fintech

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday morning? Sign up here.

Ready? Let’s talk money, startups and spicy IPO rumors.

Every quarter we dig into the venture capital market’s global, national, and sector-based results to get a feel for what the temperature of the private market is at that point in time. These imperfect snapshots are useful. But sometimes, it’s better to focus on a single story to show what’s really going on.

Enter AgentSync. I covered AgentSync for the first time last August, when the API-focused insurtech player raised a $4.4 million seed round. It’s a neat company, helping others track the eligibility of individual brokers in the market. It’s a big space, and the startup was showing rapid initial traction in the form of $1.9 million in annual recurring revenue (ARR).

But then AgentSync raised again in December, sharing at the time of its $6.4 million round that the valuation cap had grown by 4x since its last round. And that it had seen 4x revenue growth since the start of the pandemic.

All that must sound pretty pedestrian; a quickly-growing software company raising two rounds? Quelle surprise.

But then AgentSync raised again this week, with another grip of datapoints. Becca Szkutak and Alex Konrad’s Midas Touch newsletter reported the sheaf of data, and The Exchange confirmed the numbers with AgentSync CEO Niji Sabharwal. They are as follows:

That means AgentSync was worth $22 million when it raised $4.4 million, and the December round was raised at a cap of around $80 million. Fun.

Back to our original point, the big datasets can provide useful you-are-here guidance for the sector, but it’s stories like AgentSync that I think better show what the market is really like today for hot startups. It’s bonkers fast and, even more, often backed up by material growth.

Sabharwal also told The Exchange that his company has closed another $1 million in ARR since the term sheet. So its multiples are contracting even before it shared its news.

2021, there you have it.

Also this week I got to meet Ariana Thacker, who is building a venture capital fund. Her route to her own venture shop included stops at Rhapsody Venture Partners, and some time at Predictive VC. Now she’s working on Conscience.vc, or perhaps just Conscience.

Her new fund will invest in companies worth less than $15 million, have some form of consumer-facing business model (B2B and B2B2C are both fine, she said), and something to do with science, be it a patentable technology or other sort of IP. Why the science focus? It’s Thacker’s background, thanks to her background in chemical engineering and time as a facilities engineer for a joint Exxon-Shell project.

All that’s neat and interesting, but as we cover zero new-fund announcements on The Exchange and almost never mini-profile VCs, why break out of the pattern? Because unlike nearly everyone in her profession, Thacker was super upfront with data and metrics.

Heck, in her first email she included a list of her investments across different capital vehicles with actual information about the deals. And then she shared more material on different investments and the like. Imagine if more VCs shared more of their stuff? That would rock.

Conscience had its first close in mid-January, though more capital might land before she wraps up the fundraising process. She’s reached $4 million to $5 million in commits, with a cap of $10 million on the fund. And, she told The Exchange, she didn’t know a single LP before last summer and only secured an anchor investor last October.

Let’s see what Thacker gets done. But at a minimum I think she’ll be willing to be somewhat transparent as she invests from her first fund. That alone will command more attention from these pages than most micro-funds could ever manage.

The week was super busy, so I missed a host of things that I would have otherwise liked to have written about. Here they are in no particular order:

Various and Sundry

Closing, I learned a lot about software valuations here, got to noodle on the epic Roblox direct listing here, dug into fintech’s venture successes and weaknesses, and checked out the Global-e IPO filing. Oh, and M1 Finance raised again, while Clara and Arist raised small, but fun rounds.

Powered by WPeMatico

Madrid-based TaxDown, which automates income tax filing by calculating regional deductions due to users so they don’t have to navigate complex tax rules themselves, has raised €2.4 million (~$3M) in seed funding.

US-based FJ Labs has joined TaxDown’s investment board as it closes the seed round. It says all its previous investors participated in the round, including James Argalas (Presidio Union); Abac Nest, Abac’s venture capital business; Baldomero Falcones, the former Chairman at Mastercard; and the founders of Jobandtalent, Juan Urdiales and Felipe Navío (another Madrid-based startup).

For the past three years TaxDown been offering a service in Spain but is now eyeing international expansion, as well as further growth in its home market.

Last year, it says it managed more than €29M in taxes for users — delivering savings of €4M+ to users.

Its target is to hit 500,000 users in Spain this year. While international expansion is planned for the second half of 2021, with TaxDown saying it’s focused on other European and Latin American markets.

