Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

While a handful of tech companies like Zoom and Shopify are enjoying massive gains as a result of COVID-19, that’s obviously not the case for most. Weaker demand, slower sales cycles, and customer insistence on pricing concessions and payment deferrals have conspired to cloud the outlook for many tech companies’ growth.

Compounding these challenges, a lot of tech companies are struggling to raise capital just when they need it most. The data so far suggests that investors, particularly those focused on earlier stage financings, are taking a more cautious approach to new deals and valuations while they wait to see how individual companies perform and which way the economy will go. With the outcome of their planned equity financings uncertain, some tech companies are revisiting their funding strategies and exploring alternative sources of capital to fuel their continued growth.

For certain businesses, COVID-19’s impact on revenue was immediate. For others, the effects of slower economic activity and tighter budgets surfaced more gradually with deals in the funnel before the pandemic closing in April and May. Either way, in the second half of 2020, technology CFOs face a common challenge: How do you accurately forecast sales when there’s very little consensus around key issues such as when business activity will return to pre-COVID levels and what the long-term effects of the crisis might be?

Unfortunately, navigating this uncertainty is just as daunting a challenge for investors. These days, equity investors’ assessment of a company’s growth potential, and the value they are willing to pay for that growth, aren’t just impacted by their view of the company itself. Equally important is their assumptions about when the economy will recover and what the new normal might look like. This uncertainty can lead to situations where companies and their potential investors have materially different views on valuation.

While the full impact of COVID was felt too late to have a material impact on Q1 deal volumes, recently released data from Pitchbook and the NVCA suggest that 2020 will see a significant decrease in the number of companies funded, possibly by as much 30 percent compared to 2019 among early stage companies. And, while it often takes several months to see evidence of broad trends in investment terms, anecdotal evidence indicates investors are seeking to mitigate risk by demanding additional protective provisions.

Powered by WPeMatico

SocialChorus, a startup that helps distribute communications internally in a similar way marketers reach customers externally, announced a $100 million investment today led by Sumeru Equity Partners. With this investment, the firm has bought a majority stake in the company. As part of today’s deal, Sumeru will be adding three members to the SocialChorus board.

“Sumeru Equity Partners is making a majority investment in the company but also well capitalizing the business for future growth,” Mark Haller, principal at Sumeru told TechCrunch.

The company previously raised $47 million, according to Crunchbase data. Haller says this is not a buyout, so much as a partnership with those previous investors. “We’re seeing continued partnership with existing investors and we’re coming in and making that majority investment, and we’ll also be making another investment in the balance sheet,” he said.

What Sumeru is getting is a company that helps with internal communications using marketing techniques, says company CEO Gary Nakamura. “You can run campaigns with targeting segmentation and all the telemetry back that you need as a leader, as a manager, as an organization to understand how your communications are landing with your workforce,” Nakamura told TechCrunch.

The target is large companies and customers, including big names like Ford, Archer Daniels Midland and Boeing. The company reports it has 120 large customers around the world, and the business has been growing at 50% year over year.

While the company is getting this infusion of cash from Sumeru, Nakamura says he will continue to try to manage the company in a thoughtful way, and that means being careful about how they hire beyond the 120 employees the company already has.

“What we have built is a business that doesn’t require a lot of heads to run it. We can maintain a 50% growth rate with financial discipline that we’ve implemented. Historically that is what we’ve been able to do,” he said.

Sumeru Equity Partners is a private equity firm based in San Francisco. It targets mid-market companies, according to the company website, and then tries to apply operational efficiency by working with them on areas like product strategy, go-to-market acceleration and organizational development, with the goal of building up the company and taking it to exit.

Powered by WPeMatico

Earlier this month, Spanish early-stage venture capital firm K Fund officially launched its second fund, which sits at €70 million, up from €50 million the first time around.

