Finance

Auto Added by WPeMatico

Auto Added by WPeMatico

Square paid around a quarter of its present-day value for Afterpay, Alex Wilhelm notes in The Exchange. That seems like a lot. But was it too much?

“Afterpay brings global revenues, global users and a more diverse merchant network to Square,” Alex notes. “It would have had to spend to derive those assets over time. Square is willing to pay up to snag them now.”

Dana Stalder, a partner at Matrix Partners and Afterpay’s only institutional investor, describes the deal as part of a recurring “critical innovation cycle” in fintech that “determines the winners and losers” for decades to come.

“I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants,” says Stalder. “Even more so than eBay + PayPal.”

Thanks very much for reading Extra Crunch this week!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: jayk7 (opens in a new window) / Getty Images

Developers may delight in solving complex technical problems, but the problem of a career path is one many don’t think much about, Juniper Networks CTO Raj Yavatkar writes in a guest column.

He offers a solution that should appeal to developers and engineers: “Treat career advancement as you would a software project.”

Image Credits: Scott Tong

At Early Stage 2021, design expert Scott Tong shared some ways founders should think about design and branding.

If you can link your brand with your company’s reputation, I think it’s a really great place to start when you’re having conversations about brands. What is the first impression? What are the consistent behaviors that your brand hopes to repeat over and over? What are the memorable moments that stand out and make your brand, your reputation memorable?

Image Credits: Nora Carol Photography (opens in a new window) / Getty Images

If you’re fortunate enough to be considering cashing in on vested stock options, this guest column is worth a read.

“Most companies admit they need to be better at explaining how ISOs work in general, but they can’t legally work one-on-one with employees to help them exercise and sell shares the right way,” Wealthramp’s Pam Krueger and John Chapman write.

“That’s why, when the time is right, many employees actively look for help from a qualified fiduciary financial adviser who can walk these could-be ‘options millionaires’ through various cash-in scenarios.”

Image Credits: metamorworks (opens in a new window) / Getty Images

At some point, almost every early-stage startup will use paid search ads to connect with customers and throw down the gauntlet with their competitors.

Most of these initial attempts at paid search are unsuccessful. There’s a steep learning curve when it comes to transforming passive searchers into paying customers, and almost no one gets it right the first time.

In a comprehensive guest post, growth marketing expert Stewart Hillhouse identified “14 questions your paid search should answer to ensure you’re only paying for the highest-intent shoppers.”

Question 1? “What’s in it for me?”

Image Credits: Duolingo

Duolingo’s debut last week was a bright spot, Alex Wilhelm and Natasha Mascarenhas write, with the language learning app’s stock price landing above a raised IPO range.

Alex and Natasha detail five lessons to take from Duolingo’s flotation:

Image Credits: Andriy Onufriyenko (opens in a new window) / Getty Images

In the U.S. alone, yearly spending on AI R&D is expected to reach $100 billion by 2025.

But can your humble startup attract and retain users while it conducts research and product development?

“For obvious reasons, companies want to make things that matter to their customers, investors and stakeholders. Ideally, there’s a way to do both,” says João Graça, CTO and co-founder of Unbabel, an AI-powered language operations platform.

Image Credits: Bryce Durbin

As part of an ongoing series with transportation startup founders, Rebecca Bellan interviews Kodiak Robotics CEO and co-founder Don Burnette about why the autonomous trucking company remains private when so many of its rivals have gone public.

“I think there’s also lots of opportunity within the VCs and the private markets,” said Burnette.

“Kodiak is one of the only remaining serious AV trucking companies still in the private sector, and so I think that gives us some advantages in a lot of ways.”

Image Credits: Nigel Sussman (opens in a new window)

After interviewing Draper Esprit co-founder Stuart Chapman, Alex Wilhelm and Anna Heim took a look at the trend of European VCs floating themselves.

Traditional VC models “can foist artificial time constraints on investors and force them to focus their deal flow into particular stages for fund-construction reasons,” Alex and Anna write for The Exchange.

“As we found out researching this piece, the public venture model highlights some of these limitations — and may be able to alleviate them in part.”

Image Credits: Nigel Sussman (opens in a new window)

After Robinhood failed to burn up the stock charts, Alex Wilhelm wondered why, exactly, the investing and trading app’s IPO didn’t live up to expectations.

He spoke to Robinhood CFO Jason Warnick, who shared a few reasons why it was time for the company to float:

… Warnick indicated that there were a few factors at play, including that Robinhood had built out its leadership team and its internal processes, and that it had worked on user-safety-related tasks and expanded the site’s use cases. All of that is true.

Powered by WPeMatico

Indian fintech startup BharatPe has raised $370 million in a new round of financing as it looks to aggressively scale its business in the next two years. It’s the nineteenth Indian startup to become a unicorn this year (up from 11 last year) as several high-profile global investors double down in the South Asian market.

The new round — a Series E — was led by Tiger Global and valued the New Delhi-based startup at $2.85 billion (post-money), it said in a statement Tuesday evening. Dragoneer Investor Group and Steadfast Capital also participated in the new round, which brings the startup’s to-date raise to over $580 million against equity.

Tuesday’s news confirms a TechCrunch scoop from June in which we reported that the four-year-old startup was looking to raise about $250 million at a pre-money valuation of $2.5 billion. BharatPe was valued at about $900 million in its Series D round in February this year, and $425 million last year.

BharatPe co-founder Ashneer Grover confirmed that the startup was indeed looking to raise $250 million until inbound requests from investors prompted an oversubscription. The new investment also includes some secondary transactions.

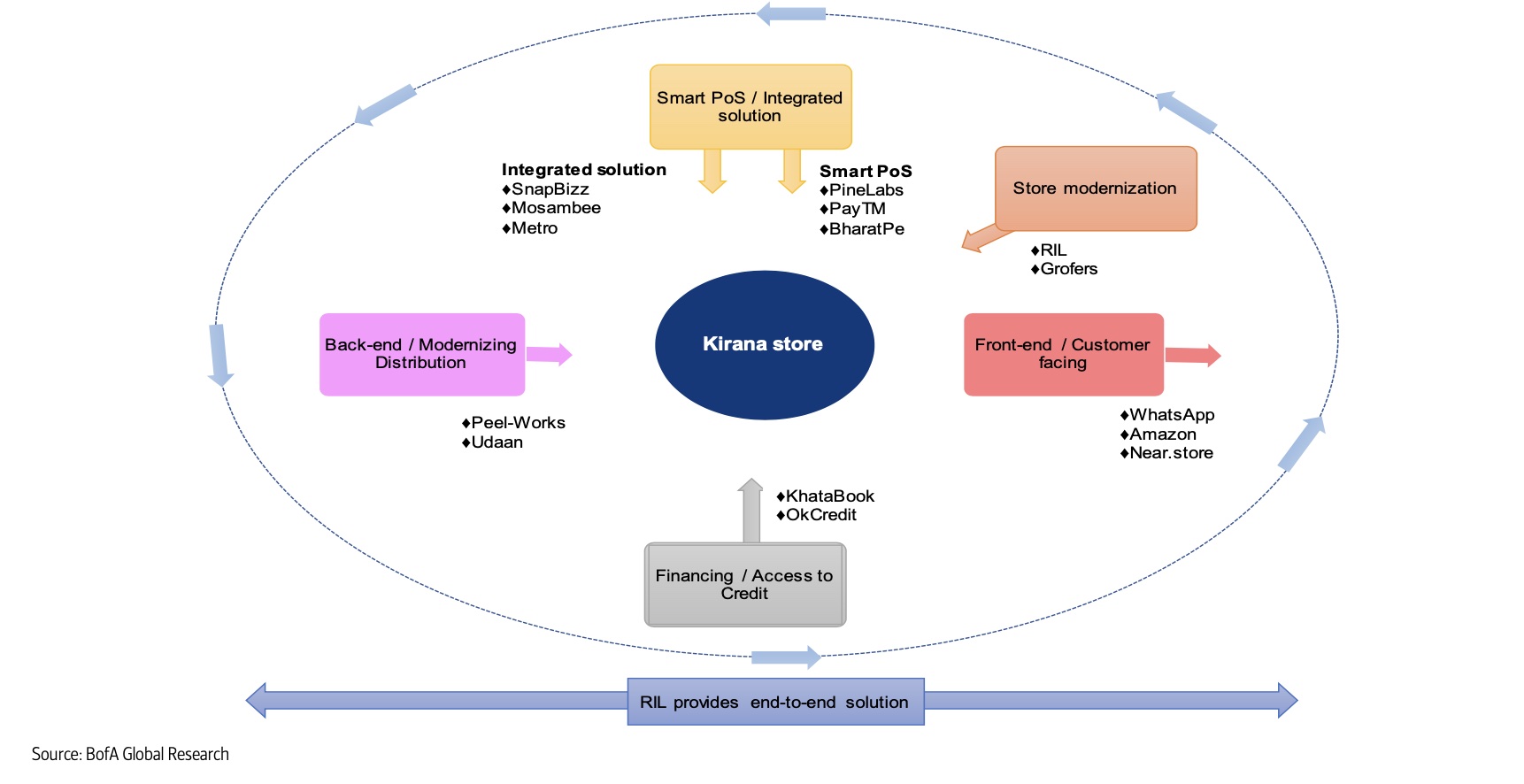

BharatPe, which counts Coatue, Ribbit Capital and Sequoia Capital India among its existing investors, operates an eponymous service to help offline merchants accept digital payments and secure working capital.

Even as India has already emerged as the second-largest internet market, with more than 650 million users, much of the country remains offline.

Among those outside of the reach of the internet are merchants running small businesses, such as roadside tea stalls and neighborhood stores. To make these merchants comfortable with accepting digital payments, BharatPe relies on QR codes and point of sale machines that support government-backed UPI payments infrastructure.

Scores of giants and startups are attempting to serve neighborhood stores in India. Image Credits: Bank of America Research

The startup, which serves more than 7 million merchants in over 130 Indian cities, said it has disbursed close to $300 million to merchant partners. It does not charge merchants for universal QR code access, but is looking to make money by lending.

The startup plans to expand its product offerings as well as work with Centrum Financial Services, with which it was recently granted the license by India’s central bank (Reserve Bank of India) to set up a small finance bank. (Centrum Financial Services has collaborated with BharatPe for the license, and the Indian startup says the two are “equal” partners.)

