Finance

Auto Added by WPeMatico

Auto Added by WPeMatico

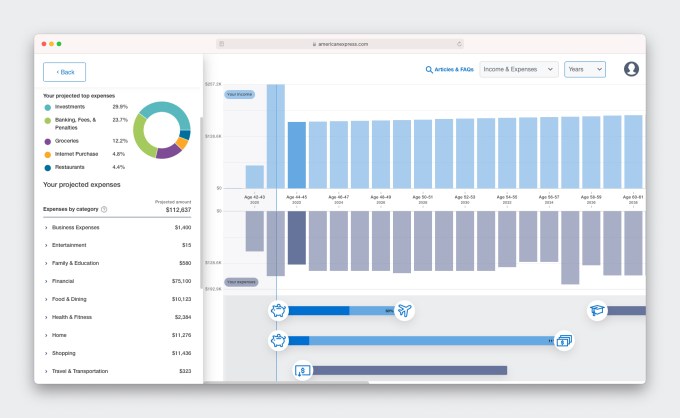

American Express is branching out into financial planning, with a little help from a seven-person startup called BodesWell.

This week, the credit card giant launched a pilot of its first self-service digital financial planning tool, dubbed “My Financial Plan (MFP).” The six-month pilot kicked off on July 11 with about 25,000 select Amex cardmembers.

American Express quietly invested in BodesWell in late 2020 via its venture arm, Amex Ventures. Since then, the financial services behemoth teamed up with the tiny startup to develop the financial planning tool for its users. The new product is designed to give users a complete picture of their financial health and help them make and achieve major life goals, such as buying a house or retirement.

TechCrunch talked with Amex Ventures’ Julia Huang, who led the investment and strategy around the new product, and BodesWell co-founder and CEO Matthew Bellows to learn more details.

The pair actually met while serving on a panel together in 2019.

“I was drawn to the fact that it was not a round-up savings tool, but rather a holistic tool to understand your full financial picture that could be used to plan for the financial impact of your life decisions,” Huang told TechCrunch.

Before deciding to invest in BodesWell, Huang says Amex Ventures — which over time has backed more than 70 startups — had “evaluated the space quite extensively.”

Huang introduced Bellows and his staff to Amex’s Digital Labs team and they embarked on jointly developing a specialized offering for Amex customers. (While Bellow is based in Boston, he says the startup is “globally distributed.”)

“Our goal is to democratize financial planning with our cardmembers by providing detailed insights and forecasts to help them with their holistic planning,” she told TechCrunch.

Image Credits: Amex Ventures

Bellows started BodesWell in early 2019 with the goal of empowering clients and customers to build their own financial plan.

“So much of financial planning software is aimed at financial advisors, and requires them to run it,” he said. “So, most people can’t get the benefits of financial planning…Our hope is to expand benefits to a lot more people.”

BodesWell will guide users in setting up a financial plan and will work even better if they sync with their other financial information via Plaid so it can “update in real time,” Huang said.

The tool “takes into account income, assets, expenses and liabilities — what cash flow looks like holistically so that users can drag & drop to plan life events,” Bellow said.

An estimated 85 million American households don’t have a financial, planner for a variety of reasons — including mistrust of a planner’s intentions or just feeling overwhelmed by the process.

The product is free during the pilot phase and American Express hasn’t yet determined if it will charge for it afterwards.

“We’re gauging first for engagement and the power of the product for our customers,” Huang told TechCrunch. “We want to make sure the product resonates and that we iterate on the product to make sure it’s good for the broader population. Our primary goal is that our customers use it and find it valuable.”

Amex Ventures has formed “some level of partnership” with more than two-thirds of its portfolio companies, she added.

“We try to engage with our portfolio in that way, to provide value with our startup ecosystem,” Huang said.

For its part, BodesWell had previously raised about $1.5 million from investors such as Cleo Capital, Ex Ventures, Riot.vc, GritCapital and Argon Capital and angels like HubSpot CEO Brian Halligan and Kintent CEO Sravish Sridhar.

Powered by WPeMatico

News broke this morning that Revolut, a U.K.-based consumer fintech player, raised a Series E round of funding worth $800 million at a valuation of $33 billion. Those figures are breathtaking not only due to their sheer scale, but also thanks to their radical divergence from Revolut’s preceding funding event.

