fintech

Auto Added by WPeMatico

Auto Added by WPeMatico

Venture capitalists and other investors have poured capital into fintech startups around the world in recent years, including a record number of rounds worth $100 million or more in the second quarter of 2020. In Q2 2020 venture-backed fintech startups raised 28 nine-figure rounds, underscoring the scale of the bet investors are making on fintech’s long-term success.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Inside that fintech wave are various hubs of activity, including payments tech, investing and banking. That last category has helped give rise to so-called neobanks, startup banking entities that offer mobile-first, consumer-friendly banking tools and services. Given the old-fashioned nature of banking in many countries (and how far out of reach banking remains for many) neobanks have seen strong uptake by users in recent years.

And the startup cohort has raised oceans of capital to help fuel its growth. In America, Chime was most recently valued at $5.8 billion after raising hundreds of millions in late 2019. More recently, neobank Revolut added $80 million to its Q1 2020 round worth $500 million. Revolut is also worth north of $5 billion. Monzo is well-funded (albeit at a recent valuation reduction), Latin America-focused NuBank is worth $10 billion, according to Crunchbase, Starling recently raised another £40 million, while Germany’s N26 is worth over $3 billion after its most recent nine-figure round.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

Of course, startups don’t raise money for fun; they raise it to invest it in their operations and drive scale. So, we knew that these megafundraisers were losing money on purpose. All the same, let’s peek at the economics of several neobanks, as their now dated and thus not at all current results can provide useful context on two points: Why investors are excited to put their capital to work in neobanks, and why neobanks always seem to have another check to announce.

To prevent my receiving unhappy emails from irked fans of these companies, please bear in mind that we’re looking several quarters back when observing the following results.

It would be lovely to have more recent data, but with European neobanks reporting their — roughly — 2019 results in recent weeks, this is what we have. We are going to parse the numbers, but we will not conflate past performance with current results. We do not know much about 2020 neobank financial performance.

Anyhoo, to the numbers. You can read the full documents from Monzo here, Starling here (or here, if that link is struggling) and Revolut here.

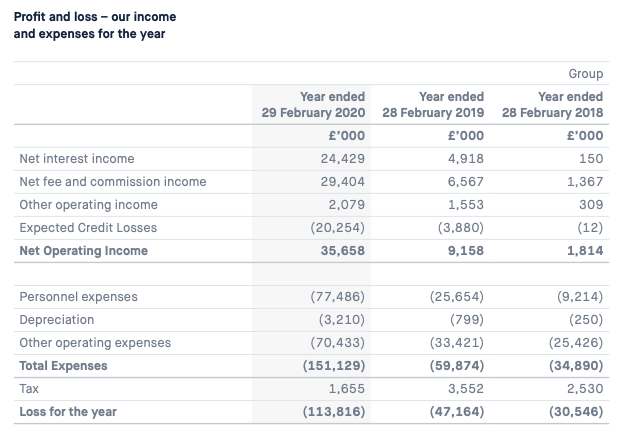

Let’s start with Monzo, which has a clear set of figures for us to peek at:

Image Credits: Monzo

Powered by WPeMatico

Point, a new challenger bank in the U.S., is launching publicly today with an invite system. While Point is technically providing a bank account, the company focuses on rewards associated with a debit card.

“I started Point as a solution about everything that is frustrating and complicated about credit cards. The incentives between credit card companies and cardholders are misaligned,” Point co-founder and CEO Patrick Mrozowski told me.

When Mrozowski first got a credit card, he was spending a ton of money to reach a certain level of spending and unlock the sign-up bonus. At the end of the month, he ended up with credit card debt for no valid reason.

“What would American Express look like today?” he says to sum up Point’s vision. It comes down to two important principles — being in charge of your budget so that you don’t end up with debt and unlocking rewards from brands that you actually interact with.

Many challenger banks want to provide a simple banking experience for the underbanked. Point doesn’t have the same positioning. Creating a Point account is more like joining a membership program.

When you sign up, you get a debit card with some level of insurance as it’s a Mastercard World Debit card. You can expect some trip cancellation insurance, rental car insurance, purchase insurance, etc.

As the name of the startup suggests, you earn points with each purchase. You get 5x points on subscriptions, such as Spotify and Netflix, 3x points on food, grocery deliveries and ride sharing, and 1x points on everything else. Points can be redeemed for dollars — each point is worth $0.01. In addition to that, Point is going to create a feed of offers with discounts, content, events and more.

Due to its premium positioning, Point isn’t free. You have to pay $6.99 per month or $60 per year to join Point. Point doesn’t charge any foreign transaction fees.

You can connect your Point account with another bank account using Plaid. It lets you top up your account using ACH transfers. Behind the scenes, Point works with Radius Bank for the banking infrastructure, an FDIC-insured bank.

