fintech

Auto Added by WPeMatico

Auto Added by WPeMatico

Affirm, a consumer finance business founded by PayPal mafia member Max Levchin, filed to go public this afternoon.

The company’s financial results show that Affirm, which doles out personalized loans on an installment basis to consumers at the point of sale, has an enticing combination of rapidly expanding revenues and slimming losses.

Growth and a path to profitability has been a winning duo in 2020 as a number of unicorns with similar metrics have seen strong pricing in their debuts, and winsome early trading. Affirm joins DoorDash and Airbnb in pursuing an exit before 2020 comes to a close.

Let’s get a scratch at its financial results, and what made those numbers possible.

Affirm recorded impressive historical revenue growth. In its 2019 fiscal year, Affirm booked revenues of $264.4 million. Fast forward one year and Affirm managed top line of $509.5 million in fiscal 2020, up 93% from the year-ago period. Affirm’s fiscal year starts on July 1, a pattern that allows the consumer finance company to fully capture the U.S. end-of-year holiday season in its figures.

The San Francisco-based company’s losses have also narrowed over time. In its 2019 fiscal year, Affirm lost $120.5 million on a fully-loaded basis (GAAP). That loss slightly fell to $112.6 million in fiscal 2020.

More recently, in its first quarter ending September 30, 2020, Affirm kept up its pattern of rising revenues and falling losses. In that three-month period, Affirm’s revenue totaled $174.0 million, up 98% compared to the year-ago quarter. That pace of expansion is faster than the company managed in its most recent full fiscal year.

Accelerating revenue growth with slimming losses is investor catnip; Affirm has likely enjoyed a healthy tailwind in 2020 thanks to the COVID-19 pandemic boosting ecommerce, and thus gave the unicorn more purchase in the realm of consumer spend.

Again, comparing the company’s most recent quarter to its year-ago analog, Affirm’s net losses dipped to just $15.3 million, down from $30.8 million.

Affirm’s financials on a quarterly basis — located on page 107 of its S-1 if you want to follow along — give us a more granular understanding of how the fintech company performed amidst the global pandemic. After an enormous fourth quarter in calendar year 2019, growing its revenues to $130.0 million from $87.9 million in the previous quarter, Affirm managed to keep growing in the first, second, and third calendar quarters of 2020. In those periods, the consumer fintech unicorn recorded a top line of $138.2 million, $153.3 million, and $174 million, as we saw before.

Perhaps best of all, the firm turned a profit of $34.8 million in the quarter ending June 30, 2020. That one-time profit, along with its slim losses in its most recent period make Affirm appear to be a company that won’t hurt for future net income, provided that it can keep growing as efficiently as it has recently.

The pandemic has had more impact on Affirm than its raw revenue figures can detail. Luckily its S-1 filing has more notes on how the company adapted and thrived during this Black Swan year.

Certain sectors provided the company with fertile ground for its loan service. Affirm said that it saw an increase in revenue from merchants focused on home-fitness equipment, office products, and home furnishings during the pandemic. For example, its top merchant partner, Peloton, represented approximately 28% of its total revenue for the 2020 fiscal year, and 30% of its total revenue for the three months ending September 30, 2020.

Peloton is a success story in 2020, seeing its share price rise sharply as its growth accelerated across an uptick in digital fitness.

Investors, while likely content to cheer Affirm’s rapid growth, may cast a gimlet eye at the company’s dependence for such a large percentage of its revenue from a single customer; especially one that is enjoying its own pandemic-boost. If its top merchant partner losses momentum, Affirm will feel the repercussions, fast.

Regardless, Affirm’s model is resonating with customers. We can see that in its gross merchandise volume, or total dollar amount of all transactions that it processes.

GMV at the startup has grown considerably year-over-year, as you likely expected given its rapid revenue growth. On page 22 of its S-1, Affirm indicates that in its 2019 fiscal year, GMV reached $2.62 billion, which scaled to $4.64 billion in 2020.

Akin to the company’s revenue growth, its GMV did not grow by quite 100% on a year-over-year basis. What made that growth possible? Reaching new customers. As of September 30, 2020, Affirm has more than 3.88 million “active customers,” which the company defines as a “consumer who engages in at least one transaction on our platform during the 12 months prior to the measurement date.” That figure is up from 2.38 million in the September 30, 2019 quarter.

