Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

Earlier this year, 15 top U.S. universities joined forces to launch a one-stop shop where corporations and startups can discover and license patents.

Working in concert, Brown, Caltech, Columbia, Cornell, Harvard, the University of Illinois, Michigan, Northwestern, Penn, Princeton, SUNY Binghamton, UC Berkeley, UCLA, the University of Southern California and Yale formed The University Technology Licensing Program LLC (UTLP) to create a centralized pool of licensable IP.

The UTLP arrives as more higher education institutions are beefing up their investment in the entrepreneurial pipeline to help more students launch startups after graduation. In some instances, schools serve as accelerators, providing students with resources and helping them connect with VCs to find seed funding.

To get a better look at the new program and more insight into the university-to-startup pipeline, we spoke to:

Orin Herskowitz: The UTLP effort is really much more about licensing to the somewhat broken interface between universities and very large companies in the tech space when it comes to licensing intellectual property. But I know USC and Columbia and many of our peers, especially over the last three to seven years, have pivoted in a massive way to helping our faculty students fulfill their entrepreneurial dreams and launch startups around this exciting university technology.

Orin Herskowitz: Universities have traditionally been a source of amazing, life-saving and life-improving inventions, for decades. There’s been a ton of new drugs and medical devices, cybersecurity improvements, and search engines, like Google, that have come out of universities over the years, that were federally funded and developed in the labs, and then licensed to either a startup or the industry. And that’s been great. At least over the last couple of decades, that interface has worked really, really well in some fields, but less well in others. So, in the life sciences, in energy, in advanced materials, in those industries, a lot of the time, these innovations that end up having a huge impact on society are based really on one or two or three core eureka moments. There’s like one or two patents that underlie an enormous new cancer drug, for instance.

In the tech space though, it’s a very different dynamic because, a lot of the time, these inventions are incredibly important and they do launch a whole new generation of products and services, but the problem is that a new device, like an iPhone, or a piece of software, might rely on dozens or even hundreds of innovations from across many different universities, as opposed to just one or two.

Jennifer Dyer: We’ve all had this renewed focus on innovation within the university and really helping our students and faculty that want to start companies, launch those companies. If you look at the space, helping educate our students that launching a company in a high-tech space may mean that they have to go out and acquire 100 different licenses, so maybe it doesn’t make sense. We’re going to be doing nonexclusive licensing, and it doesn’t preclude anyone from moving forward with this technology. This is probably the first pool for nonstandard essential patents in the high-tech space, which makes it somewhat unique. Because if you look back, most of the pools have been around standard essential patents.

Powered by WPeMatico

Since last year, we’ve been tracking the growing list of capitalists who got into the SPAC game. You can read an interview we conducted with Amish Jani, the co-founder of FirstMark Capital, about his SPAC here. And if you need a refresher on all things SPAC, we have that for you as well.

This morning, I want to better understand the trend by parsing a few new venture capitalist SPACs. We’ll examine Lerer Hippeau Acquisition Corp. and Khosla Ventures Acquisition Co. I, II and III. The SPACs are, somewhat obviously, associated with New York-based Lerer Hippeau and Menlo Park’s Khosla Ventures. And all four dropped formal S-1 filings last week.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Today’s topic may sound dry, but it really does matter. As we’ve reported, Lux Capital is in on the SPAC wager, along with Ribbit and, of course, SoftBank. Adding our latest names to the mix and you have to wonder if every VC worth a damn in the future will have their own raft of SPAC offerings.

In that way, as some late-stage venture capital funds invest earlier — and now later — full-service VC outfits will offer first check to final liquidity, will such a full-stack venture outfit be able to win more deals than a group offering a limited set of financing options? If so, the recent venture capital SPAC wave could become more of a rising tide in time, to torture a metaphor.

In that way, as some late-stage venture capital funds invest earlier — and now later — full-service VC outfits will offer first check to final liquidity, will such a full-stack venture outfit be able to win more deals than a group offering a limited set of financing options? If so, the recent venture capital SPAC wave could become more of a rising tide in time, to torture a metaphor.

Regardless, let’s quickly parse what Khosla and Lerer Hippeau are telling public investors about why they will be great SPACers before working our way backward to what the resulting pitch must be to startups themselves.

The Lerer Hippeau SPAC is the most interesting of the two firms’ combined four offerings, so we’ll start there. That isn’t to diss Khosla, but the Lerer Hippeau blank check has some explicit wording I want to highlight.

From the Lerer Hippeau Acquisition Corp. S-1 filing, read the following (bolding: TechCrunch):

As our seed portfolio matured over the last decade, we added a growth strategy to our platform through our select funds. This capital enables us to continue providing financial support to our top performing early-stage companies as they scale, and to selectively make new investments in later-stage companies in the Lerer Hippeau network. With our portfolio now maturing to the stage at which many are considering the public markets, we view SPACs as a natural next step in the evolution of our platform.

After writing that it has had four portfolio companies “publicly announced business combination agreements with SPACs” and noting that it expects more of the same, Lerer Hippeau added that it considers its “expansion into the SPAC market as a highly complementary element of our strategy to support founders throughout their entrepreneurial journeys.”

Powered by WPeMatico

Knife Capital, a South African venture capital firm, is raising a $50 million fund for startups looking to raise Series B financing. With Knife Fund III called the African Series B Expansion Fund, the firm seeks to directly invest in the aggressive expansion of South African breakout companies. It also plans to co-invest in companies across the rest of Africa.

The first fund, known as Knife Capital Fund I or HBD Venture Capital, was a closed private equity fund managed by Eben van Heerden and Keet van Zyl. The firm offered seed capital to startups. It also generated significant exits from its portfolio — Visa acquisition of fintech startup Fundamo, and orderTalk’s acquisition by UberEats come to mind.

In 2016, the VC firm launched its current 12J offering with Knife Capital Fund II. The fund (KNF Ventures), which invests primarily in Series A stage, has eight startups in its portfolio. Last year the firm told TechCrunch of its intention to extend the Fund II and open to new investors. The plan was to give startups access to networks, money and expansion opportunities.

“We want to help South African and African companies internationalize,” said co-managing partner Andrea Bohmert at the time. A testament to its cause, one of its portfolio companies, DataProphet, raised $6 million Series A to expand into the U.S. and Europe.

Bohmert tells TechCrunch that the third fund aims to address the critical Series B funding gap that has characterised the venture capital asset class in South Africa, resulting in businesses not reaching full potential or exiting too early.

