Finance

Auto Added by WPeMatico

Auto Added by WPeMatico

This afternoon Robinhood filed to go public. TechCrunch’s first look at its results can be found here. Now that we’ve done a first dig, we can take the time to dive into the company’s filing more deeply.

Robinhood’s IPO has long been anticipated not only because there are billions of dollars in capital riding on its impending liquidity, but also because the company became something of a poster child for the savings and investing boom that 2020 saw and the COVID-19 pandemic helped engender.

The consumer trading service’s products became so popular and enmeshed in popular culture thanks to both the “stonks” movement and the larger GameStop brouhaha, that the company’s public offering carries much more weight than that of a more regular venture-backed entity. Robinhood has fans, haters, and many an observer in Congress.

Regardless of all that, today we are digging into the company’s business and financial results. So, if you want to better understand how Robinhood makes money, and how profitable or not it really is, this is for you.

We will start with a more in-depth look at growth and profitability, pivot to learning about the company’s revenue makeup, discuss a risk factor or two, and close on its decision to offer some of its own shares to its users. Let’s go!

Before we get into the how of Robinhood’s growth, let’s discuss how big the company has become.

The fintech unicorn’s revenue grew from $277.5 million in 2019 to $958.8 million in 2020, which works out to growth of around 245%. Robinhood expanded even more quickly in the first quarter of 2021, scaling from year-ago revenue of $127.6 million to $522.2 million, a gain of around 309%.

Those are numbers that we frankly do not see often amongst companies going public; 300% growth is a pre-Series A metric, usually.

Powered by WPeMatico

It’s a sweltering day here in New York City, and that means Wall Street is on fire, and so is Robinhood, apparently. The popular stock trading app officially filed its Form S-1 with the SEC a few hours ago to go public, where it will trade under the ticker “HOOD.”

The Equity crew has been yammering about Robinhood for years now, and we have been chomping at the bit to see those S-1 results for what feels like ages. Well, we finally got the numbers, we chomped that bit (or at least Alex and Danny did, since Natasha went on vacation about 15 minutes before the IPO hit the wires), and so here’s a special Equity Shot to talk about all the highlights.

We talked about so much in an itsy-bitsy 15-minute episode: crazy revenue growth, crazy revenue concentration from two major sources, regulatory hurdles that the company has been clearing up, better financials with a bit of nuance on the company’s Q1 finances, and the company’s special plan for its IPO.

Wowza.

Here’s what we got up to:

And a lot more. Of course, if you hate Robinhood, we will be back with our normally scheduled Friday episode of Equity tomorrow.

Equity drops every Monday at 7:00 a.m. PDT, Wednesday, and Friday morning at 7:00 a.m. PDT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Orum, which aims to speed up the amount of time it takes to transfer money between banks, announced today it has raised $56 million in a Series B round of funding.

Accel and Canapi Ventures co-led the round, which also included participation from existing backers Bain Capital Ventures, Inspired Capital, Homebrew, Acrew, Primary, Clocktower and Box Group. The financing comes barely three months after Orum announced a $21 million Series A, and brings its total raised to over $82 million.

Orum CEO Stephany Kirkpatrick launched the company in 2019 after working for several years at LearnVest, a personal finance site founded by Alexa von Tobel that was acquired by Northwestern Mutual in 2015 for an estimated $375 million. Tobel went on to form Inspired Capital, a venture capital firm that put money in Orum’s $5.2 million seed round last August. Prior to that, the firm also provided Orum with an “inspiration check” that was the first money into the business.

“Most Americans are not familiar with the intricacies of ACH [automated clearing house) or why it takes multiple business days to move money between accounts,” Kirkpatrick said. “But none of us can allow money to wait 5-7 days to hit our accounts. It needs to be instant.”

Her mission with Orum is straightforward even if the technology behind it is complex. Put simply, Orum aims to use machine learning-backed APIs to “move money smartly across all payment rails, and in doing so, provide universal financial access.”

Orum’s first embeddable product, Foresight, launched in September of 2020. It’s an automated programming interface designed to give financial institutions a way to move money in real time. The platform uses machine learning and data science to predict when funds are available and to identify any potential risks. Its Momentum product “intelligently” routes funds across payments rails and is powered by banking providers JPMorgan Chase and Silicon Valley Bank.

“They power the back end of our Momentum platform that allows the money to move on a multirail basis,” Kirkpatrick told TechCrunch. “They power our access to real-time payments.”

Orum says it serves a range of enterprise partners, including Alloy, HM Bradley, First Horizon Bank and Zero Financial (which was recently acquired by Avant).

The volume of transactions being conducted with Orum is growing 100% month over month, Kirkpatrick said. Most of its early growth has come from word of mouth.

The remote-first company prides itself on diversity — in both its employee and investor base. For one, 48% of its 55-person headcount are female, and 48% are “nonwhite,” according to Kirkpatrick. Orum also recently joined the Cap Table Coalition — a partnership between high-growth startups and emerging investors who want to work to close the racial wealth gap — to allocate over 10% of its Series B round to underrepresented founders. For example, the financing includes investors such as the Neythri Features Fund, a group of South Asian women investing in the next generation of female founders and diverse teams.

Jeffrey Reitman, partner at Canapi Ventures (a firm whose LPs mostly consist of banks), told TechCrunch that those bank LPs conduct hundreds of millions of ACH transactions annually,

“They need a path to achieving a state where funds can be transferred instantly,” he said. “Orum’s product paves the path for many players in financial services and fintech — and beyond — to partake in faster money movement without compromising key risk principles.”

To Reitman, the company’s major differentiators are its team, which he describes as consisting of “the best group of data scientists and engineers in the space.”

“Many of their customers consider the team to be instrumental in helping to set the risk dials on how they fund transactions by teasing out key data and insights from historical transaction data,” he said. “Second, Orum is building one of the densest and most comprehensive data sets around the risks of money movement. Better data means better risk models, and it will be hard for other offerings to match Orum’s approach to building this rich data set.”

