insurance

Auto Added by WPeMatico

Auto Added by WPeMatico

This morning, Anna Heim and Alex Wilhelm dug into the EU insurtech market, interviewing European VCs and collating the biggest recent rounds to take the temperature of the waters across the pond:

Several European-based insurtech startups entered unicorn territory this year, such as Bought By Many, which offers pet insurance; London-based Zego; and Alan, a French startup that raised a $220 million round.

According to Brittain, EU startups in this sector are “still at the very early stages of innovation,” having only shown “a fraction of what’s possible” in a market that is “as large as banking.” Interestingly, he predicted that AI will play a larger role in the future as companies deploy it for fraud detection, improved customer experiences and processing claims more quickly.

“We are fully expecting the next generation of AI-driven business to unlock real-time risk analysis, pricing and claims resolution in the next few years,” he said.

Thanks very much for reading Extra Crunch; I hope you have a safe, relaxing weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman (opens in a new window)

Earlier this week, The Exchange assessed the looming Monday.com IPO before reading the tea leaves about that flotation and three others to sum up the overall state of the market.

So what do the Marqeta, Monday.com, Zeta Global and 1stDibs debuts tell us? We may have been too conservative.

Image Credits: Bessemer Venture Partners / Toast

On a recent episode of Extra Crunch Live, we spoke to Toast founder Aman Narang and Kent Bennett of Bessemer Venture Partners about how they came together for a deal, what makes the difference for both founders and investors when fundraising, and the biggest lessons they’ve learned so far.

The episode also featured the Extra Crunch Live Pitch-Off, where audience members pitched their products to Bennett and Narang and received live feedback.

Extra Crunch Live is open to everyone each Wednesday at 3 p.m. EDT/noon PDT, but only Extra Crunch members are able to stream these sessions afterward and watch previous shows on-demand in our episode library.

Image Credits: Nigel Sussman (opens in a new window)

Alex Wilhelm and Anna Heim solicited feedback from investors to get a temperature on the market for AI startup investments.

“The startup investing market is crowded, expensive and rapid-fire today as venture capitalists work to preempt one another, hoping to deploy funds into hot companies before their competitors,” they write. “The AI startup market may be even hotter than the average technology niche.”

But that’s not surprising. The Exchange was on it.

“In the wake of the Microsoft-Nuance deal, The Exchange reported that it would be reasonable to anticipate an even more active and competitive market for AI-powered startups,” Alex and Anna note. “Our thesis was that after Redmond dropped nearly $20 billion for the AI company, investors would have a fresh incentive to invest in upstarts with an AI focus or strong AI component; exits, especially large transactions, have a way of spurring investor interest in related companies.”

Their expectation is coming true: Investors reported a fierce market for AI startups.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

I started a tech company about two years ago, and ever since I’ve dreamed of expanding my company in the United States.

I would love to have a green card. Someone mentioned that I should apply for a diversity green card. Would you please provide me with more details about it and how to apply?

— Technical in Tanzania

Image Credits: MediaProduction (opens in a new window) / Getty Images

Pulley founder and three-time YC alum Yin Wu offers a tactical guide to getting a startup running in four days. Yes, just four days.

“The logistics of setting up a startup should be simple, because over the long run, complicated equity setups and cap tables cost more money in legal fees and administration time,” Wu notes.

Read on for guidance on how to get your business going in less than a week.

Image Credits: Natali_Mis / Getty Images

Innovaccer founder and CEO Abhinav Shashank and CTO Mike Sutten write in a guest column that the U.S. healthcare industry is in the middle of a massive transformation.

This shift, they write, “is being stimulated by federal mandates, technological innovation, and the need to improve clinical outcomes and communication between providers, patients and payers.”

Improving healthcare now means we need to process tremendous amounts of healthcare data. How do we do it? The cloud, which “plays a pivotal role in meeting the current needs of healthcare organizations.”

Image Credits: MrJub / Getty Images

SOSV’s Benjamin Joffe and Meghan Hind round up a “who’s who” from the venture capital firm’s SOSV Climate Tech 100, a list of the best startups addressing climate change that SOSV has supported from the very beginning.

“What can founders learn from the list about climate tech investors? In other words, who invested in the Climate Tech 100?” they ask.

