payments

Auto Added by WPeMatico

Auto Added by WPeMatico

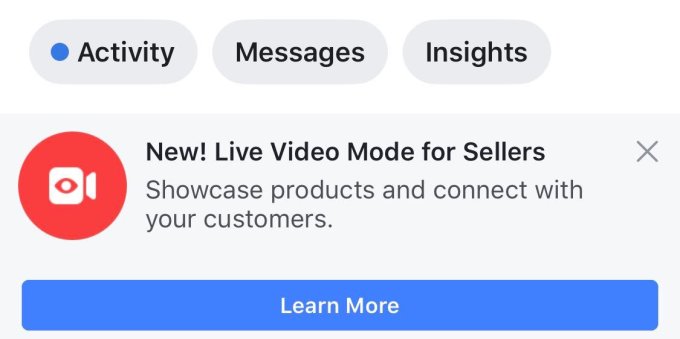

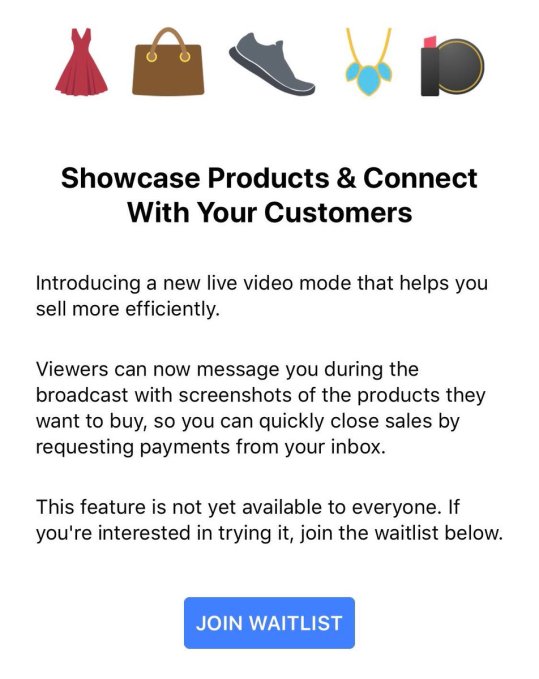

Want to run your own home shopping network? Facebook is now testing a Live video feature for merchants that lets them demo and describe their items for viewers. Customers can screenshot something they want to buy and use Messenger to send it to the seller, who can then request payment right through the chat app.

Facebook confirms the new shopping feature is currently in testing with a limited set of Pages in Thailand, which has been a testbed for shopping features. The option was first spotted by social media and reputation manager Jeff Higgins, and re-shared by Matt Navarra and Social Media Today. But now Facebook is confirming the test’s existence and providing additional details.

The company tells me it had heard feedback from the community in Thailand that Live video helped sellers demonstrate how items could be used or worn, and provided richer understanding than just using photos. Users also told Facebook that Live’s interactivity let customers instantly ask questions and get answers about product specifications and details. Facebook has looked to Thailand to test new commerce experiences like home rentals in Marketplace, as the country’s citizens were quick to prove how Facebook Groups could be used for peer-to-peer shopping. “Thailand is one of our most active Marketplace communities” says Mayank Yadav, Facebook product manager for Marketplace.

The company tells me it had heard feedback from the community in Thailand that Live video helped sellers demonstrate how items could be used or worn, and provided richer understanding than just using photos. Users also told Facebook that Live’s interactivity let customers instantly ask questions and get answers about product specifications and details. Facebook has looked to Thailand to test new commerce experiences like home rentals in Marketplace, as the country’s citizens were quick to prove how Facebook Groups could be used for peer-to-peer shopping. “Thailand is one of our most active Marketplace communities” says Mayank Yadav, Facebook product manager for Marketplace.

Now it’s running the Live shopping test, which allows Pages to notify fans that they’re broadcasting to “showcase products and connect with your customers.” Merchants can take reservations and request payments through Messenger. Facebook tells me it doesn’t currently have plans to add new partners or expand the feature. But some sellers without access are being invited to join a waitlist for the feature. It also says it’s working closely with its test partners to gather feedback and iterate on the live video shopping experience, which would seem to indicate it’s interested in opening the feature more widely if it performs well.

Facebook doesn’t take a cut of payments through Messenger, but the feature could still help earn the company money at a time when it’s seeking revenue streams beyond News Feed ads as it runs out of space there, Stories take over as the top media form and user growth plateaus. Hooking people on video viewing helps Facebook show lucrative video ads. The more that Facebook can train users to buy and sell things on its app, the better the conversion rates will be for businesses, and the more they’ll be willing to spend on ads. Facebook could also convince sellers who broadcast Live to buy its new Marketplace ad units to promote their wares. And Facebook is happy to snatch any use case from the rest of the internet, whether it’s long-form video viewing or job applications or shopping to boost time on site and subsequent ad views.

Increasingly, Facebook is setting its sights on Craigslist, Etsy and eBay. Those commerce platforms have failed to keep up with new technologies like video and lack the trust generated by Facebook’s real-name policy and social graph. A few years ago, selling something online meant typing up a generic description and maybe uploading a photo. Soon it could mean starring in your own infomercial.

[PostScript: And a Facebook home shopping network could work perfectly on its new countertop smart display Portal.]

Powered by WPeMatico

After going public in the U.K. last year, Boku has made an acquisition to expand its carrier billing services, which let users bill to their mobile bills mobile content purchases from companies like Apple, Microsoft, Spotify and 152 other app and other content purveyors. Today, Boku announced the acquisition of Danal, Inc., a specialist in mobile identity and authentication services, so that it can offer more sophisticated transaction services and also to move into new areas.

