insurance

Auto Added by WPeMatico

Auto Added by WPeMatico

Amazon has gone live with Amazon Care, a new pilot healthcare service offering that is initially available to its employees in and around the Seattle area. The Amazon Care offering includes both virtual and in-person care, with telemedicine via app, chat and remote video, as well as follow-up visits and prescription drug delivery in person directly at an employee’s home or office.

First reported by CNBC, Amazon Care grew out of an initiative announced in 2018 with J.P. Morgan and Berkshire Hathaway to make a big change in how they all collectively handle their employee healthcare needs. The companies announced at the time that they were eager to put together a solution that was “free from profit-making incentives and constraints,” which are of course at the heart of private insurance companies that serve corporate clients currently.

Other large companies, like Apple, offer their own on-premise and remotely accessible healthcare services as part of their employee compensation and benefits packages, so Amazon is hardly unique in seeking to scratch this itch. The difference, however, is that Amazon Care is much more external-facing than those offered by its peers in Silicon Valley, with a brand identity and presentation that strongly suggests the company is thinking about more than its own workforce when it comes to a future potential addressable market for Care.

The Amazon Care logo.

Care’s website also provides a look at the app that Amazon developed for the telemedicine component, which shows the flow for choosing between text chat and video, as well as a summary of care provided through the service, with invoices, diagnosis and treatment plans all available for patient review.

Amazon lists Care as an option for a “first stop,” with the ability to handle things like colds, infections, minor injuries, preventative consultations, lab work, vaccinations, contraceptives and STI testing and general questions. Basically, it sounds like they cover a lot of what you’d handle at your general practitioner, before being recommended on for any more specialist or advanced medical treatment or expertise.

Rendered screenshots of the Amazon Care app for Amazon employees.

Current eligibility is limited to Amazon’s employees who are enrolled in the company’s health insurance plan and who are located in the pilot service geographical area. The service is currently available between 8 AM and 9 PM local time, Monday through Friday, and between 8 AM and 6 PM Saturday and Sunday.

Amazon acquired PillPack last year, an online pharmacy startup, for around $753 million, and that appears to be part of their core value proposition with Amazon Care, too, which features couriered prescribed medications and remotely communicated treatment plans.

Amazon may be limiting this pilot to employees at launch, but the highly publicized nature of their approach, and the amount of product development that clearly went into developing the initial app, user experience and brand all indicate that it has the broader U.S. market in mind as a potential expansion opportunity down the line. Recent reports also suggest that it’s going to make a play in consumer health with new wearable fitness tracking devices, which could very nicely complement insurance and healthcare services offered at the enterprise and individual level. Perhaps not coincidentally, Walgreens, CVS and McKesson stock were all trading down today.

Powered by WPeMatico

Hedvig, a Swedish startup, is following in the footsteps of Lemonade, building a new generation of insurance platforms that use AI to help evaluate customers and operate on a policy of using surplus for social good. Today the company announced the next stage of its growth. The startup has closed a SEK100 million ($10.4 million) round of funding to expand from its current offering of property insurance into a wider range of categories, and begin the costly process of expanding its business into more countries beyond its home market.

The funding values the company at SEK342 million ($35.5 million) — a modest figure considering Lemonade’s recent $300 million round, reportedly (per PitchBook) at a $2.1 billion post-money valuation — but helps position the company to set its sights on being a strong regional player (if not an acquisition target for Lemonade if it wants to quickly add new regions: the latter kicked off its first services in Europe earlier this year, so its global aspirations are clear).

It currently has 15,000 customers in its home market of Sweden, who use it for property insurance on rented or owned apartments, and Lucas Carlsen, the co-founder and CEO, said in an emailed interview with TechCrunch that it “definitely” plans to expand that to houses as well as other categories. Home insurance also covers contents, such as gadgets, and travel, and Carlsen said that the former (gadgets) accounts for the majority of claims at the moment.

The round was led by Obvious Ventures, the venture fund co-founded by Twitter/Medium/Blogger co-founder Ev Williams, with D-Ax, the early-stage investment arm of Swedish retail giant Axel Johnson Group, also participating, along with past investor Cherry Ventures.

“We are building a global company. We just started in Sweden since we happened to live here, and it serves as a good test market as we have some of the worlds’ most progressive and demanding consumers. Today, we do not have any news to share about future markets, but stay tuned!,” said Carlsen.

