Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

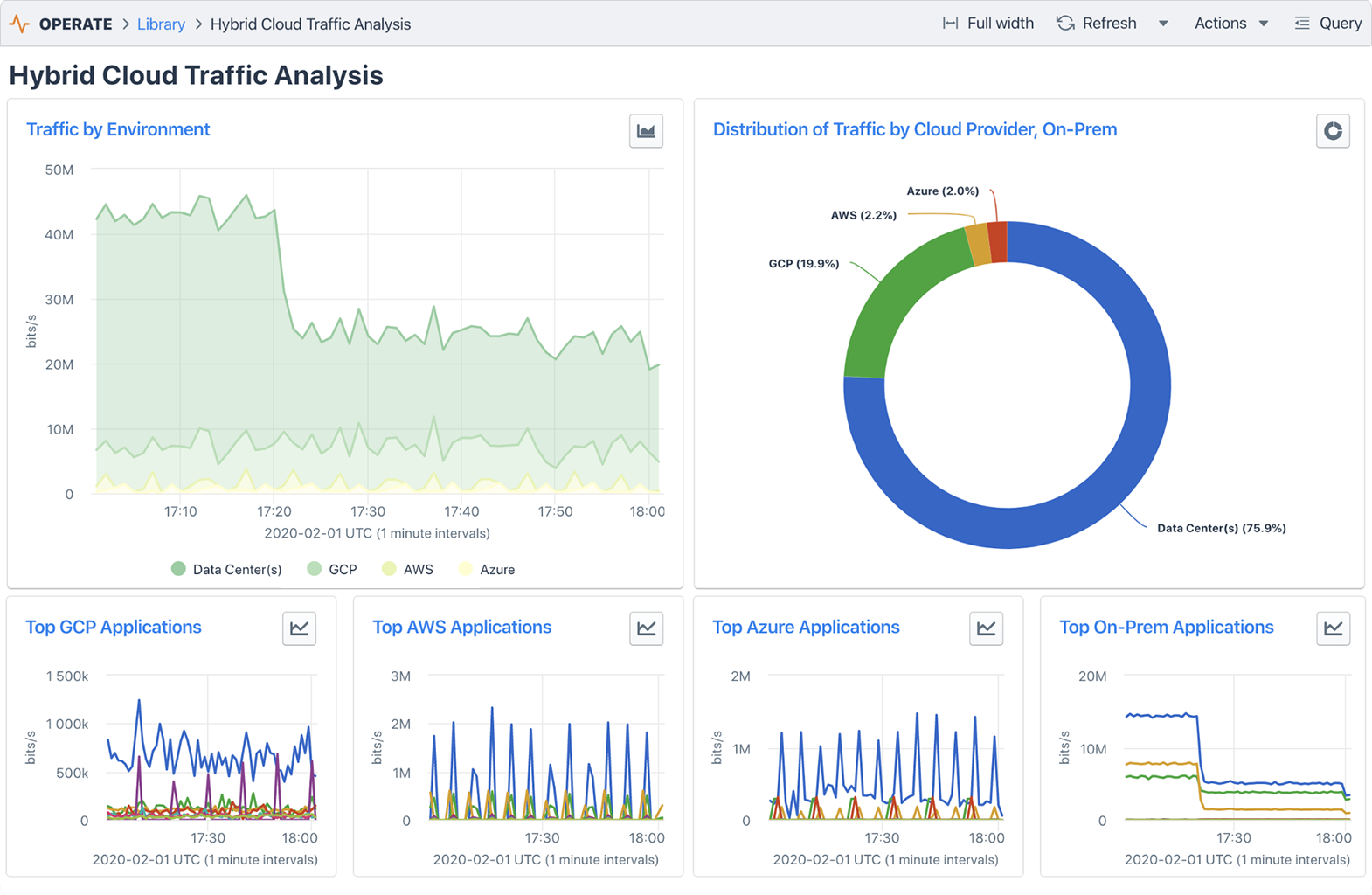

Kentik, the company once known as CloudHelix, today announced that it has raised a $23.5 million growth funding round led by Vistara Capital Partners, with existing investors August Capital, Third Point Ventures, DCVC and Tahoma Ventures also participating. With this round, Kentik has now raised a total of $61.7 million.

