Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

One of the more salient trends in the tech world — arguably the engine that propels it — has been the recurring theme of people who hone talents at bigger companies and then strike out on their own to found their own startups.

(Some, like Max Levchin, even hire entrepreneurial types intentionally to help perpetuate this cycle and get more proactive teams in place.)

It turns out that trend doesn’t just apply to companies, but also to the investors who back them. At Disrupt we talked with three venture capitalists who have followed that path: Making their names and cutting their teeth at major firms, and now building their own “startup” funds on their own steam.

On the macro level, the whole world has been living through a challenging time this year. But as we’ve seen time and again the wheels have continued to turn in the tech world.

IPOs are returning, products are being rolled out, people are buying a lot online and using the internet to stay connected, there has been a lot of M&A and promising startups are getting funded.

Indeed, if entrepreneurs and their innovations are the engine of the tech world, money is the fuel, and that is the opportunity that Dayna Grayson (formerly of NEA, now founder at Construct Capital), Renata Quintini (formerly at Lux Capital, now founder at Renegade Partners) and Lo Toney (formerly GV, now founder at Plexo Capital) have zeroed in to address.

Grayson said that part of the reason for striking out to start Construct Capital with co-founder Rachel Holt was what they saw as an opportunity to create a firm that specifically funded startups tackling the industrial sector:

“Half the U.S. economy’s GDP, half the GDP of this country, hasn’t really been digitized,” she said. “[Firms] haven’t been tech enabled. They’ve been way under invested … The time is now to build with early stage entrepreneurs.”

While Construct is focusing on a sector, Renegade was founded to focus on something else: The stage of development for a startup, and specific the Series B, which the firm refers to as “supercritical,” essential in terms of getting team and strategy right after a startup is no longer just starting out, but before and leading to scaled growth.

“We saw through our boards over and over again companies that figured out how to scale their organizations, put in the processes,” said Quintini, who co-founded Renegade with Roseanne Wincek. “On the people side, they actually went further and captured a lot more market cap and market share faster. Once we saw this opportunity, we could not let it go.”

She compares the current imperative to really focus on how to build and scale companies at the “supercritical” stage to the focus on early stage funding that typified an earlier period in the development of the startup ecosystem 15 years ago. “You could get a million dollars and be in business, a lot more people could, and you had less time to figure out what really resonated with customers,” she said. “That really gave rise to today.”

Toney has taken yet another approach, focusing not on sector, nor stage, but using capital to help germinate a whole new demographic of founders, the premise being that funding a more diverse and inclusive mix of founders is not just good for creating a more level playing field, but also for the good of more well-rounded products that speak to a wider population of users.

“I was having a great time at GV, but I just saw this opportunity as being one that was too hard to resist,” said Toney of founding Plexo, which invests not just in startups but in funds that are following a similar investment principle to his. Investing in both funds and founders is something GV did as well, but the added ability to turn that into investing with a social imperative was important. “To have this byproduct of increasing diversity and inclusion in the ecosystem [is something] I’m super passionate about,” he said.

We are living through a time when the tech world seems to be awash in capital. One of the byproducts of having so many successful tech companies has been limited partners rushing in to back more VCs in hopes of also getting some of the spoils: Many firms are closing funds in record times, oversubscribed and that’s having a knock-on effect not just in terms of startups getting funded, but VCs themselves also multiplying with increasing frequency. All three said that the fact that they all identify as more than just “another new VC”, with specific purposes, also makes it easier for them to get themselves noticed to get involved in good deals.

Grayson said that the challenge of starting a firm in the midst of a global pandemic turned out to be a piece of good fortune in disguise in an industry that thrives on the concept of “disruption” (as we at TechCrunch know all too well … ).

“We were really lucky that we started investing in a COVID world,” she said. “So many things have been up ended. And I think, you know, software adoption and technology adoption have been moved up 10-20 years in industry. [And] the way that we work together really has changed.” She also said that they’ve found themselves almost looking for companies “created in a COVID environment,” which indeed would qualify as a battle-tested business model.

In terms of raising funds themselves, Toney also recalled the period when we saw a real surge of VCs emerging to fund companies at the seed stage and the growth of “solo capitalists” around that.

