $1B

Canva gets $70M at a $2.5B valuation

Payment card startup Marqeta confirms $260M round at close to $2B valuation

Modsy scores $37M to virtually design your home

Sun Basket whips up $30M Series E

Zero raises $20M from NEA for a credit card that works like debit

Nigeria’s Gokada raises $5.3M for its motorcycle ride-hail biz

Our premium subscription service had another great week of interesting deep dives. This week, TechCrunch’s Lucas Matney went deep on Getaround’s acquisition of Drivy for his latest installment of The Exit, a new series at TechCrunch where we chat with VCs who were in the right place at the right time and made the right call on an investment that paid off. Here are some of the other Extra Crunch pieces that stood out this week:

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I discuss how startups are avoiding IPOs and VC’s insatiable interest in food delivery startups.

Powered by WPeMatico

On January 12, 2016, Grindr announced it had sold a 60% controlling stake in the company to Beijing Kunlun Tech, a Chinese gaming firm, valuing the company at $155 million. Champagne bottles were surely popped at the small-ish firm.

Though not at a unicorn-level valuation, the 9-figure exit was still respectable and signaled a bright future for the gay hookup app. Indeed, two years later, Kunlun bought the rest of the firm at more than double the valuation and was planning a public offering for Grindr.

On March 27, 2019, it all fell apart. Kunlun was putting Grindr up for sale instead.

What went wrong? It wasn’t that Grindr’s business ground to a halt. By all accounts, its business seems to actually be growing. The problem was that Kunlun owning Grindr was viewed as a threat to national security. Consequently, CFIUS, or the Committee for Foreign Investment in the United States, stepped in to block the transaction.

So what changed? CFIUS was expanded by FIRRMA, or the Foreign Risk Review Modernization Act, in late 2018, which gave it massive new power and scale. Unlike before, FIRRMA gave CFIUS a technology focus. So now CFIUS isn’t just an American problem—it’s an American tech problem. And in the coming years, it will transform venture capital, Chinese involvement in US tech, and maybe even startups as we know it.

Here’s a closer look at how it all fits together.

Image via Getty Images / Busà Photography

CFIUS is the most important agency you’ve never heard of, and until recently it wasn’t even more than a committee. In essence, CFIUS has the ability to stop foreign entities, called “covered entities,” from acquiring companies when it could adversely affect national security—a “covered transaction.”

Once a filing is made, CFIUS investigates the transaction and both parties, which can take over a month in its first pass. From there, the company and CFIUS enter a negotiation to see if they can resolve any issues.

Powered by WPeMatico

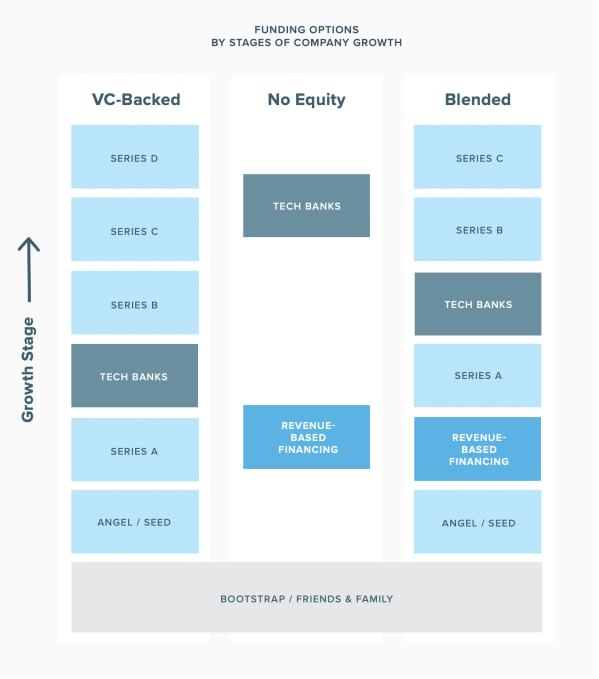

Revenue-based financing is on the rise, at least according to Lighter Capital, a firm that doles out entrepreneur-friendly debt capital.