The company announced earlier this month that it has raised a $10.5 million Series A led by Valar Ventures with Y Combinator, Kindred Ventures, Finventure Studio and business angels also participating.

Image Credits: Point

Powered by WPeMatico

The COVID-19 pandemic has forced businesses to rethink how they accept and make payments. Paper invoices, checks and point-of-sale payments have given way to “corona-free payments” through mobile apps, electronic invoicing and ACH. Although significant, this is the sideshow to a more significant reshuffling of the payments industry.

Nearly $150 trillion in worldwide B2B and B2C transactions take place every year, but only a tiny portion are digital. A lot of technology companies want their piece of that massive pie. Until recently, though, only payment facilitators (aka, “payfacs”), gateways, banks and credit card companies had access to it.

That’s changing. Whether they know it yet or not, B2B tech platforms are becoming payments companies. Payfacs are competing to integrate their technology into these platforms, which drive an ever-growing number of transactions. Revenue-sharing deals are on the table, and payfacs are pushing the competitive advantages they can offer to the clients of these B2B platforms. Capabilities like cross-border payments, seamless customer onboarding, fraud protection, marketplace payments and B2B invoicing influence, which payfacs win in “integrated payments” (the jargon for this space) and which don’t.

B2B companies that use to leave the choice of gateway to their clients need to become savvy in payment technology, both to control the user experience and to tap this new business. There’s a massive amount of revenue on the table, and it’s just too easy to blow this opportunity and alienate clients in the process.

A decade ago, the revolution in cloud computing led to a wave of B2B tech platforms promising to “disrupt” every industry. Gyms got gym management platforms. Hospitals got clinic management platforms. Retailers got commerce management platforms. Media companies got subscription management platforms. Many of these fill-in-the-blank management platforms — all independent software vendors (ISVs) — helped clients manage their operations and interactions with consumers or other businesses.

But ISVs didn’t get involved in payments, which was odd, given how complementary payments were to their platforms and how much money was at stake. Mastercard says there is about $120 trillion annually in B2B payments worldwide, and paper checks still dominate about half of the U.S.’s $25 trillion payment volume. Meanwhile, retail e-commerce sales account for $4.2 trillion out of $26 trillion in total retail, or about 16.1%, according to eMarketer. Less than 8% of global commerce is thought to occur online.

You’d think B2B software companies would find a way to generate revenue on some of that $146 trillion in transactions, but most did not. Payment processing is its own, messy, complicated niche. Payfacs go through a grueling underwriting process to provision a merchant account, which includes know-your-customer (KYC) and anti-money laundering (AML) checks. If a merchant defaults, the payfac is next in line to make good on the transactions.

When you run a venture-backed B2B platform, you have enough to worry about already.

So, B2B platforms stayed clear. They formed integrations with a basket of payfacs (Stripe, PayPal, Square, my company BlueSnap, etc.) and then let their clients choose which one to use. That’s a lot of integrations to maintain.

Powered by WPeMatico

The stakes keep getting higher for American discount brokerage Robinhood, which today disclosed that it has added hundreds of millions of dollars to its previously disclosed funding round.

Including the $280 million that the company had already announced, Robinhood said that it was “pleased to share” that it “raised an additional $320 million in subsequent closings.” Its now $600 million funding round brings its post-money valuation to $8.6 billion. Fortune first reported the news.

(A detail, but the new capital is part of the same round as it was raised at the same price. TechCrunch reported when the company’s $280 million round was announced, the fintech company was worth $8.3 billion. Another $300 million in capital at a flat share price means that the company’s valuation should have risen by only the dollar amount added. As it did.)

Robinhood has had a good business year, even if some of its practices have come under fire. The company pledged to tighten up parts of its platform relating to more exotic trading after the suicide of one of its users, for example; a topic that TechCrunch discussed at length last week.

What is inescapable is that Robinhood is having one hell of a year. When it might go public isn’t clear, especially as the private company is having no problem raising capital without an IPO. But as its value continues to rise, it becomes an increasingly remote acquisition target.

Powered by WPeMatico

If you have bought a house in the last decade, you likely started the process online. Perhaps you browsed for your future dream home on a website like Zillow or Realtor, and you may have been surprised by how quickly things moved from seeing a property to making an offer.

When you reached the closing stage, however, things slowed to a crawl. Some of those roadblocks were anticipated, such as the process of getting a mortgage, but one likely wasn’t: the tedious and time-consuming process of obtaining title insurance — that is, insurance that protects your claim to home ownership should any claims arise against it after sale.

For a product that is all but required to purchase a home, title insurance isn’t something many people know about until they have to pay for it and then wait up to two months to get.

