Finance

Auto Added by WPeMatico

Auto Added by WPeMatico

Brazil is a country riven with economic contradictions. It has one of the largest and most profitable banking industries in Latin America, and is among the world’s most developed financial markets. Financial transactions that would take days to process in the United States through ACH happen instantaneously in Brazil. This sophistication, however, masks a backward state of affairs plagued by appalling customer service, exorbitant fees and lack of banking access for many.

The country’s financial system is volatile and often leaves its citizens with few or no alternatives. According to an HBS case study, “in December 2018 the interest rate in Brazil for corporate loans was 52.3%, for consumer loans it was 120.0% and for credit card indebtedness it was 272.42%.” Those rates are many multiples higher compared to figures in neighboring countries.

Brazil’s banking system is a massive market, and one ill-served by incumbents. If someone could thread the needle of product development, strategy and political horse trading required to build a bank in a country where it is nearly impossible for foreigners to own or invest in a bank, it would be one of the great startup and economic success stories of this century.

Nubank is on its way to realizing that objective. Its story is one of unmitigated success, even by the standards of our EC-1 series on high-flying companies and their hard-learned lessons. Just last week, this Brazilian credit card and banking fintech raised a $750 million round led by Berkshire Hathaway at a $30 billion valuation, becoming one of the most valuable startups in the world. It has 40 million users across Brazil, as well as Mexico and Colombia.

Yet, it’s a startup with a CEO and co-founder who isn’t Brazilian, didn’t speak the local language of Portuguese, hadn’t started a company before, and didn’t really know a lot about banking to begin with. This is a story of how raw execution, a “faster, faster” mentality and a fanaticism for making customer experience as enjoyable as a trip to Disney World can completely change the history of an industry — and country — forever.

Our lead writer for this EC-1 is Marcella McCarthy. McCarthy, who spent significant time in Brazil growing up and is trilingual in English, Spanish and Portuguese, has been covering the LatAm and Miami ecosystems for TechCrunch with an eye to the disruption underway in these interconnected regions. The lead editor for this package was Danny Crichton, the assistant editor was Ram Iyer, the copy editor was Richard Dal Porto, and illustrations were drawn by Nigel Sussman.

Nubank had no say in the content of this analysis and did not get advance access to it. McCarthy has no financial ties to Nubank or other conflicts of interest to disclose.

The Nubank EC-1 comprises four main articles numbering 9,200 words and a reading time of 37 minutes. Here’s what’s in the bank:

We’re always iterating on the EC-1 format. If you have questions, comments or ideas, please send an email to TechCrunch Managing Editor Danny Crichton at danny@techcrunch.com.

Powered by WPeMatico

For most startups, the hardest early challenge is identifying a market and a product to serve it. That wasn’t the case for Nubank CEO David Velez, who understood the massive potential for success if he could break into Latin America’s most valuable economy with even a moderately modern banking offering.

Instead, the challenge was how to rebuild the concept of a bank in a country where banking is widely hated, all while the incumbents heavily entrenched with the state worked to block every move.

Nubank knew its market and geography, and through tenacious fundraising, inventive marketing and product development, and a series of contrarian hires, Velez and his team stripped bare the morass of Brazilian banking to build one of the world’s great fintech companies.

The challenge was how to rebuild the concept of a bank in a country where banking is widely hated, all while the incumbents heavily entrenched with the state worked to block every move.

In the first part of this EC-1, I’ll look at how Velez brought his skills and experience to bear on this market, how Nubank was founded in 2013, and how the team brought a Californian rather than Brazilian vibe to their first office on — no joke — California Street, in a neighborhood called Brooklin in the city of São Paulo.

The idea of being his own boss was ingrained in Velez from his earliest days in Colombia, where he grew up in an entrepreneurial family, with a father who owned a button factory. “I heard from my dad over and over again that you need to start your own company,” Velez said.

But years would pass and Velez still had no idea what he wanted to do. To “kill time,” and also to surround himself with entrepreneurial energy, Velez attended Stanford University — partially financed by the sale of some livestock — and then worked as an analyst at Goldman Sachs and Morgan Stanley before switching to venture capital at General Atlantic and Sequoia.

Powered by WPeMatico

As we mentioned in part 1 of this EC-1, David Velez had two key co-founding roles he needed to fill to get started building Nubank. For one, he needed a CTO to lead the engineering side of the business, as Velez didn’t have an engineering background.

