insurance

Auto Added by WPeMatico

Auto Added by WPeMatico

Eargo wants to become the ultimate consumer hearing brand.

The company’s small and virtually invisible direct-to-consumer hearing aids, which come in an AirPods-style chargeable case, are designed to help destigmatize hearing loss. One month after revealing its newest product — the Eargo Neo ($2,550), which can be customized remotely via the case’s Bluetooth connectivity — the startup has closed a $52 million Series D, bringing its total raised to date to $135 million.

The latest round of capital comes from new investor Future Fund (Australia’s sovereign wealth fund) and existing investors NEA, the Charles and Helen Schwab Foundation, Nan Fung Life Sciences and Maveron.

Headquartered in San Jose, Eargo, which counts 20,000 users, will use the cash to continuing crafting and innovating new products targeting baby boomers. The newly launched Eargo Neo is the business’s third line of high-tech hearing aids. The first, Eargo Plus ($1,450), was released in 2017 and the Eargo Max ($2,150) was launched the following year.

“We can see that the product is really making a difference for users,” Eargo chief executive officer Christian Gormsen told TechCrunch. “We have the opportunity to really create a leading brand in the consumer hearing health space.”

Roughly 48 million Americans, or 20 percent of the population, suffer from hearing loss, but, aside from some Medicare Advantage programs, insurance companies provide no reimbursement for hearing aids. Despite high price tags — this is expensive tech — Eargo’s priority is still to make its hearing aids as accessible as possible and to send a message that there’s nothing wrong with admitting to hearing loss.

“Getting a hearing aid feels like admitting a defeat, like there’s something wrong with you, but that’s not true, hearing loss is natural and happens,” Gormsen said. “The number one challenge for the entire industry is awareness. There is so little knowledge about hearing loss out there; it’s such a stigmatized category and how do you change that? The current channel doesn’t do anything to address it, the only way you can address it is through education and communication.”

“I think we’ve come far, but we are looking at 48 million Americans and we are still barely scratching the surface.”

