Finance

Auto Added by WPeMatico

Auto Added by WPeMatico

As a startup founder, there will be three scenarios in which you’ll need to understand how to properly do a quality of earnings (QofE) if you want to maximize value.

The first scenario will be when you decide to raise a Series A and subsequent VC rounds, followed by when you do a strategic acquisition, and lastly, when you sell your company.

This post is a framework for how to think and organize your QofE and go through the most common items that you’ll want to keep top of mind for every M&A and private equity transaction you may be part of.

The goal of a QofE is to adjust the reported EBITDA to calculate a restated EBITDA that best reflects the current state of the company on an ongoing basis. It also presents a historical adjusted EBITDA that is comparable throughout the last two or three years.

QofE can have a significant impact on a company valuation for three main reasons:

With that in mind, every entrepreneur must understand how to properly form a view of what is the proper adjusted EBITDA and adjusted revenue of your company. It is common for founders in an M&A process to be unfamiliar with the notion of QofE and leave value on the table.

When performed by a professional transaction service advisory team, the quality of earnings is a result of a thorough review of all the documents generally available in a data room.

This breakdown aims to ensure that you won’t be that founder and that you’ll be armed to negotiate your company valuation on equal ground with your investors. If you are in the seller’s shoes, you will get the advantage of understanding how an experienced investor or buyer thinks. If you’re in the buyer’s shoes, you’ll benefit from understanding and valuing your acquisitions better.

When performed by a professional transaction service advisory team, the quality of earnings is a result of a thorough review of all the documents generally available in a data room. These include, but are not limited to: Legal documentation, financial statements (P&L, balance sheet, cash flow), audit reports, management presentation and contracts.

When doing a QofE analysis, it’s key to consistently ask yourself: “Can or should this information translate into an adjustment of revenue or EBITDA, net working capital (NWC) or net debt?”

Why did we include NWC and net debt? That is because they often have an indirect impact on adjusted EBITDA. Think of an adjustment to the historical level of inventory. Less inventory likely means fewer storage costs. So if you adjust historical inventory, you’ll want to also impact your adjusted EBITDA.

On top of reviewing all the aforementioned documents, your QofE analysis will heavily rely on interviewing management. No matter how long you look at the financials, if you can’t have management confirm information or explain trends, you won’t be able to draw proper conclusions and understand the numbers.

Powered by WPeMatico

Assembling a startup team is harder than assembling 10 IKEA dressers, and the stakes are much, much higher.

Starting with the assumption that 90% of startups will fail and the most successful ones take an average of six years to IPO, founders must make careful decisions about whom they invite to join the core team.

Will that stellar engineer become a great CTO? Should your product person be opinionated or a team player? Are you even the best choice for CEO?

ThoughtSpot CEO Sudheesh Nair shared some of his thoughts about building a sturdy leadership team and drafted a thorough checklist for entrepreneurs who are putting a crew together. His initial advice?

“Investors love founder-CEOs, and founders are often fantastic candidates for this role. But not everyone can do it well, and more importantly, not everyone wants to.”

In a related article, Gregg Adkin, VP and managing director at Dell Technologies Capital, shared the framework he’s developed for helping founders set up their board.

Choosing the right mix of people can impact everything from fundraising to hiring: “Investors often ask founders about their board [because] it says a lot about their character, their judgment and their willingness to be challenged,” he writes.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Miranda Halpern spoke to Amsterdam-based coach Ward van Gasteren for our latest growth marketing interview, which is free to read.

In their discussion, van Gasteren addressed misconceptions about growth hacking, the mistakes most startups are likely to make, and the distinctions he draws between growth hacking and growth marketing:

“Growth hacking is great to kickstart growth, test new opportunities and see what tactics work,” he tells us.

“Marketers should be there to continue where the growth hackers left off: Build out those strategies, maintain customer engagement, and keep tactics fresh and relevant.”