Image Credits: Donald Iain Smith (opens in a new window) / Getty Images

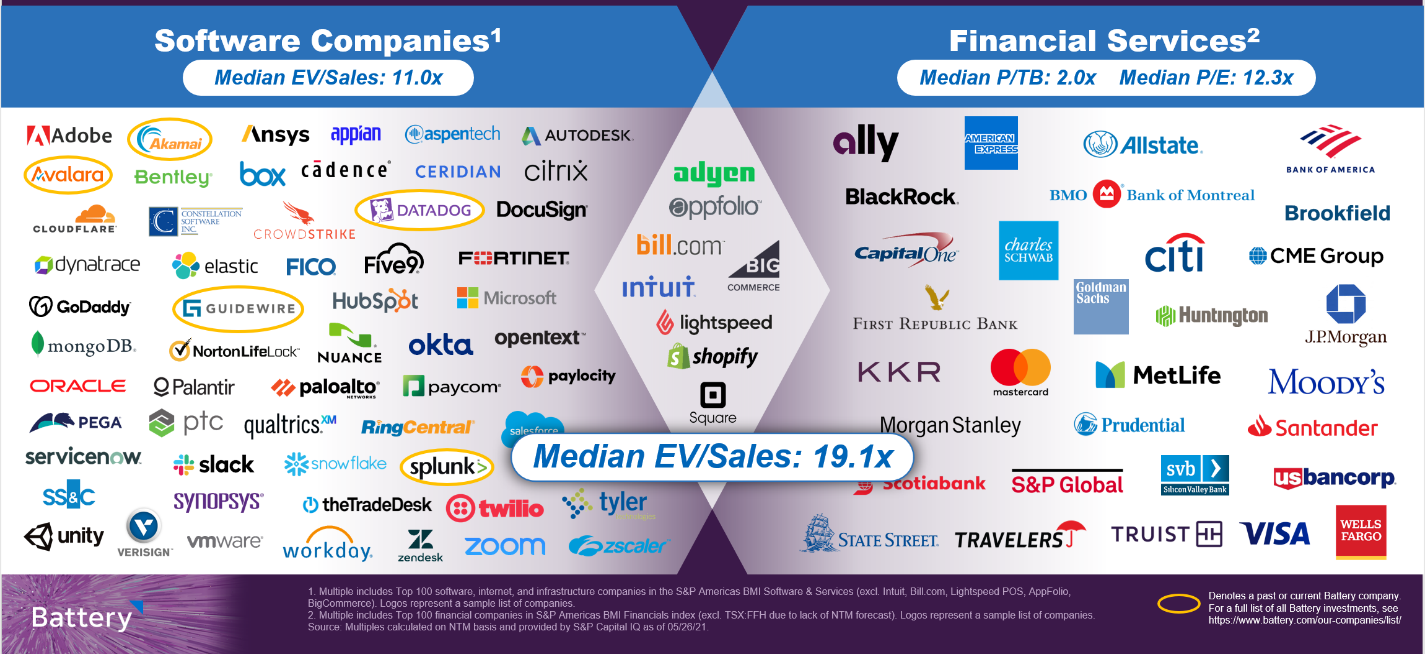

Now that we can transact from anywhere, a new, hybrid class of software companies with embedded financial services are scooping up consumers — and investors are following the action.

Using data from a Battery Ventures report about “the intersection of software and financial services,” this post examines why these companies can be so hard to value and offers a framework for better understanding their business models and investor appeal.

Image Credits: Grant Faint (opens in a new window) / Getty Images

Geoffrey Moore’s “Chasm,” a framework for marketing technology products that has been one of the canonical foundational concepts to product-market fit for three decades, needs a bit of an upgrade, Flybridge Capital’s Jeff Bussgang writes.

“I have been reflecting on why it is that we venture capitalists and founders keep making the same mistake over and over again — a mistake that has become even more glaring in recent years,” he writes.

Bussgang goes on to consider the Chasm — and propose tweaks for thinking about market size in the modern era.

Powered by WPeMatico

If money is the ultimate commodity, how can fintechs — which sell money, move money or sell insurance against monetary loss — build products that remain differentiated and create lasting value over time?

And why are so many software companies — which already boast highly differentiated offerings and serve huge markets— moving to offer financial services embedded within their products?

A new and attractive hybrid category of company is emerging at the intersection of software and financial services, creating buzz in the investment and entrepreneurial communities, as we discussed at our “Fintech: The Endgame” virtual conference and accompanying report this week.

These specialized companies — in some cases, software companies that also process payments and hold funds on behalf of their customers, and in others, financial-first companies that integrate workflow and features more reminiscent of software companies — combine some of the best attributes of both categories.

Image Credits: Battery Ventures

From software, they design for strong user engagement linked to helpful, intuitive products that drive retention over the long term. From financials, they draw on the ability to earn revenues indexed to the growth of a customer’s business.

Fintech is poised to revolutionize financial services, both through reinventing existing products and driving new business models as financial services become more pervasive within other sectors.

The powerful combination of these two models is rapidly driving both public and private market value as investors grant these “super” companies premium valuations — in the public sphere, nearly twice the median multiple of pure software companies, according to a Battery analysis.

The near-perfect example of this phenomenon is Shopify, the company that made its name selling software to help business owners launch and manage online stores. Despite achieving notable scale with this original SaaS product, Shopify today makes twice as much revenue from payments as it does from software by enabling those business owners to accept credit card payments and acting as its own payment processor.

The combination of a software solution indexed to e-commerce growth, combined with a profitable payments stream growing even faster than its software revenues, has investors granting Shopify a 31x multiple on its forward revenues, according to CapIQ data as of May 26.

Before even talking about how investors should value these hybrid companies, it’s worth making the point that in both private and public markets, fintechs have been notoriously hard to value, fomenting controversy and debate in the investment community.