Now, finally, a handful of startups are taking on the title insurance industry, hoping to make the process of buying a policy easier, cheaper and more transparent. These startups, including Spruce, States Title, JetClosing, Qualia, Modus and Endpoint, enable part or all of the title insurance buying process. Whether these startups can finally topple the title insurance monopoly remains to be seen, but they are already causing cracks in the system.

To that end, we’ve outlined what’s broken about today’s title industry; recent developments in technology and government that are priming the industry for change; and a synthesis of some key trends we’ve observed in the space, as entrepreneurs begin to capitalize on a tipping point in a century-old, $14 billion business.

To understand how startups are beginning to challenge title insurance incumbents, we need to first understand what title insurance is and what title companies do.

Title insurance is unique from other types of insurance, which require ongoing payments and protect a buyer against future incidents. Instead, title insurance is a one-time payment that protects a buyer from what has already happened — namely errors in the public record, liens against the property, claims of inheritance and fraud. When you buy a home, title insurance companies research your property’s history, contained in public archives, to make sure no such claims are attached to it, then correct any issues before granting a title insurance policy.

Powered by WPeMatico

Today Personal Capital, a fintech company that had attracted more than $265 million in private funding, announced that it is selling itself to Empower Retirement, a company that provides retirement services to other companies. The deal is worth $825 million upon closing, with another $175 million in what are described as “planned growth” incentives, according to a release.

The deal is a likely win for Personal Capital . According to Forbes, the firm was worth $660 million around the time of its Series F round of funds, which it raised in February of 2019. The company was valued at around $500 million in December of 2016, meaning that investors who put capital in at that point, or before, likely did well on their investment.

Venture groups who put capital in later, unless they had ratchets in place, likely didn’t make as much from the deal as they originally hoped. Regardless, a $1 billion all-inclusive exit is nothing to scoff at; Facebook once bought Instagram for that much money, and the sheer cheek of the transaction at the time nearly broke the internet.

During its life as a private company, Crosslink Capital, IGM Financial, Venrock, IVP and Corsair each led rounds into the company according to Crunchbase data.

Personal Capital is a consumer service that helps folks plan for retirement, and invest their capital. The company offers free financial tools, and a higher-cost wealth management option for accounts of at least $100,000. The company doesn’t like being called a robo-advisor, instead claiming to exist in the space between old-fashioned in-person wealth management relationships and fully automated options.

Regardless, the company’s sale price should help market rivals price themselves. Here are Personal Capital’s core stats (data via Personal Capital, accurate as a May 31, 2020):

So, Wealthfront and M1 Finance and others, there are some metrics for you to weigh yourselves against. Of course, other, competing companies have different monetization methods, so the comparison won’t be 100% direct.

The Personal Capital exit fits into the theme that TechCrunch has tracked lately, in which savings and investing applications have seen demand surge for their wares. This is a trend not merely in the United States where Personal Capital is based, but also abroad.

Aside from Personal Capital’s exit today, we’ve also seen huge deals in 2020 from Plaid, which sold to Visa for over $5 billion, Galileo’s exit for over $1 billion and Credit Karma’s sale for north of $7 billion. In response to this particular news item, TechCrunch’s Danny Crichton noted that fintech is “probably the hottest exit market right now.” He’s right.

Powered by WPeMatico

The fintech revolution is just getting started.

At least that’s the impression we got after a conversation with Plaid co-founder Zach Perret. He appeared on Extra Crunch Live last week to talk about his company’s announced exit to Visa and the larger fintech landscape.

Perret and Plaid announced a deal to sell the company to Visa earlier this year for $5.3 billion, a transaction that highlighted the company’s central position in the fintech world. Plaid provides APIs that link consumer bank accounts to apps and other financial services, making it the connective tissue of the fintech boom.

It’s probably no surprise, then, that Perret is bullish: “You’ve heard it a million times, but the quote of software eating the world [is true], and my corollary to that is [that] every company is a fintech company. And certainly every financial services company should be a fintech company.”

He said there’s lots of room left for fintech and finservices companies to create new products, which is not a bad view of the future if you want to be cheered up. Perret also noted that there are widespread opportunities for fintech companies to help underbanked people in the U.S. and abroad, which indicates a massive, untapped total addressable market.

To make sure you can take your own notes, we’ve included the full session below and excerpted a few passages from the transcript. (You can sign up for Extra Crunch here if you need access.)

First up, here’s the full call:

Powered by WPeMatico

Fintech startup Revolut has expanded its open banking feature to Ireland. The feature first launched in the U.K. back in February. Once again, the startup is partnering with TrueLayer to let you add third-party bank accounts to your Revolut account.

The feature launch also marks the launch of TrueLayer in Ireland. For now, Revolut users can only link their Revolut account with AIB, Permanent TSB, Ulster Bank and Bank of Ireland. Revolut and TrueLayer will add support to other banks in the future. Revolut currently has 1 million customers in the Republic of Ireland.