Edward Wible, an American computer science graduate who spent most of his career in private equity, would take that responsibility. He didn’t bring years of coding experience, but he had qualities that Velez considered more important: A strong belief in the potential of the product and an equally intense commitment to working on it.

Given the occasionally hostile reaction of most incumbent banks to their customers in Brazil, Nubank’s starkly contrasting openness and transparency has garnered a huge following.

That left an even more important role to fill — one that was much harder to define. This other co-founder would need to blend knowledge of the Brazilian market and local savvy with expertise in banking, all while embodying a Silicon Valley ethos of focusing on customers. This person would also have to work in São Paulo for minimal wages out of a small office with just one bathroom, all in the belief that their equity (both stock and sweat) would one day be worth it.

Velez would eventually stumble upon Cristina Junqueira, who was qualified to do all this, and much, much more.

“Once someone said I was the glue of the operation, and that someone else was the brains. And I said, ‘No, I’m the glue and the brains, and I bet my brain is even better than his,”’ Junqueira said.

Junqueira didn’t just lead Nubank’s drive into the Brazilian market, she also upended age-old notions of what it means to be a 21st-century bank. Her inspiration was nothing short of Disney, and her mission was to create a bank as popular as the magical kingdom itself.

A bank. As popular as Disney. Sounds like a fairy tale, frankly.

Unlike her co-founders Velez and Wible, Junqueira grew up in Nubank’s home market of Brazil. The eldest of four sisters, she remembers her parents — both dentists — always assiduously working to maintain their practice.

Their work ethic trickled down, but so did responsibility. As the oldest at home, she was forced to grow up quickly and take on responsibilities from an early age. “I remember being 11 years old and doing grocery shopping for the month,” she said. “I did everything very young.”

Powered by WPeMatico

As we saw in parts 1 and 2 of this EC-1, by mid-2013, Nubank CEO David Velez had most of what he needed to get started. He’d brought on two co-founders, assembled ambitious engineering and operations teams, raised $2 million in seed funding from Sequoia and Kaszek, rented a tiny office in São Paulo, and was armed with a mission to deliver the kind of banking services that customers in a market as large and lucrative as Brazil’s should expect.

Despite being named Nubank, however, the startup couldn’t actually be a bank: Brazil’s laws made it illegal at the time for a foreigner-run company to operate a bank. That restriction required the team to develop an inventive product strategy to find a foothold in the market while they waited for a license directly from the country’s president.

Nubank was so adamant about differentiating itself from other banks that it chose Barney purple for its brand color and first credit card.

Nubank therefore pursued a credit card as its first offering, but it had to race against a clock counting quickly down to zero. At the time, Brazil didn’t have ownership restrictions on this product segment like it did with banking, but new rules were coming into force in just a few months in May 2014 that would block a company like Nubank from launching.

The company needed to execute rapidly over the next eight months if it wanted to be grandfathered into the existing regulations. The speed of operations was frantic to say the least, and the company would go on to work even faster, ultimately propelling itself into the stratosphere of fintech startups.

It’s easy to assume that the name Nubank refers to “new bank,” but that’s not really what the founders were going for. The word “nu” in Portuguese means “naked,” and Velez and his team wanted the name to reflect their vision: To build a 21st-Century bank without any of the shackles imposed by the traditional banks in Brazil.

The team wanted to offer services to as many people as possible, as there is a huge wealth gap in Brazil, where the minimum wage is around $200 a month.

Launching with just a credit card was both a strategic and practical business decision. Credit cards were widely used in the country, and everyone understood how they worked. Additionally, you could only use credit cards to shop online in Brazil, because debit cards weren’t accepted.

Powered by WPeMatico

Nubank’s first office, on California Street in the Brooklin neighborhood of São Paulo, makes for a great beginning to the company’s story. It wasn’t a Silicon Valley garage, but this tiny, one-bathroom rented house, where 30 people worked insane hours to push out the company’s debut credit card, lends just as well to an image of entrepreneurial spirit and drive.

As Nubank continues to make international waves, more and more VC investors are taking a look at the Brazilian ecosystem and could potentially fund other upstarts in the years to come.

But as Nubank’s story continued, the team eventually had to move out of that early office, and the next several offices, too. Eventually Nubank had to relocate to an eight-story building in São Paulo, which houses a large part of the company’s now 3,000-person team.