Powered by WPeMatico

Here in the U.S. the concept of using a driver’s data to decide the cost of auto insurance premiums is not a new one.

But in markets like Brazil, the idea is still considered relatively novel. A new startup called Justos claims it will be the first Brazilian insurer to use drivers’ data to reward those who drive safely by offering “fairer” prices.

And now Justos has raised about $2.8 million in a seed round led by Kaszek, one of the largest and most active VC firms in Latin America. Big Bets also participated in the round, along with the CEOs of seven unicorns, including Assaf Wand, CEO and co-founder of Hippo Insurance; David Vélez, founder and CEO of Nubank; Carlos Garcia, founder and CEO of Kavak; Sergio Furio, founder and CEO of Creditas; Patrick Sigrist, founder of iFood and Fritz Lanman, CEO of ClassPass. (There’s a seventh CEO who wishes to remain anonymous). Senior executives from Robinhood, Stripe, Wise, Carta and Capital One also put money in the round.

Serial entrepreneurs Dhaval Chadha, Jorge Soto Moreno and Antonio Molins co-founded Justos, having most recently worked at various Silicon Valley-based companies including ClassPass, Netflix and Airbnb.

“While we have been friends for a while, it was a coincidence that all three of us were thinking about building something new in Latin America,” Chadha said. “We spent two months studying possible paths, talking to people and investors in the United States, Brazil and Mexico, until we came up with the idea of creating an insurance company that can modernize the sector, starting with auto insurance.”

Ultimately, the trio decided that the auto insurance market would be an ideal sector considering that in Brazil, an estimated more than 70% of cars are not insured.

The process to get insurance in the country, by any accounts, is a slow one. It takes up to 72 hours to receive initial coverage and two weeks to receive the final insurance policy. Insurers also take their time in resolving claims related to car damages and loss due to accidents, the entrepreneurs say. They also charge that pricing is often not fair or transparent.

Justos aims to improve the whole auto insurance process in Brazil by measuring the way people drive to help price their insurance policies. Similar to Root here in the U.S., Justos intends to collect users’ data through their mobile phones so that it can “more accurately and assertively price different types of risk.” This way, the startup claims it can offer plans that are up to 30% cheaper than traditional plans, and grant discounts each month, according to the driving patterns of the previous month of each customer.

“We measure how safely people drive using the sensors on their cell phones,” Chadha said. “This allows us to offer cheaper insurance to users who drive well, thereby reducing biases that are inherent in the pricing models used by traditional insurance companies.”

Justos also plans to use artificial intelligence and computerized vision to analyze and process claims more quickly and machine learning for image analysis and to create bots that help accelerate claims processing.

“We are building a design-driven, mobile first and customer experience that aims to revolutionize insurance in Brazil, similar to what Nubank did with banking,” Chadha told TechCrunch. “We will be eliminating any hidden fees, a lot of the small text and insurance-specific jargon that is very confusing for customers.”

Justos will offer its product directly to its customers as well as through distribution channels like banks and brokers.

“By going direct to consumer, we are able to acquire users cheaper than our competitors and give back the savings to our users in the form of cheaper prices,” Chadha said.

Customers will be able to buy insurance through Justos’ app, website or even WhatsApp. For now, the company is only adding potential customers to a waitlist but plans to begin selling policies later this year..

During the pandemic, the auto insurance sector in Brazil declined by 1%, according to Chadha, who believes that indicates “there is latent demand raring to go once things open up again.”

Justos has a social good component as well. Justos intends to cap its profits and give any leftover revenue back to nonprofit organizations.

The company also has an ambitious goal: to help make insurance become universally accessible around the world and the roads safer in general.

“People will face everyday risks with a greater sense of safety and adventure. Road accidents will reduce drastically as a result of incentives for safer driving, and the streets will be safer,” Chadha said. “People, rather than profits, will become the focus of the insurance industry.”

Justos plans to use its new capital to set up operations, such as forming partnerships with reinsurers and an insurance company for fronting, since it is starting as an MGA (managing general agent).

It’s also working on building out its products such as apps, its back end and internal operations tools, as well as designing all its processes for underwriting, claims and finance. Justos’ data science team is also building out its own pricing model.

The startup will be focused on Brazil, with plans to eventually expand within Latin America, then Iberia and Asia.

Kaszek’s Andy Young said his firm was impressed by the team’s previous experience and passion for what they’re building.

“It’s a huge space, ripe for innovation and this is the type of team that can take it to the next level,” Young told TechCrunch. “The team has taken an approach to building an insurance platform that blends being consumer-centric and data-driven to produce something that is not only cheaper and rewards safety but as the brand implies in Portuguese, is fairer.”

Powered by WPeMatico

An estimated 41 million Americans say they need life insurance but have yet to purchase coverage. Despite this awareness among consumers, the Life Insurance Marketing and Research Association estimates a $12 trillion coverage gap, with about 50% of millennials planning to purchase coverage within the next year.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution. It’s imperative for companies to consider product lines and partnerships to expand markets, create new revenue streams and provide added value to their customers.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution.