Thanks very much for reading Extra Crunch this week; I hope you have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

Image Credits: sureeporn / Getty Images

In his first column since returning to TechCrunch, reporter Ryan Lawler considered the potential ripples Square’s purchase of Afterpay may send across the pond of buy now, pay later startups.

For commentary and perspective, he interviewed:

The investors he spoke to agreed that deferring payments helps drive e-commerce, “but scale matters and long-term margins look slim for BNPL startups,” reports Ryan.

Image Credits: Ivan Bajic (opens in a new window) / Getty Images

Businesses have been deploying AI solutions for 20 years, but few have achieved the outstanding gains in efficiency and profitability promised when the technology first appeared.

But there’s a burgeoning new generation of enterprise AI, Eshwar Belani, an operating partner at Symphony AI, writes in a guest column.

“Companies on the leading edge of AI innovation have advanced to the next generation, which will define the coming decade of big data, analytics and automation — Enterprise AI 2.0.”

Image Credits: Joan Cros Garcia-Corbis (opens in a new window) / Getty Images

Over the next 18 months, one technologist says the increased adoption of embodied artificial intelligence will open a path to superintelligence — incredibly powerful software that dwarfs anything the human mind could produce.

“All the crazy Boston Dynamics videos of robots jumping, dancing, balancing and running are examples of embodied AI,” says Chris Nicholson, founder and CEO of Pathmind, which uses deep reinforcement learning to optimize industrial operations and supply chains.

“The field is moving fast and, in this revolution, you can dance.”

Image Credits: Nigel Sussman (opens in a new window)

The Exchange looks at the valuations of public insurtech companies and considers what that means for startups — but from a slightly different perspective.

“We’d typically riff on the new values of public neoinsurance companies and use that data to work our way into a guess concerning what the price declines might mean for related startups,” Alex Wilhelm writes. “Taking public-market data and using it to better understand private markets is pretty much the national pastime of this column.

“Not today.”

Image Credits: Anastassiia (opens in a new window) / Getty Images

The fact that the globe is awash in venture capital should not be news to readers of this newsletter.

For founders, it means more than just fat checks, Kunal Lunawat, the co-founder and managing partner of Agya Ventures, writes in a guest column.

“Founders would be well served to go back to the basics and focus on the principles of fundraising when determining who sits on their cap table.”

Image Credits: Nigel Sussman (opens in a new window)

Alex Wilhelm checks in on results from Starling Bank and Monzo to see what the neobanks’ most recent financial figures say about the state of neobanks overall.

“Although some neobanks are managing to clean up their ledgers and work toward profits — or reach profitability — not all are in the black,” he notes.

But among those that are?

“At least a portion of the neobanking world is financially stable enough to consider public offerings.”

Image Credits: MicroStockHub (opens in a new window)/ Getty Images

The red-hot venture capital market may give founders lots of investors to choose from, but the most important thing (if you can be choosy) is being able to trust and rely on your investors, Ripple Ventures’ Matt Cohen and True’s Tony Conrad write in a guest column.

“This … new dynamic is forcing founders to be extremely selective about exactly who is sitting around their mentorship table,” they write.

“It’s simply not possible to have numerous deep and meaningful relationships to extract maximum value at the early stage from seasoned investors.”

Image Credits: A-Digit (opens in a new window) / Getty Images

Assembling a board of directors is not merely about finding individuals who can aid your early-stage journey, Gregg Adkin, the vice president and managing director at Dell Technologies Capital, writes in a guest column.

The composition of the board can also impact your fundraising.

“Investors often ask founders about their board [because] it says a lot about their character, their judgment and their willingness to be challenged,” he writes.

Adkins offers a framework he calls “SPIFS” — for strategy, people, image, finance and systems for compliance — to aid founders in setting up a board.

Image Credits: Nigel Sussman (opens in a new window)

In the wake of Deliveroo’s plans to abandon the Spanish market after the country passed legislation requiring companies dependent on gig workers to hire employees, Alex Wilhelm wondered about the battle for smaller markets and whether third place is sufficient.