The startup reached decacorn status in far less than a decade, and it is growing faster than ever. When I interviewed CEO David Velez back in January to discuss Nubank’s $400 million Series G, he said, “We’ve gone from 12 million customers in 2019 to 34 million solely based on word of mouth.” By September last year, the company was onboarding 41,000 new customers per day.

In the five months since our interview, Nubank has managed to rope in a whopping 6 million customers to reach 40 million. It’s now valued at $30 billion.

Nubank’s present day headquarters in São Paulo, Brazil. Image Credits: NELSON ALMEIDA/AFP / Getty Images

Getting there hasn’t been easy. The company’s three co-founders, Velez, Edward Wible and Cristina Junqueira, had to make key strategic decisions about how to scale themselves to retain the company’s lead in the neobanking market. That lead is getting tougher to sustain every day. Nubank’s proliferating offerings and broader geographical remit has painted a massive target on its back, and a wide number of competitors have cropped up to run on the paths it pioneered.

Like most Disney films, a fairy-tale ending seems in order, but it’ll take a few more rotations of the film wheel to get to the ending.

For the co-founding trio, it became increasingly clear that Nubank’s growing scale demanded critical strategic decisions on how to bring order to the company.

By 2018, the company had thousands of employees, millions of customers, and they still didn’t have a head of HR. Growth until then had been somewhat unstructured. According to Junqueira, waiting so long to hire a head of HR was one of their early mistakes, because it stunted their ability to grow. “[Good] people continue to be our biggest bottleneck,” she says.

Powered by WPeMatico

French startup Lydia is better known as the dominant app for peer-to-peer payments. But the company has been adding more features, such as a debit card, account aggregation, donations, money pots and more. This week, the company is adding savings accounts thanks to a partnership with French fintech startup Cashbee.

If you aren’t familiar with Cashbee, the company lets you open savings accounts through a mobile app. After connecting your bank account with Cashbee, you can transfer money back and forth between your bank account and a savings account.

Right now, Cashbee partners with My Money Bank for the savings accounts. Cashbee doesn’t keep your money, it just acts as a middle person between your bank account and My Money Bank. With those savings accounts, users can expect an interest rate of 0.6% after an introductory rate of 2% for a few months.

Lydia basically offers the same terms and conditions with a few differences. Instead of earning 2% interest for the first three months, Lydia users only earn more interest during the first two months.

The other big difference is that Lydia asks you to put at least €1,000 on your savings account when you open it. If you go through Cashbee’s app, you only have to put €10 or more. But users can do whatever they want after that when it comes to putting some money aside and withdrawing money from the savings account.

But the fact that Cashbee is seamlessly integrated in Lydia is interesting. It’s going to expose Cashbee to a lot more users as Lydia has more than 5 million users. It’s also an important feature if Lydia wants to become a financial super app.

This savings feature competes with Livret A, the most prevailing savings account in France. Everybody can open a Livret A in a retail bank. You get an interest rate of 0.5% net of taxes. On paper, 0.6% is better than 0.5%. But Cashbee’s savings accounts aren’t net of taxes.

If you’re a student and don’t pay any taxes, that’s a better deal. But many people pay 30% in taxes on accrued interests, which means that you end up earning 0.42% in interests net of taxes with a Cashbee account.

But it’s hard to beat the simplicity of Lydia’s solution here. For instance, you can save up to €1,000,000 on your savings account while the Livret A is limited to €22,950. In other words, if you’re already using Lydia to send, receive and spend money, you might want to check out those savings accounts.

