Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

At a time when more companies are building machine learning models, Arthur.ai wants to help by ensuring the model accuracy doesn’t begin slipping over time, thereby losing its ability to precisely measure what it was supposed to. As demand for this type of tool has increased this year, in spite of the pandemic, the startup announced a $15 million Series A today.

The investment was led by Index Ventures with help from newcomers Acrew and Plexo Capital, along with previous investors Homebrew, AME Ventures and Work-Bench. The round comes almost exactly a year after its $3.3 million seed round.

As CEO and co-founder Adam Wenchel explains, data scientists build and test machine learning models in the lab under ideal conditions, but as these models are put into production, the performance can begin to deteriorate under real-world scrutiny. Arthur.ai is designed to root out when that happens.

Even as COVID has wreaked havoc throughout much of this year, the company has grown revenue 300% in the last six months smack dab in the middle of all that. “Over the course of 2020, we have begun to open up more and talk to [more] customers. And so we are starting to get some really nice initial customer traction, both in traditional enterprises as well as digital tech companies,” Wenchel told me. With 15 customers, the company is finding that the solution is resonating with companies.

It’s interesting to note that AWS announced a similar tool yesterday at re:Invent called SageMaker Clarify, but Wenchel sees this as more of a validation of what his startup has been trying to do, rather than an existential threat. “I think it helps create awareness, and because this is our 100% focus, our tools go well beyond what the major cloud providers provide,” he said.

Investor Mike Volpi from Index certainly sees the value proposition of this company. “One of the most critical aspects of the AI stack is in the area of performance monitoring and risk mitigation. Simply put, is the AI system behaving like it’s supposed to?” he wrote in a blog post announcing the funding.

When we spoke a year ago, the company had eight employees. Today it has 17 and it expects to double again by the end of next year. Wenchel says that as a company whose product looks for different types of bias, it’s especially important to have a diverse workforce. He says that starts with having a diverse investment team and board makeup, which he has been able to achieve, and goes from there.

“We’ve sponsored and work with groups that focus on both general sort of coding for different underrepresented groups as well as specifically AI, and that’s something that we’ll continue to do. And actually I think when we can get together for in-person events again, we will really go out there and support great organizations like AI for All and Black Girls Code,” he said. He believes that by working with these groups, it will give the startup a pipeline to underrepresented groups, which they can draw upon for hiring as the needs arise.

Wenchel says that when he can go back to the office, he wants to bring employees back, at least for part of the week for certain kinds of work that will benefit from being in the same space.

Powered by WPeMatico

Funding-round stories are TechCrunch’s bread and butter.

For early-stage companies, the fact that an investor has put thousands, millions (or billions) into an idea that will likely fail, and might never make money, is big news. That’s a story that we can tell every day.

From time to time, a debate pops up about the role of funding-round stories: Are financings the right metric to focus on? Should the trend be scratched and reinvented? After all, raising money is not indicative of making money. Let’s be real: news needs news to be published. There needs to be a tension, or a surprise, but most of all, a reason for the reader to keep reading.

It’s a healthy conversation, and one the Equity crew decided to discuss last Friday:

It’s easy to mock funding-round coverage: There are far more rounds than hands to write them, so the coverage is inherently partial; they are a poor milestone to use as a benchmark for growth; and coverage of the startup in question nearly always has an overly positive tilt, given that the piece in question centers around something that is a win for the company.

Yet, I still think they are worth writing and try to get to a few each week.

There are good reasons for doing so that run counter to the obvious complaints. Sure, there are more rounds than we could ever cover, but in theory we’re filtering as best we can for the most interesting, the furthest outlying and the trend-elucidating rounds that we can use as a light to better illuminate how the broader startup and technology worlds are changing.

I think TechCrunch does a reasonable job of picking the right companies to cover and we spend a good amount of time aggregating discrete funding events into trends. It’s super-hard work, as covering a single round is time-consuming and ultimately not incredibly well-read.

And yes, funding rounds are not really milestones to celebrate. The startup isn’t suddenly destined to win. Capital just means that the venture class has increased its wager on the startup generating more wealth for themselves and their backers, whom are largely already rich.