“One company exiting a market is not a big deal, but we were curious about Deliveroo’s comments regarding the need for market leadership — or something close to it — to warrant continued investment,” he writes for The Exchange.

“Is this the common reality for startups battling for market position, no matter if those markets are cities or countries?”

Powered by WPeMatico

Many VCs tout their mentorship and hands-on approach to founders, especially those who run early-stage startups. But in the recent era of lightning-fast rounds closing at sky-high valuations, the cap tables of early-stage startups are becoming increasingly crowded.

This isn’t to say that the value VCs bring has diminished. If anything, it’s quite the opposite — this new dynamic is forcing founders to be extremely selective about exactly who is sitting around their mentorship table. It’s simply not possible to have numerous deep and meaningful relationships to extract maximum value at the early stage from seasoned investors.

Founders should definitely pursue big rounds at sky-high valuations, but it’s important that they recognize how important it is to manage who they allow into their mentorship circles. Initially, founders should make sure their first layer consists of the real “doers” — usually angels and early venture investors who founders meet with weekly (or more frequently) to help solve some of the most granular problems.

Everything from hiring to operational hurdles all the way to deeper, more personal challenges like balancing family life with a rapidly growing startup.

This circle is where the real mentorship happens, where founders can be open and vulnerable. For obvious reasons, this circle has to be small, and usually consist of two to six people at most. Anything more simply becomes unwieldy and leaves founders spending more time managing these relationships than actually building their company.

How founders manage their VC circles can mean the difference in success or failure for a thousand different reasons.

The second layer should consist of the “quarterly crowd” of investors. These aren’t necessarily people who are uninterested or unwilling to participate in the nitty gritty of running the company, but this circle tends to consist of VCs who make dozens of investments per year. They, like their founders, aren’t capable of managing 50 relationships on a weekly basis, so their touch points on company issues tend to move slower or less frequently.

Powered by WPeMatico

The startup world can be a rollercoaster. While investment continues to pour in — with both founders and investors looking for the next unicorn — the reality is that 90% of startups fail, with over half of those going under in the first three years.

I’ve founded two companies that I grew and sold (Mezi and Dhingana). I encountered many of the issues that new founders face, learned on the job, and thankfully persevered. Using the knowledge that I acquired in my previous companies, I’ve founded a third — Zeni — to try and help founders make more informed, sustainable financial decisions.

For many founders, a transformative idea and initial outside investment doesn’t translate into understanding the underlying financial complexities of running a business.

Whether you’re just wrapping your seed round, or on to Series B, avoiding these common issues is the best way to ensure that you’re set on solid ground and free to focus on your vision.

Startups go under for a variety of reasons. Some fail to achieve product-market fit in a scalable way. Many others simply run out of money. While the above two reasons are often cited as the two primary reasons for startup failure, they’re also related. If you don’t solve a market problem and don’t generate customers, you’re eventually going to run out of money.

Unfortunately, many of the startups that fail shouldn’t. They’re led by bright entrepreneurs with a great idea. But for many founders, a transformative idea and initial outside investment doesn’t translate into understanding the underlying financial complexities of running a business.

When you break down the various complexities founders face in understanding business finances, there are three primary hurdles they face:

All of the above issues put increased workload and strain on founders, which can lead to burnout. Owners, on average, spend around 40% of their working hours on tasks like hiring, HR and payroll. While hiring is integral to a founders’ day-to-day role, other administrative tasks related to finance, HR and payroll distract founders from focusing on their overall vision and goals.

The good news is that by being aware of the above issues, you can solve them and eliminate the consequences of burnout, distraction and, ultimately, failure. Let’s talk about how.

