Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

As silently and swiftly as it has devastated families and communities around the world, COVID-19 has also left many startups gasping for air. Emerging companies with strong 2020 revenue forecasts have seen their high-confidence plans reduced by 60%-80% in a matter of days. Even in the best of times, startups must reach value-unlocking milestones to successfully raise new capital. But today, a globally synchronized halt to business activity has made irrelevant normal benchmarks for financing rounds.

Obtaining payroll support from the recently enacted special government programs for small businesses will not resolve the cascading problems startups are grappling with, regardless of whether or not they are VC-backed.

Product development roadmaps in many innovation-driven industries are changing in ways that may permanently alter a company’s future strategic direction. Merger and acquisition discussions are being shelved. Normal financing rounds, in process and contemplated, are contracting or being abandoned altogether. Many venture funds, including corporate venture programs, have unilaterally “taken a pause” to reevaluate the radically changing landscape for their early-stage company portfolios.

I last experienced this phenomenon in the aftermath of the Great Technology Bubble: 2002-2003. And all signs show that we are at the beginning of a new round of punitive “incentives” for venture investors to keep their companies alive.

Several of my current portfolio companies have recently proposed “emergency bridge” convertible note financings of between $5 million and $15 million, each featuring a painful feature for non-participants: multiple liquidation preferences benefiting only the new money above 3x, with discounts greater than 20% on conversion in a new equity financing. Of course, these financings are open to both existing and new investors. But the likelihood of another round is actually diminished by this type of structure.

Powered by WPeMatico

Marty Pichinson gets called a lot of things: Silicon Valley’s undertaker, its terminator, a grave digger. These aren’t meant as slights; Pichinson is the founder of Sherwood Partners, a restructuring firm that Bay Area venture firms frequently turn to when they need someone to help sell off the assets of startups they have funded. The idea is to return at least some money to the company’s creditors and, if anything is left, to the VCs, too.

We last checked in with Pichinson almost exactly three years ago when the startup world was humming along. Even then, because of the sheer number of companies that get funded — and thus the number of startups that invariably don’t make it — Sherwood Partners was helping to wind down two to four companies a week.

Now, as he told us in conversation last week, it’s winding down two to three companies every day.

So who is shutting down, how does it all work and what can VCs expect to get in terms of a return in the age of the coronavirus?

Right now, Pichinson says the shutdowns are across verticals and across stages. “We’re in companies that raised $10 million to $25 million, to companies that raised up to $1.5 billion. It doesn’t matter what size they are; when they come to us, they’re all broke. If we’re closing it down to clean up and monetize what we can, they are basically in the same position, whether they raised $20 million or they were once a billion-dollar business.”

Powered by WPeMatico

Frank, a New York-based student-facing startup, has raised $5 million in what the company described as an “interim strategic round” that Chegg, a public edtech company, took part in. According to Frank founder and CEO Charlie Javice, previous investors Aleph and Marc Rowan took part in the round alongside new investor GingerBread Capital.

The education funding-focused startup last raised known capital in December of 2017, when it closed a $10 million Series A. Frank raised a seed round earlier that same year worth $5.5 million.

According to Javice, her firm closed its round in early March, before the recent market carnage. Bearing in mind that there is always lag between when a funding round is closed and when it is announced, the new Frank round is on the fresher side of things. Most rounds are a bit more like Shippo’s recent investment (closed in December, announced in April) than Podium’s recent deal, which it started raising in mid-February of this year.

Timing aside, what Frank is doing is interesting, so let’s talk about its business, how it approached 2019 and how it’s faring in today’s changed market.

To help keep student debt low, Frank is a bit akin to TurboTax for college money, as TechCrunch wrote when covering its Series A, helping students get through a thicket of forms and aid to collect as much aid as possible while avoiding borrowing.

American higher education is too expensive, and applying for financial help is irksome and byzantine. I can safely report that sans quoting an expert, as I had to go through it as a student and only finished paying my student loans last July.