What exactly is RBF you ask? It’s a relatively new form of funding for tech companies that are posting monthly recurring revenue. Here’s how Lighter Capital, which completed 500 RBF deals in 2018, explains it: “It’s an alternative funding model that mixes some aspects of debt and equity. Most RBF is technically structured as a loan. However, RBF investors’ returns are tied directly to the startup’s performance, which is more like equity.”

Source: Lighter Capital

What’s the appeal? As I said, RBFs are essentially dressed up debt rounds. Founders who opt for RBFs as opposed to venture capital deals hold on to all their equity and they don’t get stuck on the VC hamster wheel, the process in which you are forced to continually accept VC while losing more and more equity as a means of pleasing your investors.

RBFs, however, are better than traditional debt rounds because the investors are more incentivized to help the companies they invest in because they are receiving a certain portion of that business’s monthly revenues, typically 1% to 9%. Eventually, as is explained thoroughly in Lighter Capital’s newest RBF report, monthly payments come to an end, usually 1.3 to 2.5X the amount of the original financing, a multiple referred to as the “cap.” Three to five years down the line, any unpaid amount of said cap is due back to the investor. When all is said in done, ideally, the startup has grown with the support of the capital and hasn’t lost any equity.

At this point, they could opt to raise additional revenue-based capital, they could turn to venture capital or they could tap a tech bank to help them get to the next step. The idea is RBF is easier on the founder and it allows them optionality, something that is often lost when companies turn to VCs.

IPO corner, rapid-fire edition

Slack’s direct listing will be on June 20th. Get excited.

China’s Luckin Coffee raised $650 million in upsized U.S. IPO

Crowdstrike, a cybersecurity unicorn, dropped its S-1.

Freelance marketplace Fiverr has filed to go public on the NYSE.

Plus, I had a long and comprehensive conversation with Zoom CEO Eric Yuan this week about the company’s closely watched IPO. You can read the full transcript here.

Silicon Valley entrepreneur Hosain Rahman, the man behind Jawbone, has managed to raise $65.4 million for his new company, according to an SEC filing. The paperwork, coincidentally or otherwise, was processed while most of the world’s attention was focused on Uber’s IPO. Jawbone, if you remember, produced wireless speakers and Bluetooth earpieces, and went kaput in 2017 after burning up $1 billion in venture funding over the course of 10 years. Ouch.

On the heels of enterprise startup UiPath raising at a $7 billion valuation, the startup’s biggest investor is announcing a new fund to double down on making more investments in Europe. VC firm Accel has closed a $575 million fund — money that it plans to use to back startups in Europe and Israel, investing primarily at the Series A stage in a range of between $5 million and $15 million, reports TechCrunch’s Ingrid Lunden. Plus, take a closer look at Contrary Capital. Part accelerator, part VC fund, Contrary writes small checks to student entrepreneurs and recent college dropouts.

Our paying subscribers are in for a treat this week. Our in-house venture capital expert Danny Crichton wrote down some thoughts on Uber and Lyft’s investment bankers. Here’s a snippet: “Startup CEOs heading to the public markets have a love/hate relationship with their investment bankers. On one hand, they are helpful in introducing a company to a wide range of asset managers who will hopefully hold their company’s stock for the long term, reducing price volatility and by extension, employee churn. On the other hand, they are flagrantly expensive, costing millions of dollars in underwriting fees and related expenses…”

Read the full story here and sign up for Extra Crunch here.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about the notable venture rounds of the week, CrowdStrike’s IPO and more of this week’s headlines.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

OpenFin, the company looking to provide the operating system for the financial services industry, has raised $17 million in funding through a Series C round led by Wells Fargo, with participation from Barclays and existing investors including Bain Capital Ventures, J.P. Morgan and Pivot Investment Partners. Previous investors in OpenFin also include DRW Venture Capital, Euclid Opportunities and NYCA Partners.

Likening itself to “the OS of finance,” OpenFin seeks to be the operating layer on which applications used by financial services companies are built and launched, akin to iOS or Android for your smartphone.

