Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

Mexico has been known as an up-and-coming tech hub and a gateway to the Latin American market. As an investor focused on developer-centered products, open-source startups and infrastructure technology companies with a particular interest in emerging market innovation, I have been wanting to do some firsthand learning there.

So, despite the ongoing pandemic, I took all the necessary precautions and spent roughly seven weeks in Mexico from January to March. I spent most of my time meeting founders to get a handle on what they are building, why they are pursuing those ideas, and how the entire ecosystem is evolving to support their ambitions.

Knowledge transfer is not the only trend flowing in the U.S.-Asia-LatAm nexus. Competition is afoot as well.

One fascinating, though not surprising, observation was how much LatAm entrepreneurs look to Asian tech giants for product inspiration and growth strategies. Companies like Tencent, DiDi and Grab are household names among founders. This makes sense because the market conditions in Mexico and other parts of LatAm resemble China, India and Southeast Asia more than the U.S.

What often happens is entrepreneurs first look to successful startups in the U.S. to emulate and localize. As they find product-market fit, they start to look to Asian tech companies for inspiration while morphing them to suit local needs.

One good example is Rappi, an app that started out as a grocery delivery service. Its future ambition is squarely to become the superapp of LatAm: It is expanding aggressively both geographically and productwise into delivery for restaurant orders, pharmacy and even COVID tests. It’s also introducing new payment, banking and financial-service products. Rappi Pay launched in Mexico just a few weeks ago, while I was still in the country.

Rappi now looks more like Meituan and Grab than any of its U.S. counterparts, and that’s not an accident. SoftBank, whose portfolio contains many of these Asian tech giants, invested heavily in Rappi’s previous two rounds and now has a $5 billion fund dedicated to the LatAm region. The knowledge and experience accumulated from Asian tech in the last 10 years is transferring to like-minded firms like Rappi, right under Silicon Valley’s proverbial nose.

Knowledge transfer is not the only trend flowing in the U.S.-Asia-LatAm nexus. Competition is afoot as well.

Because of similar market conditions, Asian tech giants are directly expanding into Mexico and other LatAm countries. The one I witnessed up close during my visit was DiDi.

DiDi’s foray into LatAm started in January 2018 with its acquisition of 99, a Brazilian ride-sharing company. In April 2018, DiDi entered Mexico with its bread-and-butter ride-sharing service. It wasn’t until April 2019 that DiDi launched its food delivery service, DiDi Food, in Monterrey and Guadalajara — two of the largest cities in Mexico. Its expansion hasn’t slowed down since, with a 10% extra earnings incentive to lure delivery drivers.

Image Credits: Kevin Xu

My Airbnb in Mexico City happened to be two blocks away from the large WeWork building where DiDi’s local office was located. Every day, I saw a long line of people responding to the earning incentives — waiting outside to get hired as DiDi delivery workers.

Meanwhile, the Uber office that’s literally one block away had hardly any foot traffic. As Uber and Rappi fight for more wealthy consumers, DiDi is working to attract lower-income users to grab market share, hoping that one day some of these people will reach the middle class and become profitable customers.

Powered by WPeMatico

Digital House, a Buenos Aires-based edtech focused on developing tech talent through immersive remote courses, announced today it has raised more than $50 million in new funding.

Notably, two of the main investors are not venture capital firms but instead are two large tech companies: Latin American e-commerce giant Mercado Libre and San Francisco-based software developer Globant. Riverwood Capital, a Menlo Park-based private equity firm, and existing backer early-stage Latin American venture firm Kaszek also participated in the financing.

The raise brings Digital House’s total funding raised to more than $80 million since its 2016 inception. The Rise Fund led a $20 million Series B for Digital House in December 2017, marking the San Francisco-based firm’s investment in Latin America.

Nelson Duboscq, CEO and co-founder of Digital House, said that accelerating demand for tech talent in Latin America has fueled demand for the startup’s online courses. Since it first launched its classes in March 2016, the company has seen a 118% CAGR in revenues and a 145% CAGR in students. The 350-person company expects “and is on track” to be profitable this year, according to Duboscq.