Connecting consumers with products they need through channels they already know and trust is both a massive revenue opportunity and a social good, providing financial resilience to families at a time when they need it most.

The concept of digitally bundling financial products in a packaged offering to a customer is certainly not new — but it is for the life insurance space.

Embedded finance uses technology and operations infrastructure to offer products and services through entities that may not be financial institutions at all. Think of embedded finance like on-demand shopping; customers benefit from both the transaction (buying financial protection for their families) and the convenience it provides (from whatever platform they are currently engaging with).

Similar to how Amazon saves shoppers 75 hours a year, bundling life insurance gives consumers back time in their day and can improve their financial health.

Powered by WPeMatico

Telemedicine, in its original form of the phone call, has been around for decades. For people in remote or rural areas without easy access to in-person care, consulting a doctor over the phone has often been the go-to approach. But for a large swath of the world used to taking half a day off work just for a 15-30 minute doctor’s appointment, it may seem like telemedicine was invented only last year. That’s mostly because it wasn’t until 2020 that telemedicine, in its myriad forms, debuted into the mainstream consciousness.

It’s impossible to predict how healthcare institutions will operate post-pandemic, but with so many people now accustomed to telemedicine, startups that provide services around virtual care continue to be poised for success.

Telemedicine has faced an uphill battle to become more relevant in the U.S., with challenges such as meeting HIPPA compliance requirements and insurance companies unwilling to pay for virtual visits. But when COVID-19 began raging across the globe and people had to stay home, both the insurance and healthcare industries were forced to adapt.

“It’s been said that there are decades where nothing happens, and then there are weeks when decades happen,” said StartUp Health co-founders Steven Krein and Unity Stoakes in the company’s 2020 year-end report. That statement couldn’t be truer for telemedicine: Around $3.1 billion in funding flowed into the sector in 2020 — about three times what we saw in 2019, according to the report. A health tech fund and insights company, StartUp Health counts Alphabet, Sequoia and Andreessen Horowitz as some of its co-investors.

Now that people see the benefits and conveniences of “dialing a doc” from the kitchen table, healthcare has changed forever. It’s impossible to predict how healthcare institutions will operate post-pandemic, but with so many people now accustomed to telemedicine, startups that provide services around virtual care continue to be poised for success.

Major players in the field now look at the state of healthcare as, “before COVID and after COVID,” Stoakes told Extra Crunch. “In the post-pandemic world, there’s a significant transformation that’s occurred,” he said. “It’s all accelerated; the customers have shown up. There’s more capital than ever and consumers and physicians have adapted quickly,” he added.

In the U.S., healthcare is first and foremost a business, so while there are treatment approaches that have long been proven to improve patient outcomes, if they didn’t make sense financially, they weren’t instituted at scale. Telemedicine is a great example of this.

A 2017 study by the American Journal of Accountable Care showed that telemedicine can be quite useful for managing healthcare. “The use of telemedicine has been shown to allow for better long-term care management and patient satisfaction; it also offers a new means to locate health information and communicate with practitioners (e.g., via e-mail and interactive chats or video conferences), thereby increasing convenience for the patient and reducing the amount of potential travel required for both physician and patient,” the study reads.

But as we’ve seen, it took a global healthcare emergency to drive widespread adoption of virtual healthcare in the U.S. Now that investors recognize the potential, they are increasingly pouring money into startups that promise to take telemedicine to the next level. Some of the investors backing these newer companies include StartUp Health, Andreessen Horowitz, Sequoia, Alphabet, Kaiser Permanente Ventures, U.S. Venture Partners, Maveron, First Round Capital, DreamIt Ventures, Human Ventures and Tusk Venture Partners.

Powered by WPeMatico

When disaster strikes, costs pile up quickly. Flood waters can wipe out the foundation of a home or building, just as much as wildfires can burn down the walls or the entire structure. For residents and business owners, rebuilding and rebuilding quickly is crucial: They ultimately need some place to live and offer services, and they often can’t afford to be shut out for extended periods of time.

Of course, the need for speed among consumers hits the brick wall that is the insurance industry and government’s timeline for dispersing post-disaster insurance claims and aid. It’s not uncommon for federal aid to take months or even years to arrive, and insurance companies can often take months as well to process claims, particularly after large disasters like hurricanes where thousands of claims arrive simultaneously.

Dorothy is a startup that is aiming to bridge the gap by offering, well, gap loans to users who already have existing private insurance or federal flood insurance policies. The idea is to extend cash as quickly as possible after qualification, and then Dorothy gets paid back when a claim is later processed. Much like other advance cash startups in other sectors, Dorothy takes a fee based on the size of the loan.

The company’s underwriting model assesses the likelihood that a claim will be approved given the details of a particular disaster and the user’s insurance policy.

Arianna Armelli and Claudio Angrigiani founded the company last year in the midst of the COVID-19 pandemic, naming it for the character from the “Wizard of Oz” who repeatedly said “there’s no place like home.” They met each other in graduate school at the University of Pennsylvania and explored different ways to solve the challenges of disaster finance.