“The new funding will mainly be used to fuel growth in Sweden, but we’ll also be looking at extending into new markets and insurance categories. Insurance is capital intensive and our new partners are committed to supporting our long-term vision,” he continued.

Indeed, getting an investor like Obvious (which published its own short announcement about the investment) involved could open the door to introductions with a number of other investors down the road.

“Hedvig is harnessing its purpose, the power of AI, and its human-centered product to create a modern, full-stack insurance company. Their incredible team is delivering against the mission – to give people the world’s most incredible insurance experience – and we at Obvious are honored to help scale it further,” said Vishal Vasishth, one of Obvious Ventures’ other co-founders, in a statement.

Hedvig — named, Carlsen said, after a legend of “someone who stood up for others and fought for their causes: that’s what we do,” — will sound familiar to you if you know Lemonade.

It follows in a wave of more socially forward businesses that are being created, which are using technology to help disrupt the status quo but also to bridge the gap between building services that consumers need and the principles they would like to adhere to more if possible. (Other examples include the likes of Beyond Meat, which is also backed by Obvious; as well as the plethora of electric and hybrid vehicle makers; and more.)

In the case of Hedvig and the challenge of insurance, the proposition goes like this:

Hedvig uses technology and innovative algorithms to help assess a potential customer, who is then provided with lowest-cost, and often competitively priced, premiums. Then, as a “full-stack” digital company, it also uses its algorithms to help process claims. After Hedvig uses its bigger pot of money to pay out claims, the annual surplus is donated to charities selected by its customers.

“By not pocketing this money ourselves we can focus on providing the best service possible to you and not on making more money from denying claims,” Carlsen said.

Hedvig itself makes money by taking a cut off users’ monthly premiums (it doesn’t specify how much). To date, Hedvig has not disclosed how much it has been able to “give back” according to its business model. But the philosophy is that by digitising some of the more mundane processes that are relegated to human adjustors and customer agents at traditional agencies — and by not being inherently greedy — the startup is able to provide a more pleasant, more efficient and more conscionable service.

Powered by WPeMatico

Why is tech still aiming for the healthcare industry? It seems full of endless regulatory hurdles or stories of misguided founders with no knowledge of the space, running headlong into it, only to fall on their faces.

Theranos is a prime example of a founder with zero health background or understanding of the industry — and just look what happened there! The company folded not long after founder Elizabeth Holmes came under criminal investigation and was barred from operating in her own labs for carelessly handling sensitive health data and test results.

But sometimes tech figures it out. It took years for 23andMe to breakthrough FDA regulations — it’s since more than tripled its business and moved into drug discovery.

And then there’s Oscar Health, which first made a mint on Obamacare and has since ventured into Medicare. Combined with Bright, the two health insurance startups have pulled in a whopping $3 billion so far.

It’s easy to shake our fists at fool-hardy founders hoping to cash in on an industry that cannot rely on the old motto “move fast and break things.” But it doesn’t have to be the code tech lives or dies by.

So which startups have the mojo to keep at it and rise to the top? Venture capitalists often get to see a lot before deciding to invest. So we asked a few of our favorite health VC’s to share their insights.

Powered by WPeMatico

A couple of years ago, London-based startup Zego realised gig-economy workers would need insurance, and went on to raise a very healthy £6 million in Series A funding, led by Balderton Capital. Its first products were pay-as-you-go scooter and car insurance for food delivery workers.

It’s now announced a $42 million raise in one of the largest funding rounds for a European insurtech startup, in a Series B investment led by pan-European investment firm Target Global, specialists in the fintech and mobility space, with other backers including TransferWise founder Taavet Hinrikus. The proceeds will be used to for Zego’s expansion across Europe and to increase the workforce from 75 to 150.

The raise takes the firm to a total of $51 million in funding, with new investors Latitude joining existing backers Balderton Capital and Tom Stafford of DST Global. The investment comes as the company claims a whopping 900% growth over the past 12 months.

Zego caters to the new mobility services, such as ride-hailing, ridesharing, car rental and scooter sharing, and offers a range of policies from minute-by-minute insurance to annual cover, providing more flexibility than traditional insurers, with pricing based on usage data from vehicles.