The company’s platform allows enterprises to monitor their networks, no matter whether that’s over the internet, inside their own data centers or in public clouds.

“The world has become even more internet-centric, and we are seeing growth in traffic levels, product engagement and revenue across both our enterprise and service provider customers,” said Avi Freedman, the co-founder and CEO of Kentik when I asked him why he was raising a round now. “We’ve seen an increased pace of adoption of the kind of hybrid and internet-centric architectures that Kentik is built for and thought it was a great time to increase investment, especially in product, as well as go-to-market and partner expansion to support market demand.”

Freedman says the company has been growing 100% compounded year-over-year since it launched in 2015 and now has customers in 25 countries. These include leading enterprises, SaaS companies, content providers, gaming companies, content providers and cloud and communication service providers, he tells me. Current customers include the likes of IBM, Zoom, Dropbox, eBay, Cisco and GoDaddy.

The company says it will use the new funding to invest in its product and for go-to-market investments.

One notable fact about this new round is that it is a combination of equity and growth debt. Why growth debt? “Growth debt is an attractive option for startups with the right scale and strong unit economics, especially with the changes to capital markets in response to current economic conditions,” said Freedman. “Another element that makes long-term debt attractive is that unlike equity financing, long-term debt limits dilution for everyone, but especially benefits our employees who hold common stock.” That, it’s worth noting, is also something that lead investor Vistara Capital has made one of the core tenets of its investment philosophy. “Since Kentik is now at a scale where we have enough data on the business fundamentals to be able to make growth investments using debt while still being able to repay it over time, it made sense to us and our investors,” noted Freedman.

Powered by WPeMatico

Corporate venture capitalists (CVCs) are booming in the startup space as large companies look to take advantage of the fast-paced innovation and original thinking that entrepreneurs offer.

For startups, taking funding from CVCs can come with many benefits, including new opportunities for marketing, partnerships and sales channels. Still, no founder should consider a corporate investor “just another VC.” CVCs come with their own set of priorities, strategic objectives and rules.

When it comes to choosing a CVC with which to enter negotiations, the most important step is doing your own diligence beforehand. An entrepreneur’s goal is to find the perfect match to partner with and guide you as you grow your business. So before you start discussing terms, you’ll want to understand what’s driving the CVC’s interest in venture investing.

While traditional VCs are purely financially driven, CVCs can be in the venture game for a variety of reasons, including finding new technology that might generate marketplace demand for their products. An example is Amazon’s Alexa fund, which invested into emerging companies that drive use and adoption of Alexa. Alternatively, a CVC’s parent company may be looking to invest in tech that will help them operate their own products more efficiently, such as Comcast Ventures investing in DocuSign.

As a rule of thumb, the bigger CVC funds like GV and Comcast tend to be financially driven, meaning they’ll be approaching negotiations through a financial lens. As such, the negotiating process more closely resembles an institutional fund. You as a founder have to do the work to figure out what’s driving your CVC — is this a customer acquisition or distribution opportunity? Or are they seeking to find a source of knowledge transfer and/or bring new tech into their parent company?

“Before negotiating, always look at a CVC’s existing portfolio,” says Rick Prostko, managing director at Comcast Ventures. “Have they made a lot of investments, at what stage, and with whom? From this information you’ll see the strategic thinking of the CVC, and you can determine how best to position yourself when you begin negotiations.”

Powered by WPeMatico

Corporate venture capital (CVC) is booming, with more than $50 billion of CVC capital deployed in 2018. The rise in capital expenditures by CVCs between 2013 and 2018 was an impressive 400%, according to Corporate Venturing Research Data. There are currently more than a hundred active CVC investors, and some sources suggest that almost half of all venture rounds include a strategic investor.