Powered by WPeMatico

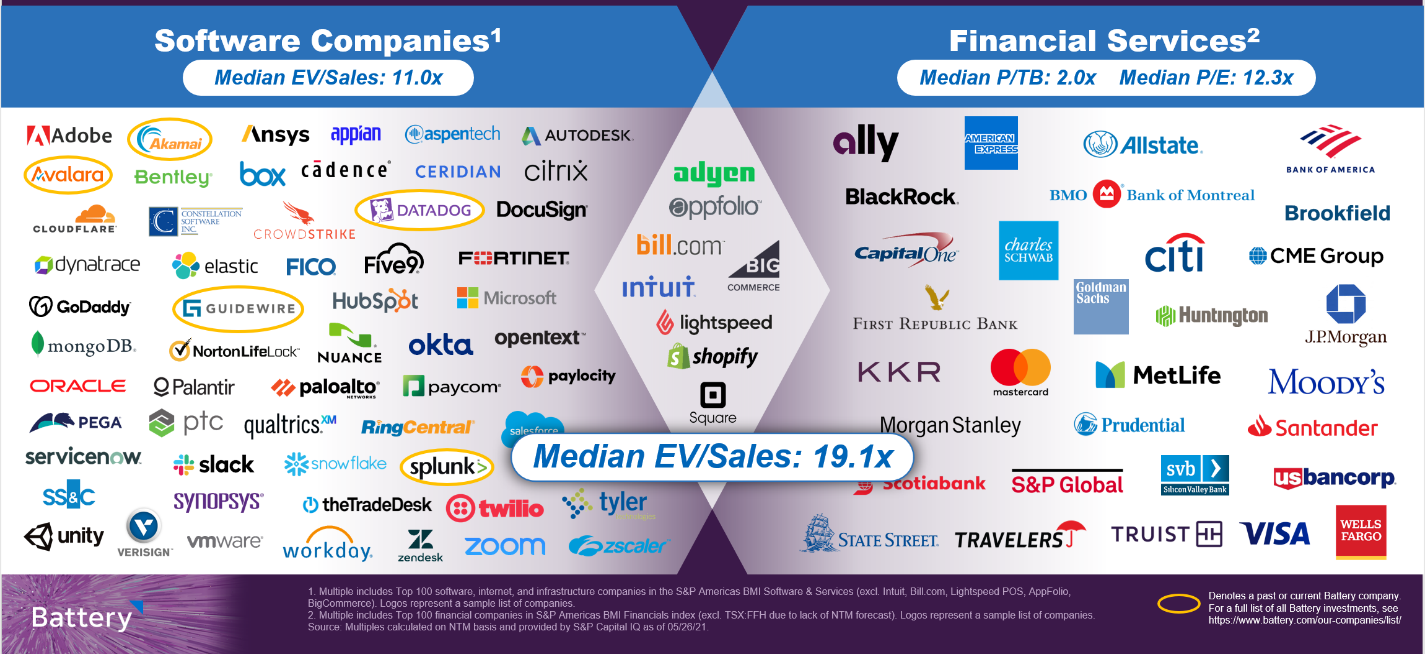

If money is the ultimate commodity, how can fintechs — which sell money, move money or sell insurance against monetary loss — build products that remain differentiated and create lasting value over time?

And why are so many software companies — which already boast highly differentiated offerings and serve huge markets— moving to offer financial services embedded within their products?

A new and attractive hybrid category of company is emerging at the intersection of software and financial services, creating buzz in the investment and entrepreneurial communities, as we discussed at our “Fintech: The Endgame” virtual conference and accompanying report this week.

These specialized companies — in some cases, software companies that also process payments and hold funds on behalf of their customers, and in others, financial-first companies that integrate workflow and features more reminiscent of software companies — combine some of the best attributes of both categories.

Image Credits: Battery Ventures

From software, they design for strong user engagement linked to helpful, intuitive products that drive retention over the long term. From financials, they draw on the ability to earn revenues indexed to the growth of a customer’s business.

Fintech is poised to revolutionize financial services, both through reinventing existing products and driving new business models as financial services become more pervasive within other sectors.

The powerful combination of these two models is rapidly driving both public and private market value as investors grant these “super” companies premium valuations — in the public sphere, nearly twice the median multiple of pure software companies, according to a Battery analysis.

The near-perfect example of this phenomenon is Shopify, the company that made its name selling software to help business owners launch and manage online stores. Despite achieving notable scale with this original SaaS product, Shopify today makes twice as much revenue from payments as it does from software by enabling those business owners to accept credit card payments and acting as its own payment processor.

The combination of a software solution indexed to e-commerce growth, combined with a profitable payments stream growing even faster than its software revenues, has investors granting Shopify a 31x multiple on its forward revenues, according to CapIQ data as of May 26.

Before even talking about how investors should value these hybrid companies, it’s worth making the point that in both private and public markets, fintechs have been notoriously hard to value, fomenting controversy and debate in the investment community.

Powered by WPeMatico

This spring, Facebook confirmed it was testing Venmo-like QR codes for person-to-person payments inside its app in the U.S. Today, the company announced those codes are now launching publicly to all U.S. users, allowing anyone to send or request money through Facebook Pay — even if they’re not Facebook friends.