OpenFin’s operating system provides three key solutions which, while present on your mobile phone, has previously been absent in the financial services industry: easier deployment of apps to end users, fast security assurances for applications and interoperability.

Traders, analysts and other financial service employees often find themselves using several separate platforms simultaneously, as they try to source information and quickly execute multiple transactions. Yet historically, the desktop applications used by financial services firms — like trading platforms, data solutions or risk analytics — haven’t communicated with one another, with functions performed in one application not recognized or reflected in external applications.

“On my phone, I can be in my calendar app and tap an address, which opens up Google Maps. From Google Maps, maybe I book an Uber . From Uber, I’ll share my real-time location on messages with my friends. That’s four different apps working together on my phone,” OpenFin CEO and co-founder Mazy Dar explained to TechCrunch. That cross-functionality has long been missing in financial services.

As a result, employees can find themselves losing precious time — which in the world of financial services can often mean losing money — as they juggle multiple screens and perform repetitive processes across different applications.

Additionally, major banks, institutional investors and other financial firms have traditionally deployed natively installed applications in lengthy processes that can often take months, going through long vendor packaging and security reviews that ultimately don’t prevent the software from actually accessing the local system.

OpenFin CEO and co-founder Mazy Dar (Image via OpenFin)

As former analysts and traders at major financial institutions, Dar and his co-founder Chuck Doerr (now president & COO of OpenFin) recognized these major pain points and decided to build a common platform that would enable cross-functionality and instant deployment. And since apps on OpenFin are unable to access local file systems, banks can better ensure security and avoid prolonged yet ineffective security review processes.

And the value proposition offered by OpenFin seems to be quite compelling. OpenFin boasts an impressive roster of customers using its platform, including more than 1,500 major financial firms, almost 40 leading vendors and 15 of the world’s 20 largest banks.

More than 1,000 applications have been built on the OS, with OpenFin now deployed on more than 200,000 desktops — a noteworthy milestone given that the ever-popular Bloomberg Terminal, which is ubiquitously used across financial institutions and investment firms, is deployed on roughly 300,000 desktops.

Since raising their Series B in February 2017, OpenFin’s deployments have more than doubled. The company’s headcount has also doubled and its European presence has tripled. Earlier this year, OpenFin also launched it’s OpenFin Cloud Services platform, which allows financial firms to launch their own private local app stores for employees and customers without writing a single line of code.

To date, OpenFin has raised a total of $40 million in venture funding and plans to use the capital from its latest round for additional hiring and to expand its footprint onto more desktops around the world. In the long run, OpenFin hopes to become the vital operating infrastructure upon which all developers of financial applications are innovating.

“Apple and Google’s mobile operating systems and app stores have enabled more than a million apps that have fundamentally changed how we live,” said Dar. “OpenFin OS and our new app store services enable the next generation of desktop apps that are transforming how we work in financial services.”

Powered by WPeMatico

Locus, an Indian startup that uses AI to help businesses map out their logistics, has raised $22 million in Series B funding to expand its operations in international markets.

The financing round for the four-year-old startup was led by Falcon Edge Capital and Tiger Global. Existing investors Exfinity Venture Partners and Blume Ventures also participated in the round. The startup has raised $29 million to date, Nishith Rastogi, co-founder and CEO of Locus, told TechCrunch in an interview.

Locus works with companies that operate in FMCG, logistics and e-commerce spaces. Some of its clients include Tata Group companies, Myntra, BigBasket, Lenskart and Bluedart. It helps these clients automate their logistics workload — tasks such as planning, organizing, transporting and tracking of inventories, and finding the best path to reach a destination — that have traditionally required intensive human labor.

“Say a Lenskart representative is visiting a house or an office to offer an eye checkup, and suddenly two more people there are interested in getting their eyes checked. The representative could attend these two new potential clients, or wrap things up with the first client and take care of his or her next appointment,” said Rastogi.

Locus looks at a client’s past data, identifies patterns and automates these kind of decisions on a large scale. In an example shared earlier with TechCrunch, Rastogi talked about how Locus had built a scanner for e-commerce companies for measuring products.