Targeting Spanish startups with an international outlook, the seed-stage firm plans to invest from €200,000 to €2 million, writing first checks in 25-30 companies. Meanwhile, a portion of the fund will also be set aside for follow-on funding for the most promising of its portfolio.

Described as business model- and sector-agnostic, K Fund currently has a mix of B2B and B2C companies in its portfolio across a wide variety of sectors, such as travel, fintech, insurtech and others. They include online travel agency Exoticca, HR software Factorial, insurtech startup Bdeo and Hubtype, a conversational messaging tech provider.

I caught up with K Fund’s Jaime Novoa to delve deeper into the firm’s investment remit, how the Spanish startup and tech ecosystem has developed over the last few years and to learn more about “K Founders,” the VC’s new pre-seed funding program.

TechCrunch: K Fund’s first fund was announced in late 2016 to back startups in Spain with an international outlook at seed and Series A. At €70 million, this second fund is €20 million larger but I gather the remit remains broadly the same. Can you be more specific with regards to cheque size, geography, sector and the types of startups you look for?

Jaime Novoa: We’re both agnostic in terms of business models and industries. Since our focus is, for the most part, Spain, we do not believe that the Spanish market is big enough to build a vertically focused fund, either in terms of business model or sector.

With our first fund we invested in 28 companies, with a slightly larger number of B2B SaaS companies than B2C ones, and across a wide variety of sectors. We do have a bit of exposure to travel and fintech/insurtech, but that’s because we’ve found several interesting companies in those spaces, not because we proactively said, “let’s invest in fintech/travel.”

In terms of check sizes, the core of the fund will be to make the same type of investments as in our first fund: first cheques from €200k to €2m and then sufficient capital for follow-on rounds. We’ll probably do a similar number of deals compared to the previous fund, but we want to have additional capital for follow-on purposes.

Powered by WPeMatico

If necessity is the mother of invention, then new business owners are getting very inventive in the ways in which they access cash. Relying on some long-tested and some new avenues to raise money, entrepreneurs are finding more ways to get public market cash faster than they would have in the past.

Whether it’s from Reg A crowdfunding dollars, Special Purpose Acquisition Companies (SPACs) or direct listings, these somewhat arcane and specialized financing vehicles are making a comeback alongside a rise in new funding mechanisms to get to market quickly and avoid the dilution that comes from private market rounds (especially since those rounds are likely to come at a reduced valuation given market conditions).

Some of these tools have existed for a while and are newly popular in an era where retail investors are driving much of the daily fluctuations of the public markets. Wall Street institutions are largely maintaining their conservative postures with regard to new offerings, so secondary market retail volume growth is outpacing institutional. Retail investors want into these new issues and are pouring into the markets, contributing to huge pops to new public offerings for companies like Lemonade this Thursday and creating an environment where SPACs and crowdfunding campaigns can flourish.

The rise of zero-commission brokerages and the popularization of fractional trading led by the startup Robinhood and adopted by every one of the major online brokers including Charles Schwab, TD Ameritrade, E-Trade and Interactive Brokers has created a stock market boom that defies the underlying market conditions in the U.S. and globally. For instance, daily trades on Robinhood are up 300% year-over-year as of March 2020.

According to data from the BATS exchange, the total trade count in the U.S. was up 71% and May trading was up more than 43% over 2019. Meanwhile, E-Trade daily average revenue trades posted a 244% increase in May over last year’s numbers.

The appetite for new issues is growing and if many of the largest venture-backed companies are holding off on going public, smaller names are using SPACs to access public capital and reach these new investors.

Powered by WPeMatico

Jamf, the Apple device management company, filed to go public today. Jamf might not be a household name, but the Minnesota company has been around since 2002 helping companies manage their Apple equipment.

In the early days, that was Apple computers. Later it expanded to also manage iPhones and iPads. The company launched at a time when most IT pros had few choices for managing Macs in a business setting.