Powered by WPeMatico

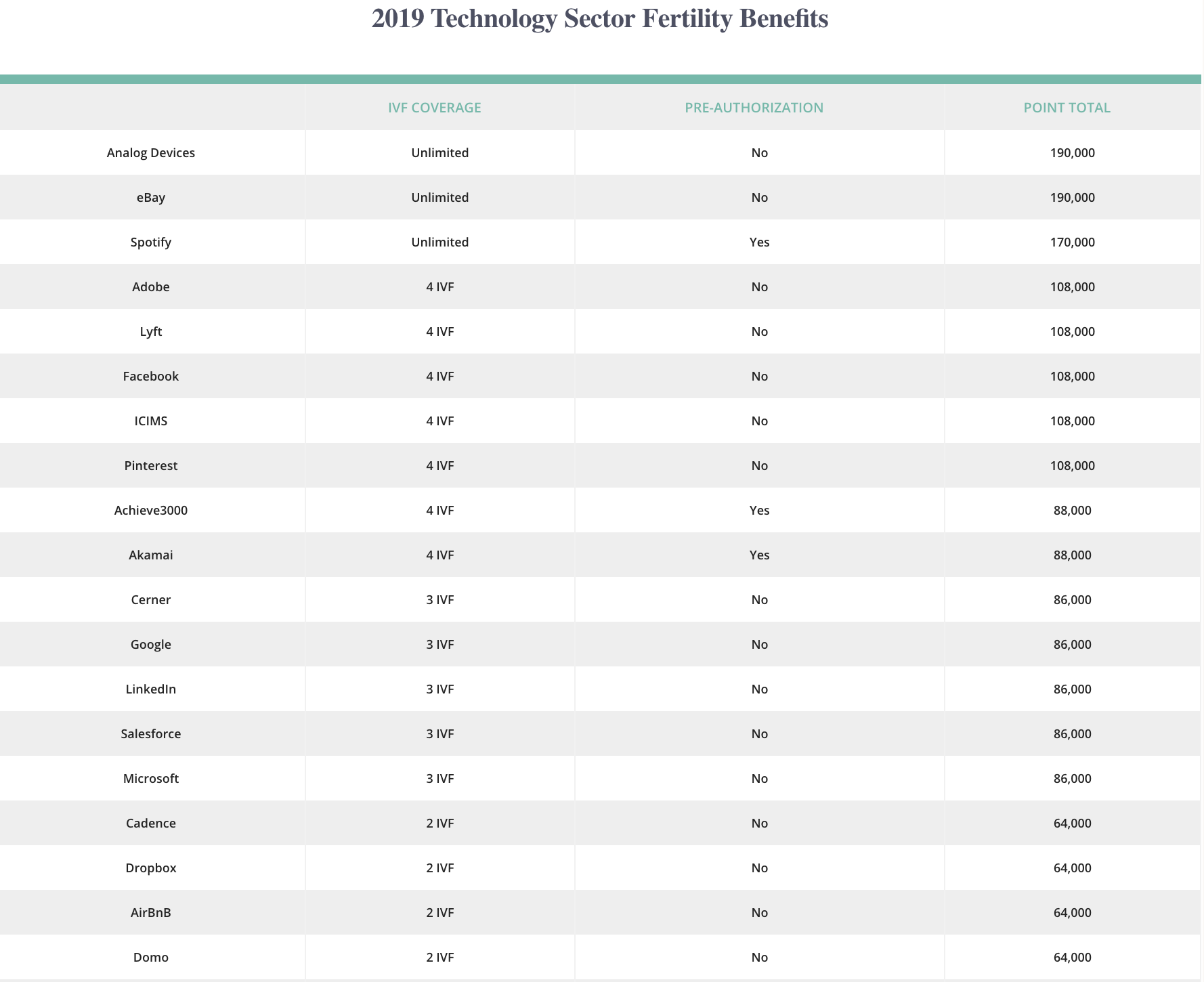

The technology sector awards women and same-sex couples the most comprehensive fertility benefit packages, according to a survey by FertilityIQ, an online platform for fertility patients to review doctors and research treatments.

The company asked 30,000 in vitro fertilisation (IVF) patients across industries about their employers’ — or their spouse’s employer’s’ — 2019 fertility treatment policy, and allocated points based on their support for IVF procedures and egg freezing, among other services.

Silicon Valley semiconductor business Analog Devices and eBay led the ranking. The two companies offer employees unlimited IVF cycles with no pre-authorization requirement, meaning employees do not need permission from insurance providers before seeking certain medical services. Pre-authorization has historically impacted lesbian, gay or unpartnered employees from accessing care quickly or at all, FertilityIQ co-founder Jake Anderson explained

Spotify, Adobe, Lyft, Facebook and Pinterest were amongst the highest-ranked technology businesses, too.

“I think a lot of people see the tech sector as being unenlightened when it comes to family values but it’s still the sector that makes the fertility benefits the most widely acceptable,” Anderson, a former consumer internet investor at Sequoia Capital, told TechCrunch.

FertilityIQ’s fertility benefits survey results.

Despite an initial outpouring of skepticism, Facebook and Apple became leaders in the fertility benefit category when they began paying for their female employees to freeze their eggs in 2014. Since then, smaller firms have opted to beef up those benefits to stay competitive with their much larger and richer counterparts.

“The Lyfts, the Airbnbs and the Ubers of the world, who clearly need to compete for those companies for talent, have effectively matched those companies dollar-for-dollar despite a much smaller war-chest,” Anderson said. “These companies that are worth 1/1000th of these bigger companies are effectively going toe-to-toe to offer whatever women need.”

Anderson and his wife, FertilityIQ co-founder Deborah Anderson, noticed improved benefits in 2018 from companies implicated by the #MeToo movement, such as Vice Media, Under Armour and Uber.

“Silicon Valley is notorious for talent moving around on you but it’s probably not coincidental that some of the companies that were in the spotlight in the #MeToo movement have added really generous benefits,” Deborah Anderson told TechCrunch.

Uber, for example, now pays for its employees to complete two IVF cycles but still requires pre-authorization.

One in 7 Americans struggle with infertility and the rate of IVF procedures only continues to increase, with the latest data indicating a 15 percent year-over-year growth rate. IVF costs roughly $22,000 per cycle, per FertilityIQ’s survey, a cost which has similarly increased 15 percent since 2015.

That’s a whole lot of cash for a fertility patient to dole out. If companies foot the bill, they’ll have a better shot at retaining talent.

“Best we can tell, there is no question that employees that get this benefit and use it are more loyal and more likely to stick around,” Jake Anderson said. “The company that helps you build your family is the company that you remain committed to.”

Powered by WPeMatico

French startup Lydia is launching an insurance product for your mobile phone. For €4.29 per month ($4.89), you can insure your phone from the Lydia app.

Lydia is one of the most popular peer-to-peer payment apps in Europe, with 1.5 million users. Think about it as a sort of Venmo or Square Cash for Europe. More recently, the company started offering more options to manage your money with a premium subscription and additional features.

While Lydia doesn’t want to replace your bank and insurance company, the company is offering an insurance product for the first time. Lydia is partnering with its investor CNP Assurances — having an insurance company as an investor has a few advantages.

So here’s what you get. You’re instantly covered against cracked screens, liquid damage and accidental damage. There’s no excess, but you’re limited to one claim per year. Phones now cost a small fortune, but you’re limited to €500 ($570) per claim.