“I think what’s really interesting about solo capitalists is [how] they take their understanding of operations, and a deep network of other technologists, both from big companies as well as entrepreneurs, and … leverage access to all that deal flow by going out and actually raising capital from other sources, whether that be high net worth individuals or family offices or even institutions,” he said.

Powered by WPeMatico

A group of U.K.-based VCs have come together to create a new virtual pitching event designed to address the problems with the current startup ecosystem that can lead to inequalities and “warm intros” made only between privileged classes and ethnicities.

Held on the 30th of September, “Access All” will be a new virtual event geared toward founders from underrepresented groups.

Participating founders will be invited to pitch their startups to a number of London’s leading VCs and companies, including Downing Ventures, Playfair Capital, SpeedInvest and SoftBank, as well as Microsoft, Amazon, Accenture and O2.

The joint initiative has been put together by Floww, Force Over Mass and Wayra UK, with the mission to create more opportunity for BAME founders, based on merit, reducing bias and addressing the problems of the “the old boys network” of venture capital deal flow.

According to some figures, startups with all-male founding teams raise 91% of the venture capital in the U.K., but the stats around ethnic minority founders are harder to find. In the U.S. for example, 0.02% of venture capital is allocated to Black female founders.

Martijn de Wever, CEO and founder of Floww, which is coordinating the event, said: “With Access All, we rallied together in the startup community because we believe that the system needs change. Black, Asian and other ethnic minority founders, need to have fair access.”

Floww’s team of accountants and content writers will work with applicants for free to review their business plans and get them ready to pitch to the participating investors. TechCrunch and Forbes journalists will be joining the panel as judges.

Founders can register here.

Powered by WPeMatico

Sprinklr has been busy the last few years acquiring a dozen companies, then rewriting their code base and incorporating them into the company’s customer experience platform. Today, the late-stage startup went back to the fundraising well for the first time in four years, and it was a doozy, raising $200 million on a $2.7 billion valuation.

The money came from private equity firm Hellman & Friedman, which also invested $300 million in buying back secondary shares. Meanwhile the company also announced $150 million in convertible securities from Sixth Street Growth. That’s a lot of action for a company that’s been quiet on the fundraising front for years.

Company founder and CEO Ragy Thomas says he sought the investment now because after building a customer experience platform, he was ready to accelerate and he needed the money to do it. He expects the company to hit $400 million in annual recurring revenue by year’s end and he says that he sees a much bigger opportunity on the horizon.

“We think it’s a $100 billion opportunity and our large public competitors have validated that and continue to do so in the customer experience management space,” he said. Those large competitors include Salesforce and Adobe.

He sees customer experience management as having the kind of growth that CRM has had in the past, and this money gives him more options to grow faster, while working with a big private equity firm.

“So what was appealing in this market for us was not just putting some more money in the bank and being a little more aggressive in growth, innovation, go to market and potential M&A, but what was also appealing is the opportunity to bring someone like a Hellman & Friedman to the table,” Thomas said.

The company has 1,000 clients, some spending millions of dollars a year. They currently have 1,900 employees in 25 offices around the world, and Thomas wants to add another 500 over the next 12 months — and he believes that $1 billion in ARR is a realistic goal for the company.

As he builds the company, Thomas, who is a person of color, has codified diversity and inclusion into the company’s charter, what he calls the “Sprinklr Way.” “For us, diversity and inclusion is not impossible. It is not something that you do to check a box and market yourself. It’s deep in our DNA,” he said.

Tarim Wasim a partner at investor Hellman & Friedman, sees a company with tremendous potential to lead a growing market. “Sprinklr has a unique opportunity to lead a Customer Experience Management market that’s already massive — and growing — as enterprises continue to realize the urgent need to put CXM at the heart of their digital transformation strategy,” Wasim said in a statement.

Sprinklr was founded in 2009. Before today, it last raised $105 million in 2016 led by Temasek Holdings. Past investors include Battery Ventures, ICONIQ Capital and Intel Capital.

Powered by WPeMatico

For many investors, the coronavirus has effectively taken geography out of the equation when it comes to vetting new opportunities.

While this dynamic opens up startups to more investment opportunities, venture capital firms that focus on a specific region are in a thornier spot. The competitive advantage they once had when raising — the notion that they’re focused on an area no one else is — is potentially threatened.