Armelli, for her part, had experienced these challenges firsthand in the wake of Hurricane Sandy in 2012. She was an architect, and her office in Manhattan had to be evacuated. She returned a few days later, but over time, realized that many of her friends still couldn’t return to their homes even weeks after the hurricane had passed. She volunteered with recovery efforts, and “went house to house in the Rockaways to remove drywall from their basements,” she said.

She continued her career, spending nearly six years as an architect and urban planner, and that training drove some of her early ideas about how to improve post-disaster recovery. “I thought the answer to these problems was designing better infrastructure and long-term sustainable solutions with planning,” she said. “After six years in planning, [I] realized these were 40-year projects.”

After meeting Angrigiani, the two explored ways to make the insurance system better for end users. They began by investigating how better flood data could help insurance companies underwrite better policies and process claims faster. They realized over time though that the insurance industry was quite sclerotic, and that a third-party provider of better flood predictive data wasn’t going to have a large impact on outcomes.

As COVID bared down on the world, they then explored business interruption insurance. Using their technology for disaster prediction, they saw an opportunity to offer “a financial supplementary product for businesses,” essentially a “credit line product that is offered to commercial business owners similar to a credit card,” Armelli said. That idea eventually morphed into the company’s current product offering targeting property owners, both businesses and individuals, with the same sort of gap loan to solve immediate cash-flow problems.

Dorothy participated in the latest cohort of Urban-X and closed a pre-seed round this past February. The company has raised a $250,000 debt facility to further test out its gap loan product, and it has 25 qualified customers in its pipeline. It’s early days, but it’s an interesting new bet on how to make insurance actually useful when people face some of the toughest moments of their lives.

It’s just one of a new crop of startups that are building new offerings in a world increasingly filled with massive disasters.

Powered by WPeMatico

Planck co-founders (from left to right): David Schapiro, CEO Elad Tsur and CTO Amir Cohen. Image Credits: Planck

Planck, the AI-based data platform for commercial insurance underwriting, announced today it has raised a $20 million growth round. The funding came from 3L Capital and Greenfield Partners, along with returning investors Team8, Viola Fintech, Arbor Ventures and Eight Roads.

This brings the New York-based startup’s total raised to $48 million, including a $16 million Series B it announced in June 2020. Planck said it currently works with “dozens of commercial insurance companies in the U.S.,” including more than half of the top-30 insurers. It will use its new funding to build its U.S. team, expand into global markets and add products for new business segments. Ernie Feirer has also joined Planck as its head of U.S. business. He previously held leadership roles at LexisNexis Risk Solutions, building data analytics solutions for property and casualty insurance carriers.

Planck’s database, which includes online images, text, videos, reviews and public records, allows it to give insurance providers real-time information that helps them determine premiums, process claims and give SMEs faster quotes. It covers more than 50 business segments, including restaurants, construction, retail and manufacturing, and can deliver analytics by simply entering a business’ name and address.

For example, if a healthcare business is seeking to buy or renew an insurance policy, Planck can give underwriters information such as the type of equipment used, what kind of drugs it prescribes and the type of surgeries it performs.

In a statement, 3L Capital principal Paige Thacher said, “Commercial carriers and brokers can no longer afford to rely upon traditional data sources as they prospect, assess risk and monitor a small business insured’s changing exposure during the policy life cycle. The new imperative is to leverage AI and machine learning technologies to dynamically harvest business insights from the insured’s digital footprint.”

Powered by WPeMatico

Sensor data from smartphones and wearables can meaningfully predict an individual’s ‘biological age’ and resilience to stress, according to Gero AI.

The ‘longevity’ startup — which condenses its mission to the pithy goal of “hacking complex diseases and aging with Gero AI” — has developed an AI model to predict morbidity risk using ‘digital biomarkers’ that are based on identifying patterns in step-counter sensor data which tracks mobile users’ physical activity.

A simple measure of ‘steps’ isn’t nuanced enough on its own to predict individual health, is the contention. Gero’s AI has been trained on large amounts of biological data to spots patterns that can be linked to morbidity risk. It also measures how quickly a personal recovers from a biological stress — another biomarker that’s been linked to lifespan; i.e. the faster the body recovers from stress, the better the individual’s overall health prognosis.

A research paper Gero has had published in the peer-reviewed biomedical journal Aging explains how it trained deep neural networks to predict morbidity risk from mobile device sensor data — and was able to demonstrate that its biological age acceleration model was comparable to models based on blood test results.

Another paper, due to be published in the journal Nature Communications later this month, will go into detail on its device-derived measurement of biological resilience.

The Singapore-based startup, which has research roots in Russia — founded back in 2015 by a Russian scientist with a background in theoretical physics — has raised a total of $5 million in seed funding to date (in two tranches).

Backers come from both the biotech and the AI fields, per co-founder Peter Fedichev. Its investors include Belarus-based AI-focused early stage fund, Bulba Ventures (Yury Melnichek). On the pharma side, it has backing from some (unnamed) private individuals with links to Russian drug development firm, Valenta. (The pharma company itself is not an investor).