Frank wants to help make college more affordable, with the company noting in a call with TechCrunch that there’s been a good number of companies working to help students service debt in a less expensive way after they’ve hired the money; it wants to help students avoid taking on so much red ink in the first place.

According to Javice, lots of students fail to finish signing up for federal aid programs, and some students wind up dropping out of programs before finishing them, leaving them saddled with debt but no degree. That’s a hell of a trap to wind up in, as student loans are the barnacles of the financial world — incredibly hard to get rid of.

According to Javice, Frank was a little early to rethinking its own growth/profit trade-off than the rest of the startup world, which woke up when WeWork filed to go public and was quickly booed off Wall Street. In mid-2019, Frank slowed growth to get closer to the margins it wanted. (Thinking out loud, this is probably how the startup managed to survive so long off its December 2017 Series A.)

Indeed, according to Frank’s CEO, it was in a comfortable cash position before this round, which she described as more a vote of confidence than a round of necessity.

Which brings us to today, and the new, COVID-19 world. In an email to TechCrunch, Javice said that “like everyone else,” her company is “adjusting to the new realities.” She added that college and university attendance “has typically been countercyclical” and that her company is “seeing a large demand for higher education and specifically financial aid.”

If the new economy winds up creating a little tailwind for Frank, it won’t be the only startup to accrue help; Slack and Zoom and other remote work-friendly companies have also seen their fortunes turn for the better in recent weeks. And now with $5 million more on hand, it can certainly meet new demand.

Update: An earlier version of this article listed Chegg as the round’s lead investor; it did receive a board seat in the transaction but Frank does not consider it a lead investor. The post has been amended.

Powered by WPeMatico

A startup that has framed itself as an Instagram for websites is now squaring up against Shopify as it nabs new funding from Google’s venture capital arm.

Brooklyn-based Universe has just closed a $10 million Series A from GV. The funding round was well in the works before the COVID-19 pandemic took hold stateside; nevertheless, CEO Joseph Cohen definitely sounded relieved to have everything signed.

“Hopefully, it’ll take some weight off their shoulders that may have been there otherwise,” said GV general partner M.G. Siegler, who led the deal and is taking a seat on their board.

When the team launched out of YC two years ago, the initial aim was to be the go-to short link for young people and creatives to stick in their Instagram bios. The mobile app allowed users to create very basic landing pages, allowing them to type up some text, toss up photos and arrange their creation across a couple of web pages.

As the startup matures and looks to home in on a more robust business model, they’re now looking to build an incredibly low-friction commerce platform. Users can add a shopping “block” to their site, add a photo, description and price and then start accepting orders.

“We’ve gone from a landing page builder to a full-fledged website builder,” Cohen told TechCrunch in an interview.

Universe is going after what Cohen calls “very small businesses.” This could be an artist selling prints, a yoga instructor charging for Zoom classes or one of their latest customers, a farmer selling live bait. “These are people who don’t work at desks,” Cohen says.

Shopify has been one of the biggest tech success stories of the past several years, but Cohen sees weaknesses for Universe to capitalize on. Shopify is “complex and not mobile-first,” he says. Universe not only doesn’t require a developer to implement, it doesn’t seem to require someone that’s particularly tech-savvy.

The price of simplicity for the end user is a hefty cut for Universe. At launch, the company isn’t taking a percentage for the first $1,000 of a customer’s revenue, but will take a 10% slice thereafter, a number that’s notably multiples higher than the rates of competitors.

Cohen acknowledges that if a business succeeds, this can be a significant expense for them, one that might push them to another platform. He say that he wants to figure out a model that can help his startup “grow and scale” with their customers, but he didn’t offer up any details on what that might look like.

The team is still working with free and paid “pro” tiers that offer advanced features like analytics. Commerce features will be available for both tiers.

Universe has raised $17 million to date. Other investors include Javelin Venture Partners, General Catalyst and Greylock Partners.