Boku will pay up to $68 million for Danal, the company said. Specifically, the financial terms are described by Boku as a “reverse triangular merger” and include 26.7 million Boku common shares of $0.0001 each (“Common Shares”), $3 million of Boku warrants exercisable at 141p each and $1 million in cash, along with a deferred consideration of up to $64 million, “satisfied in Common Shares and warrants, dependent on Danal’s future performance,” which Boku also described as “challenging performance targets for Danal, thereby allowing both parties to share the benefits of efficiencies and growth.”

Danal, Boku said, will become a part of a U.S. subsidiary of Boku.

The market is not particularly excited by the deal it seems: the company’s stock has dropped by more than 23 percent in trading today. Boku currently has a market cap of around £168 million ($216 million), and it says that total payment volume in the 10 months to October was up 124 percent to $2.8 billion (versus $1.3 billion the year before), and monthly active users were 12.2 million in October, up 83 percent on a year before.

This is not Danal’s first transaction with a carrier billing service. In 2016, it sold a portion of its business, BilltoMobile, to Bango for $3.5 million.

Boku is buying the rest of the business left behind, with a view to building a bridge between the data that carriers have about their users and services that those users might engage with either on their mobile devices or through other digital channels. This could include expanding the range of purchases that you can make through carrier billing, but it could potentially also be applied to any service that either has a risk of fraud — such as financial or government-run services — or could use a carrier data to help authenticate the identity of the user.

“Charging purchases to your phone bill has proved a great way for the world’s largest digital companies to acquire and retain users, but has had fairly limited application outside digital content,” said Jon Prideaux, CEO of Boku, in a statement. “This Acquisition allows us to offer services that go further and to improve user quality for our customers while at the same time improving the mobile experience for users. Mobile commerce is booming, yet many tools were developed to support PC-based commerce. Danal has shown that MNO data can also combat fraud, reduce friction in signup and ensure regulatory compliance on mobile. These problems are relevant not just to our existing digital customers but also in other sectors including e-commerce, finance, transportation and government.”

Notably, this potentially could help Boku grow revenues in developed markets alongside the emerging markets where it is currently active.

Danal, based in San Jose, already counts financial institutions, government agencies and retailers as customers, including Western Union, BNP Paribas, PayPal, Square, MoneyGram, Login.gov and USAA.

Boku said Danal generated revenue of $5.1 million and a loss before interest, taxation, depreciation and amortization of $5.2 million for the full year that ended December 31, 2017. Liabilities as of that date were $10.3 million.

The bigger picture for mobile payments are that while they continue to grow, they are still just around one-third of all e-commerce transactions, according to recent figures collected over the opening weekend of holiday sales.

Within that, billing to carriers is just one part of the overall mix, and after accounting for others in the transaction chain, it makes for thin margins. This explains partly why Boku would be working on adding new revenue streams. But in emerging markets, carrier billing is a popular alternative among users who may not have bank accounts and payment cards. This latest deal for Boku should help it in that area, too.

Powered by WPeMatico

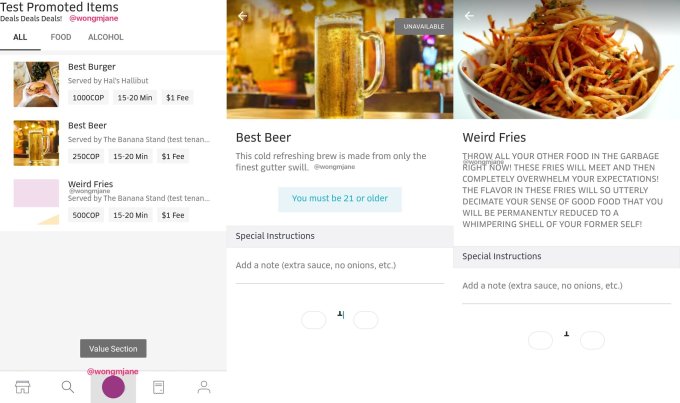

Uber Eats has effectively invented its own native ad unit. Uber confirmed to TechCrunch that a test quietly running in markets around India allows restaurants to bundle several food items together and sell them at a discounted price in exchange for promoted placement by Uber Eats in a featured section of local “Specials.” In some cases, restaurants foot the cost of the discount, while in others Uber pays for the discounts.

The Uber Specials feature demonstrates the massive leverage awarded to food delivery apps that aggregate restaurants. Users often come to Uber Eats and its competitors without a specific restaurant in mind. Uber can then point those customers to whichever food supplier it prefers. The suppliers in turn will increasingly compete for the favor of the aggregators — not just in terms of food quality, speed and review scores, but also in terms of discounts. The aggregators will win users if they offer the best deals; creating a network effect makes restaurants more keen to play ball.

TechCrunch first learned of Uber’s ambitions in the space from a mock-up of the Promoted Items Value Section feature spotted in its app by mobile researcher and frequent TC tipster Jane Manchun Wong. The fictional food items included “Best Beer” that “is made from only the finest gutter swill” and “Weird Fries” that “will so utterly decimate your sense of good food that you will be permanently reduced to a whimpering shell of your former self!” This jokey text that seemingly was never meant for public viewing also noted that the fries are so good you should “throw all your other food in the garbage right now!” Uber assured us these weren’t real.

But what it did confirm is that the discounts for promoted placement test is live in India. “We’re always experimenting with ways to make it easier to find your favorite foods on Uber Eats,, according to a statement provided by an Uber spokesperson.

The feature allows restaurants to create a bundled meal at a certain price point, such as a chicken sandwich, french fries and a drink at a price that’s less than the sum of its parts. The company tells me the goal is to take the friction out of ordering by giving people pre-set meals at a better price prominently available in the app. Attracting more customers that have plenty of other options could offset the discount. Businesses could also use it to bundle high-margin items, like soft drinks, with meals, or to get rid of overstock.

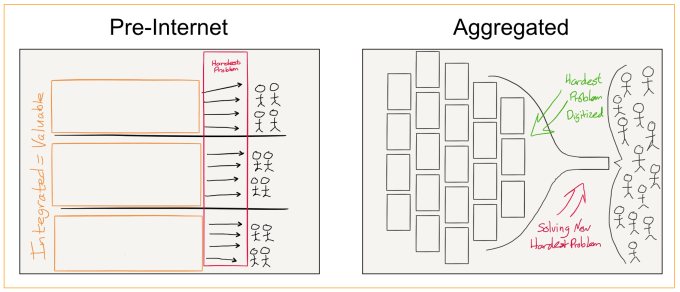

Ben Thompson’s aggregation theory describes how power accrues to aggregators that match supply with demand

It’s already common for restaurants to make “specials” out of food they have too much of. That butternut squash ravioli might only be featured because they can’t get rid of it. In that sense, you could think of Uber Specials as the inverse of surge pricing. When supply is too high, restaurants can offer discounts to gain more demand. It’s also not far off from Google Search’s keyword ads where business pay for more visibility.

Uber wouldn’t discuss whether it plans to bring the strategy to other markets, but it makes sense to assume it’s considering expansion. Done wrong, it could look a bit like Uber Eats is pressuring restaurants to surrender discounts if they want to be discoverable inside its app. If restaurants within Uber Eats get into heated competition to offer discounts, it could drive down their profits. But done right, Specials could look like a triple-win. Restaurants can offload surplus and bundle in high-margin items while scoring new customers from enhanced placement, customers get cheaper food options and Uber Eats becomes people’s go-to app for easy-to-order discounted meals.

Powered by WPeMatico

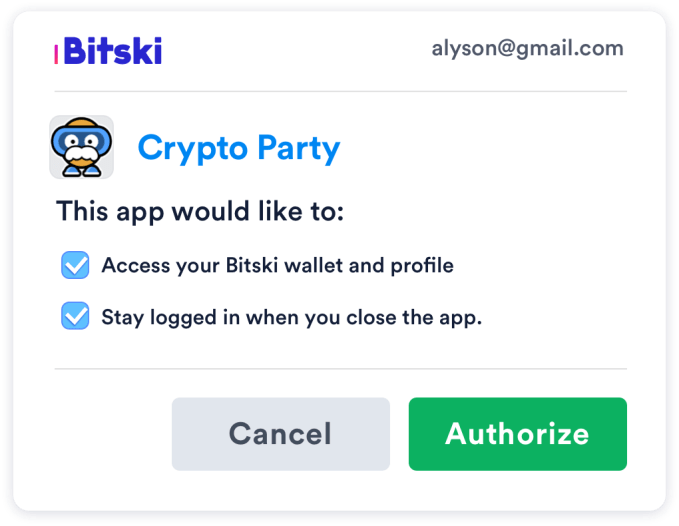

The mainstream will never adopt blockchain-powered decentralized apps (dApps) if it’s a struggle to log in. They’re either forced to manage complex security keys themselves, or rely on a clunky wallet-equipped browser like MetaMask. What users need is for signing in to blockchain apps to be as easy as Login with Facebook. So that’s what Bitski built. The startup emerges from stealth today with an exclusive on TechCrunch about the release of the developer beta of its single sign-on cryptocurrency wallet platform.

Ten projects, including 7 game developers, are lined up to pay a fee to integrate Bitski’s SDK. Then, whenever they need a user’s identity or to transact a payment, their app pops open a Bitski authorization screen, where users can grant permissions to access their ID, send money or receive items. Users sign up just once with Bitski, and then there’s no more punching in long private keys or other friction. Using blockchain apps becomes simple enough for novices. Given the recent price plunge, the mainstream has been spooked about speculating on cryptocurrencies. But Bitski could unlock the utility of dApps that blockchain developers have been promising but haven’t delivered.

“One of the great challenges for protocol teams and product companies in crypto today is the poor UX in dApps, specifically onboarding, transactions, and sign-in/password recovery,” says co-founder and CEO Donnie Dinch. “We interviewed a ton of dApp developers. The minute they used a wallet, there was a huge drop-off of folks. Bitski’s vision is to solve user onboarding and wallet usability for developers, so that they can in-turn focus on creating unique and useful dapps.”

The scrappy Bitski team raised $1.5 million in pre-seed capital from Steve Jang’s Kindred Ventures, Signia, Founders Fund, Village Global and Social Capital. They were betting on Dinch, a designer-as-CEO who’d built concert discovery app WillCall that he sold to Ticketfly, which was eventually bought by Pandora. After 18 months of rebranding Ticketfly and overhauling its consumer experience, Dinch left and eventually recruited engineer Julian Tescher to come with him to found Bitski.

Bitski co-founder and CEO Donnie Dinch

After Riff failed to hit scale, the team hung up its social ambitions in late 2017 and “started kicking around ideas for dApps. We mocked up a Venmo one, a remittance app…but found the hurdle to get someone to use one of these products is enormous,” Dinch recalls. “Onboarding was a dealbreaker for anyone building dApps. Even if we made the best crypto Venmo, to get normal people on it would be extremely difficult. It’s already hard enough to get people to install apps from the App Store.” They came up with Bitski to let any developer ski jump over that hurdle.

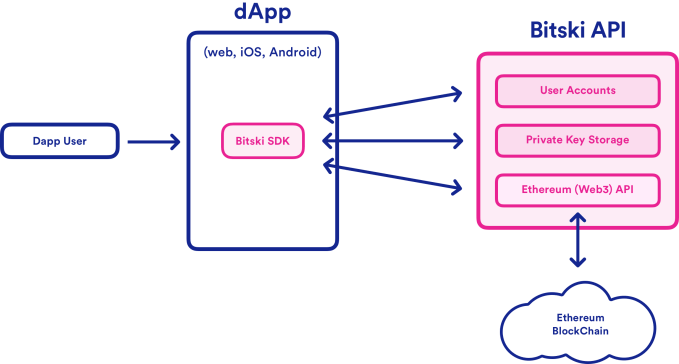

Looking across the crypto industry, the companies like Coinbase and Binance with their own hosted wallets that permitted smooth UX were the ones winning. Bitski would bring that same experience to any app. “Our hosted wallet SDK lets developers drop the Bitski wallet into their apps and onboard users with standards web 2.0 users have grown to know and love,” Dinch explains.

Imagine an iOS game wants to reward users with a digital sword or token. Users would have to set up a whole new wallet, struggle with their credentials or use another clumsy solution. They’d have to own Ethereum already to pay the Ethereum “gas” price to power the transaction, and the developer would have to manually approve sending the gift. With Bitski, users can approve receiving tokens from a developer from then on, and developers can pay the gas on users’ behalf while triggering transactions programmatically.

Magik is an AR content platform that’s one of Bitski’s first developers. Magik’s founders tell me, “We’re building towards reaching millions of mainstream consumers, and Bitski is the only wallet solution that understands what we need to reach users at that scale. They provide a dead-simple, secure and familiar interface that addresses every pain point along the user-onboarding journey.”

Bitski will offer a free tier, priced tiers based on transaction volume or a monthly fee and an enterprise version. In the future, the company is considering doubling-down on premium developer services to help them build more on top of the blockchain. “We will never, ever monetize user data. We’ve never had any intent at looking at it,” Dinch vows. The startup hopes developers will seize on the network effects of a cross-app wallet, as once someone sets up Bitski to use one product, all future sign-ins just require a few clicks.

In August, Coinbase acquired a startup called Distributed Systems that was building a similar crypto identity platform called the Clear Protocol. A “login with Coinbase” feature could be popular if launched, but the company’s focus is to spread a ton of blockchain projects. “If [login with Coinbase] launched tomorrow, they wouldn’t be able to support games or anything with a unique token. We’re a lockbox, they’re a bank,” Dinch claims.

The spectre of single sign-on’s biggest player, Facebook, looms, as well. In May it announced the formation of a blockchain team we suspect might be working on a crypto login platform or other ways to make the decentralized world more accessible for mom and pop. Dinch suspects that fears about how Facebook uses data would dissuade developers and users from adopting such a product. Still, Bitski’s haste in getting its developer platform into beta just a year after forming shows it’s eager to beat them to market.

Building a centralized wallet in a decentralized ecosystem comes with its own security risks. But Dinch assures me Bitski is using all its own hardware with air-gapped computers that have been stripped of their Wi-Fi cards, and it’s taking other secret precautions to prevent anyone from snatching its wallets. He believes cross-app wallets will also deliver a future where users actually own their virtual goods instead of just relying on the good will of developers not to pull them away or shut them down.” The idea of we’ve never been able to provably own unique digital assets is crazy to me,” Dinch notes. “Whether it’s a skin in Fortnite or a movie on iTunes that you purchase, you don’t have liquidity to resell those things. We think we’ll look back in 5 to 10 years and think it’s nuts that no one owned their digital items.”

While the crypto prices might be cratering and dApps like Cryptokitties have cooled off, Dinch is convinced the blockchain startups won’t fade away. “There is a thriving developer ecosystem hellbent on bringing the decentralized web to reality; regardless of token price. It’s a safe assumption that prices will dip a bit more, but will eventually rise whenever we see real use cases for a lot of these tokens. Most will die. The ones that succeed will be outcome-oriented, building useful products that people want.” Bitski’s a big step in that direction.

Powered by WPeMatico

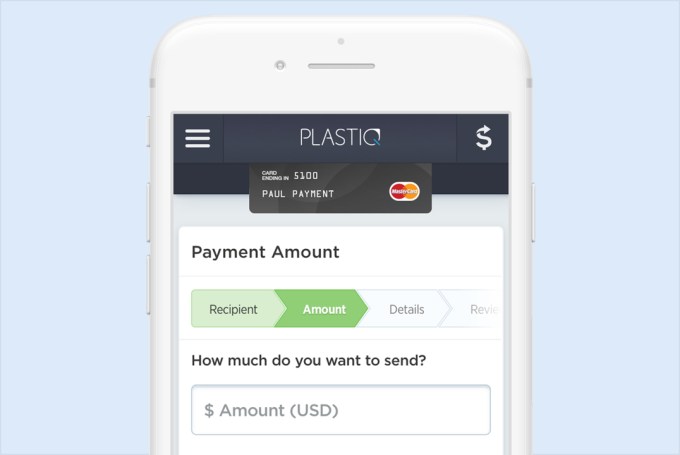

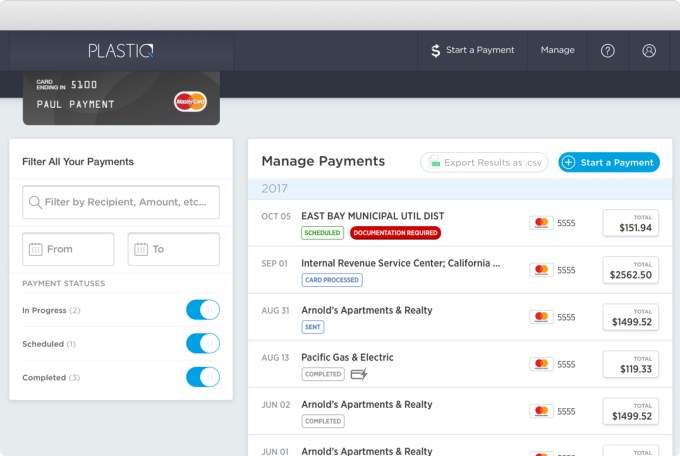

“I wasn’t asking to pay in Bitcoin!” Plastiq CEO and co-founder Eliot Buchanan recalls with a laugh. “I went to pay part of my tuition at Harvard and I was told that they didn’t (and never would) accept credit cards. It was inconvenient and seemed odd. Credit cards had been around for 50 years.” That set off the a light bulb in his head. “Why couldn’t I use a credit card to pay for this important bill? So, I set out to solve my own problem.”

Whether you’re trying to pay your rent or tuition on credit, or you have a business and want to invest in a new opportunity or get a better rate by paying vendors up front, Plastiq can help. For a flat 2.5 percent fee, you pay Plastiq through your credit card, and it issues the proper wire transfer, check or deposit for up to $500,000, or even more, on your behalf to whomever you owe.

Now with more than 1 million clients, growth-stage VCs are taking notice. Kleiner Perkins has just led a $27 million Series C for Plastiq with partner Ilya Fushman joining the board. A source says the raise that also comes from DST Global between doubles and triples Plastiq’s valuation over its 2017 Series B-1 rounds of $11 million and $16 million. Now with $73 million in total funding, it plans to add 100 people to its current team of 60, while building out its small business product and bank partnerships.

“As tens of thousands of business owners started using Plastiq actively for billions of dollars in payments, we realized we had this incredible opportunity to serve as the hub/platform on which they (SMBs) could run all their payments. The very fabric of America’s economy — and certainly much of the world — is run by rising or aspiring small business owners,” Buchanan tells me. He says that’s “the main reason that seeded this Kleiner financing and our renewed vision to ‘accelerate how small businesses grow.’ [Helping people pay with credit cards] is merely the entry point to a much broader play where we are central to how a small business runs.”

For example, if a small business wants to ramp up production of something it’s selling, it’d typically have to pay up front for manufacturing, but wait months until the stuff is shipped and sold to recoup its investment. That can put a major squeeze on the company’s operating capital. With Plastiq, the business can pay with credit up front so they don’t have to worry about being in danger of running out of money in the meantime. Plastiq also lets businesses accept credit card payments, which can win them favor with partners.

Plastiq co-founders (from left): Eliot Buchanan and Dan Choi

Specialty medical clinic chain Metro Vein pays vendors who don’t take credit with Plastiq instead. “I was able to invest in a new line of business that has enabled me to more than double our revenues in the last 10 months,” said CEO Dmitri Ivanov. And thanks to tax write-offs, business users of Plastiq can push its realized fee down to 2 percent.

Buchanan claims Plastiq doesn’t have any direct competitors that allow SMBs to pay for all their bills via credit. It does carry platform risk, though. “Like any payments business, we rely heavily on Visa, MasterCard and American Express. A challenge or risk factor is that you’re relying on very large companies that are very successful. You have to learn to work hand in hand with those partners instead of ‘disrupt them.’” He says Plastiq’s relationships with them are positive right now since it’s driving new revenue for them and helping their customers spend in new areas.

There’s also the risk that people misuse Plastiq to procrastinate on actually paying their personal bills or get in over their head investing in their business. But Plastiq’s new board member Fushman calls the service “this elegant way for businesses to tap into credit they’ve been issued but they haven’t been able to utilize before.” For many who are happy to pay though just need some time and flexibility, Plastiq can pitch in.

Powered by WPeMatico

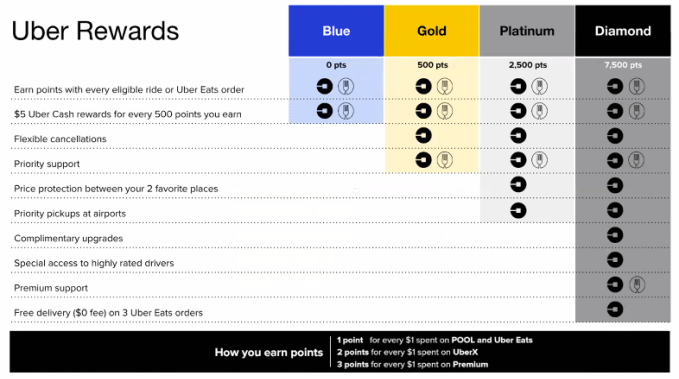

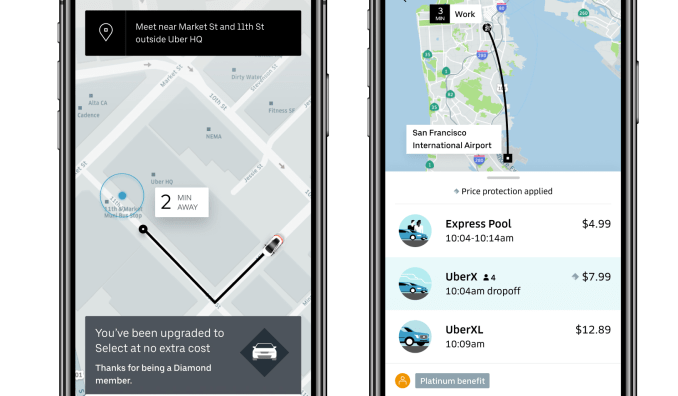

Uber’s new loyalty program incentivizes you not to check Lyft or the local competitor. Riders earn points for all the money they spend on Uber and Uber Eats that score them $5 credits, upgrades to nicer cars, access to premium support and even flexible cancellations that waive the fee if they rebook within 15 minutes.

Uber Rewards launches today in nine cities before rolling out to the whole U.S. in the next few months, with points for scooters and bikes coming soon. And as a brilliant way to get people excited about the program, it retroactively counts your last six months of Uber activity to give you perks as soon as you sign up for free for Uber Rewards. You’ll see the new Rewards bar on the homescreen of your app today if you’re in Miami, Denver, Tampa, New York, Washington, DC, Philadelphia, Atlanta, San Diego or anywhere in New Jersey, as Uber wanted to test with a representative sample of the U.S.

The loyalty program ties all of the company’s different transportation and food delivery options together, encouraging customers to stick with Uber across a suite of solutions instead of treating it as interchangeable with alternatives. “As people use Uber more and more in their everyday, we wanted to find a way to reward them for choosing Uber,” says Uber’s director of product for riders Nundu Janakiram. “International expansion is top of mind for us,” adds Holly Ormseth, Uber Rewards’ product manager.

As for the drivers, “They absolutely get paid their full rate,” Ormseth explains. “We understand that offering the benefits has a cost to Uber but we think of it as an investment,” says Janakiram.

So how much Ubering earns you what perks? Let’s break it down:

In Uber Rewards you earn points by spending money to reach different levels of benefits. Points are earned during six-month periods, and if you reach a level, you get its perks for the remainder of that period plus the whole next period. You earn 1 point per dollar spent on UberPool, Express Pool and Uber Eats; 2 points on UberX, Uber XL and Uber Select; and 3 points on Uber Black and Black SUV. You’ll see your Uber Rewards progress wheel at the bottom of the homescreen fill up over time.

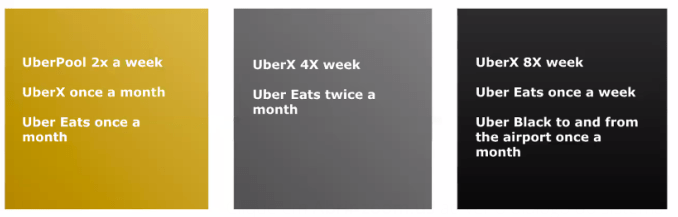

The only Uber perk that doesn’t reset at the end of a period is that you get $5 of Uber Cash for every 500 points earned regardless of membership level. “Even as a semi-frequent Uber Rewards member you’ll get these instant benefits,” Janakiram says. Blue lets you treat Uber like a video game where you’re trying to rack up points to earn an extra life. To earn 500 points, you’d need about 48 UberPool trips, 6 Uber Xs and 6 Uber Eats orders.

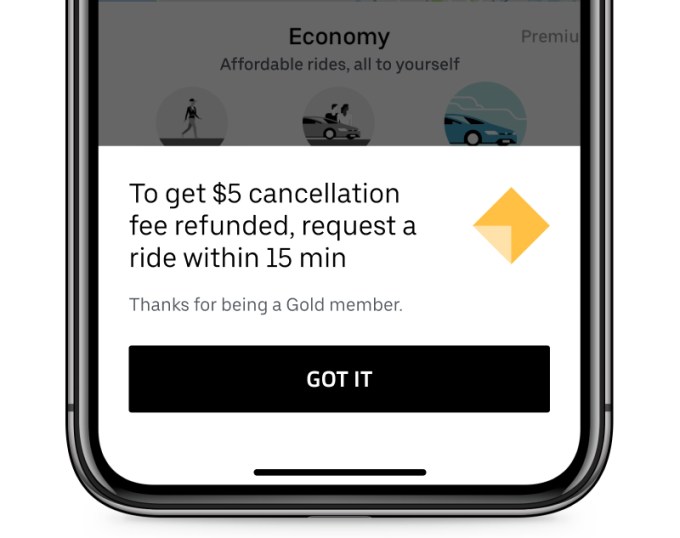

Once you hit 500 points, you join Uber Gold and get flexible cancellations that refund your $5 cancellation fee if you rebook within 15 minutes, plus priority support Gold is for users who occasionally take Uber but stick to its more economical options. “The Gold level is all about being there when things aren’t going exactly right,” Janakiram explains. To earn 500 points in six months, you’d need to take about 2 UberPools per week, one Uber X per month and one Uber Eats order per month.

At 2,500 points you join Uber Platinum, which gets you the Gold benefits plus price protection on a route between two of your favorite places regardless of traffic or surge. And Platinum members get priority pickups at airports. To earn 2,500 points, you’d need to take UberX 4 times per week and order Uber Eats twice per month. It’s designed for the frequent user who might rely on Uber to get to work or play.

At 7,500 points, you get the Gold and Platinum benefits plus premium support with a dedicated phone line and fast 24/7 responses from top customer service agents. You get complimentary upgrade surprises from UberX to Uber Black and other high-end cars. You’ll be paired with Uber’s highest-rated drivers. And you get no delivery fee on three Uber Eats orders every six months. Reaching 7,500 points would require UberX 8 times per week, Uber Eats once per week and Uber Black to the airport once per month. Diamond is meant usually for business travelers who get to expense their rides, or people who’d ditched car ownership for ridesharing.

Uber spent the better part of last year asking users through surveys and focus groups what they’d want in a loyalty program. It found that customers wanted to constantly earn rewards and make their dollar go further, but use the perks when they wanted. The point was to avoid situations where riders says, “Oh I’ve been an Uber user for years. When something goes wrong, I feel like I’m being treated like everyone else,” Janakiram tells me. When riders think they’re special, they stick around.

Uber spent the better part of last year asking users through surveys and focus groups what they’d want in a loyalty program. It found that customers wanted to constantly earn rewards and make their dollar go further, but use the perks when they wanted. The point was to avoid situations where riders says, “Oh I’ve been an Uber user for years. When something goes wrong, I feel like I’m being treated like everyone else,” Janakiram tells me. When riders think they’re special, they stick around.

One big missing feature here is a Rewards calculator. Uber could better gamify earning its perks if there was an easy way to see how many more monthly or total rides it would take to reach the next level. It’d be great to have a few little sliders you could drag around to see if I just take Uber X, how many of my average length trips would it take to level up.

Uber managed to beat Lyft to the loyalty game. Lyft just announced that its rewards program would roll out in December, allowing you to earn discounts and upgrades. But Southeast Asia’s Grab transportation service started testing a loyalty program back in late 2016 where you could manually redeem points for discounts. While Uber’s rewards are more predictable and automatic, it does seem to have cribbed Grab’s rewards period mechanic where you keep your perks through the end of the next cycle. We’ll see if Uber mistakenly gave too much away and will have to reduce the perks like Grab did, pissing off its most loyal riders.

One risk of the program is that Uber might make users at lower tiers or who don’t even qualify for Gold feel like second-class citizens of the app. “One thing that’s important is that we don’t want to make the experience for people who are not in these levels poor in any sense,” Janakiram notes. “It’s not like 80 percent of people will suddenly get priority airport pickups, but we do want to monitor very closely to make sure we’re not harming the service more broadly.”

Overall, Uber managed to pick perks that seem helpful without making me wonder why these features aren’t standard for everyone. Even if it takes a short-term margins hit, if Uber can dissuade people from ever looking beyond its app, the lifetime value of its customers should easily offset the kickbacks.

[Disclosure: Uber’s Janakiram and I briefly lived in the same three-bedroom apartment five years ago, though I’d already agreed to write about the redesign when I found out he was involved.]

Powered by WPeMatico

Zuora, the SaaS company helping organizations manage payments for subscription businesses, announced today that it had been selected as a Premier Partner in the Amazon Pay Global Partner Program.

The “Premier Partner” distinction means businesses using Zuora’s billing platform can now easily integrate Amazon’s digital payment system as an option during checkout or recurring payment processes.

The strategic rationale for Zuora is clear, as the partnership expands the company’s product offering to prospective and existing customers. The ability to support a wide array of payment methodologies is a key value proposition for subscription businesses that enables them to service a larger customer base and provide a more seamless customer experience.

It also doesn’t hurt to have a deep-pocketed ally like Amazon in a fairly early-stage industry. With omnipotent tech titans waging war over digital payment dominance, Amazon has reportedly doubled down on efforts to spread Amazon Pay usage, cutting into its own margins and offering incentives to retailers.

As adoption of Amazon Pay spreads, subscription businesses will be compelled to offer the service as an available payment option and Zuora should benefit from supporting early billing integration.

For Amazon Pay, teaming up with Zuora provides direct access to Zuora’s customer base, which caters to tens of millions of subscribers.

With Zuora minimizing the complexity of adding additional payment options, which can often disrupt an otherwise unobtrusive subscription purchase experience, the partnership with Zuora should help spur Amazon Pay adoption and reduce potential friction.

“By extending the trust and convenience of the Amazon experience to Zuora, merchants around the world can now streamline the subscription checkout experience for their customers,” said Vice President of Amazon Pay, Patrick Gauthier. “We are excited to be working with Zuora to accelerate the Amazon Pay integration process for their merchants and provide a fast, simple and secure payment solution that helps grow their business.”

The collaboration with Amazon Pay represents another milestone for Zuora, which completed its IPO in April of this year and is now looking to further differentiate its offering from competing in-house systems or large incumbents in the Enterprise Resource Planning (ERP) space, such as Oracle or SAP.

Going forward, Zuora hopes to play a central role in ushering a broader shift towards a subscription-based economy.

Tien Tzuo, founder and CEO of Zuora, told TechCrunch he wants the company to help businesses first realize they should be in the subscription economy and then provide them with the resources necessary to flourish within it.

“Our vision is the world subscribed.” said Tzuo. “We want to be the leading company that has the right technology platform to get companies to be successful in the subscription economy.”

The partnership will launch with publishers “The Seattle Times” and “The Telegraph”, with both now offering Amazon Pay as a payment method while running on the Zuora platform.

Powered by WPeMatico

Payments startup Stripe has changed the landscape for how businesses can collect funds online by using a few lines of code, and today the company is announcing that it’s picked up more funding of its own. Stripe has raised $245 million, valuing the company at $20 billion.

This is a big jump on its previous round, two years ago, that valued it at $9 billion.

Led by Tiger Global Management, other new backers included DST Global and Sequoia, along with existing investors Andreessen Horowitz, Kleiner Perkins, Khosla Ventures, General Catalyst and Thrive Capital.

The company says it plans to use the funding to hire more people for what it describes as its “distributed global engineering team.” It now has hubs in San Francisco, Seattle and Dublin (its co-founders, John and Patrick Collison, hail from Ireland), and it’s also going to launch a new hub in Singapore.

Engineering has been at the heart of the company’s growth from the start, up to now. Recall the famous essay by Paul Graham about Stripe that served as a mantra of sorts for how startups should grow. Fast forward to today, and Stripe boasts that “all told, the company deployed more than 3,200 new versions of its core API over the past year.”

The funding underscores the continuing strong climate for raising money from private backers at increasingly staggering valuations. VCs and private equity firms have raised billions, and they are looking for fast-growing, promising startups where they can invest that money. A number of startups are foregoing, or delaying, going public in favor of staying private for longer, financed by them.

“We have no plans to go public,” said John Collison in an interview. “We’re fortunate to be in the position that the Stripe business is performing very well and the long-term opportunity is that we’re very optimistic to providing the richer stack to businesses. Strong businesses do not always tend to be dependent on outside funding.”

(Not all are following this route: a key competitor of Stripe’s, Adyen, had a very strong IPO debut earlier this year.)

Stripe itself is a prime target for VCs looking to park their money in fast-growing, outsized startups. The company says it now has “millions” of customers, including Google, Didi, Mindbody, Spotify and Uber. It is live in 130 markets for acceptance and 25 countries for originating the charges.

Carving a place out for itself as a faster, easier way to integrate payments infrastructure into websites and apps, by way of a few lines of code, Stripe’s pitch is that it replaces the more laborious, and often more expensive route, of working with banks and other payment providers in a complicated chain of players that includes gateway providers, credit card processors, merchant acquirers, specialized payment methods, wallets and more.

And although Amazon is one of the world’s biggest companies, and most retailers have a digital presence, e-commerce is still a relatively nascent area, with only about three percent of all transactions occurring online at a global average. That means a big opportunity for companies like Stripe, but also competitors like Adyen, PayPal and others.

“We believe in the contingency of progress,” said Stripe CEO and co-founder Patrick Collison, in a statement. “Better global payments infrastructure will increase economic output, encourage entrepreneurship and help upstarts compete with incumbents. By bringing Stripe into more markets and building out our capabilities for companies of all sizes, we hope to accelerate innovation around the world.” Stripe estimates there will be $4 trillion in online sales by 2020 globally.

While payments is Stripe’s bread and butter, the company has also been diversifying and now also includes Stripe Issuing, Stripe Terminal, fraud detection and potentially cash advances, among its various offerings. These help the company develop stronger ties with its customers, and also potentially increase its margins.

“No one else is going as deep as us on software and the technology stack as we are,” said co-founder and president John Collison.

Powered by WPeMatico

Stripe is expanding beyond online payments with the launch of a new product for in-person payments at brick-and-mortar stores, called Terminal.

The company said Terminal has three main components — there’s hardware, namely card readers built by Stripe partners BBPOS and Verifone, but also SDKs and APIs for customizing checkout experiences, as well as software for managing connected devices.

Stripe’s co-founder and president John Collison discussed the launch at the Code Commerce conference today. Interviewer Jason Del Rey brought up Square, which seems like the obvious point of comparison, and Collison acknowledged there will probably be areas where the companies will compete.

However, he argued that Stripe and Square are largely targeting different customers — where Square built a card reader for businesses like coffee shops and restaurants, Stripe is aimed at more tech-savvy businesses. Its initial Terminal customers include Warby Parker and Glossier, and it’s also being used by software platforms like Mindbody, Zenoti, AtVenu and Universe.

As Collison put it, Stripe is built for companies “who will geek out about APIs with us.” And that applies to Terminal as well, which Collison said is specifically built for online businesses that are moving into brick-and-mortar stores. The goal here is to help them unify their online and offline customer data and experiences.

And while there’s been some debate about whether most web-based, direct-to-consumer businesses are true tech companies, he argued, “All of them value technology and fundamentally, their assets are not the retail distribution they have or anything like that.”

“We will happily work with all manner of companies, but the kinds of customers we get excited about, the kinds of customers we are designing for, are the ones who are moving very quickly,” he added.

Powered by WPeMatico

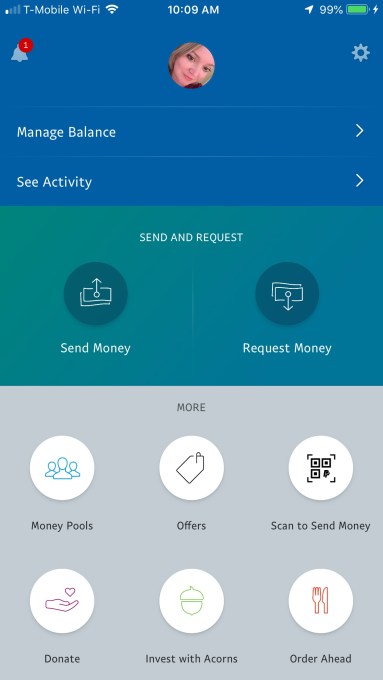

PayPal is revamping its mobile app. Again. In an effort to keep pace with newcomers like the bank-owned Zelle, PayPal says its new app will focus on making it easier to use its core features – that is, sending and requesting money. That means many of the app’s homescreen buttons – like Offers, Donate, Order Ahead and others are being tucked away underneath a new “More” menu to eliminate some of the clutter.

The PayPal homescreen had gotten a little too busy with all the extra features it has been promoting, which aren’t central to the PayPal experience. For example, it threw in a button suggesting “Invest with Acorns,” after taking a stake in the mobile investing app that rounds up purchases and automatically invests the extra change on your behalf. It has been pushing its Order Ahead functionality for years, even though no one thinks to launch a payments app when they’re hungry. Now these buttons no longer get top billing and valuable homescreen space.

Above: PayPal’s app today, before the update

However, even though PayPal is removing a lot of these extras from the homescreen, it’s not actually giving its “Send” and “Request” buttons more room. In fact, they’re getting a little less.

Today, those buttons are in the center of the homescreen, hosted in a big, greenish-blue banner. The updated app relocates them to a bottom bar.

However, it reverts the app’s color scheme to PayPal’s more familiar dark blue-and-white branding, so the relocated buttons are actually easier to see.

The homescreen instead dedicates most of its room to a new personalized notifications section.

Here, users will see alerts about money they’ve received or payment requests from others in big, blue cards you can swipe through horizontally. Below this, is a strip of profile icons and names of those you’ve recently paid – the theory being that PayPal is often used among the same set of family, friends or businesses. This makes it easier to make your next payment to one of your “regulars.”

Beneath this strip, your PayPal balance is displayed, while other notifications and settings are accessed through small buttons at the top of the screen, as before.

The overall design feels more in tune with PayPal’s brand than the last update. Though the prior big revamp, which was over two years ago, modernized things up a bit, it did so with too-light icons, small fonts and odd, off-brand color choices.

PayPal says the new app is rolling out now on Android to select markets, including Australia and Italy. It will then roll out to the U.S. and other markets worldwide, followed by a release on iOS.

Powered by WPeMatico