At times, The Exchange, TechCrunch’s markets-and-startups column, runs into two topics worth exploring in a single day. Today is such a day. You can check out our earlier notes on the buy now, pay later startup market and Apple’s entrance into the BNPL space here. Now, let’s talk about neobanks.

As TechCrunch’s Ingrid Lunden wrote earlier today concerning the news:

This latest Series E is being co-led by Softbank Vision Fund 2 and Tiger Global, who appear to be the only backers in this round. It comes on the heels of rumors earlier this month Revolut was raising big. Revolut last raised about a year ago, when it closed out a Series D at $580 million, but what is stunning is how much its valuation has changed since then, growing 6x (it was $5.5 billion last year).

Stunning indeed.

Lunden also went on to report on the company’s changing financial picture based on Revolut’s recently released 2020 results. In this entry, we’re digging more deeply into those financial results and usage metrics detailed by the fintech megacorn.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The picture that emerges is one of a company with a rapidly improving financial image, albeit with some blank spaces regarding recent customer growth.

Powered by WPeMatico

The gamification of payments is not a new concept.

A number of companies are attempting to combine gamification and payments in creative ways. And today, one such company, Play2Pay, has raised $13 million in a Series A round of funding.

The Miami-based startup has a straightforward mission. It wants to give consumers a way to reduce their bills — it claims by an average of 30%! — by playing games, watching videos and completing daily challenges, offers and surveys.

Play2Pay was bootstrapped for the first five years of its life, raising its first external capital in June of 2020 — a $7.5 million seed round from individual angel investors. Telesoft Partners led its Series A round, which included participation from Harbor Spring Capital and individual investors including former AT&T vice chairman Ralph de la Vega, former Reuters CEO Tom Glocer, Madison Dearborn Partners co-founder and senior advisor Jim Perry and Virtusa founder and former CEO, Kris Canekeratne.

The alternative payment platform says it brokers a “value exchange” between brands and consumers, converting attention and engagement into a currency, which can be redeemed for bill payment. Meanwhile, brands get a new way to promote their products and services.

Play2Pay founder and CEO Brian Boroff started the company in 2015 based on a vision that prepaid mobile phone users should have an alternative way to pay for their mobile phone service and that wireless carriers would adopt an ad-funded commercial model.

Today, the company claims to be positioned to be the world’s first “ad supported payment rail” directly integrated into payments platforms of major service providers and financial institutions. It also claims to be the only company that converts user engagement directly into bill payment.

Image Credits: Play2Pay

The “opt-in” offering is currently available to more than 100 million mobile subscribers across the United States, United Kingdom, Mexico, Brazil and Indonesia through partnerships with telecom companies such as AT&T Mexico, Cricket in the U.S., TIM in Brazil, lndosat Ooredoo in Indonesia and U.K.-based Lycamobile.

The rewarding approach seems to be resonating with users. From June 2020 to June 2021, the startup saw its ARR (annual recurring revenue) spike by nearly 300%, according to Boroff, a telecom veteran.

Among the users engaged on the platform, about 25% generated revenue daily, he said. And service providers realized up to 17% revenue expansion as a result of subscriber engagement on the Play2Pay platform, according to Boroff.

“Our distribution model is B2B2C, with Tier-1 service providers worldwide directly integrating our bill payment capability. We’re growing our audience through promotion of the service to their customer base,” he told TechCrunch.

End users, he added, can share their targeting preferences in exchange for value, giving mobile app developers and brands more information when promoting their own products and services to Play2Pay’s audience.

The platform is free for service providers and merchants, meaning the payment does not have costs or fees from interchange, acquirers, chargebacks or gateways.

Instead, Play2Pay generates revenue from mobile app developers and brands. Those developers and brands pay to access Play2Pay’s mobile audience in order to promote their products and services. For example, a mobile gaming company might pay Play2Pay $100 for every user that downloads their app from the Play2Pay app and plays the game for a period of time (such as two hours). Through its technology and partner network, Play2Pay has attribution tracking to ensure that the end user and mobile gaming company both know how much progress has been made toward completing that goal. Other formats include watching videos, completing surveys and more conventional native advertising in some areas.