Optionally, you can subscribe to a better insurance product for €9.99 per month ($11.39). In addition to phone insurance, your laptop, tablet, Nintendo Switch, Kindle, camera and other electronics are covered. You can make two claims per year and you can get back up to €500 for your phone and €1,800 for other devices. More importantly, you’re also covered against theft.

Many phone carriers sell mobile phone insurance. But they usually cost more than that. In most cases, you also need to subscribe for at least one year. In Lydia’s case, you can cancel your subscription whenever you want in the app.

If that product sounds familiar, it’s because Revolut offers a similar feature (with some drawbacks). You can subscribe to mobile phone insurance from Revolut’s mobile app.

Pricing isn’t as straightforward with Revolut, as Premium subscribers get a discount. For an iPhone X, the insurance product costs as much as €9.58 per month ($10.92) without a Revolut Premium account, or as little as €6.67 per month ($7.60) if you pay upfront and you have a Revolut Premium account.

It’s a 12-month contract with a €125 excess and no theft protection. You also need to start insuring your phone quickly after buying (within six months), otherwise you aren’t covered. Revolut works with Allianz and Simplesurance for this insurance product.

Lydia may have borrowed the idea from Revolut, but I’m not sure why you’d choose Revolut’s insurance product over Lydia’s product.

It’s interesting to see that fintech companies are creating alternative revenue streams with insurance products. Subscribing to an insurance product is quick and painless, as they already manage your money and have your card on file.

Powered by WPeMatico

One of the latest additions to the on-demand economy is Papa, a mobile app that connects college students with adults over 60 in need of support and companionship.

The recent graduate of Y Combinator’s accelerator program has raised a $2.4 million round of funding to expand its service throughout Florida and to five additional states next year, beginning with Pennsylvania. Initialized Capital led the round, with participation from Sound Ventures.

Headquartered in Miami, the startup was founded last year by chief executive officer Andrew Parker. The idea came to him while he was juggling a full-time job at a startup and caring for his grandfather, who had early onset dementia.

“I’ve always been a connector of humans,” Parker, the former vice president of health systems at telehealth company MDLIVE, told TechCrunch. “I’ve always naturally felt comfortable with all walks of life and all age groups and have just felt human connection is really critical.”

Seniors can request a “Papa Pal” using the company’s mobile app, desktop site or by phone. The pals can pick them up and take them out for an activity or have them over to play a game, complete household chores, teach them how to use social media and other technology or simply to chat. A senior is matched with a student, who must complete a “rigorous” background check, in as little as 30 seconds.

Parker says there are 600 students working with Papa an average of 25 hours per month.

“We’ve been fortunate that this is something the students really want to be part of,” he said. “They aren’t doing this for a couple extra dollars. They are doing this to help the community.”

The service costs seniors $20 per hour, $12 of which is paid to the students and $8 is returned to Papa. It’s not a subscription-based service, but seniors can pay for a premium option that lets them choose between three Papa Pals instead of being randomly paired with one of the several hundred options. The students do not provide any personal care, like bathing or grooming. And they are not a pick-up and drop-off service, like Uber or Lyft.

“We believe the Papa team has found a unique way to combat loneliness and depression in older adults,” said Alexis Ohanian, co-founder and managing partner of Initialized Capital, in a statement. “The experience that Papa Pals bring their members make it seem like they are part of a family.”

In addition to expanding to new markets, Papa is in the process of partnering with insurance companies with a goal of allowing seniors to pay for some of its services through their Medicare plans.

“Loneliness is a crisis. It’s a disease. It’s killing people prematurely,” Parker said. “We are providing a really massive impact to these people’s lives.”