The QR codes work similarly to those found in other payment apps, like Venmo.

The feature can be found under the “Facebook Pay” section in Messenger’s settings, accessed by tapping on your profile icon at the top left of the screen. Here, you’ll be presented with your personalized QR code which looks much like a regular QR code except that it features your profile icon in the middle.

Underneath, you’ll be shown your personal Facebook Pay UR which is in the format of “https://m.me/pay/UserName.” This can also be copied and sent to other users when you’re requesting a payment.

Facebook notes that the codes will work between any U.S. Messenger users, and won’t require a separate payment app or any sort of contact entry or upload process to get started.

Users who want to be able to send and receive money in Messenger have to be at least 18 years old, and will have to have a Visa or Mastercard debit card, a PayPal account or one of the supported prepaid cards or government-issued cards, in order to use the payments feature. They’ll also need to set their preferred currency to U.S. dollars in the app.

After setup is complete, you can choose which payment method you want as your default and optionally protect payments behind a PIN code of your choosing.

The QR code is also available from the Facebook Pay section of the main Facebook app, in a carousel at the top of the screen.

Facebook Pay first launched in November 2019, as a way to establish a payment system that extends across the company’s apps for not just person-to-person payments, but also other features, like donations, Stars and e-commerce, among other things. Though the QR codes take cues from Venmo and others, the service as it stands today is not necessarily a rival to payment apps because Facebook partners with PayPal as one of the supported payment methods.

However, although the payments experience is separate from Facebook’s cryptocurrency wallet, Novi, that’s something that could perhaps change in the future.

Image Credits: Facebook

The feature was introduced alongside a few other Messenger updates, including a new Quick Reply bar that makes it easier to respond to a photo or video without having to return to the main chat thread. Facebook also added new chat themes including one for Olivia Rodrigo fans, another for World Oceans Day, and one that promotes the new F9 movie.

Powered by WPeMatico

On the heels of acquiring sales tax specialist TaxJar in April, today Stripe is making another big move in the area of tax. The $95 billion payments behemoth is launching a new product called Stripe Tax, which will provide automatic, updated sales tax calculations (covering sales tax, VAT and GST) and related accounting services to Stripe payments customers initially in some 30 countries and across the U.S.

Stripe Tax is a separate service from TaxJar, but the two are not unconnected. As Stripe Tax was being built out of Stripe’s offices in Dublin over the last several months, Stripe’s business lead for EMEA Matt Henderson told me that the team had identified TaxJar as a strong company in the field. That ultimately led to M&A between them.

Sales tax — and specifically a more seamless way to deal with charging and tracking sales tax — is a painful issue for people doing business online.

Digital and physical goods are taxed in over 130 countries, Stripe said, and within that there can be a huge amount of variation and compliance complexity, since codes get updated all the time, too. Mishandled sales tax, meanwhile, can result in pretty hefty fines, sometimes up to 30% interest on past-due amounts.

Unsurprisingly, a sales tax tool has been the most-requested feature from Stripe’s customers, Henderson said, a call that presumably only got louder in the last year, as e-commerce and digital transactions went through the roof with COVID-19.

Arguably, that makes Stripe Tax one of the company’s more significant product launches, not to mention the first since announcing its monster funding round earlier this year.

Previously, Stripe customers would have resorted to using a third-party service (like TaxJar) to work out sales tax. Or, more typically, those Stripe customers would have opted to limit the number of places they sold goods and services, in order to minimize the pain of dealing with multiple, complex and usually quite localized tax codes.

“No one leaps out of bed in the morning excited to deal with taxes,” said John Collison, co-founder and president of Stripe in a statement. “For most businesses, managing tax compliance is a painful distraction. We simplify everything about calculating and collecting sales taxes, VAT, and GST, so our users can focus on building their businesses.”

Stripe said that a survey of its customers found that two-thirds of respondents said the challenge of implementing sales tax actually limited their growth.

TaxJar has built a strong system for handling that, but the company — based out of Massachusetts but with a remote team — is primarily focused on the U.S. market, which has sales tax that is complicated enough (there are 11,000 different tax jurisdictions in the country).

That leaves a lot on the table for building out sales tax tools for the rest of the world: The wider focus of Stripe Tax thus fills a particular geographical gap for the company, regardless of how well TaxJar and Stripe integrate over time.

There is another key difference worth noting between the two.