Powered by WPeMatico

Financial services as a service — where entities like neobanks, retailers and others can create and sell their own financial products by way of a few lines of code and APIs — has been one of the bigger trends in the world of fintech in recent years, with embedded finance on its way to being a $7.2 trillion market by 2030, according to a forecast from Bain Capital. Now, one of the companies building and providing those APIs is announcing some growth funding to expand.

Railsbank, which builds APIs for banking, payment cards and credit products for use by fintechs but also a wide range of other kinds of businesses, has raised $70 million in new equity funding, money that the London startup plans to use to continue growing internationally and to add more features to its product set.

“Our mission is to reinvent, unbundle and democratise access to the complex, opaque and byzantine 70-year-old credit card market, which is worth $4 trillion in the U.S. alone,” Nigel Verdon, CEO and co-founder of Railsbank, told TechCrunch in an interview last year. Verdon is a repeat entrepreneur, with one of his previous companies being Currency Cloud.

Railsbank not disclosing its valuation, but Verdon hints that it is in the high hundreds of millions and close to $1 billion.

“As a policy, we rarely talk about valuation as we prefer to talk about customers,” he told TechCrunch today. “Valuation is a very inward-facing and self-centered metric. Saying that, near-unicorn would best describe us today.”

As a point of comparison data from PitchBook noted that the company was valued at just under $200 million in its last round at the end of last year (we reported on it here).

This latest round is being led by Anthos Capital, a previous backer of the company, with Central Capital, Cohen and Company, and Chris Adelsbach’s fund Outrun Ventures, as well as other unnamed previous backers also participating. Central Capital is a strategic investor: It’s the VC arm of the largest privately held bank in Indonesia, while Cohen and Company is the founder of Bancorp. Those backers speak to where Railsbank is targeting its services and who is interested in potentially working with it.

Banking as a service, and other financial products as a service, has become one of the most significant building blocks not just in the world of fintech, but in financial services overall. As with Twilio or Sinch in communications, or Stripe in payments, the idea here is that financial specialists have built out the complicated infrastructure and partnerships that underpin a product like a credit card, or a banking account.

This is then packaged up in a service that can be integrated into another one by way of an API, and the small amount of code needed to add it to another platform. In turn, that API can be used not just by another financial services company that is consumer- or business-facing, but by any kind of company that sees offering a financial product as part of a bigger customer service and loyalty play. That could mean a retailer offering its own-brand credit card, but also a “neobank” that is building a slick front end with great customer service and personalization, without needing to build the now-commoditized banking infrastructure underneath it to run it.

Railsbank is far from being the only company that has identified and built around this concept. Other big players include Rapyd, which raised a big round at a $2.5 billion valuation earlier this year; Unit, which also has been picking up funding and growing; FintechOS, which really does what its name says; and the startup 10x was even built for incumbent players to also have access to lighter fintech as a service.

Railsbank believes its distinct from many of its would-be competitors in part because it has built a lot of its own infrastructure from the ground up (hence the “rails” in its name), “bypassing” legacy players, in contrast to others that are built as software that still ultimately runs on top of stacks (and inefficiencies) of those older providers. This also means that it is regulated as a financial institution.

Railsbank is also in the business of making some acquisitions in order to grow its business, for example acquiring the U.K. business of German fintech Wirecard when it was crashing due to financial malpractices. And it doesn’t build everything from scratch: Earlier this year it also partnered with Plaid to embed some of its services within Railsbank’s.

Railsbank does not disclose a full list of customer names but has case studies on a number of smaller clients that speak to just how widely proliferated financial services are today. They include GoSolo, Kyshi and SimpledCard.

“The market has evolved so rapidly since we founded the world’s first BaaS business, the Bancorp,” noted Betsy Cohen, chairman of Fintech Masala and founder of Bancorp, in a statement. “As we move into the $7 trillion embedded finance market, it has been great watching Railsbank’s growth story. With this investment, it’s a privilege to continue to be part of the journey with a global leader like Railsbank.”

Powered by WPeMatico

Technology plays a huge role in nearly every aspect of financial services today. As the world moved online, tools and infrastructure to help people manage their money and make payments have burgeoned the world over in the past decade.