Jamf changed that, and as Macs and other Apple devices grew in popularity inside organizations in the 2010s, the company’s offerings grew in demand. Notably, over the years Apple has helped Jamf and its rivals considerably, by building more sophisticated tooling at the operating system level to help manage Macs and other Apple devices inside organizations.

Jamf raised approximately $50 million of disclosed funding before being acquired by Vista Equity Partners in 2017 for $733.8 million, according to the S-1 filing. Today, the company kicks off the high-profile portion of its journey toward going public.

In a case of interesting timing, Jamf is filing to go public less than a week after Apple bought mobile device management startup Fleetsmith. At the time, Apple indicated that it would continue to partner with Jamf as before, but with its own growing set of internal tooling, which could at some point begin to compete more rigorously with the market leader.

Other companies in the space managing Apple devices besides Jamf and Fleetsmith include Addigy and Kandji. Other more general offerings in the mobile device management (MDM) space include MobileIron and VMware Airwatch among others.

Vista is a private equity shop with a specific thesis around buying out SaaS and other enterprise companies, growing them, and then exiting them onto the public markets or getting them acquired by strategic buyers. Examples include Ping Identity, which the firm bought in 2016 before taking it public last year, and Marketo, which Vista bought in 2016 for $1.8 billion and sold to Adobe last year for $4.8 billion, turning a tidy profit.

Now that we know where Jamf sits in the market, let’s talk about it from a purely financial perspective.

Jamf is a modern software company, meaning that it sells its digital services on a recurring basis. In the first quarter of 2020, for example, about 83% of its revenue came from subscription software. The rest was generated by services and software licenses.

Now that we know what type of company Jamf is, let’s explore its growth, profitability and cash generation. Once we understand those facets of its results, we’ll be able to understand what it might be worth and if its IPO appears to be on solid footing.

We’ll start with growth. In 2018 Jamf recorded $146.6 million in revenue, which grew to $204.0 million in 2019. That works out to an annual growth rate of 39.2%, a more than reasonable pace of growth for a company going public. It’s not super quick, mind, but it’s not slow either. More recently, the company grew 36.9% from $44.1 million in Q1 2019 to $60.4 million in revenue in Q1 2020. That’s a bit slower, but not too much slower.

Turning to profitability, we need to start with the company’s gross margins. Then we’ll talk about its net margins. And, finally, adjusted profits.

Gross margins help us understand how valuable a company’s revenue is. The higher the gross margins, the better. SaaS companies like Jamf tend to have gross margins of 70% or above. In Jamf’s own case, it posted gross margins of 75.1% in Q1 2020, and 72.5% in 2019. Jamf’s gross margins sit comfortably in the realm of SaaS results, and, perhaps even more importantly, are improving over time.

When all its expenses are accounted for, the picture is less rosy, and Jamf is unprofitable. The company’s net losses for 2018 and 2019 were similar, totaling $36.3 million and $32.6 million, respectively. Jamf’s net loss improved a little in Q1, falling from $9.0 million in 2019 to $8.3 million this year.

The company remains weighed down by debt, however, which cost it nearly $5 million in Q1 2020, and $21.4 million for all of 2019. According to the S-1, Jamf is sporting a debt-to-equity ratio of roughly 0.8, which may be a bit higher than your average public SaaS company, and is almost certainly a function of the company’s buyout by a private equity firm.

But the company’s adjusted profit metrics strip out debt costs, and under the heavily massaged adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) metric, Jamf’s history is only one of rising profitability. From $6.6 million in 2018 to $20.8 million in 2019, and from $4.3 million in Q1 2019 to $5.6 million in Q1 2020, with close to 10% adjusted operating profit margins through YE 2019.

It will be interesting to see how the company’s margins will be affected by COVID-19, with financials during the period still left blank in this initial version of the S-1. The Enterprise market in general has been reasonably resilient to the recent economic shock, and device management may actually perform above expectations, given the growing push for remote work.