This means it’s become popular with scooter and car delivery drivers, plus van and taxi fleets. The firm currently insures one-third of the U.K.’s food delivery market, largely through partnerships with Deliveroo, Just Eat and Uber Eats.

Sten Saar, CEO and co-founder of Zego, said: “When we built Zego from scratch three years ago, our mission was to transform the insurance sector by creating products which truly reflected the rapidly changing world of transport… The world is becoming more urbanized and because of this, we are moving from traditional ownership of vehicles to shared ‘usership’. This means that the rigid model of insurance that has existed for hundreds of years is no longer fit for purpose.”

Ben Kaminski, partner of lead investors Target Global, said: “With the growth of new mobility services, Zego identified a major gap in the insurance market and created a unique business model to fill it, which the incumbents will find very difficult to replicate. The potential of this company is almost limitless, and I fully expect to see its U.K. success mirrored across Europe and beyond in the coming years.”

Powered by WPeMatico

As studies show that early diagnosis and preventative therapies can help prevent the onset of Alzheimer’s, startups that are working to diagnose the disease earlier are gaining more attention and funding.

That’s a boon to companies like Neurotrack, which closed on $21 million in new financing led by the company’s previous investor, Khosla Ventures, with participation from new investors Dai-ichi Life and SOMPO Holdings.

Last year, the Japanese life insurance company Dai-ichi Life partnered with Neurotrack to roll out a cognitive assessment tool to the company’s customers in Japan.

And earlier this year, the Japanese health insurer SOMPO conducted a 16-week pilot with Neurotrack, where more than 550 of SOMPO’s employees took Neurotrack’s test and followed the Memory Health Program for four months. Neurotrack and SOMPO are now working to deepen and extend their partnership.

“As the global crisis around Alzheimer’s continues to grow, the private sector is joining government and nonprofits to address the problem in their markets. In Japan, for example, traditional insurance companies are developing novel solutions that incorporate Neurotrack’s products to advance better memory health among its population,” said Elli Kaplan, Neurotrack co-founder and CEO. “These partnerships are innovative models that we hope to replicate in other markets, enabling traditional insurance companies to create new markets while helping to address the Alzheimer’s crisis. And now they’re also investing in our company, so these companies have two ways of doing well by doing good.”

Neurodegenerative disorders are becoming a more serious issue for the island nation — and the rest of the world. In fact, over the weekend the G20 first raised the possibility that aging populations could be a global risk.

“Most of the G20 nations already experience or will experience ageing,” Bank of Japan governor Haruhiko Kuroda, told reporters from Agence France Presse. “We need to discuss problems that arise with societal ageing and how to deal with them.”

In the U.S., the estimated cost of caring for Americans with Alzheimer’s and other dementias was an estimated $277 billion in 2018, according to a study cited by WebMD. Roughly $186 billion of those costs are borne by Medicare and Medicaid, with another $60 billion in payments coming out-of-pocket. That number could top $1.1 trillion by 2050, according to the same report.

Neurotrack uses cognitive assessments that follow eye movements using the camera on a computer or mobile phone to create a baseline for cognitive functions. The company then uses a combination of brain training and diet, exercise and sleep adjustments to try to improve cognitive function and health.

Its technology is one of several different approaches startups are taking to try to provide early diagnoses and potential preventative measures against the disease.

MyndYou, another company tackling neurodegenerative diagnostics, uses an app to monitor movement among its users. The company assesses that data to determine whether there may be any issues related to cognitive function. It recently partnered with the Japanese company Mizuho to test its efficacy among Japan’s aging population.

Then there’s Altoida, another startup that launched recently to tackle the cognitive assessment market. It uses augmented reality and a series of memory tests to assess brain function and attempt to detect neurodegeneration.

Neurotrack’s technology, based on research from Emory University, has managed to attract more than just Japanese corporations. Previous investors like Sozo Ventures, Rethink Impact, AME Cloud Partners and Salesforce founder Marc Benioff have also thrown cash behind the company.

To date, the company has raised more than $50 million, including $6.8 million in grants from the National Institutes of Health and National Institute of Aging.

The company said its new investment will be used to develop new partnerships in additional global markets and continue research and development.