“Lately, we see an increase in companies able to raise $2 million to $5 million funding rounds. And while the companies are operating within their home country, in our case South Africa, such amounts take you far due to the local cost structure,” Bohmert says. “However, once these companies start gaining international traction and need to build an infrastructure outside of their home country, they need to raise significant amounts to afford so. There are currently hardly any South African VC funds, perhaps other than Naspers Foundry, that can write checks of $5 million or more and are willing to deploy them to finance the externalization of South African companies into larger markets.”

As a result, Bohmert argues that Africa has become an incubator for international VCs who can write these checks but cannot provide the local support most of these companies still need. Likewise, there are instances where international investors actively search for local co-investors in South Africa to invest in a round, and not finding one might blow the chances of them going further with the investment. This is the gap Knife Capital intends to fill by launching this fund, Bohmert says.

“We want to be the local lead investor of choice for South African technology companies looking to internationalise, co-investing with international investors who can lead the Series B discussion and further.”

This week, Knife Capital secured $10 million from Mineworkers Investment Company (MIC), a South Africa-based investment firm. The commitment positions MIC as an anchor investor to the fund alongside other local and international investors.

Nchaupe Khaole, the CIO at MIC, explained that the move to change the way local institutional investors approach venture capital investment has been in MIC’s pipeline for a while. And by partnering with Knife Capital, this idea can begin to materialize.

“Our commitment brings to the table the investment, along with many of our strengths as an experienced player. One of which is our ability to influence the companies within our portfolio to partner with us and effect real, tangible change to the South African economy. We are delighted to be a key catalyst in the success of this funding round,” he said.

As per other details, Knife Capital aims for a first close by May and a final close by the end of the year. Most of its participation will be co-investing, and the idea is to do that in 10 to 12 companies.

Powered by WPeMatico

Demetrius Curry has spent the last couple years chasing a dream.

His startup, College Cash, allows brands to petition users to create photo and video marketing content highlighting their product or service, with the wrinkle being that content creators are paid by the brands in the form of credits that go directly toward paying down their student loan debt. This model awards the brands involved a level of social good will and tax benefits.

The Dallas-area founder was inspired to tackle the student loan debt crisis after talking with his daughter about the prospect of eventually paying down her own loan debt. Curry has spent the past two years building out the nascent platform, tracking down brand partners, navigating accelerator programs, enticing users and pounding the pavement to find investors willing to bet on his vision.

College Cash has raised $105,000 to date, and is hoping to eventually wrap the funding into a $1 million seed round.

Filling out the round has been its own challenge for Curry, who has struggled at times to find opportunity, even among historic levels of capital flowing into the startup ecosystem, a distinction that has been less noticeable for black founders that still make up just a small percentage of VC allocation. In the aftermath of last summer’s protests against police brutality, a number of venture capital firms issued statements decrying institutional racism and pledging to back more underserved founders, spinning up new programs for diverse founders.

Demetrius Curry, CEO of College Cash

While Curry says he appreciates the scope of the problem and the good intentions of those making the statements, he believes that venture capital networks still have a lot to learn about what being an “underserved” founder means, and that plenty of the existing efforts feel like “lip service.” He says that even as Silicon Valley continues to idolize dropouts from prestigious universities, stakeholders have less interest in recognizing the accomplishments of founders who fought their way through poverty or found opportunity in geographies where opportunities are harder to come by.

“You can’t look for something different if you’re looking in the same places,” Curry tells TechCrunch. “When you look at the topic of ‘underserved founders,’ it’s not only a skin color thing, it’s also about where they came from and what they’ve been through.”

Curry says that it can be frustrating to compete for early-stage opportunities when investors aren’t willing to meaningfully adjust their parameters. Of particular frustration to Curry has been navigating the world of “warm introductions” to even get a foot in the door for programs meant for diverse founders, or applying for early-stage programs geared toward the “underserved” only to be told that they weren’t far enough along to qualify.

“Think about how much we had to go through to even get in the room with you,” Curry says. “I’ve sold plasma to pay a web hosting fee, nothing is going to stop me.”

College Cash’s mission of expanding opportunities for people struggling to manage their student loan debt is personal to Curry, who saw his life turn around after going back to school.

Decades ago, fresh out of the military, Curry said he had a random conversation with a stranger while eating at a Hardee’s — the discussion about what more he wanted from life ended up pushing him to to go back and get his GED and later a business degree. What followed was a career in finance that eventually led toward his recent entrepreneurial pursuits with College Cash.

The platform is firmly an early-stage venture at the moment, but Curry has big ambitions he’s building toward. His next effort is building out a College Cash tipping integration with gig economy platforms, with the aim that users of those platforms could ultimately opt to tip a worker and route that money directly toward paying down that person’s student loan debt.

Curry says the team at College Cash has been working with a “national gig economy platform” to run a pilot of the integration and has run focus groups showing that users are more likely to tip when they know that money goes toward erasing loan debt.

Powered by WPeMatico

Shell’s plan to roll out 500,000 electric charging stations in just four years is the latest sign of an EV charging infrastructure boom that has prompted investors to pour cash into the industry and inspired a few companies to become public companies in search of the capital needed to meet demand.

Since the beginning of the year, three companies have been acquired by special purpose acquisition vehicles and are on a path to go public, while a third has raised tens of millions from some of the biggest names in private equity investing for its own path to commercial viability.

The SPAC attack began in September when an electric vehicle charging network ChargePoint struck a deal to merge with special purpose acquisition company Switchback Energy Acquisition Corporation, with a market valuation of $2.4 billion. The company’s public listing will debut February 16 on the New York Stock Exchange.

In January, EVgo, an owner and operator of electric vehicle charging infrastructure, agreed to merge with the SPAC Climate Change Crisis Real Impact I Acquisition for a valuation of $2.6 billion — a huge win for the company’s privately held owner, the power development and investment company LS Power. LS Power and EVgo management, which today own 100% of the company, will be rolling all of its equity into the transaction. Once the transaction closes in the second quarter, LS Power and EVgo will hold a 74% stake in the newly combined company.

One more deal soon followed. Volta Industries agreed to merge this month with Tortoise Acquisition II, a tie-up that would give the charging company named after battery inventor Alessandro Volta a $1.4 billion valuation. The deal sent shares of the SPAC company, trading under the ticker SNPR, rocketing up 31.9% in trading earlier this week to $17.01. The stock is currently trading around $15 per share.