TaxJar came to Stripe’s attention with an established operation — 23,000 customers at the time of the announcement. Stripe (wisely) bolted that on as a standalone business, which means that new and existing customers that use TaxJar can continue to use it as is. That is to say, at least for now, they do not need to be Stripe payments customers in order to use TaxJar, even if the integration between the two platforms will only improve over time.

Stripe Tax, on the other hand, is being built from the ground up as a product aimed specifically at increasing touchpoints and stickiness with Stripe customers.

Stripe Tax provides real-time tax calculation based on customer location and product sold; transparent itemizing for customers; tax ID management in areas (like Europe) where business customers can provide their code and get a reverse charge on tax if they are under a certain turnover threshold themselves; and reconciliation and reporting across all transactions to make filing and remittance easier.

But there is for now no way to use Stripe Tax outside of Stripe payments.

This could pose some problems for some customers. These days, many of the strongest retailers will take an “omnichannel” approach that might cover selling through marketplaces, selling through websites, selling through social media and more — and not all of those experiences may be powered by Stripe. It will be worth watching whether future iterations of Stripe Tax can account for that.

Stripe’s most significant product launch prior to Stripe Tax — Stripe Treasury last December — underscores how the company is currently very focused on diversifying outside of its basic payments business and opening the platform to much wider, more scaled transactions.

Treasury, which is still in invite-only mode, saw Stripe partner with established banks to provide a business banking service, providing a way for its customers to handle money that they generate from their Stripe-powered businesses.

The full country list where Stripe Tax is launching is Australia, Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, New Zealand, the Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, Switzerland, the United States and the United Kingdom.

Updated to correct the number of customers TaxJar has to 23,000.

Powered by WPeMatico

BukuWarung, a fintech focused on Indonesia’s micro, small and medium enterprises (MSMEs), announced today it has raised a $60 million Series A. The oversubscribed round was led by Valar Ventures, marking the firm’s first investment in Indonesia, and Goodwater Capital. The Jakarta-based startup claims this is the largest Series A round ever raised by a startup focused on services for MSMEs. BukuWarung did not disclose its valuation, but sources tell TechCrunch it is estimated to be between $225 million to $250 million.

Other participants included returning backers and angel investors like Aldi Haryopratomo, former chief executive officer of payment gateway GoPay, Klarna co-founder Victor Jacobsson and partners from SoftBank and Trihill Capital.

Founded in 2019, BukuWarung’s target market is the more than 60 million MSMEs in Indonesia, according to data from the Ministry of Cooperatives and SMEs. These businesses contribute about 61% of the country’s gross domestic product and employ 97% of its workforce.

BukuWarung’s services, including digital payments, inventory management, bulk transactions and a Shopify-like e-commerce platform called Tokoko, are designed to digitize merchants that previously did most of their business offline (many of its clients started taking online orders during the COVID-19 pandemic). It is building what it describes as an “operating system” for MSMEs and currently claims more than 6.5 million registered merchant in 750 Indonesian cities, with most in Tier 2 and Tier 3 areas. It says it has processed about $1.4 billion in annualized payments so far, and is on track to process over $10 billion in annualized payments by 2022.

BukuWarung’s new round brings its total funding to $80 million. The company says its growth in users and payment volumes has been capital efficient, and that more than 90% of its funds raised have not been spent. It plans to add more MSME-focused financial services, including lending, savings and insurance, to its platform.

BukuWarung’s new funding announcement comes four months after its previous one, and less than a month after competitor BukuKas disclosed it had raised a $50 million Series B. Both started out as digital bookkeeping apps for MSMEs before expanding into financial services and e-commerce tools.

When asked how BukuWarung plans to continue differentiating from BukuKas, co-founder and CEO Abhinay Peddisetty told TechCrunch, “We don’t see this space as a winner takes all, our focus is on building the best products for MSMEs as proven by our execution on our payments and accounting, shown by massive growth in payments TPV as we’re 10x bigger than the nearest player in this space.”

He added, “We have already run successful lending experiments with partners in fintech and banks and are on track to monetize our merchants backed by our deep payments, accounting and other data that we collect.”

BukuWarung’s new funding will be used to double its current workforce of 150, located in Indonesia, Singapore and India, to 300 and develop BukuWarung’s accounting, digital payments and commerce products, including a payments infrastructure that will include QR payments and other services.

Powered by WPeMatico