But trying to lever any information from private companies is an exercise in sadistic dentistry, and startups tend to open up the most around funding rounds. So, if you want to chat with a CEO on the record for half an hour, the next time their startup raises is probably your best chance.

And there is signal in a venture round. Someone felt strongly enough about the company’s prospects to inject it with more capital, making a funding event a reasonable signal that something is going on at the company.

Then there’s the issue of positive bias. All publications have a bias. TechCrunch has many biases, the most important and salutary of which is that we think that startups are cool. We do! Quickly-growing, private companies are inherently interesting and I came back to this publication in part so that I could keep writing about them. I am never bored.

So, yes, funding-round coverage tends to be a bit more on the positive side of balanced than I would like, but I balance that by becoming increasingly orthodox as a startup scales. When a young company raises its first few million, the chat with the CEO is her telling me about her small team, first customers and fitful progress.

By the time she raises a $50 million Series C, we’re talking gross margin expansion, YoY ARR growth and diversity metrics. Before she takes her unicorn public, I’m asking pressing questions about GAAP results, the public markets and what sort of external offers are coming in for the whole concern.

Being slightly optimistic about startups when they’re young is, then, tempered by increasing scrutiny as the company grows. That seems like a fair balance for the company and our readers.

So I won’t stop covering funding rounds. Even if I didn’t have this job I probably still would for my personal blog. I always learn something from high-growth companies; they have a window into the market that is dynamic and far from ossified. And early-stage founders tend to not be overly media-trained, so they are still interesting.

And sometimes something you write winds up changing the direction of a startup. That’s always a very weird and disconcerting feeling. But as this impact is nearly always good for the company in question, you’ve only accidentally made the lives of others a bit better for a short while. It’s not so harsh a sentence.

Covering startups is one of the hardest news beats out there (trust me, I’m unbiased — I cover startups for a living).

If you cover the Senate, you report regularly on 100 individuals, their staffs and interactions. If you cover banking, you watch a handful of banks since no one gives a flying rat’s tushy about the industry’s middle market. There’s generally a limited scope in political and general business reporting where you know the key players and the key newsmakers.

In startups, you cover … everything. There are a couple of hot sectors that everyone is talking about … and then there is every other sector that might be the next hot sector, but no one has ever heard of it. It’s probably not important. But it might just be. That startup you talked to this week sounds boring. Four years later, it sells for $20 billion. The startup world is constantly changing, and unless you blow up your whole worldview on a regular basis, you’ll never keep up.

Powered by WPeMatico

Thoma Bravo must really like Flexera, an IT asset management company out of Chicago. The private equity firm bought the company for the second time today. Sources told TechCrunch the price was $2.85 billion.

Technically, Thoma Bravo is getting a majority stake in the company, buying it from previous owners TA Associates and Ontario Teachers’ Pension Plan Board. The firm originally bought Flexera in 2008 from Macrovision for just $200 million. It turned it around just three years later in 2011 for $1 billion profit, according to reports.

While reports last year had the company’s investors looking for $3 billion, they didn’t quite reach that mark, but it’s still a hefty profit as the company continues to change hands, giving each of its owners a substantial return on investment.

At $2.85 billion, Thoma Bravo will have a bigger challenge on its hands to make that same kind of return, but it sees a company it liked before and it still likes it, especially the management team, which to some degree at least remains intact.

“Jim [Ryan] and his team have positioned Flexera for sustained growth by focusing on the strategic challenges enterprises face with complex IT infrastructures,” Seth Boro, managing partner at Thoma Bravo said in a statement.

Ryan was pleased to see the company’s value continue to rise and to connect once again with Thoma Bravo. “This is a resounding vote of confidence in the growth Flexera has shown and the strategic initiatives we’ve undertaken to address the exponential challenges faced by organizations today,” he said in a statement.

Flexera was founded in 2008 and has bought 12 companies along the way, including five in the last couple of years, according to Crunchbase data. The deal is expected to close in the first quarter of next subject to regulatory approvals.