Natasha Mascarenhas, Danny Crichton and Alex Wilhelm of the TechCrunch Equity crew discussed the future of geographic-focused funds given the uptick of remote investing:

Since 2014, Steve Case and his team have made an annual bus trip across the country to meet startups in emerging startup hubs. Five days, five cities and at least $500,000 of investment dollars given to startups. Case would even offer to fly out promising and hard-to-reach startups to have them join the trip.

The Rise of the Rest fund, with more than $300 million in assets under management, has invested in over 130 startups across 70 cities, including Austin, Chicago, Detroit, Los Angeles, New Orleans and Washington, D.C.

Powered by WPeMatico

In the last few months, we’ve seen much of Silicon Valley finally start to acknowledge generations of systemic racial inequity and take actionable steps to empower and support underrepresented people in tech. Funds are looking to invest capital more equitably and have started to take concrete steps to achieve this goal.

For example, Eniac Ventures and Hustle Fund have started to meet with more Black founders via consultations and encouraging cold inbound pitches. Initiatives like venture capital fellowships run by Susa Ventures and Unshackled Ventures will allow for increased representation in investment teams. While these initiatives are exciting, it’s important to explore how we can enable sustainable change and solve the diversity problem at the root.

It’s as simple as this: Investing in diverse perspectives makes for a far more efficient economy. The data also confirms this, given that homogeneous investing teams had a success rate for M&A and IPOs that was 26.4%-32.2% lower. Data since 1990 shows that approximately only 8% of VCs identify as women, with 2% of VCs identifying as Latinx and less than 1% identifying as Black.

It’s clear that the inequitable deployment of capital that results from homogenous investment teams at VC funds has translated into missed opportunity for outsized financial returns. Since this really comes down to how venture funds operate at their core, an entity that can greatly influence this and reinvent the status quo are VC funds’ limited partners.

Limited partners are the often unheard of backers of venture capital funds. Institutional venture capital funds raise money from sources such as high-net-worth individuals (HNWs), endowments, foundations, fund of funds, banks, insurance/pension funds and sovereign wealth funds that they will in turn use to invest money into high-growth, category-defining startups (the part that you do hear about).

LPs hold a lot of power in the venture financing life cycle as institutional venture capital firms can’t write checks at the scale they do without the external financing that LPs provide. Since LPs are the source of capital, they can control who they invest in (GPs) and how they invest and manage their capital. What if LPs are the missing link who can control the flow of capital to GPs who empower, find and fund more underrepresented entrepreneurs and keep them accountable?

Powered by WPeMatico

I was recently part of an open forum about being Black in America, as well as in the startup space.

A white founder asked, “What can I do as the founder of a very early-stage startup?” The group gave various suggestions that included the obvious (or at least I would hope it’s obvious), “When you are growing your team, consider hiring Black team members,” or “When you are considering an investment from an investor, press them about the diversity of their current portfolio founders.”

But one suggestion really stood out, which was to make a concerted effort to find someone different from your current team’s makeup when bringing in subject matter experts. This intentional act shows your homogeneous team members that Black people, other racial minorities or genders can be experts too. It can also be applied when growing your team by making sure you interview diverse candidates whose level of expertise is often second-guessed.

This got me thinking about VC Monique Woodard’s statement that “Black founders are often overmentored and underinvested.” In June, at the height of the Black Lives Matter protests and open dialogue about anti-Blackness, we saw a slew of investors rushing to offer mentorship to Black founders. Some of the investors don’t have Black founders among their portfolio companies so to some onlookers, this rush to help Black founders was seen as insincere and a marketing ploy.

As a former founder, I can confidently say that most Black founders simply want a fair shot at presenting their startups to investors. The prevailing system of needing a warm introduction to access investors puts founders, especially Black founders, who don’t have the same networks as investors at a disadvantage. The proper mea culpa by these investors should be to make pitching more accessible for all founders. Although offers of mentorship are certainly welcome, the constant barriers Black founders tell me they struggle with are access to capital and networks, not a lack of talent or business savvy.

The quick emphasis on mentorship made me ask myself: How are the contributions of Black people (founders, investors, operators, etc.) to the startup space seen? Are we showcased as experts or as perpetual students in need of mentoring and advising? To directionally answer this question, I turned to podcasts. According to a New York Times article, “more than half the people in the United States have listened to one (podcast), and nearly one out of three people listen to at least one podcast every month.” This figure shows that podcasts are a wide-reaching medium that audiences use as a source of both entertainment and information.