Something notable about Jamf is that it has positive cash generation, even if in Q1 it tends to consume cash that is made up for in other quarters. In 2019, the firm posted $11.2 million in operational cash flow. That’s a good result, and better than 2018’s $9.4 million of operating cash generation. (The company’s investing cash flows have often run negative due to Jamf acquiring other companies, like ZuluDesk and Digita.)

With Jamf, we have a SaaS company that is growing reasonably well, has solid, improving margins, non-terrifying losses, growing adjusted profits and what looks like a reasonable cash flow perspective. But Jamf is cash poor, with just $22.7 million in cash and equivalents as of the end of Q1 2020 — some months ago now. At that time, the firm also had debts of $201.6 million.

Given the company’s worth, that debt figure is not terrifying. But the company’s thin cash balance makes it a good IPO candidate; going public will raise a chunk of change for the company, giving it more operating latitude and also possibly a chance to lower its debt load. Indeed Jamf notes that it intends to use part of its IPO raise to “to repay outstanding borrowings under our term loan facility…” Paying back debt at IPO is common in private equity buyouts.

Jamf’s march to the public markets adds its name to a growing list of companies. The market is already preparing to ingest Lemonade and Accolade this week, and there are rumors of more SaaS companies in the wings, just waiting to go public.

There’s a reasonable chance that as COVID-19 continues to run roughshod over the United States, the public markets eventually lose some momentum. But that isn’t stopping companies like Jamf from rolling the dice and taking a chance going public.

Powered by WPeMatico

Over the past two decades, the venture capital industry has exploded beyond anyone’s wildest imaginations.

What began as a sleepy industry in Boston and Menlo Park has now expanded to dozens of cities the world over. The National Venture Capital Association estimates that VCs deployed more than $130 billion in 2018 and 2019, and thousands of new investors have joined the ranks in recent years to find the next great startups.

All that activity, though, poses a dilemma for founders: Who actively writes checks? Who is a leader in a specific market or vertical? Who has the conviction to underwrite pathbreaking investments? Who, ultimately, do you want to have by your side for the next decade as your startup grows?

There are lists that rank VCs by their exit returns. There are lists that rank young VCs by their potential. There are lists of VCs who claim investment interest in various sectors. There are lists that try to ferret out deal volume, impact and other quantitative metrics. There are internal lists at accelerators that share collective wisdom between founders.

Who actively writes checks? Who is a leader in a specific market or vertical? Who has the conviction to underwrite pathbreaking investments? Who, ultimately, do you want to have by your side for the next decade as your startup grows?

All those lists and rankings have an important function to serve, but for all the compilations of investors out there, we couldn’t find a single one that publicly answered a simple yet vital question: Who are the VC investors who are leaders in specific verticals who should be a founder’s first stop during a fundraise?

Today’s venture industry is made up of thousands of investors with varying specialties, and far too many passive investors that are willing to participate in rounds but don’t actively participate in deals unless other investors have committed. Many don’t actively push to get deals done or don’t actively lead the charge to build a syndicate of investors.

With all that in mind, we’re excited to launch a new initiative that we hope will help answer those questions and help founders find that first check — The TechCrunch List.

![]()

Over the next few weeks, we’re going to be collecting data around which individual investors are actually willing to write the proverbial “first check” into a startup’s fundraising round and help catalyze deals for founders — whether it be seed, Series A or otherwise (i.e. out of your Series A investors, the first person who was willing to write the check and get the ball rolling with other investors). Once we’ve collected, cleaned and analyzed the data, we’ll publish lists of the most recommended “first check” investors across different verticals, investment stages and geographies, so founders can see which investors are potentially the best fit for their company.

Founders are used to being specialized; after all, they have to live and breathe their startups every single day. So it can be jarring to start talking to generalist investors who know little about a category and ask shallow questions only to render a judgment with irrelevant advice. One of the greatest impetuses for us to put together The TechCrunch List is that like founders, we also struggle to cut through the noise around the interests of individual VCs.