Digital House CEO and co-founder Nelson Duboscq. Image Credits: Digital House

In 2020, 28,000 students across Latin America used its platform. The company projects that more than 43,000 will take courses via its platform in 2021. Fifty percent of its business comes out of Brazil, 30% from Argentina and the remaining 20% in the rest of Latin America.

Specifically, Digital House offers courses aimed at teaching “the most in-demand digital skills” to people who either want to work in the digital industry or for companies that need to train their employees on digital skills. Emphasizing practice, Digital House offers courses — that range from six months to two years — teaching skills such as web and mobile development, data analytics, user experience design, digital marketing and product development.

The courses are fully accessible online and combine live online classes led by in-house professors, with content delivered through Digital House’s platform via videos, quizzes and exercises “that can be consumed at any time.”

Digital House also links its graduates to company jobs, claiming an employability rate of over 95%.

Looking ahead, Digital House says it will use its new capital toward continuing to evolve its digital training platforms, as well as launching a two-year tech training program — dubbed the the “Certified Tech Developer” initiative — jointly designed with Mercado Libre and Globant. The program aims to train thousands of students through full-time two-year courses and connect them with tech companies globally.

Specifically, the company says it will also continue to expand its portfolio of careers beyond software development and include specialization in e-commerce, digital marketing, data science and cybersecurity. Digital House also plans to expand its partnerships with technology employers and companies in Brazil and the rest of Latin America. It also is planning some “strategic M&A,” according to Duboscq.

Francisco Alvarez-Demalde, co-founder & co-managing partner of Riverwood Capital, noted that his firm has observed an accelerating digitization of the economy across all sectors in Latin America, which naturally creates demand for tech-savvy talent. (Riverwood has an office in São Paulo).

For example, in addition to web developers, there’s been increased demand for data scientists, digital marketing and cybersecurity specialists.

“In Brazil alone, over 70,000 new IT professionals are needed each year and only about 45,000 are trained annually,” Alvarez-Demalde said. “As a result of such a talent crunch, salaries for IT professionals in the region increased 20% to 30% last year. In this context, Digital House has a large opportunity ahead of them and is positioned strategically as the gatekeeper of new digital talent in Latin America, preparing workers for the jobs of the future.”

André Chaves, senior VP of Strategy at Mercado Libre, said the company saw in Digital House a track record of “understanding closely” what Mercado Libre and other tech companies need.

“They move as fast as we do and adapt quickly to what the job market needs,” he said. “A very important asset for us is their presence and understanding of Latin America, its risks and entrepreneurial environment. Global players have succeeded for many years in our region. But things are shifting gradually, and local knowledge of risks and opportunities can make a great difference.”

Powered by WPeMatico

All successful companies start off as a great idea, scribbled on the back of a cocktail napkin during a late-night meeting of the minds or gleaned from a fleeting inspiration that leaves you with a feeling of “I could do that better.”

For most, that’s as far as entrepreneurship ever goes, because, unfortunately, a great idea can’t raise money, develop a product or disrupt an industry.

It’s only an idea.