“From the beginning, our ambition has been to help people fill in their taxes all over the world. That is why we developed our proprietary software/tax language that allows a tax expert with no coding capabilities to translate the tax law into calculation and logic that can be interpreted by our backend seamlessly,” says Enrique García, CEO and co-founder. “This tax language allowed us to launch in Spain in 4 months with only one tax consultant. We are confident that we can launch a new country in only 6 months.”

“The tax filing process is far from being simple,” he goes on, explaining how its tech simplifies income tax filing in Spain. “Currently, when using the Spanish Tax Agency tax-filling tool, taxpayers need to manually apply deductions on their tax forms. The problem is, with national regional deductions being different in each region in Spain, taxpayers often do not even know they’re entitled to those deductions. Thus, by not applying them to their tax form, they lose money. What TaxDown does is leverage the advanced Spanish Tax Agency technology, which offers an API to request the financial data related to a taxpayer — always with prior authorization from the user — with 2.000+ datapoints.

“Once we have that, our algorithm ‘RITA’ is capable of understanding the user’s personal and financial data, select the optimum questions that the user needs to answer — an average of 9 over a database of 3.000+ – and precisely calculate the tax return, with no errors.”

“Technology is the heart of TaxDown,” he adds. “Besides our algorithm RITA that has been trained with over 40.000+ tax returns, today we also use AI to help our ‘taxers’ with tips on how to lower future tax bills, and we have started working on live income tax simulation for our users throughout the entire year.”

García says TaxDown calculated more than 42,000 tax returns last year with a team of just two in-house tax experts — thanks to proprietary internal tools which allow them to handle this scale (by being “80x more efficient than the Spanish average”, as he puts it). He adds that further efficiency gains are expected.

“We have developed a machine-learning tool that flags the tax returns that need to be reviewed before filing based on historical data. Thus, we continuously increase the percentage of tax returns that are automatically submitted with no manual intervention,” he tells TechCrunch, adding: “Thanks to this feature, we expect to improve our efficiency at least 5x versus last year.”

According to García, TaxDown has never had any filings rejected for inaccuracies because he says its algorithms continually run tests and validate the information with the authorities. “Furthermore, our technology can flag errors in real time in case that there is a discrepancy, so our tax experts can manually check the tax return form if needed,” he adds.

Its business model — currently — is a sort of twist on freemium, in that it will only charge users if the income tax savings it calculates for them exceed €35.

García says that so far an average of three out of 10 users see financial savings from using its tool — but he suggests it’s not only savings that motivate users; he says they also want reassurance that they are taking “the best approach with their taxes: doing them effortlessly, correctly, with all the guarantees, tapping for experts’ live help at any time, ensuring the best result they can get, and of course knowing that we have their backs in case of an audit”.

Given that wider relationship it’s building with users, TaxDown sees potential to evolve its business model by expanding to offer additional fintech services, such as financial advice, in the future.

“Our vision goes far beyond income tax return preparation, we believe that tax data is becoming one of the most valuable data assets for people (take Trump’s tax returns for example), and we want to assess our ’taxers’ based on the best and more qualitative information that we can get,” says García. “Therefore, in the future we want to be a trusted financial advisor not just for taxes, but for personal finances as well. We believe we are well positioned to be an intermediary between our users and financial institutions.”

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here — and make sure to check out our Friday show that featured the Square-Tidal deal, some recent IPOs and some super-neat rounds.

Much like today’s show, if I am being honest. Here’s the rundown:

A packed kickoff to what promises to be a packed week!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

Fintech startup ClearGlass Analytics has closed a £2.6 million ($3.6 million) funding round for its platform, which aims to create greater transparency on fees in the long-term savings market, such as pensions and the wider asset management market.

The £2.6 million seed round includes European VC Lakestar and Outward VC, the venture arm of Investec, as well as several angels from both the asset management and pension fund worlds. These include Ruston Smith, a pension trustee; Richard Butcher, chair of the PLSA (U.K. pension trade body); Chris Wilcox, former Global Head of JP Morgan Asset Management; and Rob O’Rahilly, Sikander Ilyas and Alex Large, also former JP Morgan employees.

ClearGlass is targeting the £1.5 trillion mature “Defined Benefit” pension schemes market and claims to now work with more than 500 DB pension funds. It will use the funding to expand into the U.K. Defined Contribution pension market, and consolidate its early footprint in Europe and Africa.

How ClearGlass works is that it acts as a data interface between asset managers and their clients. Pension funds then use the platform to see all of their investment costs in one place, thus getting more data than usual from more asset managers and other suppliers. This helps the funds see the “true cost” of what they are paying for the management of their investments. ClearGlass claims to be able to uncover the kinds of costs of asset management that, in some instances, can be more than double those expected.

The startup recently did an analysis of the cost and performance of more than 400 asset managers. It found that while most U.K. asset managers were meeting minimum standards for data delivery, quality and accuracy, 30 (including some powerful players) did not pass their tests.

The company was founded by Dr. Christopher Sier, a World Bank and FCA expert who previously developed the cost transparency standard at the request of the FCA, and co-founders Ritesh Singhania and Kunal Varma.

Sier, founder and CEO, said: “Finding your costs are so much larger is shocking, but also something to be celebrated. These incremental costs were always there, they just weren’t exposed, and now you can identify those and bring about change. You can’t manage what you don’t measure.”

In an interview with TechCrunch, Ritesh Singhania, COO, said getting the data about pension funds is normally “super challenging and complicated. And second of all, even when you got the data, you couldn’t make head nor tail of it because you can’t compare it across funds. What we have done is that we have been the line of communication between the manager and the pension fund. So we have built a piece of technology that helps with the communication between the asset managers, and the pension funds to be able to collect that data, check that data. And finally, give them something that doesn’t require them to spend 20 hours to understand it.”

ClearGlass was incubated by the Founders Factory accelerator.

Powered by WPeMatico

Fintech startup Revolut has its own banking license in the European Union since late 2018. It lets the company offer some additional financial services without partnering with third-party companies. And the company is going to let customers switch to Revolut Bank in 10 additional countries.

The Bank of Lithuania has granted a specialized license — it isn’t a full-fledged license per se as it focuses on some activities. The company is taking advantage of European passporting rules to operate in other European countries. Right now, Revolut takes advantage of its banking license in two countries — Poland and Lithuania.

In Lithuania for instance, you can apply for a credit card with a credit limit that’s twice the value of your monthly salary (up to €6,000). The company also offers personal loans between €1,000 and €15,000. You can pay back over 1 to 60 months.

Now, customers in Bulgaria, Croatia, Cyprus, Estonia, Greece, Latvia, Malta, Romania, Slovakia and Slovenia will be able to become Revolut Bank customers. It’s not a transparent process as you need to get through a few steps to carry your account over.

But once this process is done, your deposits are protected under the deposit guarantee scheme. If Revolut Bank shutters at some point down the road, customers can claim up to €100,000 thanks to the scheme — both euros and foreign currencies are protected.

You can expect new credit products in the 10 new markets. Overall, Revolut has attracted 15 million customers. The company recently announced that it was also applying for a banking license in the U.K., its home country and its biggest market.

Powered by WPeMatico

The day before Robinhood goes under the the Congressional hammer, domestic rival Public.com announced this morning that it has closed a $220 million funding round at a $1.2 billion valuation. News of the round was first broken by TechCrunch. Further reporting colored in the lines concerning the investment’s size and valuation range.

Confirming the funding news today, Public added a fresh metric to the mix, namely that it has reached one million members – over the course of just 18 months post-launch, the company was quick to point out.

That means that Public’s backers – its latest round was put together by prior investors, including Greycroft, Accel, Tiger Global, Inspired Capital and others – values the company at around $1,200 per current “member.” Whether or not that feels rich, we leave to you to decide.

But with rising interest in the savings and investing space – some data here — and Robinhood’s revenues growing to a run rate of more than $800 million in Q4 2020 and looking even better at the start of 2021, it’s not hard to see why investors are backing Public. It’s even easier if you believe that Robinhood’s brand has undergone material harm from its woes during the GameStop saga.

The pair, along with a host of other fintech services that offer savings and investing products, have been buoyed by a secular shift in banking away from the physical world (in-person shopping, bank branches, plastic cards) to the digital (neo-banks, ecommerce, virtual cards). Robinhood shook up the trading world with zero-cost investing, fitting neatly into the mobile and virtual banking future that is being built. And Public has taken that model a step further by dropping payment for order flow (PFOF), a method revenue generation in which companies like Robinhood get a small fee for sending their users’ trades to one particular market maker or another.