We’d argue that’s close to impossible. There is more spend on technology than ever before in history. Verticals are getting more competitive — market maps that used to have 10 to 50 companies have expanded to hundreds. The only way to compete today is to specialize, and that has never been more true for VCs.

In all, The TechCrunch List will publish the most recommended “first check” writers across 22 different categories, ranging from D2C & e-commerce brands to space, and everything in between. Through some data analysis around total investments in each space, we believe our 22 categories should cover the entirety or majority of the venture activity today.

To make this project a success and create a useful resource for founders, we need your help. We want to hear from company builders and we want to hear from them directly.

To make this project a success and create a useful resource for founders, we need your help. We want to hear from company builders and we want to hear from them directly. We will be collecting endorsements submitted by founders through the form linked here.

Through the form, founders will be asked to submit their name, their startup, the stage of company, the name of the one “first check” investor they want to endorse and a couple of minor logistical items. We are asking founders here for their on-the-record endorsement. We ask that you limit your recommendations to one (1) person per fundraise round.

While many investors may have helped you in your journey, we are specifically interested in the person who most helped you get a round underway and closed. The one who catalyzed your round. The one who guided you through the fundraise process. The one investor you would ultimately recommend to other founders who are trying to find their VC champion.

Our main goal is to help founders, dreamers and company builders find investors who will invest in them today, and with your help, we think we can. The TechCrunch List is not meant to identify every possible investor under the sun who might make an investment within a space, nor just the big household-name VCs whose reputations can sometimes seem more linked to their follower counts on Twitter as opposed to their bold term sheets.

Our hope is that this can be a go-to resource for founders looking to fundraise going forward, and with that in mind, we are very determined to improve the glaring representation gaps in the venture industry. It’s no secret that the world of VC still looks like a country-club membership roster, dominated by white men with strong opinions and loud voices. Looking at the data, it’s clear that there are groups that are particularly underrepresented, with only a small portion of the industry made up of Black, Latinx and female investors, for example.

We want to amplify these voices and we want to hear particularly from founders of color, female founders and other underrepresented groups. We also want to make sure our recommended investor lists are sufficiently representative and highlight underrepresented investors who might not have had equal opportunities in the past.

We want to help builders wade through the BS politics and fundraising annoyances that founders complain to us about on a daily basis, and help them identify qualified leads that are actually active, engaged and specialized and are the best fit to help founders raise money and grow now.

Thank you for your support. We’re excited to build The TechCrunch List with you — and for you.

Powered by WPeMatico

The venture capital industry is less transparent today than at any time in recent memory.

For all the talk about expanding access and improving its sordid record on diversity, in reality, it has never been harder for founders to figure out who can even write a check to their startups in the first place.

When I first returned to TechCrunch after my second stint in venture capital, my first piece was entitled “The loss of first check investors.” While working in the venture capital industry, it was maddening to see — particularly at the pre-seed and seed stages — how few investors were really willing to go out on a limb and invest in founders before another VC had committed a check.

It’s only gotten worse in the past two years since that article, and the complexity comes from a number of different places. As our investigation showed more than a year ago, fewer and fewer venture rounds are being announced through SEC Form D filings.

There are almost no publicly accountable datasets left indicating who is writing checks in the venture industry and which companies are receiving those checks. While stealthiness is valid in the early days of a startup, the excuse wears thin after years.

Powered by WPeMatico

Raising capital from a corporate VC can bring many benefits beyond just money. Strategic CVCs, who measure ROI based on the strength of the strategic partnership with their portfolio companies as well as the financial return, will typically seek to maximize their relationships with startups for a long time after the investment is made.

Specifically, a CVC investor can offer the following to an entrepreneur:

Partnerships. CVCs can leverage their supply chain and operations to build new partnerships that otherwise may have taken months or years for startups to create.

Distribution. Strategic CVCs can become a distribution channel for a startup, connect that startup with their suppliers, or even use the startup to become a channel for the parent company.