This rise has been driven by two factors: 1) the tech landscape is moving at a faster pace and bigger companies know they need to innovate quicker to meet market demand; and 2) the number of startups seeking CVC capital is growing as founders look beyond traditional venture funds to help grow their businesses.

Kruze Consulting and Goodwin have worked with hundreds of startups through the funding process, including those working with CVCs. Together, the two firms and their principals have decades of experience advising founders during and after their capital raises.

To help startups navigate CVC transactions, we’ve created a guide to working with CVCs. In this segment, we’ll discuss the types of CVCs, the best way to approach each type and the key things to keep in mind during initial discussions.

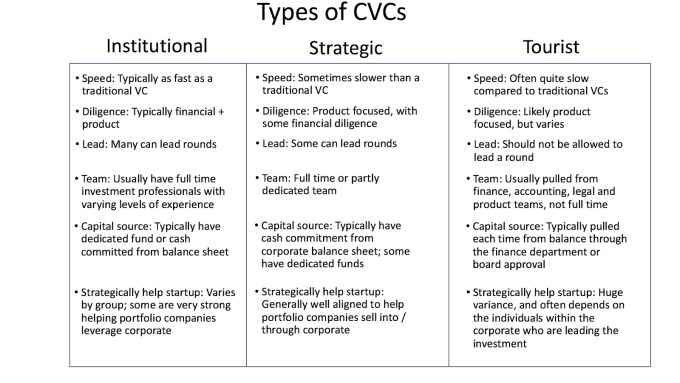

Roughly put, CVCs fall into three categories:

As the realm of CVCs becomes increasingly professionalized, more and more CVCs fall into the first category. For entrepreneurs seeking CVC investors, those in the institutional or strategic category can provide tremendous value — though it’s important that a startup know which type of CVC they’re speaking to, and have clear objectives going in that align with the CVC’s goals and strengths.

Before engaging with a CVC, or any potential investor for that matter, the most important step is to do your research. Who is the individual you’re meeting with? What’s his/her background and what deals has he/she done with this venture group? These are Must Knows before walking into the initial meeting.

Once you’re in early discussions, ask the CVC whether he or she has carry in the fund and whether the venture arm is autonomous. The answers to these questions will help you clarify whether you’re dealing with institutional versus strategic CVCs.

“With corporate-backed venture funds, it’s really key up front to know who you’re talking to,” says Allen. “It’s dangerous to call all groups that are nontraditional investors ‘CVCs’ since some are far more serious than others. Most have some degree of strategic mandate but many are increasingly investing for financial gain.”

The next question is: Are you dealing with a financially driven CVC or a strategically driven one? From a founder’s standpoint, you’ll need to know whether you’re meeting with an investor who views deals through the lens of, “I’m looking for a great team, huge market and a chance to bring in funding and connections to make a business as strong as it can be” or, “I’m looking for a solution/product/platform that I can bring into my company or use to expose my company to a brand new marketplace or technology.”

Once again, the way to determine which type of CVC you’re dealing with is to ask the right questions. In the first meeting, ask about their investment process, how investments are made and whether strategic business unit sponsorship is required for a given deal. The answers will tell you whether the CVC falls into Group 1 or 2, and you’ll be in a strong position to then make choices about whether this potential investor is right for you.

“Look for someone who will understand your business, meet with you and decide that there’s something beyond just capital that will form the basis for that relationship,” says Rick Prostko, managing director at Comcast Ventures. “In today’s venture market, founders want money AND value. Seek out a CVC who has valuable experience to provide, and look for someone who’s been an operator in this segment previously or who has valuable insight and experience to offer.”

