insurance

Auto Added by WPeMatico

Auto Added by WPeMatico

The coronavirus global health pandemic — and the new emphasis on social distancing to slow down the spread of COVID-19 — has put healthcare and tech services used to enable healthcare remotely under the spotlight. Today a startup that’s building microinsurance and healthcare services specifically targeting emerging markets is announcing a round of funding to meet a surge in demand for its services.

BIMA, a startup that provides life and health insurance policies, along with telemedicine to support the latter, all via a mobile-first platform targeting consumers in emerging markets whose primary entry point to online services is via phones, not computers, is today announcing that it has raised $30 million in funding, a growth round that the Stockholm/London-based startup plans to use to double down on its health services in the wake increased demand around COVID-19.

The company currently provides telemedicine as a service connected to its health insurance, and it has expanded to include health programs for managing illnesses and offering discounts for pharmacies, and the plan seems to be to bring more services into the mix.

This is the same approach we’re seeing from other insurance startups targeting emerging economies, including China’s Waterdrop, which recently raised $230 million. Looking at the network of services Waterdrop is building, including crowdfunding, gives you an idea of what else BIMA might potentially look to add in, too.

The round is being led by a new investor — China’s CreditEase Fintech Investment Fund (CEFIF) — with previous backers LeapFrog Investments and insurance giant Allianz (who were in BIMA’s previous, $97 million round) also participating.

The startup is not disclosing its valuation this time around, but in its previous round the company was valued at $300 million, and it has grown considerably since then.

BIMA has now clocked up 2 million tele-doctor consultations and has some 35 million insurance and health policies on its books, growing its customer base by some 11 million people in the last two years. It’s now active in 10 countries — Ghana, Tanzania and Senegal in Africa; and Bangladesh, Cambodia, Indonesia, Malaysia, Pakistan, Philippines and Sri Lanka across Asia.

At a time when we have seen a number of insure tech startups emerge in the US and Europe — with some, like Lemonade, growing into publicly-listed companies — BIMA is very notable in part because of who it targets.

It’s not higher economic brackets, or necessarily segments with disposable income, or those in developed markets with stable economies. Rather, its focus is, in its words, underserved families that typically live on less than $10 per day and are at high risk of illness or injury, with 75% of its customers accessing insurance services for the very first time, BIMA notes.

“Telemedicine and insurance are needed more than ever and COVID accelerated awareness and acceptance for these types of products amongst emerging consumers and government. They’ve gone from ‘nice to have’ to a necessity,” said Mathilda Strom, who co-founded the company with CEO Gustaf Agartson, in an interview. “Utilisation nearly doubled in our telemedicine services.” BIMA covers COVID and pandemics in general in its policies, she added. “We have paid out COVID-related claims to families of people who suffered or passed away from the illness.”

It’s also working with health authorities that have been overwhelmed in the pandemic. Pakistani government and Indonesian government now use BIMA to off-load their health services by providing teledoctor consultations or doctors chats to customers.

Aiming at developing economies where middle classes are still only materialising, currencies are potentially unstable, and there is still a lack of infrastructure means that BIMA is contending with a combination of factors that makes the bar high for entry, but it’s also potentially more rewarding because of the lack of competition and tapping a demand that is still rapidly growing.

“The onset of COVID-19 has brought home the value of telemedicine, to help prevent the spread of disease, and the importance of insurance, for peace of mind,” said Agartson in a statement.

“Through digital solutions, and a human touch, we’ve been able to serve hard to reach communities with tools and services that bring them a sense of security at such a challenging time. The funds we have raised will allow us to expand our operations and further invest in our product offering that will help us scale quickly to meet the unprecedented demand for our services.”

It’s interesting to see CreditEase, a Chinese investor, as part of this round: the idea of all-in, full service health services companies banked around the insurance proposition has been one cultivated in the Chinese market. But even with the development of HMOs in the US, it’s interesting that there have been relatively few startups around the world trying to develop similar models. BIMA stands out in part because of that.

“We are very impressed by BIMA’s innovative integration of micro insurance and tele-doctor services, which provide critical coverage to meet large unmet demand in emerging markets, and whose value is accentuated further by the current pandemic,” said Dennis Cong, managing partner at CEFIF, in a statement. “We are very happy to have the opportunity to join this meaningful journey, along with the established leading shareholders, and support the company to grow its business and expand its leadership position in its served markets.”

“The market that BIMA is serving is vast and demand for health services is tremendous,” added Stewart Langdon, a partner at LeapFrog Investments. “BIMA’s unique digital capabilities empower emerging market consumers to access many health and insurance services on a single, easy to use platform. That includes protection for millions of first-time buyers of insurance who would otherwise remain unprotected and at risk.”

“We are happy to continue our partnership with BIMA and jointly deliver telemedicine and remote healthcare services in developing markets,” said Nazim Cetin, CEO at Allianz X, in a statement. “We believe the demand for these services will continue to increase and want to manifest BIMA’s leading position in the market by providing support with our experience and network.”

Powered by WPeMatico

As the COVID-19 epidemic spread across the U.S. earlier this year, Nurx, like most other digital providers of healthcare and prescription services, saw a huge spike in demand.

Now, with $22.5 million in new financing and a surging annual run rate that could see the company hit $150 million in revenue, the company is emerging as the largest digital practice for women’s health.

“We saw this tremendous surge in need for our contraception and sensitive health services,” says Nurx chief executive Varsha Rao .

The growth hasn’t come without controversy. Only last year, a New York Times article pointed to corner cutting at the startup, which boasts Chelsea Clinton as an investor and advisor.

Undeterred, Rao said the company has now seen tremendous acceleration in all areas of its business. It’s now providing care to more than 300,000 patients on a monthly basis, boasts that $150 million run rate and has new investors like Comcast Ventures, Trustbridge and Wittington Ventures — the investment arm of one of the largest pharmacy chains in Canada, Shoppers Drug Mart.

The new $22.5 million is an extension on the company’s previous $32 million round and will take the company to profitability by 2021, according to Rao.

And while birth control and contraception are still the largest areas of the company’s business, Nurx is growing its range of services, seeing adoption of its testing for sexually transmitted infections including HPV and herpes and a new treatment area for migraines.

That focus on sexual health and what the company calls sensitive health is different from trying to be a primary care provider, says Rao. “Our real focus right now is on our core demographic who are women between the ages of 20 and 40 and really focusing on their needs,” she says. “That’s why migraines make a lot of sense. It’s not exclusively hormone-related, but it often is… One-in-four women experience migraines and they’re largely from hormonal changes… This is a condition we’re well-positioned to address.”

Another way that Nurx differentiates itself from competitors like Hims and Ro, which provide women’s health and contraceptive prescriptions as well, is through its ability to take insurance. “It’s actually pretty challenging to build the system to actually offer insurance,” says Rao. “And yet, we don’t think you can be a true healthcare company if you don’t accept insurance.”

Powered by WPeMatico

Although the 2008 global financial crisis sparked the fintech movement, in Latin America, the rise of ecommerce was responsible for the first wave of fintech startups.

Because digital payments were key to enabling the growth of ecommerce, investors funded companies like Braspag, PagSeguro, PayU, Mercado Pago and Moip in the early 2000s to take advantage of this opportunity.

Payment is still the most relevant segment, with successful cases like Stone and PagSeguro, but after the financial crisis, we started to see the rise of financial technology in lending and neobanking, generating impressive cases like Nubank, Neon, Creditas, Credijusto and Ualá.

As the ecosystem evolves and expands, let’s take a closer look at emerging trends in Latin America that might give us a hint about where to expect its next fintech unicorns.

Latin America has seen explosive growth in ride-hailing and food delivery platforms such as Uber, Didi, Rappi and iFood, creating a totally new market opportunity — many gig economy workers can’t access basic financial services such as bank accounts, personal loans and insurance. Even those who have access often struggle with financial products that that don’t suit their needs because they were designed for full-time workers.

Spotting this opportunity, Uber Money launched at Money 2020, focusing on providing drivers with financial services. As 50% of the population in Latin America is unbanked where Uber has more than 1 million drivers, the region is definitely a ripe market. Cabify is going even farther by spinning off Lana, its company that provides financial services, so it can expand its market beyond Cabify drivers to include other gig economy professionals.

Although established players in this sector have a clear advantage, they aren’t the only ones looking to explore this opportunity; Brazilian YC alumni Zippi is offering personal loans to ride-hailing drivers based on their driving earnings. As the gig economy tends to keep growing in the region, I believe we will start to see more solutions for those professionals.

As the banking world has been shaken by fintechs, insurance companies are growing aware that high regulatory barriers won’t protect their industry from disruption.

Insurance penetration in Latin America has been historically low compared to developed markets — 3.1%, compared to 8% — but the insurance market is growing well and tends to close this gap. Adding this to bad services and complex products that insurances provide, insurtech has an immense opportunity to grow.

Because purchasing insurance is historically a complicated and painful experience, the first insurtechs in the region focused on providing a better experience by digitizing the process and using online channels to acquire customers. Those insurtechs worked together with the insurance companies and operating as online broker, but now, we’re starting to see startups providing new insurance products, as well as traditional insurances in different models.

Some are partnering with insurance companies while others are competing directly with them; Think Seg and Miituo partnered with larger players to provide a pay-as-you-go model for car insurance, while Mango Life and Kakau are offering a better purchasing experience. On the other end, Crabi and Pier are rethinking the insurance model from the ground up.

As insurtechs emerge as a potential threat, incumbents are more willing to work with startups that can improve their services to enable them to compete on better grounds, which is exactly what companies such as Bdeo, Lisa, and HelloZum are doing.

Although penetrating the insurance industry is more complicated than other financial services due to high regulatory demands and steep initial operating costs, insurtechs fueled by VC investment will without any doubt try to do it. And, if we’ve learned anything from other fintech segments, it’s that entrepreneurs will find ways to overcome initial challenges.

Powered by WPeMatico

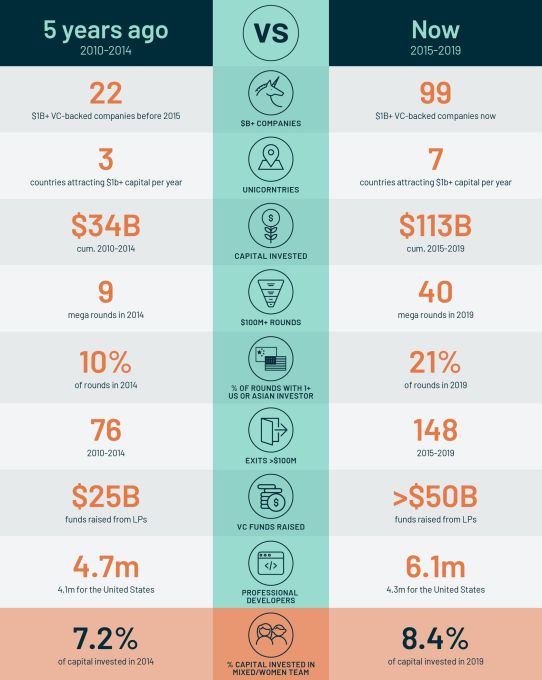

Atomico, the European venture capital firm founded by Skype’s Niklas Zennström, has released its latest annual The State of European Tech report, published in partnership with Slush and Orrick.

As part of the report, the authors surveyed 5,000 members of the ecosystem — including 1,000 founders — as well as pulling in robust data from other sources, such as Dealroom and the London Stock Exchange .

This year, the report reveals that the European tech ecosystem continues to mature and shows no sign of slowing — particularly highlighting the contrast from five years ago when the The State of European Tech report made its debut. Almost every key indicator is up and to the right, except, rather depressingly, diversity.

The data shows, for example, that competition for talent and access to the best founders has increased ferociously. And from a funding perspective, European founders have more choice than ever, especially with U.S. and Asian VC firms investing more and more in the region. Progress with gender diversity stalled, however, such as 92% of funding going to all-male teams.

I caught up with the report’s author Tom Wehmeier, Partner and Head of Insights at Atomico (also sometimes jokingly referred to as the “Mary Meeker of Europe”), where we discuss in more detail some of the key findings and why, it seems, that the rest of the world has finally woken up to Europe’s tech potential.

But first, a few headlines from the report:

Extra Crunch: It is 5 years since Atomico published the first The State of European Tech report, which really attempted to capture a data-driven snapshot of the entire ecosystem. What are some of the biggest changes you’ve seen within European tech in the intertwining years or in this year in particular?

Tom Wehmeier: If I think back to when we did the first report, people who believe that Europe could actually be an interesting player in global technology, were largely limited to people who were in the tech industry in Europe itself. If you then fast forward to today, what has clearly happened — and I think 2019 was the year where this really materialized and became part of the narrative — was that belief translating from people on the inside to a bunch of people that were on the outside.

Most obviously has been the strength of interest from from the U.S. and the number of top-tier U.S. funds that are not just increasing their level of investment activity but committing to spending more and more time here on the ground, hiring people, building teams, building a network, and getting to know companies. I think it probably surprises people to know that 19% of all rounds this year will involve at least one U.S. investor in Europe, which is more than double since since the first year we did the report.

I think the other thing, where I come back to this idea that now we have finally convinced a certain group of people about the role that Europe can play, is mainstream institutional investors. I know it is not going to be lost on you, [but] this is going to be another record year for VC fund raising from Europe. And whilst the headline numbers might not be a surprise, I think what should catch people’s attention is that the composition of the LP base here in Europe is now shifting. And finally, there’s an unlocking of institutional investors, [by which] I mean pension funds, funds of funds, insurance companies, sovereign wealth funds, who are committing to European VC at levels that are significantly increased and elevated from where they had been in the past. So, if you just take pension funds, we’re going to see close to a billion dollars invested which is up nearly three fold.

It’s a validation of what’s happening around European tech to see that now coming through and I think is ultimately something that helps to build a foundation for the next five years of success. As much as this is a report that’s looking back, it’s also about trying to understand where things go from here.

With regards to the pension funds, do you think that is driven by the general bullishness towards European tech, or do you think it’s more the macro economic reality that maybe other places where they could put their money aren’t very attractive at the moment?

I think it’s really a reflection that there’s a strong level of belief that European venture as an asset class is an attractive investment opportunity. And that is reflected by the numbers. One of the charts that we’ve got in the report is from Cambridge Associates who do the benchmarking for the VC indices… And when you look back over a 1, 3, 5, or even a 10 year horizon, the performance from European VC is demonstrating that this is a place where for anyone building a diversified portfolio, they should have some allocation. I think it’s fundamentally the strength of the investment opportunity. That is the single biggest driver for why you’re seeing this happen.

I think the biggest thing that Europe has been able to prove is that it can take a great idea and turn it into a great company and that company can scale to not just a billion dollar outcome but to a multi-billion dollar outcome and go all the way through into an IPO or into a large scale acquisition. What you’ve seen happen in 2019 is in part A reflection of what happened last year where it was obviously this record year with Spotify, Adyen, Farfetch, Elastic and others that really showed you can go full cycle from start all the way to finish. And that the magnitude of those outcomes can be at a scale that makes them globally relevant.

Are the pension funds shifting their allocation of VC away from other geographies or are they just doing more VC as a whole?

Powered by WPeMatico

French startup Luko has raised a $22 million Series A round led by Accel (€20 million). Founders Fund and Speedinvest are also participating in today’s funding round.

When you rent a place in France, you have to provide a certificate to your landlord saying that you are covered with a home insurance product. And, of course, you might want to insure your place if you own it.

While the market is huge, legacy insurance companies still dominate it. That’s why Luko wants to shake things up in three different ways.

First, it’s hard to sign up to home insurance in France. It usually involves a lot of emails, a printer, some signatures, etc. It can quickly add up if you want to change your coverage level or add some options.

As expected, Luko’s signup process is pretty straightforward. You fill out a form on the company’s website and you get an insurance certificate minutes later.

Luko partners with La Parisienne Assurances to issue insurance contracts. So far, 15,000 people have signed up to Luko.

Second, if there’s some water damage or a fire, it can take a lot of time to get it fixed. Worse, if somebody breaks into your place, you’re not going to get your money back that quickly.

Luko wants to speed things up. You can make a claim via chat, over the phone or with a video call using the mobile app. The company tries its best to detect fraud and pay a claim as quickly as possible. Luko also recently announced an integration with Lydia, a popular peer-to-peer payment app in France, so that your payment is instant.

Third, Luko has a bold vision to make home insurance even more effective. The startup wants to detect issues before it’s too late. For instance, you could imagine receiving a water meter from Luko to detect leaks, or a door sensor to detect when somebody is trying to get in. We’ll find out if people actually want to put connected objects everywhere.

Finally, Luko has partnered with a handful of nonprofits to redistribute some of its revenue — it has received the BCorp certification. The startup makes revenue by taking a flat fee on your monthly subscription. If there’s money left at the end of the year, Luko donates it to charities. Investors signed a pledge so that Luko doesn’t trade this model for growth.

Powered by WPeMatico

In 2017, when a destructive earthquake struck Puebla, Mexico, sending shock waves to Mexico City and destroying buildings in the nation’s megalopolis and its surrounding suburbs, both public and private emergency services sprung into action.

For multinational corporations operating in the city it was a test of their internal support services, which were established to meet the “duty of care” requirements that multinationals have to their foreign employees. That’s a minimum threshold which companies must meet to ensure the safety of their employees.

After the Mexico City earthquake, at least one Fortune 500 insurance company found its services lacking. It took two weeks for the company to contact all of its employees and account for everyone.

So the company turned to a new Washington-based startup called Base Operations to see if they could do a better job.

Founded by a former security and risk management consultant, Cory Siskind, Base Operations uses a suite of hosted software services and mobile applications to provide security updates to corporate customers and their employees.

The insurance company tested Base Operations’ check-in feature to see how it would perform in a simulated natural disaster and Siskind said that Base Operations had identified the location of 80% of the company’s workforce in less than two days. More than half of the company’s employees checked in within the first 24 hours.

Base Operations offers a dashboard for corporate customers to monitor their employees’ locations and for staff traveling abroad, the company has an app that provides geo-tagged alerts on potential risks based on an individual’s location.

“This is a compliance situation for companies… They have to do it,” says Siskind. “We work with a company’s chief security officers and travel security. If you send people off into an emerging market with a risk PDF… It’s not dynamic information and it just sits in a report and nobody reads it.”

Companies with a sales or marketing team traveling around need to have some sort of tool to meet their compliance regulations and duty of care standards, says Siskind.

“We have a whole set of features that nudge towards safer behaviors so that you don’t end up getting mugged and so that you don’t end up in a situation that would be damaging to you,” she says.

Siskind recently raised $1 million for Base Operations from investors including Glasswing Ventures, Spiro Ventures, the Latin American early-stage investment firm Magma Partners and Good Growth Capital. Base Operations graduated from Techstars Impact Accelerator in 2018.

The money from the company’s most recent round will be used to expand the company’s sales and marketing efforts and continue its research and development.

So far, the company has three customers, including the undisclosed insurance provider, the energy company Enel and another, yet unnamed, corporation.

Base Operations provides its services in 15 cities, including: Mexico City, São Paulo, Rio de Janeiro, Buenos Aires, Santiago, San Juan (Puerto Rico) and San Jose (Costa Rica).

Powered by WPeMatico

Thimble, which offers flexible, short-term insurance to small businesses and freelancers, is announcing that it has raised $22 million in a Series A funding round led by IAC.

Until today, the startup was known as Verifly, a name tied to the company’s initial aim of providing insurance to drone pilots. However, founder and CEO Jay Bregman (who previously founded ridesharing company Hailo) said that thanks to customer demand, the team kept adding insurance for different types of businesses — and now it’s rebranding to reflect that broader vision.

While it’s easy to talk about Thimble customers as being part of the “gig economy,” Bregman noted that these aren’t just people driving for Uber or delivering for Postmates — only 4% of the company’s customers identify as gig economy workers.

“There is this larger thing called the gig economy: People working in flexible ways, on their own terms,” he said.

In fact, Thimble now says it provides liability coverage for customers in more than 100 professions, including handymen, landscapers, DJs, musicians, beauticians and dog walkers. Policies can be purchased directly from the Thimble website or app by the hour, day, week, month or year.

The idea, Bregman said, is that as work becomes shorter term and “more transactional,” it doesn’t make sense to buy an annual insurance policy. To illustrate that point, he noted that 75% of customers didn’t have insurance before buying from Thimble, and that 50% of customers are buying policies to cover a single day or less. And the company says it’s on track to sell 100,000 by the end of the year.

Thimble’s policies are underwritten by Markel, an insurance company that Bregman praised for its “infrastructure and talent.”

At the same time, he said, “We have always been the owner of the product itself. Basically, we worked with carrier partners to bring [our products] to market; the way we do that may evolve slightly as we get older and more mature.”

Thimble has received regulatory approval to sell insurance in 48 states so far. Asked whether the broader political debates about whether gig workers are employees could affect the company’s business, Bregman pointed again to the fact that the vast majority of Thimble customers don’t consider themselves gig workers.

“Our only fear here is that in trying to solve a very particular problem with long-term gig employment, that some of these laws may actually unintentionally scare off or capture legitimate freelancers,” he said.

As for the investment, IAC’s chief strategy officer Mark Stein acknowledged that the digital media holding company doesn’t make many early-stage, minority investments. But he said that deals like this are about “planting seeds.”

“What we think about at IAC is: How can we go about planting seeds of growth for the future? What will become the next ANGI Homeservices? What will become the next Match Group?” Stein said, alluding to two IAC-owned businesses that may get spun off. “We need to find these kinds of large, addressable market opportunities now in the hopes of creating very large, industry-changing companies in the future.”

Previous investors Slow Ventures, AXA Venture Partners and Open Ocean also participated in the round, bringing Thimble’s total funding to $29 million.

Powered by WPeMatico

Next Insurance, a three-year-old U.S.-based firm that sells insurance products to small businesses, has become the latest unicorn in the nation after bagging $250 million in a new financing round, the startup said today.

Germany-based Munich Re, one of the world’s largest reinsurers, alone funded Next Insurance’s Series C round, the two said in a statement. The new financing round valued the three-year-old startup, which has raised $381 million to date, at more than $1 billion, the startup said.

Guy Goldstein, co-founder and chief executive of Next Insurance, said the startup will use the fresh capital to build new products and expand its customer initiatives. Next Insurance offers a wide-range of insurance coverage to more than 1,000 unique types of business. It has amassed over 70,000 customers in the U.S., the only market where it currently operates.

Next Insurance aims to become a one-stop insurance shop for micro and small business insurance needs. Its insurance plans and products are designed to cater to the business sectors that are often overlooked by more general insurers.

The startup offers a number of insurance products, including general liability, which covers a number of accidents at work, including property damage and physical injury; professional liability, which covers business owners from accusations of professional mistakes; and commercial auto, which pays for damage caused by or to your business vehicle.

As TechCrunch’s Steve O’Hear explained earlier, small business owners often rely on price comparison websites to figure out what kind of coverage they need and where to buy it, though that means the plans they get don’t always cover all their needs. The other option is to use a broker, but that also adds another middle person.

In a statement, Joachim Wenning, chairman of the Board of Management at Munich Re, said the new investment will help Munich Re expand its footprint in the U.S.’s insurance market of small and medium-sized commercial customers.

“Next Insurance will benefit from our expertise in primary insurance and reinsurance. This investment emphasizes Munich Re’s commitment to be the leading provider of digital insurance solutions,” added Wenning.

Next Insurance, of course, isn’t the only player attempting to address the insurance needs of small and micro-sized businesses. It competes with a handful of startups, including Lemonade, which raised $300 million in April this year, and Root Insurance, which sells car insurance and raised $100 million last year.

Powered by WPeMatico

DeadHappy, a U.K.-based insurtech startup that wants to offer more flexible life insurance and remove the taboo surrounding death, has raised £4 million in Series A funding. Backing comes from e.ventures, alongside the company’s seed investor Octopus Ventures.

Founded in 2017, DeadHappy claims to be the U.K.’s “first fully digital pay-as-you-go life insurance provider.” It offers flexible life insurance policies that are designed to be “cheaper, easier and better” than existing traditional providers. This includes pricing insurance based on your current circumstances and the option to add (or remove) further coverage on a rolling basis.

More broadly, the startup is developing what it calls its “Deathwish” platform, which is something akin to a will. The idea is that you can specify how you wish any future insurance payout to be used, such as paying off your mortgage. And there are also plans to incorporate other wishes not related to finances.

“Our vision is to change attitudes to death and we are tackling that in a number of ways,” DeadHappy co-founder Phil Zeidler tells me. “Despite death being the one certainty humans face, it remains for many a taboo subject, and the failure to talk about it and plan for it is both counterintuitive and leads to significant further trauma at the most difficult of times for family and loved ones.”

Currently the Deathwish platform offers financially motivated Deathwishes, but the longer-term plan is to enable practical Deathwishes, such as making sure your funeral is the way you want it, and what Zeidler calls emotionally motivated Deathwishes.

The idea is to help offer a way to help loved ones “achieve something meaningful in their lives, whether that’s learning how to play the drums or funding an expedition to the Amazon,” he explains.

“Crucially, customers can share these Deathwishes as they choose, which is a practical tool to ensure their wishes are clear and understood. Our platform acts as a catalyst for opening a conversation with loved ones and a place to share recorded video messages and stories.”

Meanwhile, DeadHappy says it will use the new funding for future growth by further building the technology and capabilities of its Deathwish platform. It also plans to expand its product and partnership offerings to major financial service distributors.

Powered by WPeMatico

Critical cyber attacks on both businesses and individuals have been grabbing headlines at an alarming rate. Cybersecurity has moved from a background risk for enterprises to a critical day-to-day threat to business operations, forcing executive teams to pour time and hundreds of billions in capital into monitoring and prevention efforts.

Yet even as investment in security ticks up, the frequency and cost of cybercrime to businesses continues to rapidly accelerate, with the World Economic Forum estimating the economic loss due to cybercrime could reach $3 trillion by 2020.

More companies are now turning to cyber insurance as a means of mitigating financial exposure. However, for traditional insurers, cybersecurity remains a relatively nascent and unfamiliar issue, requiring risk-assessment data points and methodologies largely different from those seen in traditional insurance products. As a result, businesses often struggle to get the scale of cybersecurity coverage they require.

Arceo.ai is hoping to expand the size and scope of the cyber insurance market for both insurers and companies, by providing insurers with effective real-time data, analytics and context, necessary for safely and efficiently underwrite cyber risk.

This morning, Arceo took a major step in achieving that goal, announcing the company has raised a $37 million round of funding led by Lightspeed Venture Partners and Founders Fund with participation from CRV and UL Ventures.

![]() Using an expansive set of global sources across a customer’s digital footprint, Arceo.AI collects internal, external and macro cyber risk data which it uses to evaluate a company’s security and cyber risk management behavior. By automating the data collection process and connecting it with insurer underwriting processes, Arceo is able to keep its data and policy assessments up to date in real-time and enable faster, more efficient quotes.

Using an expansive set of global sources across a customer’s digital footprint, Arceo.AI collects internal, external and macro cyber risk data which it uses to evaluate a company’s security and cyber risk management behavior. By automating the data collection process and connecting it with insurer underwriting processes, Arceo is able to keep its data and policy assessments up to date in real-time and enable faster, more efficient quotes.

A vital component of Arceo’s platform is its analytics offering. Using patented data science and cyber risk models, Arceo generates analytics-driven insights for insurance carriers, brokers and end-insured customers. For end-insured customers, Arceo helps companies understand whether they’re using the best mitigation strategies by providing policy recommendations and industry benchmarking to help contextualize day-to-day cyber behavior and hygiene. For underwriters, Arceo can provide specific insurance recommendations based on particular policy coverages.

Ultimately, Arceo looks to provide both insurers and the insured with actionable answers to key questions such as how one assesses cyber risk, how one determines what risks can be mitigated with technology alone, how one knows which systems are best and whether those systems are being used appropriately.

Arceo.ai Chairman Raj Shah. Image via Arceo.ai

In an interview with TechCrunch, Arceo Chairman Raj Shah explained that the company’s background expertise, proprietary data systems, and deep pedigree in both the security and insurance truly differentiate Arceo from competing solutions. For starters, both Shah and Arceo co-founder and CEO Vishaal Hariprasad have spent close to the entirety of their careers in national security and cybersecurity. Hariprasad started his career in the Airforce’s first cohort of cyber warfare officers, before teaming up with Shah to start Morta Security in 2012, a security startup the two sold to Palo Alto networks in just roughly two years.

After selling the company, Shah and Hariprasad remained in the security world before realizing that there was a natural intersection between security and insurance, and a real opportunity for risk transfer solutions.

“Having studied the market, we saw that people are spending more and more dollars on cybersecurity products… There are hundreds of thousands of new vendors every year… Spend is going up, but we don’t feel any safer!” Shah told TechCrunch.

“That’s when we said ‘Hey, we need to move beyond just thinking about technology points and products, and think about holistic cyber risk management.’ And this is where insurance has historically done a great job. Putting a price on behavior and making people think and letting them take risks… From life and death and health to buyers and property and casualty. And so cyber is that next class risk… So that’s really why we started the business. We wanted to provide a real way to manage the cyber stress that they’re facing and that will impact every single one of our digital lives.”

Since the company’s founding, Raj and Vishaal have been joined by a deep network of cyber and insurance experts. Today, Arceo also announced that Hemant Shah, founder and former CEO of catastrophe risk modeling company RMS has joined Arceo’s Board of Directors. Additionally, earlier this month, the company announced that Mario Vitale, the former CEO of publically-traded insurance companies Willis Towers Watson and Zurich Insurance Group, would be joining the Arceo team as the company’s President.

The company noted that participation from high-profile industry vets like Hemant and Mario not only further advance Arceo’s competitive advantage but also acts as another major validation of the company’s future and work to date.

According to Arceo Chairman Raj Shah, after years of investing in R&D, the latest funds will be used towards expansion efforts and scaling Arceo to the broader ecosystem of insurance and brokers. Longer-term, the company hopes to offer the most complete combined cybersecurity and risk transfer solution to insurers and the insured, easing the stress around cyber threats for both enterprises and individuals and ultimately improving broader cyber resiliency.

If you’d like to hear more from Arceo’s Raj Shah, Raj will also be joining us this year on the Extra Crunch stage at TechCrunch Disrupt SF, where he’ll discuss how founders and companies should think about potential US government investment. Grab tickets here and we hope to see you there!

Powered by WPeMatico