Branding halo. If a large company is willing to invest in your startup, it’s a strong signal that your product is good and that your business has a bright future.

Acquisition. Many CVCs invest in startups that they may want to acquire down the line. A CVC may also endorse an exit-seeking portfolio company to their partner companies or suppliers.

Granted, seeing results from these benefits takes time, and even the best of intentions during a capital raise process may not always yield an optimal strategic relationship.

Here’s a list of factors to keep in mind for founders who want the best chances of a productive and successful relationship with their CVC.

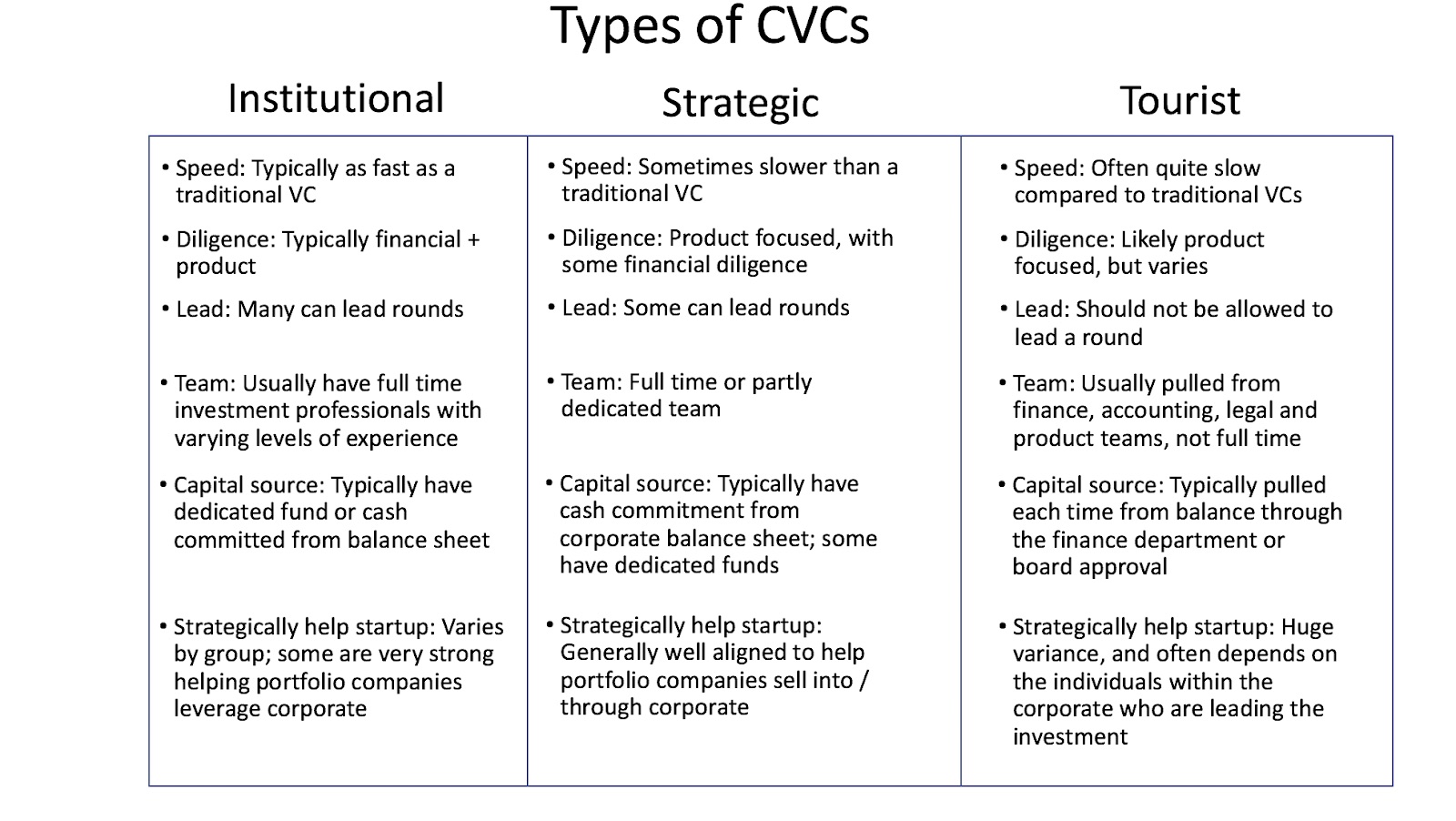

Know which type of CVC you’re dealing with from the outset. In our previous posts, we outlined the three types of CVCs — experienced institutional investors, industry-specific strategics, and beginner or “tourist” CVCs. As we’ve discussed, be sure to spend time interviewing and building relationships with CVCs to determine which type they are, what kinds of benefits and resources they can offer and what their history looks like in terms of successfully partnering with startups over time. When in doubt, ask other founders who have done deals with them!

Powered by WPeMatico

More than $50 billion of corporate venture capital (CVC) was deployed in 2018 and new data indicates that nearly half of all venture rounds will include a corporate investor. The CVC trend is heating up and the need for founders and startup executives to stay informed is higher than ever.

We’ve covered the basics in this series, including how to approach CVCs and what to know before the investment, what to look out for when negotiating, and getting the most out of a CVC partnership after the investment.

A great CVC investor can be the best of both worlds — a strong corporate champion who provides insights and connections to help your startup succeed and a committed financial partner who provides the capital you need to grow. But CVCs aren’t just VCs with different business cards. Finding the right CVC requires the right approach and strategy, and getting the right CVC on your cap table can bring unique and lasting value to your startup.

To wind down this series, here’s a list of the top 15 things every founder should know before signing a term sheet with a CVC.

Image credits: Orn/Growney