We chatted with GV’s M.G. Siegler about closing this deal and how his role as an investor has shifted since the current crisis took hold. You can read that interview on Extra Crunch.

Powered by WPeMatico

The coronavirus pandemic has pushed entrepreneurs and investors into unknown territory.

Google’s GV just led a $10 million investment in Universe, a low-friction website builder that’s venturing into the world of commerce.

The investment was in the works before COVID-19 hit America in force, but things were finalized for the Brooklyn startup in late March. I chatted with M.G. Siegler, the general partner at GV (and former TechCrunch writer) who led the deal, about how the crisis was affecting his investment work and how he was balancing portfolio work with sourcing new deals.

This interview has edited for length and clarity.

TechCrunch: This deal sounds like it was in the works before pandemic concerns really hit America, but when you saw this situation arise, did it change your thinking about this deal at all?

M.G. Siegler: The reality is we’re still going to be continuing to look for interesting opportunities to invest in. History has shown that even during great financial turmoil, many companies are still being built, although it’s certainly not easy for anyone, given that we’re all stuck inside and trying to make things work. I think Universe is in an interesting spot; they have a tool that can potentially help some of these struggling businesses move online quicker and create commerce opportunities that they really need to think about given the current realities.

So there’s no thought that we shouldn’t do something just because of the current macro environment if we’re really passionate about it to begin with. Obviously, there’s varying degrees of that for different sectors, but I do think that Universe had been in a great position before this situation, and it seems like they have different opportunities now.

Powered by WPeMatico

Airbnb said Monday that it has raised $1 billion in debt and equity from private equity firms Silver Lake and Sixth Street Partners, even as the online rental marketplace has seen its business plummet due to the COVID-19 pandemic.

Terms of the deal were not disclosed. It’s unclear how this funding might alter Airbnb’s previously shared plans to go public.

COVID-19, the disease caused by coronavirus, prompted governments throughout the world to issue stay-at-home orders, triggering a wave of cancellations in the travel and hospitality industries. Airbnb emphasized that the funds would support its ongoing work to invest over the long term, a statement aimed at couching this raise as strategic and not a bailout in troubled times.

“While the current environment is clearly a difficult one for the hospitality industry, the desire to travel and have authentic experiences is fundamental and enduring,” Silver Lake co-CEO and managing partner Egon Durban said in a statement. “Airbnb’s diverse, global, and resilient business model is particularly well suited to prosper as the world inevitably recovers and we all get back out to experience it.”

Airbnb CEO Brian Chesky acknowledged Monday that while the desire to connect and travel has been reinforced during this time, the “way it manifests will evolve as the world changes.”

Airbnb is betting how and where people work will evolve. As a result, the company said it will direct its attention and new funds toward three core products: hosts, long-term stays and Airbnb experiences.

Last month, Airbnb said it would direct $250 million to help hosts who have been impacted by COVID-19. The funds will be used to pay a host 25% of what they would normally receive through their cancellation policy if a guest cancels a reservation due to COVID-19 between March 14 and May 31. Airbnb said this policy applies retroactively to all cancellations during that period.

The move was an attempt by Airbnb to make amends to its hosts who complained that the company’s policy would allow guests to cancel reservations and receive a full refund. That policy, which is still active, lets guests who booked reservations on or before March 14 that begin anytime on or before May 31 to cancel and receive a standard refund or travel credit.

Powered by WPeMatico

Many founders will have kicked off the new year with a new fundraising round. According to the data we shared last year, March, October and November were the months when VCs were reviewing the most decks.

But the COVID-19 pandemic has ground to a halt many industries, and there are even warnings that this will affect the next two quarters in regards to fundraising.