With much of the finance world now leveraging technology to conduct business, predict trends and deliver services, financial services regulators are also developing new technologies to monitor markets, supervise financial institutions and conduct other administrative activities. The emergence of purpose-built technologies to facilitate regulator oversight has, over the past few years, garnered its own moniker of supervisory technology, or suptech.

Interest in suptech is proliferating across the globe thanks to a diverse set of prudential and conduct regulators. A sampling of regulators developing suptech include the FDIC, CFPB, FINRA and Federal Reserve in the U.S.; the U.K.’s FCA and Bank of England; the National Bank of Rwanda in Africa; as well as the ASIC, HKMA and MAS in Asia. Several “super regulators” are also engaged in suptech efforts such as the Bank of International Settlements, the Financial Stability Board and the World Bank.

The strides in suptech demonstrate that creative thinking coupled with experimentation and scalable, easily accessible technologies are jump-starting a new approach to regulation.

In this post, we’ll examine a few core suptech use cases, consider its future and explore the challenges facing regulators as the market matures. The uses are diverse, so we’ll focus on three key areas: regulatory reporting, machine-readable regulation, and market and conduct oversight.

A quick general note: Nearly every financial services regulator is engaged in some type of suptech activity and the use cases discussed in this article are intended as a sample, not a comprehensive list.

As a preliminary matter, we should quickly survey a few definitions of suptech to frame our understanding. Both the World Bank and BIS have offered definitions that provide useful outlines for this discussion. The World Bank states that suptech “refers to the use of technology to facilitate and enhance supervisory processes from the perspective of supervisory authorities.” It’s a little circular, but helpful.

The BIS defines suptech as “the use of technology for regulatory, supervisory and oversight purposes.” This is a similarly loose definition that describes the broader scope better.

Regardless of differences on the margins, the “sup” in these suptech definitions acknowledges the primacy of the idea that regulators’ objectives are to oversee the conduct, structure, and health of the financial system. Suptech technologies facilitate related regulatory supervision and enforcement processes.

Regulatory reporting refers to a broad swath of activities such as financial firms providing trading data to regulatory authorities and regulators’ analysis of financial data or corporate information to determine the projected health or potential risks facing an institution or the market.

The MAS and FDIC are incorporating transactional and financial data reported by firms as a means to assess their financial viability. The MAS, in conjunction with BIS, has run tech sprints soliciting new ideas relating to regulatory reporting, while the FDIC has “a regulatory reporting solution that would allow ‘on-demand’ monitoring of banks as opposed to being constrained by ‘point-in-time’ reporting. This project is particularly targeted at smaller, community banks that provide only aggregated data on their financial health on a quarterly basis.”

The HKMA recently outlined its three-year plan for the development of suptech, which includes developing an approach to “network analysis.” The HKMA will analyze reporting data related to corporate shareholding and financial exposure to bring them “to life as network diagrams, so that the relationships between different entities become more apparent. Greater transparency of the connections and dependencies between banks and their customers will enable HKMA supervisors to detect early warning signals within the entire credit network.”

These reporting initiatives touch on a theme regulators have continuously struggled with: How to regulate markets and firms based on a reactive approach to historical data. Regulation and enforcement are often retrospective activities — examining past behavior and data to decide how to sanction an organization or develop a regulatory framework to govern a particular type of activity or financial product. This can result in an approach to regulation too rooted in past failures, which might lack the flexibility to anticipate or adapt to emerging risks or financial products.

Powered by WPeMatico

In the wake of Coinbase’s direct listing earlier this year, other crypto companies may be looking to go public sooner than later. That appears to be the case with Circle, a Boston-based technology company that provides API-delivered financial services and a stablecoin.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Circle will not direct list or pursue a traditional IPO. Instead, the company is combining with Concord Acquisition Corp., a SPAC, or blank-check company. The transaction values the crypto shop at an enterprise value of $4.5 billion and an equity value of around $5.4 billion.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

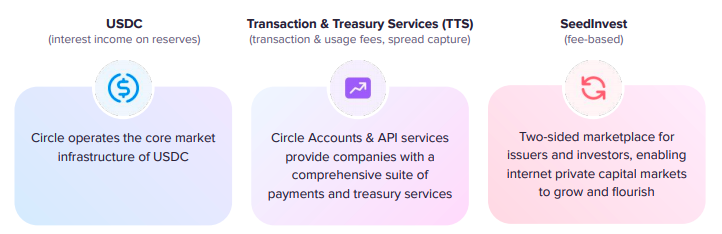

Circle’s SPAC presentation details a company whose core business deals with a stablecoin — a crypto asset pegged to an external currency, in this case, the U.S. dollar — and a set of APIs that provide crypto-powered financial services to other companies. It also owns SeedInvest, an equity crowdfunding platform, though Circle appears to generate the bulk of its anticipated revenues from its other businesses.