The growth is nice by itself, but Affirm customers are also becoming more active over time, which provides a modest compounding effect. In its most recent quarters, active customers executed an average of 2.2 transactions, up from 2.0 in third quarter of calendar 2019.

Also powering Affirm has been an ocean of private capital. For Affirm, having access to cash is not quite the same as a strictly-software company, as it deals with debt, which likely gives the company a slightly higher predilection for cash than other startups of similar size.

Luckily for Affirm, it has been richly funded throughout its life as a private company. The fintech unicorn has raised funds well in excess of $1 billion before its IPO, including a $500 million Series G in September of 2020, a $300 million Series F in April of 2019, and a $200 million Series E in December of 2017. Affirm also raised more than $400 million in earlier equity rounds, and a $100 million debt line in late 2016.

What to make of the filing? Our first-read take is that Affirm is coming out of the private markets as a healthier business than the average unicorn. Sure, it has a history of operating losses and not yet proven its ability to turn a sustainable profit, but its accelerating revenue growth is promising, as are its falling losses.

More tomorrow, with fresh eyes.

Powered by WPeMatico

While the world awaits the Airbnb IPO filing that could come as early as next week, Upstart dropped its own S-1 filing. The fintech startup facilitates loans between consumers and partner banks, an operation that attracted around $144 million in capital prior to its IPO.

First Round Capital, Khosla Ventures, Third Point Ventures, Rakuten and The Progressive Corporation led rounds in the startup, according to Crunchbase data.

There’s quite a lot to like in Upstart’s IPO filing, including rapidly advancing revenues and recent profitable period. However, the company’s revenue concentration could be a concern to some investors who recall what recently happened to Fastly shares after losing a large customer.

PitchBook data indicates that the company was last valued at $750 million thanks to its 2019 Series D worth $50 million. Can Upstart reach unicorn status with its IPO? Let’s peek at the numbers and try to answer the question.

Upstart’s technology uses what it describes as artificial intelligence (AI) to approve consumer loans. It collects consumer demand for credit and connects that demand to bank partners who fund the loans. The company’s AI-powered credit tool can give consumers “higher approval rates [and] lower interest rates,” according to its S-1 filing, which offers banks “access to new customers, lower fraud and loss rates, and increased automation.”

If Upstart’s AI tool can, in fact, more intelligently determine consumer creditworthiness, everyone could come out a winner, with consumers paying less and banks adding to their loan books without taking on outsized risk.

Powered by WPeMatico

According to industry reports, venture capital deal-making has notably rebounded since dropping off briefly in March as shelter-in-place orders gripped much of the country.

As seed-stage fintech investors, this has certainly been our experience: “Hot” deals are getting funded faster than ever, and we increasingly see the large multistage global funds competing for the earliest access to companies. However, in our experience and anecdotal conversations with other early-stage investors, that excitement has not been translating to the Series A stage.

We’ve increasingly wondered if the Series A market in fintech is really as hot as it seems. As pre-seed and seed-stage investors, we know that the health of the Series A market is of critical importance.

In early October 2020, the Financial Venture Studio put together a brief survey of the Series A market in fintech and shared it with more than 100 investors with whom we work closely. Despite the high-level numbers indicating a healthy market, our research indicates a market that remains in flux, with significant ramifications for early-stage founders.

Although the seed and pre-seed fintech market continues to attract substantial entrepreneurial and investor interest, it is also in some ways one of the easiest parts of the market to fund. The check size is smaller, the velocity of new deals is highest, and while the potential returns are also the highest, this is also the part of the market where information is most scarce. Perhaps counterintuitively, the fact that there is so little information on a business — aside from a plan, a team and maybe some early anecdotal evidence to support the vision — actually makes it easier to “pull the trigger” on deals where those data points align. There just often isn’t a lot more to dig into.

Similarly, by the time a company is raising Series B capital, they typically have some objective evidence that the idea is working. Companies are typically generating revenue, small teams have grown and become more sophisticated in how they operate, and importantly, the governance functions of a company have (hopefully) begun to take shape. The simple existence of a board member with invested capital at stake means that some of the more existential risks of the earliest stage have been mitigated.

In contrast, one of the big milestones for any startup has been to raise a Series A from an institutional investor. Besides an infusion of capital (which is often 2-3x the aggregate capital a company may have raised since its inception), this “stamp of approval” lends credibility to a small company that is trying to hire talent, sell to customers, and, in most cases, raise substantial subsequent capital.