The financial decision-making and tasks of most startups start and stop with the founder. This means that bookkeeping, bill paying, invoicing, financial projections, employee payments and taxes all run into a bottleneck. Even worse, each of these functions requires another employee, vendor or third-party expert — finance firms, admins, CFOs, CPA firms — each using its own software and applications to accomplish their goals.

Each of these parties is reporting back up to the founder, who is then in charge of making sense of it all and disseminating the information to the entities that need it. This means that not only is everything slower, but often things fall through the cracks, as communication can become a serious issue.

Worse still, this creates cash flow problems, as bills go unpaid, invoices go unsent, and important financial documents are delayed. I’ve seen revenue go unreported and invoices unsent and uncollectable due to the fragmentation-bottleneck system most founders experience.

Powered by WPeMatico

Two decades after businesses first started deploying AI solutions, one can argue that they’ve made little progress in achieving significant gains in efficiency and profitability relative to the hype that drove initial expectations.

On the surface, recent data supports AI skeptics. Almost 90% of data science projects never make it to production; only 20% of analytics insights through 2022 will achieve business outcomes; and even companies that have developed an enterprisewide AI strategy are seeing failure rates of up to 50%.

But the past 25 years have only been the first phase in the evolution of enterprise AI — or what we might call Enterprise AI 1.0. That’s where many businesses remain today. However, companies on the leading edge of AI innovation have advanced to the next generation, which will define the coming decade of big data, analytics and automation — Enterprise AI 2.0.

The difference between these two generations of enterprise AI is not academic. For executives across the business spectrum — from healthcare and retail to media and finance — the evolution from 1.0 to 2.0 is a chance to learn and adapt from past failures, create concrete expectations for future uses and justify the rising investment in AI that we see across industries.

Two decades from now, when business leaders look back to the 2020s, the companies who achieved Enterprise AI 2.0 first will have come to be big winners in the economy, having differentiated their services, scooped up market share and positioned themselves for ongoing innovation.

Framing the digital transformations of the future as an evolution from Enterprise AI 1.0 to 2.0 provides a conceptual model for business leaders developing strategies to compete in the age of automation and advanced analytics.

Starting in the mid-1990s, AI was a sector marked by speculative testing, experimental interest and exploration. These activities occurred almost exclusively in the domain of data scientists. As Gartner wrote in a recent report, these efforts were “alchemy … run by wizards whose talents will not scale in the organization.”

Powered by WPeMatico

Less than six months after raising $55 million in a Series C round of funding, SMB 401(k) provider Human Interest today announced it has raised $200 million in a round that propels it to unicorn status.

The Rise Fund, TPG’s global impact investing platform, led the round and was joined by SoftBank Vision Fund 2. The financing included participation from new investor Crosslink Capital and existing backers NewView Capital, Glynn Capital, U.S. Venture Partners, Wing Venture Capital, Uncork Capital, Slow Capital, Susa Ventures and others.

Over the past year, the San Francisco-based company has raised $305 million. With the latest financing, it has now raised a total of $336.7 million since its 2015 inception.

The company admittedly has an IPO in its sights, as evidenced by the appointment of former Yodlee CFO Mike Armsby to the role of CFO at Human Interest. It’s targeting a traditional IPO sometime in 2023, with execs saying the target is to have “$200 million+ in run-rate revenue before going public.” Currently, it’s at “tens of millions of run-rate revenue” now, and adding millions of new revenue each month.

Human Interest’s digital retirement benefits platform allows users “to launch a retirement plan in minutes and put it on autopilot,” according to the company. It also touts that it has eliminated all 401(k) transaction fees.

Demand for 401(k)s by SMBs appears to be at an all-time high, with Human Interest reporting that its sales tripled over the last year. The company has also more than doubled its headcount over the last 12 months to 350 employees.

The startup said it is seeing strong adoption in verticals that have not previously had retirement benefits, including construction, retail, manufacturing, restaurants, nonprofits and hospitality. For example, over the past three quarters, Human Interest has seen 4.5x customer growth in the restaurant sector. Since the start of the pandemic, Human Interest has experienced 2x higher enrollment growth among hourly workers than salaried workers, and hourly worker assets have tripled.