Fedichev is a theoretical physicist by training who, after his PhD and some ten years in academia, moved into biotech to work on molecular modelling and machine learning for drug discovery — where he got interested in the problem of ageing and decided to start the company.

As well as conducting its own biological research into longevity (studying mice and nematodes), it’s focused on developing an AI model for predicting the biological age and resilience to stress of humans — via sensor data captured by mobile devices.

“Health of course is much more than one number,” emphasizes Fedichev. “We should not have illusions about that. But if you are going to condense human health to one number then, for a lot of people, the biological age is the best number. It tells you — essentially — how toxic is your lifestyle… The more biological age you have relative to your chronological age years — that’s called biological acceleration — the more are your chances to get chronic disease, to get seasonal infectious diseases or also develop complications from those seasonal diseases.”

Gero has recently launched a (paid, for now) API, called GeroSense, that’s aimed at health and fitness apps so they can tap up its AI modelling to offer their users an individual assessment of biological age and resilience (aka recovery rate from stress back to that individual’s baseline).

Early partners are other longevity-focused companies, AgelessRx and Humanity Inc. But the idea is to get the model widely embedded into fitness apps where it will be able to send a steady stream of longitudinal activity data back to Gero, to further feed its AI’s predictive capabilities and support the wider research mission — where it hopes to progress anti-ageing drug discovery, working in partnerships with pharmaceutical companies.

The carrot for the fitness providers to embed the API is to offer their users a fun and potentially valuable feature: A personalized health measurement so they can track positive (or negative) biological changes — helping them quantify the value of whatever fitness service they’re using.

“Every health and wellness provider — maybe even a gym — can put into their app for example… and this thing can rank all their classes in the gym, all their systems in the gym, for their value for different kinds of users,” explains Fedichev.

“We developed these capabilities because we need to understand how ageing works in humans, not in mice. Once we developed it we’re using it in our sophisticated genetic research in order to find genes — we are testing them in the laboratory — but, this technology, the measurement of ageing from continuous signals like wearable devices, is a good trick on its own. So that’s why we announced this GeroSense project,” he goes on.

“Ageing is this gradual decline of your functional abilities which is bad but you can go to the gym and potentially improve them. But the problem is you’re losing this resilience. Which means that when you’re [biologically] stressed you cannot get back to the norm as quickly as possible. So we report this resilience. So when people start losing this resilience it means that they’re not robust anymore and the same level of stress as in their 20s would get them [knocked off] the rails.

“We believe this loss of resilience is one of the key ageing phenotypes because it tells you that you’re vulnerable for future diseases even before those diseases set in.”

“In-house everything is ageing. We are totally committed to ageing: Measurement and intervention,” adds Fedichev. “We want to building something like an operating system for longevity and wellness.”

Gero is also generating some revenue from two pilots with “top range” insurance companies — which Fedichev says it’s essentially running as a proof of business model at this stage. He also mentions an early pilot with Pepsi Co.

He sketches a link between how it hopes to work with insurance companies in the area of health outcomes with how Elon Musk is offering insurance products to owners of its sensor-laden Teslas, based on what it knows about how they drive — because both are putting sensor data in the driving seat, if you’ll pardon the pun. (“Essentially we are trying to do to humans what Elon Musk is trying to do to cars,” is how he puts it.)

But the nearer term plan is to raise more funding — and potentially switch to offering the API for free to really scale up the data capture potential.

Zooming out for a little context, it’s been almost a decade since Google-backed Calico launched with the moonshot mission of ‘fixing death’. Since then a small but growing field of ‘longevity’ startups has sprung up, conducting research into extending (in the first instance) human lifespan. (Ending death is, clearly, the moonshot atop the moonshot.)

Death is still with us, of course, but the business of identifying possible drugs and therapeutics to stave off the grim reaper’s knock continues picking up pace — attracting a growing volume of investor dollars.

The trend is being fuelled by health and biological data becoming ever more plentiful and accessible, thanks to open research data initiatives and the proliferation of digital devices and services for tracking health, set alongside promising developments in the fast-evolving field of machine learning in areas like predictive healthcare and drug discovery.

Longevity has also seen a bit of an upsurge in interest in recent times as the coronavirus pandemic has concentrated minds on health and wellness, generally — and, well, mortality specifically.

Nonetheless, it remains a complex, multi-disciplinary business. Some of these biotech moonshots are focused on bioengineering and gene-editing — pushing for disease diagnosis and/or drug discovery.

Plenty are also — like Gero — trying to use AI and big data analysis to better understand and counteract biological ageing, bringing together experts in physics, maths and biological science to hunt for biomarkers to further research aimed at combating age-related disease and deterioration.

Another recent example is AI startup Deep Longevity, which came out of stealth last summer — as a spinout from AI drug discovery startup Insilico Medicine — touting an AI ‘longevity as a service’ system which it claims can predict an individual’s biological age “significantly more accurately than conventional methods” (and which it also hopes will help scientists to unpick which “biological culprits drive aging-related diseases”, as it put it).