Not to be outdone, private equity firms are also getting into the game. Riverstone Holdings, one of the biggest names in private equity energy investment, placed its own bet on the charging space with an investment in FreeWire. That company raised $50 million in a new round of funding earlier this year.

“The writing is on the wall and the investors have to take the time. There’s been a flight out of the traditional investment opportunities in markets,” said FreeWire chief executive Arcady Sosinov, in an interview. “There’s been a flight out of the oil and gas companies and out of the traditional utilities. You have to look at other opportunities… This is going to be the largest growth opportunity of the next 10 years.”

FreeWire deploys its infrastructure with BP currently, but the company’s charging technology can be rolled out to fast food companies, post offices, grocery stores or anywhere people go and spend somewhere between 20 minutes and an hour. With the Biden administration’s plan to boost EV adoption in federal fleets, post offices actually represent another big opportunity for charging networks, Sosinov said.

“One of the reasons we find electrification of mobility so attractive is because it’s not if or how, it’s when,” said Robert Tichio, a partner at Riverstone in charge of the firm’s ESG efforts. “Penetration rates are incredibly low… compare that to Norway or Northern Europe. They have already achieved double-digit percentages.”

A recent Super Bowl commercial from GM featuring Will Farrell showed just how far ahead Norway is when it comes to electric vehicle adoption.

“The demands on capital in the electrification of transport will begin to approach three quarters of a trillion annually,” Tichio said. “The short answer to your question is that the needs for capital now that we have collectively, politically, socially economically come to a consensus in terms of where we’re going and we couldn’t say that 18 months ago is going to be at a tipping point.”

Shell already has electric vehicle charging infrastructure that it has deployed in some markets. Back in 2019 the company acquired the Los Angeles-based company Greenlots, an EV charging developer. And earlier this year Shell made another move into electric vehicle charging with the acquisition of Ubitricity in the U.K.

“As our customers’ needs evolve, we will increasingly offer a range of alternative energy sources, supported by digital technologies, to give people choice and the flexibility, wherever they need to go and whatever they drive,” said Mark Gainsborough, executive vice president, New Energies for Shell, in a statement at the time of the Greenlots acquisition. “This latest investment in meeting the low-carbon energy needs of US drivers today is part of our wider efforts to make a better tomorrow. It is a step towards making EV charging more accessible and more attractive to utilities, businesses and communities.”

Powered by WPeMatico

The wave of venture capital interest in geographies other than Silicon Valley has been building momentum over the past 5+ years. If you measure capital flow by Twitter chatter alone, you may assume the tidal wave is about to break and checks are being doled out via T-shirt launchers repurposed from hockey games.

Meanwhile, VCs will approach founders saying, “We are now looking into markets beyond Silicon Valley.”

When Mucker launched back in 2011, our founding partners, who had left Silicon Valley for LA, set out to prove that high-growth companies can be built anywhere. Our portfolio from this past decade is a testament to this very narrative. With offices in LA, Austin and Nashville — and investments all over North America, we are seeing a marked increase in receptivity to an idea we had over a decade ago to invest across the U.S. and into Canada.

As of late, I’m receiving more and more outreach from VCs based in San Francisco, New York and beyond interested in deal flow here in Nashville and the Southeast.

When we think about the opportunity beyond Silicon Valley, we are really speaking of America.

In reality, there will be some lag time before the checks being written by these same VCs are consistent with both the outward hype and existing market opportunity. The broadened geographic focus of VCs for marketing purposes and FOMO is not adequately capturing the real narrative.

In short: When we think about the opportunity beyond Silicon Valley, we are really speaking of America.

“We” is a loaded declaration. I write this as a venture capitalist and also as the biracial daughter of a first-generation immigrant, with both of my parents growing up poor by most people’s standards. One branch of my family immigrated to the U.S. from Mexico during the Mexican Revolution, the other harkens back to rural Oklahoma. The founders I meet day in and day out in the Southeast oftentimes tell a similar story.

My story is that of the average American, and yet feels light years apart from what people perceive as the “innovation economy.” Many of the people I’ve met in venture capital this past decade come from prestigious lineages with parents and grandparents who may have never associated with mine. And yet, here we are. This is America.

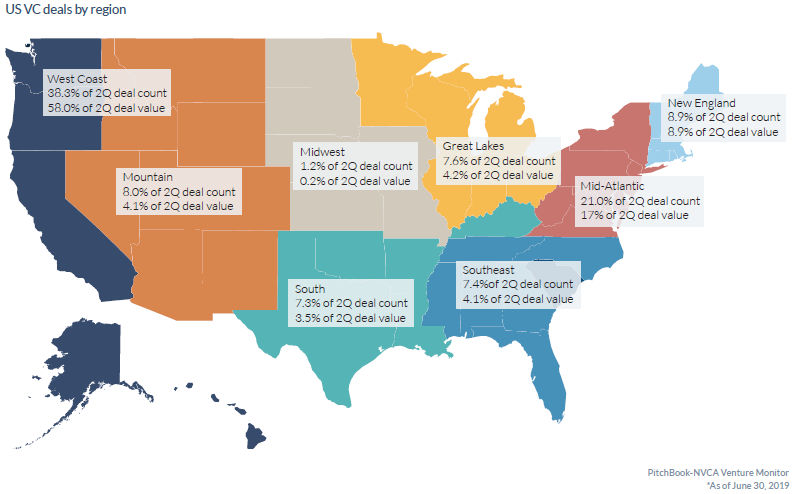

While Silicon Valley’s origins and climb to international stardom center around a collection of innovators, attracting more innovators and capital as the decades passed, one critical element arguably fell by the wayside — America as an expansive and diverse collection of states and people. Annual reporting on where venture capital dollars flow supports this discrepancy, with the majority of funds being funneled into companies based in and around Silicon Valley.

U.S. VC deals by region, as of June 2019. Image Credits: PitchBook/NVCA Venture Monitor

We find ourselves at the threshold of a decade where America will be rightfully recast as the land of opportunity for VC dollars to flow into the products and services fueling America’s future. And, at the helm of such innovations needs to be the people closest to these market opportunities, in full alignment with their customers and the nuances to best serve them.

In a post-COVID world, customers have never demanded more transparency into supply chains, workplace culture and equity ownership. Customers are more informed than ever before, with a 24/7 info line on brands and a growing scrutiny on where to place their hard-earned dollars. In short, they demand to be seen, and the founders who recognize this are the ones thriving in this new climate.