Thus, it’s critical that Series A investors remain active; if not, many of these upstart companies may fail due to a lack of investment, even if they are able to demonstrate early market traction. The Series A funding market is one of — if not the most — critical funding stage in the innovation economy because it acts as a bridge between scrappy early innovation and commercialization at scale.

It stands to reason, then, that dollar amounts invested may not be the best barometer of the ecosystem’s health. What really matters is the volume of companies being funded and the variety of product approaches being pursued.

Once the initial shock of the pandemic wore off, the VC community had to get back to business, which admittedly is harder to do for funds that write $10 million+ checks and like getting to know founders in person. Still, Series A investors made it a point to let entrepreneurs know they were, and continue to be, “open for business.”

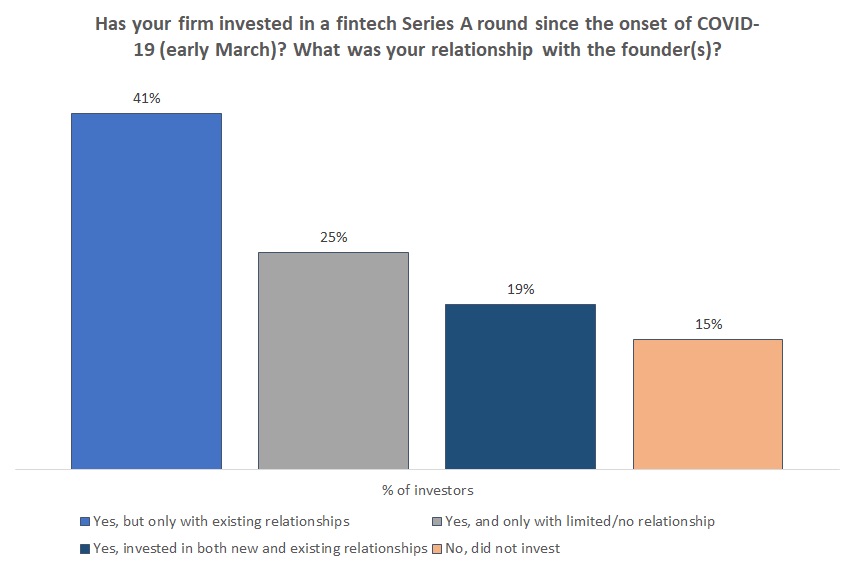

As investors have gotten more comfortable with the new normal, they have been more open to a virtual diligence process. Of the firms we surveyed, only 15% stated they have not completed a Series A investment during COVID-19 work restrictions. Of the firms who completed a Series A investment during COVID-19 (~85%), about half invested in a company whose founder(s) they had a limited or no relationship with prior to the onset of shelter-in-place orders.

Image Credits: Financial Venture Studio (opens in a new window)

The shift to a virtual environment means that process is more important than ever. Numerous investors have cited their renewed focus on following a structured approach to sourcing and diligence. The interpersonal aspect remains important to close a deal, but customer references, referrals from trusted seed-stage investors and a heightened scrutiny of metrics are all at the forefront of investors’ evaluations.

Powered by WPeMatico

As reported in the first half of our Spain-focused VC survey, the nation’s startup ecosystem continues to grow and is keeping pace with ecosystems in more developed European countries such as U.K., France, Sweden and Germany.

While main hubs Madrid and Barcelona bump heads politically, tech ecosystems in each city have been developing with local support. According to this regional investor database, Spain is home to 62 angels, 84 seed funds and 19 Series A and beyond institutional funds.

As the capital and financial center, Madrid enjoys proximity to political power and multinational companies, which is likely why it’s home to a larger proportion of fintech startups. According to Dealroom, between 2015 and 2019, Madrid’s emerging companies raised €1.5 billion. In recent years, its Arganzuela district has become known as a startup hub, but Barcelona’s Districte de la innovació is also home to a growing number of established and upcoming technology companies.

May of 2020 saw a resumption of VC activity with €70.89 million invested in startups. Wallabox, the Barcelona-based electric charger company, closed the second part of €12 million from a Series A investment. Also in May, Belvo raised €9.09 million, Accure Therapeutics €7.6 million and Cubiq Foods €4 million.

