fintech

Auto Added by WPeMatico

Auto Added by WPeMatico

Singapore-based fintech startup GoBear has raised $17 million from returning investors Walvis Participaties, a Dutch venture capital firm, and Aegon N.V., a life insurance and asset management provider. The funding brings GoBear’s total funding so far to $97 million, and will be used to expand its consumer financial services platform, which is available in seven Asian markets: Hong Kong, Indonesia, Malaysia, the Philippines, Singapore, Thailand and Vietnam.

Founder and CEO Adrian Chng told TechCrunch that GoBear will focus on what it calls its “three growth pillars”: an online financial supermarket that evolved from the company’s financial products aggregator/comparison service; an online insurance brokerage; and its digital lending business, which it recently expanded by acquiring consumer lending platform AsiaKredit.

The company has also added three new executives over the past few months: chief information technology officer Valeriy Gasratov; chief strategy officer Jinnee Lim as Chief Strategy Officer; and Mike Singh from AsiaKredit as its new chief lending officer.

GoBear originally launched in 2015 as a metasearch engine, before transitioning into financial services. The company now works with over 100 financial partners, including banks and insurance providers, and says its platform has been used by over 55 million people to search for more than 2,000 personal financial products.

The startup serves consumers who don’t have credit cards or other access to traditional credit building tools. Similar to other fintech companies that focus on underbanked populations, GoBear aggregates and analyzes alternative sources of data to judge lending risk, including patterns in consumer behavior. For example, Chng said if a loan application is filled out in less than a minute, it is more likely to be fraudulent, and applications made between 8:30PM and midnight are less risky than ones made between 2AM to 5AM.

Data points from smartphones is also used to assess creditworthiness in markets like the Philippines, where the credit card penetration rate is less than 10%, but more than 40% of the population uses a smartphone.

Despite the COVID-19 pandemic, Chng said GoBear has been gross margin positive since the end of 2019. Interest in travel insurance has declined, but the company has continued to see demand for other insurance products and lending. Its online insurance brokerage has grown its average order by 52% over the last three months, and the company has seen 50% year-over-year growth from its loan products.

There are other fintech companies in Asia that overlap with some of the services that GoBear offers, like comparison platform MoneySmart, CompareAsiaGroup and Grab Financial Group. In terms of competition, Chng told TechCrunch that not only is the market opportunity in Asia huge (he said there are 400 million underbanked people across GoBear’s seven markets), but the company also differentiates with its three core services, which are all interconnected and draw on the same data sources to score credit.

Chng anticipates that the pandemic will spur more financial institutions to begin digitizing their products and looking for partners like GoBear to help them manage risk. In turn, that will make more financial institutions open to using non-traditional data to score credit, enabling underbanked markets to have increased access to financial products.

“The momentum is here. I think now is the time for tech and data to transform financial services,” he said. “As a platform, we are really looking for partners to come with us for the next phase of growth and investment. I feel positive even with COVID-19, because I think that we will have more acceleration, and the opportunity to change people’s lives and benefit them and investors by solving tough problems will only increase.”

Powered by WPeMatico

The COVID-19 pandemic is making life worse for many startups, but not all. Those benefiting are often taking advantage of the market updraft to add more capital to their accounts. Robinhood, for example, saw usage of its consumer fintech product rise rapidly. Then the company raised a Series F worth $280 million at a new, higher valuation.

Another startup has done something similar. Human Interest, a finservices 401(k) provider for SMBs, added $10 million to its Series C today. The company’s Series C round is now worth a total of $50 million. Glynn Capital led the Series C extension.

The reason for the new capital is simple. According to Jeff Schneble, the company’s CEO, Human Interest has seen “some of the strongest sales months in the company’s history, and are seeing 2-3X year-over-year growth in customer acquisition even in the midst of the COVID-19 crisis.”

When usage and revenue scale ahead of expectations, options open up. TechCrunch had a few questions about the additional capital. Let’s explore.