Where do the customers live? I’ll give you a hint: They are largely not in Silicon Valley.

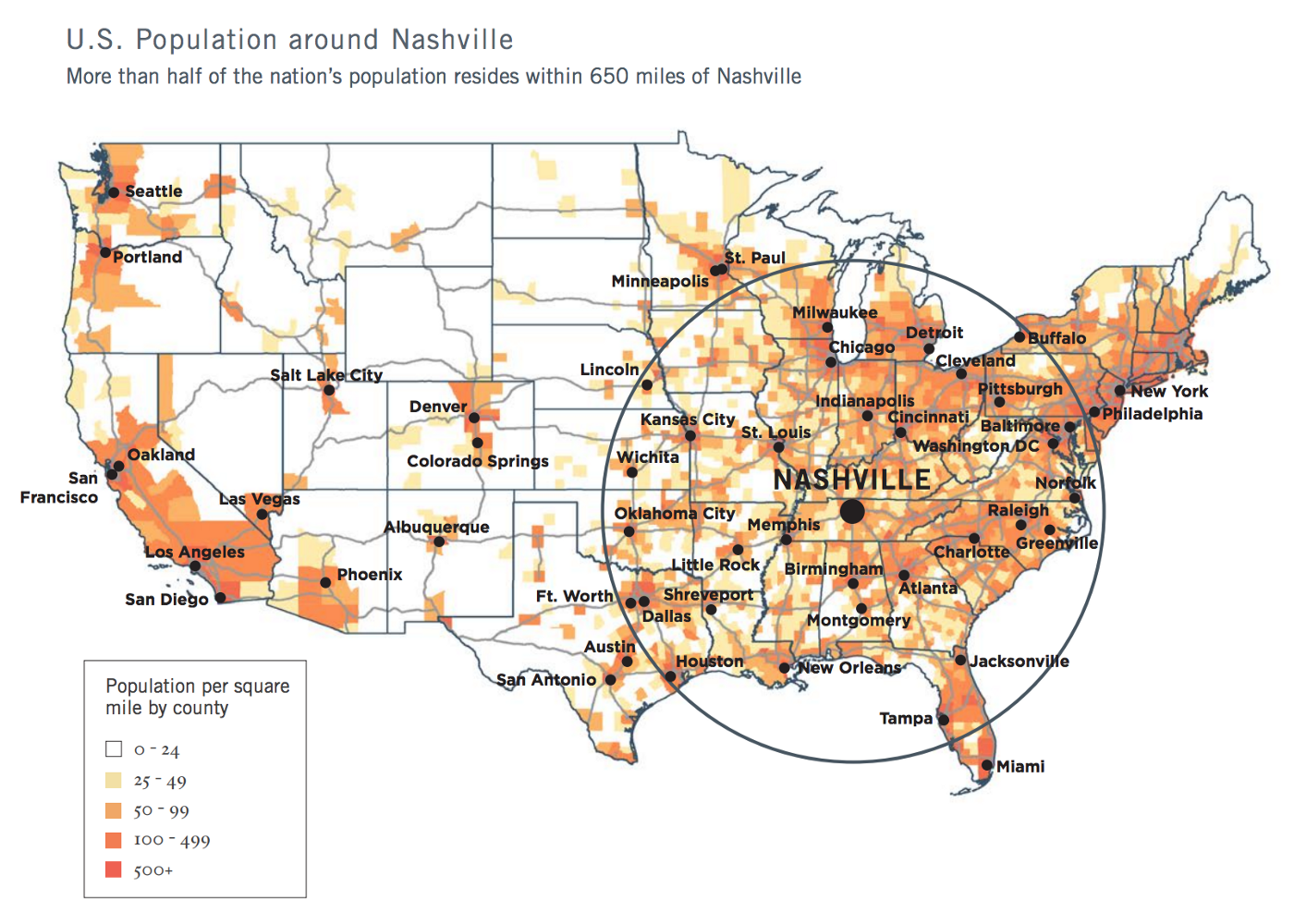

U.S. population around Nashville, TN. Image Credits: Nashville 2018 Regional Economic Development Guide

I wrote about the unfair advantage of Nashville back in 2018 when I announced the launch of Build In SE, a community I co-founded to support founders choosing to build their companies in the Southeast. Nashville is at the center of over half of the United States population within a radius of 650 miles, and within a two-hour flight of 75% of the U.S. market.

Customers come in all shapes and sizes, and founders with boots on the ground in these markets, wearing the same brand of proverbial boots as these customers, carry an unfair advantage. These same founders historically bootstrapped their companies out of need, as access to early-stage, high-risk capital can be scarce and vary widely city by city, state by state, industry by industry.

These same founders still built household name companies in the tech and innovation economy, including the likes of Mailchimp, Calendly, Lynda.com, and GoFundMe (their Series A valued them at $600 million pre-money). All of these companies have another thing in common — they were founded “beyond Silicon Valley.”

Another macrotrend at play is that of the increasing distribution of talent beyond traditional metropolitan strongholds like San Francisco and New York. Entrepreneurs, technologists and operational talent are lifestyle-seeking at a time in history when life feels all the more precious. Moving to cities like Nashville, Austin, Atlanta, Denver, Durham, Miami, et. al. means proximity to aging family members, affordable childcare and outdoor activities.

These simple pleasures were the tradeoffs people made when “pursuing their dreams” in coastal cities, picking up to move in pursuit of money (sometimes better weather). Seemingly overnight, capital abounds in the private markets just as talent becomes increasingly scarce and therefore valuable. The pendulum swung, and capital became the weaker of the two magnets; Wall Street began moving up Manhattan island toward coffee shops and dog parks when talent began to pose the question, “How long do I want my commute to be?” and “How much time do I want to reclaim for my family, and myself?”

2020 was the match to ignite this dry hillside. People trapped inside of cramped quarters with resources left to invest in a new life (or in other cases, left with nothing to lose) packed their bags for a new, up-and-coming metro.

For some, this comes with a newfound sense of community and belonging, as I experienced in 2017 when I moved from my lifelong home of Los Angeles to Nashville. In LA, my local neighborhood hardly knew one another due to the transient nature of the town. In Nashville, I became part of something greater than myself.

One of the big frustrations expressed by founders I know in markets like Nashville, Atlanta, the Research Triangle, Cincinnati and Toronto, is, “I keep hearing there is more capital available, but I’m not seeing it.” They will meet with investors, then be told they are too early, raising too little money, or too much, or not going after a “big enough market.”