For more on the deal itself, TechCrunch’s Romain Dillet has a piece focused on the transaction. Here, we’ll dig into the company’s investor presentation, talk about its business model, and riff on its historical and anticipated results and valuation multiples.

In short, we get to have a little fun. Let’s begin.

As noted above, Circle has three main business operations. Here’s how it describes them in its deck:

Image Credits: Circle investor presentation

Let’s consider each one, starting with USDC.

Stablecoins have become popular in recent quarters. Because they are pegged to an external currency, they operate as an interesting form of cash inside the crypto world. If you want to have on-chain buying power, but don’t want to have all your value stored in more volatile, and tax-inducing, cryptos that you might have to sell to buy anything else, stablecoins can operate as a more stable sort of liquid currency. They can combine the stability of the U.S. dollar, say, and the crypto world’s interesting financial web.

Powered by WPeMatico

Amsterdam-based challenger bank Bunq has been self-funded by its founder and CEO Ali Niknam for several years. But the company has decided to raise some external capital, leading to the largest Series A round for a European fintech company.

The startup is raising $228 million (€193 million) in a round led by Pollen Street Capital. Bunq founder Ali Niknam is also participating in the round — he’s investing $29.5 million (€25 million) while Pollen Street Capital is financing the rest of the round.

As part of the deal, Bunq is also acquiring Capitalflow Group, an Irish lending company that was previously owned by … Pollen Street Capital.

Founded in 2012, Ali Niknam has already invested quite a bit of money into his own company. He poured $116.6 million (€98.7 million) of his own capital into Bunq — that doesn’t even take into account today’s funding round.

But it has paid off as the company expects to break even on a monthly basis in 2021. The company passed €1 billion in user deposits earlier this year. So why is the company raising external funding after turning down VC firms for so many years?

“Everything has a right time. In the beginning of Bunq, it was important to get a laser user focus in the company. Having to also focus on fundraises and the needs of investors distracts. Bunq now is mature enough to start scaling up significantly, so more capital is welcome,” Niknam said.

In particular, the company expects to acquire smaller companies to fuel its growth strategy. Challenger banks have also represented a highly competitive market over the past years in Europe. It’s clear that there will be some consolidation at some point.

Bunq offers bank accounts and debit cards that you can control from a mobile app. It works particularly well if your friends and family are also using Bunq as you can instantly send money, share a bunq.me payment link with other people, split payments and more.

In particular, if you’re going on a weekend trip, you can start an activity with your friends. It creates a shared pot that lets you share expenses with everyone. If you live with roommates, you can also create subaccounts to pay for bills from that account.

The company offers different plans that range from €2.99 per month to €17.99 per month — there’s also a free travel card with a limited feature set. By choosing a subscription-based business model, the startup has a clear path to profitability as most users are paid users.

Powered by WPeMatico

Influential entrepreneurs like Paul Graham and Naval Ravikant always preach the need for startups to have founders-turned-investors on their cap table. As Ravikant puts it, “founders want to know that the people they are taking money from have first-hand experience.”

His platform AngelList has helped individual founders-cum-investors source and participate in deals via collectives. However, some venture firms have taken this up a notch by bringing founders to create a fund and invest together.

Today, one of such, MAGIC Fund, a global collective of founders, is announcing that it has raised a second fund of $30 million to continue backing early-stage startups across Africa, Europe, Latin America, North America, and Southeast Asia.

Since the firm’s first fund launched in 2017, MAGIC has invested in 70 companies at pre-seed and seed stages across these emerging markets. Some of these companies include Retool, Novo, Payfazz, and Mono.

MAGIC Fund has 12 founders who act as general partners. TechCrunch caught up with managing partner Adegoke Olubusi and operating partner Matt Greenleaf to learn more about the fund’s thesis and activities.

Olubusi, who had built and exited a couple of startups over the years, also dabbled with angel investing for some time. In 2017, Olubusi’s current startup Helium Health got accepted into Y Combinator. It was there he met more founders like him who were angel investors with impressive portfolios. The interesting bit? Each founder wanted to invest in other companies during YC’s Demo Day.

“So about three years ago, I was at YC, and I was going to invest in my own batch. I was pitching on the day, but I was also listening to other pitches. However, it wasn’t just me; there were many other founders as well,” Olubusi said.

After building and exiting multiple startups, some founders turn into angel investing to support startups and their ecosystems. However, most of them tend to go alone and are stuck with cutting checks in their local markets, which limits opportunities.

Some MAGIC portfolio companies

Here’s a scenario. In 2016, when unicorns Flutterwave and Kavak raised their seed rounds in Nigeria and Mexico respectively, an African biotech founder who knew about Kavak and a Latin American edtech founder interested in African fintech would not have had the capacity to evaluate those deals even if they wanted; the reason being a lack of reach and experience in both the industry or geography.

Olubusi and the other founders knew this would be a limitation in the long run if they went solo. Thus, they decided to create MAGIC. The idea was to bring global founders together with diverse skillsets in diverse industries and geographies to evaluate deals better and drive value for each other. Hence, they can participate in two unicorns instead of one.

“Instead of us investing individually because obviously, we have somewhat limited capacity in terms of how much time we have as founders because of our respective companies, why don’t we collaborate on a strategy together and co-invest together?”

“The way we thought of MAGIC was a fund of micro funds built by founders for founders,” Greenleaf continued.

In some of the personal conversations I’ve had with founders about their investors, a recurring theme has been that the most useful investors didn’t necessarily sign the biggest checks. It’s a theme Olubusi also relates to all too well.

“It was like every time we think about it, everyone who gave the most money rarely had time for us. It was so frequent that we all identified this as an actual thing. What actually drove value for us were other investors who were founders and operators, and other experienced people who were able to help us find product-market fit and fight regulators. These were actually the people in the trenches with us.”

Olubusi believes the early-stage part of investing, particularly in pre-seed and seed, is where VCs who are founder-operators find their sweet spot. They are precious when startups are trying to figure out product-market fit. And unlike traditional investors who are looking to get multiples on investments, Olubusi argues that for founders-investors, what matters is how much value they can drive for startups.

Image Credits: MAGIC Fund

MAGIC’s play is even more essential considering that it also plays in emerging markets where on-the-ground operational help is needed in industries with numerous unknowns and uncertainties.

“There is so much money in the market now and early-stage decision making at pre-seed and seed should be left in the hands of founders. Because think about it really, to make an evaluation of whether I should invest in a healthcare or fintech company in Africa, it makes sense to have those who’ve spent years battling through it in the trenches make those decisions. And what we’re trying to do with the fund is publish as much information as possible and keep performing at the 100 percentile and say this is still the best strategy and is very scalable.”

MAGIC Fund 1 was $1.5 million and Olubusi says the investments performed 5x over the period of three years. As some of these companies exited, their founders invested in MAGIC and came on board as Fund 2 partners.

MAGIC has also enlisted additional investors who, according to Olubusi, are respected for their investing abilities and ecosystem support. For instance, Olugbenga Agboola, Flutterwave CEO, is known across the African tech ecosystem as a founder who goes out of his way to help established and up-and-coming fintech companies. Hendra Kwik of Payfazz has such a reputation in Southeast Asia as well. They, alongside other founders, join MAGIC as limited partners.

Per the firm’s statement, one-third of the entire fund was contributed by the founder GPs. For its LPs, diversity play is considered as 50% of them are black while 33% are women. Some of them include Michael Seibel, Tim Draper, Rappi’s Andres Bilbao, Paystack’s Shola Akinlade, Katie Lewis, and Octopus Ventures’ Kirsten Connell. For its partners, MAGIC has brought on the likes of Stitchroom’s Tom Chen, Medumo’s Adeel Yang, Juice’s Michael Lisovetsky, and Troy Osinoff, and Evercare’s Temi Awogboro.