Once you’ve done your initial diligence, developed a relationship and determined that a CVC could be a strong investor in your business, there are important factors to be aware of as you move into the next stage of discussions. These include:

Expect deeper product and technical diligence. CVCs can call on technical, product and market experts within their corporation during the due diligence process. As such, their level of product diligence is typically more rigorous than traditional VCs. Be prepared for some grilling by subject matter experts. On the flip side, this diligence process provides you with exposure to potential customers and partners inside the corporation, so use this time to your advantage.

Be aware that you’re going to share confidential information with a large company. “CVCs know that you’re only as good as your reputation,” says Eric Budin, director at Touchdown Ventures . “As such, there are very few examples of CVCs abusing confidential information, because news of it would get around so quickly.”

Still, for a founder, the goal is to be thoughtful and strategic with what you share, and to determine whether the CVC is truly interested in doing a deal before you hand over financial, technical and competitive information. It’s possible that commercial teams at the CVC sponsor could gain unfair advantage from seeing your information, or use their CVC to gain valuable intel on the competition.

On the other hand, sharing your intel could be a fantastic way to get in front of an internal team at the parent company. The key is to think carefully about what you are being asked to share and with whom, and set ground rules with the CVC before they begin diligence.

“It’s important to understand how the corporate fund is structured and how they handle any information that’s shared,” says Prostko. “It might be in your interest to loop in a business unit [within the parent company] that could benefit from learning about your business. On the flip side, if the CVC is a potential competitor, you’ll want to be more careful about what you reveal.”

There will be a risk of regime change. Large companies operate like, well, large companies. People leave, management changes happen and priorities shift. At the outset, ask questions such as: Who will support your company if the commercial manager leading your investment leaves? What will happen to the CVC if the person leading the venture arm is fired? Will they do their pro-rata if the person leading your deal is gone? What happens to any commercial relationships that you might be working on? It’s important to have a keen understanding of internal dynamics before you enter the relationship.

“In general, the more successful a firm is, the more likely the CVC will stick around,” says Allen. “Be sure to look at the individual’s history at the firm, how long he or she has been there, and whether he or she has jumped from fund to fund. If the investing partner has come out of the corporate ‘mother ship,’ and lacks any credible venture experience, buyer beware.”

The CVC may be subject to regulatory rules. Depending on the industry, government regulations may impact how your deal is structured. Banks, for example, are subject to rules that can restrict the percentage of voting stock they can own. Foreign investors may need to comply with CFIUS regulations if your company provides certain specified technologies. Generally, the CVCs will understand the regulations that apply to them. They may not, however, bring them up until late in the process, which could lead to delays.

Commercial transactions with the corporate arm can slow things down. Purely strategic CVCs (Group 2) often require a commercial transaction to happen in connection with a venture deal. The process involved in these transactions often takes longer than the financing process, which can cause issues if the CVC is a key (but not sole) investor in the round. If you’re dealing with a Group 2 CVC, discuss this issue ahead of time to see if you can decouple the two transactions and close the investment prior to inking the commercial deal.

CVCs offer a wealth of capital, human resources and corporate partnerships for startups. But whether you choose to take CVC capital or not, you can benefit from merely approaching CVCs if you have business units operating in either the same space or a tangential space. An initial meeting both gives you an opportunity to do a sales pitch and offers the CVC a chance to vet a product or team and gain some deal insight. For founders, you gain a powerful sales opportunity that might have otherwise taken months or years to obtain.

“Even if you’re told ‘no’ by a CVC, the meeting could result in a good business relationship that could turn into a sales opportunity for you in the near future,” says Prostko.

The WRONG way to think about approaching CVC investors is something along the lines of, “I can’t raise what I want from financial VCs so I’ll go to CVCs as my second choice, since they’re more likely to say ‘yes’ and/or give me better terms.” This attitude will shut doors and cut you off from valuable partners, capital and opportunities to strategically grow your business.

Above all, stay informed as you choose whom to bring in as a partner. Ultimately, it’s your business and the responsibility to ensure that you bring in the right capital partners lies with you.