“One can now feel empowered to test for potential memory decline, given that Neurotrack’s Memory Health Program can help stave off cognitive decline. This fully integrated platform enables users to assess the state of their memory, reduce future risk for decline, and monitor progress in order to take better control of one’s memory health. We combine these tools with deep analytics to further target and personalize, creating a very powerful precision medicine solution,” said Kaplan. “Just as when you go on a diet, you use a scale to provide evidence that you’re losing weight. Neurotrack now has the equivalent of both a scale to measure and the Memory Health Program for cognitive health. This is a game-changer for dementia risk.”

Japan has national efforts targeting a reduction in the onset of dementia in 6% of people in their 70s by 2025 (the country has the world’s largest population of the elderly, with more than 20% of the country over the age of 65). Roughly 13 million people are expected to develop Alzheimer’s in Japan by 2025.

Part of the company’s success in fundraising comes from the results of a preliminary study that showed improved cognitive functions for people diagnosed with some decline in cognitive function after a year of using Neurotrack’s Memory Health Program. The company claims it has the the first fully integrated, clinically validated platform that can assess a person’s cognition through its cognitive assessment — which can predict conversion from healthy to mild cognitive impairment (MCI) or MCI to Alzheimer’s disease within three years at 89% accuracy, and within six years at 100% accuracy.

While that kind of assessment is good, Alzheimer’s symptoms can begin to appear as early as 25 years before the onset of the disease. So there’s still work to be done.

“Neurotrack has built an incredible integrative platform that is transforming our battle with Alzheimer’s,” said Jenny Abramson, founder and managing partner of Rethink Impact. “Elli’s two decades of experience in the private sector and in government are helping her scale this solution to the millions of people suffering from cognitive decline around the world. We couldn’t be more excited to continue to support Neurotrack, given both the financial opportunity and the impact they are already having on this critical disease.”

Powered by WPeMatico

OneDegree, an insurance technology startup based in Hong Kong, announced today it has extended its Series A round to $30 million, up from the $25.5 million it announced in September. Its extension, which the company is calling its “A2” round, was led by BitRock Capital, an investment firm that focuses on financial tech. Cyberport Macro Fund, Cathay Venture and investors from its initial Series A also participated.

The company is preparing to launch its online insurance platform, designed to make buying insurance plans easier for both consumers and providers by using data analytics to automate the most tedious parts of the process. The company will start with medical insurance for pets after its license is approved by the Hong Kong Insurance Authority before expanding into other products, including travel, cyber and human medical insurance.

In a press statement, OneDegree co-founder Alvin Kwock said its strategy is “not to compete head-on with traditional insurers, but rather to work together, steering the whole industry towards a fully digital ecosystem.”