“Promoting financial health is a core investment pillar for The Rise Fund. Human Interest delivers one of the most compelling solutions to the persistent problem that roughly half of Americans will not have enough savings when they reach retirement age,” said Maya Chorengel, co-managing partner at The Rise Fund, in a written statement. “Despite recent legislation, primarily at the state level, legacy programs have not, to date, produced the same participant outcomes as Human Interest.”

The company said it will be using its new capital to expand its network of integrations and partnerships with financial advisers, benefits brokers and payroll companies. It also expects to, naturally, do some hiring –– another 200 employees by year’s end, primarily in its product, engineering and revenue teams.

The 401(k) for SMB space is heating up as of late. In June, competitor Guideline also raised $200 million in a round led by General Atlantic.

Additional details around the IPO and revenue were added post-publication.

Powered by WPeMatico

The global venture capital bet on neobanks is massive. London-based Starling Bank has raised more than $900 million, per Crunchbase. The same data source indicates that Chime has raised $1.5 billion. Monzo has raised nearly $650 million. And the list goes on: E-commerce-focused neobank Juni raised $21.5 million last month. Novo, an SMB-focused neobank, raised $41 million in June. Nubank has raised $2.3 billion. And FairMoney has locked down more than $50 million.

On and on and on.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

But despite our general inclination to lump banking-focused fintech providers that serve consumers, business customers or both into a single bucket, there’s wide divergence in how the various neobank players are performing in the market.

Back in August 2020, The Exchange noted that many neobanks were racking up steep losses. Our read at the time was that the capital being poured into the fintech category was being invested aggressively in the name of growth. Based on recent results, that view is holding up.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

And Starling Bank reached what it describes as profitable territory in October 2020. Things have changed since our first look into neobank results.

The trend of positive neobank news continued this June, when Revolut reported its recent financial performance. The company did post rather negative aggregate results for the 2020 period. But when we drilled down into its quarterly results, we saw the picture of a fintech company scaling its gross margins and revenues while nearly reaching adjusted net income neutrality by Q4 2020. We were impressed.

This morning, let’s add to our running dig into neobank results by parsing recently released data from Starling Bank and Monzo. As we’ll see, although some neobanks are managing to clean up their ledgers and work toward profits — or reach profitability — not all are in the black.

Powered by WPeMatico

Reserve Trust, a Denver-based financial services provider, has raised $30.5 million in a Series A round led by QED Investors.

FinTech Collective, Ardent Venture Partners, Flywire CEO Mike Massaro and Quovo founder and CEO Lowell Putnam also participated in the financing, which included $17.9 million in secondary shares. It brings the startup’s total raised since its 2016 inception to $35.5 million.

Reserve Trust describes itself as “the first fintech trust company with a Federal Reserve master account.” What does that mean exactly? Basically, a federal reserve master account allows Reserve Trust to move dollars on behalf of its customers directly, via wire and ACH payment rails, without an intermediate or partner bank.

Historically, only banks were able to access these payment rails directly, which left both domestic and international fintechs “with limited partner options, poor technology and slow implementations when it came to embedding high-value B2B payments,” says COO Dave Cahill. Reserve Trust touts that its technology and services give companies all over the world the ability to “seamlessly move money via the first cloud-based payment system connected directly to the Federal Reserve” since it is not limited by legacy banking systems.

Image Credits: CEO Dave Wright and COO Dave Cahill / Reserve Trust

In conjunction with the fundraise, Reserve Trust is also announcing that Dave Wright has been named CEO and Cahill joined as COO. The pair worked together previously at SolidFire, a flash storage startup that Wright founded and sold to NetApp for $870 million in 2016.

Reserve Trust works with businesses that seek to embed domestic and cross-border B2B payment by offering them the ability to store funds in custody accounts that are backed by its Federal Reserve master account.