I dug into the 2018 and 2019 guest lists of three of my favorite startup-related podcasts: “This Week In Startups,” “How I Built This With Guy Raz” and “The Twenty Minute VC.” These are all top-ranked podcasts with tens of millions in downloads and over half a million subscribers.

| Podcast | Description | Typical Guest Profile |

| This Week In Startups | Entrepreneur and angel investor Jason Calacanis brings you his take on the best, worst and most interesting stories from the world of startups. Glimpse into the boardroom during deep-dive interviews with the most innovative founders and investors. Get the experts’ hottest takes on trending topics during our news roundtables. |

|

| How I Built This with Guy Raz | Guy Raz dives into the stories behind some of the world’s best-known companies. How I Built This weaves a narrative about innovators, entrepreneurs and idealists — and the movements they built. |

|

| The Twenty Minute VC | The Twenty Minute VC takes you inside the world of venture capital, startup funding and the pitch. Discover how you can attain funding for your business by listening to what the most prominent investors are directly looking for in startups, providing easily actionable tips and tricks that can be put in place to increase your chances of getting funded. |

|

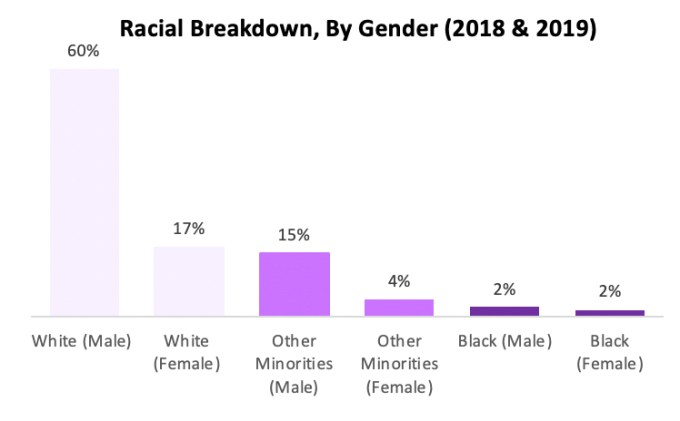

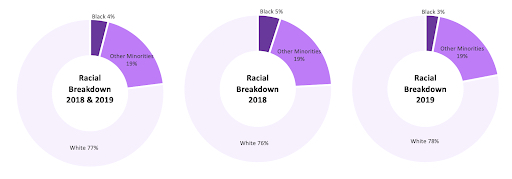

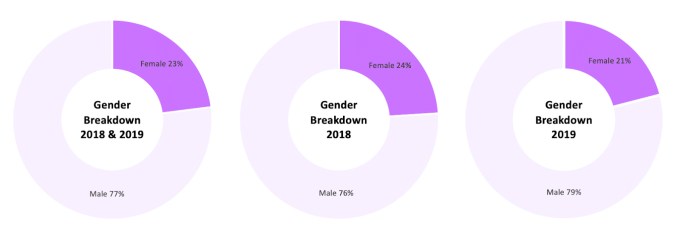

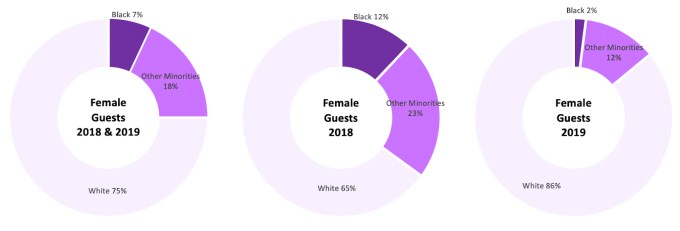

I analyzed more than 500 episodes that were aired in 2018 and 2019 across all three podcasts to get a racial and gender breakdown of guests that were featured on those episodes.