Powered by WPeMatico

Welcome, the HR software that helps organizations make and close offers to new candidates, announced the close of a $6 million seed round today, led by FirstMark Capital. Participating investors include Ludlow Ventures, Nat Turner and Zach Weinberg, and Keenan Rice and Ben Porterfield (which were existing investors), as well as a wide array of angels.

TechCrunch last covered Welcome in August, when it announced a $1.4 million funding round. That the startup was able to raise more as quickly as it has is testament to how hot the early-stage venture capital market is today, and likely an endorsement of Welcome’s economic profile and recent growth.

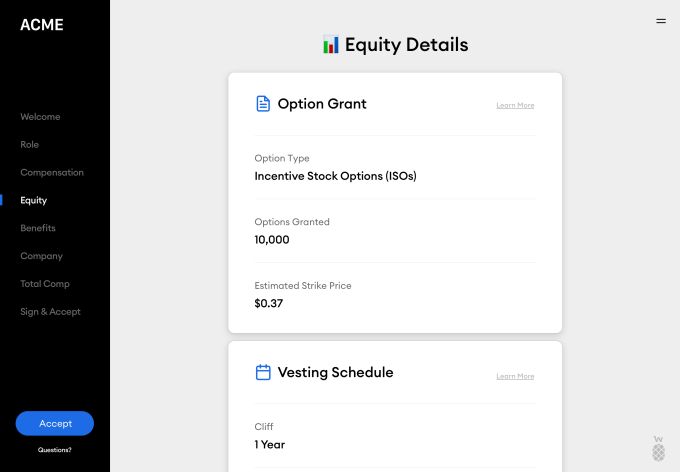

Past the new capital, Welcome is also launching a new product today called Total Rewards, which helps not just new candidates but also existing employees get a complete, easy-to-understand picture of their compensation, across salary, benefits, equity, etc.

But let’s back up.

Welcome was founded in 2019 by Nick Gavronsky and Rick Pereira, with a mission to help organizations close offers on candidates by providing a much clearer picture of compensation, particularly around equity. Co-founder and CEO Nick Gavronsky explained that many candidates don’t truly understand the value of the equity they’re offered, or how it works.

“A lot of recruiting teams aren’t well-equipped to use it as a selling tool and explain it effectively and showcase the value to candidates to help them think about their ownership at the company,” he added.

Image Credits: Welcome

Welcome allows companies to organize their compensation offers based on level and position, and deliver that information digitally to candidates in a way that makes sense.

The startup integrates with a variety of other software providers, including Slack, Lever, Greenhouse, ADP and Justworks to name a few, simplifying onboarding for Welcome clients and bringing a broad array of information into one place.

Offers sent through Welcome show a description of the role, equity details, total compensation and even include a welcome note and video. This is in stark contrast to the black and white legal PDF often sent to candidates.

Image Credits: Welcome

The next phase for the company comes in the form of the launch of Total Rewards, which is meant to help retain existing employees, helping them understand their compensation value and their potential at the company.

“Painting a better picture becomes a pre-retention tool,” said Gavronsky. “An employee will sometimes leave thousands of dollars on the table because they don’t understand what they’re walking away from. A lot of times companies will wait until that person is going to resign. Let me now bring up all the things that are great about our company and talk through your stock options. But the decision’s already made. So we wanted something that we can kind of put in with performance reviews.”

Welcome also has plans to offer a third product pillar in the form of real-time accurate industry-wide compensation data, helping companies understand where they fit into the larger ecosystem with regards to compensation.

Thus far, Welcome has 40 companies on the platform, including Uncork and Betterment, with hundreds on the waitlist, according to the co-founders. The company plans to use the funding to build out the team and the product.

Powered by WPeMatico

If I were to pick one thing that unites the global tech scene in terms of culture I would point to the respect and reverence accorded to startup founders.