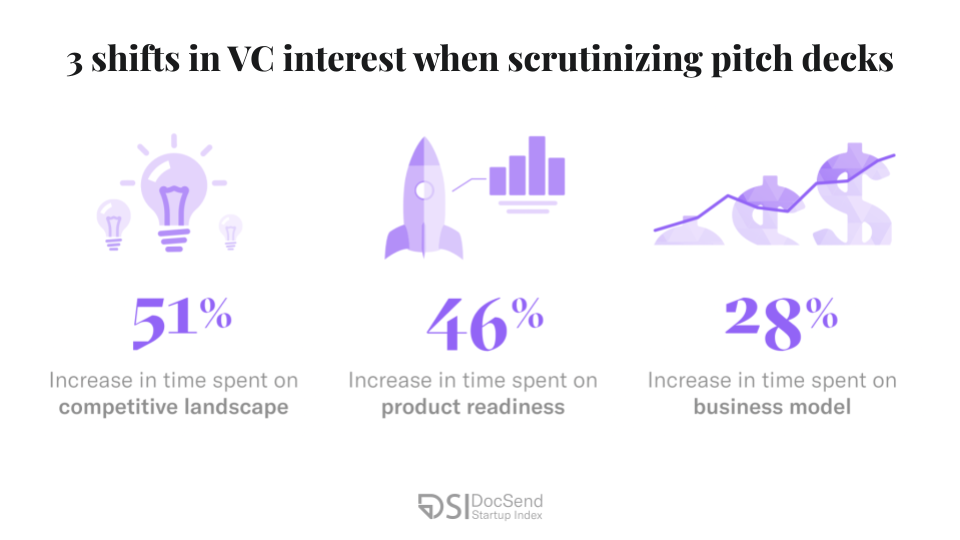

Investors’ heightened expectations for monetization potential and a company’s positioning within its competitive landscape are unlikely to lessen in the years to come, even in a post-COVID economy.

New data from the DocSend Startup Index show that for early-stage fundraising, particularly in the pre-seed round, founders need to approach VCs with much more than a great idea to secure funding. Our newest report on the state of pre-seed fundraising shows that investors became laser-focused on sections of the pitch deck that address monetization and business viability — signs that founders need to come to the table with better-defined businesses in order to succeed.

According to the data, overall founder and VC activity took a nosedive in early 2020 once the serious nature of the pandemic became apparent. But as the year progressed and investors adjusted to the new market conditions and remote dealmaking, overall activity quickly surpassed pre-pandemic levels.

Despite this flurry of activity and an unprecedented appetite for new startup pitches, investors made it very clear that strong positioning in three sections of the pitch deck was nonnegotiable.

Image Credits: DocSend(opens in a new window)

Powered by WPeMatico

When it comes to fast-moving technology, mobility zooms ahead of the pack — both literally and figuratively. Early-stage startup founders and investors need to keep their fingers on the sector’s very rapid pulse and the best place to do that is, you guessed it, TC Sessions: Mobility 2021 on June 9.

If you’re eager to introduce your early-stage startup to the top leaders, investors, experts and policy makers across the mobility tech community, don’t just attend TC Sessions: Mobility — exhibit there. Double down on essential exposure and increase your opportunities.

Budget-friendly tip: The early-bird price remains active until May 5 at 11:59 pm (PST). Buy your Startup Exhibitor Package before the deadline hits and save 35 percent.

Talk about a rapt audience. One big reason people attend the show is to see and meet exciting, innovative new startups. A Startup Exhibitor Package lets you showcase your tech, build your network and expand your opportunities for growth and success. Here’s what your package includes (Note: They’re available only to pre-Series A, early-stage startups).

Keeping with the networking theme, this is how Karin Maake, senior director of communications at FlashParking, described her experience.

“TC Sessions: Mobility isn’t just an educational opportunity, it’s a real networking opportunity. Everyone was passionate and open to creating pilot programs or other partnerships. That was the most exciting part. And now — thanks to a conference connection — we’re talking with Goodyear’s Innovation Lab.”

Don’t miss your chance to sashay your superior stuff in front of the mobility industry’s leading mover, shakers and makers. Buy a Startup Exhibitor Package now, save 35 percent and get ready for TC Sessions Mobility 2021.

Is your company interested in sponsoring or exhibiting at TC Sessions: Mobility 2021? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

Shares of Box, a well-known content-and-collaboration company that went public in 2015, rose today after Reuters reported that the company is exploring a sale. TechCrunch previously discussed rising investor pressure for Box to ignite its share price after years in the public-market wilderness.

At the close today Box’s equity was worth $23.65 per share, up around 5% from its opening value, but lower than its intraday peak of $26.47, reached after the news broke. The company went public a little over five years ago at $14 per share, only to see its share price rise to around the same level it returned today during its first day’s trading.

Box, famous during its startup phase thanks in part to its ubiquitous CEO and co-founder Aaron Levie, has continued to grow while public, albeit at a declining pace. Dropbox, a long-term rival, has also seen its growth rate decline since going public. Both have stressed rising profitability over revenue expansion in recent quarters.

But the problem that Box has encountered while public, namely hyper-scale platform companies with competing offerings, could also prove a lifeline; Google and Microsoft could be a future home for Levie’s company, after years of the duo challenging Box for deals.