Here are the investors who shared their thoughts with us for the conclusion of our Spain VC survey:

What trends are you most excited about investing in, generally?

SaaS. B2B.

What’s your latest, most exciting investment?

Kymatio.

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

Subscription B2C app for managing kids from 0 to 18 years.

What are you looking for in your next investment, in general?

Scalability,

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

Too much competition: travel. Interesting areas: quantum computing.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

More than 50% in Spain.

Which industries in your city and region seem well-positioned to thrive, or not, long term? What are companies you are excited about (your portfolio or not), which founders?

Industries: cybersecurity. Companies: Lingokids, Devo, Genially, Glovo.

How should investors in other cities think about the overall investment climate and opportunities in your city?

Spain has no Series B investors, so there are many opportunities for foreign Series B funds.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

At least in Spain, I think remote work will be only temporary. If you are freelance it is still important to work near the main cities.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19?

Retail, fashion, travel.

What is your advice to startups in your portfolio right now?

Don’t take debt if it is not extremely necessary, try to be cash flow positive — although you have to sacrifice faster growth.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Yes! In Genially: awesome growth.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

Schools opening again (four kids already).

Any other thoughts you want to share with TechCrunch readers?

Spain will be very harmed the next year, and so will the startup ecosystem.

What trends are you most excited about investing in, generally?

Powered by WPeMatico

A month after completing Y Combinator’s accelerator program, BukuWarung, an financial tech startup that serves small businesses in Indonesia, announced it has raised new funding from a roster of high-profile investors, including partners of DST Global, Soma Capital and 20VC.

The amount of the funding was undisclosed, but a source told TechCrunch that it was between $10 million to $15 million. The new capital will be used to hire for BukuWarung’s technology team. TechCrunch first profiled BukuWarung in July.

Angel investors in the round include several high-profile founders and executives: finance technology platform Plaid’s co-founder William Hockey; Tinder co-founder Justin Mateen; Superhuman founder Rahul Vohra; Adobe chief product officer Scott Belsky; Clearbit chairman and startup advisor Josh Buckley; former Uber chief product officer Manik Gupta; Spotify’s former head of new markets in Asia Sriram Krishnan; 20VC founder Harry Stebbings; Nancy Xiao, an investor with Bond Capital; and Fast co-founder Allison Barr Allen. Angel investors from WhatsApp, Square and Airbnb also participated.

Launched last year by co-founders Chinmay Chauhan and Abhinay Peddisetty, BukuWarung is targeted at the 60 million “micromerchants” in Indonesia, including neighborhood store (or warung) owners. The app was originally created as a replacement for pen and apper ledgers, but plans to introduce financial services including credit, savings and insurance. In August, the company integrated digital payments into its platform, enabling merchants to take customer payments from bank accounts and digital wallets like OVO and DANA. BukuWarung’s goal is to fill the same role for Indonesian merchants that KhataBook and OKCredit do in India.

One of the reasons BukuWarung launched digital payments was in response to customer demand for contactless transactions and instant payouts during the COVID-19 pandemic. Since introducing the feature, the company said it has already processed several million U.S. dollars in total payment volume (TPV) on an annualized basis. The company says it now serves about 1.2 million merchants across 750 locations in Indonesia, focusing on tier 2 and tier 3 cities.

Digital payments is also the first step into building out BukuWarung’s financial services, which will help differentiate it from other bookkeeping. The payments features is currently free and BukuWarung is experimenting with different monetization models, including making a small margin on fees.

“The reason why we launched payments is also very strategic, because there is a lot of pull in the market. We have already seen several millions annualized TPV in less than a month, because the payments we offer are cost-efficient as well and cheaper than to get from a bank,” Chauhan told TechCrunch.

“If you look at the Indian players, like Khatabook, they have also launched digital payments. The reason for that is because it’s a very essential step for building a business and monetization,” he added. “If you don’t have payments, you can’t do anything like that.”

Chauhan added that building a financial services platform is the difference between providing a utility app that replaces bookkeeping ledgers, and becoming an essential service for merchants that will eventually include lending for working capital, savings and insurance products. The bookkeeping features on BukuWarung will feed into the financial services aspect by providing data to score creditworthiness, and help small merchants, who often have difficulty securing working capital from traditional banks, get access to lines of credit.