Powered by WPeMatico

The novel coronavirus has been devastating for many people, families and communities — and the consequences are still being calculated. The tech world has seen wave after wave of layoffs, sometimes multiple waves at one company only weeks apart. Some startups have lost nearly all their revenue, and depending on their cash reserves, have little hope of recovering.

For VCs, the last two months have been an exercise in triage.

Partners have gone through their entire investment portfolios to identify the winners, what’s salvageable and what (at least in their minds) has no hope of resuscitation. If you are in the first two groups, it’s back to whatever normal looks like in the midst of a global pandemic and a deep economic recession.

But what if you suddenly get a call informing you that your investor — perhaps your biggest champion to date — is going to cut the rope and write you off entirely?

That’s what we are going to talk about today.

Before we go anywhere, be thankful if you even know how your investors are judging your startup. Most, unfortunately, will couch the terms they use (“we will be engaging less” or perhaps “we are unlikely to do our pro rata going forward”) rather than just saying directly, “we are writing you off; don’t call us — we’ll call you.” That’s polite and face-saving for all parties, but the lack of transparency can make decisions down the road much harder. It’s better to know where you stand, even if the news is hard.

The first step to approaching this situation is to get your bearings. Much like during a fundraise process, it’s not uncommon for different investors on your cap table to reach different conclusions about your startup’s potential. One investor may write you off, while another has you marked at a more neutral valuation or even positively. This can absolutely be frustrating, and given the emotion of this situation, it can be hard to rationally accept that an investor who once believed in you no longer does so.

Powered by WPeMatico

By the summer of 2016, Marie Outtier had spent eight years as a consultant advising media agencies and martech companies on marketing growth strategy.

Pierre-Jean “PJ” Camillieri started as a music software engineer before joining one of Apple’s consumer electronics divisions. Inspired by Siri, he left to start Timista, a smart lifestyle assistant.

When the two joined forces to co-found Aiden.ai, the combination was potent — one was a consummate marketer, the other, a specialist in machine learning. Their goal: create an AI-driven marketing analyst that offered actionable advice in real time.

Humans who manage ad campaigns must analyze vast amounts of numbers, but Outtier and Camillieri envisioned a tool that could make optimization recommendations in real time. Analytics are vast and unwieldy, so theirs was a no-brainer proposition with a market crying out for solutions.

The company’s first office was at Bloom Space in Gower Street, London. It was just a handful of hot desks and a nearby sofa shared with four other startups. That summer, they began in earnest to build the company. A few months later, they had a huge opportunity when the still 100% bootstrapped company was selected for Techcrunch Disrupt’s Startup Battlefield competition.

Interviewed by TechCrunch, they explained their proposition: Marketers wanted to know where a digital marketing campaign was getting the most traction: Twitter or Facebook. You might need to check several dashboards across multiple accounts, plus Google analytics to compile the data — and even if you conclude that one platform is outperforming the other, that might change next week as users shift attention to Instagram, potentially wasting 60% of ad spend.

Aiden was intended to feel like just another co-worker, relying on natural language processing to make the exchange feel chatty and comfortable. It queried data from multiple dashboards and quickly compiled it into flash charts, making it easy to find and digest.

Eventually, instead of managing 10 clients, marketing analysts would be able to manage 50 using dynamic predictions as well as visualizations. Aiden incorporated Outtier’s expertise into its algorithms so it could suggest how to tweak a Facebook campaign and anticipate what was going to happen.

Was appearing at Disrupt a significant moment? “It was a big deal for us,” says Outtier. “The exposure gave us ammunition to raise our first round. And being part of the Disrupt Battlefield alumni gave us many meaningful networking and PR opportunities.”

A few weeks later the company had raised a seed round of $750,000. But not without difficulty. By this time Outtier was in the latter stages of pregnancy. Raising money under these circumstances was difficult, but, she says, “it can be done. It’s tougher than ‘normal circumstances.’ It’s a bit like running a marathon, but with a fridge on your back.”