After all, creating your own company is an ambition many of us harbor. It can bring with it unparalleled freedom, a lasting legacy, prestige, wealth and the ability to do good. Across social and traditional media the feats of founders big and small are lauded for their genius on a daily basis. Many entrepreneurs go to great lengths to showcase their backbreaking hard work and eye-popping success. An outsider would be forgiven for believing that every founder is living the dream as a result of their talent and toil.

Of course, as with nearly every image projected online, the reality is quite different. There is a seldom talked about price of being a founder — the impact on one’s mental health.

A recent study by the National Institute of Mental Health found that 72% of entrepreneurs are directly or indirectly impacted by mental health issues. This compares to 48% of the general population. The damage can also affect loved ones — 23% of entrepreneurs report that they have family members with problems, which is 7% higher than the relations of nonentrepreneurs.

I am in no way a mental health expert. But what I do know from both my own experience and speaking to scores of business owners I work with is that being a founder is an inherently lonely job. Pressure is high and uncertainty pervades every decision. Fear of failure is ever present. Unaddressed, these issues can take a serious toll.

The unpalatable truth is that the situation appears to be getting worse. A similar study conducted in 2015 by Dr. Michael A. Freeman found the rate of mental health issues among founders to be lower — at 50%. While comparing different research pieces is inexact, we only need to look at how the global recession has damaged many companies and how working from home has contributed to feelings of isolation, to know that the environment for startups has got harder this year. Added to this mix is how social media continues to promote an unhealthy fetishization of hustle culture and founding myths.

A number of founders have told me that they have constant feelings of inadequacy and guilt when they compare themselves to the startup gurus who celebrate working 24/7, are constantly selling, raising money or making their millions. They feel they should be working harder or be doing better — just like all the people they read about.

So how do we address this? The first step is talking about it. This means having an environment where we can be honest that not everything is always fine. Speaking to a fellow founder, not about commercial concerns, but about personal worries can be revelatory. I’ve seen it happen in our community. It’s like an “Emperor’s New Clothes” moment.

The myth of the bulletproof, genius, hustling founder can disappear in a puff of smoke as people suddenly realize they are not alone. They find that the concerns, anxieties and uncertainties they feel are almost universal.

Experienced founders can provide invaluable support to people new to the startup scene. They can share their experiences, both failures and success, and reveal some of their coping mechanisms. I would strongly advise founders who are experiencing some of the worries I’ve outlined to actively seek out advice from both their peers and potential mentors — much in the way they may seek out commercial guidance.

Next, we need to address how we tackle the culture and myths around being a founder. Business owners need to know that many of the extraordinary “success stories” they see celebrated online are exactly that — extraordinary.

Similarly, those that promote the principle that working all hours is the only way to be successful are at best talking about what works for them, and are at worst, engaging in a performance to achieve attention. We need to think carefully about how we respond to these posts. There is a fine line between being supportive and enabling unhealthy or damaging behavior and philosophy.

After all, success in the startup scene is all relative. For some owning a small business that makes them a decent income with a good work-life balance is the goal. For others, it is simply being able to do what they love in the way that they want. Very few will get the exit that makes them a millionaire, and an infinitesimally small minority will build the next Facebook . I cannot stress enough how important it is for founders to keep their aims and ambitions in perspective and ignore the noise they hear online.

More broadly, the industry, including the media, does need to get wiser about how it views and represents founders. For example, a pervasive myth is that some of the biggest tech companies in the world started in garages with no money, then through the genius and sheer bloodymindedness of their founder they were grown into a massive corporation.

The reality is that the vast majority of these tech companies benefited from substantial seed capital from family or connections almost from day one. These founders were also quickly surrounded by highly talented people who did a lot of the heavy lifting and, whisper it, a truckload of good luck. In short, the idea of the superhuman founder perpetuated in the industry is, in nearly all cases, nonsense.

In a similar vein, there are also issues around how we frame success and failure.

Success, as I’ve mentioned earlier, is nearly always couched in the most basic numerical terms. The “unicorn” label is bandied about so often that many people fail to realize that it’s simply a valuation that a few investors have given a company. It does not reflect whether the business is actually successful in the traditional sense, i.e., making money. Generally, the startup scene celebrates and idolizes founders who make big exits or achieve “unicorn status” — less is spoken about the thousands of SMEs that employ people, develop and patent new tech, make a tidy profit and pay taxes.