Accel Partner Sameer Gandhi, who joined Orum’s board as part of the latest financing, agrees. He believes that in an 18-month period, Orum has built “game-changing technology and an exceptional team.”

“Orum is tackling financial infrastructure from its foundation,” he said.

The headline was updated post-publication to reflect the correct funding amount.

Powered by WPeMatico

Accel announced Tuesday the close of three new funds totaling $3.05 billion, money that it will be using to back early-stage startups, as well as growth rounds for more mature companies. Notably, the 38-year-old Silicon Valley-based venture firm is doubling down on global investing.

The announcement underscores both the robust confidence investors continue to have for backing startups in the tech sector and the amount of money available to startups these days.

Specifically, today Accel is announcing its 15th early-stage U.S. fund at $650 million; its seventh early-stage European and Israeli fund also at $650 million and its sixth global growth stage fund at $1.75 billion. The latter fund is in addition, and designed to complement, a previously unannounced $2.3 billion global “Leaders” fund that is focused on later-stage investing that Accel closed in December.

Accel expects to invest in about 20 to 30 companies per fund on average, according to Partner Rich Wong. Its average investment in its growth fund will be in the $50 million to $75 million range, and $75 million and $100 million out of its global Leaders fund.

But the firm is also still eager and “excited” to incubate companies, Wong said.

“We’ll still write $500,000 to $1 million seed checks,” he told TechCrunch. “It’s important to us to work with companies from the very beginning and support them through their entire journey.”

Indeed, as TechCrunch recently reported, Accel has a history of backing companies that were previously bootstrapped (and often profitable) -– the latest example being Lower, a Columbus, Ohio-based fintech, which just raised a $100 million Series A.

Interestingly, Accel is often referred to some of these companies by existing portfolio companies (also in the case of Lower, whose CEO was referred to Accel by Galileo Clay Wilkes). More often than not, companies that Accel backs out of its early-stage and growth funds are bootstrapped and located outside of Silicon Valley.

The venture firm has long looked outside of Silicon Valley for opportunities, and has had offices not only in the Bay Area, but in London and Bangalore for years. Part of its investment thesis is to “invest early and locally,” according to Wong. Examples of this philosophy include investments in companies based all over the world — from Mexico to Stockholm to Tel Aviv to Munich.

Since the time of its last fund closure in 2019, the firm has seen 10 portfolio companies go public, including Slack, Austin-based Bumble, Bucharest-based UiPath, CrowdStrike, PagerDuty, Deliveroo and Squarespace, among others.

It also had 40 companies experience an M&A, including Utah-based Qualtrics’s $8 billion acquisition by SAP and Segment’s $3.2 billion acquisition by Twilio. Also, just last week, Rockwell Automation announced it was buying Michigan-based Plex Systems for $2.22 billion in cash. Accel first invested in Plex, which has developed a subscription-based smart manufacturing platform, in 2012.

Recent investments include a number of fintech companies such as LatAm’s Flink, Berlin-based Trade Republic, Unit and Robinhood rival Public. Accel has also backed as existing portfolio companies such as Webflow, a software company that helps businesses build no-code websites and events startup Hopin.

Wong says Accel is “open-minded but thematic” in its investment approach.

Accel Partner Sonali de Rycker, who is based out of London, agrees.

“For example, we’ll look at automation companies, consumer businesses and security companies, but at a global scale. Our goal is to find the best entrepreneurs regardless of where they are,” she said.

That has only been intensified by the recent rise of the smartphone and cloud, Wong said.

“Before, companies were mostly selling to the consumer in their own country,” he added. “But now the size of the market is so dramatically bigger, allowing them to become even larger, which is one of the reasons why I believe we’re seeing investment pace at this speed.”

To support this, it’s notable that Accel’s global Leaders fund is “dramatically” larger than the $500 million Leaders fund the firm closed in 2019.

Also, de Rycker points out, companies are staying private longer so the opportunity to invest in them until they sell or go public is greater.

Accel is also patient. In some cases, the firm’s investors will develop “years-long” relationships with companies they are courting.

“1Password is an example of this approach,” Wong said. “Arun [Mathew] had that relationship for at least six years before that investment was made. Finally, 1Password called and said ‘We’re ready, and we want you to do it.’ ”

And so Accel led the Canadian company’s first external round of funding in its 14-year history — a $200 million Series A — in 2019.

While the firm is open-minded, there are still some industries it has not yet embraced as much as others. For example, Wong said, “We’re not announcing a $2.2 billion crypto fund, but we have done crypto investments, and see some very interesting trends there. We’ll look at where crypto takes us.”

Powered by WPeMatico

The U.K. is gaining in popularity as a great place to start a tech firm. The country is quickly catching up to China on the tech investment front, with VC investments reaching a record of $15 billion in 2020, according to TechNation. A global health crisis notwithstanding, London remained a favorite for investors. U.K. cities made up a fifth of the top 20 European cities, with names such as Oxford, Dublin, Edinburgh and Cambridge rising to the fore in 2020.

Bristol proved especially popular among tech investors last year — local businesses raked in an impressive $414 million in 2020, making it the third-largest U.K. city for tech investment. The city also has the most fintech startups per head in the U.K. outside London, according to Whitecap’s 2019-2020 Ecosystem Report.

Efforts by the city’s private and public sectors to modernize the city have helped it rank among the top smart cities in the U.K., attracting a bevy of tech entrepreneurs. Its proximity to London has meant that it is a good alternative for founders looking for a more affordable stay while letting them tap the capital’s financial resources. The University of Bristol also has the largest robotics department in Europe.

Use discount code HARBOURSIDE to save 25% off an annual or two-year Extra Crunch membership.

This offer is only available to readers in the U.K. and Europe, and expires on August 31, 2021.