Sometimes, one or more of these may be true. However, there are instances where these investor responses may be thinly veiled criticism of the perceived ability of the founders who might not sound, look or behave like Silicon Valley entrepreneurs.

Closing this gap of understanding between pattern-matching VCs of varying skill and startup CEOs across the country will require hard work in the coming decade. A big piece of this will require breaking bread as neighbors, with kids in the same schools, a shared affinity for the local greasy spoon and a mutual trust. This will be step one. Though really, it will require much more alignment and rigor around the very definition of America.

It is up to investors to capture this opportunity in the next decade. In fact, it is our job.

Powered by WPeMatico

Edtech is so widespread, we already need more consumer-friendly nomenclature to describe the products, services and tools it encompasses.

I know someone who reads stories to their grandchildren on two continents via Zoom each weekend. Is that “edtech?”

Similarly, many Netflix subscribers sought out online chess instructors after watching “The Queen’s Gambit,” but I doubt if they all ran searches for “remote learning” first.

Edtech needs to reach beyond underfunded public school systems to become more sustainable, which is why more investors and founders are focusing on lifelong learning.

Besides serving traditional students with field trips and art classes, a maturing sector is now branching out to offer software tutors, cooking classes and singing lessons.

For our latest investor survey, Natasha Mascarenhas polled 13 edtech VCs to learn more about how “employer-led up-skilling and a renewed interest in self-improvement” is expanding the sector’s TAM.

Here’s who she spoke to:

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

In other news: Extra Crunch Live, a series of interviews with leading investors and entrepreneurs, returns next month with a full slate of guests. This year, we’re adding a new feature: Our guests will analyze pitch decks submitted by members of the audience to identify their strengths and weaknesses.

If you’d like an expert eye on your deck, please sign up for Extra Crunch and join the conversation.

Thanks very much for reading! I hope you have a fantastic weekend — we’ve all earned it.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Bryce Durbin

Image Credits: Nigel Sussman (opens in a new window)

After falling into yesterday’s wild news cycle, Alex Wilhelm returned to The Exchange this morning with a close look at venture capital activity across Africa in 2020.

“Comparing aggregate 2020 figures to 2019 results, it appears that last year was a somewhat robust year for African startups, albeit one with fewer large rounds,” he found.

For more context, he interviewed Dario Giuliani, the director of research firm Briter Bridges, which focuses on emerging markets in Africa, Asia and Latin America.

Image Credits: MCCAIG (opens in a new window) / Getty Images

New cybersecurity ecosystems are popping up in different parts of the world.

Some of of that growth has been fueled by an exodus from the Bay Area, but many early-stage security startups already have deep roots in East Coast cities like Boston and New York.

In the United Kingdom and Europe, government innovation programs have helped entrepreneurs close higher numbers of Series A and B rounds.

Investor interest and expertise is migrating out of Silicon Valley: This post will help you understand where it’s going.

Image Credits: NurPhoto (opens in a new window) / Getty Images

Today’s smartphones are unfathomably feature-rich and durable, so it’s logical that sales have slowed.

A phone purchased 18 months ago is probably “good enough” for many consumers, especially in times of economic uncertainty.

Then again, of the record $111.4 billion in revenue Apple earned last quarter, $65.68 billion came from phone sales, largely driven by the release of the iPhone 12.

Even though “Apple’s success this quarter was kind of a perfect storm,” writes Hardware Editor Brian Heater, “it’s safe to project a rebound for the industry at large in 2021.”

Image Credits: Randy Faris (opens in a new window) / Getty Images

Finmark co-founder and CEO Rami Essaid wrote a post for Extra Crunch that candidly describes the traps he laid for himself that made him a less-effective entrepreneur.

As someone who’s worked closely with founders at several startups, each of the points he raised resonated deeply with me.

In my experience, many founders have a hard time delegating, which can quickly create cultural and operational problems. Rami’s experience bears this out:

“I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.”

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie:

I just got my U.S. citizenship! My husband and I want to bring my mom and her husband to the U.S. to help us take care of our preschooler and toddler.

My biological dad passed away several years ago when I was an adult and my mom has since remarried.