Powered by WPeMatico

Fintech startup N26 is announcing some changes in the leadership team with two new C-Level hires. First, Adrienne Gormley, pictured above, is joining the company as chief operating officer, replacing Martin Schilling who left the company in March 2020. Second, Diana Styles, pictured below, will become N26’s chief people officer.

Gormley has spent the last six years working for Dropbox in Dublin. She was the VP of Global Customer Experience as well as the head of EMEA for Dropbox. Previously, she’s worked at Google and Transware.

At N26, she will be in charge of a large chunk of the company, from customer service, to business operations, service experience and workplace division.

Styles has many years of human resources experience. She was the senior vice president of Human Resources, Global Sales and Brands at Adidas. Similarly, as chief people officer, she will oversee important aspects of the company, such as employee retention, leadership development, talent acquisition and more.

Both will be based in Berlin and report to the company’s co-founder and chief financial officer Maximilian Tayenthal. N26 has grown quite a lot over the past few years as there are now 1,500 employees working for the company.

Image Credits: N26

Powered by WPeMatico

Stripe has led a $12 million Series A round in Manila-based online payment platform PayMongo, the startup announced today.

PayMongo, which offers an online payments API for businesses in the Philippines, was the first Filipino-owned financial tech startup to take part in Y Combinator’s accelerator program. Y Combinator and Global Founders Capital, another previous investor, both returned for the Series A, which also included participation from new backer BedRock Capital.

PayMongo partners with financial institutions, and its products include a payments API that can be integrated into websites and apps, allowing them to accept payments from bank cards and digital wallets like GrabPay and GCash. For social commerce sellers and other people who sell mostly through messaging apps, the startup offers PayMongo Links, which buyers can click on to send money. PayMongo’s platform also includes features like a fraud and risk detection system.

In a statement, Stripe’s APAC business lead Noah Pepper said it invested in PayMongo because “we’ve been impressed with the PayMongo team and the speed at which they’ve made digital payments more accessible to so many businesses across the Philippines.”

The startup launched in June 2019 with $2.7 million in seed funding, which the founders said was one of the largest seed rounds ever raised by a Philippines-based fintech startup. PayMongo has now raised a total of almost $15 million in funding.

Co-founder and chief executive Francis Plaza said PayMongo has processed a total of almost $20 million in payments since launching, and grown at an average of 60% since the start of the year, with a surge after lockdowns began in March.

He added that the company originally planned to start raising its Series A in in the first half of next year, but the growth in demand for its services during COVID-19 prompted it to start the round earlier so it could hire for its product, design and engineering teams and speed up the release of new features. These will include more online payment options; features for invoicing and marketplaces; support for business models like subscriptions; and faster payout cycles.

PayMongo also plans to add more partnerships with financial service providers, improve its fraud and risk detection systems and secure more licenses from the central bank so it can start working on other types of financial products.

The startup is among fintech companies in Southeast Asia that have seen accelerated growth as the COVID-19 pandemic prompted many businesses to digitize more of their operations. Plaza said that overall digital transactions in the Philippines grew 42% between January and April because of the country’s lockdowns.

PayMongo is currently the only payments company in the Philippines with an onboarding process that was developed to be completely online, he added, which makes it attractive to merchants who are accepting online payments for the first time. “We have a more efficient review of compliance requirements for the expeditious approval of applications so that our merchants can use our platform right away and we make sure we have a fast payout to our merchants,” said Plaza.

If the momentum continues even as lockdowns are lifted in different cities, that means the Philippine’s central bank is on track to reach its goal of increasing the volume of e-payment transactions to 20% of total transactions in the country this year. The government began setting policies in 2015 to encourage more online payments, in a bid to bolster economic growth and financial inclusion, since smartphone penetration in the Philippines is high, but many people don’t have a traditional bank account, which often charge high fees.

Though lockdown restrictions in the Philippines have eased, Plaza said PayMongo is still seeing strong traction. “We believe the digital shift by Filipino businesses will continue, largely because both merchants and customers continue to practice safety measures such as staying at home and choosing online shopping despite the more lenient quarantine levels. Online will be the new normal for commerce.”

Powered by WPeMatico

A breeding ground for European entrepreneurs, Berlin has a knack for producing a lot of new startups: the city attracts top international, diverse talent, and it is packed with investors, events and accelerators. Also important: it’s a more affordable place to live and work when compared to many other cities in the region.