As recently as last week, Box announced a deal for tighter integration with Microsoft Office 365. Given the timing of the release, it was easy to speculate the news could be landing ahead of a potential deal. The Reuters article adds fuel to the possibility.

While we can’t know for sure if the Reuters article is accurate, the possible sale of Box makes sense.

The article indicated that one of the possible acquisition options for Box could be taking it private again via private equity. Perhaps a firm like Vista or Thoma Bravo, two firms that tend to like mature SaaS companies with decent revenue and some issues, could swoop in to buy the struggling SaaS company. By taking companies off the market, reducing investor pressure and giving them room to maneuver, software companies can at times find new vigor.

Consider the case of Marketo, a company that Vista purchased in 2016 for $1.6 billion before turning it around and selling to Adobe in 2018 for $4.75 billion. The end result generated a strong profit for Vista, and a final landing for Marketo as part of a company with a broader platform of marketing tools.

If there are expenses at Box that could be trimmed, or a sales process that could be improved, is not clear. But Box’s market value of $3.78 billion could put it within grasp of larger private-equity funds. Or well within the reaches of a host of larger enterprise software companies that might covet its list of business customers, technology or both.

If the rumors are true, it could be a startling fall from grace for the company, moving from Silicon Valley startup darling to IPO to sold entity in just six years. While it’s important to note these are just rumors, the writing could be on the wall for the company, and it could just be a matter of when and not if.

Powered by WPeMatico

Venture capitalists love to talk investment theses: on Twitter, Medium, Clubhouse, at conferences. And yet, when you take a closer look, theses are often meaningless and/or misleading.

OpenVC is a new, open-source initiative to collect and analyze all publicly available VC theses to help founders more efficiently find the right investors — and vice-versa. For the first time, we are sharing here our initial conclusions. We hope you’ll upload your own thesis to benchmark yourself. We’ve identified six common patterns of how VCs articulate their theses and some best practices in doing so.

Our analysis is based on two complementary datasets:

Our four primary conclusions:

For the sake of simplicity, we will consider “investment thesis” and “investment criteria” as equivalent terms moving forward, although we argue that the thesis leads to the investment criteria. We summarize how they interrelate in the table below.

A typical VC thesis: “We invest in tech startups in Europe at an early stage.” However, our experience shows that in many cases “Europe” means a handful of countries, for instance, France, U.K. and Germany; and “tech” means B2B SaaS/fintech or consumer apps.

Thirty-four VC firms in OpenVC call themselves “early stage.” Yet 30% of those don’t actually invest in pre-revenue startups. The phrase is quite ambiguous; we suggest quantifying check size so that your investment preference is clearer.

Almost every VC says that they invest in the “best” founders. However, according to PitchBook Data, since the beginning of 2016, companies with women founders have received only 4.4% of venture capital deals. Those companies have garnered only about 2% of all capital invested. This is despite the fact that the data show you’re better off investing in women.

This lack of transparency results in confused founders who chase the wrong investors. In turn, investors are overwhelmed with poorly qualified opportunities.

Christoph Janz from Point Nine Capital wrote on Twitter:

The modal VC thesis is: “We invest in great teams addressing large markets with disruptive solutions.” Who invests in lousy teams addressing tiny markets with outdated solutions? Theses also tend to use the same words across many firms, e.g., “daring” and “bold.”

In particular, in our second dataset, we found a disproportionate number of theses focused on “technical” companies (vaguely defined) and focused on companies attacking “problems of the future rather than the present,” in various permutations of that language.

| Top Visible Heuristics (in dataset of 36 U.S. VCs) | Occurrences |

| “Technical” companies (i.e., any mention of a focus on tech companies) | 26 |

| Local affinity or bias | 10 |

| Attack problems of the future rather than the present (or some variant) | 9 |

| Technical founders | 7 |

Why are the investment criteria so imprecise on the VC websites? We have three theories, in descending order of importance:

Powered by WPeMatico

Security firm McAfee announced this morning that it will be selling its enterprise business to a consortium led by the private equity firm Symphony Technology Group for $4 billion.

It should pair well with RSA, another enterprise-focused security company the private equity firm purchased last February for $2 billion.