With failure, there is an altogether different problem. The startup scene downplays failure as par for the course. It is, on the face of it, one of the industry’s great virtues. It enables people to try without fear of embarrassment. However, in practice, it can actually minimize real-world fears nearly all founders have. Failure cannot just be brushed off if you’ve devoted years of your life, spent a lot of money and have staff who rely on you. By simply thinking of failure as part of the process we cannot address and talk about this real source of concern in an open way. “Fail fast” only works for those who can afford it.

Individually, these issues may seem like nothing but white noise and the cure for suffering founders may simply be to get off social media. Unfortunately, it isn’t that simple. Social and traditional media is amplifying startup culture, not creating it. The same tropes are on display at every tech conference and meetup. To fit in, the founder is expected to be a fearless, genius visionary. Deviation from this norm, such as by displaying vulnerability around mental health, is by inference, failure.

Despite its shortcomings in relation to diversity, the startup scene is generally one of the most progressive, collaborative and open industries in the world. These virtues are ideally suited to tackling the reluctance to discuss mental health and creating the network of support that ensures people don’t suffer alone.

To make this happen, we need to dispense with the myths and hagiography around being a founder and be more honest about what the reality of running a business actually entails.

Powered by WPeMatico

BuildBuddy, whose software helps developers compile and test code quickly using a blend of open-source technology and proprietary tools, announced a funding round today worth $3.15 million.

The company was part of the Winter 2020 Y Combinator batch, which saw its traditional demo day in March turned into an all-virtual affair. The startups from the cohort then had to raise capital as the public markets crashed around them and fear overtook the startup investing world.

BuildBuddy’s funding round makes it clear that choppy market conditions and a move away from in-person demos did not fully dampen investor interest in YC’s March batch of startups, though it’s far too soon to tell if the group will perform as well as others, given how long it takes for startup winners to mature into exits.

BuildBuddy has foundations in how Google builds software. To get under the skin of what it does, I got ahold of co-founder Siggi Simonarson, who worked at the Mountain View-based search giant for a little over a half decade.

During that time he became accustomed to building software in the Google style, namely using its internal tool called Blaze to compile his code. It’s core to how developers at Google work, Simonarson told TechCrunch. “You write some code,” he added, “you run Blaze build; you write some code, you run Blaze test.”

What sets Blaze apart from other developer tools is that “opposed to your traditional language-specific build tools,” Simonarson said, it’s code agnostic, so you can use it to “build across [any] programming language.”

Google open-sourced the core of Blaze, which was named Bazel, an anagram of the original name.

So what does BuildBuddy do? In product terms, it’s building the pieces of Blaze that Google engineers have access to inside the company, for other developers using Bazel in their own work. In business terms, BuildBuddy wants to offer its service to individual developers for free, and charge companies that use its product.

Simonarson and his co-founder Tyler Williams started small, building a “results UI” tool that they shared with a Bazel user group. The members of that group picked up the tool, rapidly bringing it inside a number of sizable companies.

This origin story underlines something that BuildBuddy has that early-stage startups often lack, namely demonstrable enterprise market appetite. Lots of big companies use Bazel to help create software, and BuildBuddy found its way into a few of them early in its life.

Simply building a useful tool for a popular open-source project is no guarantee of success, however. Happily for BuildBuddy, early users helped it set direction for its product development, meaning that over the summer the startup added the features that its current users most wanted.

Simonarson explained that after BuildBuddy was initially used by external developers, they demanded additional tools, like authentication. In the words of the co-founder, the response from the startup was “great!” The same went for a request for dashboarding, and other features.

Even better for the YC graduate, some of the features requested were the sort that it intends to charge for. That brings us back to money and the round itself.

BuildBuddy closed its round in May. But like with most venture capital tales, it’s not a simple story.

According to Simonarson, his startup started raising the round during one of those awful early-COVID days when the stock market dropped by double-digit percentage points in a single trading session.