Powered by WPeMatico

opportunity")

Every time we realize something new about the coronavirus, it’s always worse than we thought: maybe we don’t develop immunity to it; maybe six feet of social distancing isn’t far enough; maybe the spread won’t wane in warmer weather.

Every time we realize something new about the economy, it’s equally bleak: maybe we can’t safely reopen for months (Georgia and South Carolina notwithstanding), maybe unemployment will top Great Depression levels, maybe travel won’t resume till mid-2021, maybe most of the businesses who have shuttered their doors will never return.

But like everything in life, within all of the bad, there’s usually some good too. And for businesses who have to deal with regulation, this may be an unusually good time to get what you need.

The federal government does not have to balance its budget, which is why multi-trillion dollar legislation like the CARES Act is possible. But cities and states have to produce a budget every fiscal year that at least looks balanced on paper. In good times, that leads to lots of new spending. But in bad times, it requires a painful series of cuts, tax and fee increases and tough decisions that are normally avoided by politicians at all costs. All of that creates opportunity for startups.

Local government will desperately need new sources of revenue. Figuring out what a politician is going to do isn’t that difficult: identify the choice with the least political downside and that’s almost always the answer. That’s why controversial policy issues like legalizing mobile sports betting or recreational marijuana often stall in state legislatures when the budget is flush (disclosure, we’re investors in FanDuel) . But now, lawmakers face a very different situation: to balance the budget, they will either need to enact deep spending cuts, raise fees and taxes, or find new sources of revenue. All of a sudden, legalizing gambling and drugs doesn’t seem so risky, politically or substantively.

Any company that can offer material new tax revenues can now see their product or service legalized and permitted in a fraction of the time it would normally take. Companies who can offer direct savings to government can now secure contracts and win procurements at a rapidly faster clip. A broke government is a friendly government. This is the moment to be aggressive.

It was less than a year ago when Amazon tried to build its second headquarters in New York City.

Despite strong support from Governor Andrew Cuomo and tepid support from Mayor Bill de Blasio, the project was widely derided as an unfair corporate boondoggle and Amazon was swiftly run out of town. In good economic times, voters have the luxury of focusing on issues that aren’t critical to their own day-to-day survival and politicians have the luxury of saying no to new jobs and tax revenue to try to score points with the base.

Not anymore. Startups in blue cities and states up and down both coasts have vastly more political leverage than they’ve had in years. Issues like privacy, worker classification reform and fears of AI are all about to take a back seat to pocketbook issues like jobs, crime and access to health care. Startups who can promise to retain jobs can now drive meaningful changes on policy, regulation, permitting, zoning, licensing and everything else they need to operate.

Startups that can offer solutions to living in a pandemic (digital payments, D2C, telemedicine, teleconferencing, tele-anything) will become shiny new toys that lawmakers want to be seen with. Delivery drones, autonomous cars, at home medical testing and other concepts that seem a little edgy will now become ideas that lawmakers have to seriously consider – if a new technology could potentially save lives during a pandemic, you really don’t want to be the politician who killed the idea.

Proposals to screw with startups won’t automatically become the top priority for the San Francisco Board of Supervisors. Facebook even now has a much stronger argument to lobby for Libra (no one in this climate wants to use cash if they can help it). The power dynamic just flipped on its head. But that only works if you understand it and take advantage of it.

In the continual debate over whether tech startups should ask government for permission or beg for forgiveness over the last few years, the zeitgeist has shifted significantly towards asking for permission. The tech-lash against Facebook, Google, Amazon, Apple and Twitter created regulatory headaches for virtually every tech company, even some early stage startups.

All of that just changed. Regulators and lawmakers now have far bigger things to worry about than whether an electric scooter needs a particular type of permit. And if saying no to new ideas from new companies means turning away desperately needed jobs and tax revenue, for all of the same reasons that it was politically salient for lawmakers to reclassify all California sharing economy workers as full time employees or reject Amazon’s overtures or limit the spread of homesharing, the opposite is now true.