TechCrunch first wanted to know if the San Francisco-based Human Interest’s new $10 million — which brings its total known capital raised to around $80 million — is earmarked for offense (greater investment into GTM functions, for example), or defense (runway extension, and so forth).

According to the CEO, the round is “more about playing offense,” with the executive adding that offense has been “something we’ve had the luxury of thinking about since the beginning of the crisis, given our large raise in February.” Human Interest intends to double its engineering team, and is “aggressively ramping up [its] GTM team (more reps, more partners, growing our marketing team and budget).”

TechCrunch was also curious about its customer profile — is Human Interest seeing growth from a different set of customers in the COVID-19 era? According to Schneble, not really: “We have not seen a significant shift in customer size, geography or vertical,” he said.

Human Interest, however, is seeing more companies coming to it looking to change 401(k) providers. Schneble told TechCrunch that “historically” 85% of his company’s customers are looking to offer “a retirement benefit for the first time.” However, “in the last couple of months” Human Interest has seen “a surge of customers with existing retirement plans that want to move to a lower-cost benefit.”

As Human Interest uses “technology, rather than people” to run its 401(k) service, the startup can offer a service that is “typically 30-50% lower-cost than a legacy 401(k) plan,” according to Schneble.

Is this new demand changing the company’s economics? TechCrunch wanted to know if market interest in 401(k) plans — consumers are flocking to savings and investing apps, likely driving more companies to add retirement savings plans for their employees — was lowering Human Interest’s customer acquisition costs (CAC).

According to the CEO, Human Interest focuses on gross-margin payback, or the time period it takes for gross-margin adjusted revenue to repay CAC. “I can’t stress how important profitability is in this space,” Schneble told TechCrunch, adding that “many of [his] competitors have negative contribution margins, which is obviously not a recipe for building a successful public company.”

The company’s gross-margin payback pace is improving, with the company telling TechCrunch that it has “come down by ~70% in the past 12 months, and is now approaching zero for many of our customers (meaning the margin contribution from their initial payment when they launch their plan covers our CAC).”

Human Interest’s gross margins help with that, with Human Interest telling TechCrunch that it has “typical software margins” on its product. That means 70%+ gross margins.

Back to the $10 million add-on, TechCrunch confirmed that the new capital was raised at the same pre-money valuation as the rest of its Series C. The CEO added the following color:

We had interest from several of the later-stage growth funds we talked to in our Series C process, but decided to move forward with Glynn Capital. They are long-term investors that plan to hold their investment in us long after we’re public (similar to one of our other large investors, Oberndorf Enterprises). While we probably could have demanded a higher price for the extension, given the acceleration we’ve seen in the last few months, we decided to optimize on partner quality instead.

Now with more capital aboard, expectations are even higher for Human Interest. Let’s see how fast it can grow.

Powered by WPeMatico

Consumer fintech startups were massively successful in 2019, attracting millions of new users and disrupting traditional retail banks and financial services with mobile-first, consumer-oriented products. Despite the economic downturn in public markets and the massive wave of cuts at public and private companies in recent weeks, fintech startups have been raising a ton of money.

It feels like they’re all building a war chest to survive the economic winter as traditional banks continue to iterate so they can catch up and offer more user-friendly services. This is not the time to raise fees, slow down on product development or plans to acquire new users.

Back in January, I looked at challenger banks and their growth trajectories, but since then, they have managed to attract even more customers. According to the most recent figures:

And that’s without mentioning Starling Bank, Atom Bank, Bunq, Bnext, Paysend, etc. At some point, there will be as many challenger banks as non-challenger banks — perhaps we shouldn’t call them challenger banks anymore.

Beyond these startups, trading app Robinhood recently reached 13 million users, international payments startup TransferWise has 7 million customers and cryptocurrency exchange Coinbase has 30 million users.

Powered by WPeMatico

Oriente, a Hong Kong-based startup that develops tech infrastructure for digital credit and other online financial services, has raised $50 million for its ongoing Series B round. The funding was led by Peter Lee, co-chairman of Henderson Land, one of Hong Kong’s largest property developers, with participation from investors including website development platform Wix.com.