BuildBuddy’s goal was to raise $1.5 million. Simonarson was worried at the time, telling TechCrunch that it was his first time fundraising, and that he wasn’t sure if his startup was going to “raise anything at all” in that climate.

But the nascent company secured its first $100,000 check. And then a $300,000 check, over time managing to fill out its round.

So what happened that got the company from $1.5 million to just over $3 million? The investor that put in $300,000 wanted to put in another $2 million. The company talked them down to $1.5 million at a higher cap (BuildBuddy raised its round using a SAFE), and the deal was done at those terms.

The startup initially didn’t want to raise the extra cash, but Simonarson told TechCrunch that at the time it was not clear where the fundraising environment was heading; BuildBuddy raised back when startup layoffs were a leading story, and a return to high-cadence VC rounds was months away.

So BuildBuddy wound up securing $3.15 million to support a current headcount of four. It intends to hire, naturally, lower its comically long runway and keep building out its Bazel-focused service.

Picking a few names from the investor spreadsheet that BuildBuddy sent over — points for completeness to the startup — Y Combinator, Addition, Scribble and Village Global, among others put capital into the round.

Dev tools are hot at the moment. Given that, as soon as BuildBuddy’s ARR starts to get moving, I expect we’ll hear from them again.

Powered by WPeMatico

Floww — a data-driven marketplace designed to allow founders to pitch investors, with the whole investment relationship managed online — says it has raised $6.7 million (£5 million) to date in seed funding from angels and family offices. Investors include Ramon Mendes De Leon, Duncan Simpson-Craib, Angus Davidson, Stephane Delacote and Pip Baker (Google’s head of Fintech U.K.) and multiple family offices. The cash will be used to build out the platform designed to give startups access to more than 500 VCs, accelerators and angel networks.

The team consists of Martijn De Wever, founder and CEO of London-based VC Force Over Mass; Lee Fasciani, co-founder of Territory Projects (the firm behind film graphics and design including “Guardians of the Galaxy” and “BladeRunner 2049”); and CTO Alex Pilsworth, of various fintech startups.

Having made more than 160 investments himself, De Wever says he recognized the need for a platform connecting investors and startups based on merit, clean data and transparency, rather than a system built on “warm introductions,” which can have inherent cultural and even racial biases.

Floww’s idea is that it showcases startups based on merit only, allowing founders to raise capital by providing investors with data and transparency. Startups are given a suite of tools and materials to get started, from cap table templates to “How To” guides. Founders can then “drag and drop” their investor documents in any format. Floww’s team of accountants then cross-checks the data for errors and processes key performance metrics. A startup’s digital profile includes dynamic charts and tables, allowing prospective investors to see the company’s business potential.

Floww charges a monthly fee to VCs, accelerators, family offices and PE firms. Startups have free access to the platform, and a premium model to contact and send their deal to multiple VCs.

Floww’s pitch is that VCs can, in turn, manage deal-sourcing, CRM, as well as reporting to their investors and LPs. Quite a claim, given all VCs to date handle this kind of thing in-house. However, Floww claims to have processed 3,000 startups and says it is rolling out to more than 500 VCs.

In a statement, De Wever said: “In an age of virtual meetings and connections, the need for coffee meetings on Sand Hill Road or Mayfair is gone. What we need now are global connections, allowing VCs to engage in merit-based investing using data and metrics.” He says the era of the coronavirus pandemic means many deals will have to be sourced remotely now, so “the time for a platform like this is now.”

AngelList is perhaps its closest competitor from the startup perspective. And the VC application incorporates the kind of functionality seen in Affinity, Airtable, Efront and DocSend. But AngeList doesn’t provide data or metrics.

Powered by WPeMatico

Vista Equity Partners hasn’t been shy about scooping up enterprise companies over the years, and today it added to a growing portfolio with its purchase of Gainsight. The company’s software helps clients with customer success, meaning it helps create a positive customer experience when they interact with your brand, making them more likely to come back and recommend you to others. Sources pegged the price tag at $1.1 billion.