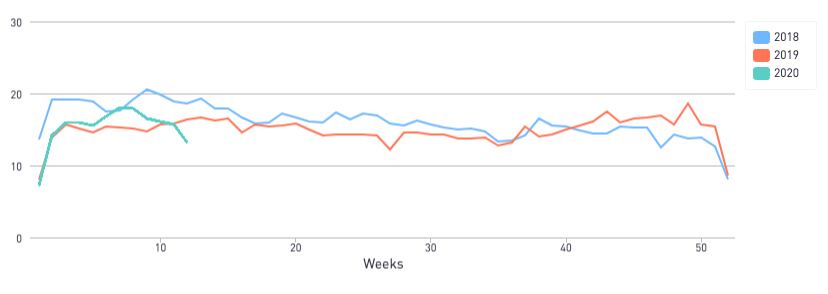

We’ve reviewed the data in our 2020 DocSend Startup Index and we’ve begun tracking the Pitch Deck Interest Metric. With San Francisco under a shelter-in-place order and many VCs scrambling to adjust their processes to an all-remote world, we saw pitch deck interest drop 11.6% when compared to the same week in 2019. While there has been a drop in interest so far, there is still a lot of activity, and VCs seem to still be reading pitch decks.

We will be monitoring the Pitch Deck Interest Metric in the coming weeks, but if you’re an early-stage startup and are in the middle of your fundraise, or are about to fundraise, there are some things you can do to help insure your startup is ready for funding before you meet with any (more) investors.

The Pitch Deck Interest Metric declined 11.6% compared to the same week in 2019

If you were about to kick off a fundraising round, you should have been prepared to contact 50 or more investors, have 20-30 meetings and spend somewhere around 20 weeks before you signed your term sheet. That’s a lot of time and energy to invest, especially when the economy is poised for a downturn and you’re most likely needed in other parts of your business.

If you’ve already started your round and are wondering if you should push through, I’ve written a piece on knowing when to quit and recalibrate versus when to push through (Extra Crunch membership required).

Many factors play into navigating a successful fundraising round, and the expectations of investors are constantly changing — specifically when it comes to the pre-seed round.

Investors are now looking for market-ready products and want to see pitch decks that feature the content they’re expecting. We expect to see this focus intensify over the coming months as VCs have more time to spend not just to review pitch decks, but on due diligence for companies in which they plan to invest. Our new report outlines advice for pre-seed startups that are looking to adjust their fundraising strategy.

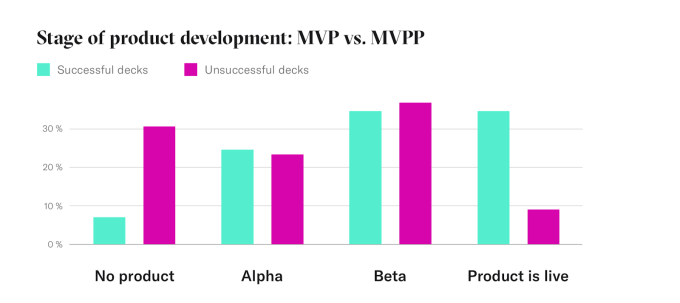

Our analysis reveals a shift in the level of readiness required by institutional investment to receive pre-seed funding. In the past, pre-seed startups could get by with just an MVPP (Minimum Viable PowerPoint). But now, investors are placing their bets on pre-seed startups that have already entered the market and developed an alpha, beta or shipping product.

In fact, 92% of companies with successful pitch decks had either an alpha, beta or shipping product, where only 68% of companies with unsuccessful pitch decks presented the same type of product readiness.

As the economy moves closer to a downturn we can expect VCs to be more cautious with their investments. The current data already shows a preference for companies that have live products; it’s worth the time and effort to be product-ready coming into a pre-seed round or if you’re a startup ready to tackle the round again with a fresh perspective.

That said, even if you do have an MVP, rethinking your pitch deck may be something else to consider. Here’s a good test. Using your pitch deck, spend three to four minutes (that’s all the time you’ll get from a VC) to pitch your business to a friend or family member who knows nothing about your business. Afterward, ask them for a one-sentence description of your company. If they’re not clearly describing what your company does and the problem it’s trying to solve, you probably need to rethink your pitch deck.