Launched in 2017 by Geoff Prentice (one of Skype’s co-founders), Hubert Tai and Lawrence Chu, Oriente focuses on markets that are underserved by traditional financial institutions. The new funding will be used for growth in Oriente’s existing markets, the Philippines and Indonesia, and expansion into new countries, including Vietnam.

It will also be used to continue building Oriente’s technology, which uses big data analytics to help merchants increase sales conversions and lower risk. Oriente has now raised more than $160 million in equity and debt, including a $105 million round in November 2018.

While many large tech companies, including Grab, Google, Facebook, Amazon, Uber, Apple and Samsung, are looking at digital payments and other online financial services, they need the tech infrastructure to do so, and partners that can also help them handle regulations in different markets.

Oriente doesn’t compete with payment providers. Instead, it is “innovating credit as a service,” Prentice told TechCrunch, by building technology that allows offline and online merchants to launch digital credit solutions quickly.

Oriente “is the only company that is focusing on building an end-to-end digital financial services infrastructure,” he added, with services created for consumers, online and offline merchants, and enterprise clients.

For consumers, the startup currently offers two apps, Cashalo in the Philippines and Finmas in Indonesia, which it says has a combined 5 million users and more than 1,000 merchants. Services include cash loans, online credit and working capital for small to medium-sized enterprises.

Oriente says that in 2019, it saw a 700% year-over-year growth in transactions and served more than 4 million new users, while merchant partners had a more than 20% increase in sales volume.

Over the next few months, Oriente plans to expand its Pay Later digital credit feature and launch new growth capital solutions for small businesses that need financing. Oriente also has several partnerships in the works to expand its enterprise solutions for larger businesses and corporations.

In Vietnam, Oriente is currently beta testing a consumer platform similar to Cashalo and Finmas. It will offer online credit and financing, as well as other services in partnership with local companies.

Oriente has also started focusing on how to serve businesses during the COVID-19 pandemic, since many merchants are coping with revenue declines, loss of users and cash flow issues.

“Over the past few weeks, we’ve reprioritized our corporate strategy to focus on the top opportunities within each market. We have also taken various steps to rebuild our organizations for optimized operational and financial efficiency in line with current and forecasted market conditions and our more focused strategy,” Prentice said.

“Our aim is not only to mitigate anticipated headwinds on liquidity but to demonstrate that our business has the potential to overcome and outperform the market in a recession—unlocking value for all stakeholders for years to come.”

Powered by WPeMatico

Digits, a fintech startup hailing from the same team that built and sold Crashlytics to Twitter, is officially launching today after two years of development. It’s also announcing a $22 million Series B round of funding led by GV, as it makes its public debut.

While the company had been fairly quiet about product details while in stealth mode, it’s today unveiling its first product: a visual, machine learning-powered expense monitoring dashboard aimed at startups and small businesses.

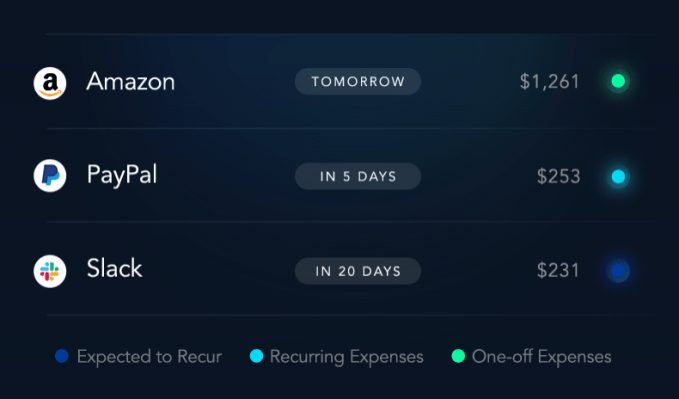

The dashboard, called Digits for Expenses, helps business owners track how their company is spending money, by showing things like spend by category, by identifying vendors and recurring expenses and by offering real-time alerts, among other features.

Instead of requiring business owners to make a switch from their existing financial solutions, Digits connects with the accounting software, banks, payroll providers, financial packages, sources of revenue and credit cards the business already uses — like Xero, QuickBooks, NetSuite, Citi, Bank of America or Chase, for example.

Instead of requiring business owners to make a switch from their existing financial solutions, Digits connects with the accounting software, banks, payroll providers, financial packages, sources of revenue and credit cards the business already uses — like Xero, QuickBooks, NetSuite, Citi, Bank of America or Chase, for example.

At launch, the list includes more than 9,000 banks, with support for Xero and NetSuite coming soon.

After setup, Digits will then automatically analyze the company’s spend and visualize it, in real time.

While visualizations of data may be reminiscent of personal finance startup Mint, Digits’ web-based solution is more technical in nature and offers an expanded analysis of the data on hand. Plus, as a business solution, it has to offer features like security, permissioning and collaborative workflows, which results in a more sophisticated product.

Digits also uses machine learning technology to predictively categorize transactions as they happen and the software can alert users to anomalies — like suspicious activity or unexpectedly large transactions — in real time. Business owners can use the dashboard to find out things like how quickly expenses are growing, what the cash flow looks like, where costs can be trimmed, what services are being paid for on a recurring basis and more, and can search for transactions.

Digits also uses machine learning technology to predictively categorize transactions as they happen and the software can alert users to anomalies — like suspicious activity or unexpectedly large transactions — in real time. Business owners can use the dashboard to find out things like how quickly expenses are growing, what the cash flow looks like, where costs can be trimmed, what services are being paid for on a recurring basis and more, and can search for transactions.

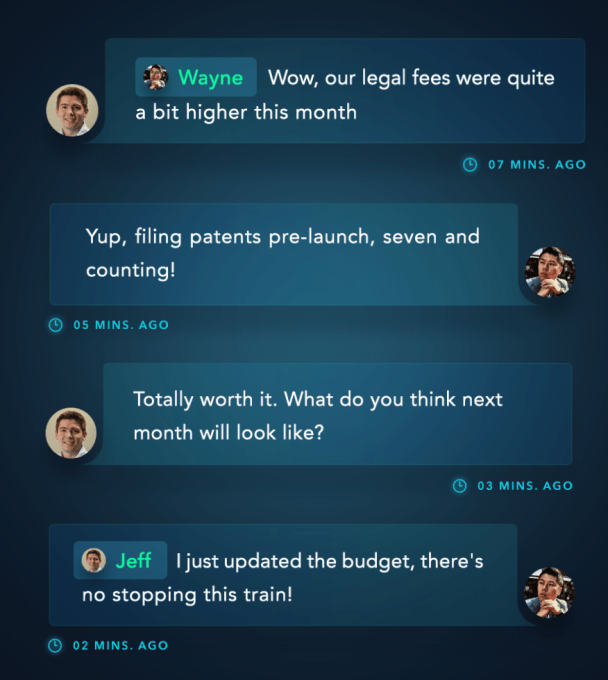

The software also supports the ability to comment on transactions, loop in a colleague to ask for clarification about a charge and upload missing receipts. Everything uses HTTPS along with TLS and certificates so data is encrypted between Digit’s services and at rest.

The original idea for Digits came from a problem that co-founders Wayne Chang and Jeff Seibert faced themselves when building Crashlytics. As they explained previously, their focus as entrepreneurs was on solving technical challenges, not on the operational side of running a business.

Many entrepreneurs also find themselves in this same space. They’re trying to solve a problem or crack a tough engineering puzzle, but instead have to redirect their time and resources to spreadsheets, financial reports, transaction records and other paperwork required to actually run the business.

“Startups and small businesses today simply don’t have the resources to manage their finances internally. Most of them still settle for spreadsheets, and the lucky ones work on an hourly basis with external accountants,” explains Seibert. “As a result, their accounting itself is seen as a cost-center, and they pay for little beyond the basic monthly financial statements — Profit & Loss, Balance Sheet, etc. By the time those statements are delivered — weeks after the end of each month — they’re already out of date,” he said.