Bristol is also home to an important startup accelerator, SETsquared. A collaborative effort by the five universities of Bath, Bristol, Exeter, Southampton and Surrey, the accelerator has supported over 4,000 entrepreneurs and helped their startups raise a total of £1.8 billion. Other startup support players include the new Science Creates VC fund, set up by entrepreneur Harry Destecroix, and TechSPARK Engine Shed.

Key emerging startups from Bristol include Graphcore, Open Bionics, Ultraleap, Immersive Labs and Five AI.

To get a better idea of the state of the tech ecosystem and the investor outlook for this city, we surveyed founders, leaders and executives involved in nurturing Bristol’s startup ecosystem.

The survey revealed that the city has a robust renewable, zero-carbon and fintech startup landscape. Robotics, VR, bio, quantum, digital and deep tech are also areas showing promise. As for the investing scene, although Bristol has a healthy angel network, the city lacks institutional VC, but with London only a drive or train ride away, this has not proved a significant problem.

We surveyed:

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Bristol is strong in renewable and zero-carbon innovation, fintech and robotics. It’s weak in industry 4.0.

Which are the most interesting startups in Bristol?

Graphcore, LettUs Grow, Open Bionics, Ultraleap and YellowDog.

What are the tech investors like in Bristol? What’s their focus?

A lot of focus on fintech, I think.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

Bristol is a great middle ground between a large dynamic city (plus it’s not far from London) and access to nice countryside area. With remote working we can expect it will attract new residents in the next few years.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

Aimee Skinner, Abigail Frear and Stuart Harrison.

Where do you think the city’s tech scene will be in five years?

Second major city in U.K. innovation.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Bristol is strong in media/animation, edtech, social impact, health and science. I’m most excited by edtech and the possibility to reach and positively impact millions of students via online learning. It’s weaker in hardware and fintech.

Which are the most interesting startups in Bristol?

Kaedim, Persona Education and One Big Circle.

What are the tech investors like in Bristol? What’s their focus?

There are several very active tech investment networks coming from several angles, e.g., university-led, groups of private angels and tech incubators. The great thing is they all collaborate and share resources, ideas and expertise in initiatives such as The Engine Shed and Silicon Gorge.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

More people are moving in, as Bristol has a great urban lifestyle with easy access to the countryside and Southwest/Wales holiday spots, and an international airport 20 minutes from the center.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

Jerry Barnes at Bristol PE Club; Abby Frear at TechSPARK; Briony Phillips at Rocketmakers; Jack Jordan-Connelly at SETsquared.

Where do you think the city’s tech scene will be in five years?

It’s developing rapidly with lots of support, so it will be bigger, attracting more investment and definitely more on the international scene five years from now.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Our tech ecosystem is strong in the aerospace and defense sector. We are excited by the scope and scale of digital transformation opportunities with AI available in this sector. The main weakness in this sector is the slow pace of transformation, especially now due to the pandemic.

Which are the most interesting startups in Bristol?

Graphcore and YellowDog.

What are the tech investors like in Bristol? What’s their focus?

Compared to the U.K. tech sector average, Bristol has a very low proportion of established companies (4% versus 8%), a higher proportion of seed stage companies (42% versus 37%), and a higher death rate (21% versus 17%). It’s a particularly young ecosystem.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

It is possible that people moving out of London will come into Bristol due to the transport links, strong ecosystem and beautiful nature of the city.

Where do you think the city’s tech scene will be in five years?

I wouldn’t be surprised if Bristol turns out to be San Francisco of Europe!

Which sectors is Bristol’s tech ecosystem strong in? What does it lack?

Bristol is strong in the medtech, veterinary, industrial sectors.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

Others have moved in.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

SETsquared.

Where do you think the city’s tech scene will be in five years?

We will see massive growth in five years.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Our sector is weak in entrepreneurial ambition among researchers, and so suffers from low rates of deep tech spinout activity from leading universities. We are most excited by the step change in activity we have seen in the past two years and culture shift towards innovation.

Which are the most interesting startups in Bristol?

Rosa Biotech, Albotherm and CytoSeek.

What are the tech investors like in Bristol? What’s their focus?

Medium strength in shallow tech; currently weak in deep tech.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

People are moving in.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

Spin Up Science, Science Creates and Science Angel Syndicate.

Where do you think the city’s tech scene will be in five years?

Very strong in deep tech with an invested local community of entrepreneurs, incubators and investors.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Bristol is strong in wireless (5G, 60 GHz, etc.), semiconductors (especially processors, AI/ML and parallel architectures), robotics and other hard tech/deep tech.

Which are the most interesting startups in Bristol?

Graphcore, Ultraleap, Blu Wireless and Five AI.

What are the tech investors like in Bristol? What’s their focus?

It’s limited. There are some angels, but few locally focused funds.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

Much the same: People choose to live in Bristol/Bath for quality of life. Much of the work is already external — commuting to London.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

Nigel Toon, Simon Knowles, Stan Boland, David May and Nick Sturge.

Where do you think the city’s tech scene will be in five years?

Much stronger, with more processor and hardware activity.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Bristol has a strong robotics, aerospace and renewables scene. I’m most excited to see how the legacy in aerospace in Bristol will translate to future industry-defining companies. The ecosystem is weak on the investor side, though London VCs are less than a two-hour train journey away.

Which are the most interesting startups in Bristol?

Graphcore, Ultraleap and Open Bionics.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

I believe Bristol will become more attractive.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

Tom Carter at Ultraleap, and Joel Gibbard at Open Bionics.

Where do you think the city’s tech scene will be in five years?

Getting closer to London and Cambridge.

Which sectors is Bristol’s tech ecosystem strong in? What are you most excited by? What does it lack?

Bristol has a strong biotech, quantum, digital, science-based/deep tech ecosystem. I’m excited by this eclectic city with exciting people that think differently.

Which are the most interesting startups in Bristol?