Magic Fund 2 will be writing $100,000 to 300,000 checks at pre-seed and seed stages focusing on fintech, healthcare, SaaS and enterprise, women’s health, developer tools.

What does the fund look for in founders? Olubusi gives two answers. One, MAGIC wants to back founders with incentives to stick through the hard times of a company.

“At pre-seed and seed, you don’t have enough data about a company to make an investment decision. Your bet is entirely on the founder and the founding team. What we know, having done this several times, is that things get harder. So when we’re looking at the founder, we’re evaluating whether or not the founder has the grit to stick through the toughest times which are going to come up.”

The second indicator factors if the founder has the willingness, openness, the flexibility to learn and use that knowledge to succeed. Greenleaf believes these strategies have incredibly helped the firm fund exceptional companies and maintain good relationships with founders.

“Most of these founders don’t view us as their investors. They view us as fellow founders who are helping them along their journey. I think that also ties into them keeping it real with us and allows us to see them as people, and not just founders. That’s one of the things that have worked in our favor,” he said.

Powered by WPeMatico

TechCrunch Early Stage is coming up soon, and all attendees can get 3 months of free access to Extra Crunch as a part of a ticket purchase. Extra Crunch is our members-only community focused on founders and startup teams.

Head here to buy your ticket to TC Early Stage.

Extra Crunch unlocks access to our investor surveys, private market analysis, and in-depth interviews with experts on fundraising, growth, monetization and other core startup topics. Get feedback on your pitch deck through Extra Crunch Live, and stay informed with our members-only Extra Crunch newsletter. Other benefits include an improved TechCrunch.com experience and savings on software services from AWS, Crunchbase, and more.

Learn more about Extra Crunch benefits here, and buy your TC Early Stage tickets here.

What is TC Early Stage?

TC Early Stage is a two-day virtual event where early-stage founders can take part in highly interactive group sessions with top investors and ecosystem experts. This particular Early Stage event has a focus on marketing and fundraising.

The event will take place July 8-9, and we’d love to have you join.

View the event agenda here, and purchase tickets here.

Once you buy your TC Early Stage pass, you will be emailed a link and unique code you can use to claim the free 3 months of Extra Crunch.

Already bought your TC Early Stage ticket?

Existing pass holders will be emailed with information on how to claim the free 3 months of Extra Crunch membership. All new ticket purchases will receive information over email immediately after the purchase is complete.

Already an Extra Crunch member?

We’re happy to extend a free 3 months of access to existing users. Please contact extracrunch@techcrunch.com, and mention that you are an existing Extra Crunch member who bought a ticket to TC Early Stage 2021: Marketing and Fundraising.

Powered by WPeMatico

Whether you are part of the accounting department, or just any employee at an organization, managing expenses can be a time-consuming and error-filled, yet also quite mundane, part of your job. Today, a startup called Pleo — which has built a platform that can help some of that work more smoothly, by way of a vertically integrated system that includes payment cards, expense management software, and integrated reimbursement and pay-out services — is announcing a big round of growth funding to expand its business after seeing strong traction.

The Copenhagen-based startup has raised $150 million — money that it will be using to continue building out more features for its users, and for business development. The round, which sets a record for being the largest Series C for a Danish startup, values Pleo at $1.7 billion, the startup has confirmed.

There are around 17,000 small and medium businesses now using Pleo, with companies at the medium end of that numbering around 1,000 employees. Now with Pleo moving into slightly larger customers (up to 5,000 employees, CEO Jeppe Rindom, said), the startup has set an ambitious target of reaching 1 million users by 2025, a very lucrative goal, considering that expenses management is estimated to be a $80 billion market in Europe (with the global opportunity, of course, even bigger).

It will also be using the funds simply to expand its business. Pleo has around 330 employees today spread across London, Stockholm, Berlin and Madrid, as well as in Copenhagen, and it will be using some of the investment to grow that team and its reach.

Bain Capital Ventures and Thrive Capital co-led this round, a Series C. Previous backers, including Creandum, Kinnevik, Founders, Stripes and Seedcamp, also participated. Stripes led the startup’s Series B in 2019. It looks like this round was oversubscribed: the original intention had been to raise just $100 million.