Rastogi said he will use the fresh capital to develop products and expand Locus in Southeast Asian and North American markets. The startup says half of its 110-person workforce is outside of India. Half of the IP it has built and the revenue it generates comes from its team outside of India.

He said the startup has spent the recent quarters studying these international markets, and has secured some anchor clients to expand the business. Locus is operationally profitable already and any additional capital goes into expanding its business, he added.

The logistics market in India has long been riddled with challenges. A growing number of startups, including BlackBuck — which raised $150 million last week — have emerged in recent years to tackle these problems.

The new funding also illustrates Tiger Global’s new strategy for the Indian market. The VC fund, which has invested in B2C businesses Flipkart and Ola in India, has made a number of investments in B2B startups in recent months. Last month, it invested $90 million in agritech supply chain startup Ninjacart, and weeks later, it gave cloud-based solutions provider Zenoti $50 million. It also participated in customer marketing service ClearTap’s $26 million round.

Powered by WPeMatico

The San Francisco Bay Area is a global powerhouse at launching startups that go on to dominate their industries. For locals, this has long been a blessing and a curse.

On the bright side, the tech startup machine produces well-paid tech jobs and dollars flowing into local economies. On the flip side, it also exacerbates housing scarcity and sky-high living costs.

These issues were top-of-mind long before the unicorn boom: After all, tech giants from Intel to Google to Facebook have been scaling up in Northern California for over four decades. Lately however, the question of how many tech giants the region can sustainably support is getting fresh attention, as Pinterest, Uber and other super-valuable local companies embark on the IPO path.

The worries of techie oversaturation led us at Crunchbase News to take a look at the question: To what extent do tech companies launched and based in the Bay Area continue to grow here? And what portion of employees work elsewhere?

For those agonizing about the inflationary impact of the local unicorn boom, the data offers a bit of reassurance. While companies founded in the Bay Area rarely move their headquarters, their workforces tend to become much more geographically dispersed as they grow.

Just because a company is based in Northern California doesn’t mean most workers are there also. Headquarters, our survey shows, does not always translate into headcount.

“Headquarters location can often be the wrong benchmark to use to identify where employees are located,” said Steve Cadigan, founder of Cadigan Talent Ventures, a Silicon Valley-based talent consultancy. That’s particularly the case for large tech companies.

Among the largest technology employers in Northern California, Crunchbase News found most have fewer than 25 percent of their full-time employees working in the city where they’re headquartered. We lay out the details for 10 of the most valuable regional tech companies in the chart below.

With the exception of Intel, all of these companies have a double-digit percentage of employees at headquarters, so it’s not as if they’re leaving town. However, if you’re a new hire at Silicon Valley’s most valuable companies, it appears chances are greater that you’ll be based outside of headquarters.

Tesla, meanwhile, is somewhat of a unique case. The company is based in Palo Alto, but doesn’t crack the city’s list of top 10 employers. In nearby Fremont, Calif., however, Tesla is the largest city employer, with roughly 10,000 reportedly working at its auto plant there.(Tesla has about 49,000 employees globally.)

High-valuation private and recently public tech companies can also be pretty dispersed.

Although they tend to have a larger percentage of employees at headquarters than more-established technology giants, the unicorn crowd does like to spread its wings.

Take Uber, the poster child for this trend. Although based in San Francisco, the ride-hailing giant has fewer than one-fourth of its employees there. Out of a global workforce of around 22,300, only about 5,000 are SF-based.

It’s unclear if that kind of breakdown is typical. We had trouble assembling similar geographic employee counts at other Bay Area unicorns, mainly because cities break out numbers only for their 10 largest employers. The lion’s share of regional unicorns are San Francisco-based, and of them only Uber made the Top 10.

That said, there is another, rougher methodology for assessing who works at headquarters: job postings. At a number of the most valuable Bay Area-based unicorns — including Airbnb, Juul, Lime, Instacart, Stripe and the now-public Lyft — a high number of open positions are far from the home office. And as we wrote last year, private companies have been actively seeking out cities to set up secondary hubs.