Berlin ranked 10th place in the 2019 Global Ecosystem Report, trailing behind only two other European cities: London and Paris. It’s home to unicorns such as N26, Zalando, HelloFresh and pioneers of the scene such as SoundCloud.

Top VCs include Earlybird, Point Nine, Project A, Rocket Internet, Holtzbrinck Ventures and accelerators such as Axel Springer Plug and Play Accelerator, hub:raum and The Family.

To get a sense of how the novel coronavirus has changed the landscape, we asked ten investors to give us an insight into their thinking during these pivotal times:

What trends are you most excited about investing in, generally?

Generally, we believe in a future in which we can leverage technology to free up humans from repetitive and tedious work and to empower them to shift their focus to what they consider more meaningful and impactful: that is creative and interpersonal activities. Thus, we are excited about founders working towards that future and finding answers across multiple industries, such as manufacturing or logistics, across all working-classes, and across different eras – before, during and after COVID.

What’s your latest, most exciting investment?

One of the recent additions of our new fund is Luminovo, a Munich-based company that develops a solution in the electronics industry to reduce the time and resources needed to go from an idea to a market-ready circuit board.

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

So far, we have only scratched the surface of the kind of efficiency gains that can potentially be achieved – particularly in industries that were considered to be boring and sluggish in the past, such as insurance or logistics. Even small improvements driven by technology can have a massive direct impact on P&L.

What are you looking for in your next investment, in general?

In general, we love to back visionary founders in the seed-stage that tap into giant industries with a high potential for digitization across Europe and the US.

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

COVID has sprung a myriad of companies in the communication and collaboration space into existence. While we believe in a future in which products and processes will be inherently remote-first, we will see a consolidation of that space that only allows for an oligopolistic market structure similar to how there is only one Zoom and Google Meet in the video communication space today.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

We have always considered ourselves as one of the few funds in Germany with a significant investment footprint both in Europe and the US. COVID has emphasized that we are able to invest entirely remotely and hence we will continue and even increase our activities across multiple hubs, such as Munich, Paris, or London.

Which industries in your city and region seem well-positioned to thrive, or not long-term? What are companies you are excited about (your portfolio or not), which founders?

Germany’s economy relies on wealthy traditional companies sitting on top of capital to be unlocked which new entrants can make use of. This has been true before 2020, and COVID will only demand more and accelerated innovation across these traditional industries ranging from automotive, manufacturing, to the chemical industry.

How should investors in other cities think about the overall investment climate and opportunities in your city?

Berlin and other German cities have consistently proven to develop and grow new leaders across multiple categories such as banking (N26), mobility (Flixbus and Lilium), or data analytics (Celonis). This is certainly driven by a mix of talents coming out of world-class educational institutions, the relative low cost of living in tech hubs, and large local incumbents with massive capital to invest and spend.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

While COVID has accelerated remote-first products and processes, we still believe that people will flock back to startup hubs such as Berlin or Munich, especially given the relatively low cost of living compared to other tech hubs like San Francisco. Nevertheless, we will continue to see an increasing number of companies scattered across multiple time zones building products that are inherently remote first, regardless where the general work environment will shift into.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

We are lucky in that our investment focus has been on sector verticals such as Logistics, Supply chain, manufacturing or the future of work, which have all captured significant tailwind from Covid.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

While our investment strategy on a high level will not change, we are putting longer sales cycles into consideration as potential customers of our portfolio companies now are focusing on capital efficiency which also holds true for our founders. Thus, we advise them to focus on extending the runway both by increasing capital efficiency as well as taking on additional funding.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

As our economy is still in the midst of dealing with the effects of COVID, it is too early to tell, but we definitely see positive indications driven by efforts of portfolio companies that could adapt quickly and shipped features catered to the current needs. One example is Personio, which extended their HR offerings with features that solve the need of customers who shifted to short-time work.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

What gave me hope was the cohesion of the German economy that fought together for solutions and support during these difficult times. One positive example was the German Startup Association that helped achieve additional governmental financial aid for German SMEs.

Any other thoughts you want to share with TechCrunch readers?

Similar to how the past financial crisis allowed companies such as Stripe or Shopify to become ubiquitous parts of our daily life, these unprecedented times now will also give birth to new forms and shapes in which new ideas will grow into large businesses and we are excited to partner up with founders willing to take a bet on that future.