TechCrunch recently joked that it seems like “there is infinite money for stock-trading startups,” in light of the anticipated Public round, which has now has arrived. Let’s see who is next to take home a big check.

Powered by WPeMatico

The hodl-crew are having quite the moment as bitcoin passed the $50,000 mark earlier today for the first time. Data pegs the peak at just over $50,500.

The price of bitcoin, the world’s best-known cryptocurrency, has historically proven a reasonable proxy for consumer interest in the cryptocurrency space, and for trading activity amongst blockchain-based assets. Bitcoin’s price has retreated since the milestone, and is now worth just over $49,000.

Bitcoin has been on a tear this year, rising from around the $30,000 mark at the start of 2021 to its recent $50,000 milestone, a gain of around 66%. Looking back a year and the gains are even more impressive, with the price of bitcoin rising from around $10,000 a year ago to its current price, a gain of 400%.

Luckily for investors and believers in other decentralized tokens, it’s not just bitcoin that is enjoying a valuation updraft. Cardano, one of the most highly valued blockchain assets, is up around 27% in the last week, according to CoinMarketCap. Its total value is nearing the $27 billion mark.

Companies built atop the burgeoning cryptocurrency space could be enjoying a boom as the price of bitcoin advances; as trading activity and consumer interest tend to rise along with the price of bitcoin, and companies like Coinbase make money from trading activity and consumer use, 2021 is starting off strongly.

Coinbase has filed to go public, and intends to pursue a direct listing in short order.

What’s driving up the price of bitcoin and its sister-tokens in the short-term? In a market melt-up its hard to point fingers with any accuracy. But broadly speaking, if it feels that nearly every asset class is setting new all-time records, so why not bitcoin as well?

Powered by WPeMatico

There’s always a fintech angle, even on Valentine’s Day.

This week, I covered Zeta, a new startup working on joint finances for modern couples. It aims to take away the money chores of a relationship, from splitting the bill at dinner to requesting rent through a payment app every month.

Aditi Shekar, the co-founder, gave me some notes about why the ongoing popularity of Venmo is validation for the company, instead of competition.

The success of Zeta hinges on the idea that people want to share their finances in an ongoing and meaningful way, and that the world of finance is ready to shift from individualism to collectivism earlier and louder. It sounds daunting, but we already know that social finance is big, as shown by apps like Venmo and Splitwise, and phenomena like the GameStop saga from just a few weeks ago.

Other startups have taken notice too, entering the world of multiplayer fintech, a term that categorizes socially focused and consumer-friendly financial services. Braid, a group-financing platform, is trying to make transactions work for various entities, from shared households to side hustles to creative projects.

Money is emotional and complex, and the opportunity within the multiplayer fintech reflects just that. The next wave of products will be able to straddle the line of comfort to successfully get adoption, and cultural shift to successfully deliver a truly collaborative cash experience.

(And in case that wasn’t enough Valentine’s Day content for you, here’s one more piece about a new dating app for gamers).

In the rest of this newsletter, we’ll talk about the new career path to CEO, our favorite startups from Techstars Demo Day and the latest SPAC you should probably know about. As always, you can find me on Twitter @nmasc_ or e-mail me at natasha.m@techcrunch.com. Want this in your inbox each week? Sign up here.

Data about startups is helpful to understand directional trends and how the flow of capital works and changes over time. But as ventures as an asset class grows and the documentation around raises gets thornier, the data can sometimes be missing a big chunk of what’s actually happening on the scenes.

Here’s what to know per Danny Crichton and Alex Wilhelm: PSA: most aggregate VC trend data is garbage and Are SAFEs obscuring today’s seed volume are two pieces that explain some of the reasons why the numbers might be flawed today. The good news is that the government is also in the dark about funding data; the bad news is that without good tracking, we don’t know how progress is being made.

Etc: Shameless plug for you to tip us on Secure Drop, TechCrunch’s submission system for any news you think is important to share. You can stay anonymous.

Image via Getty Images / Sadeugra

Amazon founder and CEO Jeff Bezos announced weeks ago that he was shifting into an executive chairman role and AWS CEO Andy Jassy would take over as chief executive. In this analysis, our enterprise cloud reporter Ron Miller explores the question: is overseeing cloud operations the new path to CEO?

Here’s what to know, per Andrew Bartels, an analyst at Forrester Research:

“In both cases, these hyperscale business units of Microsoft and Amazon were the fastest-growing and best-performing units of the companies. [ … ] In both cases, cloud infrastructure was seen as a platform on top of which and around which other cloud offerings could be developed,” Bartels said. The companies both believe that the leaders of these two growth engines were best suited to lead the company into the future.

Etc: Ember names former Dyson head as consumer CEO as the startup looks beyond the smart mug, and Monzo, the British challenger bank nearing 5 million customers, has recruited a new US CEO.

Image Credits: Amazon / Microsoft

TechCrunch covered favorites from Techstars’ three Demo Days, which were focused on Chicago, Boston and workforce development. Make sure to dig into the startups yourself to form your own opinions, but if you care what stood out to us, here’s what we ended up with.

Here’s what to know: The reason I love Demo Days is that it’s a fast way to understand what the next wave of startups and entrepreneurs are thinking about. In this year’s cohorts, we saw an exclusive sneaker marketplace, flexible life insurance and a part-time childcare platform that helps parents cover random gaps in their childcare schedule.

Etc: Without desks and a demo day, are accelerators worth it?

Image Credits: Paper Boat Creative (opens in a new window) / Getty Images

Archer Aviation, the electric aircraft startup targeting the urban air mobility market, is teaming up with United Airlines to become a publicly traded company via, you guessed it, a SPAC.

Here’s what to know per Kirsten Korosec, our transportation editor:

The agreement to go public and the order from United Airlines comes less than a year after Archer Aviation came out of stealth. Archer was co-founded in 2018 by Adam Goldstein and Brett Adcock, who sold their software-as-a-service company Vettery to The Adecco Group for more than $100 million. The company’s primary backer was Lore, who sold his company Jet.com to Walmart in 2016 for $3.3 billion. Lore was Walmart’s e-commerce chief until January.

Etc: Bumble priced and Nigeria’s IROKO plans to go public on the London Stock Exchange.

Use cloud foam to dollar sign

Seen on TechCrunch

Seen on Extra Crunch

SoftBank earnings always give key insights about how a heavyweight in venture capital is performing (and the bonanza always comes with a healthy share of content and memes). This week on Equity, we couldn’t resist nerding out about it:

Of course, if SoftBank isn’t your jam, there was a whole host of other news we chatted about, from Reddit’s latest raise to DoorDash buying a salad robot. Listen here.

Until next week,

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Natasha and Danny and Alex and Grace were all here to chat through the week’s biggest tech happenings. This week felt oddly comforting from a tech news perspective: Facebook is copying something, early-stage startup data is flawed enough to talk about and sweet DoorDash is buying robots for undisclosed sums.

So, here’s a rundown of the tech news we got into (as always, jokes aren’t previewed so you’ll have to listen to the actual show to get our critique and Award Winning Analysis*):

In good news, long-time Equity producer Chris Gates is back starting next week, which means we’ll have our biggest crew ever helping get the show put together. And, in other good news, there’s going to be more Equity than ever for you to hear. Coming soon.

Equity drops every Monday at 7:00 a.m. PST and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

*OK, so not award-winning yet. But soon enough, because manifestation works.