Image Credits: Kofi Ampadu (opens in a new window)

Image Credits: Kofi Ampadu (opens in a new window)

Image Credits: Kofi Ampadu (opens in a new window)

Image Credits: Kofi Ampadu (opens in a new window)

Image Credits: Kofi Ampadu

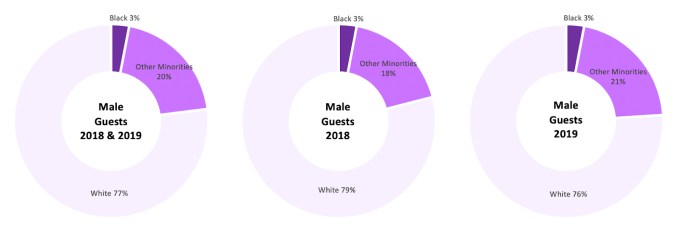

Not surprisingly, a majority of the guests featured were white men (60%). Black men and women were featured on 4% of all the episodes. A total of 15 Black (nine men and six women) unique guests were showcased as guests out of more than 400 unique guests during the two-year span. Also interesting to note that of those 15 Black guests, three were celebrities (a comedian, a TV personality and a rapper), two of whom were featured twice.

There are certainly more than 15 Black noncelebrities available who would fit the ideal guest lists of these podcasts. It is also interesting to note the percentage of Black guests decreased by 2% from 2018 to 2019 and incidentally increased by 2% for white guests during that span. The percentage of Black female guests within the female gender pool drastically decreased by 10% while white female guests increased by 21% in the two-year time period.

The results are a microcosm of what has been happening in the startup ecosystem: Black minds are undervalued and underappreciated. Oftentimes in the startup space, a founder is deemed a successful founder not based on how much money they collect from satisfied customers but by how much money they have raised from investors. Based on these misleading standards, Black founders will rarely be classified as successful because 1% of VC-backed founders are Black.

When it comes to the investor ranks, 81% of venture funds have no Black investors, so very often Black investors have to raise their own funds since the path to joining one is limited. Given these and other obstacles, I would argue Black people are the inspirational and relatable experts whose stories and advice need to be heard by wider audiences.

It is also worth noting that Black people are versed in varying topics and should not be exclusively invited on platforms to speak on Black issues. Black people are not a monolith and each person has their own passion and areas of expertise and outside of lived experiences not all Black people may be well-equipped to dissect Black issues.

In the spirit of not only pointing out systemic racism in the startup space, here is a list of emerging Black founders, investors and startup ecosystem builders, curated by Denisha Kuhlor and me. The talented people listed would make great guests for podcasts, conferences and any platforms that aim to amplify a diverse set of insights and experiences.

Methodology: Analyzed 484 guests across all three podcasts, the hosts of these podcasts were not included in the analysis as guests. As a result, podcast episodes that only included the host were excluded. Reaired podcast episodes were included in the analysis. If an episode had multiple guests, each guest was accounted for separately in the analysis.

The gender of guests was based on pronouns used to refer to guests on the podcast or publicly available information. The race of guests was objectively determined based on how the guest identifies or subjectively determined based on photographs, videos and publicly available information. The “Other Minorities” grouping includes Latinx, Southeast Asian and East Asian guests.

Disclaimer: This write-up is by no means written to cast aspersions on the three podcasts analyzed. They were simply chosen because I am an avid listener and they are all relatively popular in the startup space.

Powered by WPeMatico

A breeding ground for European entrepreneurs, Berlin has a knack for producing a lot of new startups: the city attracts top international, diverse talent, and it is packed with investors, events and accelerators. Also important: it’s a more affordable place to live and work when compared to many other cities in the region.

Berlin ranked 10th place in the 2019 Global Ecosystem Report, trailing behind only two other European cities: London and Paris. It’s home to unicorns such as N26, Zalando, HelloFresh and pioneers of the scene such as SoundCloud.

Top VCs include Earlybird, Point Nine, Project A, Rocket Internet, Holtzbrinck Ventures and accelerators such as Axel Springer Plug and Play Accelerator, hub:raum and The Family.

To get a sense of how the novel coronavirus has changed the landscape, we asked ten investors to give us an insight into their thinking during these pivotal times:

What trends are you most excited about investing in, generally?

Generally, we believe in a future in which we can leverage technology to free up humans from repetitive and tedious work and to empower them to shift their focus to what they consider more meaningful and impactful: that is creative and interpersonal activities. Thus, we are excited about founders working towards that future and finding answers across multiple industries, such as manufacturing or logistics, across all working-classes, and across different eras – before, during and after COVID.