Any QTEC, SETsquared, or UnitDX members and alumni.

What are the tech investors like in Bristol? What’s their focus?

Very early/nascent, mostly angels.

With the shift to remote working, do you think people will stay in Bristol or will they move out? Will others move in?

Probably move in! Beautiful green spaces around, lots of interesting, independent shops. And (just about) commutable from London.

Who are the key startup people in the city (e.g., investors, founders, lawyers, designers)?

The incubators — QTEC, QTIC, SETsquared and UnitDX; Bristol Private Equity Club; Harry Destecroix.

Where do you think the city’s tech scene will be in five years?

Buzzing. More great startups and VCs moving in.

Powered by WPeMatico

Lower, an Ohio-based home finance platform, announced today it has raised $100 million in a Series A funding round led by Accel.

This round is notable for a number of reasons. First off, it’s a large Series A even by today’s standards. The financing also marks the previously bootstrapped Lower’s first external round of funding in its seven-year history. Lower is also something that is kind of rare these days in the startup world: profitable. Silicon Valley-based Accel has a history of backing profitable, bootstrapped companies, having also led large Series A rounds for the likes of 1Password, Atlassian, Qualtrics, Webflow, Tenable and Galileo (which went on to be acquired by SoFi).

In fact, Galileo founder Clay Wilkes introduced the VC firm to Dan Snyder, Lower’s founder and CEO. The two companies have a few things in common besides being profitable: they were both bootstrapped for years before taking institutional capital and both have headquarters outside of Silicon Valley.

“We were immediately intrigued because Ohio-based Lower echoes both of these themes,” said Accel partner John Locke, who led the firm’s investment in Lower and is taking a seat on the company’s board as part of the investment. “Like Galileo, Lower will be one of the most successful bootstrapped fintech companies globally. The combination of a company built in a nontraditional region across the globe and a bootstrapped company reminds us of [other] companies we have partnered with for a large Series A.”

There were other unnamed participants in the round, but Accel provided the “majority” of the investment, according to Lower.

Snyder co-founded Lower in 2014 with the goal of making the home-buying process simpler for consumers. The company launched with Homeside, its retail brand that Snyder describes as “a tech-leveraged retail mortgage bank” that works with realtors and builders, among others.

In 2018, the company launched the website for Lower, its direct-to-consumer digital lending brand with the mission of making its platform a one-stop shop where consumers can go online to save for a home, obtain or refinance a mortgage and get insurance through its marketplace. This year, it launched the Lower mobile app with a savings account.

Sitting (L to R): Co-founders Dan Snyder, Grayson Hanes

Standing (L to R): Co-founders Mike Baynes, Chris Miller

Not pictured: Robert Tyson; Image credit: Lower

Over the years, Lower has funded billions of dollars in loans and notched an impressive $300 million in revenue in 2020 after doubling revenue every year, according to Snyder.

“Our history is maybe a little atypical of fintech companies today,” he told TechCrunch. “We’ve had a view going back to the start of the company that we wanted to run it profitably. That’s been one of our pillars, so that’s what we’ve done. Also, we all grew up in the mortgage industry, so we saw firsthand the size of the market, but also how broken it was, so we wanted to change it.”

In launching the direct-to-consumer digital lending brand, the company was working to make the homebuying process more “digital, transparent and easier for consumers to access,” Snyder said.

At the same time, the company didn’t want to lose the human touch.

“We tried to design the app flow in a way where you can get as far along as you can in the application but if you want, at any point in time, to talk or chat with someone, we’re available,” Snyder added.

Image Credits: Lower

Lower’s typical customer is the millennial and now Gen Z who’s aspiring to own their first home, according to Snyder.

“They might be thinking, ‘OK, I might be living in an apartment now, but in the next few years I’m going to meet someone and/or have a child and I want to unlock the investment that is a home,’” he told TechCrunch. “And we’ll help them on that journey.”

Lower’s recently launched new app offers a deposit account it’s dubbed “HomeFund.” The interest-bearing, FDIC-insured deposit account offers a 0.75% Annual Percentage Yield and is designed to help consumers save for a home with a “dollar-for-dollar match in rewards” up to the first $1,000 saved, Snyder said.

Lower works with more than 35 major insurance carriers nationally, including Nationwide, Liberty Mutual and Allstate. It has more than 1,600 employees, about half of which are based in Lower’s home state. That’s up from about 650 employees in June of 2020.

Looking ahead, the company plans to add more services and has an “aggressive roadmap” for adding new features to its platform. Today, for example, Lower sells primarily to Fannie Mae and Freddie Mac. And while it services the majority of its loans, like many large lenders, it uses a subservicer. That will change, however, in early 2022, when Lower intends to launch its own native servicing platform.

And while the company intends to continue to run profitably, Snyder said he and his co-founders “think the time is now to gain share.”

“We want to become a global brand, raise money and gain market share,” he added. “We’re going to continue to double down on product and build out our capabilities. We are the best-kept secret in fintech and plan to change that with smart branding, advertising and sponsorships.”

And last but not least, Lower is eyeing the public markets as part of its longer-term roadmap.

“Ultimately, we know we can build a great public company,” Snyder told TechCrunch. “We’re of the scale to be a public company right now, but we’re going to keep our heads down and we’re going to keep building for the next few years and then I think we can be in a spot to be a strong public business.”

Accel’s Locke points out that in the U.S., mortgage and home finance are among the largest financial service markets, and they have primarily been handled by large banks.

“For most consumers, getting a mortgage through these banks continues to be an overly complex, slow-moving process,” Locke told TechCrunch. “We believe by providing consumers a great mobile experience, Lower will gain share from incumbent banks, in the same way that companies like Monzo have in banking or Venmo in payments or Trade Republic and Robinhood in stock trading.”

Powered by WPeMatico

For most people in India, having to engage with banks doesn’t instill a sense of joy. Banks in the South Asian market are notorious for making unannounced spam calls to upsell customers loans and credit cards, even when they have been explicitly asked not to do so.