That means things businesses need — like updates, one-off reports and new budgets — can require additional costs and longer wait times, so they get skipped.

The COVID-19 pandemic has put even more pressure on small businesses, many of which are now struggling to even survive. As a result, Digits has decided to launch the product for free to those who sign up — not a free trial, but actually free. It plans to later charge for additional products and paid upgrades to support its own business.

Digits is able to make this offer because of its now-expanded venture funding.

Already, the company had raised $10.5 million in Series A funding in a round led by Benchmark. That round had included a sizable 72 angel investors as well, including founders and CEOs from companies like Box, GitHub, Tinder, Twitch, StitchFix, SoFi and several others — entrepreneurs with an understanding of the problems Digits is aiming to solve.

Today, Digits is announcing an additional $22 million led by Jessica Verrilli at GV, who also now joins Digits’ board alongside Benchmark’s Peter Fenton. (Benchmark also participated in the new round).

“Jeff and Wayne are masterful at creating intuitive, high-utility products from complicated data,” said Verrilli about the GV investment. “I saw this up close with Crashlytics and Twitter, and I’m thrilled to partner with them on Digits as they reimagine financial software for startups,” she added.

The startup, now a team of 18 and hiring, was already offering its software solution to a group of customers ahead of today’s public launch, who effectively operated as beta testers allowing Digits to refine its product. Digits isn’t able to share its customer names, for the most part. However, it noted that Coda was one of early adopters and provided valuable feedback.

It also has over 10,000 companies who joined its waitlist over the past two years who are now being let in.

At the time of its Series A, Digits saw more than $1.5 billion in transaction value flowing across its production systems. That number has since grown to $8 billion.

The software is free starting today for U.S.-based small businesses. The company plans to add support for international markets later this year.

Powered by WPeMatico

The fintech wars continue to heat up with another major exit in the space.

Consumer financial services platform SoFi announced today that it is acquiring payments and bank account infrastructure company Galileo for $1.2 billion in total cash and stock. The acquisition is dependent on customary closing conditions.

Salt Lake City-based Galileo was founded in 2000 by Clay Wilkes and was bootstrapped to profitability over the intervening two decades. My colleague Jon Shieber wrote a profile of Galileo back in November after the company announced its second round of external funding, a $77 million Series A check from Accel, which was led by growth partner John Locke. The company had previously raised an $8 million Series A round from Mercato Partners in April 2014.

Galileo provides APIs that allow fintech companies like Monzo and Chime to easily create bank accounts and issue physical and virtual credit cards, among myriad other services. While simple in theory, banking regulations and financial rules place a huge regulatory burden on fintech companies, burdens that Galileo takes on as part of its platform.

The company has found particular success in the United Kingdom, where all five of the country’s largest fintechs are customers. Globally, it processed an annualized $45 billion in transaction volume last month, up from $26 billion in October 2019 — nearly doubling in just six months.

From a strategic perspective, SoFi’s objective is that Galileo will help power its expanding suite of finance products and offer it another revenue source outside of consumer services. While SoFi was founded a decade ago to offer ways to secure better financial terms for student loans, it now offers a bevy of consumer financial options, including loan, investment and insurance products as well as cash and wealth management tools. With Galileo, it now has a clear B2B revenue component as well.

SoFi, which is now led by ex-Twitter COO Anthony Noto, has also raised hundreds of millions of new capital from the likes of Qatar in recent years. The company was most recently valued at $4.3 billion.

Galileo will operate as an independent division of SoFi, and will be continuing its operations with founder Wilkes remaining as chief executive.

As fintech valuations have rapidly expanded in recent years, the companies that empower those fintechs have increasingly become strategic for investors. Earlier this year, Visa bought Plaid for $5.3 billion, in what was considered a key exit for a finance infrastructure company. That exit brought acute investor and strategic interest to the space, interest that almost certainly accrued to Galileo, as well, and helps explain the company’s relatively quick exit from its funding round last year.