Even for earlier-stage startups, it’s not uncommon to set up headquarters in the San Francisco area for access to financing and networking, while doing the bulk of hiring in another location, Cadigan said. The evolution of collaborative work tools has also enabled more companies to add staff working remotely or in secondary offices.

Plus, of course, unicorn startups tend to be national or global in focus, and that necessitates hiring where their customers are located.

As we wrap up, it’s worth bringing up how unusual it once was for denizens of a metro area to oppose a big influx of high-skill jobs. In the past couple of years, however, these attitudes have become more common. Witness Queens residents’ mixed reactions to Amazon’s HQ2 plans. And in San Francisco, a potential surge of newly minted IPO millionaires is causing some consternation among locals, along with jubilation among the realtor crowd.

Just as college towns retain room for new students by graduating older ones, however, it seems reasonable that sustaining Northern California’s strength as a startup hub requires locating jobs out-of-area as companies scale. That could be good news for other cities, including Austin, Phoenix, Nashville, Portland and others, which have emerged as popular secondary locations for fast-growing unicorns.

That said, we’re not predicting near-term contraction in Bay Area tech employment, particularly of the startup variety. The region’s massive entrepreneurial and venture ecosystem keeps on producing valuable newcomers well-capitalized to keep hiring.

Methodology

We looked only at employment at company headquarters (except for Apple) . Companies on the list may have additional employees based in other Northern California cities. For Apple, we included all Silicon Valley employees, per estimates by the Silicon Valley Business Journal.

Numbers are rounded to the nearest hundred for the largest employers. Most of the data is for full-time employees only. Large tech employers hire predominantly full-time for staff positions, so part-time, whether included or not, is expected to reflect only a very small percentage of employment.

Cities list their 10 largest employers in annual reports. We used either the annual reports themselves or data excerpted in Wikipedia, using calendar year 2017 or 2018.

Powered by WPeMatico

TechCrunch’s Connie Loizos published some interesting stats on seed and Series A financings this week, courtesy of data collected by Wing Venture Capital. In short, seed is the new Series A and Series A is the new Series B. Sure, we’ve been saying that for a while, but Wing has some clean data to back up those claims.

Years ago, a Series A round was roughly $5 million and a startup at that stage wasn’t expected to be generating revenue just yet, something typically expected upon raising a Series B. Now, those rounds have swelled to $15 million, according to deal data from the top 21 VC firms. And VCs are expecting the startups to be making money off their customers.

“Again, for the old gangsters of the industry, that’s a big shift from 2010, when just 15 percent of seed-stage companies that raised Series A rounds were already making some money,” Connie writes.

As for seed, in 2018, the average startup raised a total of $5.6 million prior to raising a Series A, up from $1.3 million in 2010.

Now on to IPO updates, then a closer look at all the companies raising big rounds. Want more TechCrunch newsletters? Sign up here. Contact me at kate.clark@techcrunch.com or @KateClarkTweets.

![]()

Slack: The workplace communication software provider dropped its S-1 on Friday ahead of a direct listing. That’s when companies sell existing shares directly to the market, allowing them to skip the roadshow and minimize the astronomical fees typically associated with an initial public offering. Here’s the TLDR on financials: Slack reported revenues of $400.6 million in the fiscal year ending January 31, 2019, on losses of $138.9 million. That’s compared to a loss of $140.1 million on revenue of $220.5 million for the year before. Slack’s losses are shrinking (slowly), while its revenues expand (quickly). It’s not profitable yet, but is that surprising?

Zoom was the Slack we thought Slack was all along.

— alex (PVD) (@alex) April 26, 2019

Uber: The ride-hail giant is fast approaching its IPO, expected as soon as next week. On Friday, the company established an IPO price range of $44 to $50 per share to raise between $7.9 billion and $9 billion at a valuation of approximately $84 billion, significantly lower than the $100 billion previously reported estimations. The most likely outcome is Uber will price above range and all the latest estimates will be way off course. Best to sit back and see how Uber plays it. Oh, and PayPal said it would make a $500 million investment in the company in a private placement, as part of an extension of the partnership between the two.