Moreover, when a customer does reach out to a bank with a query, it can take forever to get the job done. Take ICICI Bank, India’s third largest bank and until recently my only banking partner for over six years, for an example.

It is now in its third month in figuring out who exactly in its relationship with Amazon is supposed to re-issue me a credit card. I have moved on with my life, and it looks like they did, too, likely before they even looked at my query.

Small and medium-sized businesses aren’t a big fan of banks, either. If you operate an early-stage startup, it’s anyone’s guess if you will ever be able to convince a bank to issue you a corporate account. So of course, startups — Razorpay and Open — took it upon themselves to fix this experience.

For consumers, too, in recent years, scores of startups have arrived on the scene to improve this banking experience. Whether you are a teenager, or just out of college, or a working professional, or don’t have a credit score, there are firms that can get you a credit card and loan.

But even these services have a ceiling limit of some sort. And customers aren’t loyal to any startup.

“A customer’s relationship is always with the entity where they park their savings deposit,” said Jitendra Gupta, a high-profile entrepreneur who has spent a decade in the fintech world. Since these customers are not parking their money with fintech, “the startups have been unable to disrupt the bank. That’s the hard reality.”

So what’s the alternative? Gupta, who co-founded CitrusPay (sold to Naspers’ PayU) and served as managing director of PayU, has been thinking about these challenges for more than two years.

“If you really want to change the banking industry, you cannot operate from the side. You have to fight from the centre, where they deposit their money. It’s a very time-consuming process and requires a lot of initial capital and experience with banks,” he told TechCrunch in an interview.

After more than a year and a half of raising about $24 million — from Sequoia Capital India, 3one4 Capital, Amrish Rau, Kunal Shah, Kunal Bahl, Tanglin Venture Partners, Rainmatter and others — Gupta is ready to launch what he believes will address a lot of the issues individuals face with their banks.

His new startup, called Jupiter, wants to bring “delight” to the banking experience, and it will launch in India on Thursday.

“We believe that a bank account should be a smart account, where it gives you insight, shares personalized tips and guides you through attaining some financial discipline,” he said.

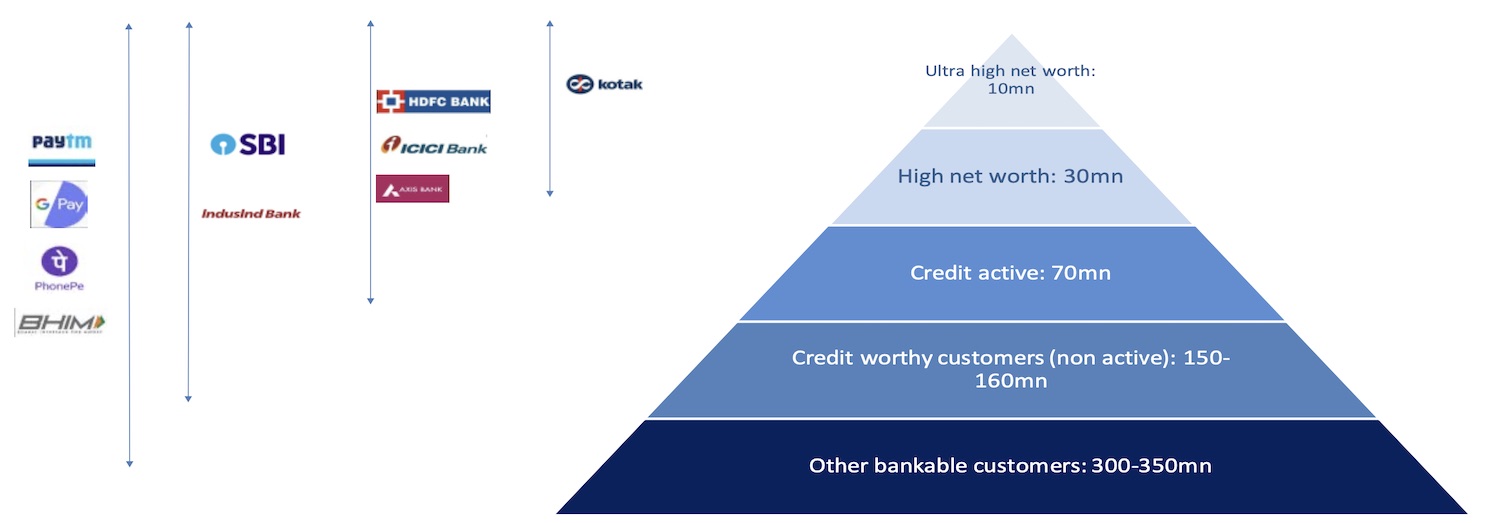

A snapshot of the reach of banks and fintech startups in India. Data: CIBIL, Statista, BofA Global Research. Image: BofA

To be sure, Jupiter, too, will offer loans and other financial services to customers. But instead of making irrelevant calls to customers, it will assess which of its customers are running short on money and give the option to take a credit line from its app itself, he said. “The upsell doesn’t need to happen by way of spam. It needs to happen by way of contextualization and personalization.”

“Jupiter has been built in a deep integration with the underlying bank, allowing the consumer to have a frictionless experience for all their banking needs,” said Amrish Rau, chief executive of Pine Labs, co-founder of CitrusPay and longtime friend of Gupta.

The startup, which employs 115 people, has developed a number of products for customers joining on day one. The products include the ability to buy now and pay later on UPI, a feature first offered in the market by Jupiter, and a mutual fund portfolio analyzer. A debit card, in-app chat with a customer service agent, expense categorisation, finding the right card, determining the existing health insurance coverage, and more are ready to ship, the startup said.

Jupiter is currently working on providing zero mark-up on forex transactions, and frictionless two-factor authentication. The startup has published a public Trello page where it has outlined the features it is working on and when it expects to ship them, as well as features suggested by its beta-testing customers. “I want to establish full transparency in what we are working on to build trust with customers,” said Gupta.