— Appreciative in Aptos

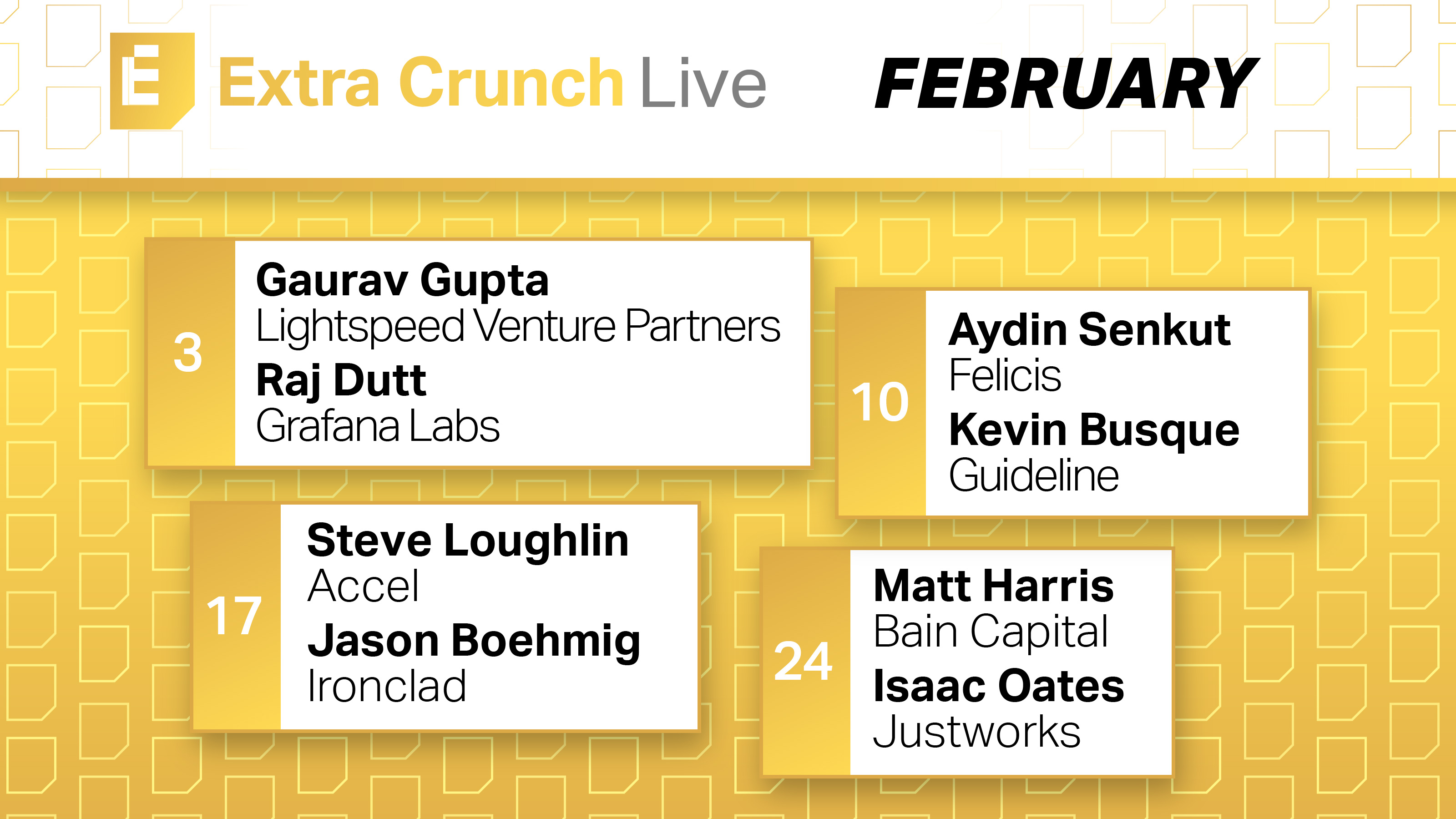

Next month, Extra Crunch Live returns with a lineup of guests who are extremely well-qualified to discuss early-stage startups.

Each Wednesday at noon PPST/3 p.m. EST, join a conversation with founders and the investors who backed their companies:

February 3:

Gaurav Gupta (Lightspeed Venture Partners) + Raj Dutt (Grafana Labs)

February 10:

Aydin Senkut (Felicis Ventures) + Kevin Busque (Guideline)

February 17:

Steve Loughlin (Accel) + Jason Boehmig (Ironclad)

February 24:

Matt Harris (Bain Capital) + Isaac Oates (Justworks)

Also, we’re adding a new feature to Extra Crunch Live — our guests will offer advice and feedback on pitch decks submitted by Extra Crunch members in the audience!

Image Credits: Aleksandar Nakic (opens in a new window) / Getty Images

Since the pandemic disrupted the social rhythms of work and school, many of us have compensated by changing our relationship to digital media.

For instance, I purchased a new sofa and thicker living room curtains several months ago when I realized we have no idea when movie theaters will reopen.

Last year, podcast sponsors spent almost $800 million to reach listeners, but ad revenue is estimated to surpass $1 billion this year. Clearly, I’m not the only person who used a discount code to buy a new product in 2020.

At this point, I can scarcely keep track of the multiple streaming platforms I’m subscribed to, but a new voice-activated remote control that comes with my basic cable plan makes it easier to browse my options.

Media reporter Anthony Ha spoke to10 VCs who invest in media startups to learn more about where they see digital media heading in the months ahead. For starters, how much longer can we expect traditional advertising models to persist?

And in a world with hundreds of channels, how are creators supposed to compete for our attention? What sort of discovery tools can we expect to help us navigate between a police procedural set in a Scandinavian village and a 90s sitcom reboot?

Here’s who Anthony interviewed:

Normally, we list each investor’s responses separately, but for this survey, we grouped their responses by question. Some readers say they use our surveys to study up on an individual VC before pitching them, so let us know which format you prefer.

Image Credits: Nigel Sussman (opens in a new window)

Data analytics platform Databricks is reportedly raising new capital that could value the company between $27 billion and $29 billion.

By the end of Q3 2020, Databricks had surpassed a $350 million run rate — a $150 million YoY increase, reports Alex Wilhelm.

At the time, he described the company as “an obvious IPO candidate” with “broad private-market options.”

Which begs the question: “Can we come up with a set of numbers that help make sense of Databricks at $27 billion?”

Image Credits: Natalia Timchenko (opens in a new window) / Getty Images

Rapid shifts in the way we buy goods and services disrupted old-school marketplaces like local newspapers and the Yellow Pages.

Today, I can use my phone to summon a plumber, a week’s worth of groceries or a ride to a doctor’s office.

End-to-end operators like Netflix, Peloton and Lemonade take a lot of time and energy to reach scale, but “the additional capital required is often outweighed by the value captured from owning the entire experience.”

Image Credits: Nigel Sussman (opens in a new window)

On January 25, Social Capital CEO Chamath Palihapitiya tweeted that he was making two blank-check deals.

Enterprise SaaS company Latch makes keyless entry systems; Sunlight Financial helps consumers finance residential solar power installations.

“There are nearly 300 SPACs in the market today looking for deals,” noted Alex Wilhelm, who unpacked both transactions.

“There’s no escaping SPACs for a bit, so if you are tired of watching blind pools rip private companies into the public markets, you are not going to have a very good next few months.”

Image Credits: dan tarradellas (opens in a new window) / Getty Images

On Monday, we published the Matrix Fintech Index, a three-part study that weighs liquidity, public markets and e-commerce trends to create a snapshot of an industry in perpetual flux.

For four years running, the S&P 500 and incumbent financial services companies have been outperformed by companies like Afterpay, Square and Bill.com.

In light of steady VC investment, increasing consumer adoption and a crowded IPO pipeline, “fintech represents one of the most exciting major innovation cycles of this decade.”

Image Credits: Acquia

On January 15, 2001, then-college student Dries Buytaert released Drupal 1.0.0, an open-source content-management platform. At the time, about 7% of the world’s population was online.

After raising more than $180 million, Buytaert exited to Vista Equity Partners for $1 billion in 2019.

Enterprise reporter Ron Miller interviewed Buytaert to learn more about his 18-year journey.

“His story is compelling, but it also offers lessons for startup founders who also want to build something big,” says Ron.

Powered by WPeMatico

In light of climate change and escalating global energy demand, more emphasis is being placed on emerging clean technologies — ranging from renewables and energy storage to nuclear power. Although these technologies have tremendous potential, they require lots of innovation, and innovation needs abundant capital.

The issue: early-stage financing for clean tech hasn’t been plentiful, and it’s stifling the growth of new energy companies. Why is this? In general, clean tech companies lack the startup advantages of agility and flexibility.