Powered by WPeMatico

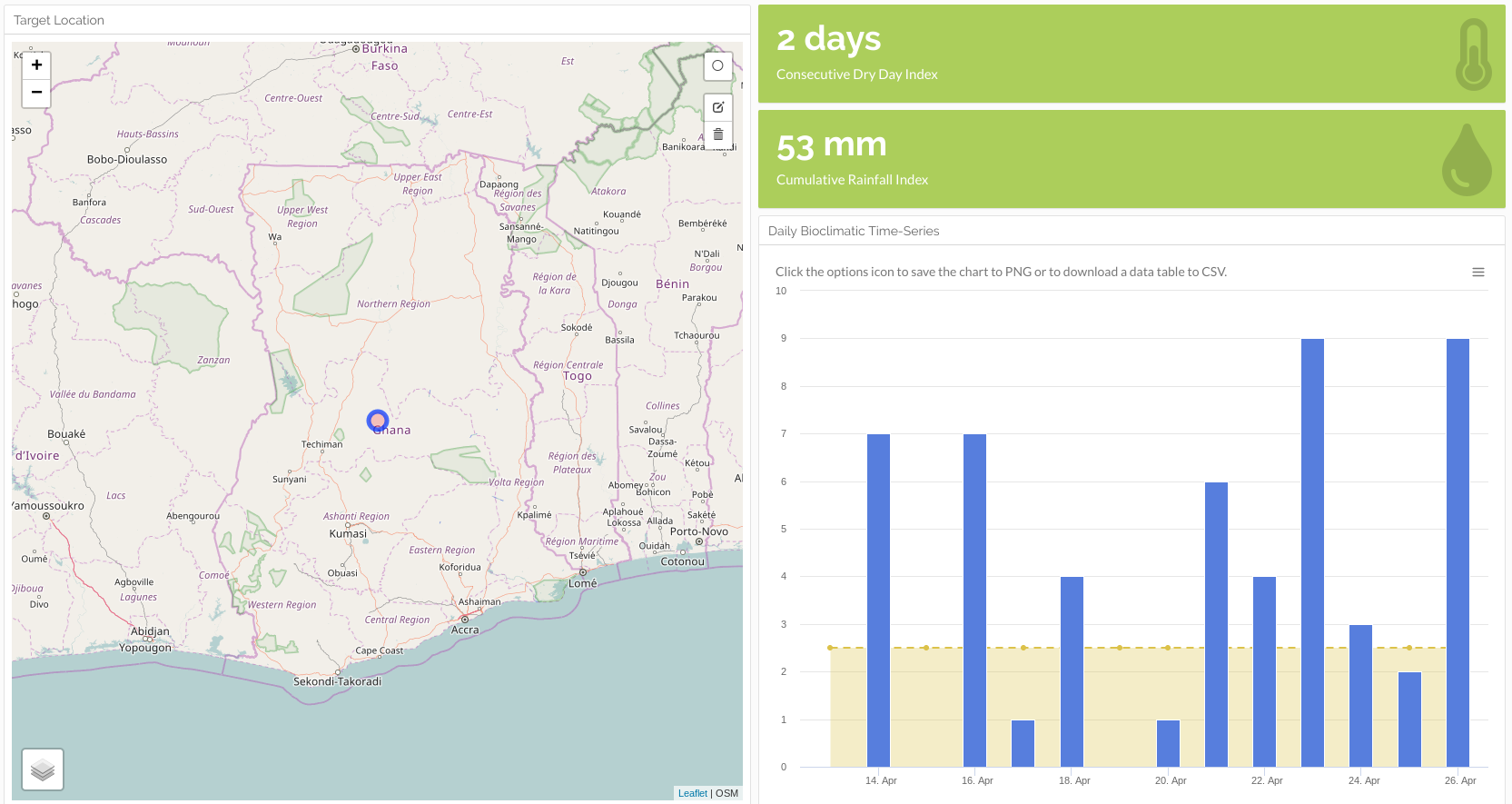

WorldCover, a New York and Africa-based climate insurance provider to smallholder farmers, has raised a $6 million Series A round led by MS&AD Ventures.

Y Combinator, Western Technology Investment and EchoVC also participated in the round.

WorldCover’s platform uses satellite imagery, on-ground sensors, mobile phones and data analytics to create insurance options for farmers whose crop yields are affected adversely by weather events — primarily lack of rain.

The startup currently operates in Ghana, Uganda and Kenya . With the new funding, WorldCover aims to expand its insurance offerings to more emerging market countries.

“We’re looking at India, Mexico, Brazil, Indonesia. India could be first on an 18-month timeline for a launch,” WorldCover co-founder and chief executive Chris Sheehan said in an interview.

The company has served more than 30,000 farmers across its Africa operations. Smallholder farmers are those earning all or nearly all of their income from agriculture, farming on 10-20 acres of land and earning around $500 to $5,000, according to Sheehan.

Farmers connect to WorldCover by creating an account on its USSD mobile app. From there they can input their region and crop type and determine how much insurance they would like to buy and use mobile money to purchase a plan. WorldCover works with payments providers such as M-Pesa in Kenya and MTN Mobile Money in Ghana.

The service works on a sliding scale, where a customer can receive anywhere from 5x to 15x the amount of premium they have paid. If there is an adverse weather event, namely lack of rain, the farmer can file a claim via mobile phone. WorldCover then uses its data-analytics metrics to assess it, and, if approved, the farmer will receive an insurance payment via mobile money.

Common crops farmed by WorldCover clients include maize, rice and peanuts. It looks to add coffee, cocoa and cashews to its coverage list.

For the moment, WorldCover only insures for events such as rainfall risk, but in the future it will look to include other weather events, such as tropical storms, in its insurance programs and platform data analytics.

For the moment, WorldCover only insures for events such as rainfall risk, but in the future it will look to include other weather events, such as tropical storms, in its insurance programs and platform data analytics.