As for Accel, the firm has long had a strategy of investing in mostly bootstrapped companies, sometimes a decade or more after their founding, with examples outside of Galileo including 1Password, Qualtrics, Atlassian, GoFundMe and Tenable. Accel also led this type of round into payments platform Braintree, where the firm met the startup’s GM Juan Benitez, who also joined Galileo’s board in November along with Accel’s Locke.

Accel’s valuation of the deal was not publicly disclosed in November, but a source with knowledge of the acquisition today characterizes the firm’s return as more than 4x. Given that Accel held the equity for roughly half a year, that’s quite the IRR multiple in an otherwise challenging global macro context. Given that the acquisition of Galileo was for cash and stock, Accel likely now holds a stake in SoFi, making at least part of the return unrealized.

Galileo was represented by Qatalyst in the transaction.

Updated April 7 to include the $8 million Series A funding round led by Mercato Partners and more context on IRR.

Powered by WPeMatico

European fintech startup Revolut is launching its app and service in the U.S. Starting today, anybody can sign up and get a Revolut debit card. In the U.S., Revolut has partnered with Metropolitan Commercial Bank for the banking infrastructure — deposits are FDIC insured up to $250,000.

In just a few years, Revolut has managed to attract over 10 million customers by building a financial hub that lets you spend, send, receive and manage money from a single app. The company recently raised a $500 million funding round, valuing the company at $5.5 billion.

But the U.S. has been watching from the sidelines. Tens of thousands of customers have signed up to the waiting list and they’ll now be able to access all of Revolut’s core features.