Gero AI is taking a different tack toward the same overarching goal — by honing in on data generated by activity sensors embedded into the everyday mobile devices people carry with them (or wear) as a proxy signal for studying their biology.

The advantage being that it doesn’t require a person to undergo regular (invasive) blood tests to get an ongoing measure of their own health. Instead our personal device can generate proxy signals for biological study passively — at vast scale and low cost. So the promise of Gero’s ‘digital biomarkers’ is they could democratize access to individual health prediction.

And while billionaires like Peter Thiel can afford to shell out for bespoke medical monitoring and interventions to try to stay one step ahead of death, such high end services simply won’t scale to the rest of us.

If its digital biomarkers live up to Gero’s claims, its approach could, at the least, help steer millions towards healthier lifestyles, while also generating rich data for longevity R&D — and to support the development of drugs that could extend human lifespan (albeit what such life-extending pills might cost is a whole other matter).

The insurance industry is naturally interested — with the potential for such tools to be used to nudge individuals towards healthier lifestyles and thereby reduce payout costs.

For individuals who are motivated to improve their health themselves, Fedichev says the issue now is it’s extremely hard for people to know exactly which lifestyle changes or interventions are best suited to their particular biology.

For example fasting has been shown in some studies to help combat biological ageing. But he notes that the approach may not be effective for everyone. The same may be true of other activities that are accepted to be generally beneficial for health (like exercise or eating or avoiding certain foods).

Again those rules of thumb may have a lot of nuance, depending on an individual’s particular biology. And scientific research is, inevitably, limited by access to funding. (Research can thus tend to focus on certain groups to the exclusion of others — e.g. men rather than women; or the young rather than middle aged.)

This is why Fedichev believes there’s a lot of value in creating a measure than can address health-related knowledge gaps at essentially no individual cost.

Gero has used longitudinal data from the UK’s biobank, one of its research partners, to verify its model’s measurements of biological age and resilience. But of course it hopes to go further — as it ingests more data.

“Technically it’s not properly different what we are doing — it just happens that we can do it now because there are such efforts like UK biobank. Government money and also some industry sponsors money, maybe for the first time in the history of humanity, we have this situation where we have electronic medical records, genetics, wearable devices from hundreds of thousands of people, so it just became possible. It’s the convergence of several developments — technological but also what I would call ‘social technologies’ [like the UK biobank],” he tells TechCrunch.

“Imagine that for every diet, for every training routine, meditation… in order to make sure that we can actually optimize lifestyles — understand which things work, which do not [for each person] or maybe some experimental drugs which are already proved [to] extend lifespan in animals are working, maybe we can do something different.”

“When we will have 1M tracks [half a year’s worth of data on 1M individuals] we will combine that with genetics and solve ageing,” he adds, with entrepreneurial flourish. “The ambitious version of this plan is we’ll get this million tracks by the end of the year.”

Fitness and health apps are an obvious target partner for data-loving longevity researchers — but you can imagine it’ll be a mutual attraction. One side can bring the users, the other a halo of credibility comprised of deep tech and hard science.

“We expect that these [apps] will get lots of people and we will be able to analyze those people for them as a fun feature first, for their users. But in the background we will build the best model of human ageing,” Fedichev continues, predicting that scoring the effect of different fitness and wellness treatments will be “the next frontier” for wellness and health (Or, more pithily: “Wellness and health has to become digital and quantitive.”)

“What we are doing is we are bringing physicists into the analysis of human data. Since recently we have lots of biobanks, we have lots of signals — including from available devices which produce something like a few years’ long windows on the human ageing process. So it’s a dynamical system — like weather prediction or financial market predictions,” he also tells us.

“We cannot own the treatments because we cannot patent them but maybe we can own the personalization — the AI that personalized those treatments for you.”

From a startup perspective, one thing looks crystal clear: Personalization is here for the long haul.

Powered by WPeMatico

While incumbent insurance providers continue to get disrupted by startups like Lemonade, Alan, Clearcover, Pie and many others applying tech to rethink how to build a business around helping people and companies mitigate against risks with some financial security, one issue that has not disappeared is fraud. Today, a startup out of France is announcing some funding for AI technology that it has built for all insurance providers, old and new, to help them detect and prevent it.

Shift Technology, which provides a set of AI-based SaaS tools to insurance companies to scan and automatically flag fraud scenarios across a range of use cases — they include claims fraud, claims automation, underwriting, subrogation detection and financial crime detection — has raised $220 million, money that it will be using both to expand in the property and casualty insurance market, the area where it is already strong, as well as to expand into health, and to double down on growing its business in the U.S. It also provides fraud detection for the travel insurance sector.

This Series D is being led by Advent International, via Advent Tech, with participation from Avenir and others. Accel, Bessemer Venture Partners, General Catalyst and Iris Capital — who were all part of Shift’s Series C led by Bessemer in 2019 — also participated. With this round, Paris-and-Boston-based Shift Technology has now raised some $320 million and has confirmed that it is now valued at over $1 billion.