Tuesday’s development further illustrates the growing interest of Tiger Global in India. The New York-headquartered firm has backed dozens of Indian startups, including social commerce startup DealShare, edtech Classplus, Apna (an app that helps blue-collar workers connect with recruiters) and home services platform Urban Company in recent months.

On Tuesday, Infra.Market, an Indian startup that helps construction and real estate companies procure materials and handle logistics for their projects, said it had raised $125 million in a round led also by Tiger Global.

Powered by WPeMatico

One of the big reasons you’re giving 110% of your talent and effort to your private company is because you’re hoping to eventually cash in on all those vested incentive stock options (ISOs) that have been sitting in some account, waiting for the day your company goes public.

There’s nothing wrong with that. Who doesn’t dream of reaping an options windfall and using it to retire early, buy a house, pay off their college loans, travel around the world or become a full-time philanthropist?

Unfortunately, when it comes to figuring out how to cash in their stock awards, most employees are on their own.

Their employers can’t always provide the answers they need — especially when the questions relate to personal finances. Most companies admit they need to be better at explaining how ISOs work in general, but they can’t legally work one-on-one with employees to help them exercise and sell shares the right way.

Most companies admit they need to be better at explaining how ISOs work in general, but they can’t legally work one-on-one with employees to help them exercise and sell shares the right way.

That’s why, when the time is right, many employees actively look for help from a qualified fiduciary financial adviser who can walk these could-be “options millionaires” through various cash-in scenarios.

Here’s a real-life example (using a pseudonym).

Kurt is a 50-year-old VP of product management at a healthcare startup that just went public. Over his three years with the company, Kurt had amassed 350,000 ISOs worth approximately $6 million. Unlike many options millionaires, he didn’t intend to cash in everything and retire early. He planned to stay with the firm but wanted to liquidate enough ISOs to pay for a vacation home and add greater diversification to his investment portfolio. This presented significant tax risks that Kurt wasn’t aware of.

If Kurt exercised his ISOs and sold the shares before a year had passed, his profits would be characterized as short-term capital gains, which are taxed as ordinary income.

To illustrate the potential tax implications of this action, we created a hypothetical scenario that showed if Kurt exercised all of his ISOs and sold the shares immediately, he would incur approximately $6 million in ordinary income, which would push him into the top tax bracket and put him on the hook for almost $3 million in combined federal and state taxes.

Powered by WPeMatico

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

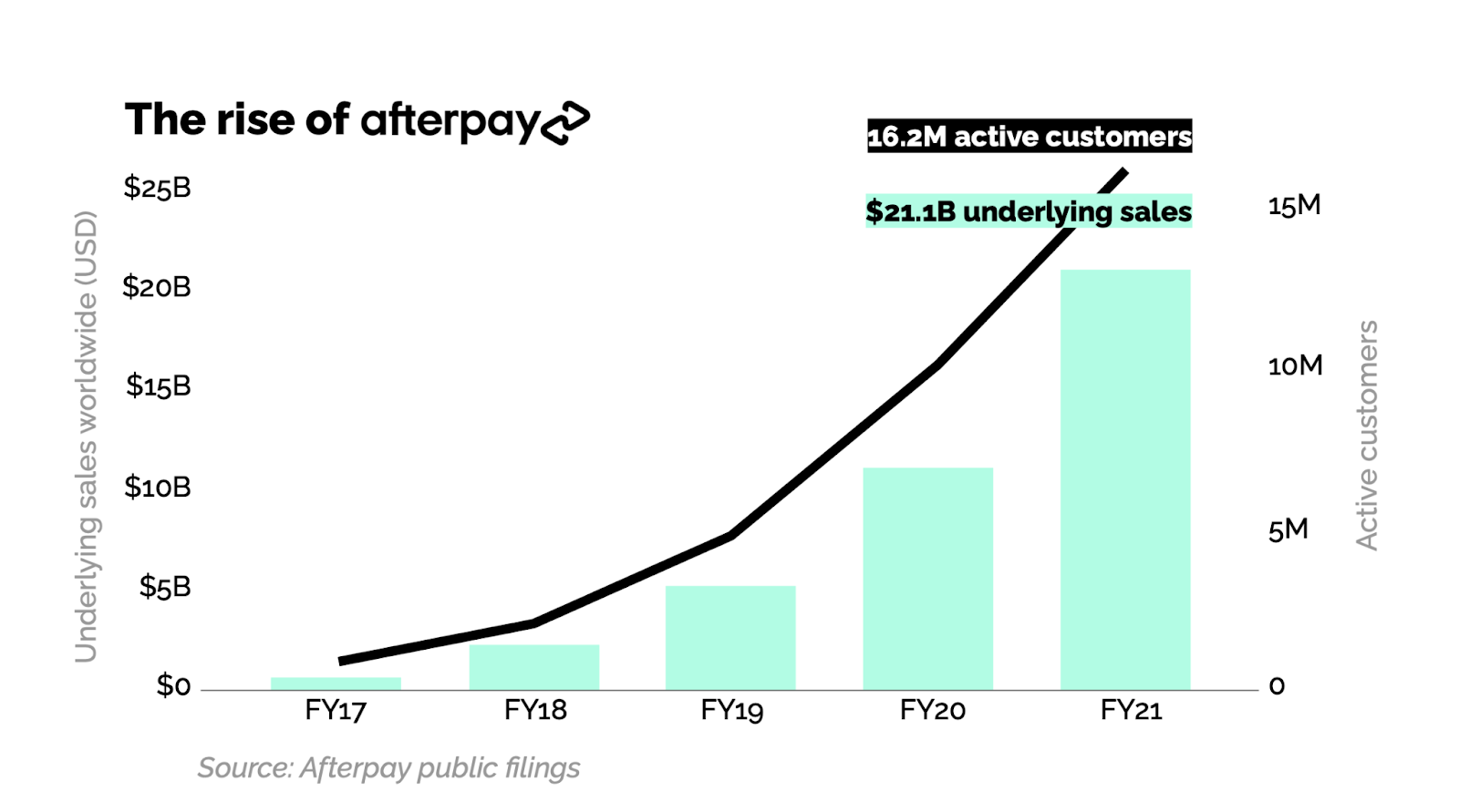

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

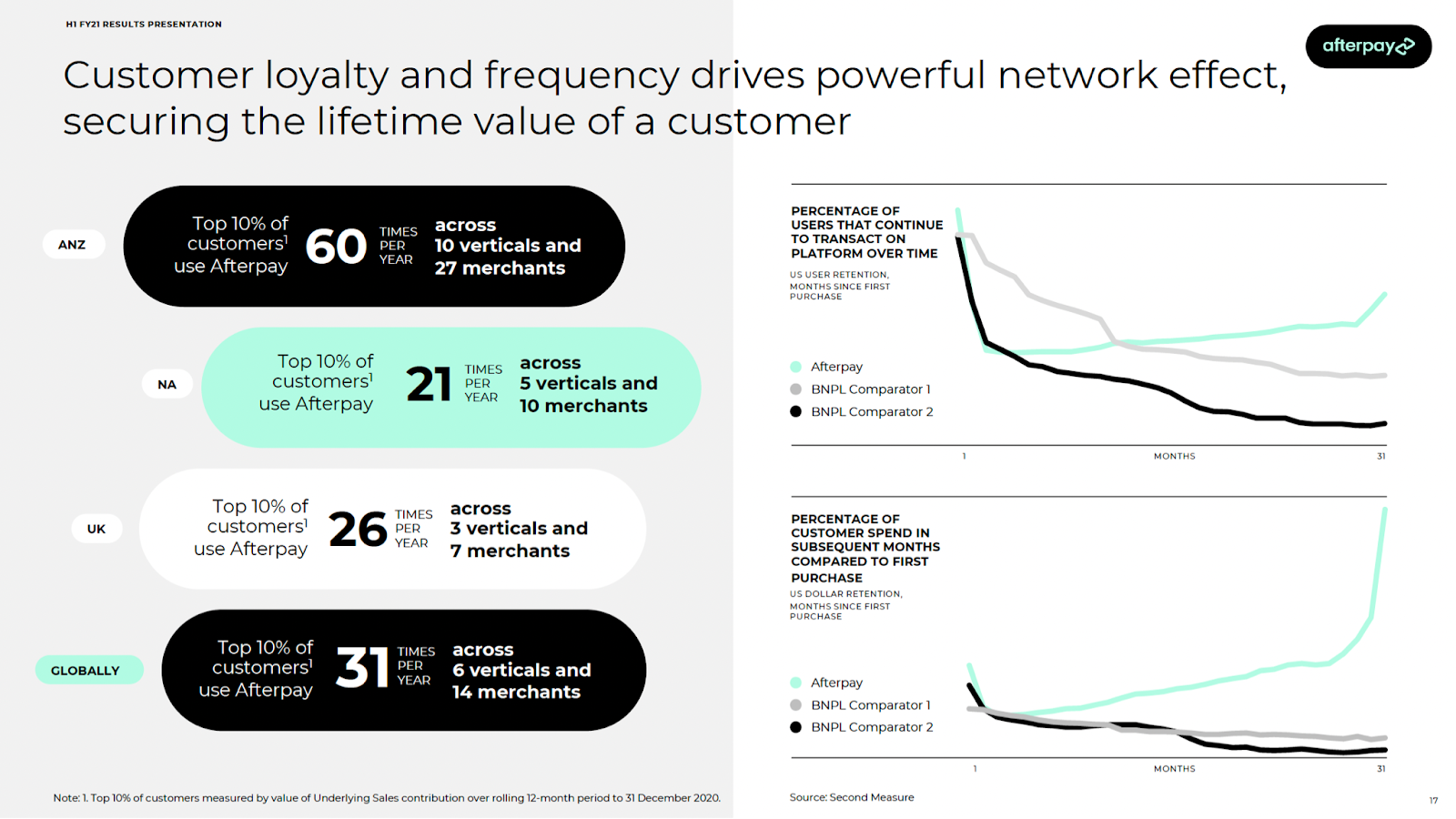

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

Chilean startup Xepelin, which has created a financial services platform for SMEs in Latin America, has secured $30 million in equity and $200 million in credit facilities.

LatAm venture fund Kaszek Ventures led the equity portion of the financing, which also included participation from partners of DST Global and a slew of other firms and founders/angel investors. LatAm- and U.S.-based asset managers and hedge funds — including Chilean pension funds — provided the credit facilities. In total over its lifetime, Xepelin has raised over $36 million in equity and $250 million in asset-backed facilities.

Also participating in the round were Picus Capital; Kayak Ventures; Cathay Innovation; MSA Capital; Amarena; FJ Labs; Gilgamesh Ventures. A group of angels also participated in the financing, including Kavak founder and CEO Carlos Garcia; Jackie Reses, executive chairman of Square Financial Services; Justo founder and CEO Ricardo Weder; Tiger Global Management Partner John Curtius; GGV’s Hans Tung; and Gerry Giacoman, founder and CEO of Clara, among others.

Nicolás de Camino and Sebastian Kreis founded Xepelin in mid-2019 with the mission of changing the fact that “only 5% of companies in all LatAm countries have access to recurring financial services.”

“We want all SMEs in LatAm to have access to financial services and capital in a fair and efficient way,” the pair said.

Xepelin is built on a SaaS model designed to give SMEs a way to organize their financial information in real time. Embedded in its software is a way for companies to apply for short-term working capital loans “with just three clicks, and receive the capital in a matter of hours,” the company claimed.

It has developed an AI-driven underwriting engine, which the execs said gives it the ability to make real-time loan approval decisions.

“Any company in LatAm can onboard in just a few minutes and immediately access a free software that helps them organize their information in real time, including cash flow, revenue, sales, tax, bureau info — sort of a free CFO SaaS,” de Camino said. “The circle is virtuous: SMEs use Xepelin to improve their financial habits, obtain more efficient financing, pay their obligations, and collaborate effectively with clients and suppliers, generating relevant impacts in their industries.”

The fintech currently has over 4,000 clients in Chile and Mexico, which currently has a growth rate “four times faster” than when Xepelin started in Chile. Over the past 22 months, it has loaned more than $400 million to SMBs in the two countries. It currently has a portfolio of active loans for $120 million and an asset-backed facility for more than $250 million.

Overall, the company has been seeing a growth rate of 30% per month, the founders said. It has 110 employees, up from 20 a year ago.

“When we talk about creating the largest digital bank for SMEs in LatAm, we are not saying that our goal is to create a bank; perhaps we will never ask for the license to have one, and to be honest, everything we do, we do it differently from the banks, something like a non-bank, a concept used today to exemplify focus,” the founders said.

Both de Camino and Kreis said they share a passion for making financial services more accessible to SMEs all across Latin America and have backgrounds rooted deep in different areas of finance.

“Our goal is to scale a platform that can solve the true pains of all SMEs in LatAm, all in one place that also connects them with their entire ecosystem, and above all, democratized in such a way that everyone can access it,” Kreis said, “regardless of whether you are a company that sells billions of dollars or just a thousand dollars, getting the same service and conditions.”

For now, the company is nearly exclusively focused on the B2B space, but in the future, it believes several of its services “will be very useful for all SMEs and companies in LatAm.”

“Xepelin has developed technology and data science engines to deliver financing to SMBs in Latin America in a seamless way,” Nicolas Szekasy, co-founder and managing partner at Kaszek Ventures, said in a statement. “The team has deep experience in the sector and has proven a perfect fit of their user-friendly product with the needs of the market.”

Chile was home to another large funding earlier this week. NotCo, a food technology company making plant-based milk and meat replacements, closed on a $235 million Series D round that gives it a $1.5 billion valuation.

Powered by WPeMatico

PayPal’s plan to morph itself into a “super app” has been given a go for launch.

According to PayPal CEO Dan Schulman, speaking to investors during this week’s second-quarter earnings call, the initial version of PayPal’s new consumer digital wallet app is now “code complete” and the company is preparing to slowly ramp up. Over the next several months, PayPal expects to be fully ramped up in the U.S., with new payment services, financial services, commerce and shopping tools arriving every quarter.

The company has spoken for some time about its “super app” ambitions — a shift in product direction that would make PayPal a U.S.-based version of something like China’s WeChat or Alipay or India’s Paytm. Like those apps, PayPal aims to offer a host of consumer services under one roof, beyond just mobile payments.

In previous quarters, PayPal said these new features may include things like enhanced direct deposit, check cashing, budgeting tools, bill pay, crypto support, subscription management, and buy now, pay later functionality. It also said it would integrate commerce, thanks to the mobile shopping tools acquired by way of its $4 billion Honey acquisition in 2019.

So far, PayPal has continued to run Honey as a standalone application, website and browser extension, but the super app could incorporate more of its deal-finding functions, price-tracking features and other benefits.

On Wednesday’s earnings call, Schulman revealed the super app would have a few other features as well, including high-yield savings, early access to direct deposit funds and messaging functionality outside of peer-to-peer payments — meaning you could chat with family and friends directly through the app’s user interface.

PayPal hadn’t announced its plans to include a messaging component until now, but the feature makes sense in terms of how people often combine chat and peer-to-peer payments today. For example, someone may want to make a personal request for the funds instead of just sending an automated request through an app. Or, after receiving payment, a user may want to respond with a “thank you,” or other acknowledgment. Currently, these conversations take place outside of the payment app itself on platforms like iMessage. Now, that could change.

“We think that’s going to drive a lot of engagement on the platform,” said Schulman. “You don’t have to leave the platform to message back and forth.”

With the increased user engagement, the company expects to see a bump in average revenue per active account.

Schulman also hinted at “additional crypto capabilities,” which were not detailed. However, PayPal earlier this month increased the crypto purchase limit from $20,000 to $100,000 for eligible PayPal customers in the U.S., with no annual purchase limit. The company also this year made it possible for consumers to check out at millions of online businesses using their cryptocurrencies, by first converting the crypto to cash then settling with the merchant in U.S. dollars.

Though the app’s code is now complete, Schulman said the plan is to continue to iterate on the product experience, noting that the initial version will not be “the be-all and end-all.” Instead, the app will see steady releases and new functionality on a quarterly basis.

However, he did say that early on, the new features would include the high-yield savings, improved bill pay with a better user experience, and more billers and aggregators, as well as early access to direct deposit, budgeting tools and the new two-way messaging feature.

To integrate all the new features into the super app, PayPal will undergo a major overhaul of its user interface.

“Obviously, the [user experience] is being redesigned,” Schulman noted. “We’ve got rewards and shopping. We’ve got a whole giving hub around crowdsourcing, giving to charities. And then, obviously, buy now, pay later will be fully integrated into it. … The last time I counted, it was like 25 new capabilities that we’re going to put into the super app.”

The digital wallet app will also be personalized to the end user, so no two apps are the same. This will be done using both artificial intelligence and machine learning capabilities to “enhance each customer’s experiences and opportunities,” said Schulman.

PayPal delivered an earnings beat in the second quarter with $6.24 billion in revenue, versus the $6.27 billion Wall Street expected, and earnings per share of $1.15, versus the $1.12 expected. Total payment volume from merchant customers also jumped 40% to $311 billion, while analysts had projected $295.2 billion. But the company’s stock slipped due to a lowered outlook for Q3, impacted by eBay’s transition to its own managed payments service.

In addition, PayPal gained 11.4 million net new active accounts in the quarter, to reach 403 million total active accounts.

Powered by WPeMatico

Cairo and Dubai-based ride-sharing company Swvl plans to go public in a merger with special purpose acquisition company Queen’s Gambit Growth Capital, Swvl said Tuesday. The deal will see Swvl valued at roughly $1.5 billion.

Swvl was founded by Mostafa Kandil, Mahmoud Nouh and Ahmed Sabbah in 2017. The trio started the company as a bus-hailing service in Egypt and other ride-sharing services in emerging markets with fragmented public transportation.

Its services, mainly bus-hailing, enables users to make intra-state journeys by booking seats on buses running a fixed route. This is pocket-friendly for residents in these markets compared to single-rider options and helps reduce emissions (Swvl claims it has prevented over 240 million pounds of carbon emission since inception).

After its Egypt launch, Swvl expanded to Kenya, Pakistan, Jordan and Saudi Arabia. The company also moved its headquarters to Dubai as part of its strategy to become a global company.

Swvl offerings have expanded beyond bus-hailing services. Now, the company offers inter-city rides, car ride-sharing, and corporate services across the 10 cities it operates in across Africa and the Middle East.

Queen’s Gambit, the women-led SPAC in charge of the deal, raised $300 million in January and added $45 million via an underwriters’ overallotment option focusing on startups in clean energy, healthcare and mobility sectors.

The statement also mentions a group of investors — Agility, Luxor Capital and Zain Group — which will contribute $100 million through a private investment in public equity, or PIPE.

Per Crunchbase, Swvl has raised over $170 million. From an African perspective, Swvl features as one of the most venture-backed startups on the continent. The company has been touted to reach unicorn status in the past and will when this SPAC merger is completed.

The company will aptly trade under the ticker SWVL. The listing will make it the first Egyptian startup to go public outside Egypt and the second to go public after Fawry. It will also make the mobility company the largest African unicorn debut on any U.S.-listed exchange, beating Jumia’s debut of $1.1 billion on the NYSE. In the Middle East, Swvl joins music-streaming platform Anghami as the second startup to go public via a SPAC merger.

Swvl had annual gross revenue of $26 million in 2020, according to the statement, and the company expects its annual gross revenue to increase to $79 million this year and $1 billion by 2025 after expanding to 20 countries across five continents.

On why Queen’s Gambit picked Swvl for this deal, Victoria Grace, founder and CEO, said in a statement that the company fit the profile of what she was looking for: “a disruptive platform that solves complex challenges and empowers underserved populations.”

“Having established a leadership position in key emerging markets, we believe Swvl is ready to capitalize on a truly global market opportunity,” she added.

In May, TechCrunch wrote that SPACs didn’t target African startups for several reasons, including a lack of global appeal and private capital and market satisfaction. Judging by Grace’s comments, Swvl has that global appeal and is ready to venture into the public market despite being in operation for just four years.

Powered by WPeMatico

Anomaly detection is one of the more difficult and underserved operational areas in the asset-servicing sector of financial institutions. Broadly speaking, a true anomaly is one that deviates from the norm of the expected or the familiar. Anomalies can be the result of incompetence, maliciousness, system errors, accidents or the product of shifts in the underlying structure of day-to-day processes.

For the financial services industry, detecting anomalies is critical, as they may be indicative of illegal activities such as fraud, identity theft, network intrusion, account takeover or money laundering, which may result in undesired outcomes for both the institution and the individual.

There are different ways to address the challenge of anomaly detection, including supervised and unsupervised learning.

Detecting outlier data, or anomalies according to historic data patterns and trends can enrich a financial institution’s operational team by increasing their understanding and preparedness.

Anomaly detection presents a unique challenge for a variety of reasons. First and foremost, the financial services industry has seen an increase in the volume and complexity of data in recent years. In addition, a large emphasis has been placed on the quality of data, turning it into a way to measure the health of an institution.

To make matters more complicated, anomaly detection requires the prediction of something that has not been seen before or prepared for. The increase in data and the fact that it is constantly changing exacerbates the challenge further.

There are different ways to address the challenge of anomaly detection, including supervised and unsupervised learning.

Powered by WPeMatico

Sila announced Monday it raised $13 million in Series A funding for its banking and payment platform that gives software teams tools to build the next generation of financial products and services.

Revolution Ventures led the round and was joined by existing investors Madrona Venture Group, Oregon Venture Fund and Mucker Capital, as well as Wise co-founder Taavet Hinrikus. The funding brings the total investment to date for Portland, Oregon-based Sila to $20 million.

The company was founded in 2018 by Shamir Karkal, Angela Angelovska, Isaac Hines and Alex Lipton to simplify digital payments and storage in a regulatory compliant way and build on blockchain technology. CEO Karkal has a long history in the fintech space, co-founding Simple, an app unifying various accounts into one accessible bank card, in 2009. It was acquired by BBVA in 2014 for $117 million and shuttered earlier this year.

Karkal told TechCrunch that the idea for Sila was born out of frustration while starting another bank. He saw a need for financial application development, but was hindered by a banking system “still stuck in the 20th century.” He thought consumers expected a different level of service, which is why many flock to fintechs.

However, whenever a business tried to connect existing banking systems, fintechs and cryptocurrency innovators, as it built and scale, would always run into technology and compliance issues, Karkal said.

“The problem with working with banks, is that you have to figure out how to integrate with their mainframe,” he added. “In the process, you end up having to also be compliance experts just to be able to do it.”

Whereas it took Karkal three years to get bank processes set up for other companies, it took Sila 18 months. Its banking APIs enable developers to create their own digital wallets, replacing the need to integrate with legacy financial institutions. Sila also has partnerships with fintech platforms, including Plaid, Alloy, Lithic and Arcus to move money, and is backed by Evolve Bank and Trust.

Sila can now get customers up-and-running in six to eight weeks. And unlike competitors that focus almost exclusively on e-commerce, most of Sila’s customers are doing regulated payments within the fintech, insurtech, commercial real estate and cryptocurrency spaces that tend to be more complex from a compliance basis, Karkal said.

Since the company launched its platform, business was building steadily, and took off in the second half of 2020. The company raised a $7.7 million seed round earlier in the year. In the last 12 months, Sila grew its revenue 10 times and customers’ end users grew over 500% in the last seven months.

Sila will use the new funding to increase headcount, target additional partners and expand product features, including its Ethereum MainNet stablecoin issuance and interoperability between FedWire and the Nacha Automated Clearing House network.

“There is a massive wave of fintechs emerging in the U.S., and we have barely scratched the surface,” Karkal said. “Places like India, Africa and Latin America could accelerate at the same time because they are mainly starting from zero. We are here to ‘arm the rebels’ and help those innovators build applications to give all end users a much better financial experience.”

As part of the investment, Clara Sieg, partner at Revolution Ventures, is joining the company’s board. She told TechCrunch she met the company’s co-founders through the Portland ecosystem.

Revolution tends to look at fintech startups from a consumer angle. Recognizing that the problem with building infrastructure meant dealing with banks, the firm set out how to find a company building the pipes to solve it, she said.

In the landscape of fintech, she considers Dwolla to be a competitor to Sila. Last week, the company raised $21 million to continue developing its API that allows companies to build and facilitate fast payments, specifically with a focus on ACH. However, it comes down to actually signing up customers, and that competitive landscape is pretty thin, Sieg added.

“Sila is building an easy way for people to program money and taking a regulatory eye to things,” Sieg said. “When Shamir was building Simple, he could see how challenging it was for incumbents to provide the tools developers need to embed financial services, and this is why we have confidence in his ability to win.”

Powered by WPeMatico

Olumide Soyombo is one of the well-known active angel investors in Nigeria tech startups and Africa at large. Since he began angel investing in 2014, Soyombo has invested in 33 startups, including Stripe-owned Paystack, PiggyVest and TeamApt.

Today, the investor is announcing the launch of Voltron Capital, a Pan-African venture capital firm he co-founded with Abe Choi, a U.S.-based entrepreneur and investor.

Voltron will be deploying capital to roughly 30 startups, mostly in pre-seed and seed stage across Africa, in a bid to “address the severe lack of access to early-stage funding for African tech companies.” The ticket sizes will range from $20,000 to $100,000, focusing on startups in Nigeria, Kenya, South Africa and North Africa.

Soyombo is one of the few founder-cum-investors on the continent, despite his company not being the traditional VC-backed startup the world has become accustomed to. In 2008, he started Bluechip Technologies with a friend, Kazeem Tewogbade as an enterprise company that provides data warehousing solutions and enterprise applications to banks, telcos and insurance firms. Some of its biggest clients include OEMs like Oracle.

Six years later, the pair decided to venture into tech, a relatively nascent industry in Nigeria at the time and began investing in startups via LeadPath, an early-stage firm they launched in Lagos, Nigeria. The idea was to invest $25,000 and take the startups through a three-month accelerator program culminating in a demo day. The plan was to run LeadPath like Y Combinator but it didn’t take off as planned.

“In 2014, three months after we found out that there was no investor to put them in front of. So you’d have to write another check yourself,” Soyombo said humorously over the phone. “We quickly saw that the accelerator model didn’t work, so we started investing individually. It’s funny how things have changed since then.”

LeadPath became a special purpose vehicle (SPV) for the pair to carry out their angel investing deals. Over the years, Soyombo has launched several SPVs for the same purpose. So, why do things differently now by creating a fund? Soyombo walks me through one of the processes he has used to fund deals over the years to answer this question.

As an influential figure in Nigeria’s tech ecosystem, Soyombo has access to almost any important deal in the market. “I get the privilege of seeing many deals before most people see them. I’ve built that network within the startup ecosystem and reputation as an angel always ready to help. So obviously, that helped me see many deals very quickly,” he said. Often, his deal flows are filled with startups seeking six-figure pre-seed to seed investments. Say, for instance, a founder is looking to raise $300,000, Soyombo can typically invest $50,000 of his own money. And based on his perception of the startup’s growth prospects, he can choose to bring his friends and acquaintances on board to fill the round.

This informal approach is what Soyombo wants to make formal via a structured format where each individual or organizational LP gets access to his deal flow simultaneously. The investor believes companies will get capital quicker this way. And the interesting bit is that his work in corporate Nigeria has allowed him to access non-traditional capital, which means some of the investors that use Soyombo’s deal flows are outside the typical Nigerian tech investing landscape.

He sees his job as someone bridging the gap of angel investing between his corporate friends and colleagues who have not typically invested in tech and startups that need their money.

“There’s a bit of FOMO now,” he said. “People, including high net worth individuals, tell me to carry them along anytime I’m investing, and then I have startups looking for capital as well. But then again, I’m not trying to get a full job by managing a full fund, which is why we’ve structured it this way.”

Anyone familiar with the happenings in African tech these past few months knows the two events that have caused this FOMO: Paystack’s exit to Stripe and Flutterwave’s unicorn status. Soyombo was an early investor in the former, marking his solitary primary exit alongside two secondaries within a portfolio that have cumulatively raised over $70 million. Thus, it’s not hard to see why Soyombo isn’t having a hard time convincing non-traditional investors, including HNIs (who are notoriously risk averse when it comes to tech investing), to write checks in startups.

“All of a sudden, everyone is interested in what’s happening in the space. The HNIs that would’ve thrown money into real estate are looking for startups. We even see older HNIs telling their children to invest on their behalf, so it’s an easier conversation to have. Most of them want to diversify their portfolio by having a piece of that pie,” he said, pointing to Paystack and Flutterwave successes.

Abe Choi (co-founder, Voltron). Image Credits: Voltron Capital

Voltron Capital will be managed on AngelList. Its investors cut across HNIs and executives from banks, telcos, among other sectors, each investing a minimum of $10,000. Voltron is similar to a typical seven-figure fund targeting pre-seed and seed-stage startups in Africa, yet it’s quite different in the way it chooses to back founders. The fund remains an embodiment of Soyombo’s investment stance, which is “founders-first regardless of the industry.”

“I’m going to continue backing interesting entrepreneurs. If Odunayo of PiggyVest was building a health tech or edtech company, I’ll still back that company,” he said, referring to the $1 million investment he made three years ago in one of Nigeria’s widely celebrated fintechs. “So I think the investability of sectors, for me, is driven by quality entrepreneurs that are going to solve problems in that area.”

In 2019, African tech startups raised a record $2 billion, according to Partech Africa. They have raised half that number already this year, and some publications predict these startups will break 2019’s record.

A large chunk of these investments goes into late-stage deals, which is typical of most tech ecosystems globally. But Africa stands out because early-stage startups find it more difficult to raise investments compared to other regions. For instance, IFC reported that 82% of African tech startups cite access to seed funding and a lack of angel investors as major problems they face. Without early-stage funding, many of the startups primed to drive this growth are missing out on vital capital to support their early operations and generate revenue, which is a key requirement for securing later rounds of funding and a larger scale.

Voltron, in its little capacity, wants to fill this gap in the best way it can. Besides listing local investors as LPs, Soyombo says startups will be able to access foreign capital too. Choi is the key to making that happen. Personally, Choi has invested in 15 startups (exiting two); therefore, his experience and network in the U.S. will be crucial in sourcing foreign capital into the continent.

Soyombo believes Stripe acquisition of Paystack has made foreign investors take notice of African startups. He humorously references Paul Graham’s tweet after the acquisition as another reason why foreign investors’ interests have also piqued. The tweet from the Y Combinator co-founder read: “Investors who ignore Nigeria now have to ask themselves: What do I know that Patrick Collision doesn’t?”

That said, the investor holds that the pace at which the African tech ecosystem is maturing should excite anyone. The quality of founders on the continent is improving and will continue in that manner because there are more problems to solve, he continued.

“Also, as our startups mature, we’ll see people leaving to set up theirs. We want the next wave of African tech success stories to not only make an impact on the continent but to be truly global; through Abe’s strategic connections to the USA, we’re confident we can provide our portfolio with the best possible opportunities to achieve this through our U.S. and global network.”

Powered by WPeMatico