Jupiter will have its own customer relationship team that will engage with the startup’s users. The startup, which last month opened a waiting list for customers to sign up, had amassed more than 25,000 applications as of two weeks ago.

Even Jupiter, which one day wishes to disrupt the banking sector, currently has to partner with banks. Its partners are Federal Bank and Axis Bank.

I asked Gupta about the excitement his investors see in Jupiter. “Everyone believes, as you see with fintech giants such as Nubank globally, that we will become a full bank,” he said.

But for the time being, Gupta said he is not looking to partner with more banks. “I don’t want Jupiter to attract customers because they want to bank with Federal or Axis. I want them to come to Jupiter because they want to bank with Jupiter,” he said.

In the next 12 months, the startup hopes to serve more than 1 million customers.

Powered by WPeMatico

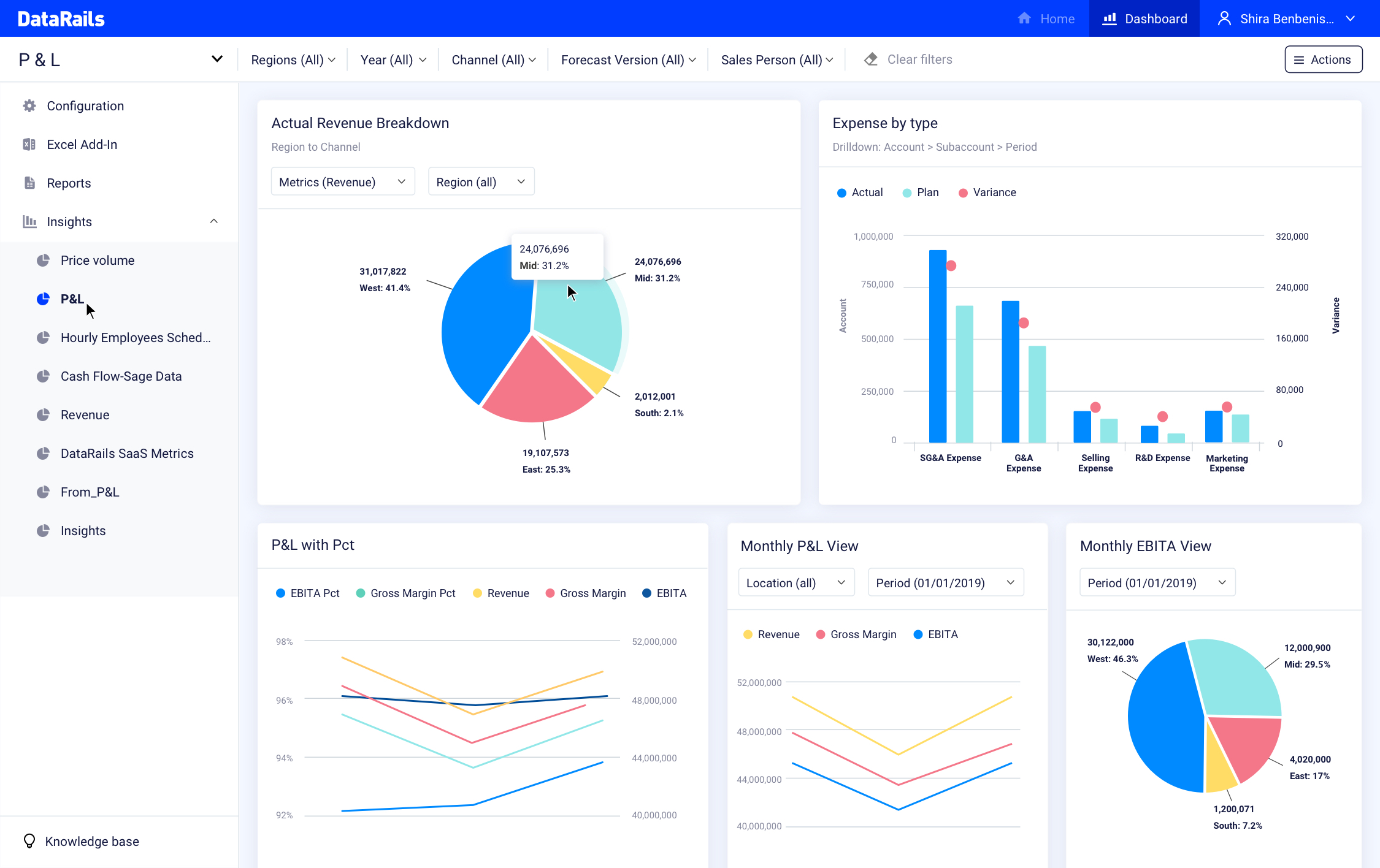

As enterprise startups continue to target interesting gaps in the market, we’re seeing increasingly sophisticated tools getting built for small and medium businesses — traditionally a tricky segment to sell to, too small for large enterprise tools, and too advanced in their needs for consumer products. In the latest development of that trend, an Israeli startup called DataRails has raised $25 million to continue building out a platform that lets SMBs use Excel to run financial planning and analytics like their larger counterparts.

The funding closes out the company’s Series A at $43.5 million, after the company initially raised $18.5 million in April (some at the time reported this as its Series A, but it seems the round had yet to be completed). The full round includes Zeev Ventures, Vertex Ventures Israel and Innovation Endeavors, with Vintage Investment Partners added in this most recent tranche. DataRails is not disclosing its valuation, except to note that it has doubled in the last four months, with hundreds of customers and on target to cross 1,000 this year, with a focus on the North American market. It has raised $55 million in total.