“Moving fast” works for products such as consumer mobile apps and SaaS solutions. The clean tech sector, on the other hand, tends to involve highly regulated, capital-intensive, mission-critical infrastructure.

That has hurt both returns and well-intentioned impact. According to Cambridge Associates, venture-backed companies have returned, on average, -15% internal rate of return (IRR) since 2000. Contrast that to venture-backed companies in healthcare, which returned 24% in IRR over the same time period.

While noble in its aims to make the world a better, cleaner, safer, healthier place through technology, clean tech venture capital has suffered simply because clean tech does not fit the traditional venture capital model. Central to the venture capital model is the ability to de-risk new ideas and significantly capitalize the most promising ones, allowing for liquidity via M&A or initial public offering (IPO).

Early-stage financing for clean tech hasn’t been plentiful, and it’s stifling the growth of new energy companies.

This construct allows for the return of venture capital dollars, plus appreciation that enables VC firms to raise new funds. These capitalization events also allow the venture-backed company to accelerate growth and maximize market impact.

How this construct works is evident when comparing healthcare and clean tech. In healthcare, new innovations are de-risked by VCs. More mature innovations are acquired or reach IPO every year. As a result, the average annual ratio of dollars raised via an exit to VC-invested dollars since 2012 is 1.8. This ratio is only 0.2 for clean tech, an 800-plus percent difference in the wrong direction. This has resulted in poor returns and limited capitalization of clean tech companies.

Given the state of the world’s environment and lack of abundant energy in emerging economies, we need to collectively fix this issue. Special purpose acquisition companies (SPACs) are significantly improving clean tech’s venture capital construct. According to Investopedia:

SPACs are companies with no commercial operations that are formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring an existing company.

Also known as “blank-check companies,” SPACs have been around for decades. In recent years, they’ve become more popular, attracting big-name underwriters and investors and raising a record amount of IPO money in 2019.

In 2020, more than 110 SPACs completed transactions in the U.S., capitalizing these companies with more than $29 billion.

In 2020, SPACs capitalized clean tech companies with almost $4 billion of capital, including Fisker, Lordstown Motors, QuantumScape, Hyliion, XL Fleet and others. This helped push the ratio of funds raised at exit to venture capital invested in 2020 from the previous 0.2 average to a much healthier 0.6, a 200% improvement.

In 2021, we will likely see even further improvement. Why? Because there are 43 active SPACs looking toward or finalizing merger targets with a clean tech focus, potentially providing $12 billion in growth capital. Even if there are no more new SPACs in 2021 and a historically low average of M&As and IPOs, 2021 promises continued improvement for clean tech investment.

One of the most high-profile clean tech SPACs was Nikola Corporation. The battery-electric and hydrogen-powered truck maker has attracted much fanfare since going public last June through a reverse merger with special purpose acquisition company VectoIQ. The company’s market capitalization soared and things seemed to be going well, but things became controversial later in the year when the company was accused of making false statements about its technology and other things.

Although examples such as Nikola have the potential to tarnish the emergence of SPACs as a way to spur clean tech investing, they shouldn’t. There are plenty of examples of emerging companies that scream quality and integrity. For example, Stem*, a leader in the energy storage optimization space, is now going public, pending SEC approval, via the Star Peak SPAC.

Public markets are receiving the SPAC with enthusiasm. Assuming the merger happens, Stem will be capitalized with greater than $450 million of cash to accelerate growth and drive impact. It’s an illustration of SPACs as a positive venture capital construct that is needed to make clean tech work and become a thriving sector.

As a long-time clean tech venture capitalist myself, it is interesting that public investment via the SPAC may be the correcting element for the clean tech VC construct. For years, I assumed that corporates would step up their M&A activity at premium valuations to solve this issue, but I’ve spent a long time waiting.

Judging by activity, corporates seem content to continue playing the still very important investor/nurturer role, versus the “owning” role. Regardless, capitalizing promising clean tech companies can only mean one thing: clean-tech-related impact is coming like never before as these companies require and use capital to scale.

New and more diverse approaches to finding and funding new, great clean tech companies are sorely needed. SPACs are going to be the tool needed to bring clean tech up to par with sectors such as healthcare. It’s a development that will benefit all of us.

*Stem is a Wind Ventures portfolio company.

Powered by WPeMatico

Citrix announced today that it plans to acquire Wrike, a SaaS project management platform, from Vista Equity Partners for $2.25 billion. Vista bought the company just two years ago.

Citrix, which is best known for its digital workspaces, sees this as a good match, especially at a time when employees have been forced to work from home because of the pandemic. Combining the two companies produces a powerful approach, one that didn’t escape Citrix CEO and president David Henshall.

“Together, Citrix and Wrike will deliver the solutions needed to power a cloud-delivered digital workspace experience that enables teams to securely access the resources and tools they need to collaborate and get work done in the most efficient and effective way possible across any channel, device or location,” Henshall said in a statement.

Andrew Filev, founder and CEO at Wrike, who has managed the company through these multiple changes and remains at the helm, believes his company has landed in a good spot with the Citrix purchase.

“First, as part of the Citrix family we will be able to scale our product and accelerate our roadmap to deliver capabilities that will help our customers get more from their Wrike investment. We have always listened to our customers and have built our product based on their feedback — now we will be able to do more of that, faster,” Filev wrote in a company blog post announcing the deal, stating a typical argument from CEOs of acquired companies.

The startup reports $140 million ARR, growing at 30% annually, so that comes out to approximately 16x its present-day revenue, which is the price companies are generally paying for acquisitions these days. However, as Wrike expects to reach $180 million to $190 million in ARR this year, the company’s sale price could look like a bargain in a few years’ time if the projections come to pass.

The price was not revealed in the 2018 sale, but it surely feels like a big win for Vista. Consider that Wrike has previously raised just $26 million.

Powered by WPeMatico

Some time ago, I gave up on the idea of finding a thread that connects each story in the weekly Extra Crunch roundup; there are no unified theories of technology news.

The stories that left the deepest impression were related to two news pegs that dominated the week — Visa and Plaid calling off their $5.3 billion acquisition agreement, and sizzling-hot IPOs for Affirm and Poshmark.

Watching Plaid and Visa sing “Let’s Call The Whole Thing Off” in harmony after the U.S. Department of Justice filed a lawsuit to block their deal wasn’t shocking. But I was surprised to find myself editing an interview Alex Wilhelm conducted with with Plaid CEO Zach Perret the next day in which the executive said growing the company on its own is “once again” the correct strategy.

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

In an analysis for Extra Crunch, Managing Editor Danny Crichton suggested that federal regulators’ new interest in antitrust enforcement will affect valuations going forward. For example, Procter & Gamble and women’s beauty D2C brand Billie also called off their planned merger last week after the Federal Trade Commission raised objections in December.

Given the FTC’s moves last year to prevent Billie and Harry’s from being acquired, “it seems clear that U.S. antitrust authorities want broad competition for consumers in household goods,” Danny concluded, and I suspect that applies to Plaid as well.

In December, C3.ai, Doordash and Airbnb burst into the public markets to much acclaim. This week, used clothing marketplace Poshmark saw a 140% pop in its first day of trading and consumer-financing company Affirm “priced its IPO above its raised range at $49 per share,” reported Alex.

In a post titled A theory about the current IPO market, he identified eight key ingredients for brewing a debut with a big first-day pop, which includes “exist in a climate of near-zero interest rates” and “keep companies private longer.” Truly, words to live by!

Come back next week for more coverage of the public markets in The Exchange, an interview with Bustle CEO Bryan Goldberg where he shares his plans for taking the company public, a comprehensive post that will unpack the regulatory hurdles facing D2C consumer brands, and much more.

If you live in the U.S., enjoy your MLK Day holiday weekend, and wherever you are: thanks very much for reading Extra Crunch.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman (opens in a new window)

After spending much of the week covering 2021’s frothy IPO market, Alex Wilhelm devoted this morning’s column to studying the OKR-focused software sector.

Measuring objectives and key results are core to every enterprise, perhaps more so these days since knowledge workers began working remotely in greater numbers last year.

A sign of the times: this week, enterprise orchestration SaaS platform Gtmhub announced that it raised a $30 million Series B.

To get a sense of how large the TAM is for OKR, Alex reached out to several companies and asked them to share new and historical growth metrics:

“Some OKR-focused startups didn’t get back to us, and some leaders wanted to share the best stuff off the record, which we grant at times for candor amongst startup executives,” he wrote.

Image Credits: Ezra Shaw (opens in a new window)

For our latest investor survey, Matt Burns interviewed five VCs who actively fund consumer electronics startups:

“Consumer hardware has always been a tough market to crack, but the COVID-19 crisis made it even harder,” says Matt, noting that the pandemic fueled wide interest in fitness startups like Mirror, Peloton and Tonal.

Bonus: many VCs listed the founders, investors and companies that are taking the lead in consumer hardware innovation.

Digital generated image of abstract multi colored curve chart on white background.

If you’re looking for insight into “why everything feels so damn silly this year” in the public markets, a post Alex wrote Thursday afternoon might offer some perspective.

As someone who pays close attention to late-stage venture markets, he’s identified eight factors that are pushing debuts for unicorns like Affirm and Poshmark into the stratosphere.

TL;DR? “Lots of demand, little supply, boom goes the price.”

Image Credits: Nigel Sussman (opens in a new window)

Clothing resale marketplace Poshmark closed up more than 140% on its first trading day yesterday.

In Thursday’s edition of The Exchange, Alex noted that Poshmark boosted its valuation by selling 6.6 million shares at its IPO price, scooping up $277.2 million in the process.

Poshmark’s surge in trading is good news for its employees and stockholders, but it reflects poorly on “the venture-focused money people who we suppose know what they are talking about when it comes to equity in private companies,” he says.

financial stock market graph on technology abstract background represent risk of investment

This week, Visa announced it would drop its planned acquisition of Plaid after the U.S. Department of Justice filed suit to block it last fall.

Last week, Procter & Gamble called off its purchase of Billie, a women’s beauty products startup — in December, the U.S. Federal Trade Commission sued to block that deal, too.

Once upon a time, the U.S. government took an arm’s-length approach to enforcing antitrust laws, but the tide has turned, says Managing Editor Danny Crichton.

Going forward, “antitrust won’t kill acquisitions in general, but it could prevent the buyers with the highest reserve prices from entering the fray.”

Image Credits: Sophie Alcorn

Dear Sophie:

I’m a grad student currently working on F-1 STEM OPT. The company I work for has indicated it will sponsor me for an H-1B visa this year.

I hear the random H-1B lottery will be replaced with a new system that selects H-1B candidates based on their salaries.

How will this new process work?

— Positive in Palo Alto

OLYMPUS DIGITAL CAMERA

After news broke that Visa’s $5.3 billion purchase of API startup Plaid fell apart, Alex Wilhelm and Ron Miller interviewed several investors to get their reactions:

Zach Perret, chief executive officer and co-founder of Plaid Technologies Inc., speaks during the Silicon Slopes Tech Summit in Salt Lake City, Utah, U.S., on Friday, Jan. 31, 2020. The summit brings together the leading minds in the tech industry for two-days of keynote speakers, breakout sessions, and networking opportunities. Photographer: George Frey/Bloomberg via Getty Images

Alex Wilhelm interviewed Plaid CEO Zach Perret after the Visa acquisition was called off to learn more about his mindset and the company’s short-term plans.

Perret, who noted that the last few years have been a “roller coaster,” said the Visa deal was the right decision at the time, but going it alone is “once again” Plaid’s best way forward.

Image Credits: Nigel Sussman (opens in a new window)

In Tuesday’s edition of The Exchange, Alex Wilhelm took a closer look at blank-check offerings for digital asset marketplace Bakkt and personal finance platform SoFi.

To create a detailed analysis of the investor presentations for both offerings, he tried to answer two questions:

Spotlit Multi Colored Coil Toy in the Dark.

Growth-stage startups in search of funding have a new option: “flexible VC” investors.

An amalgam of revenue-based investment and traditional VC, investors who fall into this category let entrepreneurs “access immediate risk capital while preserving exit, growth trajectory and ownership optionality.”

In a comprehensive explainer, fund managers David Teten and Jamie Finney present different investment structures so founders can get a clear sense of how flexible VC compares to other venture capital models. In a follow-up post, they share a list of a dozen active investors who offer funding via these non-traditional routes.

Image Credits: Anton Petrus (opens in a new window) / Getty Images

For some consumers, “cannabis has always been essential,” writes Matt Burns, but once local governments allowed dispensaries to remain open during the pandemic, it signaled a shift in the regulatory environment, and investors took notice.

Matt asked five VCs about where they think the industry is heading in 2021 and what advice they’re offering their portfolio companies:

Powered by WPeMatico