What’s your latest, most exciting investment?

One of the recent additions of our new fund is Luminovo, a Munich-based company that develops a solution in the electronics industry to reduce the time and resources needed to go from an idea to a market-ready circuit board.

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

So far, we have only scratched the surface of the kind of efficiency gains that can potentially be achieved – particularly in industries that were considered to be boring and sluggish in the past, such as insurance or logistics. Even small improvements driven by technology can have a massive direct impact on P&L.

What are you looking for in your next investment, in general?

In general, we love to back visionary founders in the seed-stage that tap into giant industries with a high potential for digitization across Europe and the US.

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

COVID has sprung a myriad of companies in the communication and collaboration space into existence. While we believe in a future in which products and processes will be inherently remote-first, we will see a consolidation of that space that only allows for an oligopolistic market structure similar to how there is only one Zoom and Google Meet in the video communication space today.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

We have always considered ourselves as one of the few funds in Germany with a significant investment footprint both in Europe and the US. COVID has emphasized that we are able to invest entirely remotely and hence we will continue and even increase our activities across multiple hubs, such as Munich, Paris, or London.

Which industries in your city and region seem well-positioned to thrive, or not long-term? What are companies you are excited about (your portfolio or not), which founders?

Germany’s economy relies on wealthy traditional companies sitting on top of capital to be unlocked which new entrants can make use of. This has been true before 2020, and COVID will only demand more and accelerated innovation across these traditional industries ranging from automotive, manufacturing, to the chemical industry.

How should investors in other cities think about the overall investment climate and opportunities in your city?

Berlin and other German cities have consistently proven to develop and grow new leaders across multiple categories such as banking (N26), mobility (Flixbus and Lilium), or data analytics (Celonis). This is certainly driven by a mix of talents coming out of world-class educational institutions, the relative low cost of living in tech hubs, and large local incumbents with massive capital to invest and spend.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

While COVID has accelerated remote-first products and processes, we still believe that people will flock back to startup hubs such as Berlin or Munich, especially given the relatively low cost of living compared to other tech hubs like San Francisco. Nevertheless, we will continue to see an increasing number of companies scattered across multiple time zones building products that are inherently remote first, regardless where the general work environment will shift into.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

We are lucky in that our investment focus has been on sector verticals such as Logistics, Supply chain, manufacturing or the future of work, which have all captured significant tailwind from Covid.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

While our investment strategy on a high level will not change, we are putting longer sales cycles into consideration as potential customers of our portfolio companies now are focusing on capital efficiency which also holds true for our founders. Thus, we advise them to focus on extending the runway both by increasing capital efficiency as well as taking on additional funding.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

As our economy is still in the midst of dealing with the effects of COVID, it is too early to tell, but we definitely see positive indications driven by efforts of portfolio companies that could adapt quickly and shipped features catered to the current needs. One example is Personio, which extended their HR offerings with features that solve the need of customers who shifted to short-time work.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

What gave me hope was the cohesion of the German economy that fought together for solutions and support during these difficult times. One positive example was the German Startup Association that helped achieve additional governmental financial aid for German SMEs.

Any other thoughts you want to share with TechCrunch readers?

Similar to how the past financial crisis allowed companies such as Stripe or Shopify to become ubiquitous parts of our daily life, these unprecedented times now will also give birth to new forms and shapes in which new ideas will grow into large businesses and we are excited to partner up with founders willing to take a bet on that future.

Powered by WPeMatico

One of the most exciting moments in the life of every newly christened founder is the sweet relief of seeing a term sheet come in from an investor. After weeks, perhaps months (but hopefully not years!), of work fundraising and pitching, there is nothing like getting that email with a PDF attached to it laying out the terms and conditions of the VC relationship going forward.

Of course, that rejoicing dampens quickly as all the specific nuances of the deal suddenly come to the forefront. It’s one thing to get the valuation you want, or the amount of capital you are seeking, but what about the setup of the board of directors? What should you do about deal terms that may shape your startup for a decade or more?

The reality of term sheets, as our guest Lior Zorea discusses, is that the terms you agree to early on at a startup tend to be the terms that will carry through for the life of the company. That means getting that first term sheet right is critical for ensuring the financial and capital success of your business.

Powered by WPeMatico

Angel funding, seed investing and generally focusing on earlier stage investing is a huge business in the world of startups these days — it helps investors get in early to the most promising companies, and (because of the smaller size of the checks) allows for even the less prolific to spread their bets.

There was a time when it was immensely difficult for a founder to get a first check, not least because there were fewer people writing them. However, Jeff Clavier was an exception to that rule.

As the founder of Uncork Capital (formerly known as SoftTech VC), he has been in the business of angel and seed investing for 16 years, popularizing the opportunity and highlighting the need for more support at this stage — well before it was cool. You could say he was early to early stage.

Clavier said that at the end of 2019, it was estimated that there were more than 1,000 firms focusing on seed investing in the market, but by the end of this year, there will be about 2,000. “Don’t ask me whether it makes any sense because when I started 16 years ago, I didn’t think would be a big deal,” he said. “But certainly that creates a bit of a conundrum for founders to try and understand.”

As of now, Clavier has made nearly 230 investments and counting.

TechCrunch Early Stage, our virtual conference highlighting that stage of startup life, was the perfect venue to hear from him on all things seed investing and building startups today. Below are some highlights, a link to the video and a pitch deck he put together for the chat. Questions were edited for space and clarity.

First thing to understand is that not all VCs are created equal. There are a bunch of different firms, tons of them out there, and you as a founder need to understand what are the specifics of your pitch opportunity, how to match with the right firm, and to figure out what stage of “early” you happen to be.

Startups can be super early, or mid-stage, which is typically what we refer to as pre-seed. Then there’s the seed stage, where you have developed a product, with a demo. And there is post-seed, where you have product but are not quite ready to raise a Series A. So who are the firms that can actually be the right fit for me at those different stages? The qualification part of the targeting is really important. Especially in a COVID environment when you can’t spend the same kind of time with each other.

It’s useful for founders to try and understand investors better, maybe asking a couple of questions like, “When is the last time you made a brand new investment at seed stage?” And “How has your investment process changed as a result of COVID?”

For investors, you want to understand how you’re going to evolve your process to cope with the fact that you don’t spend time with those founders face-to-face. Some firms are still struggling with that.

At Uncork, we’re now past the point of portfolio triage that we had in the first few weeks of of the pandemic. What was surprising to me was the speed and velocity at which some deals actually.

Powered by WPeMatico

When Rent the Runway co-founders Jennifer Fleiss and Jennifer Hyman got their first term sheet, it had an exploding clause in it: If they didn’t sign the offer in 24 hours, they would lose the deal.

The co-founders, then students at Harvard Business School, were ready to commit, but their lawyer advised them to pause and attend the meetings they had previously set up with other investors.

Twelve years later, Rent the Runway has raised $380 million in venture capital equity funding from top investors like Alibaba’s Jack Ma, Temasek, Fidelity, Highland Capital Partners and T. Rowe Capital. Fleiss gave up an operational role in the company to a board seat in 2017, as the company reportedly was eyeing an IPO.

But the shoe didn’t always fit: Earlier this year, Rent the Runway struggled with supply chain issues that left customers disgruntled. Then, the pandemic threatened the market of luxury wear more broadly: Who needs a ball gown while Zooming from home? In early March, the business went through a restructuring, furloughing and laying off nearly half of its workforce, including every retail employee at its physical locations.

In 2009, Fleiss and Hyman were successful Harvard Business School students. Hyman’s college roommate knew a prominent lawyer who agreed to advise them on a contingency basis in exchange for connecting them with potential investors.

Still, fundraising “was extremely hard,” Hyman said. “We were in the middle of a recession and we were two young women at business school who had never really done anything before.”

Fleiss said venture capital firms often sent junior associates, receptionists and assistants to take the meeting instead of dispatching a full-time partner. “It was clear they weren’t taking us very seriously,” Fleiss said, recounting that on one occasion, a male investor called his wife and daughter on speaker to vet their thoughts.

In an attempt to test their thesis that women would pay to rent (and return) luxury clothing, Fleiss and Hyman started doing trunk pop-up shows with 100 dresses. On one occasion, they rented out a Harvard undergraduate dorm room common hall and invited sororities, student activity organizations and a handful of investors.

Only one person showed up, said Fleiss: A guy “who was 30 years older than anyone else in the room.”

Powered by WPeMatico