Now you get points for creating jobs and avoiding spending cuts. Now you’re far more reticent to tell a constituent that they can’t make a few extra bucks by renting out a room (assuming anyone ever travels again). The label of job killer will start to become politically toxic, even in the most progressive wards, districts and neighborhoods in the bluest cities on each coast. The dynamic is clearly shifting back to begging for forgiveness (don’t be stupid and do things that are clearly illegal but interpreting gray areas of regulation as friendly is now a lot easier).

Unlike the financial crisis in 2008, businesses are not the culprit here. Tech companies are actually even some of the heroes of fighting the coronavirus. But most important, being punitive towards startups is no longer a clear political winner, even in the most liberal cities and states. Even if it seems counterintuitive, now is exactly the time for startups to aggressively seek policy change and regulatory relief.

Politics is about leverage. Startups now have it. They should take advantage of it before things change again.

Powered by WPeMatico

Despite all evidence to the contrary, there’s more to building a startup than raising venture capital.

Founders are finding success without overly relying on VC dollars; some are even sharing profits with their respective employees and customers without the help of traditional funding and Silicon Valley power dynamics.

As some investors slow down their funding pace, it has become clear that profitability trumps funding and venture capital can only take a startup so far when the economy tanks and outside cash streams dry up.

In the Indie.vc portfolio, profitability is its driving force. In fact, its main criterion for funding is that a startup must be on a clear path to profitability with durable fundamentals like high gross margins or the ability to start charging for a product right away, as opposed to companies that need a significant amount of upfront investment for research and development.

Profitability, Indie.vc founder Bryce Roberts tells TechCrunch, needs to be a habit, and founders need to recognize that it’s not a switch they can just turn on. Startups looking to prioritize profitability need to start out as revenue-driven businesses that replace funding milestones with profitability goals.

“Genuinely, it’s not rocket science,” he says. “Profitability isn’t this crazy, elusive thing. It’s literally more achievable than a Series A round. It’s way more achievable than a Series B round. If you look at the kind of fall-off between those rounds, most entrepreneurs would be better off finding their path to profitability and scale.”

Indie.vc, which recently announced its latest batch of investments, advises founders to make sure they have what they need to be stable and then to create and measure value, Roberts says. That value, which differs depending on the company, must be quantifiable as some metric or revenue.

To do that, Roberts says founders should adopt a mindset where they’re focused on creating revenue opportunities, rather than cost savings. Indie.vc’s model also does not prioritize hiring ahead of growth, a strategy that seems to be working for its portfolio during the pandemic.

Powered by WPeMatico

For the vast majority of startup founders who were planning their capital raise in Q1 2020, the COVID-19 blow was so dramatic and sweeping, we cannot see all its effects at once.

One big question on the minds of most founders: How should we plan our next raise in terms of timing, valuation and amounts?

Sarah Guo, partner at Greylock Partners, says the fundraising environment has slowed down significantly, but founders who have built ties with VCs via informal coffee updates and check-ins are at a clear advantage. “Early-stage bets require relationship-building,” says Guo, who has been investing in seed through Series B rounds.

Ram Shanmugam, founder and CEO of AutonomIQ*, a seed-stage code and process automation company, has been strengthening his relationships. For a company that has low operating expenses and a community of 600,000 developers, he says he is not fazed. “Our automation code brings efficiencies and in fact, we have nine inbound leads in Q2. Having said that, we are being realistic at the pace at which we can close these contracts.”

Similarly, Fred Blumer, who exited Hughes Telematics at an enviable $750 million, says he is taking a more pragmatic approach to the Series A raise for his new company, Mile Auto. “We expect to have a 5x growth in our business in 2020, even after adjusting for COVID,” he said. “Our pay-per-mile insurance is a great fit for people who are driving less.” Because so many drivers are sheltering in place, legacy insurance companies are refunding hundreds of millions of dollars to customers, which offers an advantage (and an opportunity) to a startup like his.