As you might expect, both parties are putting a happy face on the deal, talking about how they can work together to grow Gainsight further. Certainly, other companies like Ping Identity seem to have benefited from joining forces with Vista. Being part of a well-capitalized firm allowed them to make some strategic investments along the way to eventually going public last year.

Gainsight and Vista are certainly hoping for a similar outcome in this case. Monti Saroya, co-head of the Vista Flagship Fund and senior managing director at the firm, sees a company with a lot of potential that could expand and grow with help from Vista’s consulting arm, which helps portfolio companies with different aspects of their business like sales, marketing and operations.

“We are excited to partner with the Gainsight team in its next phase of growth, helping the company to expand the category it has created and deliver even more solutions that drive retention and growth to businesses across the globe,” Saroya said in a statement.

Gainsight CEO Nick Mehta likes the idea of being part of Vista’s portfolio of enterprise companies, many of whom are using his company’s products.

“We’ve known Vista for years, since 24 of their portfolio companies use Gainsight. We’ve seen Gainsight clients like JAMF and Ping Identity partner with Vista and then go public. We believe we are just getting started with customer success, so we wanted the right partner for the long term and we’re excited to work with Vista on the next phase of our journey,” Mehta told TechCrunch.

Brent Leary, principle analyst at CRM Essentials, who covers the sales and marketing space, says that it appears that Vista is piecing together a sales and marketing platform that it could flip or go public in a few years.

“It’s not only the power that’s in the platform, it’s also the money. And Vista seems to be piecing together an engagement platform based on the acquisitions of Gainsight, Pipedrive and even last year’s Acquia purchase. Vista isn’t afraid to spend big money, if they can make even bigger money in a couple years if they can make these pieces fit together,” Leary told TechCrunch.

While Gainsight exits as a unicorn, the deal might not have been the outcome it was looking for. The company raised more than $187 million, according to PitchBook data, though its fundraising had slowed in recent years. Gainsight raised $50 million in April of 2017 at a post-money valuation of $515 million, again per PitchBook. In July of 2018 it added $25 million to its coffers, and the final entry was a small debt investment raised in 2019.

It could be that the startup saw its growth slow down, leaving it somewhere between ready for new venture investment and profitability. That’s a gap that PE shops like Vista look for, write a check, shake up a company and hopefully exit at an elevated price.

Gainsight hired a new chief revenue officer last month, notably. Per Forbes, the company was on track to reach “about” $100 million ARR by the end of 2020, giving it a revenue multiple of around 11x in the deal. That’s under current market norms, which could imply that Gainsight had either lower gross margins than comparable companies, or as previously noted, that its growth had slowed.

A $1.1 billion exit is never something to bemoan — and every startup wants to become a unicorn — but Gainsight and Mehta are well known, and we were hoping for the details only an S-1 could deliver. Perhaps one day with Vista’s help that could happen.

Powered by WPeMatico

Startups need to live in the future. They create roadmaps, build products and continually upgrade them with an eye on next year — or even a few years out.

Big companies, often the target customers for startups, live in a much more near-term world. They buy technologies that can solve problems they know about today, rather than those they may face a couple bends down the road. In other words, they’re driving a Dodge, and most tech entrepreneurs are driving a DeLorean equipped with a flux-capacitor.

That situation can lead to a huge waste of time for startups that want to sell to enterprise customers: a business development black hole. Startups are talking about technology shifts and customer demands that the executives inside the large company — even if they have “innovation,” “IT,” or “emerging technology” in their titles — just don’t see as an urgent priority yet, or can’t sell to their colleagues.

How do you avoid the aforementioned black hole? Some recent research that my company, Innovation Leader, conducted in collaboration with KPMG LLP, suggests a constructive approach.

Rather than asking large companies about which technologies they were experimenting with, we created four buckets, based on what you might call “commitment level.” (Our survey had 211 respondents, 62% of them in North America and 59% at companies with greater than $1 billion in annual revenue.) We asked survey respondents to assess a list of 16 technologies, from advanced analytics to quantum computing, and put each one into one of these four buckets. We conducted the survey at the tail end of Q3 2020.