Powered by WPeMatico

Meet Fondeadora, a fintech startup based in Mexico City that wants to build a full-stack neobank. The company just raised a $14 million Series A round led by Gradient Ventures, Google’s AI-focused venture fund. Founded in 2018, the company already manages 150,000 accounts and is adding $20 million in deposits every month.

Mexico represents a massive opportunity for a challenger bank as many people still rely on cash for most of their transactions. Given that all countries are progressively switching to card and digital payments, it seems like the right time to launch Fondeadora .

Y Combinator, Scott Belsky, Sound Ventures, Fintech Collective and Ignia are also participating in the funding round.

“We launched the first crowdfunding platform in Mexico about 10 years ago,” co-founder and co-CEO Norman Müller told me. “About 50% of card transactions failed in the system.”

That platform was also called Fondeadora. After a deal with Kickstarter, Müller and Fondeadora co-founder René Serrano went back to the drawing board and thought about the problems they had while operating the crowdfunding platform. It became Fondeadora as we know it today, a challenger bank that wants to improve the banking experience in Mexico.

The team traveled across Mexico to find a bank charter that they could use. “We acquired the charter, it was owned by a group of tomato farmers in Mexico. Twenty years ago, the government gave about 10 charters to create financial inclusion,” Müller told me.

The company launched its banking service after that. You can open an account without visiting a branch. You then receive a Mastercard debit card. You can choose to receive notifications after each purchase, lock and unlock your card, send instant transfers to other users and more. There are no monthly subscription fee and no foreign transaction fee.

Up next, Fondeadora wants to democratize savings accounts. “Cash has a great UX and UI. You can touch it, you can store it in your drawer. But as a medium to generate income, it’s terrible,” Müller told me.

In the coming months, you’ll earn interest on your deposits in your Fondeadora account. “We’re investing in government bonds, it’s a very secure type of instruments. In Mexico, you can get 5% or 6% interest rate,” Müller said. The startup could allocate a small portion of deposits to medium-risk investments as well.

Image credits: Fondeadora

Powered by WPeMatico

Robinhood announced this morning that it has raised $200 million more at a new, higher $11.2 billion valuation. The new capital came as a surprise.

Astute observers of all things fintech will recall that Robinhood, a popular stock trading service, has raised capital multiple times this year, including an initial $280 million round at an $8.3 billion valuation, and a later $320 million addition that brought its valuation to $8.6 billion.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Those rounds, coming in May and July, now feel very passé in the sense that they are frightfully cheap compared to the price at which Robinhood just added new funds. D1 Partners — a private capital pool founded in 2018 — led the funding.

The unicorn’s new nine-figure tranche, a Series G, values the firm at $11.2 billion. A $2.6 billion bump in about a month is an impressive result, one that points to an inescapable conclusion: Robinhood is still growing, and fast.

How fast is the question. There are three things to bring up in this regard: Trading growth at Robinhood, the company’s soaring incomes from selling order flow to other financial institutions, and, oddly enough, crypto. Let’s peek at each and come up with a good why as to the new Robinhood valuation.

After all, we’re going to see an IPO from this company before the markets get less interesting, if it’s smart.

Robinhood is currently walking a line between enthusiasm that its trading volume is growing and conservatism, arguing that its userbase is not majority-comprised of day traders. The company is stuck between the need for huge revenue growth and keeping pedestrian users from tanking their net worth with unwise options bets.

It’s worth noting that Robinhood spent a lot of its funding round announcement email to TechCrunch talking about its users safety and education work. It makes sense given that we know that the company is seeing record trades, and record incomes from options themselves. After a Robinhood user killed themself after misunderstanding an options trade on the platform, Robinhood pledged to do better. We’re keeping tabs on how well it manages to meet the mark of its promise.

But back to the revenue game, let’s talk volume. On the trading front Robinhood has lots of darts. And by darts we mean daily average revenue trades. Robinhood had 4.31 million DARTs in June, with the company adding that “DARTs in Q2 more than doubled compared to Q1” in an email.

The huge gain in trading volume does not mean that most Robinhood users are day trading, but it does imply that some are given the huge implied trading volume results that the DARTs figure points to. Robinhood saw around 129,300,000 trades in June, which is 30 days. That’s a lot!

Powered by WPeMatico