There are a lot of fascinating companies raising colossal rounds, so I thought I’d dive a bit deeper than I normally do. Bear with me.

Carbon: The poster child for 3D printing has authorized the sale of $300 million in Series E shares, according to a Delaware stock filing uncovered by PitchBook. If Carbon raises the full amount, it could reach a valuation of $2.5 billion. Using its proprietary Digital Light Synthesis technology, the business has brought 3D-printing technology to manufacturing, building high-tech sports equipment, a line of custom sneakers for Adidas and more. It was valued at $1.7 billion by venture capitalists with a $200 million Series D in 2018.

Canoo: The electric vehicle startup formerly known as Evelozcity is on the hunt for $200 million in new capital. Backed by a clutch of private individuals and family offices from China, Germany and Taiwan, the company is hoping to line up the new capital from some more recognizable names as it finalizes supply deals with vendors, according to reporting from TechCrunch’s Jonathan Shieber. The company intends to make its vehicles available through a subscription-based model and currently has 400 employees. Canoo was founded in 2017 after Stefan Krause, a former executive at BMW and Deutsche Bank, and another former BMW executive, Ulrich Kranz, exited Faraday Future amid that company’s struggles.

Starry: The Boston-based wireless broadband internet startup has authorized the sale of Series D shares worth up to $125 million, according to a Delaware stock filing. If Starry closes the full authorized raise it will hold a post-money valuation of $870 million. A spokesperson for the company confirmed it had already raised new capital, but disputed the numbers. The company has already raised more than $160 million from investors, including FirstMark Capital and IAC. The company most recently closed a $100 million Series C this past July.

Selina & Sonder: The Airbnb competitor Sonder is in the process of closing a financing worth roughly $200 million at a $1 billion valuation, reports The Wall Street Journal. Investors including Greylock Partners, Spark Capital and Structure Capital are likely to participate. Sonder is four years old but didn’t emerge from stealth until 2018. The startup, which turns homes into hotels, quickly attracted more than $100 million in venture funding. Meanwhile, another hospitality business called Selina has raised $100 million at an $850 million valuation. The company, backed by Access Industries, Grupo Wiese and Colony Latam Partners, builds living/co-working/activity spaces across the world for digital nomads.

Fresh funds: Mary Meeker has made history with the close of her new fund, Bond Capital, the largest VC fund founded and led by a female investor to date. Bond has $1.25 billion in committed capital. If you remember, Meeker ditched Kleiner Perkins last fall and brought the firm’s entire growth team with her. Kleiner said it was a peaceful split that would allow the firm to focus more on its early-stage efforts, leaving the growth investing to Bond. Fortune, however, reported this week that a power struggle of sorts between Meeker and Mamoon Hamid, who joined recently to reenergize the early-stage side of things, was a larger cause of her exit.

Plus, SOSV, a multi-stage venture firm that was founded as the personal investment vehicle of entrepreneur Sean O’Sullivan after his company went public in 1994, has raised $218 million for its third fund. The vehicle has a $250 million target that SOSV expects to meet. Already, the fund is substantially larger than the firm’s previous vehicle, which closed with $150 million.

A grocery delivery startup crumbles: Honestbee, the online grocery delivery service in Asia, is nearly out of money and trying to offload its business. Despite looking impressive from the outside, the company is currently in crisis mode due to a cash crunch — there’s a lot happening right now. TechCrunch’s Jon Russell dives in deep here.

Extra Crunch: “When it comes to working with journalists, so many people are, frankly, idiots. I have seen reporters yank stories because founders are assholes, play unfairly, or have PR firms that use ridiculous pressure tactics when they have already committed to a story.” Sign up for Extra Crunch for a full list of PR don’ts. Here are some other EC pieces to hit the wire this week:

Equity: If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about Kleiner Perkins, Chinese IPOs and Slack & Uber’s upcoming exits.

Powered by WPeMatico