The company currently has around 100 customers across 25 different countries — with the list including Generali France and Mitsui Sumitomo, to give you an idea of where it’s pitching its business — and says that it has already analyzed nearly two billion claims, data that’s feeding its machine learning algorithms to improve how they work.

The challenge (or I suppose, opportunity) that Shift is tackling, however, is much bigger. The Coalition Against Insurance Fraud, a nonprofit in the U.S., estimates that at least $80 billion of fraudulent claims are made annually in the U.S. alone, but the figure is likely significantly higher. One problem has, ironically, been the move to more virtualized processes, which open the door to malicious actors exploiting loopholes in claims filing and fudging information. Another is the fact that insurance has grown as a market, but so too has the amount of people who are in financial straights, leading to more desperate and illegal acts to gain an edge.

Shift is also not alone in tackling this issue: the market for insurance fraud detection technology globally was estimated to be worth $2.5 billion in 2019 and projected to be worth as much as $8 billion by 2024.

In addition to others in claims management tech such as Brightcore and Guidewire, many of the wave of insurtech startups are building in their own in-house AI-based fraud protection, and it’s very likely that we’ll see a rise of other fraud protection services, built out of adjacent areas like fintech to guard against financial crime, making their way to insurance. As many a fintech entrepreneur has said to me in the past, the mechanics of how the two verticals work and the compliance issues both face are very closely aligned.

“The entire Shift team has worked tirelessly to build this company and provide insurers with the technology solutions they need to empower employees to best be there for their policyholders. We are thrilled to partner with Advent International, given their considerable sector expertise and global reach and are taking another giant step forward with this latest investment,” stated Jeremy Jawish, CEO and co-founder, Shift Technology, in a statement. “We have only just scratched the surface of what is possible when AI-based decision automation and optimization is applied to the critical processes that drive the insurance policy lifecycle.”

For its backers, one key point with Shift is that it’s helping older providers bring on more tools and services that can help them improve their margins as well as better compete against the technology built by newer players.

“Since its founding in 2014, Shift has made a name for itself in the complex world of insurance,” said Thomas Weisman, an Advent director, in a statement. “Shift’s advanced suite of SaaS products is helping insurers to reshape manual and often time-consuming claims processes in a safer and more automated way. We are proud to be part of this exciting company’s next wave of growth.”

Powered by WPeMatico

The investment landscape for insurtech startups is off to a hot start in Q2 2021. Since the end of the first quarter, we’ve seen several players in the broad startup category announce new capital, including Clearcover, Alan, Next Insurance and The Zebra.

But, as anyone who’s familiar with startups that offer insurance-related products and services knows, the sector is enough of a mixed bag that one needs to segment down to get clarity on how constituent companies are performing. So while Clearcover’s $200 million round from last week, Next Insurance’s $250 million round from the first of the month and Alan’s $220 million round from yesterday are interesting, this morning we’re going to focus a bit more on The Zebra’s side of the insurtech house.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The Exchange divides insurtech startups into three categories: neoinsurance providers, insurtech marketplaces and insurtech enablers. (You can see why we need to segment the insurtech genre!)

Briefly, neoinsurance providers are companies like Root, Metromile and Next Insurance, which use technology to underwrite and sell insurance in an updated manner; these companies also often have optimized mobile experiences.

Marketplaces like The Zebra, Gabi, Insurify and others provide a way for consumers to better identify their insurance options. And, finally, there are companies like AgentSync, which fit neatly into our third category of firms that help other companies in the insurance business digitize their operations or otherwise modernize.

Insurtech marketplaces came back into our view when The Zebra put together a $150 million Series D earlier this month and released a host of metrics regarding its growth, and Insurify dropped the news that it is partnering with Toyota.

Insurtech marketplaces came back into our view when The Zebra put together a $150 million Series D earlier this month and released a host of metrics regarding its growth, and Insurify dropped the news that it is partnering with Toyota.

This morning, let’s discuss insurtech’s 2020 as a whole, peek at some preliminary 2021 venture data and then dive deep into what we’ve collected regarding growth among insurtech marketplace players. The Exchange has data and other details from The Zebra, Insurify, Wefox and more.

Covering longitudinal progress of specific startup categories is one of our favorite things to do. So, please, walk with us!

PitchBook data regarding the insurtech category in 2020 underscores how large the startup niche has grown. Per the data company, $18.3 billion was spent last year on insurtech startups across venture capital, private equity and M&A activity. That was a billion dollars under its 2019 result, but given the pandemic’s onset, 2020’s final result is somewhat impressive — who expected insurance investing to hold up during an unprecedented global catastrophe?

This year is proving lucrative for the insurtech market, at least from a venture capital perspective. Normally I’d make a joke about how unprofitable some neoinsurance providers are at this juncture, but because our focus is elsewhere, bringing up the fact that, say, Lemonade’s adjusted losses in the final quarter of 2020 were around 150% of its revenue is kind of irrelevant. So we won’t!

Powered by WPeMatico