“But we need to be patient and mindful. While our families, health and safety are top priority, we are staying focused on our customers,” Blumer said. “Insurtech is a resilient arena, and in my past company we raised $100 million, so working with investors has never been a challenge. Keeping up with growth and perfecting the customer experience are what keep us up at night.” He said he plans to get out in the market after investor confidence returns.

Which may be a good idea, considering Jason Lemkin’s Twitter survey, where only 32% of respondents said they plan to deploy the same amount of capital as in the past. But another 30% are on the opposite end of the spectrum, deploying 40% to 60% less capital.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re taking a look at a bit of data on the European venture capital scene in Q1. As with our looks at other locales like Silicon Valley and other bits of the United States, we’re taking stock of what happened in the first quarter. Q1 2020 includes pre-COVID-19 results, though as some European countries began to lock-down before the United States, there may be more pandemic-impact in the following results than we’ve seen domestically thus far.

Today’s grip of data is via the folks over at PitchBook, who compiled a venture-focused dig through the continent’s first three months of the year. Let’s parse the top numbers, make a comparison or two and then look to what’s next.

Despite COVID-19, China’s broad shuttering and an aged bull market deep, Europe’s venture capital activity in Q1 2020 was mostly fine. It wasn’t great, and there were some less-than-winsome results that could be chalked up to the pandemic, but the first quarter provided an alright start to the year.

Powered by WPeMatico

In a message posted to its internal communications channel earlier this week, the massive startup accelerator Y Combinator said it will change the terms of its own PPP (the YC pro rata investment program) and investing in companies raising seed and Series A rounds on a case-by-case basis.

The company began a policy of investing in every seed and Series A round for its portfolio companies back in 2015.

Since then, it has taken a 7% stake in every company that raised a priced seed and Series A round, investing in more than 300 Y Combinator companies over nearly 500 rounds.

Under its new policy, the accelerator is reducing its investment size from 7% to 4% and is only investing on a case-by-case basis going forward.

The reason for the change is that the number of companies in its portfolio has gotten too large for it to invest and some of the limited partners who back the accelerator’s operations are balking at making commitments to the pro rata investment program.

“We have significantly exceeded the funds we raised for pro ratas, and the investors who support YC do not have the appetite to fund the pro rata program at the same scale,” the accelerator wrote in a post seen by TechCrunch. “In addition, processing hundreds of follow-on rounds per year has created significant operational complexities for YC that we did not anticipate. Said simply, investing in every round for every YC company requires more capital than we want to raise and manage. We always tell startups to stay small and manage their budgets carefully. In this instance, we failed to follow our own advice.”

For entrepreneurs who take investments from the accelerator, the change is pretty significant. On the accelerator’s internal messaging board they worried about the potential optics of having the accelerator not make a follow-on commitment.

YC addressed those concerns by saying it would not make an investment decision until a company had already received an initial term sheet from a lead investor.

The changes will take effect on May 8, 2020, the investor said.

“In the future, we will no longer invest automatically in every priced seed and Series A/B round. Instead, we will exercise pro rata rights on a case-by-case basis, like other investors on your cap table,” the accelerator wrote. “We’ve heard your feedback that YC’s pro rata allocation is bigger than what some of you would prefer. So for those investments we do make, we will reduce the size of our pro rata and simplify its calculation to be a flat 4% participation right in each priced round. To calculate the size of YC’s pro rata investment in your round, simply multiply the amount of capital you are raising by 4%. If our ownership right before the round is less than 4%, we will cap our investment in the round at our then-current ownership. Our intention is not to have a super pro-rata right.”

Even with the reduced investment size, YC said it would only make investments in roughly one-third of its portfolio.

“The YC Continuity team will manage these investment decisions and will work very hard to inform you within a day or two of receiving your materials,” the accelerator wrote. “We will honor any pending pro rata investments for term sheets signed before May 8. But we wanted to communicate this message broadly so that founders can plan accordingly.”

Powered by WPeMatico