The startup’s founder clarified that WorldCover’s model does not assess or provide insurance payouts specifically for climate change, though it does directly connect to the company’s business.

“We insure for adverse weather events that we believe climate change factors are exacerbating,” Sheehan explained. WorldCover also resells the risk of its policyholders to global reinsurers, such as Swiss Re and Nephila.

On the potential market size for WorldCover’s business, he highlights a 2018 Lloyd’s study that identified $163 billion of assets at risk, including agriculture, in emerging markets from negative, climate change-related events.

“That’s what WorldCover wants to go after…These are the kind of micro-systemic risks we think we can model and then create a micro product for a smallholder farmer that they can understand and will give them protection,” he said.

With the round, the startup will look to possibilities to update its platform to offer farming advice to smallholder farmers, in addition to insurance coverage.

WorldCover investor and EchoVC founder Eghosa Omoigui believes the startup’s insurance offerings can actually help farmers improve yield. “Weather-risk drives a lot of decisions with these farmers on what to plant, when to plant, and how much to plant,” he said. “With the crop insurance option, the farmer says, ‘Instead of one hector, I can now plant two or three, because I’m covered.’ ”

Insurance technology is another sector in Africa’s tech landscape filling up with venture-backed startups. Other insurance startups focusing on agriculture include Accion Venture Lab-backed Pula and South Africa based Mobbisurance.

With its new round and plans for global expansion, WorldCover joins a growing list of startups that have developed business models in Africa before raising rounds toward entering new markets abroad.

In 2018, Nigerian payment startup Paga announced plans to move into Asia and Latin America after raising $10 million. In 2019, South African tech-transit startup FlexClub partnered with Uber Mexico after a seed raise. And Lagos-based fintech startup TeamAPT announced in Q1 it was looking to expand globally after a $5 million Series A round.

Powered by WPeMatico

Cytora, a U.K. startup that developed an AI-powered solution for commercial insurance underwriting, has raised £25 million in a Series B round. Leading the investment is EQT Ventures, with participation from existing investors Cambridge Innovation Capital, Parkwalk and a number of unnamed angel investors.

A spin-out of the University of Cambridge, Cytora was founded in 2014 by Richard Hartley, Aeneas Wiener, Joshua Wallace and Andrzej Czapiewski — although both Wallace and Czapiewski have since departed.

Its first product launched in late 2016 to a number of large insurance customers, with the aim of applying AI to commercial insurance supported by various public and proprietary data. This includes property construction features, company financials and local weather, combined with an insurance company’s own internal risk data.

“Commercial insurance underwriting is inaccurate and inefficient,” says Cytora co-founder and CEO Richard Hartley. “It’s inaccurate because underwriting decisions are made using sparse and outdated information. It’s inefficient because the underwriting process is so manual. Unlike buying car or travel insurance, which can be purchased in minutes, buying business insurance can take up to seven days. This means operating costs for insurers are extremely high and customer experience isn’t good leading to a lack of trust.”

To illustrate how inefficient commercial insurance can be, Hartley says that for every £1 of premium that businesses pay to insurers, only 60 pence is set aside to pay total claims. The other 40 pence evaporates as the “frictional cost of delivering insurance.”

Powered by AI, Hartley claims that Cytora is able to distill the seven-day underwriting process down to 30 seconds via its API. This enables insurers to underwrite programmatically and build workflows that provide faster and more accurate decisions.

“Our APIs are powered by a risk engine which learns the subtle patterns of good and bad risks over time,” he explains. “This gives insurers a better understanding of the underlying risk of each business and helps them set a more accurate price. Both customers and insurers benefit.”

Typical Cytora customers are commercial insurers that are digitally transforming their underwriting process. Users of the software are either underwriters within insurance companies who are underwriting large commercial risks (i.e. an average insurance premium ~£500k and above) or business customers of insurance companies who are buying insurance direct online with an average premium of £1,000-£5,000.

“For the latter, our customers have built quotation workflows on top of Cytora’s APIs, enabling business owners to buy policies online in less than a minute without having to fill in a form,” says Hartley. “We require only a business name and postcode to issue a quote, which revolutionises the customer experience.”

To that end, Cytora generates revenue by charging a yearly ARR license fee, which increases based on usage and per line of business. The company says today’s Series B funding will be used to accelerate the expansion of its product suite and for scaling into new geographies.