The idea behind open banking is quite simple. Many online services rely on application programming interfaces (APIs) to talk to each other. You can connect with your Facebook account on many online services, you can interact with other services from Slack, etc.

Financial institutions have been lagging behind on this front, but it is changing thanks to new regulation and technical updates. With open banking, your bank account should work more like a traditional internet service.

When you connect your bank account with Revolut, you can view your balance and past transactions from a separate tab that lists all your linked accounts. Users can also take advantage of Revolut’s budgeting features with their bank accounts.

As TechCrunch’s Steve O’Hear noted when he first covered Revolut’s open banking feature, Revolut was originally authorized for Account Information Services (AIS) by the U.K. regulator, the Financial Conduct Authority. It lets you access and display information from other financial institutions.

But the startup now has permission to carry out Payment Initiation Services (PIS). It means that you’ll soon be able to initiate transfers from your bank account directly from Revolut. It should make it much easier to top up your Revolut balance, for instance.

While this feature might seem anecdotal, Revolut wants to build a comprehensive financial hub for all your financial needs — a sort of super app for everything related to money. With open banking, you theoretically no longer have to open your traditional banking app.

Image Credits: Revolut

Powered by WPeMatico

Square acquired Verse, a Spanish peer-to-peer payment app that works across Europe. Terms of the deal are undisclosed. According to Crunchbase, Verse had raised $37.6 million from Spark Capital, eVentures, Greycroft Partners and others.

Square has attracted a ton of users with Cash App, its peer-to-peer payment app that lets you easily send and receive money from your phone. But Cash App has only been available in the U.S. and the U.K.

Acquiring Verse seems like a good fit to expand Square’s presence in Europe. Verse’s team will join the Cash App division within Square.

There are many similarities between Cash App and Verse. Verse’s main feature is that it lets you send and receive money from a mobile app. Users don’t pay any fees and transfers occur in just a few seconds.

Verse users sign up with their phone numbers, which means that you can send money to other users as long as you have their phone numbers in your address book. If you don’t have enough money on your Verse account, the app can charge your debit card directly. And if you want to withdraw money from your Verse account, you can transfer your balance to your bank account.

You can also track group expenses from the app (like Splitwise), create money pots and organize events with a basic ticketing feature.

More recently, Verse launched a Visa debit card in Spain, which lets you spend money on your Verse account directly. You don’t pay any foreign exchange fees and you get two free ATM withdrawals per month. Verse uses Visa’s exchange rate.

While the startup hasn’t shared usage numbers for a while, according to App Annie, it is currently the No. 247 most downloaded app in the App Store in Spain across all categories. Peer-to-peer payment is a fragmented market. For instance, French startup Lydia has 3 million users in France.

“At this point, our main priority is enabling Verse to continue their successful growth in Europe. Verse will continue to operate as an independent business, working out of their offices with no immediate changes to their existing products, customers, or business operations,” Square wrote in the announcement.

The three most important words in this statement are “at this point.” Square doesn’t want to fix what isn’t broken. But I wouldn’t be surprised if Verse slowly evolves to become Cash App in Europe.

Image credits: Square

Powered by WPeMatico

It may have entered the game later than other leading regions such as Europe and North America, but Latin America’s fintech industry is dynamic and growing fast. The sector was recently given a valuation of more than $150 billion and continues to expand year-on-year.

And while the longer-term impact of COVID-19 on the sector is yet to be determined, there’s no doubt that the demand for certain fintech solutions is on the rise. As smaller financial institutions across the region are under pressure to digitize, many are calling on fintechs to help them along this journey. In addition, a number of SMEs are seeking out digital loan services to help them get through the crisis.

The sector’s speedy expansion has meant that regulators in LatAm are under increasing pressure to enact legislation that addresses the murky waters of fintech activity, providing confidence to consumers and investors alike. However, regulation across the region must be careful to not quash innovation, while startups must figure out how to be agile in an environment which is becoming increasingly regulated. Let’s take a closer look at what impact regulation has had so far in LatAm, and what needs to happen to strike a balance between sector growth and public trust.

Mexico is currently leading the way when it comes to fintech regulation in LatAm, thanks to its comprehensive 2018 fintech Law. The law covers most fintech activities, including crowdfunding, virtual wallet, transactions carried out with cryptocurrencies and open banking. In addition, Mexico has certain financial laws that regulate financial entities in their execution of transactions using fintech. The law also provides a regulatory sandbox for both licensed and non-licensed companies.

Brazil is the furthest ahead after Mexico, as it individually legislates crowdfunding and peer-to-peer lending, while a special congressional commission is working on a broader legislative strategy. Brazil’s Central Bank also endeavors to make open banking legislation effective by the third quarter of 2020, which will pave the way for a thriving open banking ecosystem.

Powered by WPeMatico