According to our recent report, a “less is more” attitude toward creating a compelling pitch deck for meetings could mean more success in pre-seed fundraising.

Your pitch deck will be your main calling card right now. As community events are being replaced with online gatherings during the COVID-19 pandemic, we can expect to see less one-to-one engagement at these events. So pitching a VC in person is not likely to happen anytime soon. Whether you’re sending them a cold email, or getting a warm intro from a portfolio company, you’re going to need to lead with your pitch deck.

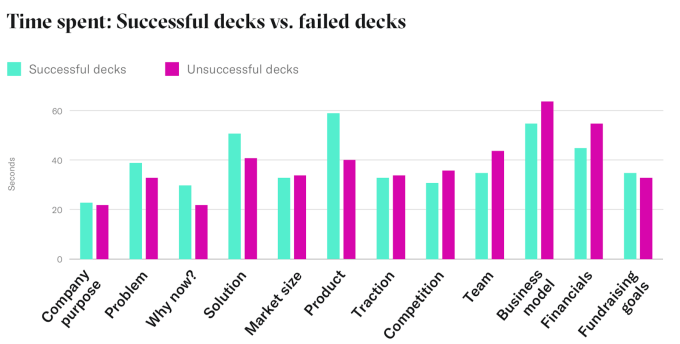

Despite the product taking a more prominent role in the fundraising round, the pitch deck is still a focal point and should be tailored to tell your story in the most effective way, as investors are spending less time evaluating them. On average, investors are spending just 3 minutes and 21 seconds on the pitch deck and the average deck is just 20 slides.

If you are in the process of reevaluating your pitch deck, it could be helpful to make sure your slides feature the right content in the right order. Investors spend nearly 50% more time on the product slides in successful pitch decks and over 18% longer on the business model in unsuccessful pitch decks. Additionally, investors spent more time on solution slides in successful decks than unsuccessful decks.

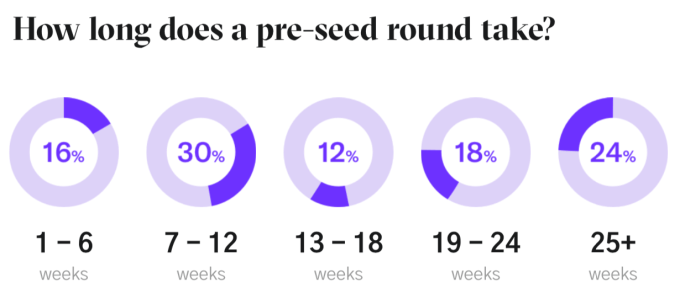

Another area that could benefit from reevaluation is the number of investors contacted, meetings held and the number of weeks spent in a funding round. Generally speaking, the average amount of investors contacted for successful fundraising rounds is 56, resulting in 26 meetings. On average, successful pre-seed startups will spend 20.5 weeks on fundraising.

When it comes to fundraising, there are diminishing returns for investor outreach. You shouldn’t need to send your deck to more than 60-70 investors and have more than 20-30 meetings. If you’re doing more than that, the ROI on your time just isn’t worth it. Because the current crisis is affecting VCs’ willingness to invest, you’re better off finding a small list of investors who are active and targeting your pitch to them. If you’ve reached out to more than 70 investors, but you’re still faced with a wall of “nos” you’re better off pausing your fundraising and addressing the feedback you’ve received so far. For more on when you should quit and reevaluate versus push through you can read my article here (Extra Crunch membership required).

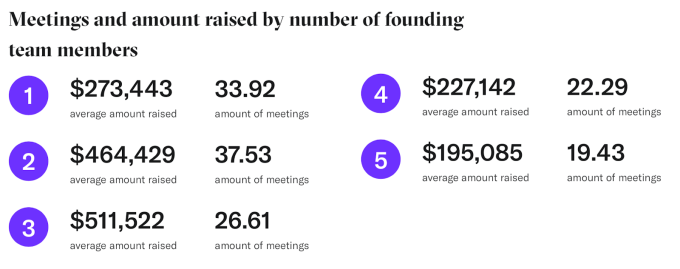

Another area pre-seed startups should evaluate is the number of founders of a company. Our data shows investors still prefer teams of two-three founders, though our data shows that being a solo founder is preferable to having too many founders. For teams of five founders, they averaged earning $195,085 while founding teams of three garnered $511,522.