Powered by WPeMatico

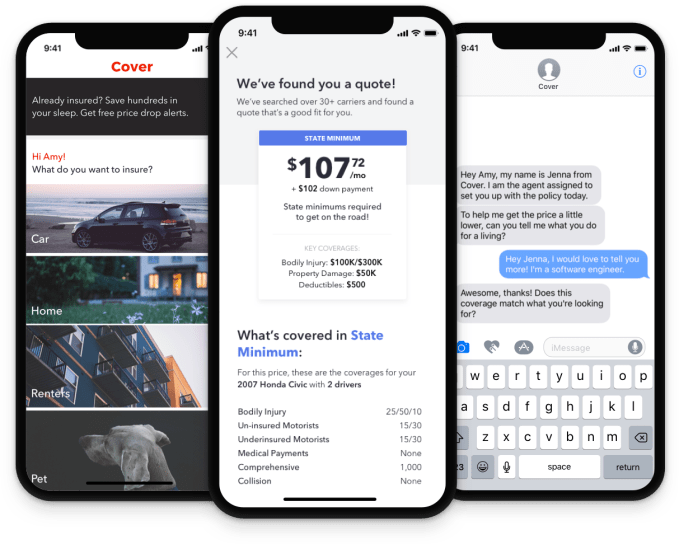

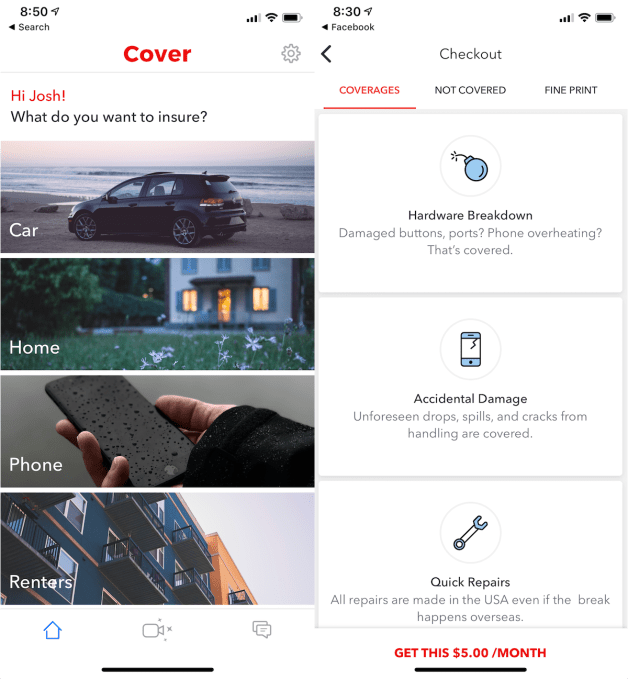

People procrastinate about buying insurance because it’s such a boring and complicated chore to compare policies. But Cover combines plans from 45 insurance companies into a single marketplace so it’s easy to find the best one for your car, home, rental, business, personal property, pets, jewelry and more. Now Cover is building powerful onboarding tricks like a driving school that earns you lower car insurance rates, and a way for Shopify merchants to sell warranties for their items.

The potential to use tech to run circles around the old insurance brokers has attracted a new $16 million Series B for Cover led by Tribe Capital’s Arjun Sethi, who led the Series A and sits on the startup’s board. The round was joined by Y Combinator, Social Capital, Exor and Samsung, and brings the company to a total of $27.1 million in funding.

“Insurance isn’t very different from being a white-collar bookie, where the house’s rake is too high and the dollars at stake are in the hundreds of billions in the U.S. alone,” says co-founder and CEO Karn Saroya. “This, all to the detriment of regular people, who view insurance as a tax. We’re here to change that perception.”

Saroya and his co-founders have deep ties. He went to high school with Anand Dhillon, is engaged to Natalie Gray and hired Ben Aneesh at the team’s previous startup, a high-end fashion marketplace called StyleKick that was eventually acqui-hired by Shopify. “We were tossing around ideas for what we wanted to do after StyleKick/Shopify, running hackathons on weekends. We built a couple different apps, but Cover — the MVP, where we just asked potential customers to take pictures of things they wanted to insure, surprised us” says Saroya. “Our customers sent us walkthroughs of their homes, pictures of their dogs and videos of themselves washing their cars. When you come across behavior that violates your expectations in consumers, that’s usually when you double-down.”

Cover co-founder and CEO Karn Saroya

So they built Cover, where you don’t have to cobble together an endless set of insurance websites or wait on hold. You download the app, pick your item, list how much you paid and where, provide some photos or video of its condition using its TensorFlow-equipped camera and Cover will check across its insurance partners and find you the best quote instantly. You can easily see what is and isn’t covered, learn how to make claims, and text with an agent if you have questions. For example, I was quickly quoted $5 per month to insure my new iPhone against damage but not loss or theft.

Cover earns between 10 to 35 percent per dollar of premium you pay. Its annualized premium already exceeds $8.5 million and is growing 30 percent per month. Thanks to its low-churn business model, easy cross-promotion of products, low training requirements for customers and no need to constantly update its existing subscriptions, Cover starts to look like a very efficient software-as-a-service business.

The big question remains whether Cover can consistently find the best rates for customers so they don’t second guess its quotes and search somewhere else. It will have to outcompete multi-insurance providers, like State Farm and Geico, as well as startups like MetroMile tackling specific insurance verticals with mobile apps. To really earn the big profits, Cover is building out its own in-house insurance plans. But that will put it under constant threat of insuring the wrong risks and ending up paying out too much.