The history of the company relates back to the global financial crisis. After the crisis, banks in the U.S. went through a process called derisking, which meant they shed businesses that on a risk return basis weren’t as strong as other businesses. One of those included the handling of U.S. dollar payments, particularly in emerging countries.

“One of the consequences of this is that it became significantly more difficult and expensive for businesses and smaller economies to trade and move U.S. dollars around the world,” Wright told TechCrunch. “And the founders of Reserve Trust saw this opportunity to build a new type of financial institution that was focused on helping to provide U.S. dollar payment services, especially to emerging fintechs in markets around the world, and helping to reconnect those economies to global trade.”

But rather than start a bank, the founders (Dennis Gingold, Justin Guilder) navigated a previously unexplored part of regulatory waters to create a state-chartered trust company with a Federal Reserve master account.

“That’s something that had never really been done before,” Wright added. “Pretty much every other trust company has to work through banks for all their payment services. Reserve Trust is the first that has actually managed to get a Federal Reserve master account and can process payments directly with the Federal Reserve.”

The complex process took about three years, and in 2018, the company got a Federal Reserve master account and started providing U.S. dollar custody and payment services for fintechs all over the world. Reserve Trust began to see strong demand from payment and fintech companies that were struggling to develop strong partner bank relationships, even though fundamentally there wasn’t any reason the banks couldn’t work with them.

“They found working with banks to be a slow process, one that didn’t involve a lot of technology expertise on the side of the banks, and it was really inhibiting their ability to develop their technology,” Wright said. And that was even here in the U.S. Today, more than half of its business is from domestic fintechs, although Reserve Trust still has a strong international presence as well.

The new funds will mainly go toward helping the company scale to handle what Wright describes as “a fairly overwhelming amount of demand” and toward building out the team, the technology and the services it needs to address the payment needs of larger, faster growing fintechs around the world.

“Most of our customers today are small and midsize fintechs, but now we’re seeing demand for much larger fintechs that have much higher payment volumes and are involved in embedded banking and B2B payments,” Wright said. “They are looking for a stronger banking partner than what they’ve been able to find among the role of traditional banks.” Customers include Unlimint and VertoFX, among others.

QED Investors partner Amias Gerety and FinTech Collective principal Matt Levinson are bullish both on Reserve Trust’s history and its potential.

The pair point to payments giant Stripe as an example of how far Reserve Trust can go.

“Stripe has significant market share doing merchant acquiring and processing e-commerce payments for the consumer,” Levinson said. “B2B payments is significantly bigger in terms of volume, so we’re talking about well over $20 trillion of addressable payment flow. But there’s no real technology company that’s brought the modern payments platform to market without being beholden to legacy banks. And that’s why we’re so excited about this business.”

Reserve Trust, he added, is giving businesses a way to facilitate B2B payments that “are smarter, faster and cheaper.”

Gerety agrees.

“Despite all the excitement around digital payments and infrastructure, there is still no fintech that can offer direct integration with the U.S. payment system,” he said. “With Reserve Trust, we are creating foundational infrastructure to hold and move payments globally and at scale.”

Powered by WPeMatico

Zeni, a Palo Alto fintech company providing real-time financial services data to venture-backed startups, raised $34 million in Series B funding led by Elevation Capital.

The new investment comes just five months after Zeni announced $13.5 million in a combined seed and Series A round. The company has now raised $47.5 million in total since it was co-founded in 2019 by twin brothers Swapnil Shinde and Snehal Shinde.

Elevation was joined in the new round by new investors Think Investments and Neeraj Arora, as well as existing investors Saama Capital, Amit Singhal, Sierra Ventures, Twin Ventures, Dragon Capital and Liquid 2 Ventures. As part of the investment, Ravi Adusumalli, founder and managing partner at Elevation Capital, will join Zeni’s board.