This may be the right time to find a co-founder. With many people working from home or out of work, this could be the opportunity to take your idea and bring on the technical founder you need. There are online groups and events popping up everywhere in response to social distancing. If you’re worried being a solo founder is going to hold you back, you may want to invest time in those new communities.

For many startups, especially if you are not in Silicon Valley where a substantial amount of funding happens, the process of fundraising can be very opaque. DocSend’s purpose in analyzing this data is to bring some transparency to the process. This in turn provides perspective.

But what founders should do, if they haven’t done so already, is to get some additional perspective. Talk to experts outside your immediate circle of influence. Don’t have a mentor or advisors? Find them. Get a different take on your product idea or the market conditions. Especially now that community events are going virtual, location doesn’t have to hold you back from joining the startup community and finding people to offer feedback on your product or company.

Fundraising is both an art and science. Combining the insights from our data with the benefit of your own community can help you get back on your feet and pitching your company with hopefully a better outcome.

Powered by WPeMatico

Four years ago, mathematician Vlad Voroninski saw an opportunity to remove some of the bottlenecks in the development of autonomous vehicle technology thanks to breakthroughs in deep learning.

Now, Helm.ai, the startup he co-founded in 2016 with Tudor Achim, is coming out of stealth with an announcement that it has raised $13 million in a seed round that includes investment from A.Capital Ventures, Amplo, Binnacle Partners, Sound Ventures, Fontinalis Partners and SV Angel. More than a dozen angel investors also participated, including Berggruen Holdings founder Nicolas Berggruen, Quora co-founders Charlie Cheever and Adam D’Angelo, professional NBA player Kevin Durant, Gen. David Petraeus, Matician co-founder and CEO Navneet Dalal, Quiet Capital managing partner Lee Linden and Robinhood co-founder Vladimir Tenev, among others.

Helm.ai will put the $13 million in seed funding toward advanced engineering and R&D and hiring more employees, as well as locking in and fulfilling deals with customers.

Helm.ai is focused solely on the software. It isn’t building the compute platform or sensors that are also required in a self-driving vehicle. Instead, it is agnostic to those variables. In the most basic terms, Helm.ai is creating software that tries to understand sensor data as well as a human would, in order to be able to drive, Voroninski said.

That aim doesn’t sound different from other companies. It’s Helm.ai’s approach to software that is noteworthy. Autonomous vehicle developers often rely on a combination of simulation and on-road testing, along with reams of data sets that have been annotated by humans, to train and improve the so-called “brain” of the self-driving vehicle.

Helm.ai says it has developed software that can skip those steps, which expedites the timeline and reduces costs. The startup uses an unsupervised learning approach to develop software that can train neural networks without the need for large-scale fleet data, simulation or annotation.

“There’s this very long tail end and an endless sea of corner cases to go through when developing AI software for autonomous vehicles, Voroninski explained. “What really matters is the unit of efficiency of how much does it cost to solve any given corner case, and how quickly can you do it? And so that’s the part that we really innovated on.”

Voroninski first became interested in autonomous driving at UCLA, where he learned about the technology from his undergrad adviser who had participated in the DARPA Grand Challenge, a driverless car competition in the U.S. funded by the Defense Advanced Research Projects Agency. And while Voroninski turned his attention to applied mathematics for the next decade — earning a PhD in math at UC Berkeley and then joining the faculty in the MIT mathematics department — he knew he’d eventually come back to autonomous vehicles.