Powered by WPeMatico

Redpoint Ventures has led a $65 million Series B in Cityblock, a healthcare company focused on providing improved care to low-income neighborhoods.

The business launched roughly 18 months ago out of Alphabet’s Sidewalk Labs, an urban innovation incubator known for projects like mobility data startup Coord, which itself raised a $5 million round in October.

“We’re a tech-enabled services company focused on caring for a population that has been traditionally overlooked by the innovation community and generally underserved across healthcare,” co-founder and chief executive officer Iyah Romm told TechCrunch. “We believe we can fundamentally redefine the way that health services are built across the country for low-income populations. These are populations that have never been prioritized.”

Romm has spent his entire career in the public health sector. Prior to joining Sidewalk Labs as an entrepreneur-in-residence in 2017, he spent one year as the chief transformation officer of the Commonwealth Care Alliance, a nonprofit medical care delivery organization.

Cityblock provides personalized medical and behavioral health and social services across a growing number of clinics on the East Coast. The company will use the investment to open additional clinics and continue the development of its core platform, Commons. The care delivery platform helps care workers collaborate and stay up to date on patients, with real-time hospital admission alerts to tools for tracking treatment progress.

Cityblock opened its first clinic, or “neighborhood hub,” in Brooklyn, New York after forging a partnership with EmblemHealth, a New York neighborhood health insurance business. They’ve since expanded to Connecticut via a partnership with ConnectiCare, a Connecticut insurance provider. Cityblock will open clinics in North Carolina later this year. Cityblock’s services come at no additional costs to members covered by partner insurance businesses.

The startup’s hope is to get these low-income demographics regular access to more affordable care. Preventative care, after all, is a whole lot cheaper than emergency room visits.

“People end up going to the ER when problems are really bad, for conditions that can be managed,” Redpoint partner and newly appointed Cityblock board member Elliot Geidt told TechCrunch. “There are 75 million people on Medicaid alone and a good portion of these people are living in the inner cities. It’s a problem that has a scope larger than most things that we see in the venture community. The big problem with this population is the existing healthcare system doesn’t work for them, it falls short on so many levels.”

New investors 8VC, Echo Health Ventures and StartUp Health also participated in the latest round, as did existing investors including Sidewalk Labs, Thrive Capital, Maverick Ventures, Town Hall Ventures and EmblemHealth.

Powered by WPeMatico

Pitched as “travel insurance for people who don’t like insurance,” U.K.-based Pluto Insurance is officially launching today with an online travel insurance product targeting millennials.

Citing research that says 40 percent of millennials don’t actually buy travel insurance, mistakenly believing that it isn’t required, the mobile-first offering not only attempts to demystify travel insurance, but is also unbundling it in a way that ensures you only pay for the cover you need or desire.

“We’ve spoken to hundreds of millennials and three things keep coming up,” says Pluto co-founder and CEO Alex Rainey. “Travel insurance is too complicated and it’s hard to know what you’re actually buying. Secondly, a lot of younger people don’t think they need it. But most importantly, there is a distinct lack of trust towards insurers, and it’s easy to see why. With exclusions buried in the fine print and insurers expecting people to print out a claim form and post it in.”

To remedy this, Rainey says Pluto wants to make travel insurance more tailored, letting you build your own policy online. “We work hard to make sure everything is easy to understand, ensuring we always explain our cover in plain English,” he says. The startup also lets you submit a claim via the mobile web app “in under 10 minutes.”

Insurance options includes gadget cover, baggage cover, cancellation cover, level of excess, cover for certain activities and travel disruption. As you add more cover, the price of your insurance changes in real time with each decision. Once you’ve built your policy, a short summary of your cover is displayed before you go ahead and purchase.

Meanwhile, the insurance itself — which, at launch, doesn’t cover pre-existing conditions, although that will be offered in the future — is in partnership with Zurich, which Rainey says was chosen because they had a 99 percent claims payout rate in 2017. “This is so so important for us to solve the trust issues in insurance,” he adds.

To that end, Pluto integrates with Facebook Messenger, including letting you use the messaging app to start a claim. You can also search your policy, check a summary of your cover or chat to a Pluto team member.

“Our customers want to do everything from their phone, when and where they want. We’ve made sure that’s possible,” says Rainey.

Powered by WPeMatico