McAfee President and Chief Executive Officer Peter Leav says that his company has decided to direct the firm’s resources to the consumer side of the business. “This transaction will allow McAfee to singularly focus on our consumer business and to accelerate our strategy to be a leader in personal security for consumers,” he said in a statement.

The company has been making some moves in the last year, returning to the public markets after a decade as a private company. In January, the company reportedly laid off a couple of hundred employees and shut down its software development center in Tel Aviv.

Although Symphony did not point directly to the RSA acquisition, the two investments create a large combined legacy security business for the firm, both of which have strong brand recognition, but might have lost some of their edge to more modern competitors in the marketplace.

Looking at McAfee’s latest earning’s report, Q42020, which the company reported on February 24, 2021, the consumer business grew at a much brisker rate than the enterprise side of the house. The former was up 23% YoY, while the latter grew at a far slower 5% rate.

As for the entire year, the company reported $2.9 billion in total FY2020 revenue, up 10% YoY. That broke down to $1.6 billion in consumer net revenue up 20% YoY, and $1.3 billion in enterprise net revenue, an increase of just 1% for the full year.

The company has a complex history, starting life in the 1980s selling firewall software. It eventually went public before being purchased by Intel for $7.7 billion in 2010 and going private again. In 2014, the company changed names to Intel Security before Intel sold a majority stake to TPG in 2017 for $4.2 billion and changed the name back to McAfee.

The transaction is expected to close by the end of this year, subject to regulatory oversight.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

Over the past decade, venture capital has become synonymous with entrepreneurship. Founders from around the world arrive in Silicon Valley with visions of record-setting A rounds and billion-dollar valuations. But what if you don’t have unicorn dreams — or you don’t want to pursue VC money?

Bootstrapping a SaaS company is not only possible — I believe it’s a saner, more sustainable way to build and scale a business. To be clear, bootstrapping isn’t always easy. It requires patience and focus, but the freedom to create a meaningful product, on your terms, is worth more than even the biggest VC check.

The freedom to create a meaningful product, on your terms, is worth more than even the biggest VC check.

I started my company, JotForm, in 2006. We’ve grown steadily from a simple web tool into a product that serves more than 8 million users — without taking a dime in outside funding. We’re profitable in an industry with big-name competitors like Google.

Most importantly, I still love this company and its mission, and I want the same for my fellow entrepreneurs. If you’re a SaaS founder who’s wary of VC funding, here are my best bootstrapping tips.

Success stories from founders who leap blindly into business without resources or relevant experience are compelling, but they’re the exception, not the rule. Working inside another organization can build your skills, your network and even inspire great product ideas.

After finishing college with a computer science degree, I worked as a developer for a New York media company. The editors always needed custom web forms, which were tedious and time consuming to build. I kept thinking, “There has to be a better way.”

That daily frustration led me to start JotForm — but I didn’t leave my job right away. I stayed with the media firm for five years and worked on my product on the side. By the time I was ready to go all in, I had the confidence, experience and savings I needed.

Many of the world’s biggest companies began as side projects, including Twitter, Craigslist, Slack, Instagram, Trello, and a little venture called Apple. If your day job doesn’t pay enough to fund the early stages of your business, consider a side gig or consulting work. There are so many ways to set yourself up for success without the pressure of VC cash or selling a chunk of your business.

The exact numbers shift every year, but data compiled by Fundable show that only 0.05% of U.S. startups are backed by VCs. Another 0.91% are funded by angel investors. The vast majority, at 57%, are funded by credit and personal loans, while 38% get funding from friends and family.

It may feel like most founders raise multimillion-dollar rounds, but that’s simply not the case. It’s also good to remember that securing VC money is complicated and time consuming. You can spend months taking meetings and presenting the perfect deck — and still leave empty handed. Be patient and stick to your own path.

SaaS founders often emphasize vanity metrics, like user acquisitions and total downloads. These numbers can measure short-term popularity, but they don’t reveal how users and customers feel about your product — or your long-term potential.

Powered by WPeMatico

When I needed a new sofa several months ago, I was pleased to find a buy now, pay later (BNPL) option during the checkout process. I had prepared myself to make a major financial outlay, but the service fees were well worth the convenience of deferring the entire payment.