By 2016, Voroninski said breakthroughs in deep learning created opportunities to jump in. Voroninski left MIT and Sift Security, a cybersecurity startup later acquired by Netskope, to start Helm.ai with Achim in November 2016.

“We identified some key challenges that we felt like weren’t being addressed with the traditional approaches,” Voroninski said. “We built some prototypes early on that made us believe that we can actually take this all the way.”

Helm.ai is still a small team of about 15 people. Its business aim is to license its software for two use cases — Level 2 (and a newer term called Level 2+) advanced driver assistance systems found in passenger vehicles and Level 4 autonomous vehicle fleets.

Helm.ai does have customers, some of which have gone beyond the pilot phase, Voroninski said, adding that he couldn’t name them.

Powered by WPeMatico

Thoma Bravo announced today that it has closed its hefty $3.9 billion acquisition of security firm Sophos, marking yet another private equity deal in the books.

The deal was originally announced in October. Stockholders voted to approve the deal in December.

They were paid $7.40 USD per share for their trouble, according to the company, and it indicated that as part of the closing, the stock had ceased trading on the London Stock Exchange. It also pointed out that investors who got in at the IPO price in June 2015 made a 168% premium on that investment.

Sophos hopes its new owner can help the company continue to modernize the platform. “With Thoma Bravo as a partner, we believe we can accelerate our progress and get to the future even faster, with dramatic benefits for our customers, our partners and our company as a whole,” Sophos CEO Kris Hagerman said in a statement. Whether it will enjoy those benefits or not, time will tell.

As for the buyer, it sees a company with a strong set of channel partners that it can access to generate more revenue moving forward under the Thoma Bravo umbrella. Sophos currently partners with 53,000 resellers and managed service providers, and counts more than 420,000 companies as customers. The platform currently helps protect 100 million users, according to the company. The buyer believes it can help build on these numbers.

The company was founded way back in 1985, and raised over $500 million before going public in 2015, according to PitchBook data. Products include Managed Threat Response, XG Firewall and Intercept X Endpoint.

Powered by WPeMatico

Got your sights set on attending TC Sessions: Mobility 2020 on May 14 in San Jose? Spend the day with 1,000 or more like-minded founders, makers and leaders across the startup ecosystem. It’s a day-long deep dive dedicated to current and evolving mobility and transportation tech. Think autonomous vehicles, micromobility, AI-based mobility applications, battery tech and so much more.

Hold up. Don’t have a ticket yet? Buy your early-bird pass and save $100.

In addition to taking in all the great speakers (more added every week), presentations, workshops and demos, you’ll want to meet people and build the relationships that foster startup success. Get ready for a radical network experience with CrunchMatch. TechCrunch’s free business-matching platform makes finding and connecting with the right people easier than ever. It’s both curated and automated, a potent combination that makes networking simple and productive. Hey needle, kiss that haystack goodbye.

Here’s how it works.

When CrunchMatch launches, we’ll email all registered attendees. Create a profile, identify your role and list your specific criteria, goals and interests. Whomever you want to meet — investors, founders or engineers specializing in autonomous cars or ride-hailing apps. The CrunchMatch algorithm kicks into gear and suggests matches and, subject to your approval, proposes meeting times and sends meeting requests.

CrunchMatch benefits everyone — founders looking for developers, investors in search of hot prospects, founders looking for marketing help — the list is endless, and the tool is free.

You have one programming-packed day to soak up everything this conference offers. Start strategizing now to make the most of your valuable time. CrunchMatch will help you cut through the crowd and network efficiently so that you have time to learn about the latest tech innovations and still connect with people who can help you reach the next level.

TC Sessions: Mobility 2020 takes place on May 14 in San Jose, Calif. Join, meet and learn from the industry’s mightiest minds, makers, innovators and investors. And let CrunchMatch make your time there much easier and more productive. Buy your early-bird ticket, and we’ll see you in San Jose!

Is your company interested in sponsoring or exhibiting at TC Sessions: Mobility 2020? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico