payments

Auto Added by WPeMatico

Auto Added by WPeMatico

If you’ve made any payments with a chip card, you’ve probably had awkward moments — those long seconds after you’ve inserted the card and everyone behind you is (literally or metaphorically) tapping their foot, waiting for the card to be processed.

Well, Square has been working on this problem for a while now. Last fall, for example, CEO Jack Dorsey said the company had gotten the processing time down to under three seconds.

Today, the company is announcing that it’s shaved even more time off, and that Square contactless and chip Readers and Registers can now process chip cards in two seconds. To achieve this, it says it’s worked closely with payment partners — and it’s also streamlined the process so that you can remove your card as soon as it’s read, without waiting for the response from the card issuer.

In contrast, when the Wall Street Journal timed chip cards in over 50 transactions a couple years ago, it found that the average processing time was 13 seconds. Those extra seconds might not sound like much in theory, but again, if you’re in a hurry or you’ve got a line of people behind you, the wait can be painful.

Plus, it sounds like this can make a real difference for businesses. In the announcement, Regan Long, co-founder and brewmaster at Local Brewing Co., said that with his brewery’s location near the Giants’ AT&T Park in San Francisco, there’s usually “a rush of customers all ready to close out their open beer tabs at the same time.”

“With Square’s chip card reader update, we’ve cut processing time in half — helping us keep customers happy and on their way to catch the first pitch,” he added.

In addition to faster chip card processing, Square is making another speed-related announcement: With the latest update, Square’s free point-of-sale app will allow sellers to skip collecting signatures if they choose.

Powered by WPeMatico

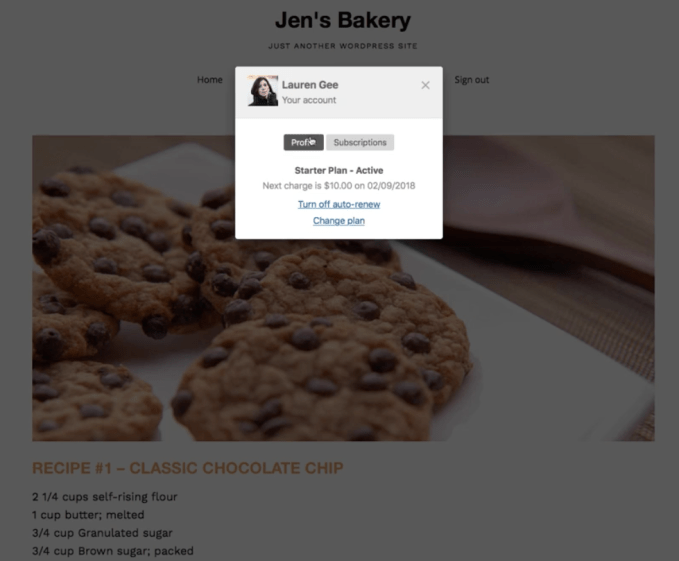

Patreon is forming a patronage empire. Today it acquired white-labeled subscription membership platform Memberful, which lets creators sell exclusive access to content through their own site instead of a centralized platform like Patreon. Rather than being folded into a Patreon feature, Memberful will run as an independent brand, maintaining its tiered pricing structure, though new sign-ups will get a rate closer to Patreon’s low 5 percent rake.

Terms weren’t disclosed for the deal that brings Memberful’s whole seven-person team and 500 paying clients aboard. But Patreon clearly sees rolling up competitors and complements in the patronage space as a worthy use of its $60 million raise at a $450 million valuation late last year that brought it to $105 million in funding. In June, Patreon bought Kit to let creators bundle in merchandise with their perks for paying monthly subscribers. It also bought out competitor Subbable back in 2015.

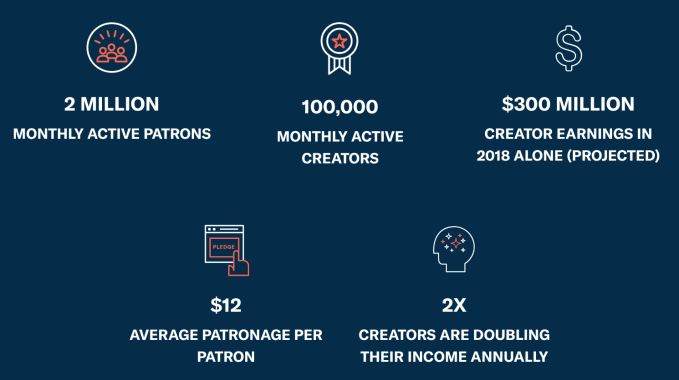

By teaming up, Patreon and Memberful will be able to provide subscription patronage services for creators, whether they want their fan community to live on Patreon, or through Memberful on their own WordPress or website with integrations of Stripe and MailChimp. Patreon already has 2 million patrons paying an average of $12 each to a total of 100,000 creators, and it expects to pay out $300 million in 2018 alone. The acquisition could let Patreon move up market, recruiting comedians, illustrators, game developers and vloggers that already have an established audience elsewhere.

“I think membership is on the up and is going to grow for the next decade,” says Patreon VP of Product Wyatt Jenkins. “Our strategy is to be an open, neutral platform,” as opposed to focusing on one type of content like YouTube with videos or Twitch with streaming where you’re locked into that platform’s tools. Memberful, launched in 2013, has bootstrapped the creation of its white-labeled tools without the need for venture funding.

Memberful gives creators like Stratechery’s Ben Thompson (who has an interview with Patreon CEO Jack Conte about the acquisition) and podcast producer Gimlet Media full control over branding, with no Patreon chrome. But it’s more expensive and also requires more work as creators have to manage their own site, customer service and payment processing. Memberful takes a 10 percent cut with no monthly fee for its limited basic tier, or $25 per month plus 4.9 percent for the full-featured pro version, though it also offers enterprise pricing. That pricing will remain for existing users, but “new customers will see a transaction fee closer to Patreon’s,” which is a flat 5 percent, a Patreon spokesperson tells me. Patreon does basically everything for a creator, but it also ropes them into the Patreon-branded ecosystem that also promotes other content makers.

Sometimes Patreon handling everything can be a problem, though. Last week it experienced a higher-than-normal volume of declines from banks of charges to patrons. That left some creators without their expected income, and required patrons to deal with the chore of calling their bank to tell them paying $1, $5 or $20 per month to their favorite creator wasn’t fraud. Patreon now tells me that “as of Friday, we let everyone know that we were back to normal decline rates, and were going to continue retrying the rest of the cards like we normally do.”

It makes sense for Patreon to race to consolidate the patronage industry as it’s being invaded by giant incumbents. Twitch, YouTube and Facebook all offer their own versions of paid subscriptions to creators that get patrons extra perks like exclusive content or badges so they stick out in chat rooms full of fans. While those platforms are all focused on video streamers, they still pose a threat to Patreon, which needs to maximize the number of successful creators it hosts in order to earn enough from its tiny cut of payments. Facebook especially could muscle in, as many creators already run their own Facebook Pages.

Asked about competition from those platforms, Jenkins said, “I think there’s a strong chance it’s a tailwind. The concept of membership is pretty new. If those big companies are going to drop millions of dollars into marketing the concept of membership I think that’s great.” He stressed the question of “Do you want to own your fan base? On YouTube, those aren’t your fans, they’re YouTube users. YouTube is incentivized to keep them watching videos so it can show ads.”

That might lead fans to unsubscribe from a creator as YouTube promotes other similar ones they could watch instead. “You don’t own the relationship.” Facebook Page admins have found that out the hard way as algorithm changes prioritize friends over public figures, making it tough to reach the followers they spent years begging to like them. If Patreon can offer creators audience growth through discovery on its interconnected network without cannibalizing anyone’s member counts, its neutrality and focus could make it a leader in this new wing of the digital economy.

Powered by WPeMatico

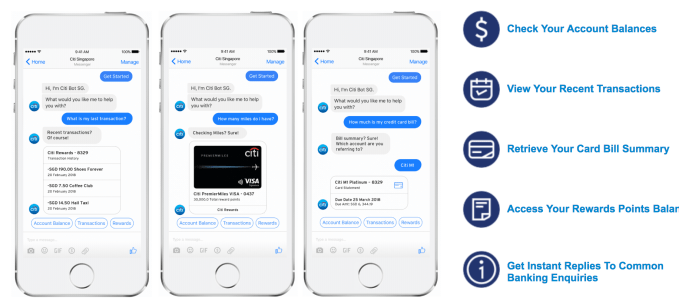

Backlash swelled this morning after Facebook’s aspirations in financial services were blown out of proportion by a Wall Street Journal report that neglected how the social network already works with banks. Facebook spokesperson Elisabeth Diana tells TechCrunch it’s not asking for credit card transaction data from banks and it’s not interested in building a dedicated banking feature where you could interact with your accounts. It also says its work with banks isn’t to gather data to power ad targeting, or even personalize content such as which Marketplace products you see based on what you buy elsewhere.

Instead, Facebook already lets Citibank customers in Singapore connect their accounts so they can ping their bank’s Messenger chatbot to check their balance, report fraud or get customer service’s help if they’re locked out of their account without having to wait on hold on the phone. That chatbot integration, which has no humans on the other end to limit privacy risks, was announced last year and launched this March. Facebook works with PayPal in more than 40 countries to let users get receipts via Messenger for their purchases.

Expansions of these partnerships to more financial services providers could boost usage of Messenger by increasing its convenience — and make it more of a centralized utility akin to China’s WeChat. But Facebook’s relationships with banks in the current form aren’t likely to produce a steep change in ad targeting power that warrants significant heightening of its earning expectations. The reality of today’s news is out of step with the 3.5 percent share price climb triggered by the WSJ’s report.

“A recent Wall Street Journal story implies incorrectly that we are actively asking financial services companies for financial transaction data – this is not true. Like many online companies with commerce businesses, we partner with banks and credit card companies to offer services like customer chat or account management. Account linking enables people to receive real-time updates in Facebook Messenger where people can keep track of their transaction data like account balances, receipts, and shipping updates,” Diana told TechCrunch. “The idea is that messaging with a bank can be better than waiting on hold over the phone – and it’s completely opt-in. We’re not using this information beyond enabling these types of experiences – not for advertising or anything else. A critical part of these partnerships is keeping people’s information safe and secure.”

Diana says banks and credit card companies have also approached it about potential partnerships, not just the other way around as the WSJ reports. She says any features that come from those talks would be opt-in, rather than happening behind users’ backs. The spokesperson stressed these integrations would only be built if they could be privacy safe. For example, signing up to use the Citibank Messenger chatbot requires two-factor authentication through your phone.

But renewed interest in Facebook’s dealings with banks comes at a time when many are pointing to its poor track record with privacy following the Cambridge Analytica scandal, where people were duped into volunteering the personal info of them and their friends. Facebook hasn’t had a big traditional data breach where data was outright stolen, as has befallen LinkedIn, eBay, Yahoo [part of TechCrunch’s parent company] and others. But users are rightfully reluctant to see Facebook ingest any more of their sensitive data for fear it could leak or be misused.

Facebook has recently cracked down on the use of data brokers that suck in public and purchased data sets for ad targeting. It no longer lets data brokers upload Managed Custom Audience lists of user contact info or power Partner Categories for targeting ads based on interests. It also more adamantly demands that advertisers have the consent of users whose email addresses or phone numbers they upload for Custom Audience targeting, though Facebook does little to verify that consent and advertisers could still buy data sets from brokers and upload them themselves

Facebook has recently cracked down on the use of data brokers that suck in public and purchased data sets for ad targeting. It no longer lets data brokers upload Managed Custom Audience lists of user contact info or power Partner Categories for targeting ads based on interests. It also more adamantly demands that advertisers have the consent of users whose email addresses or phone numbers they upload for Custom Audience targeting, though Facebook does little to verify that consent and advertisers could still buy data sets from brokers and upload them themselves

Facebook’s statement today shows more scruples than Google, which last year struck ad measurement data deals with data brokers that have access to 70 percent of credit and debit card transactions in the U.S. That led to a formal complaint to the FTC from the Electronic Privacy Information Center. [Correction: Google tells us the deals are for ad measurement data, not ad targeting as we originally published. It only learns the aggregate purchase value, not what the items were bought, and the data is encrypted.]

Cambridge Analytica has brought on an overdue era of scrutiny regarding privacy and how internet giants use our data. Practices that were overlooked, accepted as industry standard or seen as just the way business gets done are coming under fire. Internet users aren’t likely to escape ads, and some would rather have those they see be relevant thanks to deep targeting data. But the combination of our offline purchase behavior with our online identities seems to trigger uproar absent from sites using cookies to track our web browsing and buying.

Facebook’s probably better off backing away from anything that involves sensitive data like checking account balances until Cambridge Analytica blows over and it’s proven its newfound sense of responsibility translates into a safer social networking. But at least for now, it’s not slurping up our banking data wholesale.

Powered by WPeMatico

Line, the company best-known for its popular Asian messaging app, is doubling down on games after it acquired a controlling stake in Korean studio NextFloor for an undisclosed amount.

NextFloor, which has produced titles like Dragon Flight and Destiny Child, will be merged with Line’s games division to form the Line Games subsidiary. Dragon Flight has racked up 14 million users since its 2012 launch — it clocked $1 million in daily revenue at peak. Destiny Child, a newer release in 2016, topped the charts in Korea and has been popular in Japan, North America and beyond.

Line’s own games are focused on its messaging app, which gives them access to social features such as friend graphs, and they have helped the company become a revenue generation machine. Alongside income from its booming sticker business, in-app purchases within games made Line Japan’s highest-earning non-game app publisher last year, according to App Annie, and the fourth highest worldwide. For some insight into how prolific it has been over the years, Line is ranked as the sixth highest earning iPhone app of all time.

But, despite revenue success, Line has struggled to become a global messaging giant. The big guns WhatsApp and Facebook Messenger have in excess of one billion monthly users each, while Line has been stuck around the 200 million mark for some time. Most of its numbers are from just four countries: Japan, Taiwan, Thailand and Indonesia. While it has been able to tap those markets with additional services like ride-hailing and payments, it is certainly under pressure from those more internationally successful competitors.

With that in mind, doubling down on games makes sense and Line said it plans to focus on non-mobile platforms, which will include the Nintendo Switch among others consoles, from the second half of this year.

Line went public in 2016 via a dual U.S.-Japan IPO that raised over $1 billion.

Powered by WPeMatico

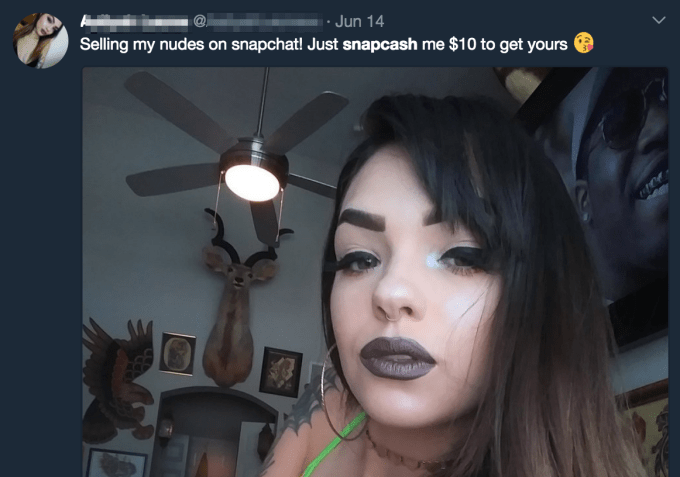

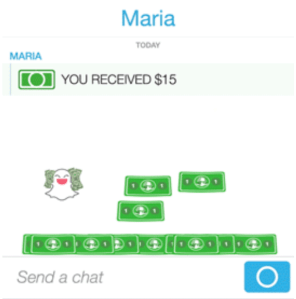

Snapcash ended up as a way to pay adult performers for private content over Snapchat, not just a way to split bills with friends. But Snapchat will abandon the peer-to-peer payment space on August 30th. Code buried in Snapchat’s Android app includes a “Snapcash deprecation message” that displays “Snapcash will no longer be available after %s [date]”. Shutting down the feature will bring an end to Snapchat’s four-year partnership with Square to power the feature for sending people money.

Snapcash may have become more of a liability than a utility. With apps like Venmo, PayPal, Zelle, and Square Cash itself, there were plenty of other ways to pay back friends for drinks or Ubers, so Snapcash may have seen low legitimate usage. Meanwhile, a quick Twitter search for “Snapcash” surfaced plenty of offers of erotic content in exchange for payments through the feature. It may have been safer for Snapchat to ditch Snapcash than risk PR problems over its misuse.

TechCrunch tipster Ishan Agarwal provided the below screenshot of Snapchat’s code to TechCrunch. When presented with the code and asked if Snapcash would shut down, a Snapchat spokesperson confirmed to TechCrunch that it would, explaining: “Yes, we’re discontinuing the Snapcash feature as of August 30, 2018. Snapcash was our first product created in partnership with another company – Square. We’re thankful for all the Snapchatters who used Snapcash for the last four years and for Square’s partnership!” The spokesperson noted that users would be notified in-app and through the support site soon.

Snapcash gave Snapchat a way to get users to connect payment methods to the app. That’s increasingly important as the company aims to become a commerce platforms where you can shop without leaving the app. Having payment info on file is what makes buying things through Snapchat easier than the web and draws brands to use Snapchat storefronts.

We’ll see how Snapchat plans evolve its commerce strategy without this driver. Earlier this month, TechCrunch revealed that Snapchat’s code contained mentions of a project codenamed “eagle” that’s a camera search feature. It was designed to allow users to scan an object or barcode with their Snapchat camera and see product results in Amazon. But since our report, mentions of Amazon have disappeared from the code. It’s unclear what will happen in the future, but camera search could give Snapchat new utility and monetization options.

We’ll see how Snapchat plans evolve its commerce strategy without this driver. Earlier this month, TechCrunch revealed that Snapchat’s code contained mentions of a project codenamed “eagle” that’s a camera search feature. It was designed to allow users to scan an object or barcode with their Snapchat camera and see product results in Amazon. But since our report, mentions of Amazon have disappeared from the code. It’s unclear what will happen in the future, but camera search could give Snapchat new utility and monetization options.

Snapcash won’t be a part of that future, though. Given Snapchat’s cost-cutting efforts including layoffs, its desperate need to attract and retain advertisers to hit revenue estimates its missed, and its persistent bad rap as a sexting app, it couldn’t afford to support unnecessary features or another scandal.

Powered by WPeMatico

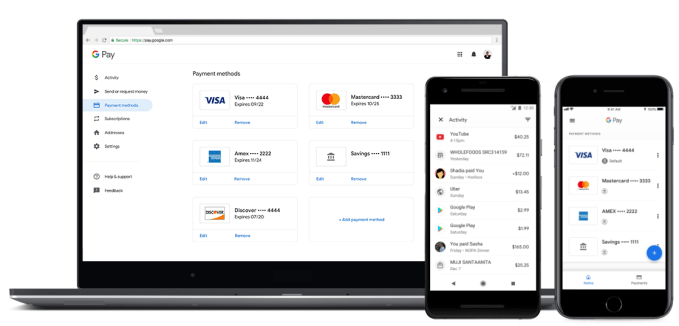

Google is making several updates to Google Pay, its recently-rebranded service for all its different payments tools. Most of these updates were announced earlier this year, but now, Google says they’re actually going live in the app.

One of the additions is peer-to-peer payments. You could already pay or request money from a friend through Google Pay Send, but as of today, you can also do it into the main Google Pay app.

Gerardo Capiel, Director of Product Management at Google Pay, noted that this makes it easier to split the bill with your friends — if you bought something with Google Pay, you can tap on the purchase and then request payment from up to five people.

Since Google is basically combining two apps, it sounds like Google Pay Send isn’t long for this world — as Capiel put it, “We want to basically bring everything into Google Pay,” but he said the timing is “TBD” on when Pay Send might be shut down.

The Google Pay app is also gaining the ability to save mobile tickets and boarding passes, to be found in a new Passes tab that will also include loyalty cards and gift cards. Ticketmaster and Southwest are supported at launch, and Google says it has plans to add Eventbrite, Singapore Airlines and Vueling.

While some of Google Pay’s functionality (like the new Passes Tab) is limited to Android, Capiel said the goal is to support users on any platform. So you can also access Google Pay on the web and on an iOS app. Now Google says it’s making it easier to manage all your payment information across platforms, allowing users (for example) to update their payment info on the web and see it reflected in their app.

Looking ahead, Capiel said his team plans to add support for more ticketing partners, and also to launch the Google Pay app in more countries — particularly the ones where the service is already being used for online payments.

“We’re working to bring everything into the app,” he added. “Some things are a little trickier than others, for a number of reasons, but we will continue to make the experience as complete as possible.”

Powered by WPeMatico

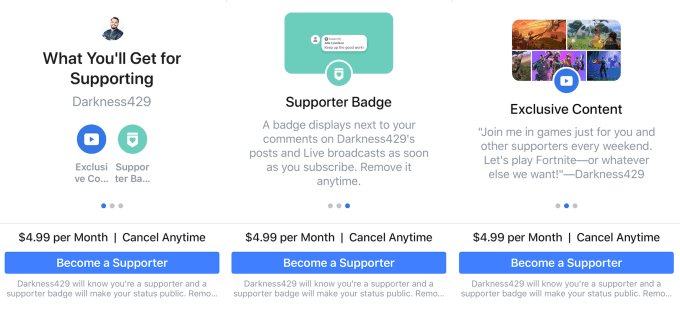

Facebook is starting to let Group admins charge $4.99 to $29.99 per month for access to special sub-Groups full of exclusive posts. A hand-picked array of parenting, cooking and “organize my home” Groups will be the first to get the chance to spawn a subscription Group open to their members.