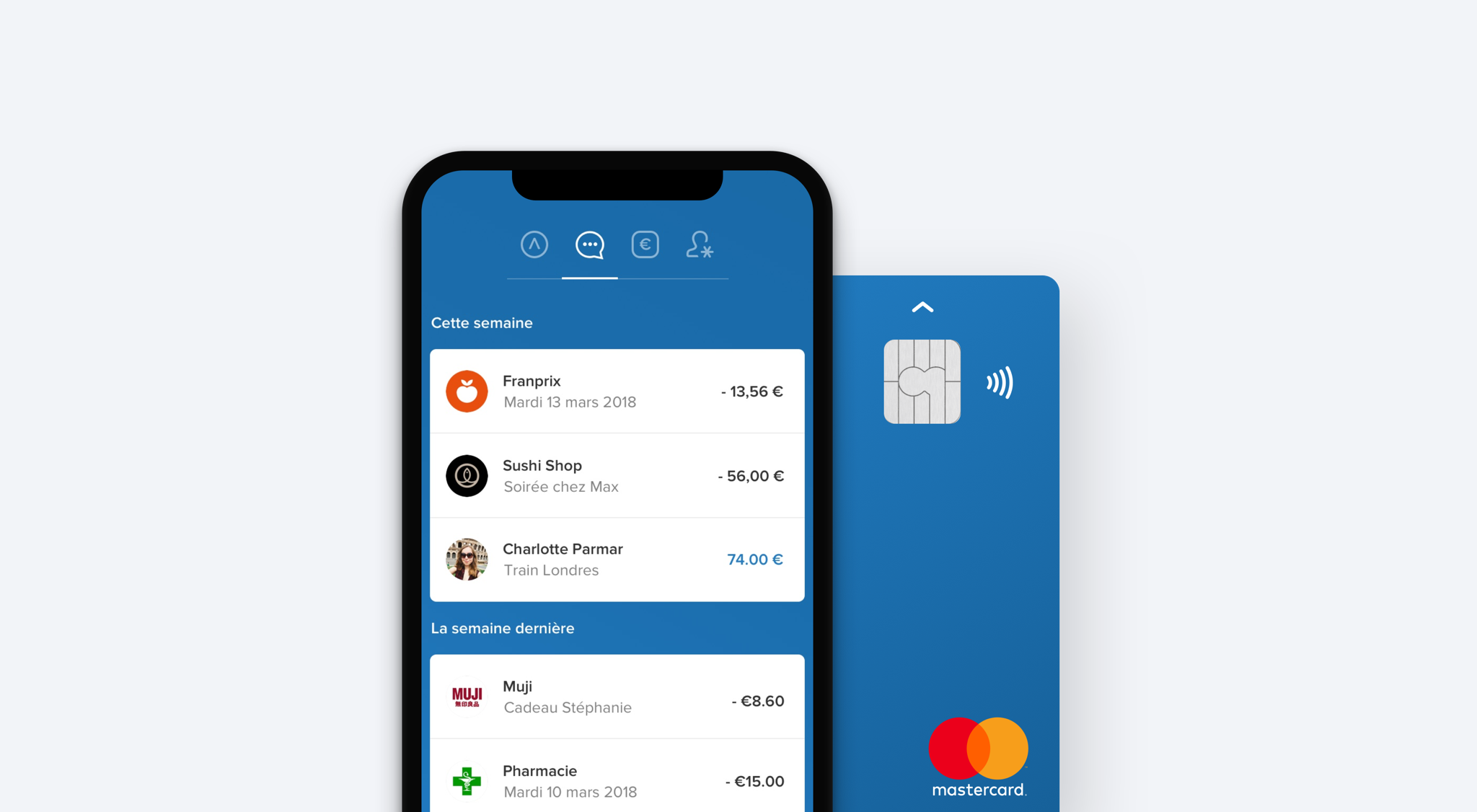

Like competing challenger banks, such as Chime and N26, Revolut lets you open an account from your phone. After downloading the app, you enter personal details and send a few official documents to comply with know-your-customer regulation.

After that, you get U.S. account details and you can instantly top up your account with a bank transfer or a card transfer. A few days later, you also receive a physical debit card. You can also generate a virtual debit card from the app.

Revolut lets you control your debit card from the app directly. You can receive notifications every time you make a transaction. You can freeze and unfreeze your card, set some limits and restrict some feature, such as online payments or ATM withdrawals.

One of Revolut’s key features is that you can convert from one currency to another based on interbank rate with a low fee — sometimes without any markup for popular currencies and small transactions (more details on foreign exchange fees here). You can hold foreign currencies in your Revolut account or send money to another Revolut user or a bank account in another country.

In the U.S., Revolut offers the ability to receive your salary two days in advance if you share your Revolut banking details with your employer.

Revolut offers a ton of additional features in Europe, but the company is starting with this basic feature set in the U.S. You can expect more features in the future, such as the ability to purchase cryptocurrencies and invest on the stock market.

In Europe, Revolut also offers insurance products through premium monthly subscriptions, mobile phone insurance, savings accounts, credit, rewards and more. Many of those features require partnerships with third-party companies. But it gives you an idea of Revolut’s roadmap in the U.S.

Powered by WPeMatico

When Visa bought Plaid this week for $5.3 billion, a figure that was twice its private valuation, it was a clear signal that traditional financial services companies are looking for ways to modernize their approach to business.

With Plaid, Visa picks up a modern set of developer APIs that work behind the scenes to facilitate the movement of money. Those APIs should help Visa create more streamlined experiences (both at home and inside other companies’ offerings), build on its existing strengths and allow it to do more than it could have before, alone.

But don’t take our word for it. To get under the hood of the Visa-Plaid deal and understand it from a number of perspectives, TechCrunch got in touch with analysts focused on the space and investors who had put money into the erstwhile startup.

Powered by WPeMatico

French startup Lydia is raising a $45 million Series B round (€40 million). Tencent is leading the round with existing investors CNP Assurances, XAnge and New Alpha also participating.

If you live in France, chances are you already know Lydia quite well. The company has become a ubiquitous mobile payment app, especially for people under 30 years old. Think about it as a sort of Square Cash or Venmo, but for France.