Coincidentally, I was siting on said sofa this morning and considering that transaction when Alex Wilhelm submitted a column that compared recent earnings for three BNPL providers: Afterpay, Affirm and Klarna.

I asked him why he decided to dig into the sector with such gusto.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

“What struck me about the concept was that we had just seen earnings from Affirm,” he said. “So we had three BNPL players with known earnings, and I had just covered a startup funding round in the space.”

“Toss in some obvious audience interest, and it was an easy choice to write the piece. Now the question is whether I did a good job and people find value in it.”

Thanks very much for reading Extra Crunch this week! Have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Colin Hawkins (opens in a new window) / Getty Images

I avoid running Extra Crunch stories that focus on best practices; you can find those anywhere. Instead, we look for “here’s what worked for me” articles that give readers actionable insights.

That’s a much better use of your time and ours.

With that ethos in mind, Lucas Matney interviewed Pilot CEO Waseem Daher to deconstruct the pitch deck that helped his company land a $60M Series C round.

“If the Series A was about, ‘Do you have the right ingredients to make this work?’ then the Series B is about, ‘Is this actually working?’” Daher tells TechCrunch.

“And then the Series C is more, ‘Well, show me that the core business is really working and that you have unlocked real drivers to allow the business to continue growing.’”

Image Credits: Bryce Durbin

A global survey of automobile owners found three hurdles to overcome before consumers will widely embrace electric vehicles:

“Theoretically, solid state batteries (SSB) could deliver all three,” but for now, lithium-ion batteries are the go-to for most EVs (along with laptops and phones).

In our latest market map, we’ve plotted the new and established players in the SSB sector and listed many of the investors who are backing them.

Although SSBs are years away from mass production, “we are on the cusp of some pretty incredible discoveries using major improvements in computational science and machine learning algorithms to accelerate that process,” says SSB startup founder Amy Prieto.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie:

Help! Our startup needs to hire 50 engineers in artificial intelligence and related fields ASAP. Which visa and green card options are the quickest to get for top immigrant engineers?

And will Biden’s new immigration bill help us?

— Mesmerized in Menlo Park

Image Credits: Jasmin Merdan / Getty Images

Founded in 1996, F5 has repositioned itself in the networking market several times in its history. In the last two years, however, it spent $2.2 billion to acquire Shape Security, Volterra and NGINX.

“As large organizations age, they often need to pivot to stay relevant, and I wanted to explore one of these transformational shifts,” said enterprise reporter Ron Miller.

“I spoke to the CEO of F5 to find out the strategy behind his company’s pivot and how he leveraged three acquisitions to push his organization in a new direction.”

Image Credits: Who_I_am (opens in a new window) / Getty Images

Cloud hosting company DigitalOcean filed to go public this week, so Ron Miller and Alex Wilhelm unpacked its financials.

“AWS and Microsoft Azure will not be losing too much sleep worrying about DigitalOcean, but it is not trying to compete head-on with them across the full spectrum of cloud infrastructure services,” said John Dinsdale, chief analyst and research director at Synergy Research.

Image Credits: Nigel Sussman (opens in a new window)

I asked Alex Wilhelm to dial back the profanity he used to describe Oscar Health’s proposed valuation, but perhaps I was too conservative.

In March 2018, the insurtech unicorn was valued at around $3.2 billion. Today, with the company aiming to debut at $32 to $34 per share, its fully diluted valuation is closer to $7.7 billion.

“The clear takeaway from the first Oscar Health IPO pricing interval is that public investors have lost their minds,” says Alex.

His advice for companies considering an IPO? “Go public now.”

Image Credits: Nigel Sussman (opens in a new window)

Last week, Alex wrote about how cryptocurrency trading platform Coinbase was being valued at $77 billion in the private markets.

As of Monday, “it’s now $100 billion, per Axios’ reporting.”

He reviewed Coinbase’s performance from 2019 through the end of Q3 2020 “to decide whether Coinbase at $100 billion makes no sense, a little sense or perfect sense.”