Like other business processes, managing expenses and handling company spending has come a long way in the last many years.

Gone are the days where expenses inevitably involved collecting paper receipts and inputting them manually into a system in order to be reimbursed; now, expense management software links up with company-issued cards and taps into a range of automation tools to cut out some of the steps in the process, integrating with a company’s internal accounting policies to shuffle the process along a little less painfully. And there are a number of companies in this space, from older players like SAP’s Concur through to startups on the cusp of going public like Expensify as well as younger entrants bringing new technology into the process.

But, there is still lots more room for improvement. Rindom, Pleo’s CEO who co-founded the company with CTO Niccolo Perra, said the pair came up with the idea for Pleo on the back of years of working in fintech — both were early employees at the B2B supply chain startup Tradeshift — and seeing first-hand how short-changed, so to speak, small and medium businesses in particular were when it came to tools to handle their expenses.

Pleo’s approach has been to build, from the ground up, a system for those smaller businesses that integrate all the different stages of how an employee might spend money on behalf of the company.

Pleo starts with physical and virtual payment cards (which can be used in, for example, Apple Wallet) that are issued by Pleo (in partnership with MasterCard) to buy goods and services, which in turn are automatically itemized according to a company’s internal accounting systems, with the ability to work with e-receipts, but also let people use their phones to snap pictures of receipts when they are only on paper, if required. This is pretty much table stakes for expense software these days, but Pleo’s platform is going a couple of steps beyond that.

Users (or employers) can integrate a users’ own banking details to make it easier to get reimbursed when they have had to pay for something out of their own pocket; or conversely to pay for something that shouldn’t have been charged on the card. And if there are invoices to be paid at a later date from the time of purchase, these too can be actioned and set up within Pleo rather than having to liaise separately with an accounts payable department to get those settled. Higher priced tiers (beyond the basic service for up to five users) also lets a company set spending limits for individual users. Pricing is based on number of users, per month.

Pleo also has built fraud protection services into the platform to detect, for example, cases when a card number might have been compromised and is being used for non-work purposes.

What’s notable is that the startup has built all of the tech that it uses, including the payments feature, from the ground up, to have full control over the features and specifically to be able to add more of them more flexibly over time.

“In the beginning we ran with a partner in services like payments, but it didn’t allow us to move fast enough,” Rindom said in an interview. “So we decided to take all of that in-house.”

It seems like this opens the door to a lot of possibilities for how Pleo might evolve in the years ahead now that it’s focused on hyper-growth. However, Rindom added that whatever the next steps might be, they will remain focused on continuing to solve the expenses problem.

“When it comes to our infrastructure we use it only for ourselves,” he said. “We have no plans of selling [for example, payments] as a service, even if we do have a lot of other ideas for broadening our offerings.” Indeed, the ability to pay invoices was launched only in April of this year. “We come up with things all the time, but will launch only those relevant to customers.” For now, at least.

That focus and perhaps even more than that the execution and customer traction are what have brought investors around to backing a fintech out of Copenhagen.

“The future of work empowers employees with the tools they need to be effective, productive, and successful,” said Keri Gohman, a partner at Bain Capital Ventures, in a statement. “Pleo understands this critical shift for modern companies toward employee centricity—providing workers with a fun-to-use spend management app that automatically tracks their corporate spending and generates expense reports, paired with the powerful tools businesses need to create full visibility and management of every penny spent.”

Bain has been a pretty active investor in European fintech, also backing GoCardless in its recent round. “BCV invests in founders who aren’t afraid to tackle big problems, and Jeppe and Nicco saw a big challenge that employers faced—tracking all corporate spending and reconciling expenses back to the general ledger—and solved it with elegant technology that both employers and employees love,” added Merritt Hummer, a partner at Bain Capital Ventures.

Thrive is also a notable backer here, and it will be interesting to see how and if Pleo links up with others in the VC’s portfolio, which include companies like Plaid, Gong and Trade Republic.

“Pleo has already transformed the way that over 17,000 companies think about managing their expenses, saving them time and lowering costs while increasing transparency,” noted Kareem Zaki, a general partner at Thrive Capital, in a statement. “We are excited to partner closely with the Pleo team to help drive their next phase of growth.”

Powered by WPeMatico