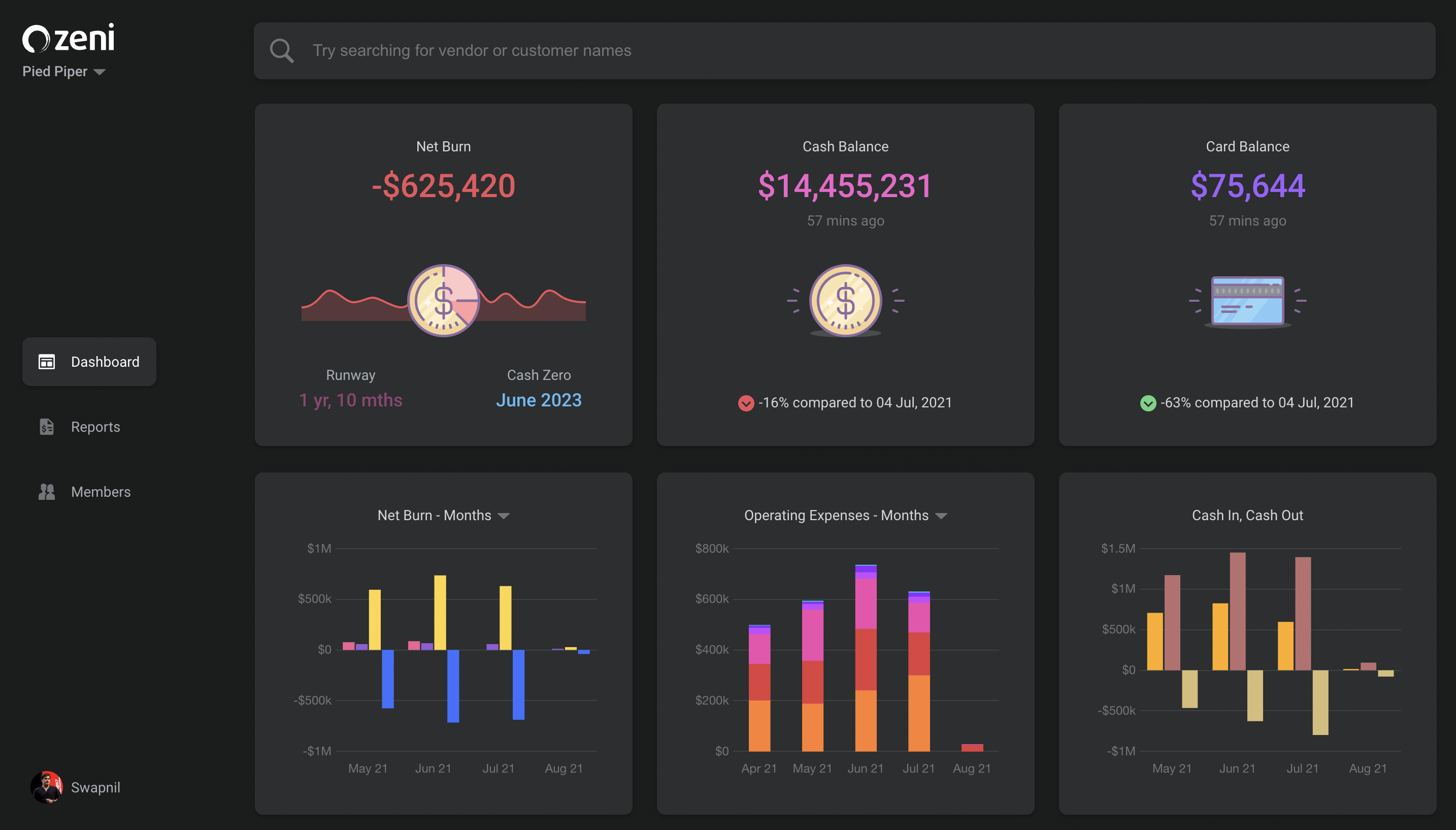

The Shinde siblings started the company after selling their last company, Mezi, a travel concierge, to American Express in 2018. Zeni’s AI-powered finance concierge platform offers bookkeeping, accounting, tax and CFO services, managing these for a flat monthly fee starting at $299 per month. Founders have real-time access to financial insights via the Zeni Dashboard, including cash in and out, operating expenses, yearly taxes and financial projections. They can also download the financial data in the “slice” that they want.