“At first, we wanted to raise less but we ended up raising more,” Lydia co-founder and CEO Cyril Chiche told me in a phone interview.

The company has managed to attract 3 million users in France. More impressive, 25% of French people between 18 and 30 years old have a Lydia account — and 5,000 people sign up every day. Lydia currently has 90 employees.

More recently, the company has expanded beyond peer-to-peer payment. First, the company wants to help you manage your money in many different ways with an important value — everything should happen in real time.

You can create multiple Lydia accounts to put some money aside or use money in that sub-account for a specific purpose. That feature alone turns the app into a versatile money management app.

For instance, you can associate a Lydia payment card with a Lydia account and a virtual card with another Lydia account — that virtual card works with Apple Pay, Google Pay, Samsung Pay and more. You can change those settings in real time.

You can share accounts with other Lydia users. And shared accounts are truly shared — everyone can top up and withdraw money from that account. You can spend directly from that account or withdraw money to another account.

You can also turn any Lydia account into a money pot account. In just a few taps, you can generate a link and share it with your friends so that they can add money using their regular payment card or a Lydia account.

More recently, the company has introduced “the market”, a marketplace of other financial products. From the Lydia app, you can borrow up to €1,000 in just a few seconds. You can also insure your phone and other mobile devices. You can get some free credit when you open a bank account, insure your home with Luko, switch to another electricity and gas provider, compare mobile phone and internet providers and more.

And that strategy is going to be key in the future. “We have an ambitious goal, which is turning Lydia into a mobile financial service app,” Chiche said.

He also pointed out that the company that has been the most successful when it comes to creating a mobile marketplace of financial products is Tencent with WeChat.

“Tencent is also the number one player in the video game industry, and there’s no industry with as much user engagement,” Chiche said. Tencent acquired Supercell, bought 40% of Epic Games, acquired Riot Games (League of Legends), invested in Ubisoft, Activision Blizzard, Discord, etc. Lydia hopes that it can learn from Tencent on the user engagement front.

Compared to many fintech startups, Lydia doesn’t want to replace banks altogether — the company says it wants to build a meta-banking app. Peer-to-peer payments represent the top of the funnel and a great user acquisition strategy thanks to networking effects.

You can then connect your Lydia account with your bank account and your debit card. This way, you can send money back and forth between your Lydia accounts and your bank account. As a user, that strategy slowly pays off over time. After a while, you end up spending money directly from your Lydia account and relying more heavily on Lydia’s native payment features, with your bank account acting as a money back end.

At the bottom of the funnel, Lydia hopes that it can turn active Lydia users into paid customers with a handful of in-house and third-party financial products. In other words, Lydia doesn’t want to become a credit institution like a traditional bank, it wants to become a financial hub. Expanding the marketplace will be a big focus for the company going forward.

While Lydia is available in other European countries, Lydia is still massively used in its home market with other markets lagging behind. With today’s funding round, growth in foreign countries is going to be the second key topic.

Powered by WPeMatico

Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

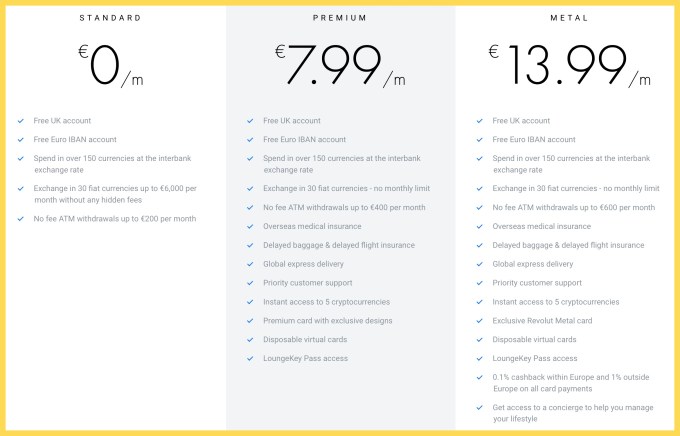

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Powered by WPeMatico