During the test, Facebook won’t be taking a cut, but because the feature bills through iOS and Android, those operating systems get their 30 percent cut of a user’s first year of subscription and 15 percent after that. But if Facebook eventually did ask for a revenue share, it could finally start to monetize the Groups feature that’s grown to more than 1 billion users.

The idea for subscription Groups originally came from the admins. “It’s not so much about making money as it is investing in their community,” says Facebook Groups product manager Alex Deve. “The fact that there will be funds coming out of the activity helps them create higher-quality content.” Some admins tell Facebook they actually want to funnel subscription dues back into activities their Group does together offline.

Content users might get in the exclusive version of groups includes video tutorials, lists of tips and support directly from admins themselves. For example, Sarah Mueller’s Declutter My Home Group is launching a $14.99 per month Organize My Home subscription Group that will teach members how to stay tidy with checklists and video guides. The Grown and Flown Parents group is spawning a College Admissions and Affordability subscription group with access to college counselors for $29.99. Cooking On A Budget: Recipes & Meal Planning will launch a $9.99 Meal Planning Central Premium subscription group with weekly meal plans, shopping lists for different grocery stores and more.

But the point of the test is actually to figure out what admins would post and whether members find it valuable. “They have their own ideas. We want to see how that is going to evolve,” says Deve.

Here’s how subscription Groups work. First, a user must be in a larger group where the admin has access to the subscription options and posts an invitation for members to check it out. They’ll see preview cards outlining what exclusive content they’ll get access to and how much it costs. If they want to join, and they’re already an approved member of larger free group, they’re charged the monthly fee right away.

They’ll be billed on that date each month, and if they cancel, they’ll still have access until the end of their billing cycle. That prevents anyone from joining a group and scraping all the content without paying the full price. The whole system is a bit similar to subscription patronage platform Patreon, but with a Group and its admin at the center instead of some star creator.

Back in 2016, Facebook briefly tested showing ads in Groups, but now says that was never rolled out. However, the company says that admins want other ways beyond subscriptions to build revenue from Groups and it’s considering the possibilities. Facebook didn’t have any more to share on this, but perhaps one day it will offer a revenue split from ads shown within groups.

Between subscriptions, ad revenue shares, tipping, sponsored content and product placement — all of which Facebook is testing — creators are suddenly flush with monetization options. While we spent the last few decades of the consumer internet scarfing up free content, creativity can’t be a labor of love forever. Letting creators earn money could help them turn their passion into their profession and dedicate more time to making things people love.

Powered by WPeMatico

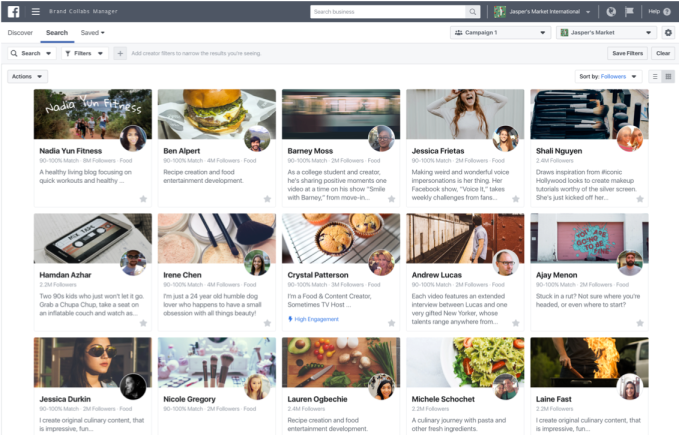

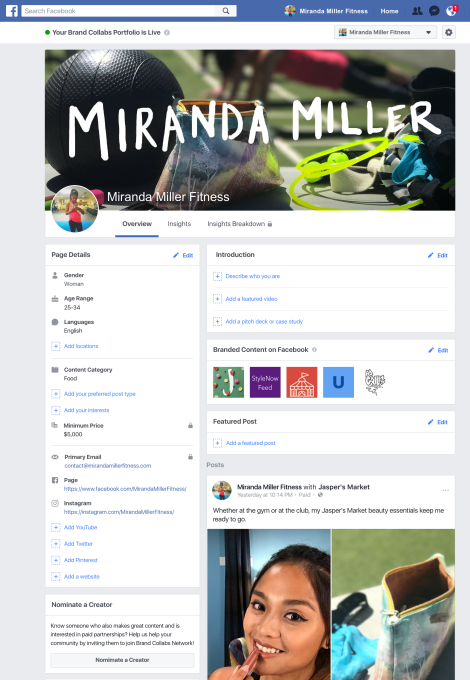

Facebook wants to help connect brands to creators so they can work out sponsored content and product placement deals, even if it won’t be taking a cut. Confirming our scoop from May, Facebook today launched its Brand Collabs Manager. It’s a search engine that brands can use to browse different web celebrities based on the demographics of their audience and portfolios of their past sponsored content.

Creators hoping to score sponsorship deals will be able to compile a portfolio connected to their Facebook Page that shows off how they can seamlessly work brands into their content. Brands will also be able to find them based on the top countries where they’re popular, and audience characteristics like interests, gender, education, relationship status, life events or home ownership.

Facebook also made a wide range of other creator monetization announcements today:

Facebook also made a big announcement today about the launch of interactive video features and its first set of gameshows built with them. Creators can add quizzes, polls, gamification and more to their videos so users can play along instead of passively viewing. Facebook’s Watch hub for original content is also expanding to a wider range of show formats and creators.

Facebook needs the hottest new content from creators if it wants to prevent users’ attention from slipping to YouTube, Netflix, Twitch and elsewhere. But to keep creators loyal, it has to make sure they’re earning money off its platform. The problem is, injecting Ad Breaks that don’t scare off viewers can be difficult, especially on shorter videos.

But Vine proved that six seconds can be enough to convey a subtle marketing message. A startup called Niche rose to arrange deals between creators and brands who wanted a musician to make a song out of the windows and doors of their new Honda car, or a comedian to make a joke referencing Coca-Cola. Twitter eventually acquired Niche for a reported $50 million so it could earn money off Vine without having to insert traditional ads. [Disclosure: My cousin Darren Lachtman was a co-founder of Niche.]

But Vine proved that six seconds can be enough to convey a subtle marketing message. A startup called Niche rose to arrange deals between creators and brands who wanted a musician to make a song out of the windows and doors of their new Honda car, or a comedian to make a joke referencing Coca-Cola. Twitter eventually acquired Niche for a reported $50 million so it could earn money off Vine without having to insert traditional ads. [Disclosure: My cousin Darren Lachtman was a co-founder of Niche.]

Vine naturally attracted content makers in a way that Facebook has had some trouble with. YouTube’s sizable ad revenue shares, Patreon’s subscriptions and Twitch’s fan tipping are pulling creators away from Facebook.

So rather than immediately try to monetize this sponsored content, Facebook is launching the Brand Collabs Manager to prove to creators that it can get them paid indirectly. Facebook already offered a way for creators to tag their content with disclosure tags about brands they were working with. But now it’s going out of its way to facilitate the deals. Fan subscriptions and tipping come from the same motive: letting creators monetize through their audience rather than the platform itself.

Spinning up these initiatives to be more than third-rate knockoffs of Niche, YouTube, Patreon and Twitch will take some work. But hey, it’s cheaper for Facebook than paying these viral stars out of pocket.

Powered by WPeMatico

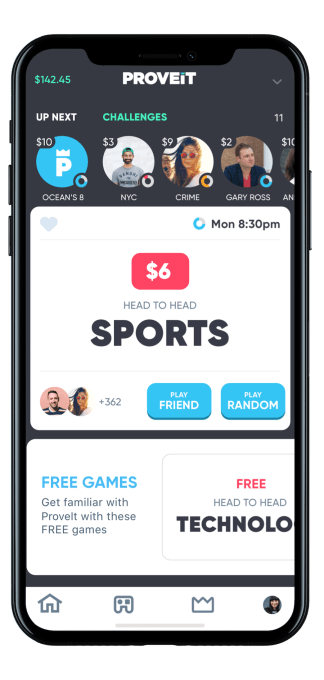

Pick a category, wager a few dollars and double your money in 60 seconds if you’re smarter and faster than your opponent. Proveit offers a fresh take on trivia and game show apps by letting you win or lose cash on quick 10-question, multiple choice quizzes. Sick of waiting to battle a million people on HQ for a chance at a fraction of the jackpot? Play one-on-one anytime you want or enter into scheduled tournaments with $1,000 or more in prize money, while Proveit takes around 10 percent to 15 percent of the stakes.

“I’d play Jeopardy all the time with my family and wondered ‘why can’t I do this for money?’ ” says co-founder Prem Thomas.

Remarkably, it’s all legal. The Proveit team spent two years getting approved as “skill-based gaming” that exempts it from some laws that have hindered fantasy sports betting apps. And for those at risk of addiction, Proveit offers players and their loved ones a way to cut them off.

The scrappy Florida-based startup has raised $2.3 million so far. With fun games and a snackable format, Proveit lets you enjoy the thrill of betting at a moment’s notice. That could make it a favorite amongst players and investors in a world of mobile games without consequences.

“I could spend $50 for a three-hour experience in a movie theater, or I could spend $2 to enter a Proveit Movies tournament that gives me the opportunity to compete for several thousand dollars in prize money,” says co-founder Nathan Lehoux. “That could pay for a lot of movies tickets!”

St. Petersburg, Fla. isn’t exactly known as an innovation hub. But outside Tampa Bay, far from the distractions, copycatting and astronomical rent of Silicon Valley, the founders of Proveit built something different. “What if people could play trivia for money just like fantasy sports?” Thomas asked his friend Lehoux.

St. Petersburg, Fla. isn’t exactly known as an innovation hub. But outside Tampa Bay, far from the distractions, copycatting and astronomical rent of Silicon Valley, the founders of Proveit built something different. “What if people could play trivia for money just like fantasy sports?” Thomas asked his friend Lehoux.

That’s the same pitch that got me interested when Lehoux tracked me down at TechCrunch’s SXSW party earlier this year. Lehoux is a jolly, outgoing fella who became interested in startups while managing some angel investments for a family office. Thomas had worked in banking and health before starting a yoga-inspired sandals brand. Neither had computer science backgrounds, and they’d raised just a $300,000 seed round from childhood friend Hilt Tatum who’d co-founded beleaguered real money gambling site Absolute Poker.

Yet when he Lehoux thrust the Proveit app into my hand, even on a clogged mobile network at SXSW, it ran smoothly and I immediately felt the adrenaline rush of matching wits for money. They’d initially outsourced development to an NYC firm that burned much of their initial $300,000 seed funding without delivering. Luckily, the Ukrainian they’d hired to help review that shop’s code helped them spin up a whole team there that built an impressive v1 of Proveit.

Meanwhile, the founders worked with a gaming lawyer to secure approvals in 33 states including California, New York, and Texas. “This is a highly regulated and highly controversial space due to all the negative press that fantasy sports drummed up,” says Lehoux. “We talked to 100 banks and processors before finding one who’d work with us.”

Proveit founders (from left): Nathan Lehoux, Prem Thomas

Proveit was finally legal for the three-fourths of the U.S. population, and had a regulatory moat to deter competitors. To raise launch capital, the duo tapped their Florida connections to find John Morgan, a high-profile lawyer and medical marijuana advocate, who footed a $2 million angel round. A team of grad students in Tampa Bay was assembled to concoct the trivia questions, while a third-party AI company assists with weeding out fraud.

Proveit launched early this year, but beyond a SXSW promotion, it has stayed under the radar as it tinkers with tournaments and retention tactics. The app has now reached 80,000 registered users, 6,000 multi-deposit hardcore loyalists and has paid out $750,000 total. But watching HQ trivia climb to more than 1 million players per game has proven a bigger market for Proveit.

“We’re actually fans of HQ. We play. We think they’ve revolutionized the game show,” Lehoux tells me. “What we want to do is provide something very different. With HQ, you can’t pick your category. You can’t pick the time you want to play. We want to offer a much more customized experience.”

![]()

To play Proveit, you download its iOS-only app and fund your account with a buy-in of $20 to $100, earning more bonus cash with bigger packages (no minors allowed). Then you play a practice round to get the hang of it — something HQ sorely lacks. Once you’re ready, you pick from a list of game categories, each with a fixed wager of about $1 to $5 to play (choose your own bet is in the works). You can test your knowledge of superheroes, the ’90s, quotes, current events, rock ‘n roll, Seinfeld, tech and a rotating selection of other topics.

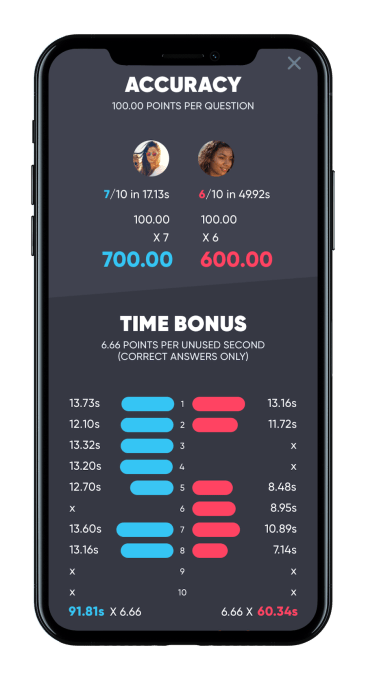

In each Proveit game you get 10 questions, 1 at a time, with up to 15 seconds to answer each. Most games are head-to-head, with options to be matched with a stranger, or a friend via phone contacts. You score more for quick answers, discouraging cheating via Google, and get penalized for errors. At the end, your score is tallied up and compared to your opponent, with the winner keeping both player’s wagers minus Proveit’s cut. In a minute or so, you could lose $3 or win $5.28. Afterwards you can demand a rematch, go double-or-nothing, head back to the category list or cash out if you have more than $20.

The speed element creates intense, white-knuckled urgency. You can get every question right and still lose if your opponent is faster. So instead of second-guessing until locking in your choice just before the buzzer like on HQ, where one error knocks you out, you race to convert your instincts into answers on Proveit. The near instant gratification of a win or humiliation of a defeat nudge you to play again rather than having to wait for tomorrow’s game.

The speed element creates intense, white-knuckled urgency. You can get every question right and still lose if your opponent is faster. So instead of second-guessing until locking in your choice just before the buzzer like on HQ, where one error knocks you out, you race to convert your instincts into answers on Proveit. The near instant gratification of a win or humiliation of a defeat nudge you to play again rather than having to wait for tomorrow’s game.

Proveit will have to compete with free apps like Trivia Crack, prize games like student loan repayer Givling and virtual currency-based Fleetwit, and the juggernaut HQ.

“The large tournaments are the big draw,” Lehoux believes. Instead of playing one-on-one, you can register and ante up for a scheduled tournament where you compete in a single round against hundreds of players for a grand prize. Right now, the players with the top 20 percent of scores win at least their entry fee back or more, with a few geniuses collecting the cash of the rest of the losers.

Just like how DraftKings and FanDuel built their user base with big jackpot tournaments, Proveit hopes to do the same… then get people playing little one-on-one games in-between as they wait for their coffee or commute home from work.

Thankfully, Proveit understands just how addictive it can be. The startup offers a “self-exclusion” option. “If you feel that you need to take greater control of your life as it relates to skill-gaming,” users can email it to say they shouldn’t play any more, and it will freeze or close their account. Family members and others can also request you be frozen if you share a bank account, they’re your dependant, they’re obligated for your debts or you owe unpaid child support.

“We want Proveit to be a fun, intelligent entertainment option for our players. It’s impossible for us to know who might have an issue with real-money gaming,” Lehoux tells me. “Every responsible real-money game provides this type of option for its users.

That isn’t necessarily enough to thwart addiction, because dopamine can turn people into dopes. Just because the outcome is determined by your answers rather than someone else’s touchdown pass doesn’t change that.

Skill-based betting from home could be much more ripe for abuse than having to drag yourself to a casino, while giving people an excuse that they’re not gambling on chance. Zynga’s titles like Farmville have been turning people into micro-transaction zombies for a decade, and you can’t even win money from them. Simultaneously, sharks could study up on a category and let Proveit’s random matching deliver them willing rookies to strip cash from all day. “This is actually one of the few forms of entertainment that rewards players financially for using their brain,” Lehoux defends.

With so much content to consume and consequence-free games to play, there’s an edgy appeal to the danger of Proveit and apps like it. Its moral stance hinges on how much autonomy you think adults should be afforded. From Coca-Cola to Harley-Davidson to Caesar’s Palace, society has allowed businesses to profit off questionably safe products that some enjoy.

For better and worse, Proveit is one of the most exciting mobile games I’ve ever played.

Powered by WPeMatico

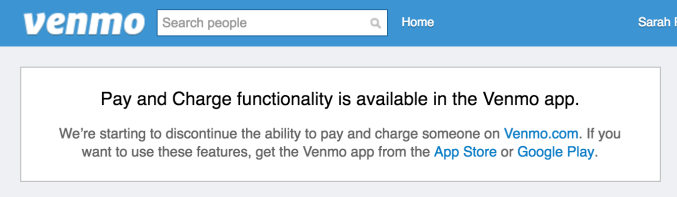

PayPal-owned, peer-to-peer payments app Venmo is ending web support for its service, the company announced in an email to users. The changes, which are beginning to roll out now, will see the Venmo .com website phasing out support for making payments and charging users. In time, users will see even less functionality on the website, the company says.

The message to users was quietly shared in the body of Venmo’s monthly transaction history email. It reads as follows:

NOTICE: Venmo has decided to phase out some of the functionality on the Venmo.com website over the coming months. We are beginning to discontinue the ability to pay and charge someone on the Venmo.com website, and over time, you may see less functionality on the website – this is just the start. We therefore have updated our user agreement to reflect that the use of Venmo on the Venmo.com website may be limited.

The decision represents a notable shift in product direction for Venmo. Though best known as a mobile payments app, the service has also been available online, similar to PayPal, for many years.

The Venmo website today allows users to sign in and view their various transaction feeds, including public transactions, those from friends, and personal transactions. You can also charge friends and submit payments from the website, send payment reminders, like and comment on transactions, add friends, edit your profile, and more.

Some users may already be impacted by the changes, and will now see a message alerting them to the fact that charging friends and making payments can only be done in the Venmo app from the App Store or Google Play.

It’s not entirely surprising to see Venmo drop web support. As a PayPal-owned property after its acquisition by Braintree which later brought it to PayPal, there’s always been a lot of overlap between Venmo and its parent company, in terms of peer-to-peer payments.

Venmo had grown in popularity for its simple, social network-inspired design and its less burdensome fee structure among a younger crowd. This made it an appealing way for PayPal to gain market share with a different demographic.

It’s also cheaper, which people like. PayPal doesn’t charge for money transfers from a bank account or PayPal balance, but does charge 2.9 percent plus a $0.30 fixed fee on payments from a credit or debit card in the U.S. Venmo, meanwhile, charges a fee of 3 percent for credit card payments, but makes debit card payments free. That’s appealing to millennials in particular, many of whom have ditched credit cards entirely, and are careful about their spending.

Plus, as a mobile-first application, Venmo was offering a more modern solution for mobile payments, at a time when PayPal’s app was looking a bit long in the tooth. (PayPal has since redesigned its mobile app experience to catch up.)

Another factor in Venmo’s decision could be that, more recently, it began facing competition from newcomer Zelle, the bank-backed mobile payments here in the U.S. which is forecast to outpace Venmo on users sometime this year, with 27.4 million users to Venmo’s 22.9 million. In light of that threat, Venmo may have wanted to consolidate its resources on its primary product – the mobile app.

Not everyone is happy about Venmo’s changes, of course. After all, even if the Venmo website wasn’t heavily used, it was used by some who will certainly miss it.

@venmo i only use the website to send/receive payments so in guess you’re cancelled!

— respectfully yours (@biking_away_) June 15, 2018

@venmo This makes me really #sad….”Venmo has decided to phase out some of the functionality on the https://t.co/Dw7W551BsL website over the coming months.” #CanWeGoBackToHowItWas

— V Lav (@Druzy920) June 14, 2018

@venmo Why are you breaking your website?

— Lozaning (@lozaning) June 14, 2018

@VenmoSupport @venmo Just got an email saying you’re phasing out website functions. What’s the justification? Pay and charge by web is incredibly useful.

— Woode (@Woode2380) June 14, 2018

Venmo email: “We are beginning to discontinue the ability to pay and charge someone on the https://t.co/iAFTbn3EY0 website, and over time, you may see less functionality on the website – this is just the start.”

Is this a threat?

— Noah Mittman (@noahmittman) June 14, 2018

Reached for comment, Venmo explained the decision to phase out the website functionality stems from how it sees its product being used.

A Venmo spokesperson told TechCrunch:

Venmo continuously evaluates our products and services to ensure we are delivering our users the best experience. We have decided to begin to discontinue the ability to pay and charge someone on the Venmo.com website. Most of our users pay and request money using the Venmo app, so we’re focusing our efforts there. Users can continue to use the mobile app for their pay and charge transactions and can still use the website for cashing out Venmo balances, settings and statements.

The company declined to clarify what other functionality may be removed from the website over time, but noted that using Venmo to pay authorized merchants is unaffected.

Powered by WPeMatico