At the time of its seed/Series A round, the company was managing more than $200 million in funds each month, and that has ballooned to more than $500 million, CEO Swapnil Shinde told TechCrunch. Its customers range from pre-revenue startups to businesses generating more than $100 million in annual revenue.

In addition to the cash in and cash out analysis, the company also created a search function for transactions and spend and income trends on every customer and vendor, Snehal Shinde, chief product officer, said.

Zeni’s dashboard

Zeni experienced 550% revenue growth year-over-year, while the company’s customer base grew 375%, driven by referrals and organic growth, Swapnil Shinde said.

Despite the growth, the Series B came as a surprise to the siblings. The company was already “very well capitalized,” with a majority of the previous round still around, Swapnil Shinde said.

However, Zeni began receiving so many inbound inquiries that he said it was too exciting to pass on. Especially with the addition of Elevation Capital as an investor. Shinde said that was appealing because the firm was an investor in Paytm, and “knows how to partner and build unicorns.”

The new funding will be used to continue scaling and building the bookkeeping and accounting functions and to accelerate hiring, particularly in the engineering, sales and finance team verticals. Shinde expects to double or triple the finance team in the next year.

“As our customers scale through to their Series B, the more you can use our solution in real time to see what is happening with your finances, especially with startups and businesses having more of a remote workforce,” Swapnil Shinde added. “Zeni fits with that.”

Ash Lilani, managing partner at Saama Capital, one of Zeni’s earliest and largest investors, said he knew how big the total addressable market was — $200 billion — and how much these kinds of financial services were a giant pain point for startup companies.

“To know where you stand financially in real time is hard to do, usually, you get that information at month-end,” Lilani said. “I believe we have the opportunity to build a large company. Though Zeni is going after startups today, the small and medium markets can be leveraged. As they grow, Zeni will become their controller on the back end, while companies can just hire a CFO for the strategic decisions.”

Powered by WPeMatico

On Sunday Square announced it was gobbling up Afterpay in a deal worth $29 billion at the time of announcement. Alex followed up yesterday with more details on why the deal made sense for Square and Afterpay over here, but we wanted to ask some notable VCs what it means for the startup market.

For context, the Square deal follows a ton of money and interest flowing into the BNPL market. Just this year, VCs have invested in companies like Alma ($59.4 million, January 2021), Scalapay ($48 million, January 2021), Wisetack ($19 million, February 2021), Zilch ($80 million, April 2021) and Dividio ($30 million, June 2021).

Most of the investors we reached out to were generally bullish on the Square and Afterpay integration, but they were less excited about opportunities for other consumer BNPL businesses to emerge.

Then there’s Klarna, which raised $639 million at a post-money valuation of $45.6 billion in June, after raising $1 billion in March at a post-money valuation of $31 billion.

There’s also interest from some major public companies. After a slow start, PayPal is aggressively pushing BNPL services with merchants that offer it as a payment option. And there are reports that Apple is building its own BNPL offering through Apple Pay.

We reached out to Commerce Ventures founder and GP Dan Rosen, Better Tomorrow Ventures founding partner Jake Gibson, Fika Ventures partner TX Zhuo, and Matthew Harris of Bain Capital Ventures to see what they thought of the deal, as well as what it might mean for the opportunity for other BNPL companies and startups.

The main takeaways? “Buy now, pay later” may be effective at driving retail conversion, but scale matters and long-term margins look slim for BNPL startups.

Now, let’s hear from the venture community.

Why is the BNPL market so hot?

Powered by WPeMatico