There are plenty of benefits to taking CVC investments. Many CVC investments lead to acquisitions, and even if the discussions with a CVC fall apart, your meeting can result in valuable introductions that yield new business relationships. The rising CVC trend offers a brave new world for entrepreneurs. If you know the ropes of CVC investing, you could be in for a partnership that benefits you both.

Powered by WPeMatico

As investors’ appetites sour in the midst of a pandemic, a three-and-a-half-year-old Indian firm has secured $10.3 billion in a month from Facebook and four U.S.-headquartered private equity firms.

The major deals for Reliance Jio Platforms have sparked a sudden interest among analysts, executives and readers at a time when many are skeptical of similar big check sizes that some investors wrote to several young startups, many of which are today struggling to make sense of their finances.

Prominent investors across the globe, including in India, have in recent weeks cautioned startups that they should be prepared for the “worst time” as new checks become elusive.

Elsewhere in India, the world’s second-largest internet market and where all startups together raised a record $14.5 billion last year, firms are witnessing down rounds (where their valuations are slashed). Miten Sampat, an angel investor, said last week that startups should expect a 40%-50% haircut in their valuations if they do get an investment offer.

Facebook’s $5.7 billion investment valued the company at $57 billion. But U.S. private equity firms Silver Lake, Vista, General Atlantic, and KKR — all the other deals announced in the past five weeks — are paying a 12.5% premium for their stake in Jio Platforms, valuing it at $65 billion.

How did an Indian firm become so valuable? What exactly does it do? Is it just as unprofitable as Uber? What does its future look like? Why is it raising so much money? And why is it making so many announcements instead of one.

It’s a long story.

Billionaire Mukesh Ambani gave a rundown of his gigantic Indian empire at a gathering in December 2015 packed with 35,000 people including hundreds of Bollywood celebrities and industry titans.

“Reliance Industries has the second-largest polyester business in the world. We produce one and a half million tons of polyester for fabrics a year, which is enough to give every Indian 5 meters of fabric every year, year-on-year,” said Ambani, who is Asia’s richest man.

Powered by WPeMatico