The challenge that DataRails has identified is that on one hand, SMBs have started to adopt a lot more apps, including software delivered as a service, to help them manage their businesses — a trend that has been accelerated in the last year with the pandemic and the knock-on effect that has had for remote working and bringing more virtual elements to replace face-to-face interactions. Those apps can include Salesforce, NetSuite, Sage, SAP, QuickBooks, Zuora, Xero, ADP and more.

But on the other hand, those in the business who manage finances and financial reporting are lacking the tools to look at the data from these different apps in a holistic way. While Excel is a default application for many of them, they are simply reading lots of individual spreadsheets rather than integrated data analytics based on the numbers.

DataRails has built a platform that can read the reported information, which typically already lives in Excel spreadsheets, and automatically translate it into a bigger picture view of the company.

For SMEs, Excel is such a central piece of software, yet such a pain point for its lack of extensibility and function, that this predicament was actually the germination of starting DataRails in the first place,

Didi Gurfinkel, the CEO who co-founded the company with Eyal Cohen (the CPO) said that DataRails initially set out to create a more general-purpose product that could help analyze and visualize anything from Excel.

Image: DataRails

“We started the company with a vision to save the world from Excel spreadsheets,” he said, by taking them and helping to connect the data contained within them to a structured database. “The core of our technology knows how to take unstructured data and map that to a central database.” Before 2020, DataRails (which was founded in 2015) applied this to a variety of areas with a focus on banks, insurance companies, compliance and data integrity.

Over time, it could see a very specific application emerging, specifically for SMEs: providing a platform for FP&A (financial planning and analytics), which didn’t really have a solution to address it at the time. “So we enabled that to beat the market.”

“They’re already investing so much time and money in their software, but they still don’t have analytics and insight,” said Gurfinkel.

That turned out to be fortunate timing, since “digital transformation” and getting more out of one’s data was really starting to get traction in the world of business, specifically in the world of SMEs, and CFOs and other people who oversaw finances were already looking for something like this.

The typical DataRails customer might be as small as a business of 50 people, or as big as 1,000 employees, a size of business that is too small for enterprise solutions, “which can cost tens of thousands of dollars to implement and use,” added Cohen, among other challenges. But as with so many of the apps that are being built today to address those using Excel, the idea with DataRails is low-code or even more specifically no-code, which means “no IT in the loop,” he said.

“That’s why we are so successful,” he said. “We are crossing the barrier and making our solution easy to use.”

The company doesn’t have a huge number of competitors today, either, although companies like Cube (which also recently raised some money) are among them. And others like Stripe, while currently not focusing on FP&A, have most definitely been expanding the tools that it is providing to businesses as part of their bigger play to manage payments and subsequently other processes related to financial activity, so perhaps it, or others like it, might at some point become competitors in this space as well.

In the meantime, Gurfinkel said that other areas that DataRails is likely to expand to cover alongside FP&A include HR, inventory and “planning for anything,” any process that you have running in Excel. Another interesting turn would be how and if DataRails decides to look beyond Excel at other spreadsheets, or bypass spreadsheets altogether.

The scope of the opportunity — in the U.S. alone there are more than 30 million small businesses — is what’s attracting the investment here.

“We’re thrilled to reinvest in DataRails and continue working with the team to help them navigate their recent explosive and rapid growth,” said Yanai Oron, general partner at Vertex Ventures, in a statement. “With innovative yet accessible technology and a tremendous untapped market opportunity, DataRails is primed to scale and become the leading FP&A solution for SMEs everywhere.”

“Businesses are constantly about to start, in the midst of, or have just finished a round of financial reporting — it’s a never-ending cycle,” added Oren Zeev, founding partner at Zeev Ventures. “But with DataRails, FP&A can be simple, streamlined, and effective, and that’s a vision we’ll back again and again.”

Powered by WPeMatico

Small businesses have traditionally been underserved when it comes to IT — they are too big and have too many requirements that can’t be met by consumer products, yet are much too small to afford, implement or thoroughly need apps and other IT build for larger enterprises. But when it comes to neobanks, it feels like there is no shortage of options for the SMB market, nor venture funding being invested to help them grow.

In the latest development, Novo, a neobank that has built a service targeting small businesses, has closed a round of $40.7 million, a Series A that it will be using to continue growing its business, and its platform.

The funding is being led by Valar Ventures with Crosslink Capital, Rainfall Ventures, Red Sea Ventures and BoxGroup all participating. The startup is not disclosing valuation, but Novo — originally founded in New York in 2018 but now based out of Miami — has racked up 100,000 SMB customers — which it defines as businesses that make between $25,000 and $100,000 in annualized revenues — and has seen $1 billion in lifetime transactions, with growth accelerating in the last couple of years.

There are a wide variety of options for small businesses these days when it comes to going for a banking solution. They include staying with traditional banks (which are starting to add an increasing number of services and perks to retain small business customers), as well as a variety of fintechs — other neobanks, like Novo — that are building banking and related financial tools to cater to startups and other small businesses.

Just doing a quick search, some of the others targeting the sector include Rho, NorthOne, Lili, Mercury, Brex, Hatch, Anna, Tide, Viva Wallet, Open and many more (and you could argue also players like Amazon, offering other money management and spending tools similar to what neobanks are providing). Some of these are not in the U.S., and some are geared more at startups, or freelancers, but taken together they speak to the opportunity and also the attention that it is getting from the tech industry right now.

As CEO and co-founder Michael Rangel — who hails from Miami — described it to me, one of the key differentiators with Novo is that it’s approaching SMB banking from the point of view of running a small business. By this, he means that typically SMBs are already using a lot of other finance software — on average seven apps per business — to manage their books, payments and other matters, and so Novo has made it easier by way of a “drag and drop” dashboard where an SMB can integrate and view activity across all of those apps in one place. There are “dozens” of integrations currently, he said, and more are being added.

This is the first step, he said. The plan is to build more technology so that the activity between different apps can also be monitored, and potentially automated

“We’re able to see this is your balance and what you should expect,” he said. “The next frontier is to marry the incoming with outgoing. We’re using the funding to build that, and it’s on the roadmap in the next six months.”

Novo has yet to bring cash advances or other lending products into its platform, although those too are on the roadmap, but it is also listening to its customers and watching what they want to do on the platform — another reason why it’s clever to make it easy to for those customers to integrate other services into Novo: not only does that solve a pain point for the customer, but it becomes a pretty clear indicator of what customers are doing, and how you could better cater to that.

Listening to the customers is in itself becoming a happy challenge, it seems. Novo launched quietly enough — between 2018 and the end of 2019, it had picked up only 5,000 accounts. But all that changed during 2020 and the COVID-19 pandemic, which Rangel describes as “just hockey stick growth. We grew like crazy.”

The reason, he said, is a classic example of why incumbent banks have to catch up with the times. Everyone was locked down at home, and suddenly a lot of people who were either furloughed or laid off were “spinning up businesses,” he said, and that led to many of them needing to open bank accounts. But those who tried to do this with high-street banks were met with a pretty significant barrier: you had to go into the bank in person to authenticate yourself, but either the banks were closed, or people didn’t want to travel to them. That paved the way for Novo (and others) to cater to them.

Its customer numbers shot up to 24,000 in the year.

Then other market forces have also helped it. You might recall that banking app Simple was shut down by BBVA ahead of its merger with PNC; but at the same time, it also shut down Azlo, it’s small business banking service. That led to a significant number of users migrating to other services, and Novo got a huge windfall out of that, too.

In the last six months, Novo grew four-fold, and Rangel attributed a lot of that to ex-Azloans looking for a new home.

The fact that there are so many SMB banking providers out there might mean competition, but it also means fragmentation, and so if a startup emerges that seems to be catching on, it’s going to catch something else, too: the eye of investors.

“The ability of the Novo team to grow the company rapidly during a year where businesses have faced unprecedented challenges is impressive,” said Andrew McCormack, founding partner at Valar Ventures, the firm co-founded by Peter Thiel, another big figure in fintech. “Novo tripled its small business customer base in the first half of 2021! Their custom infrastructure and banking platform put them in prime position to expand their services at an even faster pace as we come out of the health crisis. All of us at Valar Ventures are excited to join this team.”

Powered by WPeMatico

How big is the market in India for a neobank aimed at teenagers? Scores of high-profile investors are backing a startup to find out.

Bangalore-based FamPay said on Wednesday it has raised $38 million in its Series A round led by Elevation Capital. General Catalyst, Rocketship VC, Greenoaks Capital and existing investors Sequoia Capital India, Y Combinator, Global Founders Capital and Venture Highway also participated in the new round, which brings FamPay’s to-date raise to $42.7 million.

TechCrunch reported early this month that FamPay was in talks with Elevation Capital to raise a new round.

Founded by Sambhav Jain and Kush Taneja (pictured above) — both of whom graduated from Indian Institute of Technology, Roorkee in 2019 — FamPay enables teenagers to make online and offline payments.

The thesis behind the startup, said Jain in an interview with TechCrunch, is to provide financial literacy to teenagers, who additionally have limited options to open a bank account in India at a young age. Through gamification, the startup said it’s making lessons about money fun for youngsters.

Unlike in the U.S., where it’s common for teenagers to get jobs at restaurants and other places and understand how to handle money at a young age, a similar tradition doesn’t exist in India.

After gathering the consent from parents, FamPay provides teenagers with an app to make online purchases, as well as plastic cards — the only numberless card of its kind in the country — for offline transactions. Parents credit money to their children’s FamPay accounts and get to keep track of high-ticket spendings.

In other markets, including the U.S., a number of startups including Greenlight, Step and Till Financial are chasing to serve the teenagers, but in India, there currently is no startup looking to solve the financial access problem for teenagers, said Mridul Arora, a partner at Elevation Capital, in an interview with TechCrunch.

It could prove to be a good issue to solve — India has the largest adolescent population in the world.

“If you’re able to serve them at a young age, over a course of time, you stand to become their go-to product for a lot of things,” Arora said. “FamPay is serving a population that is very attractive and at the same time underserved.”

The current offerings of FamPay are just the beginning, said Jain. Eventually the startup wishes to provide a range of services and serve as a neobank for youngsters to retain them with the platform forever, he said, though he didn’t wish to share currently what those services might be.

Image Credits: FamPay

Teens represent the “most tech-savvy generation, as they haven’t seen a world without the internet,” he said. “They adapt to technology faster than any other target audience and their first exposure with the internet comes from the likes of Instagram and Netflix. This leads to higher expectations from the products that they prefer to use. We are unique in approaching banking from a whole new lens with our recipe of community and gamification to match the Gen Z vibe.”

“I don’t look at FamPay just as a payments service. If the team is able to execute this, FamPay can become a very powerful gateway product to teenagers in India and their financial life. It can become a neobank, and it also has the opportunity to do something around social, community and commerce,” said Arora.

During their college life, Jain and Taneja collaborated and built an app and worked at a number of startups, including social network ShareChat, logistics firm Rivigo and video streaming service Hotstar. Jain said their work with startups in the early days paved the idea to explore a future in this ecosystem.

Prior to arriving at FamPay, Jain said the duo had thought about several more ideas for a startup. The early days of FamPay were uniquely challenging to the founders, who had to convince their parents about their decision to do a startup rather than joining firms or startups as had most of their peers from college. Until being selected by Y Combinator, Jain said he didn’t even fully understand a cap table and dilutions.

He credited entrepreneurs such as Kunal Shah (founder of CRED) and Amrish Rau (CEO of Pine Labs) for being generous with their time and guidance. They also wrote some of the earliest checks to the startup.

The startup, which has amassed over 2 million registered users, plans to deploy the fresh capital to expand its user base and product offerings, and hire engineers. It is also looking for people to join its leadership team, said Jain.

Powered by WPeMatico