Image Credits: Alla Aramyan (opens in a new window) / Getty Images

A skilled software sales team devotes a lot of resources to pinpointing potential customers.

Poring through LinkedIn and reviewing past speaker lists at industry conferences are good places to find decision-makers, for example.

Despite this detective work, GGV Capital investor Oren Yunger says sales teams still need to identify the deal-blockers who can spike a deal with a single email.

“I call this person the Chief Objection Officer.”

Image Credits: Klaus Vedfelt / Getty Images

Every startup wants to raise its profile, but for many early-stage companies, marketing budgets are too small to make a meaningful difference.

“Providing real value through content is an excellent way to build authority in the short and long term,” says Amanda Milligan, marketing director at growth agency Fractl.

Image Credits: luchezar (opens in a new window) / Getty Images

The most effective marketing uses good storytelling, not persuasion.

According to Caryn Marooney, general partner at Coatue Management, every compelling story is relevant, inevitable, believable and simple.

“Behind most successful companies is a story that checks every one of those boxes,” says Marooney, but “this is a central challenge for every startup.”

On a recent episode of Extra Crunch Live, Ironclad founder and CEO Jason Boehmig and Accel partner Steve Loughlin discussed the pitch that brought them together almost four years ago.

Since that $8 million Series A, Loughlin joined Ironclad’s board. “Both agree that the work they put in up front had paid off” when it comes to how well they work together, says Jordan Crook.

“We’ve always been up front about the fact that we consider the board a part of the company,” said Boehmig.

From April 1-2, some of the most successful founders and VCs will explain how they build their businesses, raise money and manage their portfolios.

At TC Early Stage, we’ll cover topics like recruiting, sales, legal, PR, marketing and brand building. Each session includes ample time for audience questions and discussion.

Use discount code ECNEWSLETTER to take 20% off the cost of your TC Early Stage ticket!

Powered by WPeMatico

This morning Citadel ID announced a combined $3.5 million raise for its income and employment verification service. The startup provides an API to customer companies, allowing them to rapidly verify details of consumer employment.

The capital came from a blend of venture firms and angels. On the firm side, Abstract and Soma VC were in there, along with ChapterOne. Brianne Kimmel put capital in as well, according to the startup. And denizens with work histories at companies like Zynga (Mark Pincus), Stripe (Lachy Groom), Carta (Henry Ward) and others also put cash into the fundraise. (The company reached out to add that Fathom Capital also put a good amount in the round.)

Citadel was founded back in June of 2020, before raising capital, snagging its first customer and shipping its product all inside of the same year.

The idea for Citadel ID came when co-founder Kirill Klokov worked at Carta, the cap-table-as-a-service startup that recently built an exchange for the trading of private stock. Klokov discovered while working on the tech side of the company how hard it was to verify certain data, like employment and income and identity.

As Carta deals with money, stock and the collection and distribution of both, you can imagine why having a quick way to verify who worked where, and since when, mattered to the company. But Klokov came to realize that there wasn’t a good solution in the market for what Carta needed, sans building integrations to a host of payroll managers by hand and dealing with lots of data with varying taxonomies. That or using an in-the-market product, like Equifax’s The Work Number, which the founder described as expensive and offering relatively low coverage.

To fill the market void Klokov helped found Citadel ID, quickly building integrations into payroll managers where there were hooks for code, and working around older login systems when needed. Citadel ID’s service allows regular folks to provide access to their employment data to others, allowing for the verification of their income (a rental group, perhaps), or employment (Carta, perhaps) quickly.

Per the startup the market demand for such verifications is in the hundreds of millions every year in the United States. So, Citadel should have plenty of market space to grow into. Citadel ID has around 20 customers today, it told TechCrunch, and charges on a per verification basis.

Finally, while Citadel also offers data via its website and not merely through its API, the startup still fits inside the growing number of startups we’ve seen in recent quarters foregoing traditional SaaS, and instead offering their products via a developer hook (sometimes referred to as a “headless” approach). API-delivered startups are not new, after all Twilio went public years ago. But their model of product delivery feels like it’s gaining momentum over managed software offerings.

Let’s see how quickly Citadel ID can scale before it raises its Series A.

Powered by WPeMatico