“We built Cover because we saw an opportunity to build elegant products that could deliver on pricing and customer experience in a way that no incumbent insurance entity can,” Saroya concludes. By bringing the service to mobile and making it a seamless part of owning something, Cover could ensure you’re insured, even if insurance is the last thing you want to think about.

Powered by WPeMatico

OneDegree, a Hong Kong-based insurance technology startup, announced today that it has closed a Series A totaling HKD $200 million (about $25.5 million). Half of that amount was pledged by investors to OneDegree pending regulatory approval through the Hong Kong Insurance Authority’s new fast-track licensing program for online-only insurers. The company, which participated in Cyberport, the Hong Kong government’s startup incubator, claims this is the largest ever fundraising round for a pre-revenue insurance tech startup in Hong Kong.

OneDegree is currently not disclosing its list of investors because its new shareholders are being vetted by the Insurance Authority, founder and CEO Alvin Kwock tells TechCrunch, but it includes institutional investors and family offices. The South China Morning Post reports that speculation among brokers peg Tencent and Alibaba as probable backers.

OneDegree has developed an online insurance platform that lets consumers purchase personal lines and health insurance products without needing to consult with an agent. Instead, they find and buy policies through an app that is connected to a backend that automates claims processing, policy management and customer service.

The startup will initially sell medical insurance plans for pets. While there are more than 500,000 pet dogs and cats in Hong Kong, only about 2% to 3% are covered by insurance, compared to 42% in the United Kingdom, says OneDegree. The startup blames this on ineffective distribution, since pet insurance has relatively low premiums and is therefore overlooked by insurance agents, even though the number of pet dogs and cats in Hong Kong is increasing at an average annual growth rate of 3.5% and their owners are a relatively affluent demographic.

OneDegree plans to use its Series A to on tech development, launching new products and marketing. The funding will also serve as risk capital once it launches its insurance business.

In a press statement, Cyberport chairman George Lam said “As a key driver of digital technology development in Hong Kong, we are definitely excited to see local fintech start-ups like OneDegree successfully securing recognition from renowned institutional investors and attracting sizable funding that will enable faster growth.”

Powered by WPeMatico

Berlin based Internet of Things (IoT) startup relayr, whose middleware platform is geared towards helping industrial companies unlock data insights from their existing machinery and production line kit by linking Internet connected sensors and edge devices to platform controls, has been acquired by insurance group Munich Re in a deal which values the company at $300 million.

relayr was founded back in 2013 with the initial aim of helping software developers hack around with hardware, at a time when developer interest in IoT was just taking off.

The startup went on to pass through startupbootcamp and crowdfunded a cute looking chocolate-bar shaped hardware starter kit before expanding into building a hardware agnostic cloud services platform to act as a central hub for data flows. relayr then further honed its focus to the needs of industrial IoT, and its platform — which is now used by around 130 businesses — offers end-to-end middleware combined with device management and IoT analytics, and can operate in the cloud, on-premise or a hybrid of both depending on customers needs.

We first covered the Berlin-based startup back in 2014 when it closed a $2.3M seed round. It’s raised $66.8M in total, according to Crunchbase, which includes a $30M Series C round in February led by Deutsche Telekom Capital Partners.

relayr did not disclose the investors in its 2014 seed at the time, saying only that they were unnamed U.S. and Switzerland-based investors. But Kleiner Perkins and Munich Re (via its HSB subsidiary which is acquiring relayr now) were named as investors in later rounds, along with Deutsche Telekom .

Insurance giants and telcos have a clear strategic interest in IoT — with the technology promising to drive network usage and utility on the telco side, and offering transformative potential for the insurance industry as data streams can be used to monitor equipment performance and predict (and even steer off) costly failures.

Munich Re said today that its HSB subsidiary is acquiring 100% of relayr in a deal that values the business at $300M. (It’s not clear if it’s all cash or a mix of cash and stock — we’ve asked. Update: A spokeswomen for Munich Re confirmed the transaction will be financed with “internal cash funds” from the group).

It says the deal will help it “shape opportunities in the fast-growing IoT market”, and is envisaging a joint business model with the combined pair developing not just tech solutions for clients but risk management, data analysis and financial instruments.

“IoT is already significantly changing our world and has the potential to disrupt the traditional insurance and reinsurance industry through new business models, services and competitors,” said Torsten Jeworrek, member of Munich Re’s board of management in a statement. “I am truly happy to announce this acquisition, as it supports our strategy to combine our knowledge of risk, data analysis skills and financial strength with the technological expertise of relayr. This is our basis to develop new ideas for tomorrow’s commercial and industrial worlds.”

“We are delighted to strengthen our relationship with Munich Re/HSB to push digitalization in commercial and industrial markets and strive for our mission to help commercial and industrial businesses stay relevant,” added relayr CEO, Josef Brunner. “The unique combination of the companies demonstrates the importance to deliver business outcomes to customers and the need to combine first-class technology and its delivery with powerful financial and insurance offerings. This transaction is a great opportunity to build a global category leader.”

The pair have been partnered since 2016, when the insurance firm invested in relayr’s Series B, but say they see the acquisition strengthening Munich Re’s financial and insurance offerings while also offering a route to expand relayr’s middleware business via leveraging the insurance group’s large client base.

“Back in 2016, HSB invested in relayr in an effort to harness the strategically significant business potential offered by IoT. relayr’s end-to-end IoT solutions for the industrial and commercial sectors are an ideal addition to our Group’s capabilities,” said Greg Barats, president and CEO of HSB, and the person responsible for Munich Re’s IoT strategy, in another supporting statement. “HSB has always focused on insurance and technology… relayr will help us to rapidly implement our global strategy to develop new IoT solutions for our clients. Digital transformation in the industrial and commercial sectors offers opportunities for new services and financial applications.”

relayr says it already offers industrial companies which are seeking to digitalise their businesses a “comprehensive range of services” — such as being able to extract and analyse data from machines and equipment to determine when a machine is likely to fail (and it touts cutting costs, increased energy efficiency and product quality improvement as among the benefits its platform offers) — but says the acquisition will allow it to develop its “innovative value stack”, by enabling new revenue models, cost reduction, and “increased effectiveness across industries”.

It also sees benefit in sitting under the established Munich Re umbrella — as a way to convince customers it will be a long-term business partner. It adds that it will continue to maintain its current focus on IoT for the industrial sector.

Powered by WPeMatico

For the last decade, the largest technology companies have increasingly looked outside of tech to grow their operations. From automotive to retail to groceries, these companies use massive competitive advantages in the form of data, consumer relationships and software engineers to fundamentally change markets.

Now, companies like Apple and Google and Amazon are eyeing innovation across the insurance landscape. For example, Amazon is teaming with JPMorgan and Berkshire Hathaway to create a new way to approach health insurance, focusing first on the group’s own employees. On the retail side, Amazon is selling product insurance and extended warranties at the point of sale and investing in insurtech startups. Meanwhile, Tesla is developing an insurance product specific to the Model S. Waymo, Uber and Lyft are certainly having similar conversations internally.

Obviously, these are all preliminary steps. Insurance is a complex, multifaceted and, yes, risky business. In the end, whether or not companies like Amazon become insurers themselves depends on their appetite for risk, their ability to innovate and the potential pay off.

To start, let’s look at the reasons why tech giants are well-suited to upend the space.

Like many businesses, a large aspect of a successful insurance business is distribution. Just look at brokers, which are a major means of distribution for insurers today — their cut can be up to 30 percent of the cost of an insurance policy. Brokers also see better margins than insurers themselves, usually around 10 percent net margins. Facebook, Amazon, Apple, Microsoft and Google (FAAMG) possess direct relationship with billions of consumers and could, over time, disrupt the broker business.

The big secret in insurance is that insurers are actually terrible at using their data. Different departments (marketing, underwriting, claims) rarely work together, and their data tends to be siloed. FAAMG, on the other hand, has put data at the core of their offering; they know how to leverage analytics and AI to create better products.

Tech giants may be tempted to use their troves of data to compete with insurers directly.

They also have access to data that insurers can only dream of having: global geospatial imagery of homes, infrastructure and buildings; location, browsing and advertising data; even real-world behavioral data from smartphones and IoT devices. Combining all these signals can create a very complete picture of human behavior, interests and risk profile.

Tech innovation has long been a challenge for insurance incumbents. Old systems are difficult to displace in any industry, but the complexity of insurance, tradition of relying on the past to predict the future and silos of data can make it a Herculean effort. Tech giants, on the other hand, regularly cannibalize their own revenue with new products and can enlist tens of thousands of engineers to develop fantastic digital customer experiences and bring large-scale efficiencies to back-end insurance systems through better software and AI.

So, yes, FAAMG has a number of major advantages over insurance incumbents. But for tech giants, new verticals and initiatives are also longer-term decisions around margins and market scope. It’s an obvious point, but if FAAMG wants to jump into insurance, they’ll want a decent return. Can they find that in insurance?

There are a number of reasons why it might be a tough sell.

Average insurance net margins are 3-8 percent, and 25-30 percent gross margins, which are meager for tech standards. Software companies average around 80 percent gross margins and around 15 percent net margins. Even consumer hardware like the iPhone — a costly endeavor by software standards — sees 55-60 percent gross margins.

Within insurance, health tends to have the highest margins, followed by property and casualty (i.e. home and auto insurance), followed by life insurance. So if anything, healthcare is probably the closest thing to “low-hanging fruit” — but it’s not exactly attractive to most companies outside insurance.

Such low margin also means that one major event can destroy a company’s balance sheet for an entire fiscal year (think disasters like hurricanes, fire, flood, etc.). In addition, tech companies don’t have the historical data and actuarial scientists that insurers have spent decades building up, so they might be more prone to misjudging their overall risk exposure.

For insurers, evaluating and underwriting policies is an expensive endeavor. Claims, customer support and back-end are costly and complex. That said, most insurance companies are already outsourcing the development of core administration software to companies like GuideWire and Duck Creek, and then customizing the software to meet their specific needs at the last mile. So it’s not as huge of a leap as it once was to think that the likes of Amazon or Google could develop similar infrastructure in-house to rival incumbent systems. Or, they could easily buy one of the development companies outright and subsume that expertise.

Still, the creation and underwriting of policies is something tech giants have avoided to date. Amazon has been working on warranties for certain products as an add-on to their margins — but these were backed and administered by The Warranty Group rather than Amazon itself. Before that, Amazon acted as a sales channel for SquareTrade and built up an understanding of the warranty business before diving in deeper. Tesla, as another example, announced it was selling Tesla-branded tailor-made policies for its vehicle owners, but those policies were backed by Liberty Mutual.

What role will tech giants in the U.S. play in the insurance landscape?

Then, in January, Amazon made a well-publicized announcement, in tandem with Berkshire Hathaway and JPMorgan, around its intention to create a private healthcare option for their workers. We don’t know much about the initiative, but Amazon has been working on a healthcare technology project codenamed 1492 for some time. Rumors point to a “platform for electronic medical record data, telemedicine, and health apps.” Amazon’s technology paired with Berkshire Hathaway’s insurance knowledge and JPMorgan’s financial expertise makes the creation of a new health insurance entity more likely. If so, this would be a significant shot across the bow of U.S. healthcare insurers.

Of all the tech giants, it would not be a surprise if Amazon were the first to jump into insurance. Amazon has mastered the art of building massive businesses off of razor-thin margins. They’re also targeting health insurance, which presents the best margin opportunity. They can test their offering within the company first and then scale across their massive consumer base. Finally, they have a history of building out complex back-end services for their own purposes before offering it to their customers — just look at AWS.

Signs point to yes. Recently, Google’s sister company, Verily, “has been in talks with insurers about jointly bidding for contracts that would involve taking on risk for hundreds of thousands of patients.” In addition, Apple will be opening a network of medical clinics for its employees.

It may not stop at health insurance. There’s no question technology is changing human behavior and society, and as the developers of much of this new tech, FAAMG will inevitably be pushed closer to other sectors of insurance, as well, including home and auto.

Autonomous vehicle fleets will make companies like Tesla, Google and Uber the owners of tens of thousands of cars, subjecting them to the risk that comes with that. Meanwhile, IoT hardware and accompanying services are bringing tech giants into the living room. That’s a literal statement when it comes to Amazon Key. Nest, Google Home and Amazon Echo are more innocuous, but provide all sorts of data about what’s going on inside the home and could, someday, help inform the creation of real-time home insurance policies.

It also can be instructive to look at markets outside the U.S. In East Asia, businesses are taking a more aggressive posture vis-à-vis insurance. Baidu, Alibaba, Rakuten, Tencent and LINE have all shown some level of appetite for offering their own insurance products. These companies can verify identities, enforce trust and access the behavioral and financial data necessary to provide better policies than many insurance incumbents in those countries.

They also are exploring new ways of looking at risk and changing user behavior: Tencent’s WeSure is paying users to stay healthy by walking more, while Yongqianbao, a lending company, tracks unconventional digital data to determine credit risk, such as phone brand (iPhone users are less likely to default) and whether they let their phone batteries run down.

Still, the question remains: What role will tech giants in the U.S. play in the insurance landscape? Will they act as a channel for existing insurers, as a provider of data and analytics to those insurers or even as a provider of direct insurance themselves?

Insurance may not be lucrative-enough for tech giants in the short-term, but as real-time data and analytics are used to create insurance policies, tech giants may be tempted to use their troves of data to compete with insurers directly. Until then, we can expect insurers and tech giants to form alliances, as they have in East Asia, with tech companies using insurance and warranties as a value-add for their customers, and insurers using tech companies as a sales channel. Regardless, the story of FAAMG (and others) in insurance is undoubtedly just getting started, and we’ll have to check back in as the landscape develops.

Powered by WPeMatico

Planck Re, a startup that wants to simplify insurance underwriting with artificial intelligence, announced today that it has raised a $12 million Series A. The funding was led by Arbor Ventures, with participation from Viola FinTech and Eight Roads. Co-founder and CEO Elad Tsur tells TechCrunch that the capital will be used to expand Planck Re’s product line into more segments, including retail, contractors, IT and manufacturing, and grow its research and development team in Israel and North American sales team.

The Tel Aviv and New York-based startup plans to focus first on its business in the United States, where it has already launched pilot programs with several insurance carriers. Tsur says that Planck Re’s clients generally use it to help underwrite insurance for small to medium-sized businesses, including business owner policies, which cover property and liability risks, and workers’ compensation.

Founded in 2016 by Tsur, Amir Cohen and David Schapiro, Planck Re poses its technology as a more efficient and accurate alternative to the lengthy risk assessment questionnaire insurers ask clients to fill out. Its platform crawls the internet for publicly available data, including images, text, videos, social media profiles and public records, to build profiles of SMBs seeking insurance coverage. Then it analyzes that data to help carriers figure out their potential risk.

Before launching Planck Re, Tsur and Cohen founded Bluetail, a data mining startup that was acquired by Salesforce in 2012, where it served as the base technology for Salesforce Einstein. Schapiro was previously CEO of financial analytics company Earnix.

There are already a handful of startups, including SoftBank-backed Lemonade, Trōv, Cover, Hippo and Swyfft, that use algorithms to make picking and buying insurance policies easier for consumers, but AI-based underwriting is still a nascent category. One example is Flyreel, which focuses on underwriting property insurance and recently signed a deal with Microsoft to accelerate its go-to-market strategy.

Tsur says Planck Re is developing more dedicated algorithms to meet the evolving needs of insurance providers. For example, many underwriters now want to know if clients in photography use aerial imaging equipment, so Planck Re’s imaging process capabilities automatically check images for that information.

He adds that being able to automate underwriting enables carriers to find new distribution channels, including allowing customers to apply for insurance online without needing to fill out any forms. Planck Re also continues to monitor and underwrite policies, which means if a customer’s risk profile changes, insurers can react quickly.

In a statement, Arbor Ventures vice president and head of Israel Lior Simon said, “We are excited to partner with Planck Re and the driven, entrepreneurial team. Insurance companies are thirsty for actionable data, to assess risk, gain real time insights and enhance customer understanding. Planck Re aims to empower them through a streamlined digital approach, which we believe will truly alter the insurance industry.”

Powered by WPeMatico

Ethos, the company that bills itself as making life insurance accessible, affordable and simple, has officially come out of stealth with an $11.5 million investment led by one of the world’s top venture firms, Sequoia Capital, and additional participation from the family offices of Hollywood’s biggest stars and an NBA all-star.

Jay Z’s Roc Nation, and the family funds of Kevin Durant, Robert Downey Jr. and Will Smith, all participated in the new round for Ethos, and Sequoia Partner Roelof Botha is taking a seat on the company’s board. Because nothing says star power like a life insurance startup.

The life insurance market is one that’s been attracting interest from venture investors for a little over a year now. Companies like England’s Anorak, HealthIQ, Ladder, Mira Financial, and France’s Alan, which is backed by Partech Investments (among others), Fabric and Quilt, are all pitching life insurance products as well.

Ethos is licensed in 49 states, which is pretty comparable to the offering from providers like Haven Life, the Mass Mutual-backed life insurance product.

What has made the life insurance market interesting for investors is the fact that consumers’ interest in it continues to decline. Whether it’s because no one trusts insurers to actually pay out, or because Americans are putting their faith in the anti-aging technologies from funds like the Longevity Fund, folks just aren’t buying insurance products the way they used to.

So when investors see the numbers of users of a formerly ubiquitous product decline from 77 percent in 1989 to below 60 percent in 2018, the assumption is that there’s room for new companies to come in and provide better service.

Scads of investors have taken the same bet, which makes Ethos a marketing play as much as anything else. In the company’s press release it touts the fast, easy and inexpensive process for getting a quote.

The initial process requires only four questions to get a quote and a 10 minute survey to get a policy (in most cases). The company says 99 percent of its applicants don’t need a medical exam or blood test to get a policy.

What may have been most interesting to investors is the pedigree of the company’s co-founders. Peter Colis and Lingke Wang have both worked in the insurance industry before. They previously co-founded a life insurance marketplace called, Ovid Life.

“Life insurance is critical for families, but the process is broken for those who want and need it,” said Peter Colis. “We are consumer advocates, intensely focused on expanding life insurance accessibility to the millions of U.S. families who have college debt, mortgages, spouses and children to care for, and who want to be financially empowered to live their lives without worry.”

Ethos founders Lingke Wang and Peter Colis

Powered by WPeMatico