Powered by WPeMatico

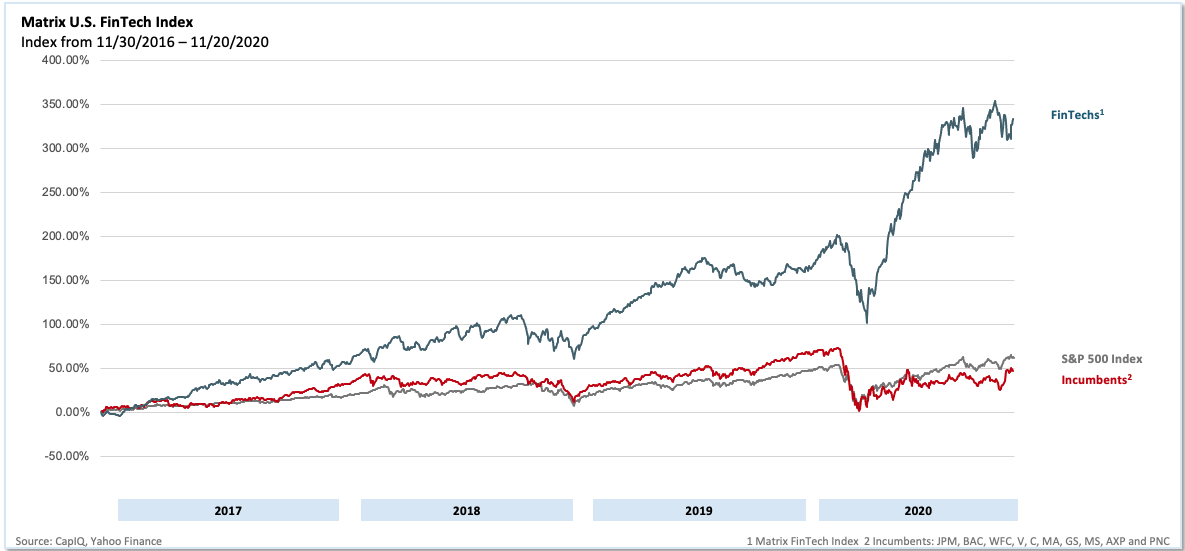

Three years ago, we released the first edition of the Matrix Fintech Index. We believed then, as we do now, that fintech represents one of the most exciting major innovation cycles of this decade. In 2020, all the long-term trends forcing change in this sector continued and even accelerated.

The broad movement away from credit toward debit, particularly among younger consumers, represents one such macro shift. However, the pandemic also created new, unforeseen drivers. Among them, millennials decamped from their rentals in crowded cities to accelerate their first home purchases to the benefit of proptech companies and challenger mortgage players alike.

E-commerce saw an enormous acceleration in growth rates, furthering adoption of online payments platforms. Lastly, low interest rates and looming inflation helped pave the way for the price of Bitcoin to charge toward $30,000. In short, multiple tailwinds combined to produce a blockbuster year for the category.

In this year’s refresh of the Matrix Fintech Index, we’ll divide our attention into three parts. First, a look at the public stocks’ performance. Second, liquidity. Third, we highlight one major trend in the sector: Buy Now Pay Later, or BNPL.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index. While the underlying performance of these companies was strong, the pandemic further bolstered results as consumers avoided appearing in-person for both shopping and banking. Instead, they sought — and found — digital alternatives.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index.

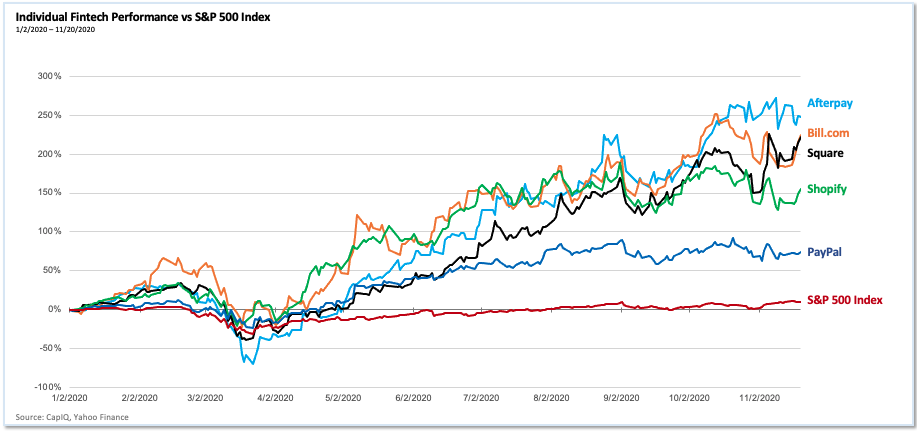

Our own representation of the public fintechs’ performance is the Matrix Fintech Index — a market cap-weighted index that tracks the progress of a portfolio of 25 leading public fintech companies. The Matrix fintech Index rose 97% in 2020, compared to a 14% rise in the S&P 500 and a 10% drop for the incumbent financial service companies over the same time period.

2020 performance of individual fintech companies vs. SPX Image Credits: CapiQ, Yahoo Finance

Matrix U.S. Fintech Index, 2016 -2020 Image Credits: CapiQ, Yahoo Finance

E-commerce undoubtedly stood out as a major driver. As a category, retail e-commerce grew 35% YoY as of Q3, propelling PayPal and Shopify to add over $160 billion of market capitalization over the year. For its part, PayPal in the third quarter signed up 15 million net new active accounts (its highest ever).

Powered by WPeMatico