Respondents in the first group were “not exploring or investing” — in other words, “we don’t care about this right now.” The top technology there was quantum computing.

Bucket #2 was the second-lowest commitment level: “learning and exploring.” At this stage, a startup gets to educate its prospective corporate customer about an emerging technology — but nabbing a purchase commitment is still quite a few exits down the highway. It can be constructive to begin building relationships when a company is at this stage, but your sales staff shouldn’t start calculating their commissions just yet.

Here are the top five things that fell into the “learning and exploring” cohort, in ranked order:

Technologies in the third group, “investing or piloting,” may represent the sweet spot for startups. At this stage, the corporate customer has already discovered some internal problem or use case that the technology might address. They may have shaken loose some early funding. They may have departments internally, or test sites externally, where they know they can conduct pilots. Often, they’re assessing what established tech vendors like Microsoft, Oracle and Cisco can provide — and they may find their solutions wanting.

Here’s what our survey respondents put into the “investing or piloting” bucket, in ranked order:

By the time a technology is placed into the fourth category, which we dubbed “in-market or accelerating investment,” it may be too late for a startup to find a foothold. There’s already a clear understanding of at least some of the use cases or problems that need solving, and return-on-investment metrics have been established. But some providers have already been chosen, based on successful pilots and you may need to dislodge someone that the enterprise is already working with. It can happen, but the headwinds are strong.

Here’s what the survey respondents placed into the “in-market or accelerating investment” bucket, in ranked order:

Powered by WPeMatico

Listen up, space fans and aficionados. You have just 48 hours left to secure an early-bird ticket to TC Sessions: Space 2020, a two-day virtual conference dedicated to early-stage space startups and the community that supports them. Join the brilliant minds, leading founders, shrewd investors and boundary-pushing engineers determined to shape the future of space exploration and everything that entails.

Early-bird pricing remains in orbit for another 48 hours. Buy your ticket ($125) before the orbit decays on November 13 at precisely 11:59 p.m. (PT) and save $100.

You’ll have an outstanding selection of presentations, interviews, panel discussions, breakout sessions and interactive Q&As available at the click of your mouse. Expert speakers — spanning the public, private and defense sectors — will share a veritable galaxy of wisdom, experience and insight.

What level of expertise are we talking here? Well, and this is just for starters, we have NASA Associate Administrator of Human Exploration & Operations Mission Directorate Kathryn Lueders, Rocket Lab CEO Peter Beck, U.S. Space Force Chief of Space Operations General Jay Raymond, Lockheed Martin VP and Head of Civil Space Programs Lisa Callahan.

Topics cover a broad swath of technologies, including 3D-printed rockets, earth observation data, orbital operations, ground station networks, launch services, broadband communications, defense operations and manufacturing in space. Explore the event agenda here.

You’ll find up-and-coming early-stage startups and sponsors showcasing their technology in our expo area. See the latest innovations and connect with potential customers, collaborators or investors. And be sure to take advantage of CrunchMatch. Our free AI-based platform takes the pain out of networking and helps you find and connect with the people who align with your goals. It’s the perfect tool to bridge a virtual conference and connect with attendees around the globe.

If you want to showcase your startup in the expo, buy a Startup Exhibitor Package. The price includes three passes, online exhibit space and lead-generation capability. Here’s a hot opportunity — each exhibiting startup gets five minutes to pitch live to Session attendees. Talk about focused exposure.

Pro Pitch Tip: Have a team member hit record right before you step up to the virtual stage, and you’ll have a video of your TC Session pitch — study it for ways to improve or hey, it could be a straight-up marketing tool right out of the gate.

Don’t miss your opportunity to learn from, engage and connect with other brilliant members of your elite community at TC Sessions: Space 2020 on December 16-17. Don’t space out on early-bird savings — only 48 hours left! Purchase your ticket before November 13 at 11:59 p.m. (PT).

Is your company interested in sponsoring TC Sessions: Space 2020? Click here to talk with us about available opportunities.

Powered by WPeMatico